Did The Supreme Court Just Give The CFPB Too Much Power - Radio Interview on Lars Larson Show5/22/2024

1 Comment

Originally published at Daily Caller.

The Biden administration’s heavy regulation of America’s banking industry hinders economic growth and raises consumer costs. As FDIC Chair Martin Gruenberg faces scrutiny over the agency’s toxic workplace culture, lawmakers have a prime opportunity to address the broader issue of overregulation. Instead of focusing solely on internal misconduct, Congress should seize this moment to reduce the oppressive regulatory framework burdening financial institutions and the economy. The current banking regulatory environment is burdensome and counterproductive. Tens of thousands of pages of rules and guidance dictate banking operations and are treated as legally binding by U.S. regulators. Multiple agencies, including the Federal Reserve, FDIC, OCC, and CFPB often overlap and contradict each other, leading to confusion and inefficiency. This excessive regulation is an administrative burden and a significant barrier to economic prosperity. The Biden administration’s regulatory overreach is evident in the extensive presence of government examiners within banks. These examiners enforce ad hoc mandates that effectively dictate business decisions, and failure to comply can result in secret, unappealable ratings downgrades. This system creates a chilling effect, stifling innovation and growth. The annual stress tests conducted by the Federal Reserve impose the highest bank capital requirements globally. However, these tests rely on opaque models and unrealistic scenarios and are never subjected to public scrutiny. This significantly impacts how banks operate and adds to the regulatory burden. The lack of transparency undermines the credibility of regulatory agencies and results in unnecessary costs for banks, which are often passed along to consumers. Furthermore, the politicization of agencies such as the CFPB, FDIC, and OCC exacerbates the problem. These agencies increasingly pursue regulatory agendas through public relations stunts and policy announcements from the White House rather than through transparent processes. The predominantly progressive leanings of regulatory staff further bias outcomes against the banking industry, contributing to an environment in which financial institutions are unfairly targeted and overburdened with compliance costs. The economic consequences of this regulatory overreach are profound. As compliance costs soar, assets are migrating away from traditional banks, despite banks having access to deposits and being able to provide low-cost credit. This mainly affects community, mid-sized, and regional banks, which struggle with the high compliance costs of holding a banking charter. For all banks, high capital requirements and intense supervision increase the cost of lending, significantly impacting small businesses and low- to moderate-income individuals. This limits access to credit and slows economic growth. Reducing these excessive regulations would lead to significant gains in economic activity, highlighting the substantial benefits of reducing overregulation. The Biden administration’s excessively complex regulations, oppressive oversight, and politicized agenda stifle innovation, raise consumer costs, and hinder economic growth. Given these glaring issues, Congress should streamline regulations, increase transparency by requiring regulatory agencies to publish their models and scenarios for public comment, and ensure regulatory agencies operate independently of political influence. This would provide regulatory relief for community, mid-sized, and regional banks to enhance competition and access to credit. By reining these excesses in, Congress can unshackle the economy and promote a more competitive, dynamic financial sector that benefits all Americans. The potential rewards — a more prosperous, innovative, and dynamic America — make this a fight worth undertaking. Join me in this insightful episode of Let People Prosper as I dive into the economic implications of government regulations with Dr. James Broughel, a senior fellow at the Competitive Enterprise Institute.

We explore: - Which regulations pose the greatest economic burdens? - How crucial are cost-benefit analyses in regulatory practices? - Can some regulatory adjustments be "free lunches"? Don’t forget to like, subscribe, and share this episode to help spread valuable information. For more insights and bi-weekly episodes, subscribe to my newsletter at vanceginn.substack.com. Visit vanceginn.com for additional resources.  Originally published at Daily Caller.

