Property taxes in Wyoming have increased dramatically, placing a substantial burden on taxpayers. This proposal outlines a bold, practical plan to eliminate property taxes through disciplined government spending and targeted surplus distribution to reduce school district property taxes.

Property Taxes are Growing Too Fast:

Process for Eliminating Property Taxes: The proposed process involves three critical steps aimed at systematically reducing and eventually eliminating property taxes while fully funding state government operations and school districts:

Expected Outcomes

Economic Gains

Conclusion This proposal seeks to relieve Wyoming residents of the oppressive property tax burden. The discipline it imposes on state spending directly benefits all Wyoming taxpayers – surplus money flows back into their pockets, not into government accounts to be spent by politicians. Achieving this bold reform will allow Wyoming to flourish now and for future generations. Full research paper here.

0 Comments

Originally published at Texans for Fiscal Responsibility.  Executive Summary

Originally published at The City Journal.

In November 2023, Texas voters approved a constitutional amendment, HJR 2, which Governor Greg Abbott said would “ensure more than $18 billion in property tax cuts—the largest property tax cut in Texas history.” Texas homeowners’ hopes were dashed at the start of 2024, however, when they got their property tax bills. The promised $18 billion reduction amounted to only $12.7 billion in new property tax relief, a fraction of the state’s record $32.7 billion budget surplus, while the other $5.3 billion merely maintained property tax relief from years past. While Texas doesn’t have a state income tax, it does have the nation’s sixth-most burdensome property taxes. These taxes obstruct peoples’ ability to buy homes and price others out of the homes they’re in. Texans expect and deserve clarity about their property tax bills, but state policymakers’ failed promises and lack of transparency have eroded public trust. Despite the governor’s claim, the 2023 tax relief package, spread over two years, isn’t even the state’s largest historic property tax cut. In 2006, the Texas legislature apportioned $14.2 billion to reducing residents’ property taxes, cutting school district maintenance and operations (M&O) property tax rates by a third for 2008–09 biennium, and making up the difference with a revised franchise tax, a higher cigarette tax, and a higher motor vehicle sales tax. Adjusted for inflation, 2023’s cut would have had to exceed $21 billion to surpass the 2006 cut. The new package's biggest achievement was saving taxpayers $5 billion in 2023 by reducing the maximum school district M&O property tax rate by 10.7 cents per $100 valuation; it also raised the homestead exemption of taxable value for school district M&O property taxes to $100,000 and limited appraisal-value increases to 20 percent for other property. And yet, Texans’ total property taxes paid in 2023 nevertheless rose by $165.2 million over 2022, an overall increase of 0.4 percent. That net increase came from school district tax hikes to fund more debt ($890.2 million); municipal governments ($1.3 billion); county governments ($1.5 billion); and special purpose districts ($1.5 billion). These hikes effectively washed away state-level reductions. While this result is ultimately the fault of local governments, the state should have done more to provide relief and restrict localities’ spending and taxes. This growth in local property tax collections is part of a larger trend. From 1998 to 2023, Texas’s total property taxes collected rose 338 percent while the rate of population growth plus inflation was just 136 percent. No wonder so many Texans feel as though they are being crushed by housing unaffordability. How can Texas fix its spending problem? Rather than resort to temporary fixes, the state needs a robust spending cap in its constitution like Colorado’s Taxpayer’s Bill of Rights (TABOR), which limits state and local government spending increases to no more than the rate of population growth plus inflation. Though Colorado’s TABOR has been the gold standard for a state spending limit since its enactment in 1992, it can be improved. At this time, TABOR applies to Colorado’s general revenue, less than half of its total funds; it should be expanded to apply to all state funds, which would account for about two-thirds of its budget, as originally intended. Texas, or Colorado itself, could also improve the model by replacing the latter’s policy of refunding excess tax revenue to taxpayers with up-front income-tax-rate cuts. Texas enacted a statutory spending limit in 2021, but it lacks teeth, as an overriding constitutional spending limit covers just 45 percent of the budget and can be exceeded by a simple majority. In conjunction with a stronger constitutional spending limit, the Texas legislature should implement strategic budget cuts. These efforts combined with the stricter constitutional spending limit would create opportunities for surpluses at the state and local levels, which would pave the way for the state to reduce school M&O property taxes annually until they are fully eliminated. This alone would shave off nearly half of the property tax burden in Texas. Viewed from the coasts, Texas is a beacon of economic freedom. But as its spending and property tax data show, it isn’t perfect. The Texas legislature should acknowledge its failed promises and deliver real property tax relief for its citizens.  Originally published at Dallas Express.

Home “owners” in Dallas and surrounding cities find themselves grappling with the weight of unaffordability as property taxes soar, increasing by $120 million despite the touted cuts at the end of 2023. A recent study reveals the burden on renters in Texas and nationwide, with many paying over 30% of their monthly income on housing. A factor contributing to this rising cost of renting, and housing in general, is soaring property taxes. The predicament stems from excessive state and local spending and purported property tax “cuts” that too often merely shift the burden through exemptions. Renters, technically anyone with a monthly payment or a mortgage since homeowners are just renting from the government, bear the brunt of this financial strain, emphasizing the urgent need for fiscal reform. Late last year, Dallas residents witnessed a modest one-cent property tax reduction rate, with surrounding cities experiencing varying degrees of reduction. Fort Worth saw a 4-cent reduction, and McKinney a 3-cent reduction. Despite these adjustments, most cities, including Dallas, faced increased property taxes eclipsed by rising spending and housing appraisals. Even in Plano, recognized for its low property taxes in the DFW area, homeowners will endure higher monthly property tax amounts due to home valuation hikes. The incongruity between property tax decreases and housing cost increases is alarming, prompting a closer look at the numbers. According to Axios, the average taxable value of homes in Denton County rose from approximately $402,000 in 2022 to around $449,000 in 2023. Similarly, the average market value of Collin County homes increased from about $513,000 in 2022 to roughly $584,000 in 2023. One doesn’t need to be a mathematician to recognize how a property tax decrease of even a few cents doesn’t begin to keep pace with skyrocketing home valuations and rent. No wonder 20% of Dallas homebuyers looked to get out of the city last year. The crux of the issue lies in reining in local spending. The axiom holds: the burden of government is not how much it taxes but how much it spends. Dallas, with its escalating budget that reached a historic high last year, renders proposed property tax cuts inconsequential. My new research released by Texans for Fiscal Responsibility highlights how property taxes continued to go up last year by $165 million, even with the Texas Legislature passing $12.7 billion in new property tax relief. This ended up being the second largest property tax relief in Texas history, not the largest as many politicians have been claiming since last July, which is what I wrote then. The best path for Texans is to finally have their right to own their prosperity instead of renting from the government by paying property taxes forever. This can be done by restraining state and local government spending and using resulting state surpluses to reduce school property tax rates until they’re zero. And by local governments, including Dallas, using their resulting surpluses to reduce their property tax rates until they’re zero. Dallas must adopt a spending limit, one that does not permit the budget to exceed the rate of population growth rate plus inflation – a measure aligned with what the average taxpayer can afford. Performance-based budgeting and independent efficiency audits, preferably conducted by private auditors, should identify opportunities for improvements and reductions in ineffective programs, helping provide more opportunities for property tax relief. Dallas leaders can empower their constituents by redirecting taxpayer money to them while funding limited government. The adoption of these strategic measures not only benefits homeowners but extends its positive impact to renters and business owners, providing tangible rewards for their hard work and fostering a more economically vibrant community. Dallas leaders are responsible for ushering in a new era of fiscal responsibility that ensures affordability for all residents and supports sustained economic growth. The path to long-lasting property tax relief is clear: let’s seize this opportunity for positive change and secure a brighter, more prosperous future for Dallas.  Originally published at Texans for Fiscal Responsibility. Podcast: Is Texas Becoming Like California? TRUTH On State Spending, Property Taxes & More1/24/2024 This BONUS episode of the Let People Prosper show is with Bradley Swail, host of the Texas Talks podcast.

Today, we discuss: 1) Why "largest property tax relief in Texas history” became the second biggest due to excessive state spending and how the Lone Star State can eliminate the property tax for good; 2) The problem with a mandated minimum wage and reckless spending at the state and federal levels and; 3) Policies Texas leaders and lawmakers should adopt to strengthen the Texas model. Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. Also, subscribe and see show notes for this episode on Substack (www.vanceginn.substack.com) and visit my website for economic insights (www.vanceginn.com). I hope you enjoy the fantastic 67th Let People Prosper Show episode with TX State Rep. Brian Harrison! Please subscribe to my newsletter if you haven’t already, and subscribe to my podcast wherever you get yours. I would appreciate it if you would also rate and review my podcast! Brian (bio) and I discuss:

Click below to watch the episode and read on for show notes: We discuss:

1) The potential comeback of COVID shutdows and mask mandates, and why that would be fruitless for communities and public health; 2) How to reform the broken U.S. safety net system with the implementation of Empowerment Accounts, and how these differ from Universal Basic Income; and 3) How high property taxes in Texas are making home ownership unattainable for many or are driving seniors out of their homes, and how Texas could reasonably reduce property taxes until they are eliminated. Be sure to check out and subscribe to the "This Week in Bitcoin" podcast. You can watch this episode and others along with my Let People Prosper Show on YouTube or listen to it on Apple Podcast, Spotify, Google Podcast, or Anchor. Please share, subscribe, like, and leave a 5-star rating! For show notes, thoughtful insights, media interviews, speeches, blog posts, research, and more, check out my website (www.vanceginn.com) and please subscribe to my newsletter (www.vanceginn.substack.com), share this post, and leave a comment.  Texas Governor Greg Abbott (R) recently signed into law the tax relief compromise by the Legislature’s second special session. This relief is historic with the country’s largest tax cut and the largest net tax cut in Texas history.

