Originally published at Texans for Fiscal Responsibility. Overview

Texas’ employment has been up for 44 of the last 46 months since May 2020.

Figure 1. Texas Labor Market by Industry  Source: U.S. Bureau of Labor Statistics Economic growth has picked up, but personal income lags the U.S. average.

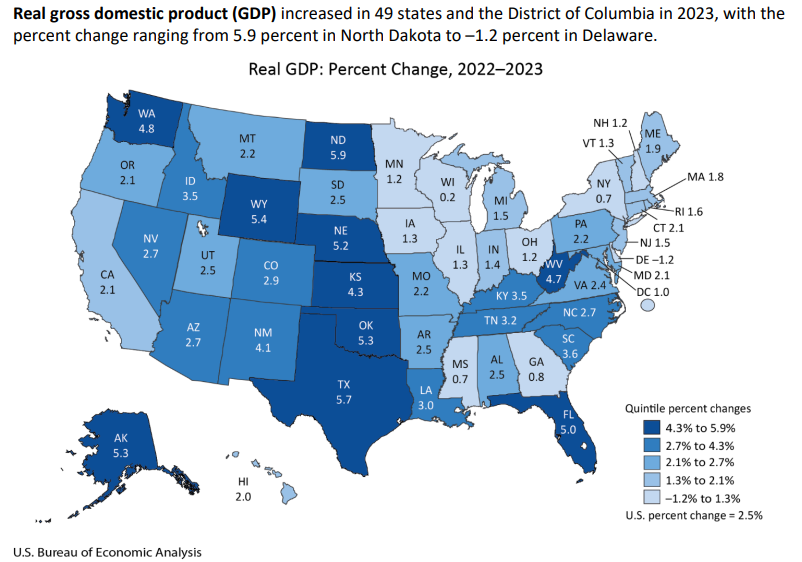

Figure 2: Real Gross Domestic Product by State in 2023  Improve the Texas Model with pro-growth policies that limit government by:

0 Comments

How Government Influences Bridge Repairs and Minors on Social Media | This Week’s Economy Ep. 543/29/2024 In “This Week’s Economy” episode 54, I discuss the following and more:

See show notes on Substack: www.vanceginn.substack.com Visit my website for more economic insights: www.vanceginn.com  Originally published at Texans for Fiscal Responsibility. Highlights

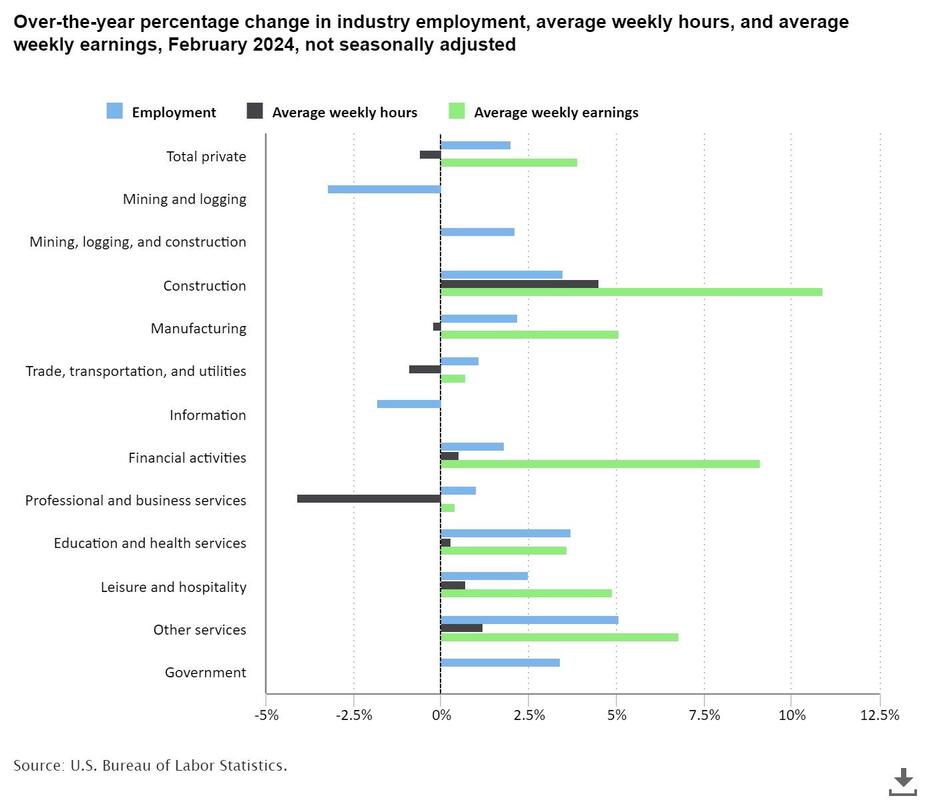

Figure 1: Real Average Weekly Earnings Remain Down 4.2% Since January 2021  Source: Fed FRED Labor Market The Bureau of Labor Statistics recently released its U.S. jobs report for February 2024, which was another mixed report with some strengths but many weaknesses.

Figure 2. Changes in Employment by Industry Over the Last Year  Source: Fed FRED

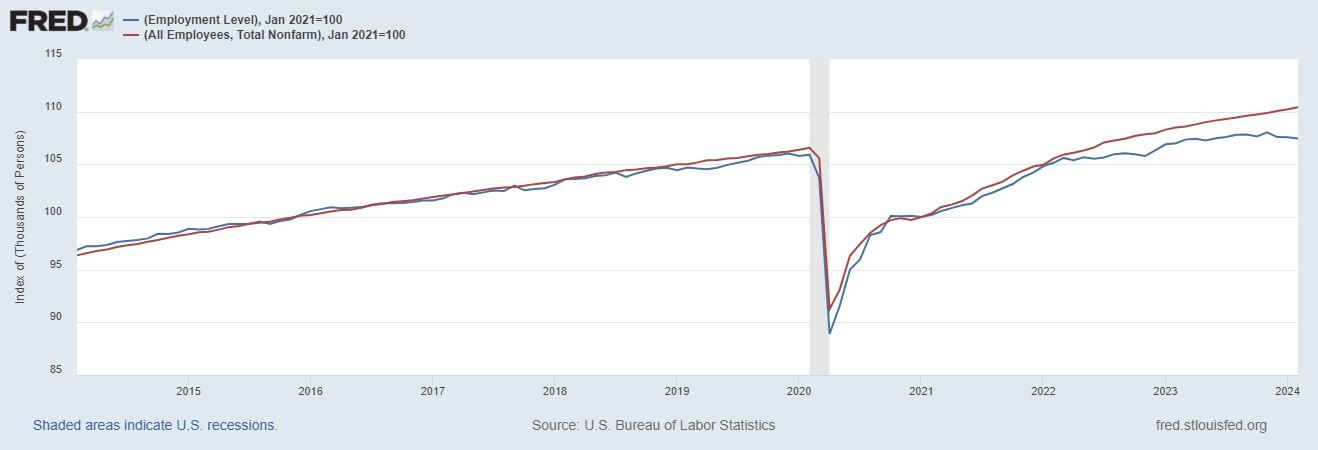

Figure 3. Establishment Nonfarm Jobs Far Outpace Household Employment Level Since March 2022  Source: Fed FRED