The National Association of Insurance Commissioners’ (NAIC) recent regulatory proposals have concerned stakeholders across the U.S. insurance landscape. At the heart of the controversy are proposed changes that could fundamentally alter how life insurance companies invest in financial instruments, with far-reaching consequences for the broader economy and, more specifically, the retirement security of millions of Americans. The NAIC, as a non-governmental entity that wields considerable influence over the insurance industry’s regulatory framework, operates in a unique space where its decisions can have national implications. Its recent move to increase capital requirements from 30% to 45% on residual asset-backed securities (ABS) tranches is a poignant example of regulatory action with unintended consequences. The proposal reflects a perceived higher risk assessment by necessitating higher financial reserves against these investments. However, this risk reassessment and the consequent regulatory response have not gone unchallenged. Critics, armed with analyses such as the Oliver Wyman report, contend that the data does not substantiate these changes, highlighting a dissonance between the empirical evidence and regulatory action. The implications of the NAIC’s proposals extend beyond the immediate financial health of life insurance companies to impact broader retirement planning. By disincentivizing investments in ABS and similar financial instruments, these regulatory changes threaten to narrow the investment options available to life insurance companies. Given the critical role that life insurance companies play in providing annuity products and as major institutional investors, the potential for these regulatory changes to affect market dynamics and returns for retirees is a major concern. These decisions should be made from a bottom-up approach in the marketplace, not from a top-down approach by NAIC. Amidst these regulatory developments, the suggested influence of external political forces, including the Biden administration and labor unions, introduces an additional layer of complexity. The assertion that these proposals may be driven by broader political objectives, rather than by an unbiased assessment of market risks and consumer protection needs, underscores the potential for regulatory processes to be co-opted for ideological ends. This prospect is particularly troubling in retirement planning, where American workers’ and retirees’ economic well-being and choices should be paramount. The debate over the NAIC’s proposed regulatory changes highlights the broader challenges of ensuring that this regulatory body operates with a commitment to transparency, accountability and evidence-based policymaking. An institutional framework that supports free-market competition, consumer choice and the economic interests of Americans in this financial space is needed, given the oversized influence of NAIC and the government. As the insurance industry navigates these regulatory waters, the call for a balanced, data-driven approach to regulation — prioritizing American workers’ long-term financial security and the U.S. economy’s health — is urgent. Regulation should be the last resort instead of the first for potential problems, as the marketplace, through a well-functioning price system, is best at regulating things to those who want and provide them most. The NAIC’s regulatory proposals represent a critical juncture for the U.S. insurance industry and the financial system supporting American retirement planning. The potential for these proposals to disincentivize key investment strategies poses a considerable risk to the sustainability of defined-contribution plans. It highlights the need for vigilant oversight of the regulatory process to hold regulators in check. Stakeholders, including policymakers, industry leaders and the public, must engage in substantive dialogue to ensure that future regulatory actions are grounded in solid empirical evidence and aligned with the prosperity of Americans. As this debate unfolds, upholding principles of competition, consumer protection and the integrity of the retirement planning framework in the marketplace remains paramount. At best, the NAIC proposal should be delayed for a year to give more time to examine its effects. But given the evidence so far, the proposal should be trashed.  Originally published at Econlib.