But it falls short of what Texans were promised of the largest property tax cut in the state’s history, as it’s instead the state’s second largest property tax cut because of the largest spending increase in Texas history. Rather than providing substantial relief and simplifying the property tax system, the package presents a burdensome approach that could hinder the state's progress. By overspending and adopting a convoluted tax relief strategy, Texas risks falling behind states rather than leading the way in addressing real property tax concerns. The deal provides $12.7 billion in new property tax relief out of the nearly $33 billion surplus as the Legislature increased the upcoming 2024-25 biennial budget by more than 30% in state funds. This is the largest increase in Texas history and well above the the key rate of population growth plus inflation of 16% over the last two years. The major target for property tax relief was reducing school district maintenance and operations (M&O) property taxes. These property taxes are essentially a statewide property tax, which is prohibited by the state’s constitution, as they are partially determined by the state’s school finance system that includes redistribution of property taxes from school districts with high-valued property to districts with lower-valued property. Of the nearly $33 billion in state surplus funds and tens of billions more in new revenue available, the state allocated just $7.1 billion for a modest 10.7-cent reduction per $100 valuation in those property tax rates, called “compression,” which provides long-lasting relief and benefits everyone. The other $5.6 billion is for raising the homestead exemption by $60,000 to $100,000 for the appraised value of primary residences to determine how much is paid for school district property taxes. But this will be short-lived as valuations rise quickly and has failed to provide long-lasting relief the last three times it’s been tried in Texas since 1997 while benefitting only only homeowners. The $12.7 billion over the next two years will hardly alleviate the burden of property taxes on Texans and is a far cry from eliminating them altogether as Gov. Abbot initially set out to do. The package also includes a pilot project of an appraisal cap on non-homestead property at 20% per year for three years. This property doesn’t have a cap on it today so this will benefit some but will mean that local governments will just ratchet up property tax rates to bring in the tax revenue they desire to grow spending. There will also now be three elected officials added to county appraisal boards. Texans are left with this compromise package that unnecessarily complicates the tax system and obstructs efforts to eliminate school M&O property taxes, enabling the government to pick winners and losers. In this case, renters would undoubtedly be among the losers, and they are nearly 40% of households across the state. A more robust approach is necessary soon to achieve significant, long-lasting property tax relief for Texans. The best path being discussed is to buy down school district M&O property tax rates with surplus funds starting with limiting government spending, which was lacking this session after years of an improving budget picture. Ways to improve this overall package would have been by institutionalizing the buy-down plan and imposing spending limits on local governments. The final part of the package is $600 million to raise the exemption of gross receipts to pay franchise taxes from $1 million to $2.47 million, which is important but doesn’t help reduce property taxes and is less effective than cutting the franchise tax rates until they’re zero. This brings the total amount of new tax relief to $13.3 billion. This amount is lower than the $14.2 billion that the Legislature provided to buy down school property taxes in 2008-09, which would be about $21 billion to have the same purchasing power today. And even if you include the state maintaining its property tax rate reduction in 2019 of $5.3 billion in this year’s budget for a total of about $18.6 billion, it would not equal $21 billion. But that 2008-09 relief was done by raising bad taxes of the franchise tax, sales tax on motor vehicles, and cigarette tax which this time no taxes are raised as the taxpayer funds come from surplus money. So, this 2023 tax relief package can be called the “largest net tax cut in Texas history” but not the “largest property tax cut,” and is the largest tax cut in the country. But Texans could have had more relief if the state hadn’t spent so much. Eliminating school property taxes is a crucial next step for Texans to truly own their homes instead of renting from the government forever. And this will be achieved faster when politicians stop spending so much. So while this historic relief is much appreciated, there’s much more to do next session for Texans to stop renting and start owning. Originally published at Real Clear Policy.  (The Center Square) – The property tax relief package passed by the state Legislature is the second largest in Texas history, economist Vance Ginn, president of Austin-based Ginn Economic Consulting, says.

While at the Texas Public Policy Foundation, Ginn helped devise a plan to eliminate one of multiple property taxes homeowners pay: the school maintenance and operations (M&O) tax. Eliminating this tax over time was part of Gov. Greg Abbott’s call for the first and second special legislative sessions. Ginn, who sat down with The Center Square to explain differing property tax relief approaches, was also integral to implementing federal tax reform efforts when he worked at the White House’s Office of Management and Budget under the Trump administration. After the legislature passed an $18 billion property tax relief package Thursday, House Speaker Dade Phelan said it was “the largest cut in Texas history.” Lt. Gov. Dan Patrick said it was “the largest property tax relief package in Texas history, and likely the world.” Abbott, when running for reelection for his third term, vowed to return half of the state’s record $33 billion surplus to taxpayers. On Wednesday, he said the package allocated “at least $13.5 billion from our historic budget surplus to provide substantial relief to property taxpayers across Texas.” With additional money from the budget, he said they were delivering “over $18 billion in property tax cuts.” According to Ginn’s analysis, the package includes $12.7 billion in new relief and $5.3 billion from the earlier-approved state budget. Neither $13.5 billion nor $12.7 billion is half of the surplus, he points out. The combined $18 billion in property tax cuts, Ginn also points out, isn’t the largest property tax cut in state history. That occurred under Gov. Rick Perry in the 2008-2009 legislative session when the legislature passed $14.2 billion in property tax relief, he said. In order to surpass that, adjusting for inflation, “for us to have the same purchasing power of those dollars back then it would need to be about $21 billion,” he said. “This isn't the largest tax cut in history. It's substantial, it's historic, probably the second most ever.” But more problematic, he says, is the Republican-led legislature spent more money than ever before. “This session was the largest spending increase in Texas history of more than 20%,” he said. “If you look at all funds, and more than 30% if you look at state funds, the state's portion is up by a massive 30%. More than $50 billion being spent; that’s more than ever before. “If you spend too much, you can't provide as much in tax relief. That's just dollars coming from the taxpayers.” The $33 billion surplus means the state over collected taxes, he added. “That should be returned to the taxpayer. And the best way to do that,” through property tax reduction, “is through compression.” “The research that I've done on this in the past is that's the only way you can get to zero. If we really want to eliminate property taxes, which is what Governor Greg Abbott said he wants to do, you can't do it by raising the homestead exemption. You could raise the homestead exemption to $1 million, $2 million, $3 million but you're always going to have property values that are above that. So that can't get you to zero.” “Appraisal caps don't do that either,” he said, because they just slow growth, referring to the House plan, which was included in the bill. “Appraisal caps don't reduce property taxes. The only way to get to $0 per a $100 valuation, meaning a 0% tax rate, is by compression, lowering property tax rates until they get to zero. If you want to talk about limiting the growth of property taxes or a small relief, then you can talk about appraisal caps or homestead exemptions. But if you want elimination, and actually reduce them over time, the only way, the gold standard, is compression.” Ginn explained how compression works. "Rght now, when people pay property taxes to the school districts, the districts are funded at a set amount. The amount [that taxpayers overpay] that goes over the set amount, known as recapture, spills over and goes to Austin. When we talk about compression, what we're saying is we're wanting to reduce the recapture amount by the state funding a reduction in school M&O property tax rates. “You do this by using state dollars collected from taxpayers, mostly sales taxes, but also franchise taxes. The school districts still receive the same amount of money because state law requires them to be fully funded. The difference is how much [recapture money] goes to Austin or not.” Compression going to zero would eliminate recapture altogether, he explains. Recapture is one reason why “the school property tax is essentially a statewide property tax,” he said. While the M&O tax is “determined by the school finance formulas that are set by the Texas legislature, “It's local in name only. That's why the focus has been to eliminate it at the state level. Use record levels of sales taxes and surplus dollars to reduce, compress the school district property tax until it goes all the way to zero.” Original post at Washington Examiner from The Center Square.  An Overview