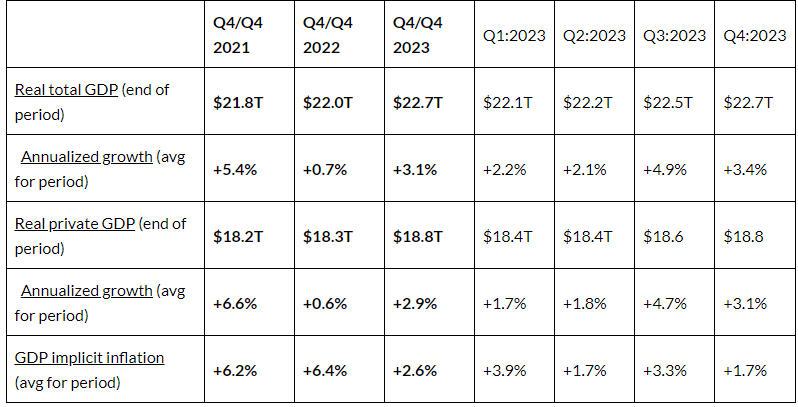

Economic Growth The U.S. Bureau of Economic Analysis recently released the third estimate for economic output in the fourth quarter of 2023.

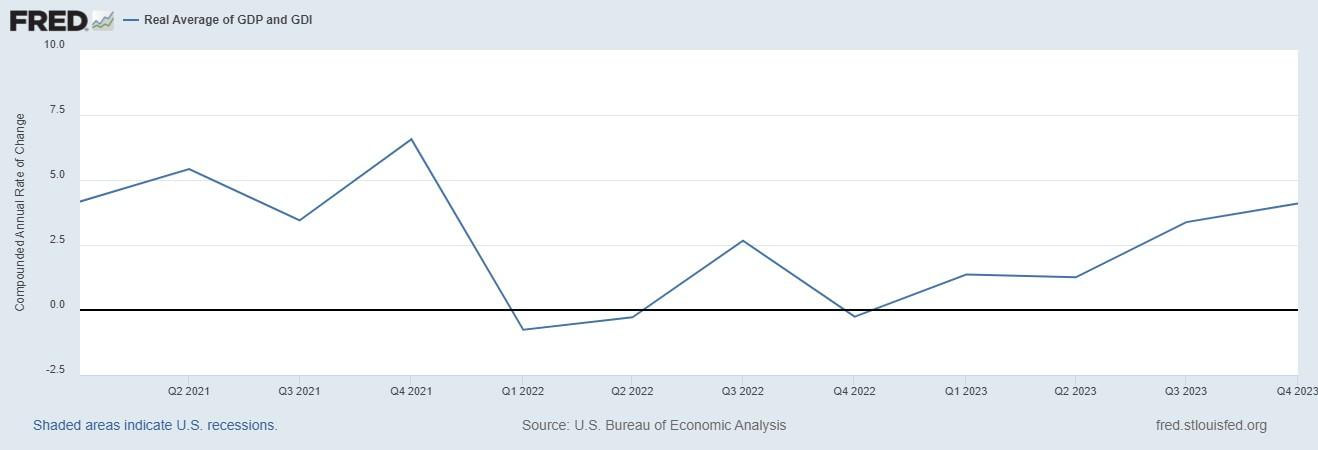

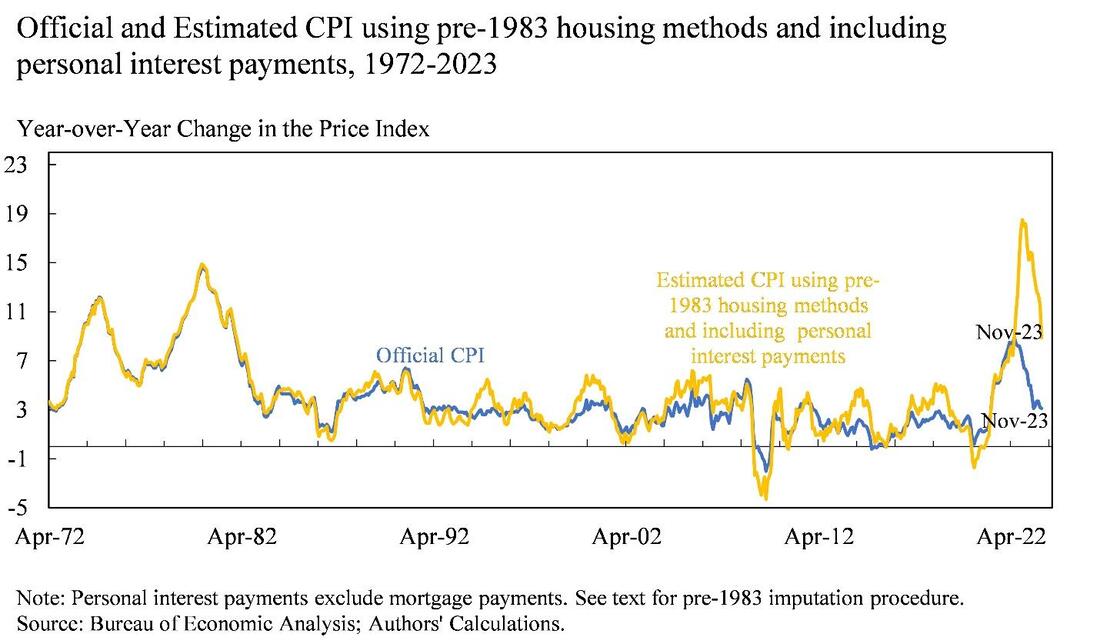

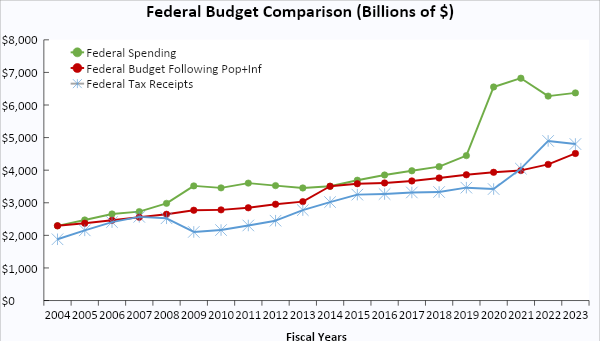

Table 1: Economic Output, Growth, and Inflation  Another key measure of economic activity is the real average of GDP and GDI, which accounts for domestic production and income and is known as real gross domestic output. Real GDO in the third quarter increased by 3.4%, and in the fourth quarter increased by 4.1% to $22.5 trillion. Figure 4 shows how this measure has declined on an annualized basis in three of the last eight quarters, increasing this value by only 2.9% since the fourth quarter of 2021 before the two consecutive quarters of declines in the first and second quarters of 2022. Figure 4. Annualized Real Gross Domestic Output Growth  Meanwhile, the federal budget deficit continues unabated because of overspending and declining tax collections from a weaker economy. The national debt has ballooned to $34.6 trillion, and net interest payments on the debt will soon be a top federal expenditure, rising to above $1 trillion. The Federal Reserve has monetized, or printed, much of the new Treasury debt to keep interest rates artificially lower than where the market would suggest. The Fed will need to cut its balance sheet (total assets over time) more aggressively if it is to stop manipulating markets (see this for types of assets on its balance sheet) and persistently tame inflation. The current annual inflation rate of the consumer price index (CPI) has been moderating since a peak of 9.1% in June 2022 but remains elevated at 3.2% in February 2024. Compared with the Fed’s average inflation rate target of 2%, which really should be 0%, the current CPI inflation rate is too high, as are other key measures of inflation. A recent paper by Larry Summers, who was the 71st Secretary of the Treasury for President Clinton and Director of the National Economic Council for President Obama, and co-authors notes that if the calculation of CPI kept housing calculation methods and personal interest payments in, then the latest peak in inflation would have been 18% instead of 8.1%. Figure 5 shows their chart with these data that also highlights how the method-adjusted inflation would be closer to 10% instead of the reported 3.1%. Figure 5. CPI Inflation Differences When Methods Are Similar Over Time  Just as inflation is always and everywhere a monetary phenomenon, deficits and high taxes are always and everywhere a spending problem. David Boaz at Cato Institute has noted how this problem is caused by both Republicans and Democrats. To control this fiscal and monetary crisis, the U.S. needs a fiscal rule like the Responsible American Budget (RAB) with a maximum spending limit based on the rate of population growth plus inflation. This was recently released as part of Americans for Tax Reform’s Sustainable Budget Project, highlighting this approach’s benefits at the federal, state, and local levels. If Congress had followed this approach from 2004 to 2023, Figure 4 shows tax receipts, spending, and spending adjusted for only population growth plus chained-CPI inflation. Instead of an (updated) $20.2 trillion national debt increase, there could have been only a $700 billion debt increase for a $19.5 trillion swing in a positive direction that would have substantially reduced the cost of this debt to Americans. The Republican Study Committee recently noted the strength of this type of fiscal rule in its FY 2025 “Fiscal Sanity to Save America.” To top this off, the Federal Reserve should follow a monetary rule so that the costly discretion stops creating booms and busts. Figure 6: Federal Budget Gap Shrinks If Spending Limited to Population Growth Plus Inflation  Bottom Line

Bidenomics has been a failure and the policy approach must be redirected to pro-growth policies that shrink government rather than big-government, progressive policies. It’s time for a limited government with sound fiscal and monetary policy that provides more opportunities for people to work and have more paths out of poverty. Recommendations:

In the wake of the Baltimore bridge collapse, a major U.S. port has come to a standstill. The Port of Baltimore is the top U.S. port for vehicle imports and exports, as well as for farm and construction machinery. U.S. Transportation Secretary Pete Buttigieg told MSNBC on Wednesday that while there are many ports on the U.S. East Coast, “there is no substitute for the Port of Baltimore being up and running.”