President Biden signed a sweeping executive order to “harness” and “keep” artificial intelligence, two words you never want to hear from the government. This new regulation will inhibit Americans’ flourishing because restricting free markets never works. The EO is reported to ensure safety, equity, and responsible development. While these goals may appear laudable, delving deeper reveals that this motion will hinder economic progress and stifle the innovation it aims to promote. That’s why policies must always be judged by their results rather than their intentions. Details of the order’s objectives include safety tests, industry standards, and government oversight to address potential risks associated with AI. Forcing AI companies to conduct safety tests before going public, known as “red teaming,” will significantly slow the development and deployment of AI technologies. It’s well-established that innovation thrives in an environment of minimal regulatory interference called “permissionless innovation.” So introducing these bureaucratic hurdles will hinder fast-growing AI and all the industries that have begun to rely on it. Medicine and biotech, in particular, have realized remarkable potential with AI that has life-saving ramifications. But Biden’s overreaching EO wants to harness that. As is the case with many regulations, the EO comes at not just a cost to the individuals it affects but to the government’s pocketbook as well. As part of its endeavor to “preserve individuals’ privacy,” the administration will fund the Research Coordination Network. At a time when wages aren’t keeping pace with inflation and the average American family is losing real money due to a suffering economy, the government adding an expense like this is an insult to injury. Congress needs to reduce spending, and the Fed needs to slash its bloated balance sheet now more than ever. One of the most troubling aspects of the EO is its emphasis on regulating AI in the workforce out of concern for the technology displacing workers. Although there has been some uproar out of concern over AI destroying jobs, research shows that only 34% of Americans fear job displacement due to AI. And for good reason. Not only now but historically, concerns about new technologies displacing workers have been overblown. A Harvard paper published in 2013 predicted that by 2023, almost half of all American jobs would be replaced by AI. Clearly, the calculation has not come to pass. That’s because technology is a tool, not a threat. Frequently, implementing AI and technology like it allows humans to do more complex or human-facing jobs that AI can’t do or that people don’t want AI to do. AI is a transformative technology that has the potential to revolutionize various industries, from healthcare to finance and beyond. In a free market, competition drives innovation and efficiency, benefiting consumers and businesses. Restricting AI through excessive regulations and government oversight threatens this dynamic. While the intention behind Biden’s EO on AI may be to ensure responsible development and safe use, the economic consequences could be dire. To maintain America’s leadership in AI and foster economic growth, lawmakers and leaders must avoid overregulation and unnecessary restrictions on this transformative technology. Instead, we should encourage innovation, protect intellectual property, and ensure that AI remains a powerful tool for driving economic prosperity and improving the lives of all Americans. In the fast-paced world of technology, the last thing we need is government interference that hampers progress. dEverything old is new again, and that’s turning out to be true in the case of a growing drumbeat to use antitrust tools to rein in big technology companies like Apple, Amazon, Meta, and Google. But as a new policy report from the Pelican Institute points out, expanding the enforcement powers of antitrust agencies will do more harm than good—and an existing approach to protect consumers and producers, while encouraging innovation, is the better path forward. In their report “Antitrust & Enforcement: Letting Markets Work without Empowering Government,” Ted Bolema, Ph.D., J.D., Antitrust and Competition Fellow at the Innovators Network Foundation, and Vance Ginn, Ph.D., Chief Economist at the Pelican Institute, write that while the current frustrations with the size of large tech companies and censorship practices may be warranted, giving government enforcers and bureaucrats more power is not the answer. Instead, existing antitrust laws and the consumer welfare standard are still the best tools for protecting competition and consumers. “For the last 50 years or so, scholars and courts have operated with a consensus about the goal of antitrust enforcement: the consumer welfare standard, which asks, ‘does the conduct in question make consumers better or worse off?’” Bolema and Ginn write. “Antitrust enforcement based on the consumer welfare standard protects one of the most important outcomes of the competitive market process and is worth preserving.” Bolema and Ginn also note that calls to create new antitrust tools in response to conduct by “Big Tech” are misguided and will do far more to empower politicians and government bureaucrats than to prevent abusive conduct by technology companies. “Expanding the enforcement powers of antitrust agencies — as many on the left and some on the right now wish to do — harkens back to an older ‘big is bad’ approach,” they write. “Rather than promoting competition, such a retrograde approach undercuts the competitive market process which provides more innovation, cheaper prices, and better-quality goods and services necessary for continued human flourishing.” Bolema and Ginn say that the consumer welfare standard—and putting power in the hands of consumers and producers— is the tried and true path to ensuring their best interests. “As history has proven, empowering people in the marketplace rather than bureaucrats in government results in more efficient and effective outcomes and better supports liberty and prosperity,” Bolema and Ginn conclude. You can read the full report, “Antitrust & Enforcement: Letting Markets Work without Empowering Government,” here. Originally published by Pelican Institute.  In a desperate attempt to garner public favor before the midterms, President Biden set his sights on a new target to distract Americans from the pressing inflation problem: overdraft fees. Those low-percentage charges issued by banks to customers who use more money than they have in their accounts are apparently dire.

Biden tweeted: “My Administration is making clear that charging Americans for a bounced check they deposit or an overdrafted bank account isn’t just wrong. It’s illegal.” In the official White House statement, he refers to these charges as “hidden fees,” discounting that bank account holders voluntarily sign off on the possibility of overdraft fees when they open an account. Unlike Biden, most people understand that what’s illegal is using someone else’s funds without permission, not issuing a penalty for doing so. Eliminating overdraft fees would disempower personal responsibility through government overreach and reduce the opportunity for some to open an account. Charges are a practical price for using an institution’s capital to support money mismanagement, and an underreaction, one could argue, to theft. As it turns out, nothing is free, including using the bank’s money when you’ve overspent yours. This is bad enough, as people have begun to think that scarce things are free, but Biden says he isn’t stopping at overdraft fees. He’s also going after what he’s branded as “surprise” fees, such as family seating fees issued by airlines, switch fees from internet and cable services, and service fees from concert and sporting venues. Notably, he claims that these charges are more menacing than typical add-on fees and that “firms should be free to charge more to add mushrooms to your pizza.” So, what’s more menacing about concert venues charging a service fee to cover operational costs than Pizza Hut charging for extra toppings so they can still turn a profit? There isn’t a difference. What’s malicious is that Biden wants to penalize businesses for trying to stay profitable in a recession that he’s prolongingby addressing “problems” like these instead of the 40-year high inflation that’s removing purchasing power from consumers and hurting families. Biden insists that these “junk fees” are undetectable by consumers and therefore unfair, and that this makes it impossible for people to compare the real costs between service providers. Those seeking to promote more government involvement in businesses,almost always undermine individual agency. The reality is that consumers can fight against fees, take their business elsewhere, or choose to pay them if they think it’s worth it. That’s what prices in a free-enterprise system of capitalism are all about: allowing people to improve their lives. There are always trade-offs in life, and if the Biden administration successfully removes all these fees, we can expect to see another kind of trade-off instituted in its place. Nothing scarce is free. Every decision we make gives up something else, which economists call opportunity costs. Politicians too often think they can ignore this fact, but they do so at the peril of the people whom they serve. This kind of overreach isn’t just insulting to Americans, it’s harmful to a free-market system that operates best with limited government. By convincing people that they’re powerless to manage their money or find the best service provider because they’re helpless against “big scary businesses,” the government creates enough public concern to justify stepping in where they have no business doing so. The economy is suffering enough under Biden’s overregulation, Congress’ overspending, and the Fed’s overprinting; the last thing it needs is another barrier to growth and organic competition. Biden can quit trying to kid the American public that overdraft fees, which make up less than one percent of annual household spending, are the culprit for this lackluster economy. Instead, he should scrap his failed policies and promote free-market solutions that let people prosper. Originally published at AIER  Everyone is feeling the pinch at the supermarket these days, as inflation—measured by the decline in the purchasing power of money for a basket of goods and services—recently hit a 40-year high. From eggs to milk, it is getting harder to bring home the bacon. Nowhere has that been more visible than in the prices for beef.

