Our new report highlights Louisiana’s economic situation based on the most recent data. The report is based on several key factors that indicate how the economy, labor market, and public policy influence the lives of everyday Louisianans. While some of these data indicate a relatively strong labor market–such as the historically low unemployment rate–there are underlying factors showing Louisiana’s economic struggle. Our Louisiana Comeback will happen through reforms that remove government barriers, bring jobs and opportunity back to Louisiana, and let people prosper. We must decide: Will we continue to hold on to the status quo (which hasn’t done us any favors), or will we embrace the significant reforms necessary to bring jobs and opportunity to Louisiana? We need the latter. Read the full two-pager: Economic Report Oct 2023 Originally published by Pelican Institute.

0 Comments

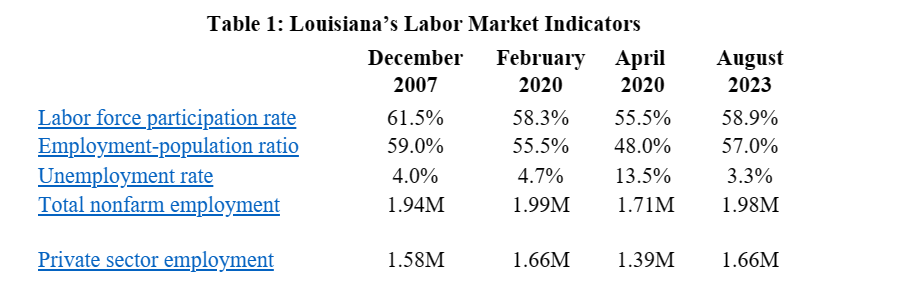

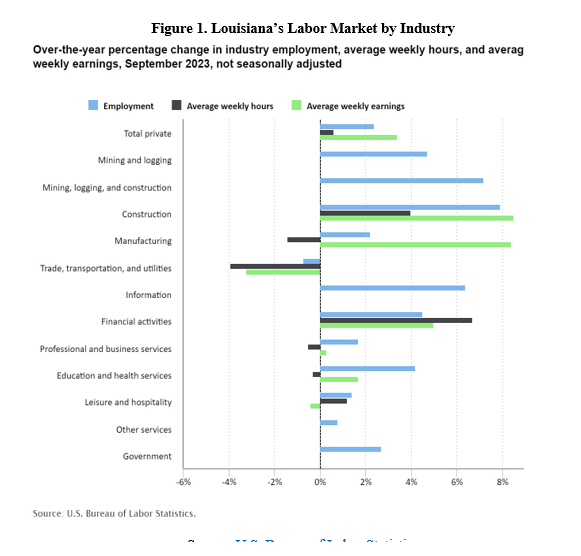

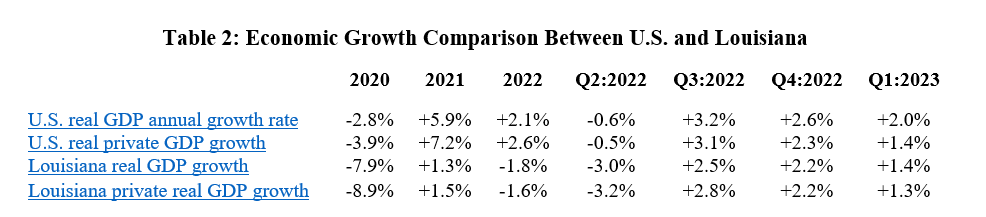

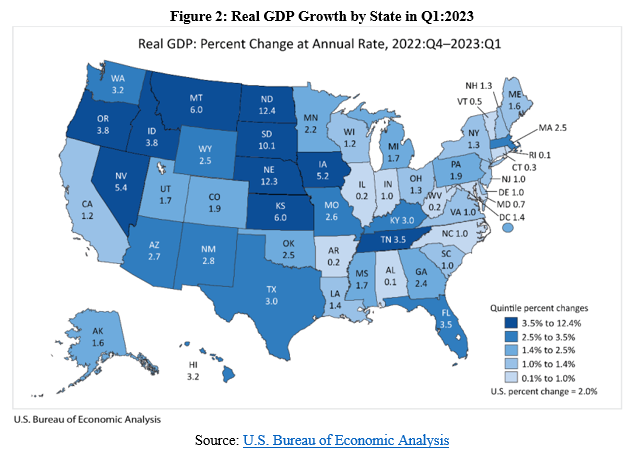

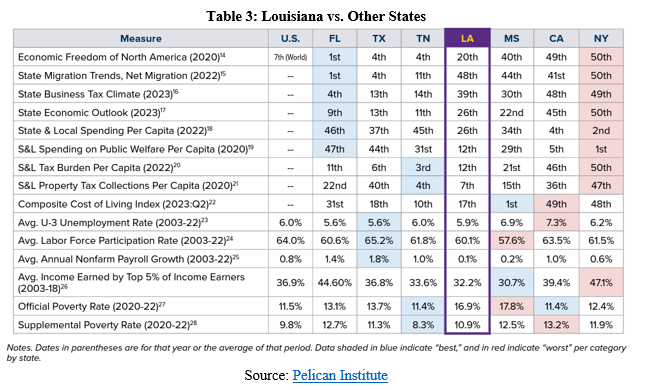

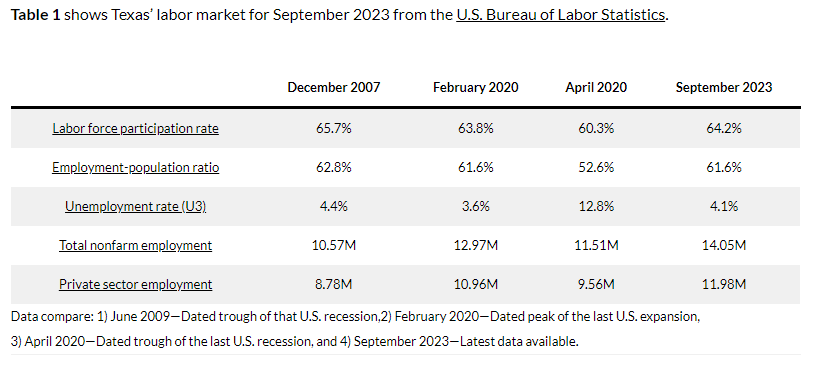

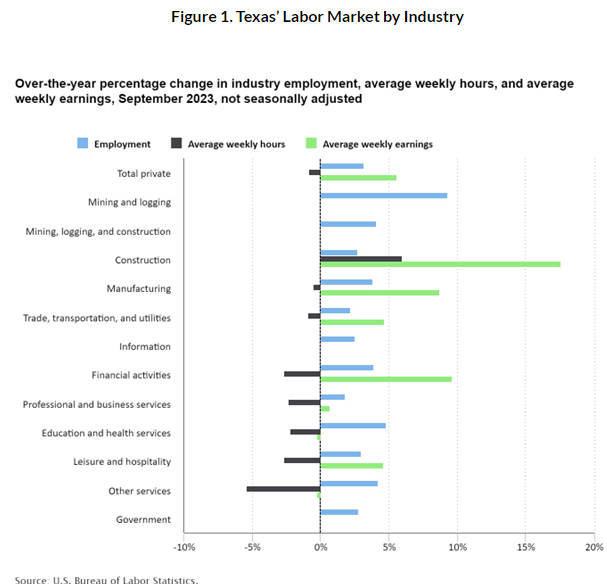

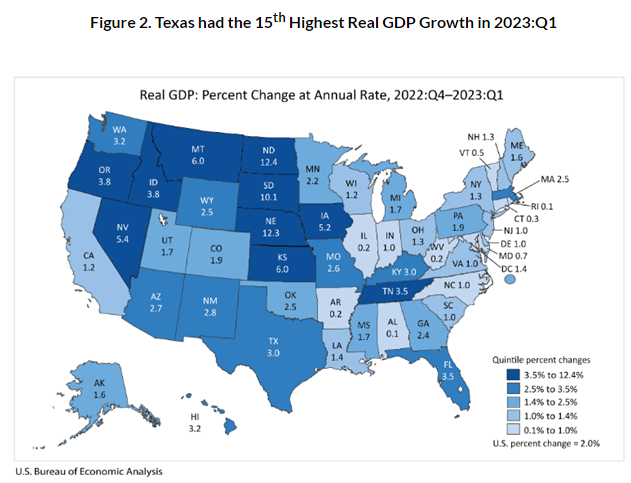

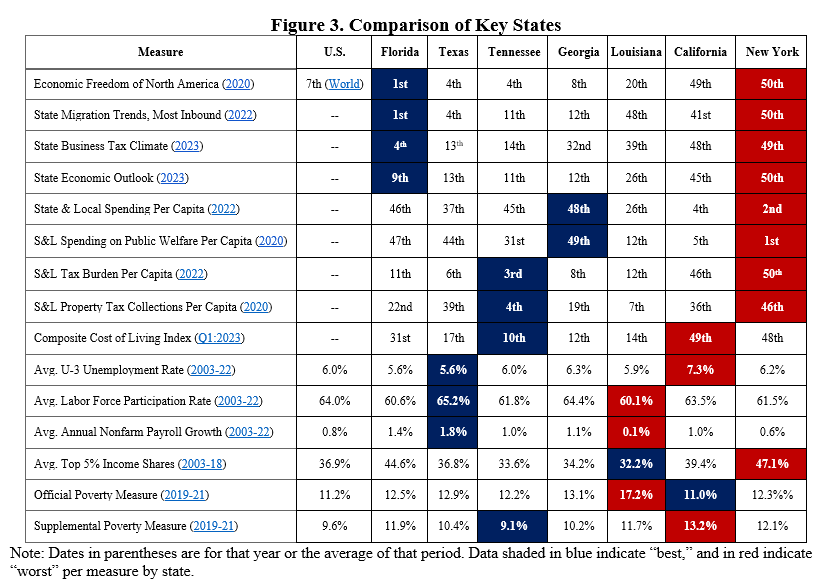

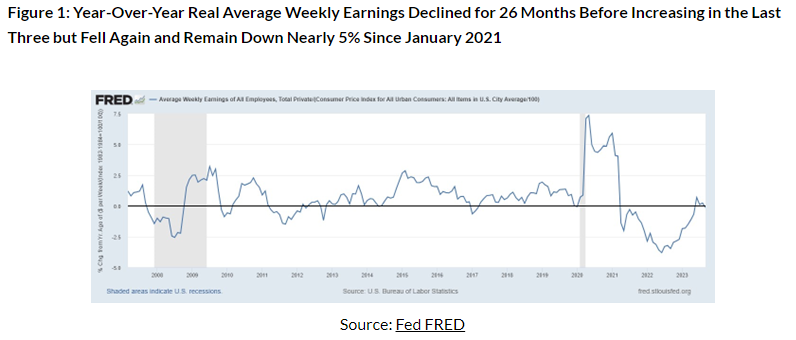

At first glance, you might think that Louisiana’s economy is doing great. After all, the state’s September 2023 jobs report shows record lows for the unemployment rate at 3.3% and and people unemployed at 67,930. Louisiana Governor John Bel Edwards cheered these data in a press release: “Louisiana continues to set records for low unemployment. We’ve had 30 consecutive months of job growth and have added nearly 280,000 jobs since the worst of the pandemic. In fact, our employment levels are now higher than they were before COVID. Experts believe that our bipartisan work to grow and diversify our economy will benefit Louisiana for years to come. Economist Dr. Loren Scott recently predicted that Louisiana will add more than 80,000 jobs over the next two years. And we’ve done it all while overcoming historic natural disasters and a state government budget crisis. I have never been more optimistic about Louisiana than I am today.” But does what you hear in the media or by some politicians match reality? Let’s dive into the data to see how things are going for Louisianans. We should know that the Pelican State has many fantastic resources but too many failed public