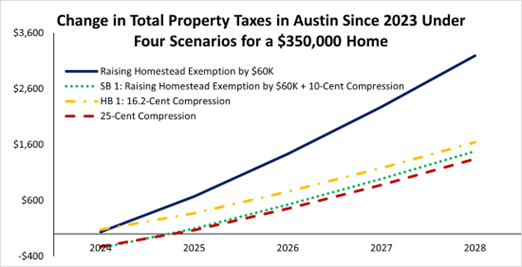

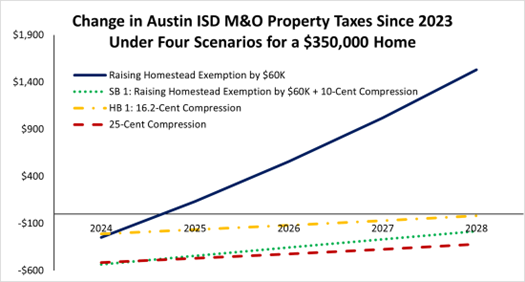

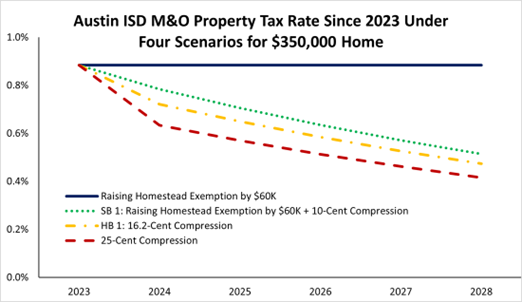

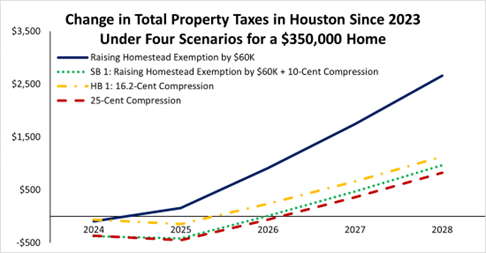

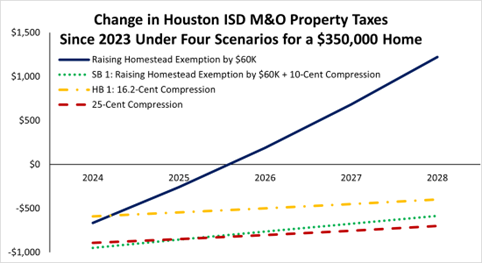

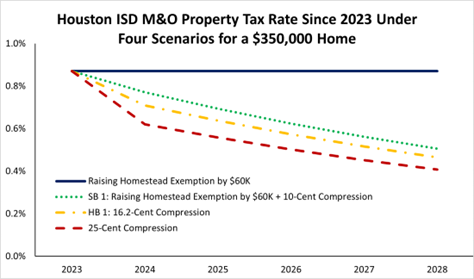

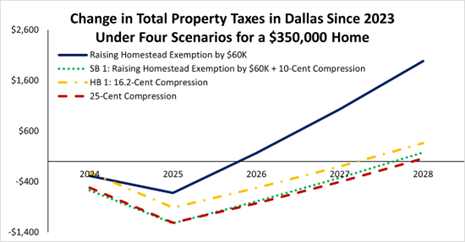

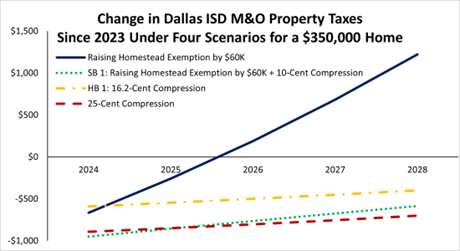

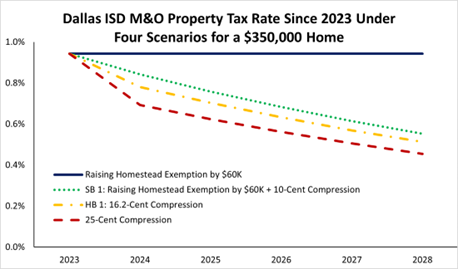

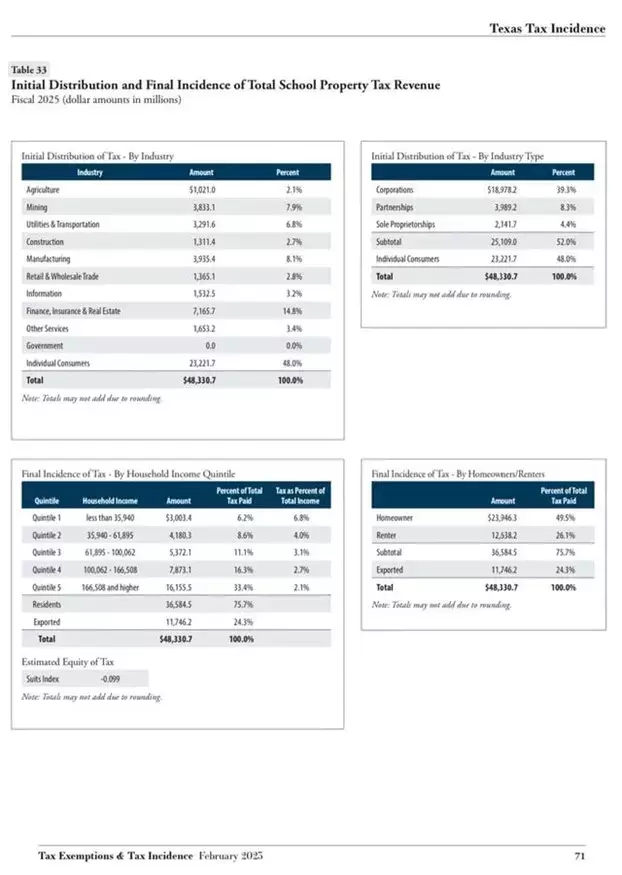

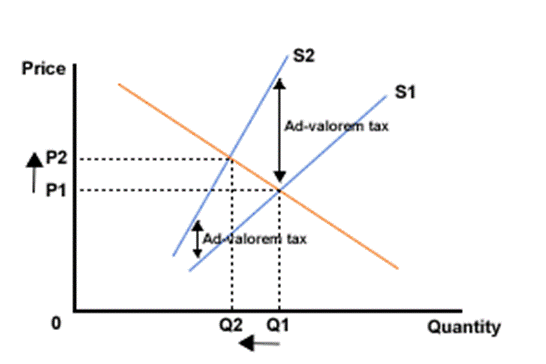

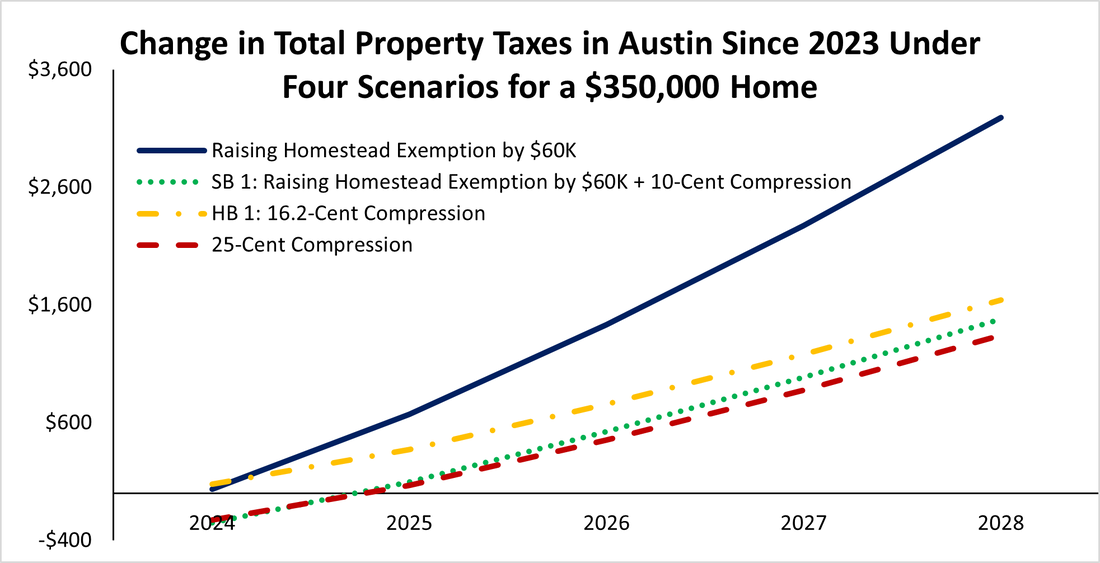

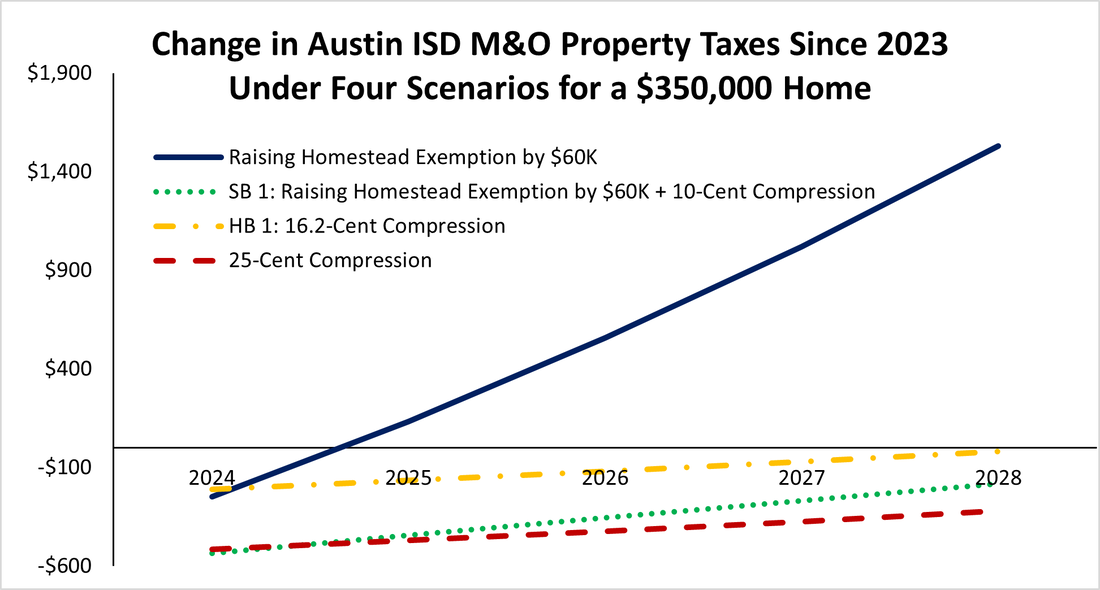

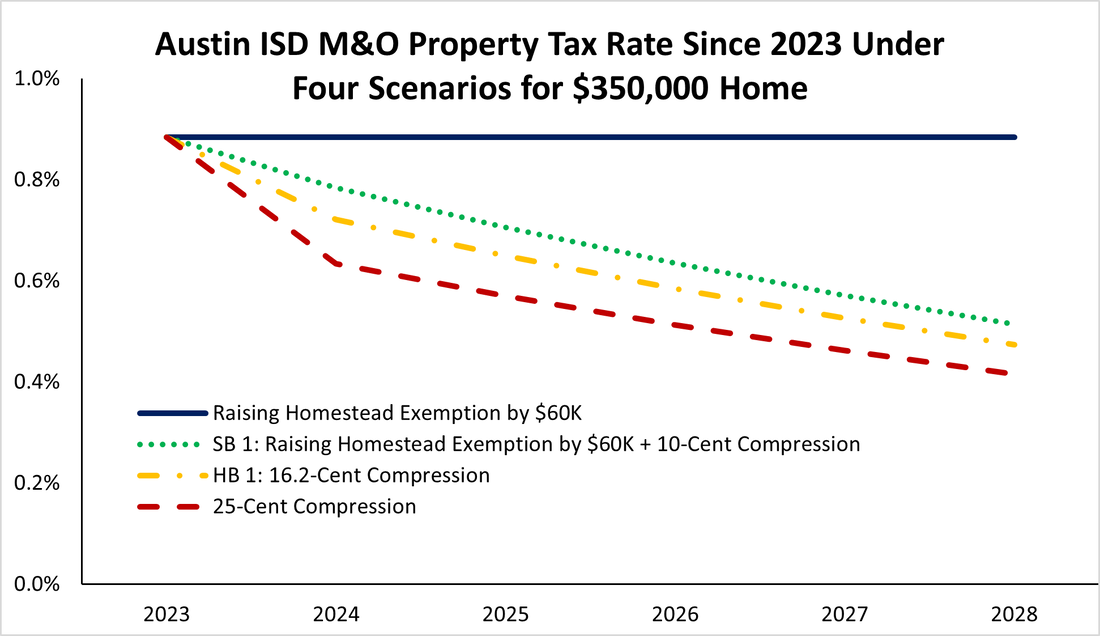

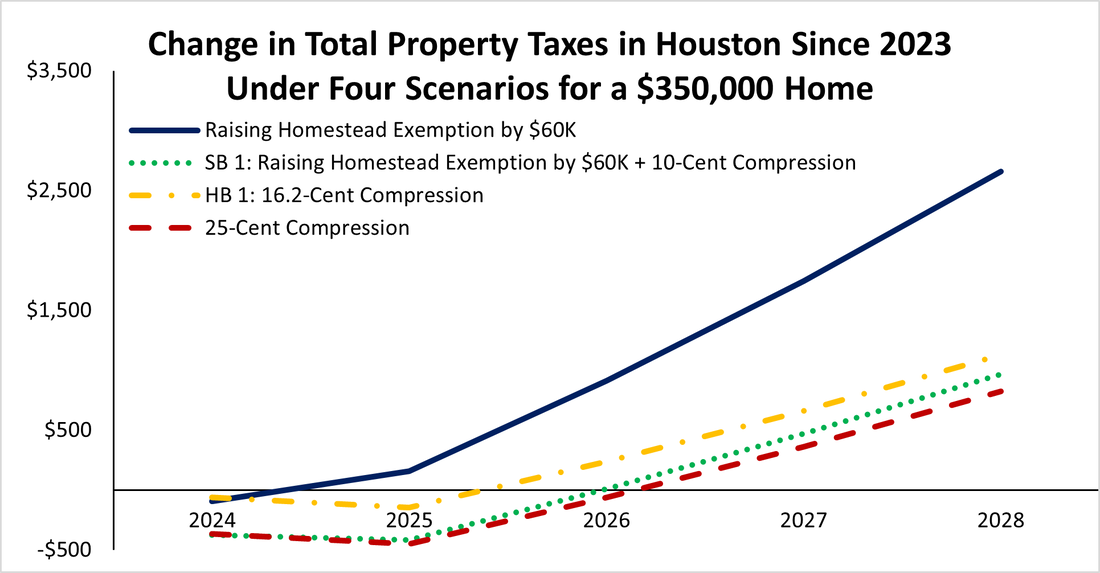

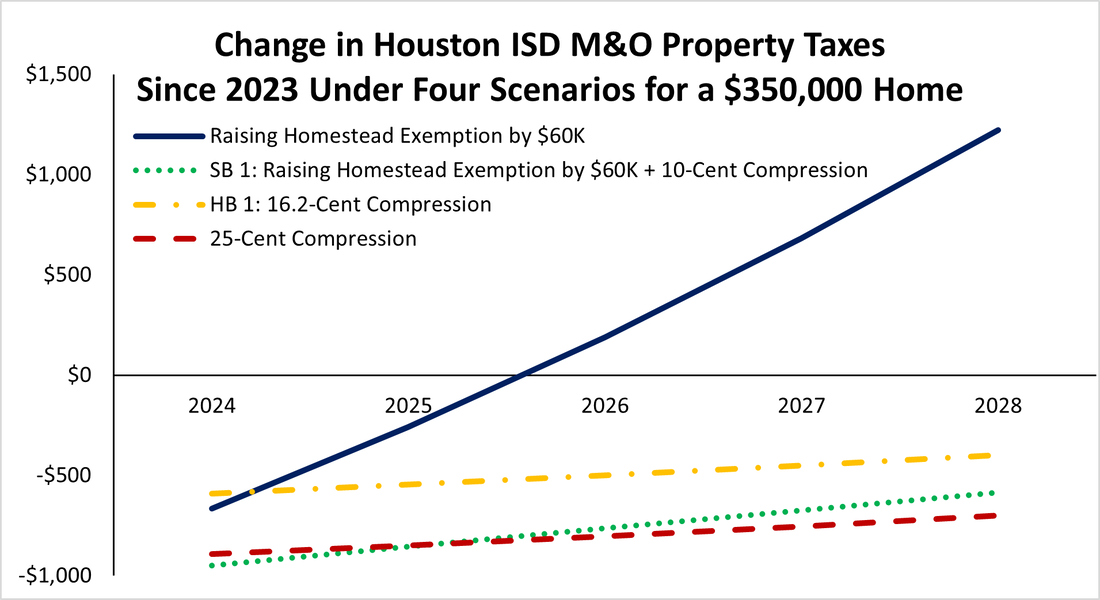

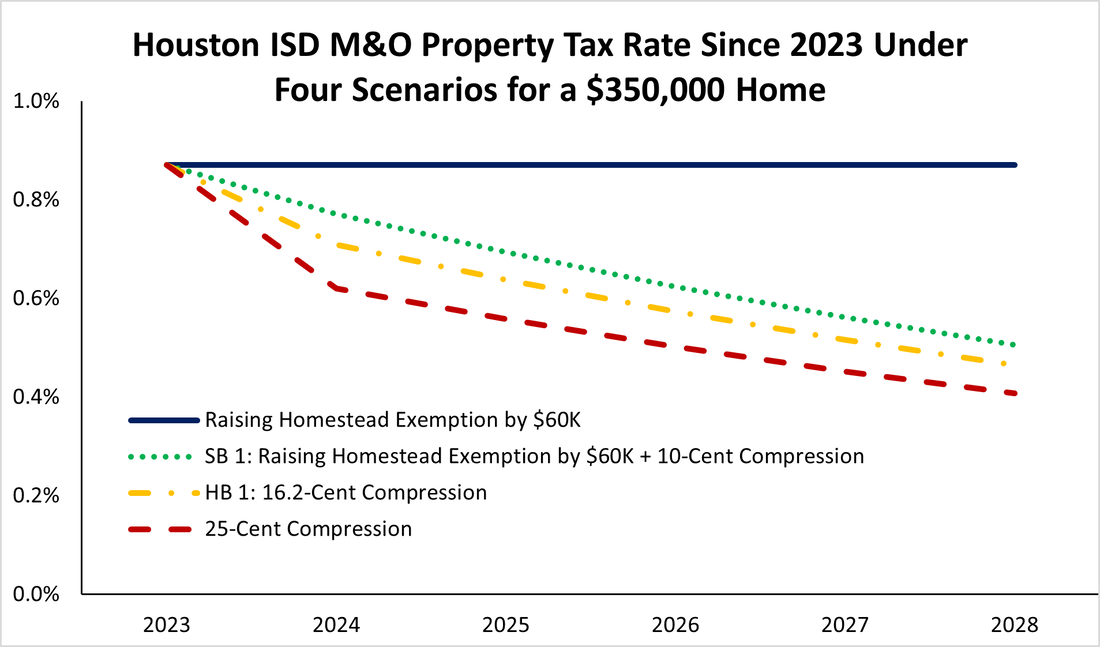

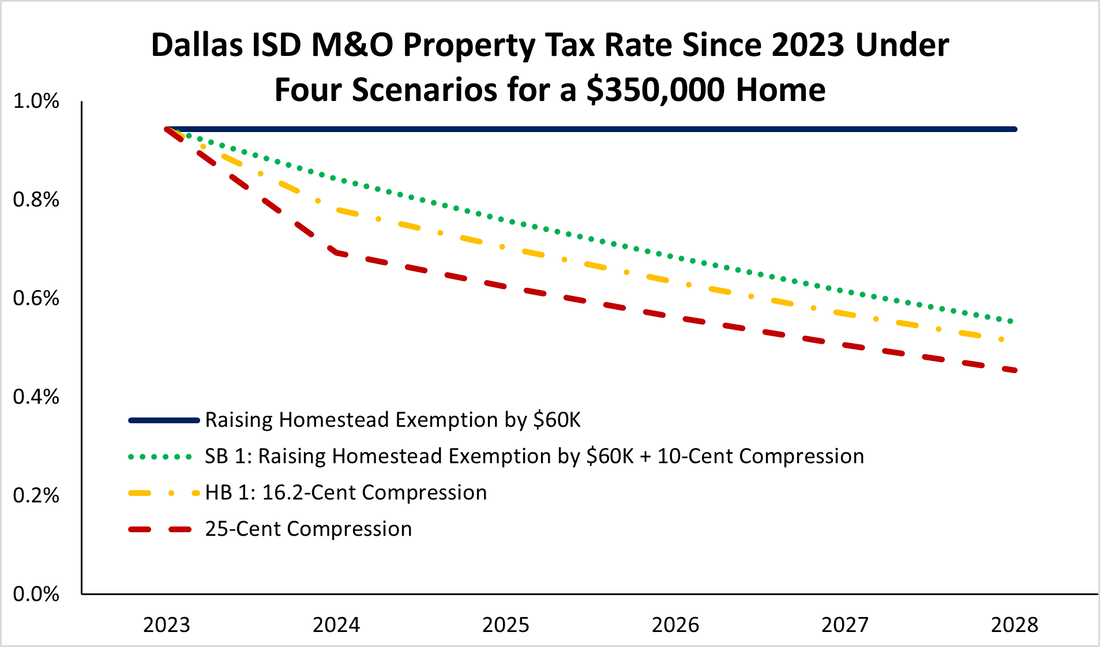

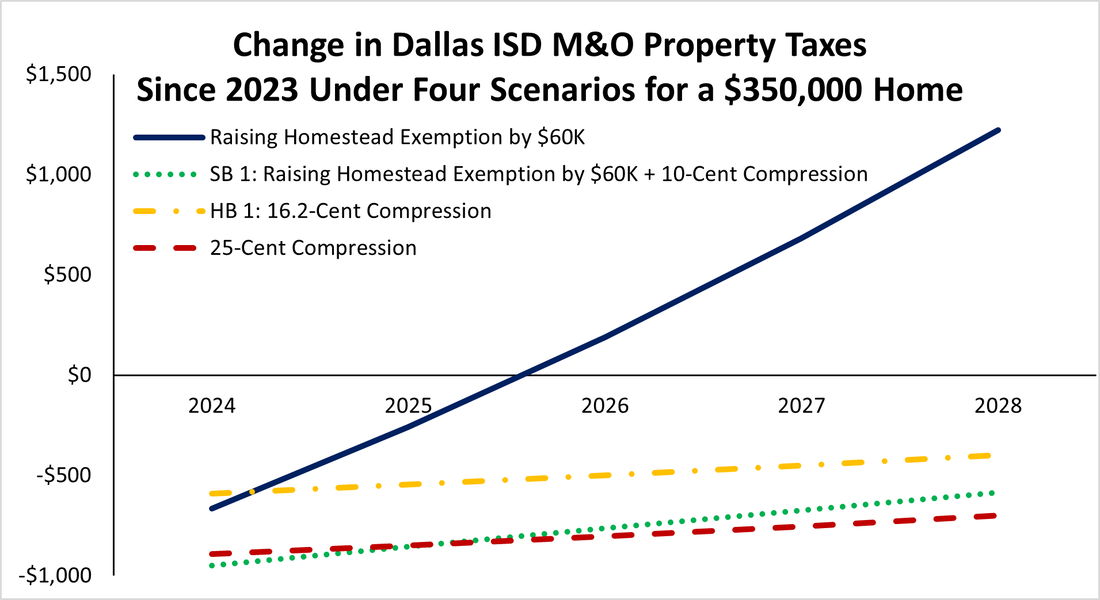

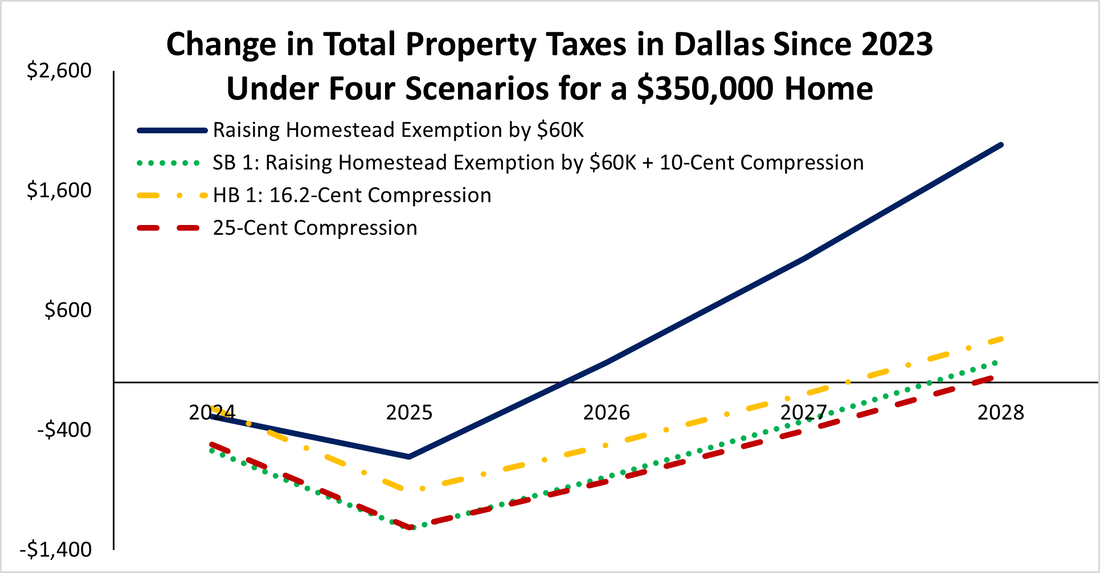

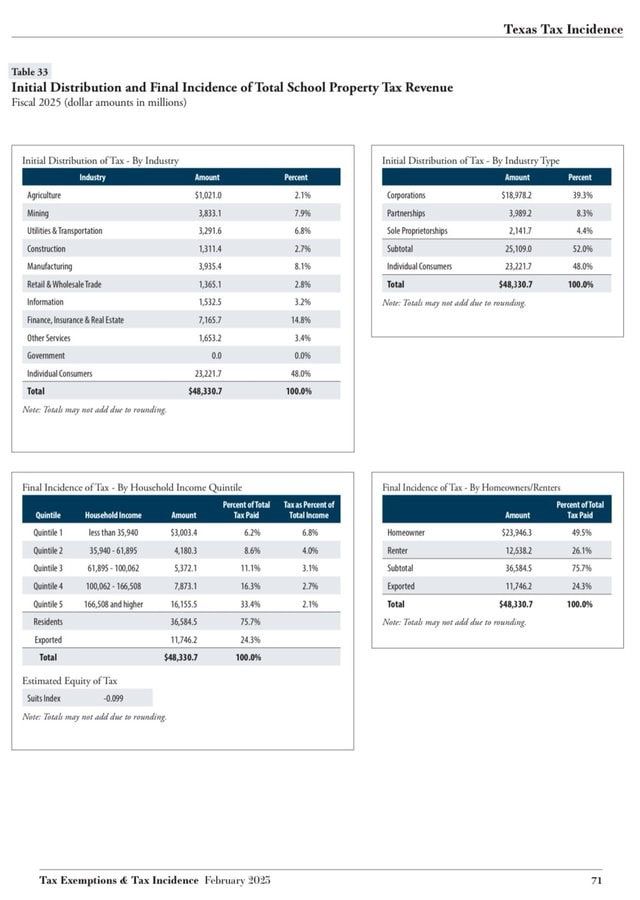

The good news is that state officials in Texas have been debating how to provide one of the largest tax cuts in the state’s history and were even talking about eliminating school maintenance and operations (M&O) property taxes. But that good news withered away in the second special session of the 88th Texas Legislature, as the amount looks to be only about $12.7 billion in new relief (an additional $5.3 billion to maintain past relief was passed in HB 1 budget) of the at least $33 billion surplus. And given that the largest property tax cut was $14.2 billion for 2008-09, the state would need to provide $21 billion in new relief this time for it to be the largest tax cut in Texas history, so Texans could have the same purchasing power of relief as they had then. While there has been a lot of debate on how the state should provide property tax relief of school district maintenance and operations (M&O) property taxes, which comprise more than 40% of total property taxes collected by local governments across the state, the best way to provide the most relief to everyone is through compression. This is simply using state dollars—mostly through sales taxes—to buy down school district M&O property tax rates that the state mostly controls with its school finance formulas. Instead, the compromise between the House and Senate, which Governor Abbott looks poised to sign, is a watered-down approach that provides too little in relief—just $12.7 billion in new relief in SB 2 (88(2))—because they chose to spend too much. And there is too little in compression with just $7 billion for 10.7 cents per $100 valuation in reduction for school M&O property taxes. The rest is a combination of raising the homestead exemption for school districts by $60,000 to $100,000, limiting non-homestead appraisal growth to 20% for three years, and requiring three directors on appraisal district boards to be elected with counties that have a population of 75,000 or more. The next part of the package is SB 3 (88(2)), raising the franchise tax exemption for gross revenue to $2.45 million from $1 million. The final piece is HJR 2 (88(2)), which puts this package (except the compression) on the November 7, 2023, ballot for voters to consider approving. While it is good that there is so much going to tax relief, this package will make the tax system more complicated, make it more difficult to eliminate school M&O property taxes, contribute to higher school M&O property tax rates, and shift the burden around as homesteads and small businesses are chosen as the winners while renters and other employers are losers. The government should not be in the business of socially engineering people’s lives through the tax code by picking winners and losers, and this is exactly what this package does. Paths to Eliminating Property Taxes I have long researched and published on eliminating property taxes in Texas. There are different ways to do it, but the one discussed most recently by Texans for Fiscal Responsibility and Governor Abbott was the buy-down of school M&O property taxes until they’re eliminated, something I supported in a paper I co-authored in 2018. The plan has been through multiple iterations. My July 2021 co-authored paper looked at