While inflation has contributed to the increase in the price of beef, the scary truth is there is a more nefarious reason for this: excess regulation. The beef industry can be categorized into three sectors: cow-calf, stockyard, and slaughterhouse operations. Slaughterhouses have long been allowed to operate in what’s considered an oligopoly, as they’re heavily regulated by the United States Department of Agriculture (USDA) and Federal Drug Administration (FDA). A century ago, the Packers and Stockyards Act aimed to fix what was considered to be a market failure. It broke up the five major slaughterhouses controlling the beef industry. Yet today, only four slaughterhouses control 80% to 85% of America’s beef. Now, the Senate Agriculture Committee has passed two bills that aim to do that exact thing the Packers and Stockyards Act was supposed to do. That begs the obvious question: Is more regulation really the answer to this bloody mess? The proposed legislation of the Cattle Price Discovery and Transparency Act would require slaughterhouses to buy more cattle on the cash market. And the Meat and Poultry Special Investigator Act would require the USDA to investigate and prosecute anti-competitive practices. Cow-calf producers and stockyards are margin operators in one of the most complex markets in the world, and often fall victim to unpredictable forces like fluctuating demand, adverse weather, and disease. Of course, there are inherent risks in every market, and participants accept those risks. The issue here is these operators can appear to be unfairly squeezed by slaughterhouses that seem to be manipulating prices. These practices include utilizing market strategies such as forward contracting and retaining ownership. Forward contracting allows buyers and sellers to complete transactions months in advance to price in risk of the cash market. This strategy was intended to be a risk management tool for producers, giving them better control over their profit margins. Secondly, slaughterhouses have taken advantage of the “retained ownership” principle by purchasing their own stockyard inventory. Cattle in stockyards are typically owned outright by the yard or owned by cow-calf producers that retain ownership and pay on a per-head or per-day rate. So, in the event of unforeseen demand changes like, perhaps, a pandemic, inflation, drought, or mysterious cattle deaths, slaughterhouses can pull up their own inventory and mitigate any cost of buying cattle ready to be slaughtered at the cash market value. Put plainly, the new legislation would limit slaughterhouse’s ability to slaughter cattle they own in hopes of forcing them to offer producers higher prices. But this can only go so far. And likewise, there’s only so much regulation that can be implemented to correct issues created by overregulation. Threatening prosecution for market manipulation violations doesn’t break up the oligopolies because it addresses the wrong problem. Instead of trying to impose regulations to attempt to remedy the power disparity, eliminating the regulations that create barriers to entry in the first place would break up packer conglomerates naturally. In short, the answer to eliminating unfair pricing schemes does not lie in implementing additional regulations to an already heavily regulated industry. According to a 2022 report by the USDA, 900 slaughterhouses are federally inspected and 1,900 plants are not. The non-federally inspected plants that meet their states’ inspection standards can only sell or transport beef intrastate, barring them from being in direct competition with the Big Four. State inspections are required to meet criteria “at least equal to” federally inspected facilities. One solution is to add competition by deregulating the inspection requirements, which would result in more competitors for the slaughterhouses, helping achieve what as the two proposed bills aim to do through market forces instead of government regulation. Continued regulation of a market at this level is identical to how many experts believe India and many African countries fell into complete food dependence on their government. Congress’s signaled sympathy for cattlemen the past three years is probably all in vain—especially considering its legislation created the problem in the first place. Most importantly, consumers are about to feel even more pain at the meat counter come this fall. Without substantial deregulation of the beef industry, sly slaughterhouse owners and confused senators may enjoy their prime rib dinner, while the rest of us settle for chicken—or worse, “plant-based proteins.” Published at TPPF with Livia Lavender  Today, the Texas Public Policy Foundation released five papers that together form a responsible strategy for the state’s immediate and long-term economic growth.