policies that keep Louisianans from reaching their full potential. This has been the case for a while, but most recently, the jobs reports indicate slowing employment growth and a declining labor force. Work matters, as it brings about dignity and self-sufficiency and leaves fewer people needing help from government safety net programs. These data below show that while the labor market data can look good on the surface, there are many real problems facing Louisianans that need to be addressed by state leaders. Fortunately, the Pelican Institute’s “Comeback Agenda,” including our fiscal reform plan, supports ways to overcome these challenges. Here are key issues in Louisiana’s economy. Table 1 provides Louisiana’s labor market data for important dates from the U.S. Bureau of Labor Statistics. These dates are December 2007, when the Great Recession started; February 2020, when the last expansion peaked before the COVID-19-related shutdowns; April 2020, when the shutdown recession ended; and September 2023, for the latest data available.  The unemployment rate would be 4.9% if Louisianans hadn’t left the state since pre-COVID. The unemployment rate is calculated using data from the household survey and isn’t a great measure of the labor market. This is because unemployment in the numerator and the labor force in the denominator are volatile measures as people enter and exit Louisiana and the labor force. Considering data from pre-COVID to compare with the Governor’s statement, the working-age population is down by 36,329 to 3.5 million. Even though the labor force is up 1,566 since then, the many people who have left the state keep the unemployment rate lower than otherwise. If we include the departed population in the labor force and unemployment, the unemployment rate would be 4.9%, substantially higher than the reported 3.3%. Moreover, if the working-age population hadn’t declined, the labor force participation rate would be 59.3% instead of the 58.9% rate today. Louisiana’s employment has not increased for 30 consecutive months. While the Governor is correct that there have been about 280,000 jobs since pre-COVID, there have not been “30 consecutive months of job growth.” The payroll survey shows that nonfarm employment is up 270,300 and the household survey shows that employment is up 295,065 since February 2020. There was an increase in nonfarm employment by 8,900 jobs in September (6th most in percentage terms of any state). But this was after