Originally published at Dallas Morning News.

More conservatives are likely to be elected to the statehouse in November. This is a historic opportunity in 2025 to enact a new budget that provides property tax relief, empowers all families with universal school choice and puts state spending in Texas on a more sustainable trajectory in 2025. Texas, in a nation grappling with unsustainable government spending, stands out for its relative fiscal restraint and economic dynamism. However, despite historically prudent budgetary policies, Texas lawmakers enacted the largest two-year budget increase last year and the second-largest property tax relief measure (though many claimed it was the largest). According to the Sustainable Budget Project by Americans for Tax Reform, Texas, unlike the federal government and the vast majority of states, has done better at aligning its budget growth with the average taxpayer’s ability to pay for government spending, as measured by the rate of population growth plus inflation. Over the past decade, federal spending has escalated by an astonishing 81.7%, nearly quadrupling the 23.2% rate of population growth plus inflation, according to Americans for Tax Reform data. In stark contrast, Texas has exhibited fiscal restraint, ensuring its spending did not spiral out of control. The implications of such fiscal prudence are profound. If the federal government had followed the sustainable budget approach from 2014 to 2023, it could have saved taxpayers an estimated $2.1 trillion in 2023 alone. Texas’ measured approach during this period allowed the state to spend and tax $22.0 billion less than it might have otherwise, benefiting taxpayers and the broader economy. The recent and uncharacteristic budgetary excesses in Texas diminish the capacity for property tax relief. Further property tax reform is crucial. Property taxes are unfair, burdensome, and they keep people renting from the government by paying property taxes forever. The competitive landscape is also evolving, with states like North Carolina and Florida thriving by implementing aggressive tax cuts and regulatory reforms. Texas must respond by intensifying its commitment to pro-growth policies and fiscal conservatism if the Lone Star State is to maintain economic leadership. A constitutional spending limit, similar to Colorado’s Taxpayer Bill of Rights, would help put state spending in Texas on a sustainable trajectory. Even in a blue state where progressives are in charge, this measure has effectively kept state and local spending in check. Its adoption in Texas would ensure that state and local budgets grow in line with the average taxpayer’s ability to pay. To truly distinguish itself, Texas should consider a strategic overhaul of its tax system, particularly in property taxes. With no personal income tax, Texas could relieve property holders of a significant financial burden by eliminating school district maintenance and operations property taxes. This shift, funded through better-controlled state and local government spending, could transform the economic landscape for homeowners and businesses. The state could achieve this monumental feat by using the resulting surpluses from spending restraint to reduce school district M&O property tax rates, aiming to phase them out over the next decade. The Texas Legislature already controls the school finance formulas so this property tax is mostly “local” in name only, and legislators have been phasing it down in recent years. It’s possible to reduce and even eliminate truly local property taxes by cities, counties, and special purpose districts through spending restraint that would produce surpluses, which can then be used to drive property tax rates down to zero over time. Some localities would take longer than others to accomplish this, but as people vote with their feet to places without property taxes, other local governments would look for ways to eliminate theirs. The result would be less government spending and little to no property taxes in Texas. This shift in a pro-growth direction would enhance homeowners’ financial freedom and support more economic growth through increased personal savings and business investment. Texas’ economic policies have historically positioned the state as a leader in job creation and financial freedom, helping to achieve record economic growth, job growth and in-migration. However, the path forward requires conserving and enhancing these policies. Texas must adapt to the changing economic landscapes by fostering a more favorable business climate, reducing governmental interference, and revamping its tax system to maintain and strengthen its competitive status. By prioritizing spending restraint, strategic tax relief and universal school choice, Texas can secure a prosperous economic future and set a standard for budgetary sustainability. Grover Norquist is president of Americans for Tax Reform, a taxpayer organization founded in 1985 at the request of President Ronald Reagan. Vance Ginn is a senior fellow at ATR, president of Ginn Economic Consulting, and previously served in the White House’s Office of Management and Budget.

0 Comments

Originally published at National Review Online.

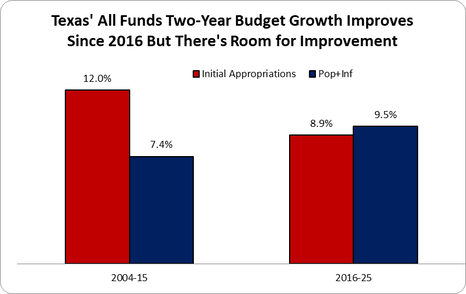

States must restrain spending growth while cutting and flattening income-tax rates. Economist Milton Friedman famously said, “I am in favor of cutting taxes under any circumstances and for any excuse, for any reason, whenever it’s possible. The reason I am is because I believe the big problem is not taxes, the big problem is spending.” This sentiment encapsulates the driving force behind the tax-cut revolution transforming the American economic landscape. This movement toward lower, flatter, and, in some cases, no income taxes is reshaping state fiscal policies to relieve taxpayers from funding excessive government. For instance, Georgia’s reduction of the state income-tax rate from 5.49 percent to 5.39 percent and Idaho’s shift to a flat income-tax rate of 5.8 percent enhance competitiveness and support more economic activity. Iowa’s adoption of a flat income tax rate of 3.8 percent, one of the lowest in the nation, further exemplifies this trend. Arkansas reduced individual and corporate tax rates, providing tax relief for the third time in 15 months. Hawaii’s substantial increase in standard deductions and adjustment of tax brackets aims to provide relief to low- and middle-income families. Kansas included property-tax relief alongside consolidating its income tax from three to two brackets. The tax-cut revolution represents a shift towards more efficient and equitable tax systems. By adopting flatter, lower tax rates, states can enhance their economic competitiveness and improve the quality of life for their residents. However, these tax cuts must be accompanied by sustainable budgeting practices that limit government spending. In 2023, Americans for Tax Reform (ATR) launched The Sustainable Budget Project, which monitors state government spending and tracks which states have or have not enacted sustainable budgets. The project defines a sustainable budget as one that limits the pace of state government spending to lower than the rate of population growth plus inflation. This approach ensures that government growth is kept in check, preventing excessive taxation and debt accumulation. Examining spending trends from 2014 to 2023 reveals the crux of the problem. Aggregate 50-state spending, excluding funding from taxpayers through the federal government, increased by 59.1 percent during this period. If states had restrained their spending to the rate of population growth plus inflation, they would have spent $1.44 trillion in 2023, $430 billion less than the $1.87 trillion spent. Over the entire decade, this would have saved $1.4 trillion, leaving more money in taxpayers’ pockets. Some states have demonstrated the benefits of sustainable budgeting. ATR found that six states held total spending growth below population growth plus inflation: Alaska, Colorado, North Dakota, Oklahoma, Texas, and Wyoming. Additionally, six other states held growth in state funds, which excludes federal funds, below the rate of population growth plus inflation: Louisiana, Massachusetts, Montana, North Carolina, Ohio, and Rhode Island. Sustainable budgeting is the key to ensuring long-term prosperity. By focusing on responsible budgeting and reducing obstacles to economic growth, such as high spending, taxes, and regulations, states can create an environment where everyone can prosper.  Government Spending Is The Problem The late, great economist Milton Friedman said, "The real problem is government spending." This is true as spending comes before taxes or regulations. In fact, if people didn't form a government or politicians didn’t create new programs, then there would be no need for government spending and no need for taxes. And if there was no government spending nor taxes to fund spending then there would be no one to create or enforce regulations. While this might sound like a utopian paradise, which I agree, there are essential limited roles for governments outlined in constitutions and laws. Of course, most governments are doing much more than providing limited roles that preserve life, liberty, and property. This is why I have long been working diligently for more than a decade to get a strong fiscal rule of a spending limit enacted by federal, state, and local governments promptly under my calling to "let people prosper," as effectively limiting government supports more liberty and therefore more opportunities to flourish. Fortunately, there have been multiple state think tanks that have championed this sound budgeting approach through what they've called either the Responsible, Conservative, or Sustainable State Budget. I recently worked with Americans for Tax Reform to publish the Sustainable Budget Project, which provides spending comparisons and other valuable information for every state. This groundbreaking approach was outlined recently in my co-authored op-ed with Grover Norquest of ATR in the Wall Street Journal. When Did This Budget Approach Begin? I started this approach in 2013 with my former colleagues at the Texas Public Policy Foundation with work on the Conservative Texas Budget. The approach is a fiscal rule based on an appropriations limit that covers as much of the budget as possible, ideally the entire budget, with a maximum amount based on the rate of population growth plus inflation and a supermajority (two-thirds) vote to exceed it. A version of this approach was started in Colorado in 1992 with their taxpayer's bill of rights (TABOR), which was championed by key folks like Dr. Barry Poulson and others. (picture below is from a road sign in Texas)  Why Population Growth Plus Inflation? While there are many measures to use for a spending growth limit, the rate of population growth plus inflation provides the best reasonable measure of the average taxpayer's ability to pay for government spending without excessively crowding out their productive activities. It is important to look at this from the taxpayer’s perspective rather than the appropriator’s view given taxpayers fund every dollar that appropriators redistribute from the private sector. Population growth plus inflation is also a stable metric reducing uncertainty for taxpayers (and appropriators) and essentially freezes inflation-adjusted per capita government spending over time. The research in this space is clear that the best fiscal rule is a spending limit using the rate of population growth plus inflation, not gross state product, personal income, or other growth rates. In fact, population growth plus inflation typically grows slower than these other rates so that more money stays in the productive private sector where it belongs. To get technical for a moment, personal income growth and gross state product growth are essentially population growth plus inflation plus productivity growth. There's no reasonable consideration that government is more productive over time, so that term would be zero leaving population growth plus inflation. And if you consider the productivity growth in the private sector, then more money should be in that sector at the margin for the greatest rate of return, leaving just population growth plus inflation. Population growth plus inflation becomes the best measure to use no matter how you look at it. Given the high inflation rate more recently, it is wise to use the average growth rate of population growth plus inflation over a number of years to smooth out the increased volatility (ATR's Sustainable Budget Project uses the average rate over the three years prior to a session year). And this rate of population growth plus inflation should be a ceiling and not a target as governments should be appropriating less than this limit. Ideally, governments should freeze or cut government spending at all levels of government to provide more room for tax relief, less regulation, and more money in taxpayers' pockets. Overview of Conservative Texas Budget Approach Figure 1 shows how the growth in Texas’ biennial budget was cut by one-fourth after the creation of the Conservative Texas Budget in 2014 that first influenced the 2015 Legislature when crafting the 2016-17 budget along with changes in the state’s governor (Gov. Greg Abbott), lieutenant governor (Lt. Gov. Dan Patrick), and some legislators. The 8.9% average growth rate of appropriations since then was below the 9.5% biennial average rate of population growth plus inflation since then, which this was drive substantially higher after the latest 2024-25 budget that is well above this key metric (before this biennial budget the growth rate was 5.2% compared with 9.4% in the rate of population growth plus inflation).  This approach was mostly put into state law in Texas in 2021 with Senate Bill 1336, as the state already has a spending limit in the constitution. The bill improved the limit to cover all general revenue ("consolidated general revenue") or 55% of the total budget rather than just 45% previously, base the growth limit on the rate of population growth times inflation instead of personal income growth, and raise the vote from a simple majority to three-fifths of both chambers to exceed it instead of a simple majority. There are improvements that should be made to this recent statutory spending limit change in Texas, such as adding it to the constitution and improving the growth rate to population growth plus inflation instead of population growth times inflation calculated by (1+pop)*(1+inf). But this limit is now one of the strongest in the nation as historically the gold standard for a spending limit of the Colorado's Taxpayer Bill of Rights (TABOR) has been watered down over the years by their courts and legislators, as it currently covers just 43% of the budget instead of the original 67%. My Work On The Federal Budget In The White House From June 2019 to May 2020, I took a hiatus from state policy work to serve Americans as the associate director for economic policy ("chief economist") at the White House's Office of Management and Budget. There I learned much about the federal budget, the appropriations process, and the economic assumptions which are used to provide the upcoming 10-year budget projections. In the President's FY 2021 budget, we found $4.6 trillion in fiscal savings and I was able to include the need for a fiscal rule which rarely happens (pic of President Trump's last budget).  Sustainable Budget Work With Other States and ATR When I returned to the Texas Public Policy Foundation in May 2020, as I wanted to get back to a place with some sense of freedom during the COVID-19 pandemic and to be closer to family, I started an effort to work on this sound budgeting approach with other state think tanks. This contributed to me working with many fantastic people who are trying to restrain government spending in their states and the federal levels. Here are the latest data on the federal and state budgets as part of ATR's Sustainable Budget Project. From 2014 to 2023, the following happened: Federal spending increased by 81.7%, nearly four times faster than the 23.1% increase in the rate of population growth plus inflation.

