Originally published at American Institute for Economic Research.

The Economist recently compared Joe Biden’s and Donald Trump’s economic records, concluding Biden wins so far. While the article raises valid points, it excludes key details that make the findings questionable. Ten months from now, there’s a high likelihood Biden and Trump could go head-to-head again for the presidency, especially after the results from the Iowa caucus. But voters should be informed about the effects of their policies on key issues like immigration, inflation, and wages. Starting with a divisive bang, let’s look at each leader’s track record concerning immigration. The Economist correctly noted that apprehensions along the southern border were much lower under Trump. They increased by the most in 12 years during the economic expansion of 2019, decreased early in the COVID-19 pandemic when people could be turned away for public health concerns, and rose again during the lockdowns. While some may see apprehensions rising between Trump and Biden as a loss for Biden, I see it as a loss for both. This metric is somewhat unreliable, given one person can be caught and counted multiple times, and those caught are a subset of total migrants. The truth is immigration is good for the economy, but government failures create unnecessarily complex barriers against legal immigration, contributing to the humanitarian crisis along the Mexico border today. Neither President has pushed for what’s needed (market-based immigration reforms) both lose. Inflation is another hot topic, especially for Biden. The Economist hands the win to Trump, as inflation was far lower during his presidency. But can we give him the credit? Remember, Trump pressured the Federal Reserve to reduce its interest rate target and expand its balance sheet, which was inflationary. His deficit spending skyrocketed during the lockdowns and was mostly monetized by the Federal Reserve, contributing to what was always going to be persistent inflation. Biden made this deficit spending and resulting inflation much worse. Add in the Fed’s many questionable decisions, such as doubling its assets, cutting and maintaining a zero interest rate target for too long, and focusing too much on woke nonsense, and we can see how this was always going to be persistent inflation. But even the Fed’s latest projections indicate it won’t hit its average inflation target of two percent until at least 2026. Likely, it will cut the current federal funds rate target range of 5.25 percent to 5.5 percent three times this year, keep a bloated balance sheet to finance massive budget deficits, and run record losses. If so, this inflation projection is too rosy. Some of Trump’s policies helped stabilize prices, including his tax and regulation reductions. But he still allowed egregious spending. Biden has doubled down on red ink that has contributed to the recent 40-year-high inflation rate. While inflation has been moderating recently under Biden, Trump gets the win. Of course, neither Presidents nor Congress control inflation, as that job is the Fed’s, but its fiscal policies influence it. When it comes to inflation-adjusted wages, The Economist grants a tie. Let’s consider real average weekly earnings that include hourly earnings and hours worked per week, adjusted for the chained consumer price index, which adjusts for the substitution bias and has been used for indexing federal tax brackets since the Tax Cuts and Jobs Act of 2017. Trump’s era witnessed a robust upward trajectory of real earnings, with considerable gains by lower-income earners, thereby reducing income inequality. We must acknowledge a real wage spike in 2020 during Trump’s lockdowns, marked by the loss of 22 million jobs and various challenges. To maintain a fair analysis, I disregard this spike. A year later, real wages demonstrated a decline under Biden. Extending the timeframe to two years later, real wages remain relatively flat to slightly increased. To provide a contextual understanding, when we consider the trend under Trump, excluding the 2020 spike, real wages for all private workers or production and nonsupervisory workers fall below those observed during Biden. It’s worth noting, however, that these wages have been higher since 2019, albeit nearly stagnant for all private workers. Given real earnings, I agree with The Economist that Trump and Biden are tied. While much more can be said for each President’s policies, continuing to add context when making assessments is crucial. I give Trump a nuanced “win” overall because his policies supported more flourishing during his first three years until the terrible mistake of the COVID lockdowns, with its huge, long-term costs. I should note that I made a strong case inside the White House for no shutdowns and less government spending but, alas, my efforts, and those by others, lost to Fauci, Birx, and Trump. Given the improved purchasing power during his presidency, Trump receives better poll ratings than Biden after three years of their presidencies. But this win doesn’t mean that Trump’s record is best regarding these issues, protectionism, and more. Let’s hope free-market capitalism, the best path to let people prosper, is on display this November, no matter who is on the ballot.

0 Comments

This Week's Economy Ep. 14 | Inflation is Americans’ Top Concern, State Jobs Report, & Minimum Wage6/23/2023 Thank you for reading the Let People Prosper newsletter, which today includes the 12th episode of "This Week's Economy,” where I briefly share insights every Friday on key economic and policy news across the country. Today, I cover: 1) National: New Pew Research poll reveals that inflation is the top concern for Americans on both sides of the political aisle, Fed needs to do more, and financial markets remain loose; 2) States: New state-level jobs report and which states are leading and breakdown of the largest spending increase in Texas history and why it's not good for keeping the Texas Model strong; and 3) Other: The importance of educating young audiences on capitalism and socialism and my experience teaching with a "minimum wage" game to a group of high school students. You can watch this episode and others along with my Let People Prosper Show on YouTube or listen to it on Apple Podcast, Spotify, Google Podcast, or Anchor. Please share, subscribe, like, and leave a 5-star rating!

For show notes, thoughtful insights, media interviews, speeches, blog posts, research, and more, check out my website (https://www.vanceginn.com/) and please subscribe to my newsletter (www.vanceginn.substack.com), share this post, and leave a comment. Today, I'm honored to be joined by Leslie Ford, adjunct fellow at the American Enterprise Institute’s Center on Opportunity and Social Mobility and a senior fellow with the Alliance for Opportunity. We discuss: 1) The history of the war on poverty, how safety net programs have evolved, and where the war on poverty stands today; 2) How safety net programs can discourage upward mobility and keep people trapped in poverty through penalties such as those on marriage; and 3) Data on what requirements help safety net recipients achieve long-lasting self-sufficiency and prosperity, and more. You can watch this interview on YouTube or listen to it on Apple Podcast, Spotify, Google Podcast, or Anchor. Please share on social media, subscribe to your favorite platform and my newsletter, like it, and leave a 5-star rating.

Find show notes, thoughtful economic insights, media interviews, speeches, blog posts, research, and more at my website and here in my Substack newsletter. Please subscribe to this newsletter, share it with your friends and family, and leave me a comment.  On Wednesday night, the House passed what could be one of the worst debt ceiling deals in U.S. history, as it doesn’t provide the fiscal responsibility needed for suffering Americans.

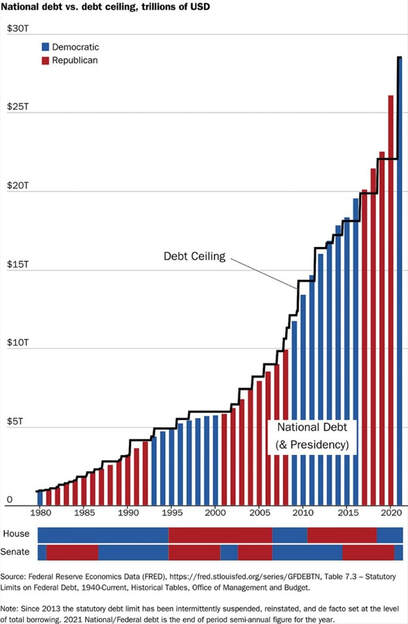

In fact, this deal perpetuates most of the same reckless policies that have contributed to stagflation, leaving Americans struggling financially. Despite what appears to be a relatively strong labor market, wages have failed to keep pace with inflation on an annual basis for more than two years. Homeownership has become unattainable for many, and higher prices have forced over half of the adult population to reduce their savings. You would think that such widespread suffering would motivate Congress to reform its fiscal insanity, but apparently, that’s not the case. While 49 out of 50 states have a balanced budget amendment and most have a spending limit, there are no such rules at the federal level. The debt ceiling is the only mechanism, other than elections, that we have to keep Congress’ spending in check. By suspending the debt ceiling, we’re inviting more reckless spending, which is why our national debt has skyrocketed to a ridiculous amount of more than $31 trillion. The net interest on the debt alone will soon surpass $1 trillion. The new debt ceiling bill allows politicians to kick the can further down the road of payment for the debt to our children and grandchildren to deal with later. By raising the debt ceiling for another two years and only imposing a one percent annual spending limit next year, there’s ample room for the debt and spending to continue to grow at an already bloated budget. A more reasonable timeframe for suspending the limit would have been two months, giving Republicans and Democrats the opportunity to pursue essential spending restraint. Irresponsible spending is a bipartisan problem, but Republicans, with their majority in the House and a platform of fiscal conservatism, bear even greater responsibility to address this issue. Two years is an extensive period considering the adverse effects of the current national debt on inflation, interest rates, the U.S. dollar’s status, and the result of exacerbating the daily struggle of Americans to make ends meet, let alone pursue the largely destroyed American Dream. Some argue that Congress should budget like a family. However, they should budget even more conservatively as Congress is entrusted with the hard-earned tax dollars of the public, not their own. Unleashing spending on out-of-control war efforts with the lack of major reforms and cuts where needed in the budget when our country teeters on the brink of financial crisis doesn’t promote individual liberty or economic growth. In the meantime, fiscal conservatives in Congress should continue advocating for a spending limit rule such as seen in the states to put an end to this crisis. A responsible budget that grows, if it grows at all, by less than the rate of population growth plus inflation, which represents the average taxpayer’s ability to afford spending, would be a great goal. Without substantial spending restraint, Americans can expect more suffering. As economist Milton Friedman once said, the ultimate burden of government is not how much it taxes but how much it spends. This debt ceiling bill was an opportunity to help reduce this burden, and we lost that. Originally published by the Daily Caller. What REALLY Happens in the White House, Need Tax & Spending Reforms & More w Paul Winfree | Ep. 455/23/2023 Today, I'm honored to be joined by economist and trusted public policy adviser Paul Winfree, who has served in top management and policy roles in the White House, U.S. Senate, and think tanks. We discuss:

Paul Winfree is an economist and a trusted public policy advisor. He has served in top management and policy roles in the White House, the US Senate, and in think tanks.