cumulative losses of 3,600 jobs during June and July for an increase of just 18,100 jobs over the last four months. Over the last 30 months, there have been seven months with declining net jobs in the payroll survey and nine months with declines in the household survey, which has had four straight months of declines for a total of 17,564 fewer people employed in that period. So, Louisianans have actually been struggling over the last 30 months. Louisiana will add a projected 80,000 more jobs over the next two years, indicating slower job creation. Considering nonfarm employment over a longer period, it is up by 46,000 jobs from a year ago (20th most in the country) for a 2.4% increase (12th fastest). This would result in 92,000 jobs added over the next two years if this pace continued, but the Governor says one projection is just 80,000 jobs added over that period, indicating slower job creation. Also, nonfarm employment is down by 13,700 jobs since February 2020 (one of only a few states that have not regained lost jobs since then). Jobs in the private sector increased by 520 last month to 1.66 million, and government employment increased by 8,300 jobs to 320,500. There is growing weakness in the labor market, with some job losses and average weekly earnings not rising as fast as CPI inflation of 3.7% in many industries (Figure 1).  Another weakness is economic growth. Table 2 shows how the U.S. and Louisiana economies performed since 2020, as reported by the U.S. Bureau of Economic Analysis.  The steep declines were during the shutdowns in 2020 in response to the COVID-19 pandemic, which was when the labor market suffered most. Figure 2 shows how the increase in real GDP in Louisiana of +1.4% in Q1:2023 ranked 31st in the country to $289.9 billion, after an annual decline in economic output by -1.8% in 2022 which was the second worst in the country.  The BEA also reported that personal income in Louisiana grew at an annualized pace of +6.2% (ranked 27th) to $258.5 billion in Q1:2023 (above +5.1% U.S. average). There was personal income growth of 0.0% in 2022, ranking 50th of the states. Compared with neighboring states based on several measures there continue to be major concerns in Louisiana (see Table 3).  Bottom Line: Louisiana’s economy is weak when it comes to the labor market and economic growth and when compared with other states. Bold, transformational reforms can unleash the potential of Louisianans and make the state more competitive.