“These five approaches make for good economic policy anytime,” said TPPF Chief Economist Vance Ginn, Ph.D. “But they are especially important as the state recovers from government-imposed shutdowns. Together, these strategies will help return Texas to the prosperity we saw before COVID-19 and help get us there fast.” The Five-Step Strategy is:

“During the shutdown, the state suspended some rules and regulations, proving they weren’t essential for health and safety in the first place,” said Rod Bordelon, TPPF’s Policy Director for the Remember the Taxpayer Campaign. “Instead of waiting for the crisis to end to re-evaluate these regulations, we should repeal them now and review others in an ongoing basis so that Texans aren’t held back by unnecessary restrictions.” The Responsible Recovery Agenda also stresses that budget writers should avoid seeking additional state revenue through increased fees and taxes. “Raising taxes is a costly endeavor — even more so in a recession because it distorts behavior at a time when the economy is weak, delaying recovery and leading to even greater economic stress,” said Benjamin Priday, Ph.D., Economist at TPPF. “Legislators should close budget gaps first by strategically employing the Rainy Day Fund and by trying to find ways to reduce spending. The Responsible Recovery Agenda is a comprehensive approach to addressing the budget challenges Texas faces in the wake of COVID-19 shutdowns while also preserving the success of the Texas Model, which has strengthened the state’s economy. For a historical look at the budget and other ways to improve the budget process, the Foundation also released The Real Texas Budget report.  On May 19, 2020, President Trump signed the Executive Order on Regulatory Relief to Support Economic Recovery. In Section 6 of the EO, titled the “Fairness in Administrative Enforcement and Adjudication,” it includes ways to improve the institutional framework of how federal regulations are enforced. The EO should help empower people to be protected from undue, expensive, unclear regulatory overreach by the federal government that costs Americans trillions of dollars over time. https://www.texaspolicy.com/overview-of-the-presidents-executive-order-on-regulatory-relief-to-support-economic-recovery-path-forward/ In this Let People Prosper episode, we discuss local government transparency and efforts to rein in progressive policies like government-mandated paid sick leave, state reforms to the criminal justice system, and the failure of the Texas House to pass a Conservative Texas budget...but there was a good discussion about property tax relief!

#letpeopleprosper In this Current Events Friday episode of the Let People Prosper show, James Quintero, Dr. Derek Cohen, and I discuss:

Thanks for watching and be sure to subscribe. #letpeopleprosper In this Let People Prosper episode, let's discuss how the best path to prosperity is capitalism and that starts with a job. The more ways that we can free up the labor market from government barriers to opportunity, such as the minimum wage and occupational licensing, the more prosperity we can all enjoy. My recent op-ed in the Investor's Business Daily titled "Amazon's Minimum Wage Revelation: It's About Competition, Not Workers" notes the opportunity costs associated with a government-mandated minimum wage compared with a private market decision: "Just as the company's management had the freedom to consider the firm's profitability and outlook in deciding whether to offer the higher wage, other private employers should have the same freedom. Amazon apparently thinks they shouldn't, hence the lobbying for a national mandate. Those lobbying efforts could end up doing even more harm." My recent paper with Dr. Edward Timmons titled "Occupational Licensing: Keeping People Poor" notes the huge cost that many licenses have on people whether they be workers, consumers, or employers. We highlighted this in a recent op-ed: "Between 1993 and 2012, Texas added licensing requirements for 22 low-income occupations. Data from the Texas Department of Licensing and Regulation indicate a 460 percent increase in the number of licenses issued by the department, far surpassing the state’s population growth of 37.5 percent in that period. By making it harder for aspiring workers in Texas to enter the job market, licenses artificially inflate wages — and this means higher prices for the services provided. National estimates suggest that licensing inflates wages of professionals by about 15 percent. And this means consumers pay higher prices. In addition, individuals looking to enter a new field may be prevented from achieving their dreams." For the sake of human flourishing, we should be doing all we can to reduce government barriers to prosperity that are socialist programs like the minimum wage (price of labor control) and occupational licensing (quantity of labor control). #LetPeopleProsper  In this episode, I explore the following questions: What are claimed market failures? Do they exist? Can government intervention correct them? Is there such thing as government failure? It's important to ask these questions to determine whether or not market failure or government failure are the bigger problem in society. Much of this has do with the differences between Mainline Economics (my preference) and Mainstream Economics.