this buy-down approach of using 90% of state surplus dollars above a stricter spending limit of population growth plus inflation to compress school M&O property tax rates until they are zero within about a decade; the other approach explored in this paper was of tax reform that would broaden the sales tax base to eliminate those taxes immediately, without raising the rate, based on a dynamic economic model. Both of these were built on a strong spending limit, given spending is the ultimate burden of government on taxpayers. The latest was a December 2022 co-authored paper where we address the affordability crisis in Texas and how the buy-down plan would help with this while providing more economic growth. I also wrote a 2023 paper updating this based on how quickly this could be done if a frozen budget with zero growth was used to provide more surplus funding to eliminate these property taxes. I also wrote another 2023 paper noting how there is no need to be fearful about a recession or reduced revenue as there would be the need for spending restraint or cuts, plenty of money in the rainy day fund, or excess reserves held by school districts to address any shortfall to maintain the relief and fund public education. Adding to this research were two professors at Rice University who, in 2018, also studied different reforms of the buy-down approach and the sales tax expansion approach to eliminate school M&O property taxes. They found that these approaches would provide substantial benefits to the state in terms of increased economic growth and job creation. After reviewing different options for the buy-down approach, compression is best because everyone benefits, including from the dynamic effects of more growth, more jobs, and lower prices. It’s also the only way that’s being discussed today to get the school M&O property tax rate to 0%. Another approach to provide property tax relief was pushed by the Senate this year and looks to be included in the bill passed in the second special session: raising the homestead exemption from $40,000 to $100,000. But this approach will never eliminate those taxes and will push the burden of funding spending to everyone else, making the system less equitable while quickly evaporating any relief from appraisal growth and making the path to elimination harder because rates will rise from it when school spending increases. Given the different approaches discussed this year by the House and governor and then the Senate and lieutenant governor, I did an analysis of the median valued home in Texas of $350,000 in Austin, Houston, and Dallas. I used the tax rates for each of these locations and had the home increase in value by 10% per year, which is the maximum growth for a homestead under current law. I didn’t change anything else to provide an apples-to-apples comparison of a tax reform in 2023 to estimate what would happen over the next five years given a 1) $60,000 increase in the homestead exemption, 2) SB 1 (88(1)) with $60,000 increase in the homestead exemption and 10-cent compression (similar to tax relief package in second special session), 3) HB 1 (88(1)) with 16.2-cent compression, and 4) what would be largest tax cut in Texas history of $21 billion with a 25-cent compression. I should note that this modeling is just on a homestead, so it doesn’t account for the much more broad-based effects of the compression scenarios. Austin The following three charts are for Austin, including Austin ISD, to see what these four scenarios would look like given the assumptions above in each year. The first chart shows what would happen for total property taxes (i.e. ISD, city, county, and special purpose district property taxes) under these scenarios compared with the total tax paid of $5,945 for a $350,000 home in Austin. The results show that SB 1 and the 25-cent compression are similar; however, both of them would have only one year of lower total property taxes until 2025, when the amount paid would exceed that of 2023. The second chart shows similar results as SB 1 and the 25-cent compression have the greatest effects on the 2023 ISD M&O property taxes of $3,089. However, HB1 also provides relief until 2028, when the amount paid would exceed that of 2023. But, more importantly, given these are only homesteads and don’t account for families who pay rent or own a business, the third chart’s example shows that HB 1 with 16.2-cent compression and the 25-cent compression cut the tax rate the most over time, as this compression in just 2024 continues to buy down the rate as values increase by 10%.    