Originally published at Pelican Institute.  The headlines are filled with positive economic news for Louisiana, boasting record-low unemployment rates and impressive job growth. But digging deeper into the data reveals a more nuanced and challenging economic landscape that deserves attention and fast action.

At first glance, Louisiana's unemployment rate appears to be a shining success at just 3.3%. Governor John Bel Edwards has been vocal about the state's accomplishments, boasting a record low unemployment rate, "30 consecutive months of job growth," and the addition of nearly 280,000 jobs since the pandemic's peak. But the unemployment rate only tells part of the story. Looking at the data from before the COVID-19 pandemic, there are 36,329 fewer people of working age in Louisiana, totaling 3.5 million. Even though the number of people actively looking for work has increased by 1,566, many have left the state for better opportunities. This is why the unemployment rate seems lower than it is. Had those 36,329 people stayed in Louisiana to be part of the workforce and unemployment numbers, the real unemployment rate would be 4.9%, which is 48% higher than 3.3%. This statistic challenges the narrative and reveals underlying workforce participation and retention challenges. Considering jobs added over the last 30 months, the Pelican State has had seven months of declining net jobs in the payroll survey and nine months with declines in the household survey. The latter measure has declined for four straight months resulting in 17,564 fewer people employed in that period, pointing to a turbulent job landscape. At the same time, Louisiana’s gross domestic product (GDP) has seen concerning ups and downs. In 2022, the state's real GDP shrank by 1.8%, making it one of the poorest performers in the nation. The most recent data indicate a modest 1.4% growth in the first quarter of 2023, ranking 31st in the country. These figures reveal economic instability and emphasize the need for a comprehensive approach to sustainable growth. Finally, assessing personal income figures for state residents reveals additional economic weakness. The first quarter of 2023 showed more promising trends for state residents’ personal income, with personal income growing at an annualized rate of 6.2%, ranking 27th nationwide. However, that has yet to make up for 2022, when personal income did not grow at all, making Louisiana’s personal income last among the 50 states that year. The results are in: Louisiana’s economy is lacking, and transformative reforms are vital to unlock the Pelican State’s potential. If Louisiana continues on its current path, it risks maintaining a poor business tax climate, facing ongoing outmigration of residents, and perpetuating one of the highest poverty rates in the country. Implementing better spending restraint, substantial tax reform, significant regulatory relief, universal education freedom, enhanced workforce development, and improved safety net programs are practical solutions that would empower Louisianans. Fortunately, a recent poll underscores that these essential reforms are not only needed but also desired by Louisiana's residents. The Pelican State has the potential to become "the next big thing," a place where people want to move, provided its leaders take fast action to secure a brighter and more prosperous future for all. This is possible given a new governor and many state lawmakers next year. Originally published at The Center Square. Why the Rich Getting Richer Benefits the Poor and Middle Class w Former U.S. Senator Phil Gramm10/30/2023 Today, I'm joined on episode 68 of the "Let People Prosper" show by Former U.S. Senator Phil Gramm. Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. Also, subscribe and see show notes for this episode on Substack (www.vanceginn.substack.com) and visit my website for economic insights (www.vanceginn.com).

Phil (bio) and I discuss:

Thank you for listening to the 32nd episode of "This Week's Economy," where I briefly recap and share my insights on key economic and policy news.

Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. Also, subscribe and see show notes for this episode on Substack (www.vanceginn.substack.com) and visit my website for economic insights (www.vanceginn.com). Today, I cover: 1) National: The newly appointed House Speaker Mike Johnson, how President Biden's student loan "forgiveness" plan will disadvantage lower-income earners while making higher education more expensive, and while the latest GDP report may seem promising at first, but is less impressive when considering details; 2) States: Texas has a new roughly $18 billion surplus that should be put toward buying down property taxes until they are zero, but that likely won't happen given what's on Texas' ballot, and Louisiana's GDP and personal income rates show that aggressive improvement is needed in The Pelican State; and 3) Other: Why you don't want to miss last week's podcast with Texas State Representative Brian Harrison and the upcoming episode with Former U.S. Senator Phil Gramm on the myth of American inequality.  The Texas Legislature just found out it has a huge opportunity to correct its profligate spending failures made earlier this year. But instead, they’re gearing up to spend more at the expense of strapped taxpayers. This would be a fatal error for the Lone Star State.