This enters controversial territory in economics and politics by discussing the myths of "market failure." Supposed market failures usually include problems with markets because of asymmetric information (occupational licensing and healthcare), monopolies (utilities and EpiPen), and externalities (pollutants) that can theoretically be corrected by government intervention. However, I make the case that these issues in markets are generated by government intervention, not unhampered markets, and the introduction of government intrusion to attempt to correct these potential issues only expand government and make the problem worse. Moreover, there are no free-market government solutions, which is why toxic pollutants should be dealt with by letting markets sufficiently price them or alternatively, though not recommended, by regulation. Policy solutions such as a carbon tax indirectly price externalities and the price will always be wrong because of the "knowledge problem" taught by economist Friedrich Hayek and the poor modeling that's done by so-called experts (see William Easterly's book The Tyranny of Experts). In general, the institutional structure of an economy should be supported by the government through upholding contracts, protecting people, and providing very few public goods. Instead of resorting to government intervention to solve supposed market failures, we should first understand that the government is likely the problem and Let People Prosper by promoting institutions with strong private property rights and fewer barriers to entry and exit markets. #LetPeopleProsper In this episode, I have a conversation with Dr. Brandon Logan, who is the Director of the Center for Families & Children at the Texas Public Policy Foundation, about his fantastic work in helping kids and families prosper more throughout their lives.

The most essential institution is the family, and with government crowding out many of a family's basic functions, civil society suffers. By letting people prosper through limited government, whereby parents have the freedom to raise their child as they see fit without abuse, families can have the best opportunities to flourish. Here's more on Dr. Logan: Before joining the Foundation, Brandon represented hundreds of children as attorney and guardian in child welfare courts throughout Texas. He is certified as a Child Welfare Law Specialist by the National Association of Counsel for Children. Brandon has also represented parents, grandparents, and foster families in custody and adoption cases across the state. Brandon earned his undergraduate degree from Texas A&M University. He holds a law degree and doctorate in human development and family studies from Texas Tech University, where he also taught courses in child welfare policy and family dynamics. His academic work includes child maltreatment, abuse trauma and treatment, and family and father engagement. Brandon and his wife, Mindy, were raised in the same small West Texas town and are blessed with five young children – four boys and a baby girl. Texas ports contribute $650 billion in trade and support 1.6 million Texas jobs. But as goods travel through Texas ports, Texans and all Americans are paying a higher price than necessary from an uncompetitive market of harbor pilots.

Ships entering a U.S. port must be guided by a licensed harbor pilot, which is noted as “compulsory pilotage” in Chapter 61 of the Texas Transportation Code. Pilots are tasked with guiding, not helping steer, ship captains with navigating harbor waters and docking safely. They can provide a valuable service not only to the ship and its cargo, but also to the safety of other ships on the open waters and communities near ports. However, the harbor pilot market is in need of competition from current barriers of a too restrictive state license and the collusive nature of licensed pilots on commission boards deciding who can get a license. The Texas State Pilots Association grants a monopoly in most ship traffic coming into Texas ports. Rates and pay are regulated by a commission board, usually the same board that oversees the port. Harbor pilots must receive federal and state licenses, with the federal license allowing them to guide ships under the U.S. flag and the state license allowing them to guide ships under the U.S. and foreign flags—in other words, the state license is more valuable than the federal license. Licensed harbor pilots dominate these commission boards, contributing to a conflict of interest. They can essentially give themselves a raise, decide which fees to charge shippers, and restrict interested people from obtaining a license. Because a harbor pilot is compulsory for mariners, the state license restricts the number of pilots, and admittance into the association is limited, annual salaries of harbor pilots are driven arbitrarily higher from monopoly power to more than $400,000, or $192.31 per hour. Pilotage-related fees can add up to 10 percent of U.S. shipping costs. These monopolistic wages reduce investment, decrease job creation, and encourage shippers and other industries to use ports in other areas, or different modes of transportation. The potential net result is lower economic prosperity. In fact, the American Great Lakes Port Association noted that research shows pilotage costs in Great Lakes-Seaway have contributed to less economic growth, employers moving elsewhere, and fewer jobs created in the region. Last, but certainly not least, pilot fees paid by shippers are eventually passed on to the consumer. These higher prices reduce consumers’ purchasing power and standard of living. A step toward breaking up the monopolistic situation in the harbor pilot market would be for commission boards to provide a more competitive, objective environment for those seeking a harbor pilot license. Better yet, the state should issue a license to whomever complies with required criteria instead of a commission board deciding whom can get one. The American Pilots Association states that pilots would not be able to act independently, in the public interest, or have enough investment if there was competition. However, almost every other industry allows competition, and even those industries with restrictive licensing requirements have specific requirements that help avoid nepotism. In Florida, a study found that opening the harbor pilot system to competition could lower annual port costs by $35 million and create roughly 5,000 jobs in related industries. As with all occupational licensing, Texas should consider whether licensing harbor pilots protects people from health and safety risks. Specifically, assuming there is a risk and a need for licensing, Texas could simply abide by the federal license or at least reduce the requirements of the state license. Ultimately, competition in the market of harbor pilots would support improved quality and safety at a lower price as has been the proven result from unhampered markets throughout history. This would not only benefit those who would like to be a harbor pilot but can’t get access to a license but also Texans from a lower cost of living. Let people prosper by adding competition in the harbor pilots market.  BY VANCE GINN AND DREW WHITE, OPINION CONTRIBUTORS