TRUTH On Inflation, Housing Market, Interest Rates, & Incentives w. Dr. Chuck Beauchamp | Ep. 445/16/2023 In today's new episode of the "Let People Prosper" podcast, I'm thankful to be joined by Dr. Chuck Beauchamp for a thought-provoking discussion on new inflation numbers and the current economy. We discuss: 1) The newest inflation numbers and how the rate is impacting various markets including food, housing, and energy; 2) Interest rates' impact on the housing market and the crisis of affordability; and 3) Why the U.S. dollar's status could continue to wane and more. You can watch this interview on YouTube or listen to it on Apple Podcast, Spotify, Google Podcast, or Anchor (please share, subscribe, like, and leave a 5-star rating). Chuck’s bio:

Find show notes, thoughtful economic insights, media interviews, speeches, blog posts, research, and more here at my website (https://www.vanceginn.com/) or Substack newsletter (https://vanceginn.substack.com). Please subscribe to the newsletter, share it with your friends and family, and leave me a comment.  The U.S. dollar will likely soon lose its status as the global reserve currency. The dollar’s global reserve dominance has declined in recent years. As a result, international trade partners are hedging new connections. This will restructure the global economic order and create challenges ahead, especially for middle-class Americans.

Americans should know what’s happening and how they can prepare for this possibility. But first, what does it mean to be the world’s global reserve currency, and why does it matter? The U.S. Dollar is the dominant global reserve currency. It’s widely accepted and is the preferred medium of exchange for international transactions. The dollar has enjoyed this status for the past 80 years due to its strong reputation acquired across a long history of America’s rising military prowess, fulfilling its financial obligations, and maintaining a strong economy. These institutional foundations of the dollar created high demand among foreign entities. One of the most important transactions utilizing the dollar is the purchase of oil. Oil is currently priced in dollars globally and other dollar-denominated assets. Losing or weakening the dollar’s position and value results in higher oil prices. The dollar’s elevated demand has helped keep its value high relative to other currencies. This prompted many countries to tie their currency directly to our dollar. The U.S. benefited by leveraging foreign demand for dollars into loans to the U.S. federal government. Foreign investors lend the U.S. high volumes of money because of the debt’s dollar denomination. The higher demand for U.S. Treasury securities pushes down domestic interest rates. This influences lower rates on mortgages and business loans, which help provide increased investment and economic growth. Losing or weakening the dollar’s reserve position will result in increased interest rates, decreased investment, and weak to negative economic growth. The dollar’s reserve status has also meant an increased volume of international trade. Ultimately, international trade helps keep interest rates and inflation moderately low. Losing or weakening the dollar’s reserve position will result in increased inflation. Trouble for the dollar is on the horizon. The once-givens about the dollar have come into question recently due prominently to excessive deficit spending. Foreign investors are reducing their demand for dollars as they diversify their portfolios. This combination contributed to the ballooning of the debt, depreciated the dollar, led to higher inflation and falling year-over-year real average weekly earnings for 25 straight months, and drove up interest rates, thereby slowing economic activity. Of course, this will have tradeoffs and many of them won’t be good. As mentioned, the major tradeoffs will be higher inflation and interest rates. The latter will trigger a move by the Federal Reserve to attempt to lower interest rates. But if its target rate is held below what markets dictate, the Fed will monetize the debt, increase the money supply, and drive inflation higher. The long-term result will be even higher interest rates to tame inflation. Unfortunately, the consequences of higher interest rates and inflation would be severe. People should expect higher mortgage rates than the already rising average rate of 6.4%. This is the highest in 15 years. Ultimately, higher interest rates would result in a steeper contraction in the housing market, exacerbate economic weakness, increase job losses, and worsen poverty. But maybe more importantly, it would likely crush middle-class Americans and the lifestyle that they’ve been accustomed to having for decades. The higher cost of shelter, food, gasoline, and energy as the dollar loses its reserve currency status would wreck havoc on their budgets and force major decisions about what’s best for their families. This could mean having to put off saving for college, going on vacations, and living in much smaller homes. All because our government couldn’t spend our money wisely. Therefore, the government should take serious steps to restore confidence in the dollar before a bad situation for Americans becomes worse or irreconcilable. To start, the federal government should reduce deficit spending. The long-term goal should be a balanced budget and an eventual start to paying down the debt. This will be pro-growth as the government stops redistributing taxpayer money from productive to unproductive activities. It will also strengthen the fiscal and economic situation of the U.S. The result will be an improvement in foreigners’ outlook on the dollar that would help preserve the dollar’s status. Dollar-focused policies should be tied to reducing the money in circulation. This should occur as the Federal Reserve reduces its balance sheet. Doing so tames inflationary pressures and could even result in some disinflation. This would allow the hard-earned dollars of Americans to go further than they do today. These policy improvements should be put into law with fiscal and monetary policy rules. The rules should remove the discretion of big-government spenders and printers. This would enable people’s livelihoods to get back on track and improve for generations. The potential loss of the dollar’s reserve currency status could have significant economic consequences, and there are even more than highlighted here. There is, however, reason for optimism: The U.S. economy is resilient and adapts well to challenges. But will those in D.C. allow for that to happen in the dynamic marketplace? Time will tell. But let’s hope so before it’s too late for middle-class Americans and everyone else to have the opportunity to fulfill their hopes and dreams. Originally published at The Daily Caller with Chuck Beauchamp, Ph.D. This Week's Economy Ep. 8 | TRUTH On Inflation, U.S. Dollar, Debt Ceiling, Texas & Louisiana Policy5/12/2023 Thank you for checking out the 8th episode of "This Week's Economy,” where I briefly share insights every Friday on key economic and policy news across the country. Subscribe to receive new posts and support my work. Today I cover:

1) National: Breaking down the latest report on CPI inflation and how it relates to real average weekly earnings, what’s going on with the debt ceiling debate, and why the Fed should continue to raise its interest rate target and cut its balance sheet; 2) States: ALEC's newest "Rich States, Poor States" report findings related to where Texas stands in comparison with Utah and Florida, what the legislatures are doing late in the sessions of Texas (here), Louisiana (LA jobs report and tax relief), and elsewhere; and 3) Other: New findings on the importance of work-life balance, the value of the U.S. dollar, and more. You can watch this episode and others along with my Let People Prosper Show on YouTube or listen to it on Apple Podcast, Spotify, Google Podcast, or Anchor (please share, subscribe, like, and leave a 5-star rating!). For show notes, thoughtful insights, media interviews, speeches, blog posts, research, and more, continue to check out my website (https://www.vanceginn.com/) and please subscribe to my Substack newsletter (https://vanceginn.substack.com). Research: The Inflation Reduction Act's Costly New Tax Credits for Electric Vehicle Batteries4/10/2023  Executive Summary The U.S. Congress passed and President Biden signed into law the so-called “Inflation Reduction Act” (IRA) in August 2022. The IRA includes many provisions which are now estimated to cost $1.2 trillion over a decade per Goldman Sachs’ more recent analysis compared with the Congressional Budget Office’s (CBO) initial estimate of $391 billion. Part of this substantially higher estimated cost is because of the new cost estimates for tax credits for electric vehicle (EV) battery cells and modules manufactured in the U.S. Instead of the initially estimated cost of $30.6 billion by the CBO, new estimates based on more precise projections and growth in the EV market indicate that this could be as high as $196.5 billion (540% higher than initially estimated) per the Mercatus Center and Goldman Sachs. This higher estimate appears more accurate than the original CBO estimate given the large increase in the EV market and the expanding use of these tax credits. Given that the cost of these subsidies passed by Congress and communicated to the public appears to be substantially undervalued, the CBO and other nonpartisan agencies and committees responsible for providing Congress with accurate revenue estimates and sound economic analysis should reexamine their calculations. Originally published at Americans for Tax Reform.  Both Republicans and Democrats at the national level have put us down a path of slow growth, massive deficits, and high inflation. With a new Republican majority in the U.S. House and the daunting debt ceiling fight over the bloated $31.4 trillion national debt almost exclusively due to excessive spending, there’s a proven pro-growth, pro-liberty path.