Result: American taxpayers could have been spared more than $2.5 trillion in taxes and debt just in 2023 if federal and state governments had grown no faster than the rate of population growth plus inflation during the previous decade. And this would be even more if we considered the cumulative savings over the period.  My hope is that if we can get enough state think tanks to promote this budgeting approach, get this approach put into constitutions and statutes, and use it to limit local government spending as well, there will be plenty of momentum to provide sustainable, substantial tax relief and eventually impose a fiscal rule of a spending limit on the federal budget. This is an uphill battle but I believe it is necessary to preserve liberty and provide more opportunities to let people prosper. Sustainable State Budget Revolution Across The Country Below are the states and think tanks which I'm working with and this revolution is going, which you can find an overview of this budgeting approach in Louisiana and should be applied elsewhere. I update these periodically, successful versus not successful budgeting attempts being 20-7 so far.

If you're interested in doing this in your state, please reach out to me. For more details, check out these write-ups on this issue by Grover Norquist and I at WSJ, Dan Mitchell at International Liberty, and The Economist.  Originally published at Law & Liberty.

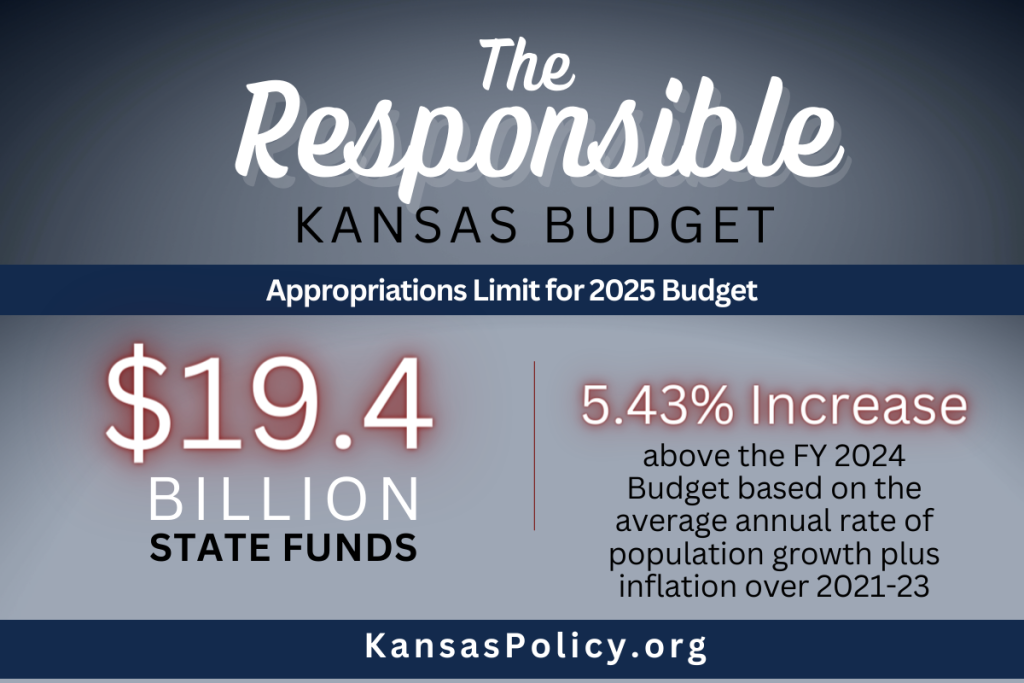

The Congressional Budget Office (CBO) just released the February 2024 Budget and Economic Outlook, and projections look grim. This year, net interest cost—the federal government’s interest payments on debt held by the public minus interest income—stands at a staggering $659 billion in 2023 and has recently soared to about $1 trillion. Unless politicians face these facts and restrain spending, Americans can expect rising inflation and painful tax hikes without improvement in public services. Some politicians quickly blamed a lack of tax revenue, calling for repealing the 2017 Trump tax cuts. But how much more money can they take? New IRS data shows that 98% of all income taxes are paid by the top 50% of income earners, those making at least $46,637. Moreover, 35% of Americans feel worse off than 12 months ago and inflation remains the primary concern for those across the income spectrum. So perhaps, rather than taking more money, the government should own up to its mistakes. The massive net interest costs result from bad spending habits, not a lack of revenue. This requires the federal government to adopt strict fiscal and monetary rules to rein in wasteful deficit spending and money printing that fuel higher interest rates and inflation. Net interest cost is the second largest taxpayer expenditure after Social Security and is higher than spending on Medicaid, federal programs for children, income security programs, or veterans’ programs. And it’s expected to grow. The CBO projects net interest to surpass Medicare spending this year and balloon to $1.6 trillion in 2034 as a result of higher debt and higher interest rates. Interest rates on Treasury debt are at the highest since 2007, paying between 4% and 5.5%, and the rates are expected to rise further. As the stockpile of gross federal debt is expected to grow by about $20 trillion to $54 trillion over the next decade, politicians will face an increasing temptation to rely on the Federal Reserve to pay for it by printing money. If the Fed does, the dollar’s value will decline, and Americans will continue to struggle financially. In an ideal world, politicians will organize the budget process to focus on funding a limited government and ensuring Americans keep their hard-earned money. They would also have plans to cut spending during times of economic downturn to reduce tax burdens on families and businesses and avoid the Keynesian fallacies of deficit spending to fill gaps in economic growth. However, America isn’t Shangri-La. As Thomas Sowell poignantly notes, a politician’s first goal is to get elected, the second goal is to get reelected, and the third goal is far behind the first two. So long as there are investors happy to purchase Treasury debt, there will be politicians who are happy to sway voters with generous spending programs financed by public debt. This must end. Instead, Washington should require strong institutional constraints with a spending limit. The limit should cover the entire budget and hold any budget growth to a maximum rate of population growth plus inflation. This growth limit represents the average taxpayer’s ability to pay for spending. Following this limit from 2004 to 2023 would have resulted in a $700 billion debt increase instead of the actual increase of $20 trillion. Such a policy has been in effect in Colorado since 1992. It is the Taxpayer’s Bill of Rights (TABOR) amendment to the Colorado Constitution. TABOR has revenue and expenditure limitations that apply to state and local governments. The revenue limitation applies to all tax revenue, prevents new taxes and fees, and must be overridden by popular vote. Expenditures are limited to revenue from the previous year plus the rate of population growth plus inflation. Any revenue above this limitation must be refunded with interest to Colorado citizens. A spending cap like TABOR is necessary but not sufficient to solve the problem because politicians in Washington can still pressure the Federal Reserve to pay for the increased debt by printing money. Therefore, it must be combined with a monetary rule to force fiscal sustainability while requiring sound money with fewer distortions in the economy. Monetary rules can come in many forms. While no rule is perfect, research shows that a rule-based monetary policy can result in greater stability and predictability in money growth than the current policy of “Constrained Discretion” whereby the Fed follows rules during “normal times” and has discretion during “extraordinary times.” Whether we are in ordinary or extraordinary times is up to policymakers, who typically don’t want to “let a good crisis go to waste,” as they say. Milton Friedman advocated for a money growth rate rule, the “k-percent rule.” This rule states that the central bank should print money at a constant rate (k-percent) every year. A variation of this rule was used by Fed Chair Paul Volcker in the late 1970s and early 1980s to tackle the Great Inflation with much success. Unfortunately, the Fed had already done too much damage with excessive money growth before then, so the cuts to the Fed’s balance sheet contributed to soaring interest rates that forced destructive corrections in the economy, resulting in a double-dip recession in the early 1980s. This led to the Fed abandoning money growth targeting in October 1982. It is important to note, though, that this “monetarist experiment” was not bound to any law, constitutional or statutory. During that time, the Fed still operated under discretion, which is why it was able to abandon the monetary growth rule just a few years after it had begun, unfortunately. There are other rules that could be applied. John Taylor proposed what’s been coined the Taylor Rule, which estimates what the federal funds rate target, which is the lending rate between banks, should be based on the natural rate of interest, economic output from its potential, and inflation from target inflation. Scott Sumner most recently popularized nominal GDP targeting, which uses the equation of exchange to allow the money supply times the velocity of money to equal nominal GDP. It has different variations, but the key is that velocity changes over time, so the money supply should change based on money demand to achieve a nominal GDP level or growth rate over time. By focusing on a rules-based approach to spending and monetary policy, Americans do not have to worry about electing the perfect candidate every election. Proper constraints will nudge even the worst politicians to make fiscally responsible choices and reduce net interest costs. Furthermore, America will be better positioned to respond to crises at home and abroad. If Congress wants to see who is to blame for the grim CBO projections, they should look in the mirror. Stop looking to take hard-earned money away from Americans and focus on sound budget and monetary reforms now.  Originally published at Kansas Policy Institute. Kansas, like most states, has a spending problem, not a revenue problem. The 2025 Responsible Kansas Budget offers several ways that the state can limit its spending to pave the way for tax reform and economic growth in the future. In June 2023, Kansas ended FY 2023 with collected tax revenues at $10.2 billion – a 4.1% or $402 million increase over the collected tax revenues of FY 2022. According to the Kansas Legislative Research Department, even if Kansas had enacted a flat tax bill during its 2023 legislative session, the state would end FY 2028 with $2.7 billion in its ending balance and $1.8 billion in the Budget Stabilization Fund, totaling $4.5 billion in reserves. At the same time, spending has grown massively over the last decade. According to the FY 2025 Governor’s Budget Report, the approved FY 2024 General Fund budget of $9.918 billion is 13.6% more than the approved 2023 budget. In FY 2020, the State Fund appropriations equaled $12.6 billion, but has ballooned into and after the COVID-19 pandemic to be $19 billion in FY 2023 and a base of $18.4 billion for FY 2024. If Kansas’s annual appropriations had grown at the rate of population growth plus inflation since FY 2005, State Fund appropriations would be $6.4 billion lower in FY 2024 than the actual base appropriations. This equates to a $46.6 billion cumulative difference from FY 2005 to FY 2024. What this number represents is higher taxes on Kansans, slower economic growth, and fewer opportunities for people to flourish.  Originally published at Pelican Institute.