Houston The following charts are for Houston, with similar results for each of the scenarios.    Dallas The following charts are for Dallas, with similar results.    In my conversations with CBS News Texas, ABC 13 Houston, and The Texan, I recently explained how compression is the gold standard to eliminate school M&O property taxes. I also recently wrote[VG1] how the Texas Legislature had the largest spending increase in Texas history this session, thereby not providing enough in property tax relief. I argued that Governor Abbott should veto the budget or at least $8 billion of budget items and use it for compression so that Texans get record relief. But that did not happen. It should be noted that compression will help renters. The Texas comptroller’s report (see Table 33 below) finds that 26% of school property taxes is passed along to renters. Businesses submit 52% of those taxes, but people pay for them through higher prices, lower wages, fewer jobs, and higher rent. Simple supply and demand shows that the property taxes would rotate the private market supply of housing leftward, thereby raising rents and lowering the quantity supplied compared with the free market. In other words, the market does set the rents, but that market is distorted by property taxes, so removing those school taxes would help push down rents through competition. When the landlord has a vacancy and is paying lower property taxes, then she will lower the rent given lower cost to attract tenants. It may not happen overnight, but it will as that’s how competition works, and those businesses that don’t will be forced out of the market through losses. This wouldn’t just be a shift in supply of housing that would reduce rents; that would happen some when this tax is cut and certainly when it’s eventually eliminated, but that’s not the only way.  The following chart shows that there’s movement down the demand curve as the supply curve corrects to the private supply curve (S1) rather than the distorted supply curve (S2) with the ad-valorem property tax, which will lower prices and increase the quantity supplied. This is through competition that will happen as consumers will have more negotiating power and landlords will want to rent out every unit but won’t if they don’t lower their rents, as their competition will because their costs have been reduced.  From the fact that property taxes are going down, there’s a reduction in cost by the landlords, so they have the ability to get more renters at a lower rent. As renters know, if property taxes don’t go down, they will go to another location—hence more consumer power. The consumer has much power in every market if they choose to wield it, especially when government gets out of the way. Again, it wouldn’t change rents overnight, as many are in leases, but it would over time. One of the issues contributing to the affordability crisis in Texas, especially for lower-income folks, is skyrocketing property taxes. Any relief would be most appreciated by 100% of property holders through compression. Lowering school M&O property tax rates through compression is the best path for everyone to benefit from lower taxes, more economic growth, and tax rates that would go to zero. Many groups shown in the page below have already stated their support for the buy-down plan, which was supported by the governor; the House passed much of it, though that was mostly thrown out in the final package. And they needed to add HB 16 (88(2)) by State Rep. Briscoe Cain, which would put in statute the buy-down plan to zero, along with his HB 17, which would impose spending limits on local governments.  Conclusion