How will this affect the U.S. economy—and even global supply chains? NTD spoke to Vance Ginn, the president of Ginn Economic Consulting and the former chief economist at the U.S. Office of Management and Budget, to find out more.  Originally published at AIER.

Recently, the Biden administration handed $1.5 billion to the nation’s largest domestic semiconductor manufacturer, GlobalFoundries, the biggest payout from the CHIPS and Science Act of 2022 so far. The argument for this corporate welfare is America is too dependent on chips from China and Taiwan so more should be made domestically. Instead of seeing how America should reduce the cost of doing business for all semiconductor businesses here, some businesses will be picked as winners and others as losers. The cost of this form of socialism gives capitalism a bad rap and should be rejected. This move echoes a broader trend of governments worldwide intervening in their economies through industrial policy. A cocktail of targeted subsidies, tax breaks, and regulatory tinkering, industrial policy aims to sculpt economic outcomes by favoring specific industries or firms, all for the supposed benefit of the national economy. Industrial policy puts business “investment” decisions in the hands of government bureaucrats. What could go wrong? While its champions tout its potential to boost competitiveness and spur innovation, the reality often tells a different story, especially in light of massive deficit spending. In practice, industrial policy tends to fan the flames of higher prices and sow the seeds of economic destruction. Politicians too often meddle with voluntary market dynamics by artificially bolstering favored sectors through subsidies and tax perks, resulting in the misallocation of resources and distorted prices. Moreover, the infusion of government funds to bankroll these initiatives with borrowed money can contribute to the Federal Reserve helping finance the debt, increasing the money supply, and stoking inflation. The nexus between deficit spending and prices looms large over industrial policy. When politicians resort to deficit spending to bankroll industrial ventures, they put upward pressure on interest rates by issuing more debt and competing with scarce private funds. Elevated interest rates disturb private investment, ushering in a likely economic slowdown. Suppose deficit financing leans heavily on monetary expansion, whereby the central bank snaps up government debt. In that case, it fuels inflation by flooding the market with money that chases fewer goods and services. The national debt is above $34 trillion, and the Federal Reserve has already monetized much of the increase in recent years. Racking up even more deficits is insane: repeating the same mistakes and expecting a different result. Excessive spending and money printing have landed us with above-target inflation for over three years running. The repercussions of industrial policy ripple beyond inflation to encompass the broader economic landscape. Excessive government meddling in specific industries crowds out private investment and entrepreneurship. When particular firms enjoy subsidies and preferential treatment, it distorts the competitive landscape and deters innovation. This stifles economic vibrancy and impedes the rise of new industries or technologies crucial for sustained growth. For a cautionary tale of how Biden’s recent move could play out, look no further than Europe. Nations like Sweden, heralded by the West as a utopian example of big government yielding big benefits, spent the last year grappling with economic strife driven by dwindling private consumption and housing construction. Europe’s penchant for industrial policy, marked by subsidies, high taxes, and regulatory hoops, has contributed to its economic stagnation. To sidestep the dilemma of industrial policy missteps, policymakers should stop propping up their favorite sector or industry and instead unleash people to flourish by getting the government out of the way. Politicians should foster an environment conducive to entrepreneurship, innovation, and competition. This entails cutting government spending, reducing taxes, trimming red tape, and championing trade by removing barriers to private sector flourishing. By allowing market forces to determine resource allocation and rewarding entrepreneurship and risk-taking, people here and elsewhere can unleash their full potential and adapt to changing circumstances more effectively than under industrial policy frameworks. Biden’s billion-dollar amount to one company may seem like a lot, but that’s just a drop in the bucket of what’s to come from the CHIPS Act. Instead, these funds should be eliminated, preventing Congress from taking us further down the road to serfdom. Originally published at Texans for Fiscal Responsibility.  Executive Summary

Originally published at Texas Scorecard.