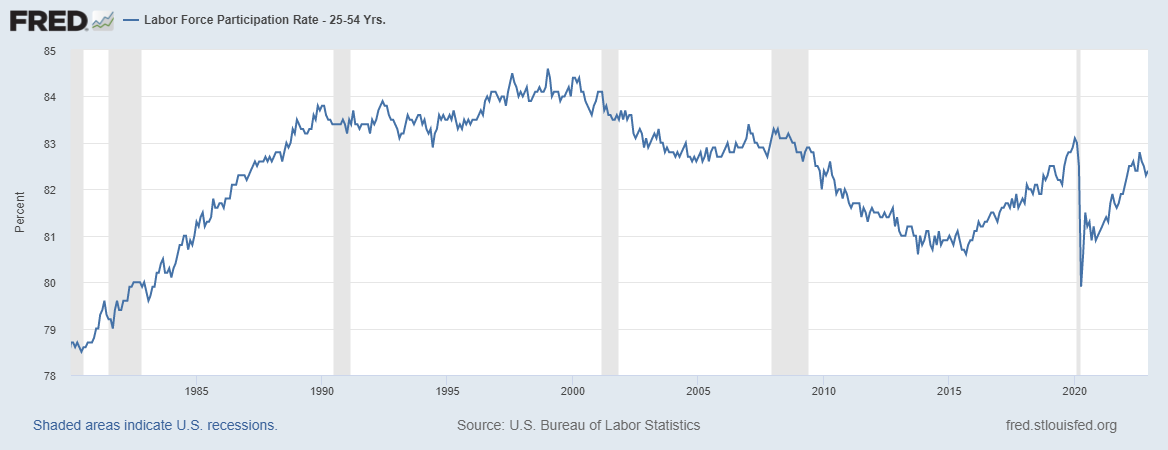

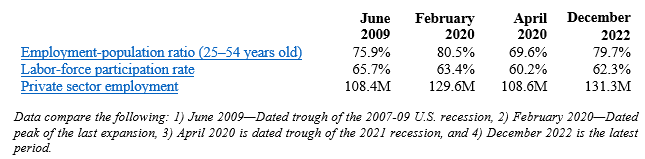

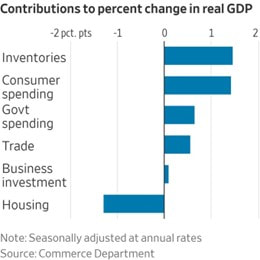

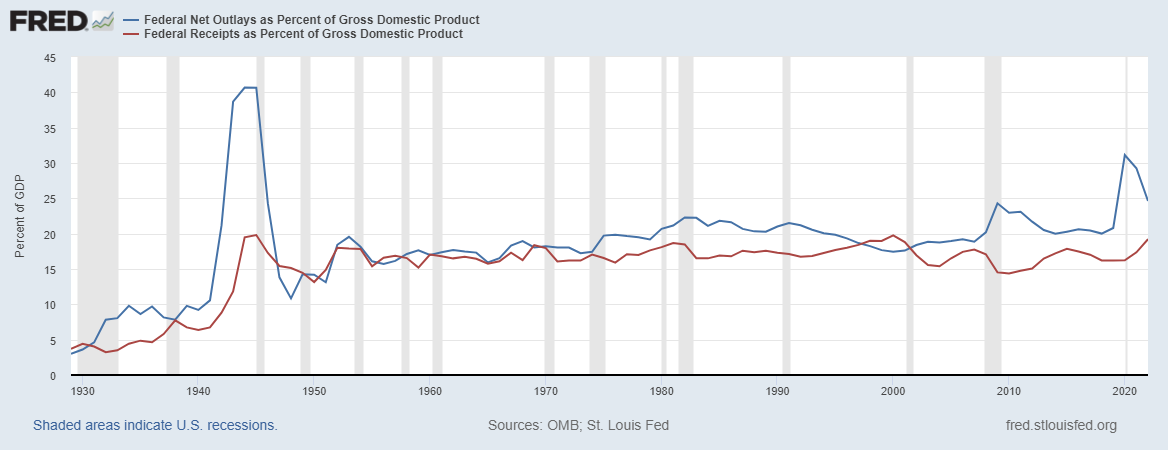

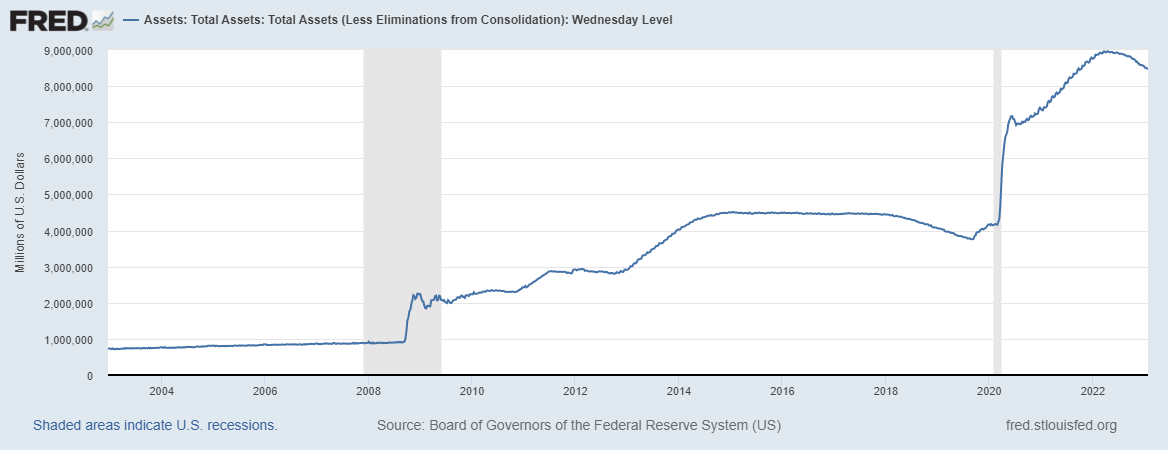

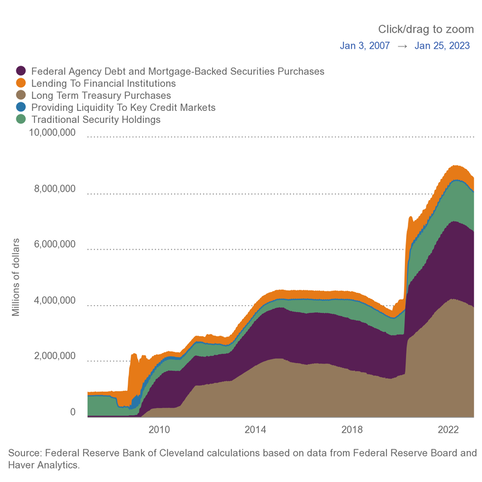

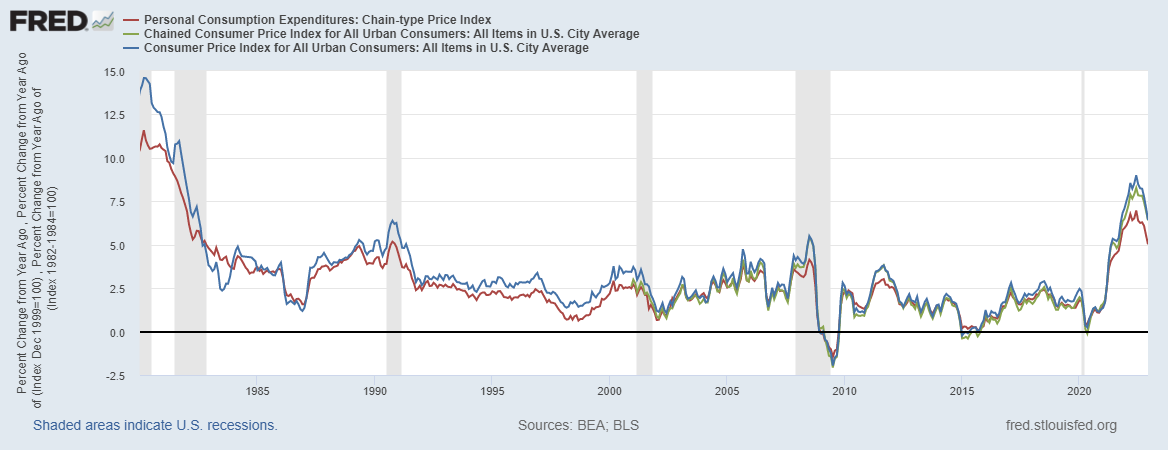

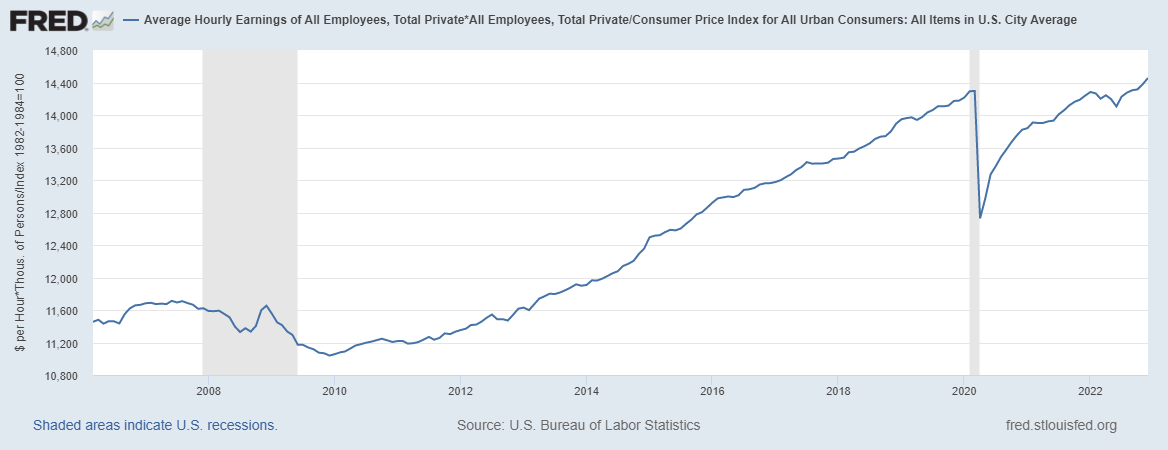

In 2022, the U.S. had real GDP growth of just 0.9 percent (Q4-over-Q4), the highest inflation in 40 years, the highest mortgage rates in 20 years, and the worst stock market in 14 years. Average real weekly earnings have now declined year-over-year for 22 straight months. Fortunately, history is a good guide for how to overcome this mess. The two of us have served as chief economists at the Office of Management and Budget (OMB), though 50 years apart. One of us (Arthur Laffer, originator of the “Laffer Curve”) was the first chief economist of the OMB in the Nixon White House. The other (Vance Ginn) was the last associate director for economic policy at the OMB in the Trump White House. While much has changed since the OMB was formed in 1970, the problems are basically the same today. There remains a lot of unjustifiable government spending, prosperity-killing taxes, unwarranted regulations, excessive liquidity, and harmful interference in international trade. But just because counterproductive economic policies have been around for a long time doesn’t mean we shouldn’t try for a better world. Each of the above areas is the subject of intense debate. In politics, these debates have their short-term winners and losers as judged by elections. But the principles of economics aren’t determined by votes. The remedy for economic malaise has been and is less government, not more. Free-market, pro-growth policies are the cure. The legacy of the 1970s is now called the era of stagflation, and the 2020s are shaping up to be known for the same, or worse. Even with 50 years of experience, many people still haven’t learned a lesson. During the Nixon and Ford administrations, the economy was stifled at every turn. The dollar was taken off gold and devalued, resulting in higher inflation. Then there was the imposition of wage and price controls, which did nothing to stop inflation but instead ravaged the economy. Government spending was out of control. Taxes were raised, and tariffs imposed, including a 10 percent import tax surcharge; such was the wisdom of the D.C. crowd. The consequences were rising inflation, stock market collapse, impeachment, and a weak economy. Then, President Jimmy Carter tried to do more of the same with the same consequences. There followed a true renaissance, led by President Ronald Reagan’s tax and regulatory cuts and Federal Reserve Chairman Paul Volcker’s sound monetary policy. Inflation crashed, the stock market soared, new jobs surged, and Reagan won re-election in a landslide, winning 49 states. And then there was the sad interlude of George H.W. Bush, who broke his promise by raising taxes, leading to a one-term presidency. President Bill Clinton, partnering as he did with House Speaker Newt Gingrich, cut government spending by 3 percentage points of GDP, cut capital gains tax rates while exempting owner-occupied homes from this tax altogether, and finally, he and the Republicans pushed the North American Free Trade Agreement (NAFTA) through Congress. On the bad side, he raised the top two tax rates. But the spending restraint contributed to a budget surplus for four straight years. President George W. Bush, with a penchant for spending more and for temporary tax cuts, was followed by President Barack Obama, with a desire on steroids to spend even more, plus he nationalized health care. Stagnation took hold, and prosperity faded. In his first two years, President Trump reversed some of the prior 16 years of bad policy with substantial tax cuts, historic deregulation, and other measures that helped get government out of the way, contributing to the lowest poverty rate and the highest real median household income on record. But with the onset of the pandemic, prosperity was cut short by the ill-advised massive spending increases and lockdowns. Today, we’re once again mired in a sea of bad policies and bad consequences despite President Joe Biden’s self-serving narrative. With tax hikes, massive spending, oppressive energy regulations, soaring debt levels, trade protectionism, and a bloated Fed balance sheet, stagflation was given a brand-new lease on life. We should follow the proven, pro-growth path (not currently taken) of sound money, minimal regulations, free trade, flat taxes, and most of all, spending restraint for the sake of the economy and human flourishing. It’s also great politics. With this elixir in hand, it would be springtime again in America. And that is something Americans can believe in. Vance Ginn, Ph.D., is an economist and senior fellow at Young Americans for Liberty and previously served as the associate director for economic policy of the White House’s Office of Management and Budget from 2019 to 2020. Arthur Laffer, Ph.D., is an economist from Nashville, Tennessee, and was the first chief economist of the White House’s Office of Management and Budget. Originally published at The Federalist. Key Point: Americans are suffering under big-government policies as average weekly earnings adjusted for inflation are down for 21 straight months. It's time for pro-growth policies to unleash economic potential to let people prosper.  Overview: The irresponsible “shutdown recession” and subsequent government failures have led to a longer, deeper recession with high inflation that are having persistent consequences for many Americans’ livelihoods. This includes excessive federal spending redistributing scarce private sector resources with deficit spending of more than $7 trillion since January 2020 to reach the new high of $31.4 trillion in national debt—about $95,000 owed per American or $250,000 owed per taxpayer. This new debt has hit its limit and needs to be addressed with spending restraint as the Federal Reserve monetized most of the new debt, leading to a 40-year-high inflation rates. The failed policies of the Biden administration, Congress, and the Fed must be replaced with a liberty-preserving, free-market, pro-growth approach by the new majority by House Republicans so there are more opportunities to let people prosper.  