Texas Comptroller Glenn Hegar recently released the Comptroller's Revenue Estimate (CRE). This report acts like a financial checkup to confirm sufficient tax revenue available to cover expenditures based on the state’s balanced budget amendment. The current two-year tax revenue for 2024-25 was updated higher to $194.6 billion available for general spending, an increase of 24.8% from the previous budget. This certified revenue estimate exceeds the $176.3 billion appropriated by the 88th Legislature for general purposes, resulting in a projected surplus of $18.3 billion. This large amount is from a more vibrant economy than previously estimated and could go a long way to putting school property taxes on a path to elimination. Yet the Texas Legislature’s recent out-of-control spending habits indicate taxpayers probably won’t get more property tax relief than the minimal amount passed this year. The state wants to increase spending on a government school system in the current third special session rather than on students to have universal school choice. And spending could go up by more than $13 billion outside of the expenditure limit if voters approve most of the 14 constitutional amendments on the state ballot this year. Add it all up, and it’s no wonder that Texans find living in many places across the state unaffordable. While Texas has witnessed major economic achievements this year, such as noteworthy records for labor force participation and job creation, the 88th Legislature's actions raise serious concerns about the future. This year, the Lone Star State passed its largest spending increase, largest corporate welfare, and just the second-largest property tax cut in state history, which the latter will underwhelm homeowners when they get their bills. This could be a major problem for Republicans who have touted this as the “largest property tax cut in the world” or the “largest property tax cut in Texas history.” While Texans grapple with an affordability crisis, spending the state surplus and voters approving the proposed ballot items, except propositions 3 (prohibit wealth taxes) and 12 (abolish Galveston County treasurer’s office), would add insult to injury. Rather than squandering the surplus, the Texas Legislature should prioritize strengthening the Texas Model by: 1. Spending less at the state and local levels, strengthen the state’s spending limit with the rate of population growth plus inflation covering all state funds, and have that spending limit also cover local government spending similar to Colorado’s Taxpayer’s Bill of Rights. 2. Taxing less by putting local property taxes on a path to elimination using surpluses to reduce school district M&O property tax rates until they are zero. Local governments should leverage their surpluses to reduce their property tax rates until they are zero. 3. Regulating less by removing barriers to work, removing occupational licensing restrictions, reforming safety nets, and passing universal school choice. Strengthening the Texas Model isn't just about fiscal responsibility; it's about securing a thriving future for generations to come. Texas, with its unique spirit and determination, can continue to lead the way, fostering an environment where free-market capitalism thrives and individuals prosper. The surplus, instead of being frittered away on needless pursuits, should be a catalyst for transformation that redefines the Lone Star State's destiny, safeguards liberty, and sows the seeds of enduring prosperity. Originally published at The Center Square.  Texas has been a leader in job creation. But Texas faces major headwinds as this year’s 88th Legislature has looked more like California than what Texans expect. There is a better way.

The labor market continues to improve in Texas even as there are some weaknesses.

Originally published at Texans for Fiscal Responsibility. I hope you enjoy the fantastic 67th Let People Prosper Show episode with TX State Rep. Brian Harrison! Please subscribe to my newsletter if you haven’t already, and subscribe to my podcast wherever you get yours. I would appreciate it if you would also rate and review my podcast! Brian (bio) and I discuss:

While the latest “strong” US jobs report and “cooling” CPI inflation have been touted as promising, a closer look reveals more complexity, and many American families continue to bear the brunt of DC’s failures over the last three-plus years.

The payroll survey’s net gain of 336,000 non-farm jobs is a popular headline, as the figure nearly doubled expectations. But the household survey, a second crucial report by the US Bureau of Labor Statistics, shows that only 84,000 jobs were added in September. Meanwhile, the unemployment rate stayed at 3.8 percent, which would be much higher if more people were looking for work. Let’s consider the labor force participation rate of 62.8 percent to double-check the headlines. If this rate were 63.3 percent, as it was in February 2020, there would be 1.4 million more people in the labor force. If they are all unemployed, today’s unemployment rate would be nearly 5 percent, which is substantially higher than the touted 3.8 percent rate. There have also been substantial revisions to the non-farm jobs report in recent months because of volatile data used for seasonal adjustments since the shutdowns, which makes much of it “garbage in, garbage out.” There were, for example, an additional 119,000 jobs added over just July and August than what was initially reported, giving us reason for pause with all of these reports. In short, this volatility in the job market data makes it challenging to discern actual trends, especially when Americans continue to be concerned about the economy. On top of a fickle job market, the latest consumer price index (CPI) sits at 3.7 percent over the past year, while the core inflation, which excludes food and energy, is 4.1 percent. This core inflation rate is double the Federal Reserve’s average inflation rate target and doesn’t show any signs of reverting to 2 percent any time soon. This problem was created by the Fed’s bloated balance sheet, which results from its willingness to help finance the federal budget deficits caused by excessive government spending. Until Congress reins in government spending and money printing, inflation will strain household budgets. Also, real (inflation-adjusted) average weekly earnings dropped by 0.2 percent over the past year, and the average family’s real income has suffered a significant blow, with a decline of more than $7,000 since the start of 2021. These financial setbacks are not coincidental. They are the direct result of the progressive policies of the Biden Administration, the Federal Reserve’s bloated balance sheet, and Congress’s habit of excessive spending. If we want to understand the true state of our economy, we should pay more attention to the Fed’s balance sheet, which remains a crucial indicator of inflationary pressures. This is why I was never on team “transitory inflation.” Even a relatively superficial understanding of the work of Milton Friedman, Friedrich Hayek, and John Taylor has indicated from the start that we would face persistent inflation. Sure, supply-side factors contributed to higher prices in some markets, as did supply chain bottlenecks. But those are short-term fluctuations that don’t tell the entire story of reduced purchasing power for everyone over a longer period, which is a story of failed public policy on top of the failed shutdowns during the pandemic. The explanation is pretty straightforward. There was a sudden halt in the economy due to pandemic shutdowns that distorted many exchanges throughout the marketplace. The federal government then sent out redistributed money to individuals and employers so they wouldn’t have to fret too much during a stressful time. This propped up many Americans, creating any number of zombie firms, zombie workers, and a debt-fueled zombie economy. But this alone wouldn’t explain the inflation, as increased government spending doesn’t stimulate anything other than more government and some specific markets. Next, the Fed more than doubled its balance sheet, increasing its assets from $4 trillion to $9 trillion. This doesn’t lead to long-term economic growth, but it does contribute to many market distortions and inflation across the economy. Much of this money stays in the hands of the banks, mortgage companies, and others at the upper part of the income spectrum. Only then does some of it spread further, in a process known as the Cantillon effect. The problem is not only a propped-up economy with multiple asset bubbles, but reduced purchasing power that punishes lower-income families the most. Few, if any, of the positives from more money in circulation goes to these families. Instead, they have seen whatever savings they had dwindle. To achieve a more stable and prosperous economic future, we must strike a balance between sound fiscal and monetary policies and curb excessive government spending and money printing. This will only begin to happen when we have rules that control discretionary policies by the administration, Congress, and the Fed. While headline jobs and inflation data might suggest a strong economic recovery, digging just a little deeper into the data shows a weak economy with major challenges. It’s time for policymakers to take a hard look at the factors contributing to these economic woes and adopt prudent policies that address the root causes of stagflation. Originally published by AIER.  Originally published at American Institute for Economic Research.