Texas can pass bold school choice legislation when the next legislative session starts in January 2025. This could finally happen because of the recent election wins in the House primaries, efforts led by Gov. Greg Abbott. The election wins include pro-school choice candidates beating anti-school choice incumbents or filling seats of retiring anti-school choice members. More incumbents, including House Speaker Dade Phelan, were forced to a runoff in May. Moreover, 80 percent of Republicans voted for Proposition 11 on the primary ballot to support school choice, which matters in a dominantly red state. In the evolving educational reform landscape, universal education savings accounts (ESAs) provide the best path to empower parents to decide their children’s education. They are also a practical, fiscally responsible strategy for reimagining the future of education. At least 10 states have passed universal school choice, and more are likely to do so soon. But these states haven’t reached the pinnacle of what a competitive education system should look like. The optimal school choice approach should liberate education from the constraints of the monopoly government school system, draw upon successful market-driven solutions, and offer a simplified education finance system. The Texas Legislature essentially controls the current school finance system with funding from taxpayers through taxes collected by the state, school district, and federal governments. The inefficiency and ineffectiveness of the status quo are stark, including questionable but relevant declining test scores. This highlights a critical need for an approach that better serves students’ and families’ unique needs and aspirations. The state’s school finance system is based on many factors to the school system, but the Texas Education Agency recently reported that the average funding per student was $14,928 in the 2021-22 school year. Total funding was $80.6 billion for 5.5 million students. Of course, this is how much is spent, but the actual cost of the monopoly government school system is hidden and driven higher by politics rather than market outcomes. ESAs provide flexibility in covering many educational services, including various schooling options, tutoring, testing, and other related expenses. This empowers parents to customize their children’s education to suit individual learning styles and interests. This adaptability is vital for fostering environments where children excel academically, socially, and emotionally. Implementing a universal ESA program demands a framework that balances simplicity with accountability, ensuring the focus remains on expanding educational opportunities and improving student outcomes. While many current ESA programs run alongside the government school system, this doesn’t provide the most competitive framework. Running them in tandem, whereby the funding remains the same or even increases for government schools while creating a new system to fund ESAs, is costly and lacks the incentives for optimal outcomes. Instead, we should pursue a simplified education finance approach that maximizes competition, reduces costs, and lowers taxes by funding students, instead of a system. A bold proposal would provide parents with an ESA of $10,000 per child for the school year but paid monthly or the preferred frequency to choose any approved schooling, including government, private, charter, home, co-op, tutoring, or other types of schooling. With about 6.3 million school-age children in Texas, the annual total expenditure would be $63 billion, or $17.6 billion less than what’s being spent today on government schools. Parents could receive an ESA of as much as $12,800 per student to keep the same expenditures as today. However, given the bloated bureaucracy and misguided direction of government schools, the $10,000 amount would help force efficiencies while reducing taxpayers’ costs and incentivizing new education providers. The lower cost of $17.6 billion would provide an opportunity for substantial school property tax relief. Combining ESAs and property tax relief would further accentuate the proposal’s appeal, addressing the lack of school choice and burdensome property taxes. The bold approach eliminates most, if not all, of the current antiquated government school finance system with one that gives parents a way to meet their children’s unique learning needs best. It would help alleviate the hardship for many families that can choose alternatives for financial reasons, pay lower property taxes, or have money remaining to invest in their children’s quality of life and educational pursuits. As states across the nation begin to recognize the transformative potential of this bold universal school choice approach, the momentum is undeniable. This trend underscores a growing consensus on the need for educational systems that prioritize choice, flexibility, and parental empowerment. By breaking free from the monopoly government school finance system and embracing a bold ESA finance approach that empowers parents, we can pave the way for a future where every child can achieve their full potential.  Originally published at The Center Square.

The recent surge of bills attempting to rein in social media outrage in Florida and across America has sparked debate over the role of government in regulating them. Florida Gov. Ron DeSantis vetoed an initial bill banning minors on social media. In his veto message, he said, “Protecting children from harms associated with social media is important, as is supporting parents’ rights and maintaining the ability of adults to engage in anonymous speech.” We should empower parents to determine what's best for their children on social media, or otherwise. This will work better than putting politicians and government bureaucrats in charge, which is what these types of bills do. These bills are likely unconstitutional, as they violate the First Amendment. Furthermore, excessive government regulation of social media stifles innovation and entrepreneurship in the digital space, especially small businesses. By imposing burdensome restrictions on online platforms, we risk hindering the development of new technologies and services that could benefit families. A more pragmatic approach fosters competition in the marketplace, allowing consumers to choose the platforms that best align with their values and preferences. These regulations would hurt many start-up firms as they won’t have the resources to hire as many lawyers to jump through the hoops imposed on them that larger, incumbent companies can afford. They would also need to pay third-party verification systems that cost thousands of dollars, making it more challenging to start a business, as noted in a recent report by Engine. Gov. DeSantis has been a vocal advocate for parental empowerment, emphasizing the importance of transparency and accountability from social media companies. His initial pushback of government overreach of social media should be championed rather than resorting to bans for questionable reasons, as social media isn’t the culprit for bad parenting or bad legislation. In light of ongoing NetChoice cases at the Supreme Court, where the organization has fought against state-level regulations deemed infringing on free speech and commerce, we should uphold free speech in the digital age. By joining parents in advocating for greater transparency and accountability by social media companies where applicable, we can champion the interests of Americans and assert state sovereignty. Rather than relying on government mandates and regulations, we should foster a culture of parental responsibility and provide families with the resources they need to navigate the digital landscape safely. If politicians and bureaucrats take over these responsibilities, it will lead to less incentive for parents to be engaged with their kids and what they’re doing online. This would be a terrible path forward as the government has already made bad situations worse regarding safety-net handouts, a monopoly government school system, and more. Let’s stick with a proven approach that supports parents and social media providers rather than a top-down, likely unconstitutional one. Today, I am joined by Dr. Ed Timmons, the Service Associate Professor of Economics and Director of the Knee Regulatory Research Center at the John Chambers School of Business and Economics at West Virginia University.