Labor Market: The U.S. Bureau of Labor Statistics recently released the U.S. jobs report for December 2022. The BLS’s establishment report shows there were 223,000 net nonfarm jobs added last month, with 220,000 added in the private sector. Interestingly, while there have appeared to be a relatively robust number of jobs created, a recent report by the Philadelphia Fed find that if you add up the jobs added in states in Q2:2022 there were just 10,500 net new jobs rather than more than 1 million initially estimated. This further indicates that the recession started in (likely) March 2022 (more on this below). That expected revision to the establishment report supports the weak data in the BLS’s household survey, which employment increased by 717,000 jobs last month but had declined in four of the last nine months for a total increase of 916,000 jobs since March 2022. This number of net jobs added since then is much lower than the report 2.9 million payroll jobs in the establishment. The official U3 unemployment rate declined slightly to 3.5%, but challenges remain, including: 3.1% decline in average weekly earnings (inflation-adjusted) over the last year, 0.4-percentage point lower prime-age (25–54 years old) employment-population ratio than in February 2020, 0.6-percentage point below prime-age labor force participation rate, and 1.0-percentage-point lower total labor-force participation rate with millions of people out of the labor force.   These data support my warnings for months of stagflation, recession, and a “zombie economy.” This includes “zombie labor” as many workers are sitting on the sidelines and others are “quiet quitting” while there’s a declining number of unfilled jobs than unemployed people to 4.5 million And that demand for labor is likely inflated from many “zombie firms,” which run on debt and could make up at least 20% of the stock market and will likely lay off workers with rising debt costs. Economic Growth: The U.S. Bureau of Economic Analysis’ released economic output data for Q4:2022. The following provides data for real total gross domestic product (GDP), measured in chained 2012 dollars, and real private GDP, which excludes government consumption expenditures and gross investment.  The shutdown recession in 2020 had GDP contract at historic annualized rates because of individual responses and government-imposed shutdowns related to the COVID-19 pandemic. Economic activity has had booms and busts thereafter because of inappropriately imposed government COVID-related restrictions in response to the pandemic and poor fiscal policies that severely hurt people’s ability to exchange and work. Since 2021, the growth in nominal total GDP, measured in current dollars, was dominated by inflation, which distorts economic activity. The GDP implicit price deflator was +6.1% for Q4-over-Q4 2021, representing half of the +12.2% increase in nominal total GDP. This inflation measure was +9.1% in Q2:2022—the highest since Q1:1981—for a +8.5% increase in nominal total GDP that quarter. This made two consecutive declines in real total (and private) GDP, providing a criterion to date recessions every time since at least 1950. In Q3:2022, nominal total GDP was +7.6% and GDP inflation was +4.4% for the +3.2% increase in real total GDP. But if inflation had been as high as it was in the prior two quarters or had the contribution of net exports of goods and services (driven by natural gas exports to Europe) not been 2.9%, real total GDP would have either declined or been essentially flat for a third straight quarter. In Q4:2022, there was a similar story of weaknesses as nominal total GDP was +6.4% and GDP inflation was +3.5% for the +2.9% increase in real total GDP. But if you consider the +2.9% real total GDP growth was driven by contributions of volatile inventories (+1.5pp), government spending (+0.6pp), and next exports (+0.6pp) which total +2.7pp, the actual growth is quite tepid. For all of 2022, real total GDP growth is reported +2.1% year-over-year but measured by Q4-over-Q4 the growth rate was only +0.96%, which was the slowest Q4-over-Q4 growth for a year since 2009 (last part of Great Recession).  The Atlanta Fed’s early GDPNow projection on January 27, 2023 for real total GDP growth in Q1:2023 was +0.7% based on the latest data available. The table above also shows the last expansion from June 2009 to February 2020. The earlier part of the expansion had slower real total GDP growth but had faster real private GDP growth. A reason for this difference is higher deficit-spending in the latter period, contributing to crowding-out of the productive private sector. Congress’ excessive spending thereafter led to a massive increase in the national debt that would have led to higher market interest rates. This is yet another example of how there is always an excessive government spending problem as noted in the following figure with federal spending and tax receipts as a share of GDP.  But the Fed monetized much of it to keep rates artificially lower thereby creating higher inflation as there has been too much money chasing too few goods and services as production has been overregulated and overtaxed and workers have been given too many handouts. The Fed’s balance sheet exploded from about $4 trillion, when it was already bloated after the Great Recession, to nearly $9 trillion and is down only about 6% since the record high in April 2022. The Fed will need to cut its balance sheet (see first figure below with total assets over time) more aggressively if it is to stop manipulating so many markets (see second figure with types of assets on its balance sheet) and persistently tame inflation.   The resulting inflation measured by the consumer price index (CPI) has cooled some from the peak of 9.1% in June 2022 but remains hot at 6.5% in December 2022 over the last year, which remains at a 40-year high (highest since June 1982) along with other key measures of inflation (see figure below). After adjusting total earnings in the private sector for CPI inflation, real total earnings are up by only 1.1% since February 2020 as the shutdown recession took a huge hit on total earnings and then higher inflation hindered increased purchasing power.   Just as inflation is always and everywhere a monetary phenomenon, high deficits and taxes are always and everywhere a spending problem. The figure below (h/t David Boaz at Cato Institute) shows how this problem is from both Republicans and Democrats.  As the federal debt far exceeds U.S. GDP, and President Biden proposed an irresponsible FY23 budget and Congress never passed one until the ridiculous $1.7 trillion omnibus in December, America needs a fiscal rule like the Responsible American Budget (RAB) with a maximum spending limit based on population growth plus inflation. If Congress had followed this approach from 2002 to 2021, the (updated) $17.7 trillion national debt increase would instead have been a $1.1 trillion decrease (i.e., surplus) for a $18.8 trillion swing to the positive that would have reduced the cost to Americans. The Republican Study Committee recently noted the strength of this type of fiscal rule in its FY 2023 “Blueprint to Save America.” And the Federal Reserve should follow a monetary rule.