While the latest “strong” US jobs report and “cooling” CPI inflation have been touted as promising, a closer look reveals more complexity, and many American families continue to bear the brunt of DC’s failures over the last three-plus years. The payroll survey’s net gain of 336,000 non-farm jobs is a popular headline, as the figure nearly doubled expectations. But the household survey, a second crucial report by the US Bureau of Labor Statistics, shows that only 84,000 jobs were added in September. Meanwhile, the unemployment rate stayed at 3.8 percent, which would be much higher if more people were looking for work. Let’s consider the labor force participation rate of 62.8 percent to double-check the headlines. If this rate were 63.3 percent, as it was in February 2020, there would be 1.4 million more people in the labor force. If they are all unemployed, today’s unemployment rate would be nearly 5 percent, which is substantially higher than the touted 3.8 percent rate. There have also been substantial revisions to the non-farm jobs report in recent months because of volatile data used for seasonal adjustments since the shutdowns, which makes much of it “garbage in, garbage out.” There were, for example, an additional 119,000 jobs added over just July and August than what was initially reported, giving us reason for pause with all of these reports. In short, this volatility in the job market data makes it challenging to discern actual trends, especially when Americans continue to be concerned about the economy. On top of a fickle job market, the latest consumer price index (CPI) sits at 3.7 percent over the past year, while the core inflation, which excludes food and energy, is 4.1 percent. This core inflation rate is double the Federal Reserve’s average inflation rate target and doesn’t show any signs of reverting to 2 percent any time soon. This problem was created by the Fed’s bloated balance sheet, which results from its willingness to help finance the federal budget deficits caused by excessive government spending. Until Congress reins in government spending and money printing, inflation will strain household budgets. Also, real (inflation-adjusted) average weekly earnings dropped by 0.2 percent over the past year, and the average family’s real income has suffered a significant blow, with a decline of more than $7,000 since the start of 2021. These financial setbacks are not coincidental. They are the direct result of the progressive policies of the Biden Administration, the Federal Reserve’s bloated balance sheet, and Congress’s habit of excessive spending. If we want to understand the true state of our economy, we should pay more attention to the Fed’s balance sheet, which remains a crucial indicator of inflationary pressures. This is why I was never on team “transitory inflation.” Even a relatively superficial understanding of the work of Milton Friedman, Friedrich Hayek, and John Taylor has indicated from the start that we would face persistent inflation. Sure, supply-side factors contributed to higher prices in some markets, as did supply chain bottlenecks. But those are short-term fluctuations that don’t tell the entire story of reduced purchasing power for everyone over a longer period, which is a story of failed public policy on top of the failed shutdowns during the pandemic. The explanation is pretty straightforward. There was a sudden halt in the economy due to pandemic shutdowns that distorted many exchanges throughout the marketplace. The federal government then sent out redistributed money to individuals and employers so they wouldn’t have to fret too much during a stressful time. This propped up many Americans, creating any number of zombie firms, zombie workers, and a debt-fueled zombie economy. But this alone wouldn’t explain the inflation, as increased government spending doesn’t stimulate anything other than more government and some specific markets. Next, the Fed more than doubled its balance sheet, increasing its assets from $4 trillion to $9 trillion. This doesn’t lead to long-term economic growth, but it does contribute to many market distortions and inflation across the economy. Much of this money stays in the hands of the banks, mortgage companies, and others at the upper part of the income spectrum. Only then does some of it spread further, in a process known as the Cantillon effect. The problem is not only a propped-up economy with multiple asset bubbles, but reduced purchasing power that punishes lower-income families the most. Few, if any, of the positives from more money in circulation goes to these families. Instead, they have seen whatever savings they had dwindle. To achieve a more stable and prosperous economic future, we must strike a balance between sound fiscal and monetary policies and curb excessive government spending and money printing. This will only begin to happen when we have rules that control discretionary policies by the administration, Congress, and the Fed. While headline jobs and inflation data might suggest a strong economic recovery, digging just a little deeper into the data shows a weak economy with major challenges. It’s time for policymakers to take a hard look at the factors contributing to these economic woes and adopt prudent policies that address the root causes of stagflation. I hope you enjoy the 31st “This Week’s Economy” episode! Please subscribe to my newsletter if you haven’t already, and subscribe to my podcast wherever you get yours. I would appreciate it if you would also rate and review my podcast! Today, I cover:

A year after the Supreme Court struck down President Biden’s student loan forgiveness plan, he presented a new scheme to the Department of Education on Tuesday. While it is less aggressive than the prior plan, this proposal would cost hundreds of billions of taxpayer dollars, doing more harm than good.