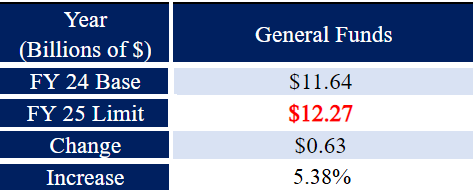

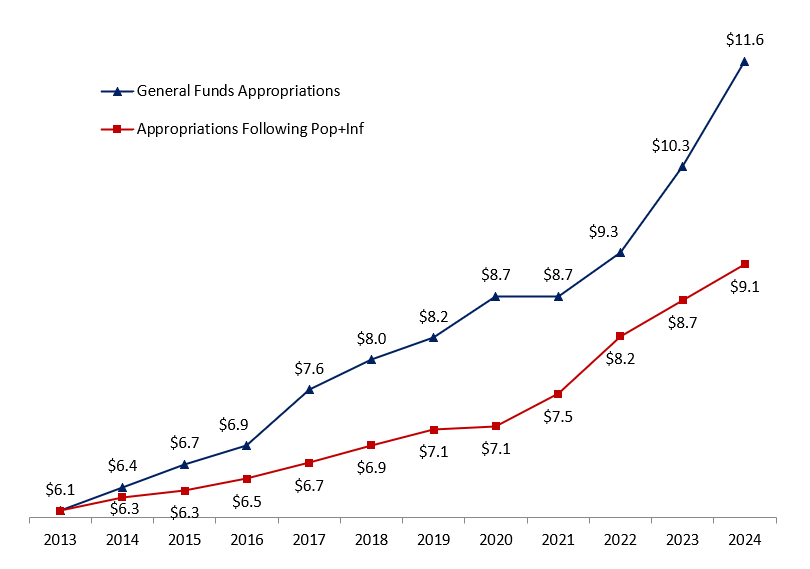

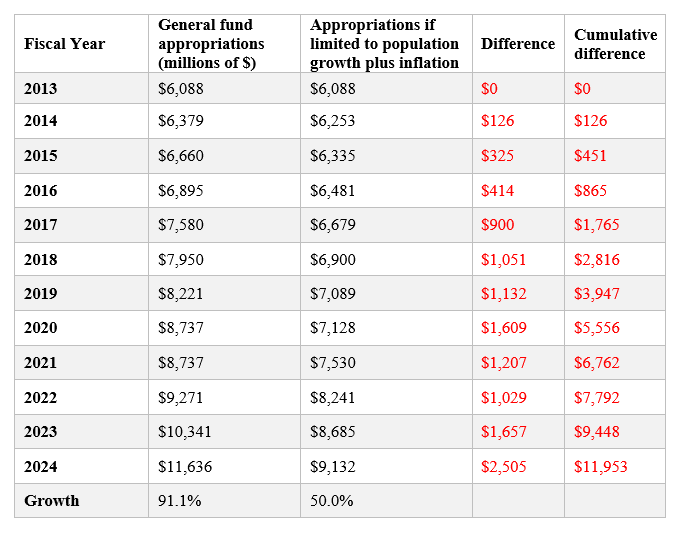

Spending, not taxes, is the ultimate burden of government. If you don’t spend money on a program, you don’t need to collect taxes to fund it. And if you don’t spend money on programs, the government can’t regulate things. Remember that government spending is paid for by the people, as the government creates nothing to earn income, so considering what people can afford is crucial. This is why it’s essential for governments at every level to narrow their scope to the essential functions enshrined in constitutions. Otherwise, spending grows too much and results in taxes being too burdensome on people. Governments across the country and the globe are spending too much. And it appears that a sustainable budget revolution is happening! I’ve been working for over a decade to help state, federal, and local governments create and adopt sustainable budgets that fund limited government. This is critical to keeping taxes and regulations lower than otherwise, so families and entrepreneurs have more of their hard-earned money in their pockets. This standard is called a fiscal rule or a tax and expenditure limit (TEL), which goes like this: a government’s budget growth cannot exceed the rate of population growth plus inflation. How does this simple rule work? This approach started in 2013 when I helped develop the Conservative Texas Budget. After years of excessive spending in Texas, we defined the narrative of a tangible cap on appropriations based on the rate of population growth plus inflation. There was no change in the state’s law right away, but this approach worked well for several sessions by helping keep spending within this rate, which represents the average taxpayer’s ability to pay for spending. Importantly, this is a maximum growth limit, as most states need to spend much less than this limit as they are already spending too much, which will help leave more money in people’s pockets. Over the years, this rule has been used to help state and local governments make their budgets more sustainable. One such victory came in 2021 when Texas put Senate Bill 1336 into law. The bill changed the state’s budget limit to not exceed the rate of population growth and inflation when it had been based on personal income growth. This was an extraordinary reform that took nearly a decade to accomplish. It’s not perfect, as it should be in the state’s constitution and should cover all state funds and use population growth plus inflation. But it’s one of, if not the, best in the country. The other spending limit that has long been the gold standard is the Taxpayer’s Bill of Rights (TABOR) in Colorado, which I recently outlined how it needed to be improved as it has been weakened over time. By working with think tanks, grassroots organizations, and lawmakers across the country, I’ve helped create and pass sustainable budgets for the following states: Alaska, Florida, Iowa, Michigan, Mississippi, Montana, South Carolina, and Tennessee. I’ve also worked with other states where a sustainable budget was proposed, such as Kansas and Louisiana, but hasn’t yet passed. Partnering with Americans for Tax Reform, I’ve contributed to creating the Sustainable Budget Project, which monitors state government spending and evaluates the adoption of sustainable budgets across all states. This Project has a slightly different methodology and purpose than the one outlined above, as the focus is on spending at the end of a budget period instead of the one I’ve been using for appropriations at the start of the appropriations process. Together, these approaches can help states define the narrative about the need for spending restraint on the budget process’s front and back end. Given the excessive spending by governments and the incentive to continue doing so, there should be as many safeguards as possible. As Louisiana enters a new year with a new session and new governor this year, lawmakers have an extraordinary opportunity to prioritize sustainable budgeting by adopting what we’re calling a Responsible Louisiana Budget. The Pelican Institute released the first iteration of the RLB last year and the second one this year. This isn’t just about fiscal responsibility; it’s an effort that will help the people of Louisiana prosper. It will do so by helping Louisianans not be overburdened by unnecessary taxes for more money in their pockets. It’s Geaux Time in Louisiana, and that includes sustainable budgeting! Originally published at Pelican Institute. The report to achieve Louisiana’s 2024-2025 Responsible Budget presents solutions to rein in the extraordinary growth of the budget in order to give the state a competitive advantage, much like those used in other states, such as Texas and Florida, limiting the amount of funding appropriated at the beginning of each fiscal year. Over the past decade, state spending has increased an average of 5.9% per year. Using the recommended Responsible Budget growth limit outlined in this report, state spending would have increased by only 2.1% per year, which would allow the excess state revenue to be saved for tax relief for Louisiana families. Originally posted at South Carolina Policy Council. Thanks to a robust state economy, plentiful business opportunities, and a relatively low cost of living, South Carolina remains one of the fastest-growing states in the nation. To maintain this strong position and promote further growth, it is crucial for S.C. legislators to limit state spending and reduce the government’s burden on taxpayers. The S.C. Policy Council created the South Carolina Sustainable Budget (SCSB) to assist in this effort. The SCSB is a maximum limit on annual recurring general funds[1] appropriations based on the rate of state population growth plus inflation. First published in 2022 and again in early 2023, it has served as a data-driven resource to help rein in unsustainable spending and provide more opportunities for tax relief. Unfortunately, the state did not adhere to the SCSB limit of $11.20 billion for its fiscal year (FY) 2024 budget; instead, it appropriated $11.64 billion – a 12.56% increase above the FY23 base of $10.34 billion. To turn the tide of excessive budget growth and provide more room for tax relief, the Policy Council is issuing its third SCSB. Table 1 provides the results outlined in this report for the FY25 SCSB. Table 1. The FY25 South Carolina Sustainable Budget for Appropriations of Recurring General Funds  Based on population and inflation data in 2023, the recommended recurring general funds appropriations limit[2] for South Carolina’s FY25 budget is $12.27 billion. With inflation moderating somewhat since reaching a 40-year high in 2022, primarily because of the errant policies in D.C., the SCSB ceiling is higher than it would be under normal economic circumstances. For example, the average annual rate of population growth plus inflation since 2013 has been 3.78%. Accordingly, the S.C. Legislature should consider freezing spending at the current FY24 budget of $11.64 billion. This would help correct recent overspending in the state’s budget and help put the state on a more sustainable budget path. It would also leave more money available for needed tax relief. At a minimum, recurring general fund appropriations in the FY25 budget must remain below $12.27 billion. Overview A sustainable budget – sometimes called a conservative or responsible budget – is a model for state budgeting that sets a maximum limit on appropriations or spending based on the rate of population growth plus inflation. This metric serves as an indicator of what the average taxpayer can afford to pay for government provisions. It accounts for 1) More people in the state who could potentially pay taxes; 2) Wage growth that’s typically tied to inflation over time to pay taxes; and 3) Economies of scale, as not every new person or wage increase should be associated with new government spending. The SCSB does not make specific recommendations on how general funds should be appropriated in the budget. Instead, it gives legislators the flexibility to appropriate taxpayer dollars to government programs as determined by the General Assembly, while ensuring that spending growth remains in line with what people can afford. Such a voluntary spending limit is key to putting South Carolina in a position for further tax relief. In 2022, Gov. Henry McMaster and lawmakers enacted the first-ever state personal income tax cut, which immediately reduced the top rate from 7% to 6.5% and collapsed the lower bracket to 3%. It also scheduled additional yearly 0.1% cuts to the top rate until it reaches 6%, though general fund revenues must project at least 5% annual growth for the cuts to trigger. The problem with this approach is that it relies on continued revenue growth to deliver incremental tax relief. Following the SCSB would help to accelerate this process, freeing up revenue to buy down the top rate to 6% immediately and fueling other tax cuts. On the other hand, unsustainable spending could build pressure to reverse course and raise taxes, leaving South Carolinians with fewer opportunities to flourish. SC Appropriations vs. Sustainable Budget Figure 1 compares the previous twelve years[3] of South Carolina’s recurring general fund budget appropriations (FY13 to FY24) to those appropriations when limited each year to the rate of population growth plus inflation. Figure 1. South Carolina General Fund Appropriations v. SCSB 12-year GF appropriations: $98.5 billion (+91.1%) 12-year GF appropriations limited to population growth + inflation: $86.5 billion (+50.0%)  Notes. Budget amounts are based on data from South Carolina’s state budget publications, Fed FRED for state population growth and U.S. chained-CPI inflation, and authors’ calculations. Appropriations did not increase from FY20 to FY21 because the state operated on a continuing resolution in FY21.[4] Key takeaways (see Table 2):