Bottom Line: Americans are struggling from bad policies out of D.C., which have resulted in a recession with high inflation. Instead of passing massive spending bills, like passage of the “Inflation Reduction Act” that will result in higher taxes, more inflation, and deeper recession, the path forward should include pro-growth policies. These policies ought to be similar to those that supported historic prosperity from 2017 to 2019 that get government out of the way rather than the progressive policies of more spending, regulating, and taxing. The time is now for limited government with sound fiscal and monetary policy that provides more opportunities for people to work and have more paths out of poverty. Recommendations:

Social Security is on the verge of a funding crisis, and there's renewed debate about how to fix it.

Members of Congress are proposing several ways to shore up social security. It's top of mind for many after a December report by the Congressional Budget Office that says two trust funds used to pay for Social Security will be depleted by 2033. Some say the solution is simple: change the date on which excess reserves are invested, thus saving the program money. Economist Vance Ginn says that might help, but it won't fix the bigger problem. “There’s a lot more payments going out compared to the amount of benefits or taxes or interests that’s being put into the trust fund,” Ginn explained. Some Democrats have proposed raising taxes on the rich to fund Social Security. While Republicans, like Representative Rick Allen of Georgia, have proposed raising the age of retirement. Originally posted at KTRH News in Houston, Texas.  America is in the midst of an identity crisis, and it’s probably not the kind you’d think. Our nation is wrecked by an abysmal economy and unhappy people losing confidence in their country. In such unhappiness, people on both sides of the political aisle too often propose “solutions” that grant the government more control of our lives, even though that control is usually the source of the problem.

The American experiment has paved the way for millions to escape poverty and build a better life via a free-market system with a constitutional republic that encourages innovation and results in more human flourishing than ever before. We need to get back to those roots. I had the opportunity to discuss this phenomenon with Dr. Samuel Gregg, author of the book The Next American Economy and distinguished fellow at the American Institute for Economic Research, who said this country’s founding values are based on “liberty and personal responsibility.” What set America apart was a vision for commoners to determine their own future, and we continue to rank as the most entrepreneurial country in the world. American’s earliest ideals demanded liberty and responsibility, rejecting directives from a distant King. As a result, the roles of the federal and state governments were carefully managed by a system of federalism, with checks and balances to restrain overreach and protect liberty. According to Gregg, this ongoing experiment is why immigrants are continually inspired to leave their homes and venture to the United States. These core tenets of America have become less defined over the past century. America has increasingly chosen big government over individual liberties, thereby reducing the benefits of free-market capitalism. The major expansions of government started in the progressive era, with Presidents Teddy Roosevelt, Woodrow Wilson, and Herbert Hoover. Those historic expansions were put on steroids by President Franklin D. Roosevelt’s “New Deal,” which prolonged and deepened the Great Depression. Likewise, President Lyndon B. Johnson’s “Great Society” program ballooned government through the creation Medicare and Medicaid, among others. The results have been massive government spending with increased dependency on government programs. President George W. Bush’s expansion of Medicare with Part D provided some prescription drug coverage for seniors, with questionable results, at a massive cost. President Barack Obama’s Obamacare expanded government control, contributing to the high cost and declining quality of US healthcare. President Trump’s attempt to punish China with tariffs actually punished low-income Americans most. Most recently, President Biden’s 2022 “Inflation Reduction Act” further grows government, without reducing inflation and at a huge cost to taxpayers. Inflating the role of government in an attempt to solve underlying issues created by big government created a vicious cycle that continues today. Government meddling distorts the economy by blocking and confusing free people’s choices. This results from a cultural shift, where Americans increasingly seem to believe government can solve problems better than markets or individuals. This belief is contradicted by the evidence. The lack of belief in free markets is really the lack of believe in free people, as the market is nothing but people. Big government is usually the cause of economic and social problems, so trying to solve them with more government just exacerbates the issues. A severe deficit in the knowledge of history, both of culture and economics, helps explain why post-modern socialist solutions increasingly entrance younger generations. Unlike older countries, America’s identity comes from the “texts, documents, and debates” that created our founding, says Gregg. Surveys show that only 1 in 3 Americans can pass a citizenship test, because most of them aren’t familiar with the foundational ideas outlined in our texts and documents. A national identity crisis is near-inevitable, when we forget our core values of liberty and personal responsibility The further we stray from the principles that made our nation great (including free-market capitalism, a constitutional republic, and personal responsibility) the more swiftly we head down what economist Friedrich Hayek called “the road to serfdom.” Only by learning our unique history, and grasping the principles of free-market economics free from burdensome interference, can Americans embark on the next American economy. Originally published at AIER. As Congress rolled out the $1.7 trillion omnibus government-funding bill, an economist broke down the effects of large federal spending amid big deficits and high debt, the impact on tuition, and the need for oversight of some of this taxpayer money. NTD spoke to Vance Ginn, the president of Ginn Economic Consulting, who warned against massive spending, given a federal deficit of over $1.3 trillion and a national debt of over $31 trillion. Ginn called on Americans to say “no” to the bill and let the next Congress draft a budget, and alleged that the omnibus bill expands social safety nets without connecting them back to people joining the workforce.

Originally posted at NTD News.  The latest inflation report reveals that inflation is slowing, but it remains at a 40-year high.