Original can be found at The Hill The good news keeps coming. Since the passage of the Tax Cuts and Jobs Act, announcements about increased investment in the U.S. and various companies offering employees bonuses haven’t stopped. The vast majority of Americans will prosper from the Tax Cuts and Jobs Act. As an economist and policy analyst, we’ve been skeptical of the Trump administration’s direction on some issues, like NAFTA renegotiations, but we’re encouraged by the results of regulatory and tax reforms because they let people prosper, the flipside of what’s been stifling us. This first major rewrite of the federal tax code in a generation is a historic moment for our republic. The institutional framework that stifled Americans can again work for We the People instead of for bloated governments. We admit that the bill isn’t perfect and encourage Congress to follow this massive $5.5 trillion gross tax cut with spending restraint. That’s especially important because without spending reductions roughly $500 billion could be added to the national debt in the next decade. Also, doing so will help keep the roughly $112 trillion in federal IOUs from requiring government to further infiltrate our lives. We’ve experienced government’s overreach during the worst recovery since WWII of about two percent annual growth while the national debt almost doubled under the Obama administration’s high tax and spend policies. This reshaping of institutions increased barriers to prosperity through excessive regulations, like ObamaCare, and higher taxes that redistributed resources among people. America voted for a new institutional direction in 2016. Regarding regulations, the Trump administration has already repealed 67 of them while creating only three. Entrepreneurs can now budget lower costs longer which contributes to more investments in workers and capital. The result is faster economic growth with a three percent average annualized growth the last three quarters of 2017 matching GDP’s long-term average, which has lifted consumer sentiment. The tax bill’s most sweeping changes include cutting the corporate tax rate and individual income tax rates for most Americans. Sixty percent of the gross tax cuts go to families while the rest goes to businesses. As expected, critics claim these changes benefit the rich. Interestingly, the corporate tax rate cut once had bipartisan support, as President Obama proposed cutting it to 28 percent, and progressives passed and extended much of President Bush’s personal income tax cuts. Regardless, permanently cutting the corporate tax rate from 35 percent, the highest in the developed world, to 21 percent, slightly below the worldwide average, drastically improves employment prospects. Often missed in the discussion is that corporations simply submit taxes to the government because people pay them through higher prices, lower wages, and fewer jobs available. Cutting the corporate tax rate means corporations can pass those savings along to people. Businesses are reporting they will pay bonuses and higher wages, immediate pay increases to let people freely prosper. On the individual income tax side, most taxpayers will pay less tax until at least 2026. According to good tax policy, the tax bill doesn’t flatten as it leaves seven income tax brackets, but it broadens the base by eliminating many exemptions and deductions and simplifies the code by doubling the standard deduction. Critics claim that these changes could increase income inequality. But history shows that the tax code is not the place to deal with supposed income inequality as it fluctuates whether taxes are high or low. By changing the institutional incentives through this tax bill, more people can move up the income ladder. But, do only the rich get a tax cut? No. The Tax Foundation calculated the changes in tax liability for multiple households and found that each of them would pay less tax. An individual earning $30,000 with no kids could pay $379 less in taxes. An individual earning $50,000 with two kids could pay $1,892 less in taxes. A married couple filing jointly earning $165,000 with two kids could pay $2,224 less in taxes. And a married couple filing jointly earning $2 million could pay $18,904 less in taxes. All income groups receive a tax cut. Higher income people pay fewer dollars than those with lower income, but that’s because they pay more in income taxes. For example, the top 10 percent of income earners pay 70 percent of federal income taxes collected. However, the share of income taxes paid could become more progressive under these tax changes. It’s not just more money in people’s pocket, but doubling the standard deduction lets many people spend less time on their taxes and more time with their families. This is great news for working Americans. Icing on the cake would be for Congress to restrain government spending, the ultimate burden of government. Bipartisan welfare reform in the 1990s helped cut spending but more importantly improved the lives of many Americans as they returned to work or received better assistance. The amount of waste, fraud, and abuse in these programs along with too many dollars to bureaucracy and not to people make welfare a good place to start. Reforms to the major drivers of Medicaid, Medicare, and Social Security must be on the table to restrain spending growth while improving them for the truly needy. Until then, let’s celebrate the Trump administration’s new institutional direction that has long supported prosperity. Skepticism is healthy to provide proper checks and balances on government. But when pro-growth policies like regulatory and tax reforms improve human flourishing, we’re much more optimistic about the future. Vance Ginn, Ph.D., is director of the Center for Economic Prosperity and senior economist and Drew White is senior federal policy analyst, both at the nonprofit Texas Public Policy Foundation.  Federal regulations are often a complex cobweb of repetitive, useless rules determined by federal bureaucrats rather than elected officers. These regulations may have good intentions of providing clean water, increasing public safety, and other benefits, but it’s important to consider the costs of those measures. Far too often, government avoids considering these costs that are detrimental to everyone’s well-being.