Join us on Let People People Show Episode 89 as we discuss the following: - Purpose of government licenses - Costs and benefits of occupational licensing - Ways to get the government out of the way of work Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. Subscribe and see show notes for this episode on Substack - www.vanceginn.substack.com Visit my website for economic insights - www.vanceginn.com Who’s REALLY To Blame for the Housing Affordability Crisis: Investors, Markets, or Governments?3/22/2024 In “This Week’s Economy” Episode 53, I discuss the following and more:

- What’s up with the housing market? - Will Louisiana be next to get universal school choice? - Why can’t we treat people like people instead of pawns? Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. Subscribe and see show notes for this episode on Substack - www.vanceginn.substack.com Visit my website for economic insights - www.vanceginn.com  Last week, the Texas Association of Business, Fort Worth Chamber of Commerce, Longview Chamber of Commerce, U.S. Chamber of Commerce, and American Bankers Association sued to block the Consumer Financial Protection Bureau’s (CFPB) final rule to lower the credit card late fees cap to $8.

This lawsuit challenges the Biden Administration's terrible price control idea that would hurt Texans. Given the entities that sued to block this rule and the effect on Texans, the case should continue in Texas instead of moving it elsewhere as the CFPB would like. Credit card late fees, what some call “junk fees,” are the cost of someone paying their bill late. Nothing is free, so there’s a charge for paying late, as it also influences the expected cash flow of credit card companies. It’s not a price gouging scheme; it’s simply a way to take the risk of giving credit to those in need while keeping cash flow for profitability. This is not only important for businesses, but it also provides an incentive for people to pay their bill online. Without a market-based credit card fee, the cost will be on those who need credit the most as they won’t be able to get it or pay much higher interest rates. The Wall Street Journal Editorial Board wrote: “Even the CFPB acknowledges, the lower penalty may cause more borrowers to pay late, and as a result incur higher ‘interest charges, penalty rates, credit reporting, and the loss of a grace period.” Many Texans depend on credit card access to pay their living expenses. There are more than 3 lines of credit per user in Texas. More than 3 million small businesses also rely on access to credit to grow and expand. Some card issuers most impacted by this rule, including Citi, Chase, and Synchrony, have extensive operations in Texas. JCPenney, based in Plano, offers one of the country's most popular co-branded credit cards through its partnership with Synchrony. The retailer, which employs more than 2,000 Texans, is just a few years removed from bankruptcy and stands to lose big if this misguided rule is allowed to stand. Reports indicate late fees account for 14 to 30 percent of department store credit card revenue. Given the current state of credit card delinquencies at a 10-year high, the CFPB’s rule would exacerbate an already dire situation. This would have far-reaching effects on our community and economy, particularly as consumers and small businesses increasingly rely on credit to navigate lower inflation-adjusted average weekly earnings by 4.2% since January 2021. Most of the plaintiffs in this lawsuit are local organizations that recognize the importance of defending and preserving access to credit. Texas is the rightful venue for this battle.  Originally published at AIER.

ohn Cochrane’s The Fiscal Theory of the Price Level examines the relationship between fiscal policy and inflation, which many consider to be the increase in the price level of a basket of goods and services. An influential and accomplished economist at the Hoover Institution, Cochrane is one of the most forward-thinking economists today. His approach challenges conventional wisdom and presents a compelling case for reevaluating our understanding of the economy. I learned much from reading the book and while interviewing him about it on my Let People Prosper Show podcast. I highly recommend reading this extensive book, though I have reservations about fiscal policy trumping monetary policy when considering the influence on inflation. Cochrane begins by laying out the foundational principles of his theory. He emphasizes the roles of government debt, taxes, and inflation expectations on prices. He argues that traditional economic models, which focus primarily on the role of central banks in controlling inflation through monetary policy, such as those by Milton Friedman, overlook the substantial effect of fiscal variables on prices. By uniquely integrating fiscal considerations and the public’s expectations about those factors into economic analysis, Cochrane aims to provide a more robust framework for understanding and predicting inflationary trends. He delves into various theoretical and empirical aspects of fiscal theory, drawing on a wide range of literature and evidence to support his arguments. He explores the implications of government budget constraints, the role of Ricardian equivalence that assumes a balanced budget over time, and the potential limitations of conventional monetary tools in controlling inflationary pressures. His thorough examination of these issues provides readers with a comprehensive understanding of the complexities of studying the relationship between fiscal policy and inflation. Cochrane’s arguments are persuasive and well-supported, but some aspects of his analysis warrant scrutiny. One area of contention is Cochrane’s emphasis on the primacy of fiscal policy in driving inflationary dynamics, particularly his assertion that the Federal Reserve plays a secondary role compared to Congress in shaping inflation outcomes. While Cochrane makes a compelling case for the importance of fiscal variables, the penultimate creator of inflation is the Fed when it creates more money than the goods and services produced. Milton Friedman, who extensively studied the role of the Fed in economic activity and inflation, said: “Inflation is always and everywhere a monetary phenomenon. It is a result of a greater increase in the quantity of money than in the output of goods and services which is available for spending.” The Fed controls what’s called “high-powered money” of various assets on its balance sheet. These assets include mostly Treasury securities from the tens of trillions of dollars in debt issued by the federal government. It also includes mortgage-backed securities, lending to financial institutions, federal agency debt, and other lending facilities. I agree with Cochrane that federal deficits give ammunition to the Fed when it purchases Treasury debt, grows high-powered money, contributes to more money chasing too few goods and services, and results in inflation. But other assets on the Fed’s balance sheet also matter, especially since the Great Financial Crisis in 2008 when the Fed started quantitative easing. Cochrane’s framework overlooks the significant role of monetary policy in influencing inflation expectations and shaping the broader economic environment. While fiscal policy can play a role in determining long-term inflation trends, as the debt distorts interest rates in the market, the Fed’s control of the money supply to target the federal funds rate and influence other rates along the yield curve remains a potent tool for managing expectations. While we should challenge Congress to adopt a fiscal rule for sustainable budgets to relieve excessive spending that drives up the national debt, this does not undermine the source of inflation: the Fed. But if Congress could balance its budget, which hasn’t happened since 2001, it would remove a bullet the Fed could shoot at the economy. In other words, a sustainable fiscal policy, wherein Congress passes balanced budgets by limiting government spending — the ultimate burden of government and the source of budget deficits — would help control inflation. While this could mitigate the assets available for the Fed to add to high-powered money, it would not solve the inflation problem because of many other available assets. Another issue that arises from considering fiscal policy the prime mover of inflation is how it works in practice. Fiscal policy is not directly expansionary or contractionary, as it is just taking funds from some people to give to others, with many of the takers being politicians and bureaucrats in government. These actions move money around in the economy without increasing productive activity that creates goods and services. There are roles for the federal, state, and local governments, but those should be limited to those outlined in constitutions. If Congress would abide by the Constitution, whereby it funded only limited government instead of the bloated federal government today, then fiscal policy would not be so burdensome. Fiscal policy would also not fall into the Keynesian trap of trying to “stabilize economic activity,” as the only thing that governments typically stimulate is more government because of the created failures due to the limited knowledge and rent seeking by politicians and bureaucrats. The underlying problem is usually government failures that cannot be resolved by more government. When Congress returns to its limited, constitutional roles, the federal budget will be drastically cut, resulting in lower taxes and opportunities to pay down and retire the national debt. This would also help reduce the massive distortions throughout the economy from government spending, taxes, and regulations. It would also decrease the Fed’s influence on the economy, but not entirely because of the other assets available for its disposal. The Fed also distorts economic activity through its ability to influence each stage of the production process with the assets on its balance sheet and its effect on interest rates. When the Fed purchases Treasury debt and increases high-powered money, the new money does not go to everyone simultaneously. Instead, the money trickles down from the financial sector to other sectors based on credit availability and other factors, in what is called the Cantillon effect. The manipulation of different markets throughout the production process of goods by the new money and the influence the purchase of assets by the Fed has on interest rates create boom and bust cycles. There is ample evidence about these economic steps, especially from the Austrian business cycle theory. Fiscal policy influences many steps in the production process through subsidies, tax breaks, and regulations, which hinder the voluntary production of individual goods and services through a well-functioning price system. But Congress cannot increase the money supply, which only the Fed can do, nor influence the general price level nor the resulting inflation. All things considered, Cochrane’s comprehensive exploration of fiscal theory and extensive analysis of its implications for the price level riveted me. His methodical dissection of economic concepts and pragmatic approach to examining fiscal policy offered a fresh perspective on economic dynamics. In conclusion, the Fiscal Theory of the Price Level offers a valuable contribution to the ongoing debate surrounding the determinants of inflation and the role of fiscal policy in the economy. While I’m sympathetic to Cochrane’s arguments, it is essential to recognize the importance of a central bank’s monetary policy in causing inflation through its balance sheet. Additionally, we should acknowledge the distortions caused by government policy, whether fiscal or monetary, and recognize the secondary role of fiscal policy compared to monetary policy in addressing inflationary pressures. To ensure sound economic outcomes, it is imperative to establish strong fiscal and monetary rules that provide an institutional framework limiting the burdens of government actions on our lives and livelihoods. Despite my dissent on the emphasis placed on fiscal policy’s role in inflation, the book’s productive discourse on the delicate dynamics of key economic elements make this an important contribution to inflation studies. Today, I am joined by Dr. John B. Taylor, the George P. Shultz Senior Fellow in Economics at the Hoover Institution and the Mary and Robert Raymond Professor of Economics at Stanford University.