As the legendary economist Milton Friedman noted, “One of the great mistakes is to judge policies and programs by their intentions rather than their results.” Higher education in America is costly, and this “forgiveness” would make it worse. Signing up for potentially life-long student loans at a young age is too normalized. At the same time, not enough borrowers can secure jobs that offer adequate financial support to pay off these massive loans upon graduation or leaving college. These issues demand serious attention. But “erasing” student loans, as well-intentioned as it may be, is not the panacea Americans have been led to believe. Upon closer examination, the President’s forgiveness plan creates winners and losers, ultimately benefiting higher-income earners the most. In reality, this plan amounts to wealth redistribution. To quote another top economist, Thomas Sowell described this clearly: “There are no solutions, only trade-offs.” Forgiving student loans is not the end of the road but the beginning of a trade-off for a rising federal fiscal crisis and soaring college tuition. When the federal government uses taxpayer funds to give student loans, it charges an interest rate to account for the cost of the loan. To say that all borrowers no longer have to pay would mean taxpayers lose along with those who pay for it and those who have been paying or have paid off their student loans. According to the Committee for a Responsible Federal Budget, student debt forgiveness could cost at least $360 billion. Let’s consider that there will be 168 million tax returns filed this year. A simple calculation suggests that student loan forgiveness could add around $2,000 yearly in taxes per taxpayer, based on the CRFB’s central estimate. Clearly, nothing is free, and the burden of student loan forgiveness will be shifted to taxpayers. One notable feature of this plan is that forgiveness is unavailable to individuals earning over $125,000 annually. In practice, this means that six-figure earners could have their debts partially paid off by lower-income tax filers who might not have even pursued higher education. This skewed allocation of resources is a sharp departure from progressive policy. Data show that half of Americans are already frustrated with “Bidenomics.” Inflation remains high, affordable housing is a distant dream, and wages fail to keep up with soaring inflation. Introducing the potential of an additional $2,000 annual tax burden at least for those already struggling, mainly to subsidize high-income earners, adds insult to injury. Furthermore, it’s vital to recognize that the burden of unpaid student loans should not fall on low-income earners or Americans who did not attend college. Incentives play a crucial role in influencing markets. By removing the incentive for student loan borrowers to repay their debts, we may encourage more individuals to pursue higher education and accumulate debt without the intention of paying it back. After all, why would they when it can be written off through higher taxes for everyone? The ripple effect of this plan could be far-reaching. It may make college more accessible for some, opening the floodgates for students and the need for universities to expand and hire more staff, leading to even higher college tuition. This perverse incentive will set a precedent that will create a cycle of soaring tuition, which would counteract the original goal of making higher education more affordable. While the intention behind President Biden’s student loan forgiveness may appear noble (in likelihood, it is a rent-seeking move), the results may prove detrimental to our nation’s economic stability and fairness. And if the debt is monetized, more inflation will result. Forgiving student loans will exacerbate existing problems, with the brunt of the burden falling on lower-income Americans. Instead of improving the situation, it will likely create an intricate web of financial consequences, indirectly affecting the very people it aims to help. But that is the result of most government programs with good intentions. Originally published at Econlib. Check out the highlights from my recent segment on Fox Business. Former Office of Management and Budget chief economist Vance Ginn and Slatestone Wealth chief market strategist Kenny Polcari analyze how the Middle East conflict and House speaker standstill impact markets.

Full segment on Fox Business here. Please subscribe to my newsletter if you haven’t already, and subscribe to my podcast wherever you get yours. You can find direct links to follow my work at the buttons at the end of this post. I would appreciate it if you would also rate and review my podcast! Ben (bio) and I discuss:

Please subscribe to my newsletter if you haven’t already, and subscribe to my podcast wherever you get yours. You can find direct links to follow my work at the buttons at the end of this post. I would appreciate it if you would also rate and review my podcast! Today, I cover:

Highlights

Overview

The Bureau of Labor Statistics recently released its U.S. jobs report for April 2023, which was another mixed report with some strengths but many weaknesses.

Economic Growth The U.S. Bureau of Economic Analysis recently released the third estimate for economic output for Q2:2023.