The stock market rose, as softer-than-expected inflation rate gave investors hope the Federal Reserve may not have to raise its target rate quite as fast. A 7.7-percent increase in prices over the last year shouldn’t make people hopeful. Many Americans can’t afford soaring living expenses, however, and the economy will worsen before there’s any relief. Adding to this struggle are inflation-adjusted average weekly earnings, which are down 4 percent over the last year, and have been declining for nearly two years. This deflating of the American Dream is the result of big-government policies, creating too much money chasing too few goods. Just the necessity of food is a struggle. Food prices at work and school are up 95 percent. Eggs are up 43 percent, and chicken, 15 percent. Gasoline to drive to the store is up nearly 18 percent and electricity, 14 percent, so even making meals at home can rock the budget. To cope with less purchasing power, Americans are not only saving less, they’re also accruing credit card debt, to a record high of nearly $1 trillion. Even in states with comparatively low cost of living, like Texas, people with full-time jobs can’t make ends meet for their families and are showing up at food banks for help. Unfortunately, the worst is yet to come. The Fed’s meager strategy for fighting inflation hasn’t included aggressively cutting its $8.6 trillion balance sheet. The balance sheet is only about 3.8 percent less than its record high in April 2022, after more than doubling during the pandemic. This overprinting of money affects many markets, as those dollars aren’t evenly distributed across the economy, resulting in distorted price signals. The Federal reserve adding assets to its balance sheet (by buying Treasury debt, agency debt, and mortgage-backed securities) kept interest rates artificially low. Those markets are starting to correct, as mortgage rates have risen to 20-year highs of around 7 percent. The Fed created the current inflationary situation (too much money), which was fueled by Congress’s deficit spending, and exacerbated by Biden’s overregulation (too few goods and services). Now, the false “boom” is busting. Hardworking families and entrepreneurs bear the brunt. To combat the problem it helped create, the Fed is raising its target federal funds rate, which has grown at the fastest pace since Paul Volcker was Chairman in the early 1980s. Volcker understood that the Fed’s balance sheet mattered most, which seems to be overlooked by the Fed and many economists today. The Fed’s hike of 75 basis points on November 2 brought the top of the target range to 4 percent, which was the fourth consecutive 75-basis-point hike, after rates were held at essentially zero for two years. The Fed signaled that it will slow target rate hikes to likely 50 basis points in December, pushing the top rate to 4.5 percent by the end of 2022. This would be the highest rate in 15 years. The Fed’s attempt to correct elevated inflation comes too late to avert the economic consequences of keeping the target rate too low for too long. As a result, Americans are suffering from persistent inflation, higher interest rates, and a prolonged, deeper economic recession. What should be done? We need pro-growth policies. The executive branch should focus on cutting regulations. Congress should prioritize making the Trump-era tax cuts permanent, cutting the corporate tax rate, and passing spending limits to help balance the budget. The Fed, the source of so much money mischief, should adhere to a monetary rule that will cut its balance sheet as much as possible, hopefully down to nothing. These pro-growth, liberty-oriented policies will unleash the economic potential of the productive private sector and get people back working again at well-paid jobs, while substantially reducing inflation. Big-government policies must end before they send us further down the road to serfdom. Our newly elected officials have a responsibility to prioritize fighting inflation, and restoring the American Dream. Originally posted at AIER.  While a stagnating economy with high inflation is what economists usually call stagflation, the current situation is worse, as the real economy is declining. So there’s much less to go around for everyone—making us poorer in the process.

This inflation-recession could be resolved by Washington reversing course, but President Joe Biden and Democrats in Congress are doing the opposite. Their new bill, called the “Inflation Reduction Act” (IRA), will spend more, raise taxes, increase debt, and contribute to more inflation, resulting in a deeper recession. The IRA includes estimated hikes in taxes with a new 15% corporate minimum tax rate, 87,000 new Internal Revenue Service (IRS) agents to audit more taxpayers, and new closure of “carried interest loophole.” These are each bad policies, but especially during a recession. These add up to an estimated tax hike of about $730 billion compared with current policy over the next 10 years. The main tax hike is the new alternative minimum tax (AMT) of 15% on book income for corporations with net income exceeding $1 billion. This proposal has a rosy revenue projection of $313 billion. But businesses don’t pay taxes; they just submit them. People pay them, through higher costs, lower wages, and fewer jobs. The dynamic effects will result in less tax revenue collected from this hike. According to a recent study by the Tax Foundation, this tax hike alone would contribute to killing 23,000 jobs, a 0.1% cut in wages, and 0.1% less in economic output. If we consider other provisions like the tax hikes on carried interest and reinstatement of the federal Superfund program, the total number of jobs killed is 30,000 with every income group having a reduction in after-tax income. Clearly, this wouldn’t reduce inflation or help the economy recover. But there’s more. While the IRA is aimed at taxing the rich and corporations more, the Congressional Joint Committee on Taxation finds that every income group except those with income between $10,000 to $20,000 per year would face a higher average tax rate. This would mean President Biden’s pledge to not tax anyone earning less than $400,000 per year would be broken, with about half of the burden falling on those earning less than $200,000 per year. And the $80 billion in additional funding for 87,000 new IRS agents to increase tax enforcement and compliance is expected to bring in a phony amount of about $200 billion over a decade. But this will just increase more bureaucracy in an already overly bureaucratic federal government that will make Americans’ lives worse as they put more costs on taxpayers. Specifically, there could be 1.2 million more individual audits per year, and you can bet when the IRS doesn’t increase tax collections from legal tax returns they will come after every tax group, not just those making more than $400,000 per year. On the spending side, the IRA provides tax incentives and subsidies for unreliable wind and solar energy, an expansion of Obamacare subsidies until 2025, and other expenditures to the tune of about $430 billion. Using these rosy assumptions, there is a projected deficit reduction of $300 billion over 10 years. However, more conservative estimates suggest that the IRA will have less deficit reduction and will likely increase the deficit. The Tax Foundation, Penn Wharton Budget Model (PWBM), and Congressional Budget Office (CBO) calculate a $178 billion, $247.8 billion, and $101.5 billion in deficit reduction over the next decade, respectively. But assuming the Obamacare subsidies are extended over the full 10-year period for an apples-to-apples comparison, the PWBM estimates that would bring that deficit reduction down by $158.9 billion to just $88.9 billion over the decade, which is the same amount of the deficit in just June 2022. But recall that these estimates are compared with current policy assumptions over the next decade, which already have massive deficits because of reckless spending, so the IRA will most likely make the deficit worse. Spending will be permanent and is on the front end of the bill, while taxes will likely be temporary and are more on the back end—so the deficit will be higher in the first few years, which will give the Federal Reserve more debt to purchase thereby creating more inflation. And the higher taxes, more debt, and more inflation will stifle economic growth so a deeper recession will result. The IRA does the opposite of what the name implies. This is now too common with Democrats in Congress as they like to keep redefining things that don’t match their narrative. They should instead name this bill the “Inflation Recession Act” because we will get more of both. This far-left agenda must be rejected. Kill the bill. Published at TPPF with Daniel Sanchez-Pinol  Americans are sacrificing their savings to keep up with soaring inflation.

This burden has contributed to consumer sentiment reaching its lowest level in June since the University of Michigan started the survey in January 1978. And the progressive policies in D.C. could soon make this bad situation worse. The personal saving rate, which is the share of after-tax income not used for consumption, declined again to 5.1% in June. This is after it reached 33.8% in April 2020, which was a record high since January 1959, after the first round of “stimulus” checks sent by Congress during the shutdowns. There were two more rounds of checks sent by Congress, along with enhanced unemployment payments and other handouts that weren’t connected to work, which kept the saving rate historically high as many places were shut down and people made more from handouts than they did while working. Remember, nothing is free. Those handouts and other government spending contributed to more than $6 trillion in additional national debt, which the Federal Reserve then mostly monetized—leading to the generational high in inflation. The higher inflation outpaced saving and income growth since then, as the costly policies came home to roost and cut the saving rate to 5.1%—the lowest since August 2009. What will happen when Americans run out of savings? But there’s little reprieve in sight as inflation looks to keep rising or at least not abating soon from bad policies in D.C. Inflation, which is the loss of purchasing power of your dollar, continues upward to 6.8% in June 2022 as measured by the personal consumption expenditure (PCE) price index—the highest since January 1982. The PCE inflation measure accounts for the substitution effect from high priced goods to lower priced goods. This isn’t reflected in the often-reported measure of the consumer price index (CPI) inflation rate of 9.1%, which is the highest since November 1981. Both measures show Americans’ money isn’t going nearly as far as it did a year ago. In fact, families’ purchasing power is set to be cut in half in just 10 years at the pace of PCE inflation and even faster for CPI inflation. This implies that in order to maintain the same consumption levels, households have to allocate more income to consumption than to savings. And many Americans are turning to increased debt as their savings dry up. Household debt increased to a record high of $16 trillion in the second quarter of 2022. Not surprisingly, credit card debt grew the most by 13%, which is the fastest increase in 20 years. Moreover, household debt to real economic output passed the 80% mark at the end of 2021. It’s up to 82% in the second quarter of 2022, a historically high rate, as debt increased and the real economy declined for two straight quarters. This share will likely get worse in the following quarters as Americans go through their savings and dip further into debt. And interest rates going up means the amount to pay interest on the debt will contribute to higher balances and more pressure to meet their financial obligations. No wonder people don’t feel secure about their economic future. Bad policies by Congress and the Federal Reserve contributed to this destruction and could even make things worse. Congress spent too much, leading to massive deficits, which gave the Fed debt to purchase to inject money into the economy over the last two years. That inflated “boom” had to eventually “bust.” And that’s what is happening now as the redistribution by Congress has slowed some and the Fed is finally raising its target interest rate allowing markets to correct. But Congress should be spending much less and the Fed should be more aggressive in tightening the money supply and raising its interest rate target. The famous Taylor rule suggests a rate of at least 6%, which is substantially higher than the current range between 2.5% to 2.75%. Ultimately, what’s needed now are pro-growth policies of spending, taxing, regulating, and printing cuts instead of what’s coming out of Washington. President Biden and Democrats in Congress aren’t helping the situation with the “Inflation Reduction Act,” as it will lead to more debt and more inflation that will further deplete savings, thereby making a bad situation worse for Americans. Things must change. Published at TPPF with Daniel Sanchez-Pinol  The U.S. government is bankrolling favored businesses at the expense of taxpayers and other businesses. Again. By continually involving itself in the market, government is impeding economic growth and the potential of industries to reach their full potential. That must change.