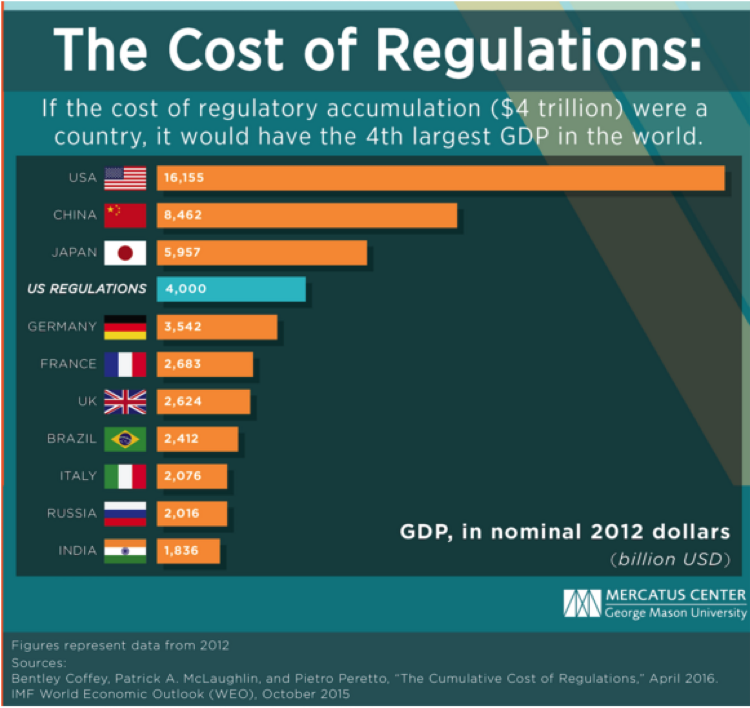

It’s no secret that big government restricts the economy, but by how much? According to a new study by the Mercatus Center, federal regulations that have accumulated from 1980 to 2012 cost Americans approximately $4 trillion! Figure 1 shows that this huge cost translates into about 25 percent of the U.S economy, $13,000 per American, or the fourth largest economy in the world. Clearly, Americans are being stifled by too much red tape. Figure 1: Federal regulations have hindered economic progress to the tune of $4 trillion since 1980. The study’s findings show that federal regulations have reduced average U.S. economic growth by about 0.8 percentage points per year since 1980. While this doesn’t seem like a big deal, it’s important to note that economic growth compounds over time. Therefore, the negative gap between economic growth without regulations compared with actual growth grows larger as it builds on itself each period. Mercatus has the federal regulation and state enterprise (FRASE) index that ranks the economic impact of federal regulation on states. Texas ranks as having the 6th highest, or the state’s industries are negatively influenced 29 percent more than the national average. This is a huge cost to Texans as noted in Figure 2 with the tremendous number of federal regulations on businesses. The cost of federal regulation on Texas is not only burdensome at the federal level. States also plague their businesses with burdensome regulation. Texas' successful economic model is one that other states and federal lawmakers would be wise to follow, but even Texas could do far better when it comes to regulation. In the Mercatus Center’s Freedom in the 50 States report, Texas ranks only 24th for regulatory freedom. One reason is stringent occupational-licensing requirements; the Institute of Justice ranks Texas as having the 17th most burdensome set of them. These regulations protect existing businesses from new competition and make it harder for low-skilled workers to find employment, making everyone losers in the process. To have the best economic environment for opportunities to prosper and higher standards of living, regulation at the federal and state levels should be dramatically scaled back. The cost of every regulation must be considered, and those that have a higher cost than benefit should be scrutinized and ultimately not imposed. This is how we can begin to reclaim the American Dream for far too many who feel as though it is out of reach. |

Vance Ginn, Ph.D.

|

RSS Feed

RSS Feed

Proudly powered by Weebly