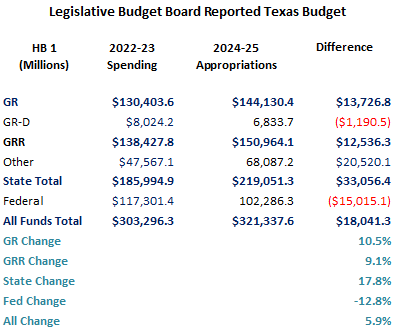

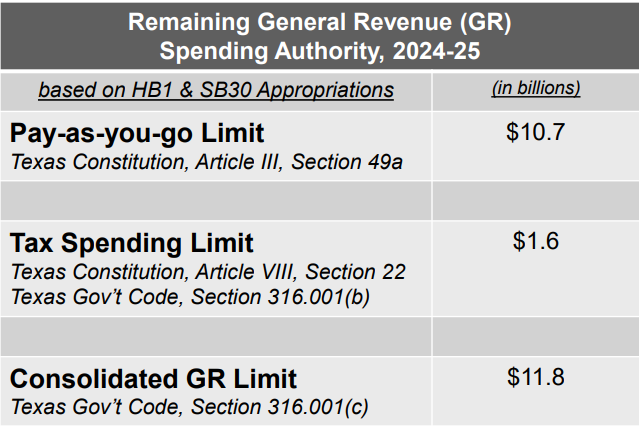

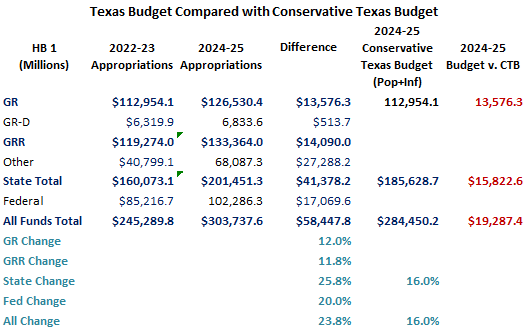

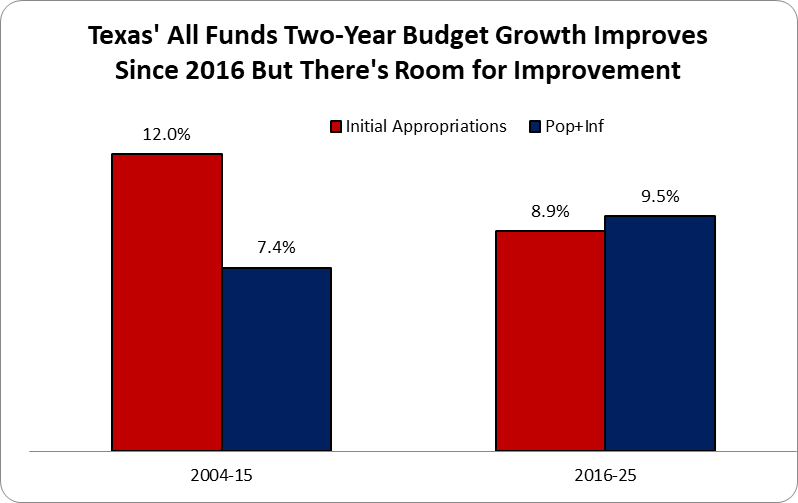

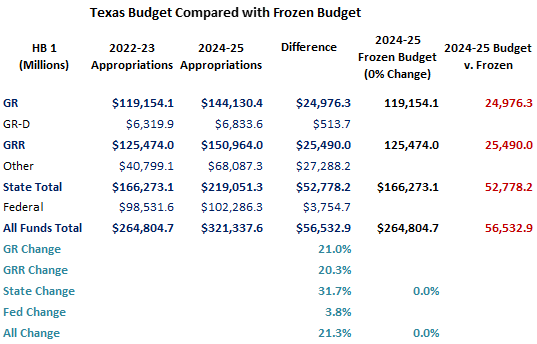

At the end of the day, I’m glad Texans are talking about property tax relief. Other states have been cutting taxes, so Texas can’t sit back and be competitive with other states without spending less and cutting taxes, as corporate welfare makes the problems worse. The Legislature unfortunately passed a revamp of the expired Chapter 313 in HB 5 during the regular session. This new version, called Chapter 403, provides property tax abatements issued by school districts to mostly big businesses. Fortunately, when school district M&O property taxes are eliminated, this corporate welfare will be eliminated, too. There are so many reasons to eliminate property taxes. Texas will be an economic juggernaut! And what’s maybe the most important is that Texans will have more of their right to own property preserved instead of renting from the government forever with this immoral wealth tax known as property taxes. Raising the homestead exemption might be a part of the final deal, but we should remember that it picks winners and losers, is not sound tax policy, and has been tried three times (1997, 2015, and 2021) without substantial reductions in those taxes paid. I’m okay with broadening the sales tax base and eliminating school M&O property taxes immediately and using surplus dollars above a stricter spending limit to buy down sales taxes over time. This would also broaden the sales tax base for local governments, which should use those funds to buy down their own property taxes and limit their spending with a restrictive limit like the state’s based on population growth and inflation to use surplus dollars to buy down the rest until they are zero. But there isn’t the political will yet to take this approach, so the best way right now is the buy-down path for school property taxes by the state and local government buying down their own could happen over the next decade for the eventual elimination of all property taxes in Texas. The way to do this is by sufficiently reining in government spending, which the Legislature did not do this session—thereby wasting an unprecedented opportunity to do something big. Eliminate school property taxes first, then find a way to eliminate the rest. My preference is to limit all local government spending to the state’s spending limit based on population growth and inflation, and use 90% of their surpluses to buy down their own property taxes until they are zero. This is a path to giving Texans their God-given right to own property. Get tax relief done for Texans! Stop renting, start owning! Originally published by Texans for Fiscal Responsibility.  Unfortunately, Texas Governor Greg Abbott (R) signed the Texas budget passed by the 88th Texas Legislature with largest spending increases, largest corporate welfare increases, and largest social safety net increases without the largest property tax cuts in Texas history. State officials can claim that the budget increases by less than the rate population growth and inflation using the data in the table below by the Legislative Budget Board.  But those calculations use fuzzy math as they're based on inflating the 2022-23 base budget of general revenue not dedicated by the constitution and consolidated general revenue with more spending then increasing it by the rate of population growth times inflation of 12.33% (determined by the average of population growth times inflation over the last two years and the upcoming two years) compared with 2024-25 appropriations which will be higher later when the supplemental bill passes. These calculations are then spending-to-appropriations which are like comparing apples with oranges, not appropriate accounting. Even with these calculations, the Legislative Budget Board shows that there is $10.7 billion in tax revenue remaining, $1.6 billion available under the constitutional spending limit using general revenue not dedicated by the constitution, and $11.8 billion available under the 2021 spending limit using consolidate general revenue using general revenue and dedicated general revenue.  The charts below are more accurate ways to evaluate the budget growth from an appropriations-to-appropriations approach for an apples-to-apples comparison. Understanding that any growth in the budget means an expansion of government, there are two strong arguments: 1) Freezing the budget in inflation-adjusted per capita terms using the rate of population growth plus inflation (i.e., Conservative Texas Budget and responsible budget approach in other states), which was 16% over the last two fiscal years, is appropriate as it grows slower than the economy over time. This approach excludes $13.3 billion in COVID-related funding in the first biennium and excluding new and old property tax relief amounts of $6.2 billion ($100 million in new relief) in the first period and $17.6 billion ($12.3 billion in new relief and $5.3 billion in old relief) in the second period to not include one-time federal funding and amounts that don't grow government.  Using the CTB approach above, here's how the budget has improved since implementation of the CTB started with the 2016-17 budget. This looked much better before the current 2024-25 budget, but the massive growth of the current budget raised the growth of initial appropriations even as the rate of population growth plus inflation rose slightly during the latter five budget period. If the growth of the budget is not controlled, it will soon surpass the rate of population growth plus inflation like it did during the prior six budget periods.  2) Freezing the budget with zero growth as the budget is already too big (i.e., Frozen Budget), including COVID-related funds in the first period and new and old property tax relief amounts in both periods.  Both of these approaches show that while the general revenue-related (GRR) funds amount is below the rate of population growth and inflation (either plus or times) for the CTB approach, the broader measures of state funds and all funds that better represent the burden of government spending on taxpayers are well above either metric. And when using the Frozen Budget approach, the only budget amount below either rate of population growth and inflation is federal funds.

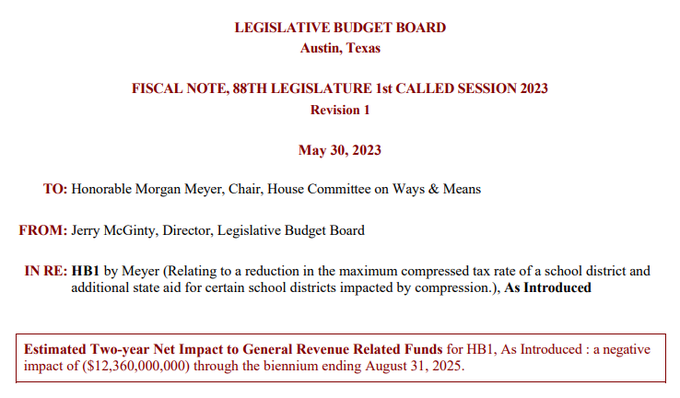

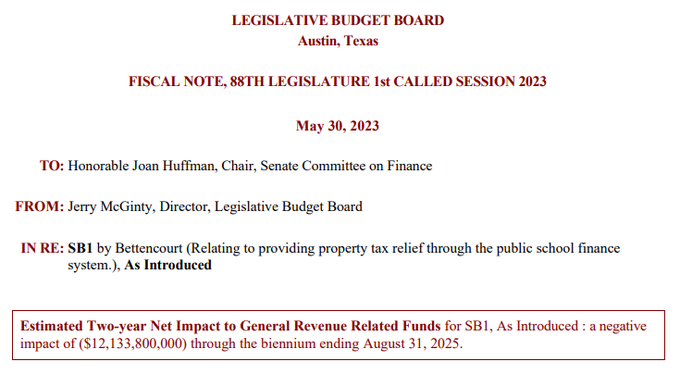

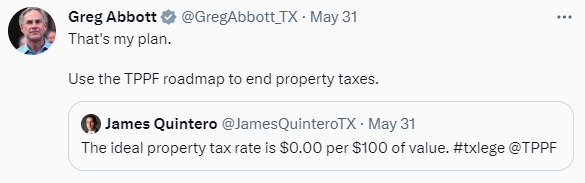

In other words, they are using fuzzy math when it comes to the budget and property tax relief. This looks much more like what would be done in California rather than Texas. This is not what Texans want or expect from their elected officials. If this continues, Texas will be California soon. There’s time to turn some of this around with at least passing more for property tax relief that does it correctly (here's why) for everyone through compression of school M&O property taxes on their path to zero. It would be great if they could get to $21B in new relief, which is the $14.2 billion in property tax relief provided in 2008-09 adjusted for inflation, instead of the $12.3B currently discussed but that looks unlikely now so it won’t be the largest property tax relief in Texas history. The red state of Texas must not sit back on its laurels. The populist trend must not continue. Do what's in the best interest for everyone which is limiting or cutting government spending, taxes, and regulations so that there's more freedom for people to do what's in their best interest and let people prosper. It's great to see that state officials in Texas are debating how to provide one of the largest tax cuts in the state's history. Unfortunately, that amount is only about $12.3 billion in new relief (an additional $5.3 billion to maintain past relief) of the at least $33 billion surplus. And given that the largest property tax cut was $14.2 billion for 2008-09, the state would need to provide $21 billion in new relief this time for it to be the largest tax cut in Texas history so that Texans can have the same purchasing power of relief as in 2008. While there's a lot of debate of how the state should provide property tax relief of school district maintenance and operations (M&O) property taxes, the best way to provide the most relief to everyone is through compression, which is using state dollars mostly through sales taxes to buy down school district M&O property taxes that the state mostly controls with its school finance formulas, and it is the best way being discussed to get those taxes to zero. The Texas House already passed HB1 in the first special session that provides $12.4 billion for a 16.2-cent (per $100 valuation of property) compression of ISD M&O property taxes.  Meanwhile, the Texas Senate already passed SB1 that provides $12.1 billion for 10-cent compression and a $60K increase in homestead exemption to $100K for ISD M&O property taxes.  Texas Governor Greg Abbott then tweeted that his plan is the plan outlined by the Texas Public Policy Foundation which uses state surplus dollars for compression of ISD M&O property taxes each session until they are zero.  I’m very familiar with this plan as I co-authored the original version with my former colleagues at TPPF in 2018. The plan has been through multiple iterations. My July 2021 co-authored paper looked at this buy-down approach of using 90% of state surplus dollars above a stricter spending limit of population growth plus inflation to compress school M&O property taxes until they are zero within about a decade or a tax reform that would broaden the sales tax base to eliminate those taxes immediately without raising the rate based on a dynamic economic model. And the latest was a December 2022 co-authored paper where we address the affordability crisis in Texas and how the buy down plan would help with this while providing more economic growth.  I also wrote a 2023 paper updating this based on how quickly this could be done if a frozen budget with zero growth was used to provide more surplus funding to eliminate these property taxes. And I also wrote another 2023 paper noting how there is no need to fear about a recession or reduced revenue as there would be the need for spending restraint or cuts, plenty of money in the rainy day fund, or excess reserves held by school districts to address any shortfall to maintain the relief and fund public education.  Two professors at Rice University also studied different reforms in 2018 of the buy down approach and the sales tax expansion approach to eliminate school M&O property taxes and they found that these would provide substantial benefits to the state.  Compression is best because everyone benefits, including from the dynamic effects of more growth, more jobs, and lower prices, and it's the only way that's being discussed today to get the school M&O property tax rate to 0%. The other path by the Senate is to raise the homestead exemption from $40,000 to $100,000 but that will never eliminate those taxes and will push the burden of funding spending to everyone else making the system less equitable while evaporating any relief quickly from appraisal growth and making the path to elimination harder .because rates will rise from it. Given the different approaches being discussed by the House/Governor and Senate/Lt. Governor, I did an analysis of the median valued home in Texas of $350,000 in Austin, Houston, and Dallas. I used the tax rates for each of these locations and had the home increase in value by 10% per year, which is the maximum growth for a homestead under current law. I didn't change anything else to provide an apples-to-apples comparison of a tax reform in 2023 to estimate what would happen over the next five years given a 1) $60,000 increase in the homestead exemption, 2) SB 1 with $60,000 increase in the homestead exemption and 10-cent compression, 3) HB 1 with 16.2-cent compression, and 4) what would be largest tax cut in Texas history with a 25-cent compression. I should note that this modeling is just on a homestead so doesn’t account for the much more broad-based effects of the compression scenarios. Austin The following three charts are for Austin, including Austin ISD, to see what these four scenarios would look like given the assumptions above in each year. The first chart shows what would happen for total property taxes (i.e. ISD, city, county, and special purpose district property taxes) under these scenarios compared with the total tax paid of $5,945 for a $350,000 home in Austin, which the results show that SB 1 and the 25-cent compression are similar but both of them would have only one year of lower total property taxes until 2025 when the amount paid would exceed that of 2023. The second chart shows similar results as SB 1 and the 25-cent compression have the greatest effects on the 2023 ISD M&O property taxes of $3,089 but HB1 also provides relief until 2028 when the amount paid would exceed that of 2023. But, more importantly, given these are only homesteads and don't account for families who pay rent or own a business, the third chart shows that HB 1 with 16.2-cent compression and the 25-cent compression cut the tax rate the most over time as this compression in just 2024 continues to buy down the rate as values increase by 10% in this example.    Houston The following charts are for Houston with similar results for each of the scenarios.    Dallas The following charts are for Dallas with similar results.    I recently explained how this would work and how compression is the gold standard with the only meaningful way to eliminate school M&O property taxes that are being discussed now in my conversation on CBS News Texas. I also recently wrote how the Texas Legislature had the largest spending increase in Texas history this session thereby not providing enough in property tax relief. I argued that Gov. Abbott should veto the budget or at least $8 billion of budget items and use it for compression so that Texans get record relief.  It should be noted that compression will help renters. The Texas Comptroller's report (see figure below) finds that 26% of school property taxes are passed along to renters, and businesses submit 52% of those taxes but people pay for them through higher prices, lower wages, fewer jobs, and higher rent. Simple supply and demand shows that the property taxes would rotate the private market supply of housing leftward thereby raising rents and lowering the quantity supplied compared with the free market. In other words, the market does set the rents but that market is distorted by property taxes so removing those school taxes would help push down rents through competition. When the landlord has a vacancy and is paying lower property taxes, then she will lower the rent given lower cost to attract tenants. It may not happen overnight but it will as that’s how competition works, and those biz that don’t will by forced out of the market through losses.  This wouldn't just be a shift in supply of housing that would reduce rents, which would happen some when this tax is cut and certainly when it’s eventually eliminated, but that’s not the only way. There’s also movement down the demand curve as the supply curve corrects to the private supply curve (S1) rather than the distorted supply curve (S2) with the ad-valorem property tax which will lower prices and increase the quantity supplied. This is through competition which will happen as consumers will have more negotiating power and landlords will want to rent out every unit but won’t if they don’t lower their rents as their competition will because their costs have been reduced.  From the fact that property taxes are going down there’s a reduction in cost by the landlords so they have the ability to get more renters at a lower rent. And renters would know this as property taxes go down or they will go to another location. Hence, more consumer power, which the consumer has much power in every market if they choose to wield it, especially jelly when govt gets out of the way. It wouldn’t change rents overnight as many are in leases, but it would over time. One of the issues contributing to the affordability crisis in #Texas especially for lower-income folks is skyrocketing property taxes. Any relief would be most appreciated by 100% of property holders through compression. Lowering school M&O property tax rates through compression is the best path for everyone to benefit, not only from lower taxes but also more economic growth, and for those taxes to go to zero. Many groups have already stated their support for the buy down plan, which is also supported by the Governor and the House has passed much of it though they need to add HB 5 by Rep. Briscoe Cain which would put in statute the buy down plan to zero.  At the end of the day, I'm glad Texans are talking about property tax relief as other states have been cutting taxes so Texas can't sit back and be competitive with other states without spending less and cutting taxes, as corporate welfare makes the problems worse. The Legislature unfortunately passed a revamp of the expired Chapter 313 in HB 5 during the regular session that is now called Chapter 403, which provides property tax abatements issued by school districts to mostly big businesses. Fortunately, when school district M&O property taxes are eliminated, this corporate welfare will be eliminated, too.