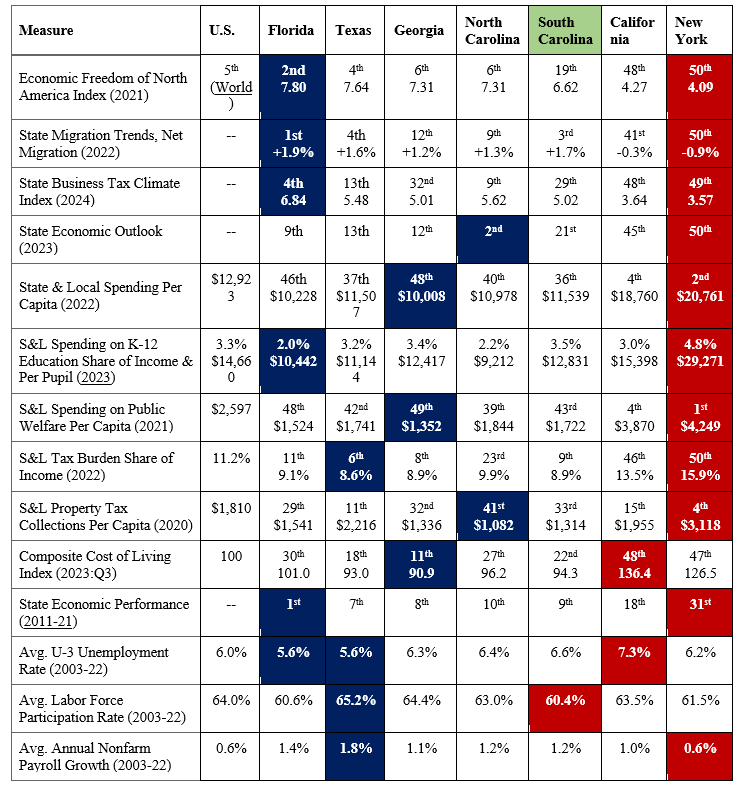

Note. Budget amounts are based on data from South Carolina’s state budget publications, Fed FRED for state population growth and U.S. chained-CPI inflation, and authors’ calculations. These data provide clear evidence that there is room for the state to limit spending growth to reduce taxes substantially. South Carolina has been one of the 25 states in the last three years to cut income taxes, which has helped the state improve compared to its neighbors. However, North Carolina recently passed legislation that could eventually bring their income tax rate to 2.49%, which would be the lowest in the country, excluding the seven states without personal income taxes. On that list are Florida and Tennessee, two major competitors for jobs and investment in the Southeast. South Carolina could improve its position by passing sustainable budgets and using the surplus revenue to cut taxes, especially income taxes. See Table A in the Appendix for more comparisons of South Carolina with other states. Follow the SC Sustainable Budget We strongly encourage legislators to follow the SCSB when drafting South Carolina’s FY25 budget. As a data-driven resource, the SCSB sets a clear spending limit based on what the average taxpayer can afford to pay for government services. Surpassing this limit will fuel excessive government growth and promote unsustainable spending, leaving less revenue that can be used to lower taxes. Recent budget projections show a historic opportunity for tax relief – if legislators are willing to take it. In its November 2023 forecast, the S.C. Board of Economic Advisors (BEA) estimates a recurring budget surplus of $673.1 million for FY25. It also projects the cost of lowering South Carolina’s top personal income tax rate from 6.4% to 6.3% to be roughly $100 million (which is accounted for by BEA prior to their $673.1 million projection). Based on current data, we estimate[1] it would cost an additional $300 million in revenue to cut the top rate immediately to 6% in the new budget. Accordingly, this all-at-once cut could be achieved using less than half of the projected recurring surplus. Passing a sustainable budget would be easier if state agencies followed South Carolina’s legal budget process. Under current law, agencies are supposed to justify every dollar they are requesting when submitting their annual budget plans to the governor – explaining why both new and current programs deserve taxpayers’ money. The law follows a concept known as zero-based budgeting, where all expenses need to be justified annually based on need and performance without regard to previous budgets. Despite this legal mandate, agencies only provide details for new spending requests each year. Fortunately, South Carolina is decently prepared for a rainy day should it occur. Voters in 2022 approved two amendments to increase contributions to the state reserve funds – raising the General Reserve Fund from 5% to 7% (over several years) and the Capital Reserve Fund from 2% to 3% of the previous year’s general fund revenue. By law, the reserve funds act primarily as a shield against year-end budget deficits. While these reserve funds are important to withstand volatility in the budget, lawmakers should focus on limiting or cutting the budget for it to be sustainable over time. Conclusion Following the SCSB will put South Carolina in a better position to reduce taxes, avoid the cost of excessive government growth, and give citizens more opportunities to flourish. Had this been done since 2013, the state could have substantially lowered personal income taxes, if not eliminated them. Fortunately, the upcoming budget provides state leaders with another crucial opportunity to rein in spending and deliver much-needed relief. South Carolina taxpayers are counting on it. Appendix: How Does South Carolina Compare with Other States? Table A shows how South Carolina compares with the largest four states in the country (i.e., California, Texas, Florida, New York) and neighboring states (i.e., Arkansas and Mississippi) based on measures of economic freedom, government largesse, and economic outcomes. Table A. Comparison of States for Measures of Economic Freedom and Outcomes  Notes. Dates in parentheses are for that year or the average of that period. Data shaded in blue indicate “best,” and in red indicate “worst” per category by state.

These rankings show that South Carolina is better than most states in terms of economic freedom, but is substantially less economically free than its neighbors of Georgia and North Carolina. South Carolina does better than others in this comparison in terms of having the lowest supplemental poverty rate and near the best in net migration. South Carolina has the highest state and local government spending per capita among its neighbors and a substantially worse business tax climate than North Carolina. The data show that states with less economic freedom (e.g., New York, California, and South Carolina) tend to perform economically worse. On the other hand, those states with more economic freedom (e.g., Florida, Texas, Georgia, and North Carolina) tend to perform economically better. Given these comparisons, South Carolina has much room for improvement to be more competitive and, more importantly, provide more opportunities for human flourishing.  This was originally published at National Review.