Congress recently passed the CHIPS Act, which is a $280 billion spending boondoggle that will provide funding of $52.2 billion to computer chip manufacturers. To sweeten the pot, Congress is also offering a 25% tax credit for semiconductor fabrication, which could cost an estimated $24 billion over five years. And these subsidies could support production in other regions, such as China and Europe. President Joe Biden will sign this obscene corporate welfare scheme into law soon. Congress claims this will strengthen domestic semiconductor production and help the U.S. compete with China, but that rhetoric is wrong. Domestic production of these technologies has been slowing since 1990. The U.S. still has valuable domestic producers, like Texas Instruments and Intel, but these corporations recently accounted for 12% of global chip production in 2021, down from 37% in 1990, according to the Boston Consulting Group. While the federal government might seem smart for attempting to help this industry compete, its methodology is flawed. Expanding corporate welfare will only serve to degrade competition and diminish the free-market principles that uphold the U.S. economy. This flawed approach is apparent when considering the data around prices of chip production. The total 10-year cost of ownership of a new semiconductor fabrication plant in the U.S. is 30% higher than in Taiwan, South Korea, or Singapore, and 37% to 50% higher than in China—or $10 to $40 billion dollars depending on the product. Anywhere from 40% to 70% of the difference in price is directly attributable to the incentives government provides that contribute to reduced competition. Throwing taxpayer money at the problem is a solution in search of a problem. In 2021, the U.S. semiconductor industry had substantial growth. In the closing months of 2021, American sales increased by 5.2%. That year the market had the largest share of growth worldwide, expanding 27.4%. While recessions in the U.S. and elsewhere have reduced consumption of goods that use semiconductor chips and as production increases, there has been a reduction in shortages and lower chip prices—contributing to lower stock prices. While the U.S. lags China in semiconductor production, the U.S. industry is growing faster, and we still lead by large margins in research, development, and design. The U.S. industry is a leader in chip design, and accounts for roughly 60% of all global fabless firm sales, and some of the largest integrated device manufacturers. The U.S. accounts for the largest share of the global design workforce, speaking to our leadership and development prowess. Earmarking $76 billion of taxpayer money for an already growing industry while in the midst of a recession is politically irresponsible and economically destructive. Moreover, spending to this degree fuels the bloated national debt during a recession and puts upward pressure on inflation if the Federal Reserve monetizes the debt. While President Biden will likely sign the CHIPS Act, Congress ought not use this as a precedent to subsidize more industries. The outsourcing of semiconductor production should be a wake-up call to the burdensome overregulation, overspending, and over-taxation domestically on businesses; not a license to spend more taxpayer money. With more subsidies going to specific companies, less investment and the further fleeing of business from America to places with more attractive and beneficial economic circumstances will continue. Advocates like U.S. Sen. Tom Cotton tried to justify this bill by claiming that “by ceding semiconductor manufacturing and development to countries like China, the United States has fallen behind and given the Chinese Communist Party dangerous leverage over our nation.” While China has leverage over America in that department for now, this corporate welfare is economically harmful. In the process of providing cash to businesses, corporate welfare takes money from taxpayers and consumers, reducing economic growth and increasing the debt that has many risks—including economic and national security. Because corporate welfare disrupts natural market processes, it shifts money from the most productive economic actors to those less productive—but more politically connected. This creates economic inefficiency and stunts competition, making the situation worse. The U.S. government ought to instead cut the cost of doing business domestically by reducing government spending, taxes, and regulations. By correcting the current government failures in this market in this way, Americans will flourish more. Published at TPPF with Noah Busbee  The economic shock from the shutdowns in response to the COVID-19 pandemic were unprecedented. Never had state governors imposed stay-at-home orders that cut people off from their lives and livelihoods. Those costly policies were bad enough, but then came historic increases in deficit spending and money creation.

While these may have been well-intentioned policies early on, their repercussions—amplified by misguided macroeconomic policy since January 2021—continue to plague many Americans. The antidote is pro-growth policies. There was a vibrant economy on the eve of this shock. In fact, about three quarters of the flows of people into employment were Americans returning to the workforce—the highest on record. For context, 2.3 million prime-age Americans—people between the ages of 25 and 54—returned to the labor force during Trump, after 1.6 million left during the Obama recovery. This happened with a robust private sector providing many opportunities because the Trump administration focused on removing barriers by getting the Tax Cuts and Jobs Act of 2017 through Congress and providing substantial, sensible deregulation. We often hear that these tax cuts were “trickle-down economics” or “tax cuts for the rich and big business.” But the change in real (inflation-adjusted) wages was positive across the income spectrum. The bottom 10% of the wage distribution rose by 10% while the top 10% rose half as fast. And real wealth for the bottom 50% increased by 28%, while that of the top 1% increased by just 9%. The results show those tax cuts weren’t designed for the “rich.” In 2019, the real median household income hit a record high, and the poverty rate reached a record low. Poverty rates fell to the lowest on record for Blacks and Hispanics, and child poverty fell to 14.4%—a nearly 50-year low. Clearly, Americans were doing well across the board, especially those who had historically been left behind. These stellar results were from reducing barriers by government in people’s lives—a stark contrast to what happened by state governments during the pandemic and exacerbated thereafter by Biden’s big-government policies. While there were similar spending bills passed into law during both administrations, it’s comparing apples and oranges. Trump supported congressional efforts in March and April 2020 when huge swaths of the economy were shut down, 22 million Americans were laid off, and 70% of the economy faced collapse. In contrast, Biden substantially increased regulations immediately and passed a nearly $2 trillion spending bill in March 2021—an amount equal to approximately 10% of the U.S. economy, at a moment when the U.S. economy was already 10 months into recovery. Another difference was that Trump introduced sunsets for emergency pandemic provisions so that they would expire. But Biden continued and expanded many of them, increasing dependency on government. Through March 2022, employment is back up 20.4 million but remains 1.6 million below the peak in February 2020. While Biden touts the most jobs gained in one year in 2021, more jobs were recovered in just the two months of May and June 2020 than in all 12 months of 2021, and nearly two-thirds of this jobs recovery was during Trump. Moreover, job gains of 6.7 million in 2021 were far less than the glorified projections coming from the White House of around 10 million. Just think if Biden had practiced the pro-growth policies of Trump. Instead, inflation is at a 40-year high and looks to continue to soar, fueled by a host of self-imposed costly policies in Washington. This includes Biden’s over-regulating of the oil and gas sector, massive unnecessary spending bills, and attempts to drastically raise taxes. And the Federal Reserve has more than doubled its balance sheet over the last two years, purchasing a majority of the $6 trillion increased national debt in that period, which is a 25% increase to $30 trillion. These policies, which simultaneously boost demand while constraining supply, have brought the prospect of stagflation—high inflation and low growth—back for the first time since the late 1970s. Rather than directly addressing the crisis, Biden has consistently deflected the issue by first doubting the reality of inflation to now falsely blaming it on corporate greed or Russian President Vladimir Putin. But the causes and consequences fall at his feet. It’s time to return to the proven, pro-growth policies that worked during the Trump administration, along with an essential missing factor then of spending restraint by Congress. Doing so will provide a solid foundation for more opportunities to let people prosper. This commentary was based on the remarks by Mr. Ginn and Mr. Goodspeed on a panel at the Texas Public Policy Foundation’s 2022 Policy Orientation. https://www.texaspolicy.com/biden-should-pivot-to-trumps-pro-growth-policies/  Americans have less money than they had last year—though taxes haven’t been raised. So what’s the problem? Inflation, which has increased at a 40-year high annual pace of 7.9%. It acts as a hidden tax because we don’t see it listed on our tax bills, but we sure see less money on our bank accounts.