Join us as we discuss the economic situation, the performance of monetary and fiscal policies, the importance of policy rules like his famous Taylor rule, and lessons in economic freedom. Without economic freedom and policy rules, we are unlikely to let people prosper. Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. See show notes for this episode on Substack and subscribe to receive it in your inbox: www.vanceginn.substack.com Visit my website for economic insights: www.vanceginn.com In today’s This Week’s Economy episode 52, I discuss the benefits of economics, school choice, spending limits, abundance, vacations, and much more in 8 minutes!

I explain how abundance matters through a limited government that provides more rest and leisure. Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. See show notes for this episode on Substack and subscribe to receive it in your inbox: www.vanceginn.substack.com Visit my website for economic insights: www.vanceginn.com  Originally published at AIER.

Taxing unrealized capital gains on property, stocks, and other assets is not just a bad idea, it’s an economic fallacy that undermines economic growth and personal liberty. Unfortunately, President Biden’s $7.3 trillion budget proposes such a federal tax. Vermont and ten other states have made similar moves. This tax should be rejected, as it is fundamentally unjust, likely unconstitutional, and would hinder prosperity and individual freedom. A tax on unrealized capital gains means that individuals are penalized for owning appreciating assets, regardless of whether they have realized any actual income from selling them. If you purchased a stock for $100 this year, for example, and it increased to $110 next year, you would pay the assigned tax rate on the $10 capital gain. You didn’t sell the asset, so you don’t realize the $10 appreciation, but must pay the tax regardless. The following year, it dropped to $100, so there was a loss of $10. Would you be able to deduct that loss from your tax liability? The devil is in the details of the approach to this tax, but the devil is also in the tax itself. Adam Michel of Cato Institute explained two types of unrealized taxes in President Biden’s latest budget:

Taxing unrealized capital gains contradicts the basic principles of fairness and property rights essential for a free and prosperous society. Taxation, if we’re going to have it on income, should be based on actual income earned, not on paper gains that may never materialize. Moreover, taxing unrealized gains hurts economic activity by discouraging investment and capital formation, the lifeblood of a dynamic economy. When individuals know their unrealized gains will be taxed, they have less incentive to invest in productive assets such as stocks, real estate, or businesses. This leads to a misallocation of resources and slower economic growth. Additionally, this tax reduces the capital available for entrepreneurship and innovation. Start-ups and small businesses often rely on investment from individuals willing to take risks in the hope of eventually earning a return on their investment. By taxing unrealized capital gains, we discourage risk-taking and stifle innovation, essential elements for improving productivity and raising living standards. The tax undermines personal liberty by infringing on individuals’ property rights and financial privacy. It gives the government unprecedented control over people’s assets and creates a powerful disincentive for individuals to save and invest. This is particularly troublesome in an era of increasing government surveillance and intrusion into private affairs. Proponents of taxing unrealized capital gains argue that it is a way to address income inequality and raise revenue for social programs. This argument can’t withstand scrutiny. This tax does little to address the root causes of income inequality, such as government failures in fiscal and monetary policies. Instead, this new tax would merely redistribute wealth from productive individuals to the government, thereby further misallocating hard-earned money. Furthermore, the tax revenue raised from this tax will be far less than proponents anticipate, as individuals will work less, invest less, and find ways to avoid such taxes through legal paths. This would result in less economic prosperity and a resulting decline in tax collections. From an economic and moral perspective, taxing unrealized capital gains from property, stocks, and other assets is a bad idea. It undermines economic growth, stifles innovation, and infringes on personal liberty. Instead of resorting to the misguided policies of the Biden administration and some states, we should remove barriers created by the government. These include reducing spending, taxes, and regulations. We should also impose fiscal and monetary rules. Achieving these goals and ending the bad idea of a new tax on unrealized capital gains will encourage investment, entrepreneurship, and economic opportunity for all. Only then can we truly unleash the potential of a free and prosperous society. Could Colorado become one of the seven states with no income tax? Vance Ginn, former White House Office of Management and Budget, believes the state is on the #Path2Zero.

Originally published at Washington Times.