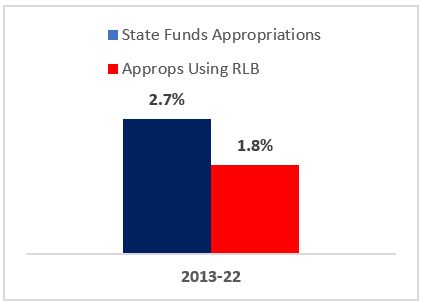

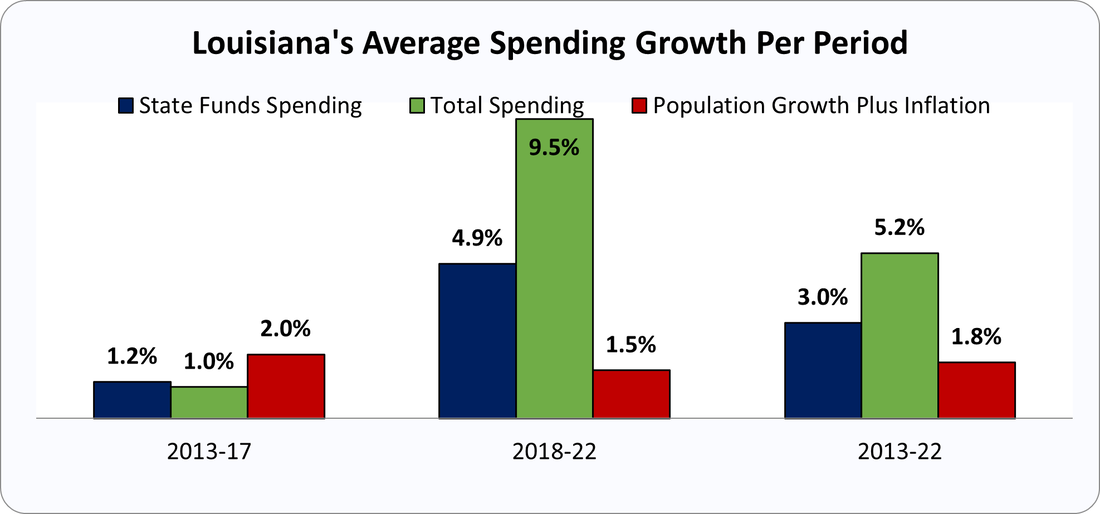

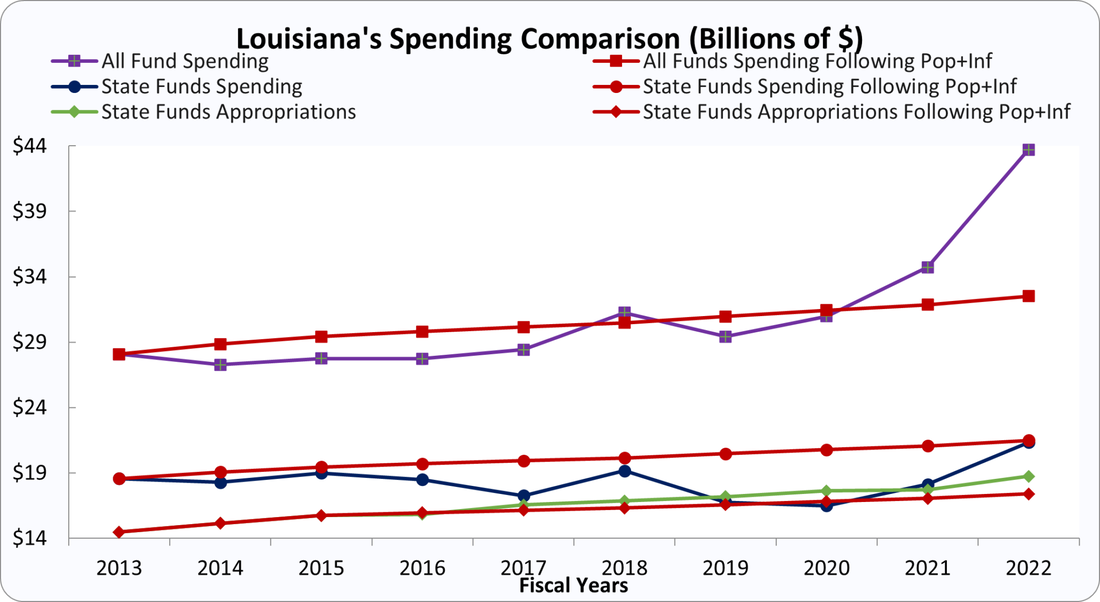

Colorado governor Jared Polis (D) and Art Laffer, the economist and Presidential Medal of Freedom honoree, recently critiqued the state’s Taxpayer’s Bill of Rights (TABOR) at this venue. While not meritless, much of their argument is paradoxical, highlighting an overarching issue of fiscal unsustainability that warrants a reality check. TABOR recently had its 30th birthday. Voters approved the constitutional amendment in 1992, establishing the strongest tax and expenditure limit in the country. It’s been the gold standard for a sound spending limit ever since. Under the amendment, annual growth in spending cannot exceed the state’s population growth plus inflation, which is a good measure of the average taxpayer’s ability to pay for spending. When adopted, the limit covered about two-thirds of state spending. It requires voter approval for tax increases and mandates refunds to taxpayers if tax revenue exceeds the limit. In their critique, Polis and Laffer correctly acknowledge that TABOR surpluses indicate that income-tax rates are too high. They’re correct that the state should seek to reduce income-tax rates to prevent overcollection instead of handing out refunds. They’re also correct that a broader tax base is preferable. It enables the tax rates, and therefore the marginal effect of the tax burden, to be reduced as much as possible for all. But Polis and Laffer incorrectly criticize TABOR without realizing its pivotal role in achieving their purported goal to reduce taxes. Without a crucial spending check such as TABOR, the state would tie its budget directly to revenue levels, eliminating any surplus. While Polis has only recently touted reducing state income-tax rates with surpluses, the Independence Institute has long supported a plan called “Path to Zero.” The plan simply limits government spending and uses resulting surpluses to lower tax rates until they’re zero. This is similar to my efforts in Texas, Louisiana, and other states, which start with a sustainable budget approach, as recently explained in a release by Americans for Tax Reform. Unfortunately, courts and politicians have eroded the strength of TABOR over time, primarily because of politicians’ lack of fiscal restraint. The result has been that TABOR now covers less than half of state spending, allowing expenditures of all state funds, which excludes federal funds, to grow faster than population growth plus inflation. Specifically, appropriations of all state funds have increased by 74.2 percent, compared with an increase of just 46.5 percent in population growth plus inflation over the last decade. This has resulted in the state appropriating $4.2 billion more in just fiscal year 2023–24 than if it had been limited to the rates of population growth plus inflation over time, amounting to higher spending and taxes of about $3,300 per family of four. The summed difference each year in all state funds above this metric over the decade amounts to $16.3 billion, or $11,300 per family of four. These amounts don’t necessarily mean that the state needs to start cutting its budget to get back on track, but they do mean that the time to start reining in the budget is now, to reduce these excessive burdens on taxpayers. To that end, Ben Murrey, director of the Independence Institute’s fiscal-policy center, and I have shown the path forward with the Sustainable Colorado Budget (SCB). The SCB is a maximum threshold for the initial appropriations of all state funds and is based on TABOR’s rate of population growth plus inflation. This will help reinforce the original intent of TABOR, by broadening the spending limit to all state funds. The plan would limit nearly two-thirds of state spending each year, as when voters first adopted TABOR. Doing so will result in larger surpluses to reduce income-tax rates yearly until they’re zero. Polis and Laffer are right to want rate reductions, but there are none if there is no surplus. For the upcoming FY 2024–25, the SCB proposes an all-state funds ceiling of $27.70 billion. This uses the prior FY 2023–24 amount of $26.15 billion and increases it by 5.9 percent, calculated using TABOR’s current method and reflecting a 1.0 percent increase in the state’s population and 4.9 percent inflation. As noted above, it would be even better to grow the budget by less or not at all to correct past budgeting excesses. This more robust TABOR approach outlined in the SCB helps to freeze inflation-adjusted spending per capita, allowing the average taxpayer to afford the cost of government. In recent years, the current TABOR limit alone has already produced substantial surpluses that have been refunded to Coloradans. But instead of using this year’s $1.7 billion TABOR surplus to refund overcollected taxpayer dollars, the legislature could have cut the income-tax rate from a flat rate of 4.4 percent, which ranks 14th in the country, to 3.81 percent. Further, had the state over the past decade followed the SCB, which has a larger base budget, lawmakers could have lowered the income-tax rate to 2.96 percent, putting it on a faster path to becoming the lowest flat income-tax rate in the country, below North Carolina’s 2.49 percent. It would also pave the way to zero income taxes by 2042. Polis in his recent article criticizes TABOR for acting as a spending restraint rather than a mechanism to reduce tax rates. Indeed, his track record in the governor’s office demonstrates his distaste for limitations on spending. The state budget has grown 45 percent since he took office less than five years ago; his budget request for the upcoming fiscal year would constitute an astounding 52 percent increase. In a state with a constitutional balanced-budget requirement, it’s paradoxical to support tax cuts without spending restraints. Unfortunately, given his poor track record on spending and his critique of TABOR’s spending restraints — which he and Laffer improperly call a revenue limit — Polis is unlikely to adopt our sustainable budget to produce larger surpluses with which to cut tax rates. On the contrary, this year he supported a measure that would have increased state spending above the current limit, erroneously claiming that it would cut taxes using state surpluses. “A similar tax-rate reduction for property taxes, Proposition HH, failed on the ballot recently in Colorado,” Polis and Laffer write in their recent NRO article. While a clever misdirection, this argument doesn’t hold up. Prop HH didn’t directly offset the TABOR surplus through tax cuts, as an income-tax reduction would. That’s because the measure influenced only local property-tax revenue. Because the State of Colorado generates no tax revenue from property taxes, as those are collected only by local governments, reducing those rates won’t affect the TABOR surplus. Polis and Laffer contend that the state budget indirectly benefits from local property taxes. However, Prop HH would have lessened the state’s share of local funding by only approximately $125 million.  Originally published at Independence Institute. In 1992, Colorado voters adopted the Taxpayer’s Bill of Rights (TABOR) to limit the growth in state and local spending. Over the past three decades, however, politicians from both parties and a complicit judicial branch have exempted more and more state spending from the TABOR limit. When voters adopted TABOR, 67% of state spending was subject to the limit. Today, the majority of state spending is not subject to the limit. Consequently, state spending has far outpaced Coloradans’ incomes over the last decade. To uphold the original intent of voters when they adopted TABOR, Independence Institute proposes the Sustainable Colorado Budget (SCB), which limits state spending from state funds (excluding federal funds) at the rate of population growth plus inflation. The state should then use the surplus revenue above the SCB spending limit to reduce the income tax rate for all taxpayers.  Originally posted at Pelican Institute where I co-wrote it with Jamie Tairov. The Pelican Institute has highlighted the need for better state budgeting and tax reform. This includes the Responsible Louisiana Budget (RLB), which was released earlier this year. The RLB shows that Louisiana’s budget has been growing at unsustainable levels, and that an improved growth factor for the expenditure limit and initial appropriations is needed. Recently, Americans for Tax Reform released a similar comparison for all 50 states, including Louisiana, in its Sustainable Budget Project. This report shows that, on the surface, Louisiana’s spending has not been as unsustainable as the RLB shows. Why is there a different outcome in the two reports?

Outcomes of Each Report The Responsible Budget model is currently being used successfully in other states to rein in spending. This is what Louisiana’s budget would have looked like had the RLB been employed over the last ten years.

Here are the findings from ATR’s Sustainable Budget study over the last decade:

Total spending in FY 22 was 34.4%, or $11.2 billion, higher than the improved expenditure limit. This means that a family of four is paying $8,800 more in taxes to pay for the excess spending, which is not sustainable spending.  Is One Report Better Than the Other?