In fact, inflation-adjusted average hourly earnings for private employees are down 2.8% over the last year. This means a person with $31.58 in earnings per hour is buying 2.8% less of a grocery basket purchased just last February. “For a typical family, the inflation tax means a loss in real income of more than $1,900 per year,” stated Joel Griffin, a research fellow at The Heritage Foundation. The hidden tax of rapid inflation has been avoided for four decades. But that’s understandable because we haven’t seen these sorts of reckless policies out of Washington since the Carter administration. The policies from the Biden administration’s excessive government spending and the Federal Reserve’s money printing must correct course now before things get worse. What’s causing inflation is being debated. One claim is “Putin’s price hikes” stem from the Russian president’s invasion of Ukraine. While this has contributed to oil and gasoline prices spiking recently, these prices—and general inflation—were already rising rapidly. This was because of the Biden administration’s disastrous war on fossil fuels through increased financial and drilling regulations, cancelation of the Keystone XL pipeline, and more. Specifically, the price of West Texas Intermediate crude oil is up about 110% since Biden took office, yet only up 21% since Russia invaded Ukraine. And to think, the U.S. was energy independent in the sense that it was a net exporter of petroleum products in 2019. Another claim is the supply-chain crisis. For example, the global chip shortage has contributed to a large shortage and subsequent increase in the average price of new vehicles—to a record high of $47,000, up 12% over the last year. This contributed to buyers switching to used cars, which has pushed the average price up to nearly $28,000, about 40% higher. These two claims will likely be transitory price increases, though not sufficient to drive down overall inflation to what we’ve experienced for the last year-plus. Inflation is persistent because of rampant government spending and money printing. Larry Kudlow, who served as the director of the National Economic Council for President Trump, stated that inflation “is destroying working folks’ pocketbooks and devaluing the wages they earn, and the root cause of the inflation is way too much government spending, too many social programs without workfare, and vastly too much money creation by the Federal Reserve.” Both political parties share the blame for too much government spending, which has caused the national debt to balloon to $30 trillion. Just over the last two years, the debt has increased by 25% or $6 trillion. While some of that may have been necessary during the (inappropriate) shutdowns in response to the COVID-19 pandemic, much of the nearly $7 trillion passed in spending bills was not, especially the trillions by the Biden administration far after the pandemic had slowed and people were returning to work. Laughably, Speaker of the House Nancy Pelosi recently argued that government spending is helping inflation and President Biden argued that he’s cutting the deficit. Both are false. Government spending doesn’t change inflation because it just redistributes money around in the economy. And the deficit would only be rising from Biden’s big-government policies but he’s taking advantage of an optical illusion: one-time COVID-19 relief funding drying up and tax revenues rising partially from the effects of inflation. Ultimately, the driver of inflation is from discretionary monetary policy by the Federal Reserve as it monetizes much of the $6 trillion in added national debt since early 2020. The Fed did this to keep its federal funds rate target from rising above the range of zero to 0.25% by more than doubling its balance sheet to $9 trillion. More money is fueling the ugly government spending and bubbly asset markets that’s resulting in dire economic consequences. Instead, we need to learn what Presidents Harding and Coolidge realized a century ago. This would mean a return to sound fiscal policy, monetary policy, and the dollar that built on the principles of America’s founding. We need binding fiscal and monetary rules to hold politicians and government officials in check of we hope to tame inflation and return to prosperity. https://www.texaspolicy.com/the-tax-increase-thats-hidden-in-plain-sight/  It’s bad enough when politicians enact witless economic policies with huge price tags, but it’s even worse when those policies destroy American lives and livelihoods. New research shows that this will be the pandemic-era legacy of the politicians that forcibly closed businesses, made people stay home, then incentivized millions of out-of-work Americans to give up the opportunity to get their lives back on track.

It’s now clear that half the states kept destructive policies in place even after their devastating effects were known. What should have been a temporary bridge to keep people afloat while America tackled COVID-19 became a nightmare of dependence and depression. In March of 2020, the federal government began paying weekly “bonuses” known as supplemental insurance to people on unemployment. That meant many people received more money from unemployment insurance than they did while working. It was even expanded to include those who hadn’t paid into the program. By the fall, the country began emerging from the pandemic, vaccines became available, and business started to open again and look for workers. The speed of American resilience was something to behold. But the government refused to make the transition with the rest of the country and kept paying people to stay home. Eliminating people’s jobs and paying them to be unemployed was robbing millions of Americans of the dignity that comes with finding purpose and achieving self-sufficiency. It destroyed lives, driving dependency on government, contributing to drug and alcohol addiction, and exacerbating isolation and depression. These effects of the program were blatantly obvious through the spring of 2021 but that didn’t stop the Biden Administration and Congress from extending the benefits through September. By the summer of 2021, the nation had nearly 11 million unfilled jobs, a spike from just under 7.2 million at the beginning of the year. That’s why 26 states decided to terminate the unemployment bonuses early instead of letting them expire in September 2021. At the time, some in the media portrayed the move as cruel, ripping critical funds away from those struggling during the pandemic. But new research from the Texas Public Policy Foundation shows that the states that ended the benefits early had superior job growth, ending the soul-crushing dependency inflicted upon millions by the misguided policy. By the end of 2021, only Texas and three other states that ended the bonuses early had regained all the jobs that they lost during the pandemic. In the states that continued paying the unemployment bonuses through September 2021, job growth was anemic. Roughly 3 million more people stayed on unemployment in states that maintained the increase in benefits versus the states that ended the program early. The states that continued this policy deserve particular scorn for going down this fatuous path because they should have known better. The unemployment bonuses were first implemented in 2020 during the depths of the government-imposed restrictions and the disastrous results were known a year later. Yet they pushed forward full throttle irrespective of the harm it was causing to millions of Americans. There were better solutions. Early in the pandemic when much wasn’t known, Congress could have eliminated federal payroll taxes. Instead of creating a new disincentive to work, policymakers could have removed an existing disincentive and let workers keep more of what they earned. A July 2020 study found that eliminating payroll taxes would have added 2.7 million jobs in six months. Later, after we learned more about the pandemic and the costs of shutdowns, the Biden administration should have focused on ending state government-imposed shutdowns. These shutdowns were a failure that did little to nothing to mitigate the pandemic’s effects yet contributed to massive business closures and job losses, along with a host of other problems that will be long-lasting.. The experiment with unemployment “bonuses” should be closed and never opened again. It unnecessarily prolonged the economic devastation brought on the country by the pandemic and slowed the path to recovery for millions of Americans. Job creation proved to be the fastest road to provide help and hope. https://www.texaspolicy.com/the-real-cost-of-pandemic-era-policies/  Government spending is at the heart of sound public policy. But out-of-control spending for decades has created substantial economic destruction and ongoing threats that must be remedied before things get worse. Fortunately, we have examples of how fiscal rules can solve this problem. We must put these rules into place before our economy gets any worse.

Excessive federal government spending has created mounting budget deficits that have driven the national debt to $30 trillion. This debt has given the Federal Reserve ammunition to use to excessively print money, resulting in the highest inflation in 40 years. And inflation destroys our purchasing power as it is a hidden tax that erodes our livelihood. Controlling spending takes discipline, and applying fiscal rules can help. Policymakers should follow the examples a century ago of Presidents Warren G. Harding and Calvin Coolidge, who demonstrated that controlling spending and cutting the debt is possible. President Harding assumed office in 1921 when nation was suffering an overlooked severe economic depression. Hampering growth were high income tax rates and a large national debt after WWI. Congress passed the Budget and Accounting Act of 1921 to reform the budget process, which also created the Bureau of the Budget (BOB) at the U.S. Treasury Department (which was changed in 1970 to the Office of Management and Budget in the Executive Office of the President). President Harding’s chief economic policy was to rein in spending, reduce tax rates, and pay down debt. Harding, and later Coolidge, understood that any meaningful cuts in taxes and debt couldn’t happen without reducing spending. Charles G. Dawes was selected by Harding to serve as the first BOB Director. Dawes shared the Harding and Coolidge view of “economy in government.” In fulfilling Harding’s goal of reducing expenditures, Dawes understood the difficulty in cutting government spending as he described the task as similar to “having a toothpick with which to tunnel Pike’s Peak.” To meet the objectives of spending relief, the Harding administration held a series of meetings under the Business Organization of the Government (BOG) to make its objectives known. “The present administration is committed to a period of economy in government…There is not a menace in the world today like that of growing public indebtedness and mounting public expenditures…We want to reverse things,” explained Harding. Not only was Harding successful in this first endeavor to reduce government expenditures, his efforts resulted in “over $1.5 billion less than actual expenditures for the year 1921.” Dawes stated: “One cannot successfully preach economy without practicing it. Of the appropriation of $225,000, we spent only $120,313.54 in the year’s work. We took our own medicine.” Overall Harding achieved a significant reduction in spending. “Federal spending was cut from $6.3 billion in 1920 to $5 billion in 1921 and $3.2 billion in 1922,” noted Jim Powell, a Senior Fellow at CATO Institute. Harding and the Republican Party viewed a balanced budget as not only good for the economy, but also as a moral virtue. Dawes’s successor was Herbert M. Lord, and just as with the Harding Administration, the BOG meetings were still held on a regular basis. President Coolidge and Director Lord met regularly to ensure their goal of cutting spending was achieved. Coolidge emphasized the need to continue reducing expenditures and tax rates. He regarded “a good budget as among the most noblest monuments of virtue.” Coolidge noted that a purpose of government was “securing greater efficiency in government by the application of the principles of the constructive economy, in order that there may be a reduction of the burden of taxation now borne by the American people. The object sought is not merely a cutting down of public expenditures. That is only the means. Tax reduction is the end.” “Government extravagance is not only contrary to the whole teaching of our Constitution, but violates the fundamental conceptions and the very genius of American institutions,” stated Coolidge. When Coolidge assumed office after the death of Harding in August 1923, the federal budget was $3.14 billion and by 1928 when he left, the budget was $2.96 billion. Altogether, spending and taxes were cut in about half during the 1920s, leading to budget surpluses throughout the decade that helped cut the national debt. The decade had started in depression and by 1923 the national economy was booming with low unemployment. If this conservative budgeting approach—which was tied with sound monetary policy for most of the period—had been continued, the Great Depression wouldn’t have happened. Officials at every level of government today should learn from this extraordinary lesson that fiscal restraint supports more economic activity as more money stays in the productive private sector. With spending out of control at the federal level and in many states and local governments, the time is now for spending restraint and strong fiscal rules to set the stage for more economic prosperity today and for generations to come. https://www.texaspolicy.com/learning-from-the-champions-of-fiscal-conservatism/  We were promised job growth—after all, that was the main selling point for the March 2021 American Rescue Plan Act (ARPA) from President Biden and the congressional Democrats. Promise made—promise broken.