There are so many reasons to eliminate this tax. Texas will be an economic juggernaut! And what's maybe the most important is that Texans will have more of their right to own property preserved instead of renting from the government forever from this immoral wealth tax known as property taxes. Raising the homestead d emotion might be a part of the final deal, but we should remember that the homestead exemption picks winners and losers, is not sound tax policy, and has been tried three times (1997, 2015, and 2021) without substantial reductions in those taxes paid. 'm okay with broadening the sales tax base and eliminating school M&O property taxes immediately and using surplus dollars to buy down sales taxes over time. This would also broaden the sales tax base for local governments which should use those funds to buy down their own property taxes and limit their spending with a restrictive limit like the state's based on population growth and inflation to use surplus dollars to buy down the rest until they are zero. But there isn’t the political will yet do this approach so the best way right now is the buy down path for school property taxes by the state and local government buying down their own could happen over the next decade for the eventual elimination of all property taxes in Texas. The time to start doing this is now. Get tax relief done for Texans!  Texas’ 88th regular legislative session, sine die as of Memorial Day, will be remembered as the one that got Texas closer to looking like California and less like the leading pro-market and limited government Lone Star State.

Instead of the desired “largest property tax cut in Texas history,” school choice, and spending restraint that would best let people prosper, legislators passed the largest increases in spending, corporate welfare, and safety nets in state history. Texas taxpayers can only hope that Gov. Greg Abbott’s (R) just-called special session will help with property tax relief but there will need to be more special sessions for universal school choice and other pro-prosperity priorities. The newly passed total budget for the upcoming two-year period amounts to $321 billion, which is a 21.3% increase from what was initially appropriated in the prior period. Excluding federal funds, state funds increased by 31.7% to $219.1 billion. These are the largest increases in recent history and likely ever. And both are substantially above the rate of population growth plus inflation of 16% over the last two fiscal years. In short, legislators passed massive budget increases which aren’t conservative or responsible and will make it difficult to sustain these expenditures over time. Making matters worse, the Legislature provides over $10 billion in new corporate welfare, the largest amount in state history. This includes renewal of property tax abatements by school districts, HB 5, that had died in December 2022, money for the governor’s Texas Enterprise Fund, and subsidies for natural gas projects, movie production, broadband projects, water projects, state parks, and more. And much of this will be on the ballot this November to create new funds to spend on these efforts, which voters should reject. Instead, these expenditures should be done in the normal budget process as constitutionally dedicating these taxpayer dollars will remove them from under the constitutional spending limit, allowing the state to spend even more. Texans were quick to celebrate the movement toward new property tax relief efforts, which is a major burden for property owners across the state. And with a surplus of $33 billion, there was the opportunity to do so by rightfully returning these over collected taxes. But those cuts never materialized in the wake of less effective solutions of appraisal caps and homestead exemptions taking precedence over the previously promised historical property tax cut. The gold standard for relief of school district maintenance and operations property taxes is through compression, which means that the state uses mostly sales taxes to buy down those property tax rates and thus tax collections by the most possible. And the amount should be about $21 billion, or 25-cent compression, in inflation-adjusted dollars to have the same purchasing power today as what was the largest property tax cut of $14.2 billion in 2008. This is a critical path to eliminating nearly half of the property tax burden in Texas so people can truly own their property instead of renting from the government forever. Still, any relief provided is made much less effective with the passage of HB5, which is just Chapter 313 revamped. HB5 gives more corporate welfare to big businesses by allowing school districts to give tax breaks to companies for new buildings, thereby choosing winners and losers among school districts affected. As school districts lose property tax funds at the hands of HB5, state funds must compensate for the loss on the backs of taxpayers across the state. These big spending, big corporate welfare, and no tax relief represent a potential turning point in the wrong direction that harms a robust economy. In the first called special session this week, there has already been a bill passed by the Texas House that would provide that opportunity by compressing school district M&O property taxes by 16.2 cents per $100 valuation with $12.4 billion. The Texas Senate has a proposal that would compress those taxes by 10 cents per $100 valuation and raise the homestead exemption by $60,000 to $100,0000 with $12.1 billion. So far, Gov. Abbott has said that the call was only for compression but Lt. Gov. Dan Patrick (R) has been pushing back. At the end of the day, compression is best as it helps everyone, is long-lasting as a share of taxable value, and, more importantly, is the only way to eliminate these taxes. But what’s still a problem is that these amounts are only about one-third of the $33 billion surplus, meaning the Legislature wants to spend more money than return to taxpayers. This is not the path to prosperity as at least $21 billion in new tax cuts is needed for this to be the largest property tax relief in Texas history. Lawmakers should prioritize responsible relief measures that encourage job growth and support initiatives that promote long-term economic prosperity by reducing spending, cutting taxes, and supporting prosperity. Originally published by The Center Square. Larry and Glenda Legler think the state should be using much of its nearly $33 billion surplus to give Texans a break on their property taxes.

Larry Legler said, "The state's got an ungodly amount of money that they need to do something with." But after months of promises to do that, Republican leaders still can't agree on the way to provide relief. "That's what's getting frustrating." Governor Greg Abbott prefers ending the school maintenance and operations or "M&O" portion of your property taxes over ten years. That portion alone is about 42% of your property tax bill. To make that happen, the state would shift sales tax, other state revenues, and surplus money to pay for public schools. That would allow the state to gradually reduce the rate for M&O property taxes until they're eliminated altogether. Vance Ginn, a conservative economist and president of Ginn Economic Consulting, has pushed this idea for years. "It's the only way that you can get to $0 school district property taxes is by buying down those rates because that rate can go to zero which zero out of a hundred-dollar valuation for a home is $0. And so that is still $0, and you've eliminated that tax." But Lt. Gov. Dan Patrick and the Texas Senate have a different plan. While it uses more state revenues and less property taxes to pay for schools, it would also increase homestead exemptions for most homeowners from $40,000 to $100,000. And for homeowners over 65, it would raise homestead exemptions from $70,000 to $110,000. Patrick said it would provide nearly double the savings for homeowners than the Governor's plan. CBS News Texas asked Patrick earlier this week if he doesn't support eliminating the school property tax. He said, "You can't get there. You only have sales tax to prop up a state of 30 to 35 to 40 million people the next decade. What happens when we have a decline and sales taxes go down? You'll have no money to pay your bills. You can't be a one-legged horse." Ginn disagreed. "The Comptroller said we're going to have about $27 billion in the rainy-day Fund. The rainy-day fund is there to cover unforeseen revenue shortfalls which would be exactly this sort of situation." Abbott said 30 business and other groups support his plan. The Leglers said because they're seniors, they prefer the plan from Patrick and the Senate. "Everything's gone sky high and when people can't get the medications they need, which is not our case, but many people we know, or they can't afford groceries, a loaf of bread at the grocery store, we got a problem." Both the House and Senate have approved different legislation, and until they pass the same bill, the Governor cannot sign it into law. Abbott will speak Friday about this, and other issues related to the regular and special legislative sessions. Originally published by CBS Texas. News: Property Taxes Primed for a Special Session After Appraisal Reform Dispute Stalls Out5/29/2023  State leaders promised “historic” property tax relief this session, but though it is near the finish line, it will not make it past the checkered tape before the body adjourns sine die on Monday.