No. Both reports are accurate and serve different purposes. The RLB uses initial appropriations which helps lawmakers easily compare appropriation amounts from year to year as they are drafting the budget during session. Because it covers spending instead of appropriations, the ATR study is a backwards-looking metric that can be used for making longer-term spending decisions, but it will be limited in its use during a legislative session. Both reports compare the current expenditure limit with a proposed improved expenditure limit. The current limit is the three-year average of personal income growth, which is an extremely volatile measure. The proposed improved limit is the three-year average of population growth plus inflation. The RLB and ATR reports can work together, providing limits on the front and back end to ensure that spending remains responsible throughout the year. Both reports show recent elevated appropriations and spending. There is clearly room for budgeting restraint in Louisiana. These measures have benefits to lawmakers and the public so that they can have the tools necessary to restrain government spending and provide a responsible budget. Doing so will have many payoffs over time, including making the comeback in the Pelican State happen more quickly by eliminating personal income taxes, providing a more dynamic economy, and improving opportunities for people to flourish. Federal and state layouts are vastly outpacing the combined rate of inflation and population growth.  The U.S. national debt recently passed $33 trillion, more than 120% of gross domestic product. Left-wing politicians assert that Americans are undertaxed, but the data show that the government spends too much.

Americans for Tax Reform launched the Sustainable Budget Project in September to document the rise in government spending over the past decade. The results are clear: Overspending is the problem. Between 2013 and 2022, aggregate annual spending by the 50 state governments, excluding federal funds, increased 51.7%. Total annual federal spending rose 69.4% during the decade, more than three times as fast as the 21.6% increase in the rate of population growth plus inflation. If government grows faster than this rate, then it is growing faster than what the average taxpayer can afford. Had the federal government limited the growth in spending to a maximum of the population growth rate plus inflation during that decade, in 2022 the federal government would have spent $1.6 trillion less than it did, resulting in at least a $200 billion surplus. If the federal government had done this over the past two decades, the national debt would have increased by less than $500 billion instead of $19 trillion. If state governments had limited spending growth to the rate of population growth plus inflation during the last decade, they would have spent $1.39 trillion in 2022, $344 billion less than the $1.74 trillion they actually spent. Had federal and state governments simply grown no faster than the rate of population growth plus inflation, taxpayers could have been spared at least $2 trillion in taxes and debt in 2022 and trillions of dollars more over time. The U.S. hasn’t needed drastic budget cuts, just slower, more sustainable debt growth. Our project defines each state’s overspending problem by providing a dollar-figure spending ceiling and allowing anyone to see how government spending in a state has grown relative to the rate of population growth plus inflation. It will publish and promote an annual benchmark spending level for every state, which lawmakers must not exceed if they want to keep state spending in check. Limiting state spending to the Sustainable Budget Project benchmark isn’t impossible. Lawmakers in more states are beginning to implement the sorts of structural reforms necessary to slow the rate of government spending to a sustainable clip. During the past decade, Colorado and Texas have demonstrated that this can be done. Colorado spent a cumulative $12.8 billion less over the past decade than what could have been available under the benchmark. State lawmakers could have dramatically cut the state’s individual income tax. Instead, there is a push in Colorado to raise taxes and destroy the Taxpayer’s Bill of Rights, the state’s constitutional requirement that all tax increases be subject to voter approval and revenue collected in excess of the state spending cap be refunded to taxpayers. Texas spent $16.4 billion less than the benchmark over the past decade, savings that could have been used to eliminate its gross-receipts-style franchise tax and other bad taxes. Rather than continuing to keep state spending in check, Texas lawmakers instead passed the largest state budget in the state’s history this year. Excessive spending at the federal, state and local levels of government deserves more attention. Tax hikes are easy to identify, but there has been no objective, binary metric to determine whether a state government spends too much. By focusing on the rate of population growth plus inflation, the Sustainable Budget Project provides such a standard. Governors and state legislators need to implement reforms and practice restraint to slow the steep upward trajectory of government spending. That lawmakers in large, politically important states have already demonstrated this ability has shown their counterparts in other states and in Washington that sustainable budgeting is possible. With more modest growth in state government spending, lawmakers can lower taxes and Americans can keep more of what they earn. Mr. Norquist is president of Americans for Tax Reform. Mr. Ginn, a senior fellow at ATR, served as chief economist of the White House’s Office of Management and Budget, 2019-20. Originally published at Wall Street Journal.  In 2023, Americans for Tax Reform launched The Sustainable Budget Project, a new venture that monitors state government spending and tracks which states have or have not enacted sustainable budgets.

The Sustainable Budget Project defines a sustainable budget as one that limits the pace of state government spending to lower than the rate of population growth plus inflation, which accounts for the average taxpayer’s ability to pay for government spending.

From 2013 to 2022, the following happened:

There four states that held growth in state funds and all funds below the rate of population growth plus inflation over the last decade, thereby keeping taxes lower than the average taxpayer can afford:

Go to ATR's Sustainable Budget Project to find out the following information:

Originally posted at Americans for Tax Reform. Overview

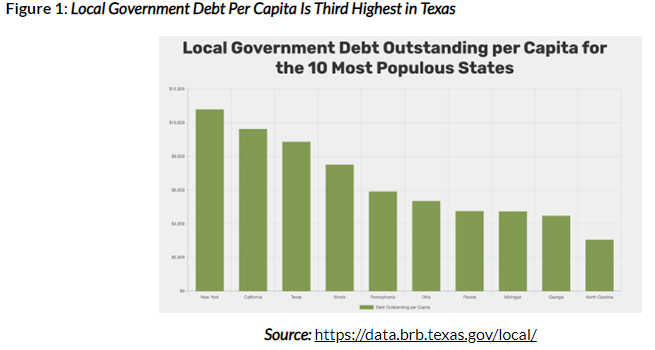

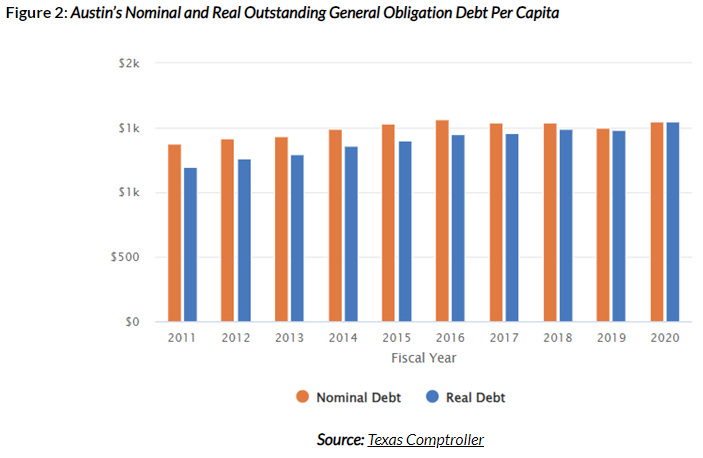

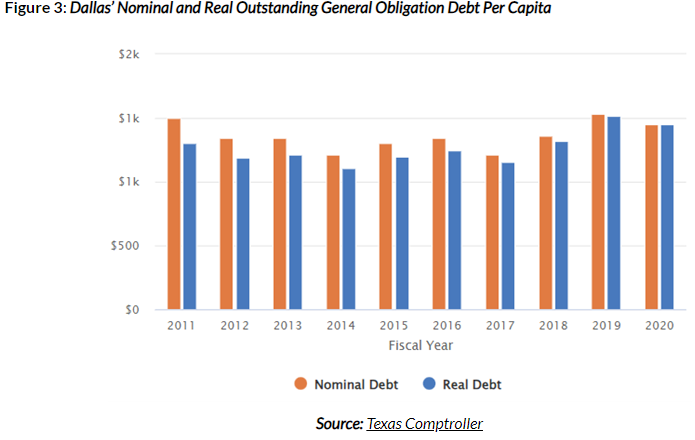

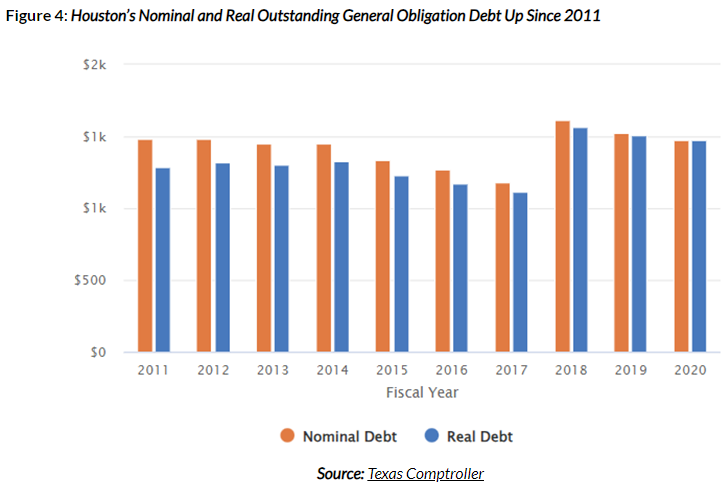

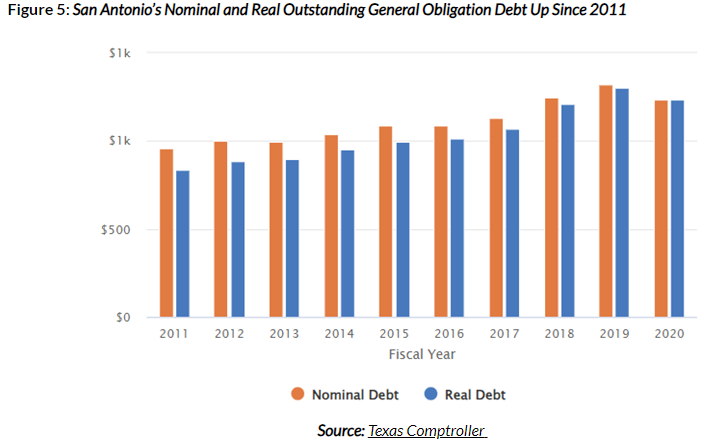

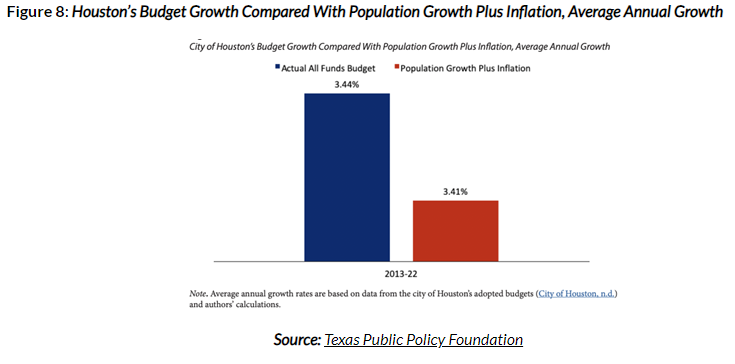

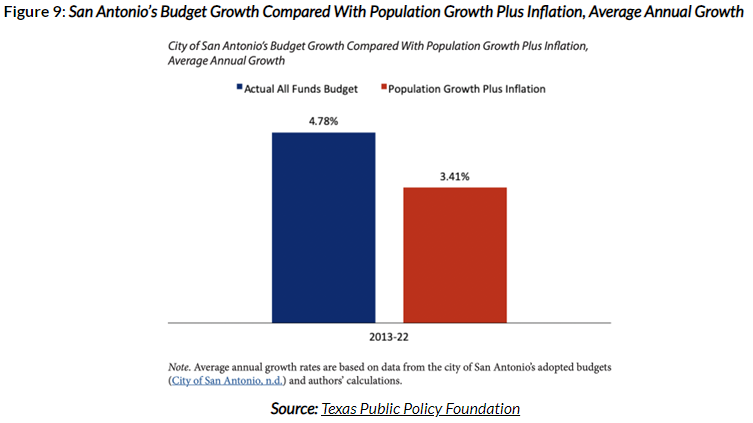

Debt A recent report by the Texas Bond Review Board notes that Texas’ total outstanding local government debt is $280 billion, resulting in debt per capita of $8,869. This puts Texas’ local debt per capita in third place of the largest 10 states, behind only New York ($10,788) and California ($9,621), and nearly twice as high as in Florida ($4,753) (Figure 1).  The following figures show the Texas Comptroller’s data for nominal and real (inflation-adjusted) outstanding general obligation (GO) debt for four of the largest cities in Texas (Austin, Dallas, Houston, and San Antonio). Each of them shows increased GO debt per capita from 2011 to 2020 in nominal and real amounts. But these amounts per capita show some differences.

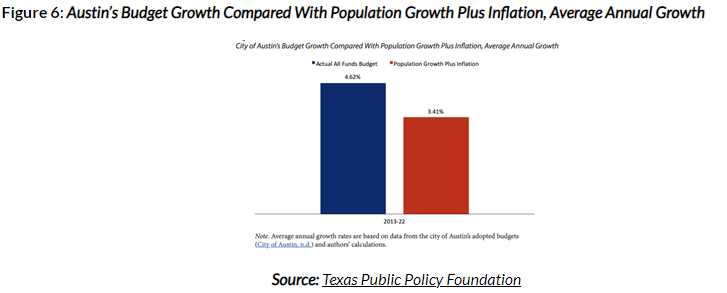

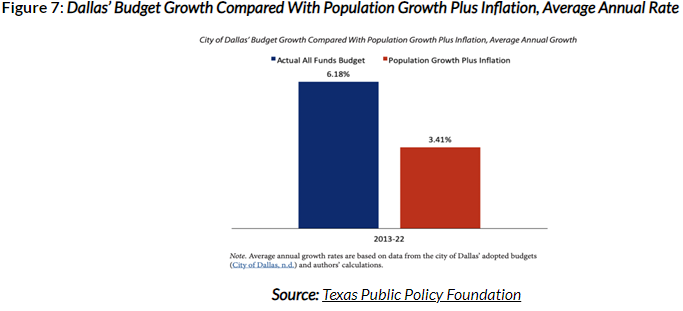

The unsustainable deficit accumulation across many of Texas’ local governments reflects irresponsible spending. Economist Michael Munger called this “Deficits Are Future Taxes” (DAFT), meaning, increased debt signals a current spending issue and a future taxation problem for the next generations. This is a significant challenge for the state’s future and drives up property taxes higher than otherwise. Spending My analysis in June 2022 found that Texas’ four major cities have exceeded a responsible city budget for years, contributing to higher taxes and debt. This responsible budget sets a maximum threshold based on the average taxpayer’s ability to pay for it, which is best represented by a fiscal rule of a spending limit with the rate of population growth plus inflation. Of course, this growth is a maximum as the budget really should be frozen or even cut for most governments given their spending excesses over time. Truth in Accounting defines the local taxpayer burden as “the approximate dollar amount that would be required of each taxpayer in order to pay off all of a government’s liabilities today. It is calculated by dividing the ‘money needed to pay bills’ by the estimated number of taxpayers in the state or city,” demonstrating the depth of debt.

When local governments want to spend more given their balanced budget requirements, they must raise taxes, and they primarily raise property taxes. Tax Revenue The Texas Comptroller reports that property taxes are the biggest revenue source for local governments. Here are the current total property tax rates for these large cities:

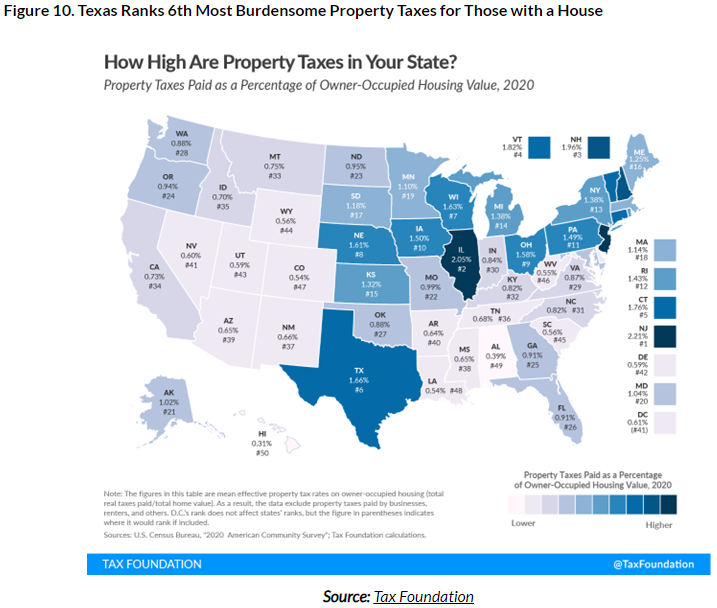

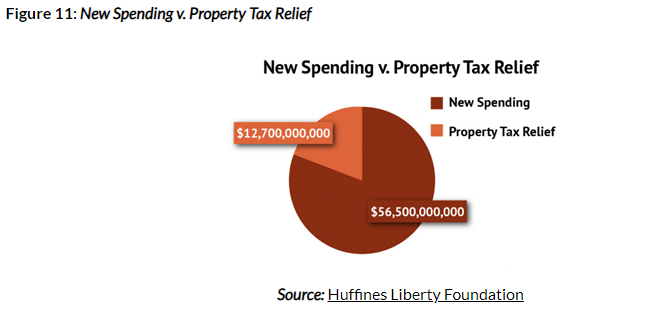

According to the Tax Foundation, Texas currently has the sixth-highest property tax burden on those with a home in the country (Figure 10)  Although the Lone Star State has no income tax, its substantial property tax burden increases because of excessive local government spending increases in recent decades has burdened renters and holders of a home, reducing the state’s affordability. The Tax Foundation’s state business tax climate ranks Texas 38th out of 50 for the burden of property taxes. The Texas Legislature recently passed and Governor Greg Abbott signed Senate Bill 2 with $12.7 billion in property tax relief. This package includes reducing the school district maintenance and operations (M&O) property taxes by 10.7 cents per $100 valuation. It also includes raising the homestead exemption for school district property taxes by $60,000 to $100,000. However, this package should have been much larger, as there were $33 billion in surplus funds available and tens of billions of dollars more available, leaving plenty of taxpayer money to return. The property tax bills provided further complicate the tax system and will not result in as much relief as some are advertising. The best approach was to reduce school district M&O property tax rates with all the relief provided. This should have been at least $21 billion for a reduction of 25 cents per $100 valuation. This would have provided the largest property tax cut in Texas history (Figure 11) instead of the second largest because of the largest spending increase in the state’s history.  Recommendations

For the state to stay competitive and improve the future for Texans, Texas should seek to reform the largest hindrances to its economic flourishing: government spending and property taxes.

Conclusion The ultimate burden of government is not how much it taxes, but how much it spends. This is true at the national, state, and local levels. Texas boasts many metrics of economic freedom, including no personal income taxes, less burdensome regulations, and relatively less government spending. Recent increases in these areas hinder opportunities to prosper. Immediate policy changes to state and local budgeting that will eliminate property taxes, increase transparency for budgets, debts, and taxes, and strengthen their fiscal situation will help Texas better support prosperity for Texans today and for generations to come. Moreover, this will finally give Texans their God-given right to own property instead of renting from the government forever. Stop renting, start owning! Originally published with links to all sources at Texans for Fiscal Responsibility.  President Calvin Coolidge regarded “a good budget as among the most noblest monuments of virtue.” Government spending is at the heart of sound public policy. President Coolidge understood the importance of economy in government in order to achieve sound public policy. President Coolidge’s fiscal conservatism is being exemplified at the state level by Iowa Gov. Kim Reynolds, who is making fiscal conservatism a priority resulting in benefits to Iowans. Gov. Reynolds, just as with Coolidge, understands that prudent budgeting is a virtue.