In President Biden‘s recent State of the Union address, he painted a rosy economic picture, touting what he called “Bidenomics” as the driving force behind what he claims is a robust economy. He pointed to a low unemployment rate, the absence of a recession, and a lower inflation rate as evidence of success. Reality, however, tells a different story. And Mr. Biden’s recently released irresponsible budget sends the federal government and America further toward bankruptcy. Despite the president’s assertions, the economy and inflation remain top concerns for most Americans. The disconnect between the headlines and the lives of ordinary citizens underscores the profound challenges facing the nation’s economic landscape. This sense of malaise can be directly attributed to the flawed principles underlying Bidenomics, as outlined in his latest budget. These include excessive spending, taxation and regulation. Each is destructive, but together, they are catastrophic. The result has been stagflation and less household employment in four of the last five months. There have also been lower inflation-adjusted average weekly earnings by 4.2% since January 2021, when Mr. Biden took office. Rather than fostering economic growth and prosperity, Bidenomics has stifled innovation, investment and job creation. At its core, Bidenomics represents a misguided attempt to address complex economic issues through heavy-handed government intervention. While the administration may tout short-term gains, the long-term consequences of such policies are far-reaching and unaffordable. The reality is that excessive government spending has led to unsustainable levels of debt, burdening future generations with the consequences of fiscal irresponsibility. Similarly, excessive taxation is stifling entrepreneurship and dampening economic activity, limiting opportunities for individuals and businesses alike. Excessive regulation serves only to hamper innovation and drive up costs, exacerbating the challenges facing working families. Unfortunately, Mr. Biden’s latest budget proposal doubles down on these bad policies. Even with rosy assumptions of tax collections being a higher share of economic output over time as the tax hikes will reduce growth and, therefore, lower taxes as a share of gross domestic product, the budget continues massive deficits every year. This will result in higher interest rates, higher inflation, more investment These results have been highlighted in economic theory by economists such as Alberto Alesina and John B. Taylor. Their research has found that raising taxes doesn’t help close budget deficits because of the reduction in growth from higher taxes in a dynamic economy. The way forward should be cutting or at least better-limiting government spending — the ultimate burden of government on taxpayers. Amid these challenges, America also needs a return to optimism and flourishing. This includes leadership that inspires confidence, fosters innovation, and empowers people to pursue their dreams. We need out-of-the-box policies prioritizing economic freedom and individual opportunity, allowing the entrepreneurial spirit to thrive and driving growth and prosperity. More specifically, this means reducing the burden of government intervention through lower spending and taxes, streamlining regulations, and fostering an environment where entrepreneurship can thrive. By embracing fiscal sustainability and making tough choices, we can ensure the long-term stability and prosperity of our nation. In short, while Mr. Biden tries to spin a positive narrative about the economy, the facts speak for themselves. We cannot afford Bidenomics, no matter the headlines, what was touted in the State of the Union address, or the latest budget. The stakes are too high, and the consequences too grave, to ignore the reality of our economic situation. We need leadership that is willing to confront the hard truths and enact policies that prioritize the well-being of all Americans, fostering an environment where optimism and flourishing can thrive. Today, I am joined by Dr. Justin Callais, who is an Assistant Professor of Economics at the University of Louisiana at Lafayette.

Join us as we discuss social mobility in the 50 states, Louisiana’s economic and population challenges, sound economics, and much more. This includes the lack of social mobility in Louisiana from too much government. Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. See show notes for this episode on Substack and subscribe to receive it in your inbox: www.vanceginn.substack.com Visit my website for economic insights: www.vanceginn.com  Originally published at National Review Online.

Few government programs are regularly up for debate as much as the Supplemental Nutrition Assistance Program (SNAP), commonly known as food stamps. The latest controversy is whether the food purchased by its recipients should be restricted to healthier diets that exclude snacks and sodas. While this approach seems reasonable, its tradeoffs necessitate SNAP reforms that balance keeping this costly program temporary for recipients while supporting their agency and choice for long-term self-sufficiency. Enacted in its current form in 1964 as part of President Lyndon B. Johnson’s War on Poverty, SNAP has evolved into one of the nation’s most extensive safety-net programs, assisting more than 42 million Americans at a cost to taxpayers of $113 billion in 2023. With the Farm Bill coming up for reauthorization by Congress on September 30, it’s time to consider improvements for SNAP and other programs in the existing legislation. The Farm Bill has included funding and rules for commodity programs since it was first enacted in the Agricultural Adjustment Act of 1933. But nutrition (primarily through SNAP) is expected to account for 84 percent of the $1.5 trillion spent on programs in the bill over the next decade. The free-market approach to SNAP reform should be rooted in economic freedom and individual empowerment and emphasize the importance of preserving flexibility in food purchases while promoting self-sufficiency and work for recipients. This perspective draws inspiration from the teachings of free-market economists such as Milton Friedman, who championed the idea of individual choice in economic decision-making. Since its inception, SNAP has undergone numerous reforms and expansions, reflecting shifting societal attitudes and economic realities. Originally conceived as a program to provide recipients quick, temporary relief from hunger and malnutrition, SNAP has become a permanent fixture for many people experiencing economic hardship. For example, a household of four — to be eligible, its gross monthly household income must not exceed $3,250 — will receive a maximum monthly allotment of $973 per month. Central to SNAP reform should be the concept of self-sufficiency. SNAP can honor recipients’ dignity and agency as they navigate their way through the challenges posed by poverty by allowing them to make purchases based on their preferences and circumstances, even if that includes snacks or soda. This flexibility respects recipients’ autonomy and acknowledges their capacity to make informed decisions about their dietary needs. This can also help reduce the incentive for recipients to sell SNAP allotments to others and purchase items they prefer more. We should also acknowledge that these food subsidies distort the grocery market. The restrictions on what SNAP recipients can purchase today drive them to specific items such as milk. The artificial boost in demand then drives up the price and sometimes the profit margins for those items, thereby making them more expensive for everyone while lining the pockets of a few suppliers. Because SNAP raises some prices for Americans and adds to the national debt, contributing to higher interest rates and inflation, we need a better-functioning program or we need to end it. In addition to promoting self-sufficiency, a flexible SNAP program should align with work to reduce poverty so recipients use the program temporarily as intended. Rather than imposing top-down restrictions on food choices, as some are trying to do, policy-makers should focus on unleashing opportunities for recipients to improve their circumstances through education, training, and employment. These steps have a proven record of supporting long-term success. Furthermore, a streamlined approach to SNAP administration would improve the program’s effectiveness while minimizing waste and abuse. By reducing bureaucratic hurdles, we could help ensure that the taxpayer dollars that fund the program are used more efficiently to support those in need. As policy-makers contemplate reforms to SNAP with the upcoming Farm Bill renewal, they must recognize the program’s historical context and evolution. Originally conceived as a temporary measure for recipients to address hunger and malnutrition, SNAP has become a permanent, costly safety net for many recipients. By preserving flexibility in food purchases and empowering recipients with more opportunities to work and move out of poverty, we can support individual freedom and decision-making, two fundamental elements of a vibrant and prosperous society. The Farm Bill presents an opportunity to do so through meaningful reforms to SNAP that help strengthen Americans’ resolve to overcome obstacles. The above reforms would make the help provided by SNAP temporary and flexible, and complement it with a pathway to work. There should also be a push to reduce bureaucratic bloat by streamlining the program and arranging for periodic independent efficiency audits by third-party private firms or a state auditor, so that its funds only go to the people they are intended for. Moreover, adhering to more free-market approaches across the economy — with less government spending, lower taxes, and reduced regulation — can provide more opportunities for people to get jobs and move out of poverty forever. This will allow people to flourish rather than being dependent on government programs that discourage self-sufficiency. As we navigate the complexities of food insecurity, let us heed the wisdom of free-market economics and empower recipients to chart their path to a brighter future. In today’s This Week’s Economy episode 51, I discuss the latest hot topics on Super Tuesday, Biden’s SOTU, universal school choice, and much more!

Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. See show notes for this episode on Substack and subscribe to receive it in your inbox: www.vanceginn.substack.com Visit my website for economic insights: www.vanceginn.com  Originally published at Law & Liberty.

The Congressional Budget Office (CBO) just released the February 2024 Budget and Economic Outlook, and projections look grim. This year, net interest cost—the federal government’s interest payments on debt held by the public minus interest income—stands at a staggering $659 billion in 2023 and has recently soared to about $1 trillion. Unless politicians face these facts and restrain spending, Americans can expect rising inflation and painful tax hikes without improvement in public services. Some politicians quickly blamed a lack of tax revenue, calling for repealing the 2017 Trump tax cuts. But how much more money can they take? New IRS data shows that 98% of all income taxes are paid by the top 50% of income earners, those making at least $46,637. Moreover, 35% of Americans feel worse off than 12 months ago and inflation remains the primary concern for those across the income spectrum. So perhaps, rather than taking more money, the government should own up to its mistakes. The massive net interest costs result from bad spending habits, not a lack of revenue. This requires the federal government to adopt strict fiscal and monetary rules to rein in wasteful deficit spending and money printing that fuel higher interest rates and inflation. Net interest cost is the second largest taxpayer expenditure after Social Security and is higher than spending on Medicaid, federal programs for children, income security programs, or veterans’ programs. And it’s expected to grow. The CBO projects net interest to surpass Medicare spending this year and balloon to $1.6 trillion in 2034 as a result of higher debt and higher interest rates. Interest rates on Treasury debt are at the highest since 2007, paying between 4% and 5.5%, and the rates are expected to rise further. As the stockpile of gross federal debt is expected to grow by about $20 trillion to $54 trillion over the next decade, politicians will face an increasing temptation to rely on the Federal Reserve to pay for it by printing money. If the Fed does, the dollar’s value will decline, and Americans will continue to struggle financially. In an ideal world, politicians will organize the budget process to focus on funding a limited government and ensuring Americans keep their hard-earned money. They would also have plans to cut spending during times of economic downturn to reduce tax burdens on families and businesses and avoid the Keynesian fallacies of deficit spending to fill gaps in economic growth. However, America isn’t Shangri-La. As Thomas Sowell poignantly notes, a politician’s first goal is to get elected, the second goal is to get reelected, and the third goal is far behind the first two. So long as there are investors happy to purchase Treasury debt, there will be politicians who are happy to sway voters with generous spending programs financed by public debt. This must end. Instead, Washington should require strong institutional constraints with a spending limit. The limit should cover the entire budget and hold any budget growth to a maximum rate of population growth plus inflation. This growth limit represents the average taxpayer’s ability to pay for spending. Following this limit from 2004 to 2023 would have resulted in a $700 billion debt increase instead of the actual increase of $20 trillion. Such a policy has been in effect in Colorado since 1992. It is the Taxpayer’s Bill of Rights (TABOR) amendment to the Colorado Constitution. TABOR has revenue and expenditure limitations that apply to state and local governments. The revenue limitation applies to all tax revenue, prevents new taxes and fees, and must be overridden by popular vote. Expenditures are limited to revenue from the previous year plus the rate of population growth plus inflation. Any revenue above this limitation must be refunded with interest to Colorado citizens. A spending cap like TABOR is necessary but not sufficient to solve the problem because politicians in Washington can still pressure the Federal Reserve to pay for the increased debt by printing money. Therefore, it must be combined with a monetary rule to force fiscal sustainability while requiring sound money with fewer distortions in the economy. Monetary rules can come in many forms. While no rule is perfect, research shows that a rule-based monetary policy can result in greater stability and predictability in money growth than the current policy of “Constrained Discretion” whereby the Fed follows rules during “normal times” and has discretion during “extraordinary times.” Whether we are in ordinary or extraordinary times is up to policymakers, who typically don’t want to “let a good crisis go to waste,” as they say. Milton Friedman advocated for a money growth rate rule, the “k-percent rule.” This rule states that the central bank should print money at a constant rate (k-percent) every year. A variation of this rule was used by Fed Chair Paul Volcker in the late 1970s and early 1980s to tackle the Great Inflation with much success. Unfortunately, the Fed had already done too much damage with excessive money growth before then, so the cuts to the Fed’s balance sheet contributed to soaring interest rates that forced destructive corrections in the economy, resulting in a double-dip recession in the early 1980s. This led to the Fed abandoning money growth targeting in October 1982. It is important to note, though, that this “monetarist experiment” was not bound to any law, constitutional or statutory. During that time, the Fed still operated under discretion, which is why it was able to abandon the monetary growth rule just a few years after it had begun, unfortunately. There are other rules that could be applied. John Taylor proposed what’s been coined the Taylor Rule, which estimates what the federal funds rate target, which is the lending rate between banks, should be based on the natural rate of interest, economic output from its potential, and inflation from target inflation. Scott Sumner most recently popularized nominal GDP targeting, which uses the equation of exchange to allow the money supply times the velocity of money to equal nominal GDP. It has different variations, but the key is that velocity changes over time, so the money supply should change based on money demand to achieve a nominal GDP level or growth rate over time. By focusing on a rules-based approach to spending and monetary policy, Americans do not have to worry about electing the perfect candidate every election. Proper constraints will nudge even the worst politicians to make fiscally responsible choices and reduce net interest costs. Furthermore, America will be better positioned to respond to crises at home and abroad. If Congress wants to see who is to blame for the grim CBO projections, they should look in the mirror. Stop looking to take hard-earned money away from Americans and focus on sound budget and monetary reforms now. Today, I am joined by the Center for Freedom and Prosperity’s President Dr. Dan Mitchell. Join us as we discuss Biden’s hype about junk fees, excessive spending crisis, and much more.

Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. Subscribe and see show notes for this episode on Substack - www.vanceginn.substack.com Visit my website for economic insights - www.vanceginn.com In today’s This Week’s Economy episode 50, I discuss the latest hot topics on Big Tech, fiscal commission, sustainable budgets, Texas spending, school choice, and much more!

Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. Subscribe and see show notes for this episode on Substack - www.vanceginn.substack.com Visit my website for economic insights - www.vanceginn.com |

Vance Ginn, Ph.D.

|

RSS Feed

RSS Feed

Proudly powered by Weebly