Last summer, Gov. Greg Abbott called on the Legislature to appropriate “at least half” of the then-$27 billion projected budget surplus to provide “the largest property tax cut ever in the history of Texas.” The comptroller’s January Biennial Revenue Estimate increased that total to $32.7 billion in the state treasury and $27 billion in the Economic Stabilization Fund, also known as the state’s savings account. That’s a lot of tax dollars to disburse, and number one on Abbott’s list was property taxes — which was also high on the list of both chambers. But after a lengthy, attention-grabbing impeachment proceeding against Attorney General Ken Paxton on Saturday afternoon, the clock ticked on toward the midnight deadline to distribute the conference committee report for the last-remaining property tax proposal. And then, some Sunday evening scrambling on a last-minute deal turned out to be more smoke than fire — the House conferees announced the signing of a deal last night, and posted a picture of them waiting for the Senate’s conferees to come sign it, but that ultimately did not happen. Details of that blueprint have not been disclosed as both sides have kept their cards close to their chest. The Texan can confirm that plan included the $12 billion for rate compression, a $70,000 standard homestead exemption, a $100,000 elderly and disabled homestead exemption, and a 7.5 percent appraisal cap on all real property. After a hastily convened meeting with Lt. Gov. Dan Patrick and Abbott, Speaker Dade Phelan (R-Beaumont) made a beeline for the House dais and adjourned the body until Monday morning with no deal announced on marquee property tax relief. Discussions continued into Monday morning but no deal was struck — appraisal caps being the point of insurmountable disagreement. Abbott tacitly weighed into the debate, gesturing at putting rate compression above all else, but it did little to move the needle one way or the other. The Texas House passed a revamped version of Senate Bill (SB) 3 on May 19 — a plan that included $12 billion for new rate compression and the 5 percent appraisal cap on all property from its original plan. But it also included a $100,000 homestead exemption, double what the Senate included in its proposal. Ultimately, the two sides could not coalesce on a compromise; the House dug its heels in for an appraisal cap reduction and extension, while the Senate dug its heels in against it. The ramped-up homestead exemption was not enough to entice the upper chamber to swallow the appraisal cap pill. Lt. Gov. Dan Patrick has maintained it to be a total non-starter in the upper chamber. As passed by the House, SB 3 would have amounted to $16.3 billion in property tax curtailment, plus the $5.3 billion already in the budget to maintain previous levels of compression. Because of this stalemate, and the emphasis Abbott has placed on it, property tax relief is sure to be on the list of issues for the coming special session — expected, but not yet confirmed, to start Tuesday. Property tax relief was on the governor’s list of emergency items at the beginning of the session. Even with the appraisal reform stalemate, there is a starting point of common ground between the chambers. The 2024-2025 state budget, approved by both chambers over the weekend, earmarks $17.3 billion for rate compression — $5.3 billion to maintain previous levels and $12 billion to add to it. The budget has no line item for homestead exemption increases and the appraisal cap extension would not require any financial injection. When the two bodies reconvene, it’s unclear how this stalemate could be resolved other than both just throwing up their hands and moving forward only with the rate compression — the aspect they both agree on. The previous record for the largest property tax cut is $14 billion in the mid-2000s. Both chambers of the Legislature have said their plans surpass that line — including the $5.3 billion to maintain current levels. Critics of that claim — such as Vance Ginn, former chief economist for the Texas Public Policy Foundation — have set the line at $20 billion in today’s dollars accounting for inflation, and also say that the entire sum of dollars going toward property tax relief should be allocated to compression. On top of this, add in the fact that to maintain levels of compression next biennium, the state will have to allocate the same amount of money toward it. Otherwise, tax bills will jump. Before the House adjourned sine die, Lt. Gov. Dan Patrick issued a letter asking for Abbott to include the Senate’s property tax plan — a $70,000 standard homestead exemption, $30,000 elderly and disabled homestead exemption, a $25,000 business personal property tax exemption, and a business inventory tax credit — among a litany of other priorities. Despite the appraisal stalemate running out the clock on this session, the Legislature will quickly have another go at the issue and the chance to fulfill the promises made before and during the 88th regular session. Originally published by The Texan.  Lt. Gov. Dan Patrick, along with several senators, announced a new bill package this week designed to reduce property taxes through several different methods.

Sens. Paul Bettencourt (R-Houston), Tan Parker (R-Flower Mound), Bob Hall (R-Rockwall), Joan Huffman (R-Houston), and Charles Perry (R-Lubbock) joined Patrick in a press conference on March 14. The package included three bills that would offer a combined estimated $16.5 billion in property tax relief. Lt. Gov. Patrick opened the press conference and invited Sen. Bettencourt to walk through the proposals, saying, “No one knows more about property taxes.” “What we have is tremendously good news for Texas taxpayers today,” Bettencourt said. “It’s important to know that we’re touching every taxpayer, every homeowner, every business owner, with needed tax relief,” Bettencourt claimed. “We’re spending the money as wisely as we can to get the maximum tax relief possible — and this plan has eye-popping numbers.” Senate Bill 3, filed by Bettencourt, would increase the homestead exemption for property taxes from $40,000 to $70,000 and allow seniors to deduct an additional $30,000. Bettencourt claimed the increases would save homeowners $800 to $1,000 over the course of the next two years. Bettencourt was also responsible for SB 4, which would contribute another $5.38 billion to buy down or “compress” school district property taxes, as explained in the bill analysis. The final bill in the property tax reduction package was SB 5, filed by Parker. The proposal would increase the “business personal property exemption from a $2,500 de minimis exemption to a $25,000 universal exemption.” Additionally, Parker’s bill would “provide eligible taxable entities a credit equal to 20% of the amount of ad valorem taxes paid during the period on which the report is based.” In the press conference, Parker claimed the bill would deliver $1.5 billion of relief to business owners. All of these measures were included in Lt. Gov. Patrick’s legislative priorities, as reported by The Dallas Express. Several of the property tax reduction measures have already garnered bipartisan support in the Senate. “We’ve never had $16.5 billion dollars to throw at property tax relief, and that is a record number, and it is well spent, and I believe it will be well received by the citizens and taxpayers of the great state of Texas,” noted Bettencourt. Patrick also explained, “The real key to save Texans’ taxes is to limit the size of government. That’s the key.” However, the proposals have disappointed some economic policy experts and taxpayer advocacy groups, who had hoped for different approaches to the tax burden. Vance Ginn, the president of Ginn Economic Consulting, directed The Dallas Express to a statement where he claimed, “[T]he Senate’s overly-complicated property tax package (#SB4, #SB4, #SB5) of $16.5B won’t put any property taxes on a path to elimination so Texans will continue to not have their right to own property.” Instead, Ginn urged that Texas needs to “[s]pend less and use surpluses to reduce school M&O [maintenance and operations] property taxes by state and other property taxes by local [governments] until all are ZERO so Texans can finally have the right to own their property and ultimately stop renting and start owning.” Similarly, Noah Betz, the executive director at the Huffines Liberty Foundation, explained to The Dallas Express, “We strongly believe this package falls short of being real property tax relief.” A statement from former Texas Senator Don Huffines added that “[a] major shortcoming of the Senate bills is that they do nothing to limit future increases in rates and levies by local governments, including school districts.” Tim Hardin, the president of Texans for Fiscal Responsibility, told The Dallas Express, “although we support any property tax relief we do not feel as though the Senate package goes far enough. … We would like to see property taxes be put on a path towards elimination.” Originally published at Dallas Express.  Overview

Texans for Fiscal Responsibility’s 3-Step Plan to Eliminate All Property Taxes

This paper was initially published by Texans for Fiscal Responsibility.  Texans are struggling with high property taxes, soaring prices, and stagnant income. As a result, most big-budget players favor some property tax relief. For instance, Gov. Greg Abbot declared his intention to use half of the actual surplus fund ($16.3 billion) for this initiative. Likewise, Lt. Gov. Dan Patrick revealed that property tax relief is his first legislative priority.

However, the economic outlook for 2023 is not encouraging. The IMF has announced a slowdown in the global economy, and a third of the world’s economy is expected to be in a recession in 2023. Moreover, the consensus among large financial institutions is that the U.S. will have a recession this year. Consequently, in such a bloomy scenario, caution is warranted on how to use Texas surplus funds prudently. Based on previous data, the Foundation finds that Texas has enough funds to use toward property tax relief, even in the worst-case scenario. Our three key findings are:

Considering that the State’s finances are robust enough to face a recession, the Foundation has proposed a path toward completely eliminating school districts’ maintenance and operations property taxes by using state surplus general revenue-related (GRR) funds to buy them down over time to zero. By following the spending limit of population plus inflation, assigning at least half of the current surplus and 90% of the future surplus thereafter, we should expect the elimination of school district M&O property taxes over the next decade. In case of any revenue shortfall, school districts could cover it with their reserve funds. By gradually replacing property taxes with more efficient sales taxes, more Texans would be able to boost their savings, afford a new home, and preserve their property while improving their ability to afford housing and other necessities. Originally published at TPPF.  In the last two decades, local property taxes in Texas have grown far faster than the average taxpayer’s ability to pay for them. Moreover, high property taxes are aggravating the housing affordability crisis by increasing the overall out-of-pocket cost of keeping a property. Therefore, we propose a buydown plan for property tax relief. Our simulation shows that the state can limit spending and use the resulting surplus state taxes collected to buy down school district maintenance and operations (M&O) property taxes until they are eliminated over the next decade. If, in addition, all local governments in Texas were to also limit spending and use the resulting surplus funds to reduce their property taxes, Texans could have substantial tax relief to mitigate this affordability crisis. Key Points

Americans are facing a housing affordability crisis – and Texans are no exception.

Texas families struggle to make ends meet with high inflation, stagnating wages, and rising mortgage rates. Add high property taxes to the equation, and it is not difficult to see why 1-in-2 Texans reported that they were behind on rent or mortgage payments and that eviction or foreclosure in the next two months is likely. Property tax relief is needed more than ever to help homeowners, renters, and businesses during these challenging times. For this purpose, the Texas Public Policy Foundation proposes a way to cut local property taxes substantially next year, and cut them nearly in half over the next decade. In Texas, the housing market is cooling as there were three months of supply of homes for sale relative to demand in September 2022, which is the highest since May 2020 after a couple of years of a very tight housing market. This cooling of the housing market resulted from mortgage rates topping 7%, a 20-year high that dramatically raises borrowing costs and monthly payments. Another contributing factor to the affordability crisis in Texas is high and rising local property taxes. Texas is blessed to have constitutional bans against a personal income tax and a statewide property tax. But while Texas has a costly gross receipts-style tax called a franchise tax, which should be eliminated, the most burdensome taxes discussed during soccer practices or business events are local property taxes. These taxes have nearly tripled over the past 20 years. And it’s wrong to think that property taxes are high because there is no personal income tax, as other states like Florida and Tennessee have much lower property tax burdens. The problem is excessive local government spending that requires more taxes. Property taxes are regressive. The Texas Comptroller’s office estimates that the lowest 20% of income earners will pay 6.9% of their total income in property taxes compared with 1.9% for the highest income quintile in 2023. Moreover, the Tax Foundation ranks Texas 11th in property tax collections per capita, 6th for its burden on homeowners, and 13th most burdensome to businesses, which is ultimately passed to consumers. Consequently, property tax relief is a top priority to help relieve some of the housing affordability issues. Reducing property taxes for Texans would keep more money in their pockets to satisfy their desires during a rising affordability crisis. To do so, the Foundation proposes eliminating nearly half of total property taxes. The proposal uses state general revenue-related funds to replace the maintenance and operations (M&O) property taxes partially funding independent school districts (ISD), which is about $60 billion per biennium. Specifically, most, if not all, surplus general revenue-related funds, which the Legislature has the most control over, above the state’s new state spending limit based on the rate of population growth plus inflation would be used to replace the ISD M&O property taxes each period until they’re eliminated. We calculate that this could happen in a decade. We use the average two-year growth rates over the last decade from 2012 to 2021, given that the state has a biennial budget for general revenue-related funds of 9.3% and a rate of population growth and inflation of 6.7%. We then use a reasonable 90% of this 2.6-percentage points surplus each biennium and half of the latest 2022-23 surplus of $27 billion to find this is achievable while fully funding public schools based on the current state-determined school finance formulas. With a record $27 billion expected surplus and another $14 billion likely in the state’s rainy day fund, the state has plenty of taxpayer money to fund limited government provisions within the normal taxes collected while returning surplus money to Texans. This is a historic opportunity to provide substantial property tax relief and more opportunities for businesses to move to Texas without costly incentive deals. The result would be Texas having a more robust economy, more job creation, more investments, and more opportunities to prosper so that Texans can be more able to afford their desired livelihood. Originally published at The Center Square  Americans are facing a housing affordability crisis—and Texans are no exception.