Despite the national economic malaise from high inflation and stagnant growth, Iowa’s fiscal foundation was strong heading into the 2023 legislative session. Last year, Gov. Reynolds and the Iowa Legislature continued to place a priority on prudent budgeting. The general funds budget for fiscal year 2023 was $8.2 billion, increasing by just 1 percent from the prior year. This session the legislature enacted an $8.5 billion budget for fiscal year 2024, which is a 3.6 percent increase from the previous year’s budget. This holds the budget well below the Conservative Iowa Budget, which set a cap on the budget of $8.8 billion based on the maximum rate of population growth plus inflation of 7.4 percent. In other words, taxpayers benefit from the budget growing well below the growth of the economy, allowing more money in the productive private sector. In January, Gov. Reynolds proposed an $8.48 billion budget, which reflected her priorities including funding the Students First Act, which created a universal Education Savings Account program. After budget negotiations between the House and Senate, the Legislature passed a budget that was a slight increase from the governor’s original proposal. The $8.5 billion budget spends only 88.25 percent of projected tax collections. Since 2018, Gov. Reynolds and the Legislature have placed an emphasis on passing tax reforms and restraining the growth of spending. This approach has left more money in taxpayers’ pockets with a substantial tax relief package headed toward a low flat tax by 2026. What too many people overlook is that significant tax cuts like Iowa’s are only made possible by years of prudent and conservative budgeting. Without spending restraint, any tax relief, regardless of the tax, becomes impossible. The evidence is clear that prudent budgeting is paying off for Iowans. Iowa’s budget continues to be in surplus. The surplus for fiscal year 2023 is projected to be $1.7 billion and the current estimated surplus for fiscal year 2024 is projected to be $2 billion. In addition, Iowa’s reserve accounts (Cash Reserve Fund and the Economic Emergency Fund) will continue to be funded at their statutory limits with a combined balance of over $961 million. The Taxpayer Relief Fund will also continue to increase. The balance in the Taxpayer Relief Fund for fiscal year 2023 is $2.7 billion and this is estimated to increase to $3.5 billion in fiscal year 2024. Both Gov. Reynolds and legislative leaders have signaled that further income tax reform will be a priority for the 2024 legislative session. The Taxpayer Relief Fund, which was originally created for the purpose of income tax relief, will be instrumental in further income tax rate reductions. Iowa Senate Republicans introduced an income tax reform proposal this past session that if enacted would have sped up the income tax rate cuts and used the Taxpayer Relief Fund to phase-out the income tax altogether. In addition to restraining spending, Gov. Reynolds also made some important reforms that will impact future state spending. One of her major priorities was to reform state government. Gov. Reynold’s state government reform measure consolidates and makes government more efficient. Currently, Iowa has 37 executive branch cabinet agencies – more than all neighboring states. The governor’s proposal will reduce the number of executive-level agencies to 16, streamlining and cutting bloated bureaucracy while saving taxpayer dollars. It is estimated that this plan will save taxpayers over $214 million over four years. This was the first major reform of Iowa’s bureaucracy in nearly 40 years. Further, Reynolds issued an executive order at the beginning of the legislative session that requires an extensive review process of Iowa’s regulatory code. Both reforming Iowa’s bureaucracy and reducing burdensome regulations are essential in the path to sustaining limited spending. In its Fiscal Policy Report Card on America’s Governors 2022, the Cato Institute ranked Gov. Reynolds as the best governor. “Governor Reynolds has been a lean budgeter and dedicated tax reformer since entering into office in 2017,” wrote Chris Edwards and Ilana Blumsack, authors of the report. This year, Gov. Reynolds and the Legislature are continuing this trend. Iowa is at the forefront of conservative budgeting that other states and the federal government should follow. Originally published at The Center Square and co-authored with John Hendrickson at Iowans for Tax Relief Foundation. This Week's Economy Ep. 8 | TRUTH On Inflation, U.S. Dollar, Debt Ceiling, Texas & Louisiana Policy5/12/2023 Thank you for checking out the 8th episode of "This Week's Economy,” where I briefly share insights every Friday on key economic and policy news across the country. Subscribe to receive new posts and support my work. Today I cover:

1) National: Breaking down the latest report on CPI inflation and how it relates to real average weekly earnings, what’s going on with the debt ceiling debate, and why the Fed should continue to raise its interest rate target and cut its balance sheet; 2) States: ALEC's newest "Rich States, Poor States" report findings related to where Texas stands in comparison with Utah and Florida, what the legislatures are doing late in the sessions of Texas (here), Louisiana (LA jobs report and tax relief), and elsewhere; and 3) Other: New findings on the importance of work-life balance, the value of the U.S. dollar, and more. You can watch this episode and others along with my Let People Prosper Show on YouTube or listen to it on Apple Podcast, Spotify, Google Podcast, or Anchor (please share, subscribe, like, and leave a 5-star rating!). For show notes, thoughtful insights, media interviews, speeches, blog posts, research, and more, continue to check out my website (https://www.vanceginn.com/) and please subscribe to my Substack newsletter (https://vanceginn.substack.com). In Let People Prosper episode #42, I talk w James Hohman with Mackinac Center for Public Policy about improving Michigan's economy, right-to-work policies, corporate welfare, and budget. On today's episode of the "Let People Prosper" show, I'm thankful to be joined by James Hohman, Director of Fiscal Policy at the Mackinac Center for Public Policy and host of The Overton Window Podcast.

We discuss: 1) Right-to-work policies, workers' unions, and corporate welfare; 2) How shutdowns impacted the economy of his home state, Michigan; and 3) A path forward for the state, and others, to prosper with a Sustainable Michigan Budget and more. You can watch this interview on YouTube or listen to it on Apple Podcast, Spotify, Google Podcast, or Anchor (please share, subscribe, like, and leave a 5-star rating). James’ bio:

In Let People Prosper episode #41, I talk w Dan Mitchell, Ph.D., about the need government spending limits, benefit of flat tax revolution, Fed's booms and bust cycles, and more to let people prosper. On today's episode of the "Let People Prosper" show, which was recorded on March 24, 2023, I'm thankful to be joined by Dr. Dan Mitchell, President of the Center for Freedom and Prosperity and blogger at International Liberty.

We discuss: 1) Lessons from history on government spending and why strong spending limits are needed at every level of government; 2) Issues with the Fed creating artificial cycles of booms and busts; and 3) Reasons to be optimistic about the flat tax & and school choice revolutions happening in states across the country. You can watch this interview on YouTube or listen to it on Apple Podcast, Spotify, Google Podcast, or Anchor (please share, subscribe, like, and leave a 5-star rating). Dan Mitchell’s bio:

For show notes, thoughtful economic insights, media interviews, speeches, blog posts, research, and more, check out my personal website and subscribe to my Substack newsletter where you can get every episode in your inbox.  Budgeting responsibly is key to Louisiana’s Comeback Agenda, and Pelican’s Chief Economist, Dr. Vance Ginn, has released a plan to rein-in state spending. Check out the proposed Responsible Louisiana Budget, below. This plan gives Louisiana a competitive advantage and is similar to those used in other states, like Texas and Florida, limiting the amount of funding appropriated at the beginning of each fiscal year, which has made lower taxes possible. Originally posted at Pelican Institute.  A new report by Dr. Vance Ginn, senior fellow at The James Madison Institute and president of Ginn Economic Consulting recommends that the state continue to limit the burden of government spending. The Conservative Florida Budget (CFB) sets a maximum threshold in all funds appropriations for FY 2024 of $116.2 billion. This maximum threshold is based on the 5.5% rate of the 3-year average of population growth plus inflation over the last three years from 2020 to 2022, which reasonably represents the average taxpayer’s ability to pay for government spending. “Legislators should use the CFB as a guide this session. Given the economic headwinds from the poor fiscal and monetary policies out of D.C. contributing to elevated inflation and risks of a deep recession along with past state budget excesses, the Legislature should pass a budget well below the CFB, similar to the Governor’s budget. Doing so will ensure a conservative budget that will help keep more money in taxpayers’ pockets through larger tax relief, so families and entrepreneurs have the most opportunities to flourish.” — Dr. Vance Ginn, Senior Fellow, The James Madison Institute; President, Ginn Economic Consulting. Originally published by James Madison Institute.  With a debt ceiling fight and bank failures, Congress’ day of reckoning to spend less is now.

Inflation is sky-high, purchasing power is sinking, 60% of Americans live paycheck to paycheck, and credit card debt is soaring to nearly $1 trillion. To make matters worse, between the fourth quarter of 2021 to the fourth quarter of 2022, U.S. real GDP grew by just 0.9%, the slowest growth in a “recovery” since at least 2009 amid the Great Recession. The more the federal budget deficit grows because of excessive government spending, the more the budget is crowded out from funding legislative priorities. In turn, Congress is forced to find ways to pay for interest on the debt, which will soon exceed $1 trillion. It’s not just the budget that’s getting crowded out; productive activity in the private sector fueled by entrepreneurs is stifled due to too much money chasing too few goods and services at the hands of tyranny imposed by big government. The underlying culprits to these economic catastrophes are reckless, weaponized government spending, often funding tyranny against Americans, and the Federal Reserve holding a bloated balance sheet. This excess national debt and money printing contributed to the latest closure of Silicon Valley Bank and will have further consequences. These government failures should be addressed by Congress spending less. This should include reducing federal funds sent to states. Not only do federal funds diminish federalism by making states dependent on the federal government but it also comes with massive red tape. The U.S. system of federalism provides a unique laboratory of competition to see what works across the states. This is best observed and encouraged by letting states be as independent as possible. Considering that federal deficits are expected to increase by an average of $2 trillion annually over the next decade, states would be wise to prepare for fewer federal funds as Congress’ purse strings will tighten. According to Congressman Chip Roy (R-TX) in a recent interview, another major way the government drives up spending is by hiding behind so-called mandatory expenditures such as Medicare and Social Security, and discretionary spending, which is funding tyranny through the weaponization of bureaucrats. “We have to commit to not funding tyranny such as the IRS going after minorities and poor people,” said Congressman Roy. “Why should we fund the FBI labeling Scott Smith, a man who stood up for his daughter being sexually assaulted to her school board, a domestic terrorist? Likewise, military funding should go toward making us a strong defense, not to ensuring that recruits ‘stay woke’ and never say ‘sir’ or ‘ma’am.’” While it’s politically popular for the government to honor its commitments like Social Security and Medicare for current retirees, mandatory spending is excessive and needs reforms to remain solvent over time. Cutting non-defense discretionary spending–including abolishing Departments of Education and Energy–to pre-Covid levels, would mean saving $3 trillion over the next decade. But both Republicans and Democrats have to work at this as they’re equally culpable of driving up spending under many administrations. And these expenditure savings need to be closer to $8 trillion to stabilize the debt to output level per the Committee for a Responsible Federal Budget. In addition to tightening up federal funds sent to states and mandatory expenses, the government should consider adopting a Responsible American Budget, similar to what’s been practiced in Texas, Florida, and Tennessee, that’s helping their economies thrive. This would require adopting some sort of fiscal rule like a spending cap, but as Congressman Roy emphasized, without passing exceptions that would render the rule irrelevant. If such a rule based on the maximum growth rate of population growth plus inflation, which represents what the average taxpayer can afford, had been in place, then we would have accrued $500 billion in new debt rather than $19 trillion over the last 20 years. Returning the federal government to its constitutional role of preserving liberty is key to economic growth. The surest way to suffocate the productive private sector from innovating and Americans from prospering is to let spending increases continue. This is the biggest threat to the American dream today, which younger generations are already counting dead as they’ve seen such poor economic growth in their lifetimes. If the future of the nation and opportunities for upcoming generations is important, the government must earn Americans’ trust by spending less, reforming mandatory programs, cutting federal bureaucracy, and promoting other pro-growth policies. As Congressman Roy shared, “I didn’t inherit a free country to pass down an unfree one. We have to fight.” Originally posted at The Daily Caller.  Iowa’s fiscal foundation remains strong despite national economic uncertainty because of the state’s fiscal conservatism and prudent budgeting.