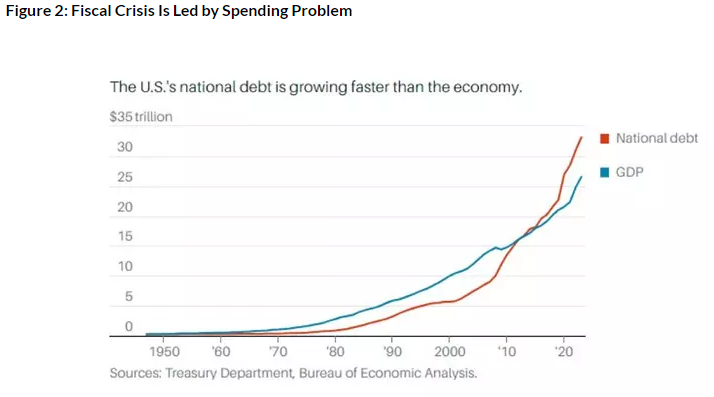

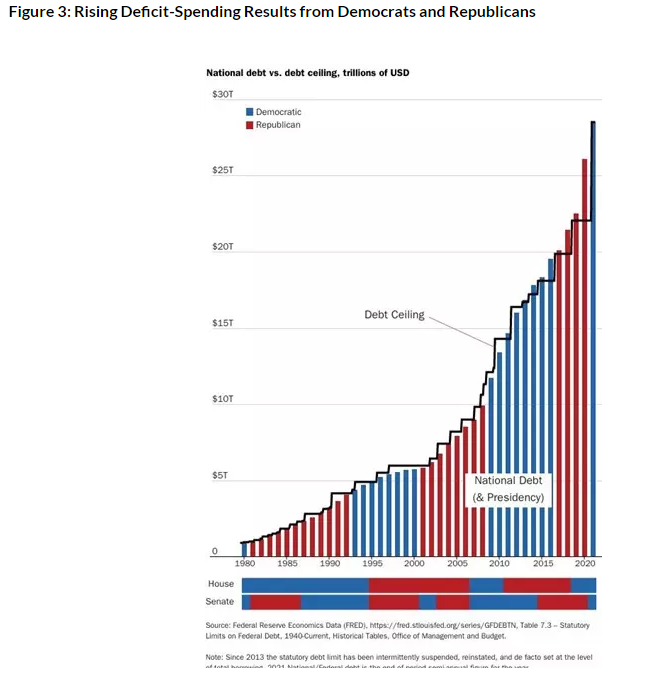

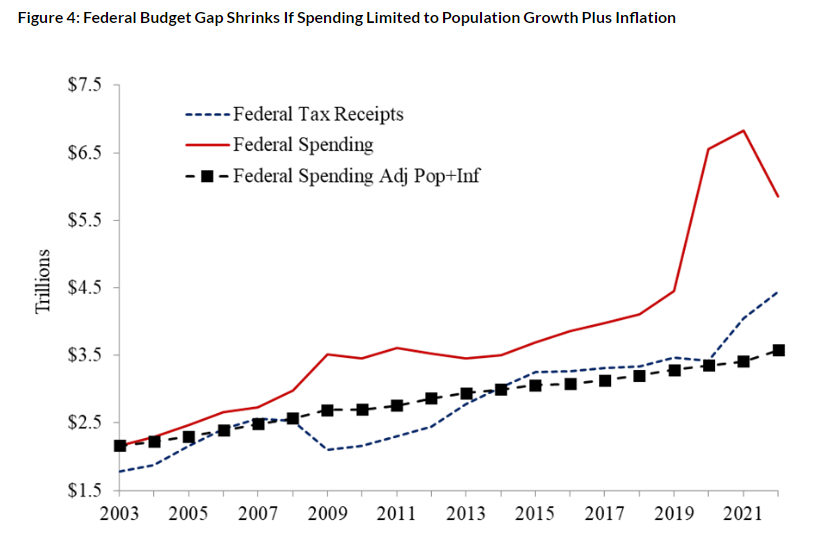

The latest indicator of this concern is U.S. real GDP was revised lower to just a 2.1% increase last quarter. Moreover, previous quarters were revised lower and there continue to be indications of a recession in early 2022 from two consecutive quarters of declining economic activity and relatively weak thereafter. Another measure of economic activity is the real average of GDP and GDI which accounts for domestic production and income. It increased by just 1.4% to $22.1 trillion. This important measure has declined in half of the last six quarters, increasing this value by only 1.2% since the first quarter of 2022, which is likely when the recession started. Meanwhile, the federal budget deficit is growing faster because of overspending and declining tax collections from a weak economy (See Figure 2). The national debt has ballooned to $33.5 trillion, and net interest payments on the debt will soon be a top federal expenditure of at least $1 trillion. Adding to these fiscal challenges are other large, unnecessary expenditures of taxpayer money.  The Fed has monetized, or printed, much of the new debt to keep interest rates artificially lower than where the market would have them. This created higher inflation as there was too much money chasing too few goods and services. And this has been exacerbated as production has been overregulated and overtaxed and workers have been given too many handouts. The Fed will need to cut its balance sheet (total assets over time) more aggressively if it is to stop manipulating markets (see this for types of assets on its balance sheet) and persistently tame inflation. The current annual inflation rate of the consumer price index (CPI) has been cooling since a peak of +9.1% in June 2022 but remains elevated at 3.7% in September 2023, which remains too high as are other key measures of inflation. Just as inflation is always and everywhere a monetary phenomenon, deficits and taxes are always and everywhere a spending problem. David Boaz at Cato Institute has noted how this problem is from both Republicans and Democrats (See Figure 3).  In order to get control of this fiscal crisis which is contributing to a monetary crisis, the U.S. needs a fiscal rule like the Responsible American Budget (RAB) with a maximum spending limit based on the rate of population growth plus inflation. This was recently released as part of Americans for Tax Reform’s Sustainable Budget Project. If Congress had followed this approach from 2003 to 2022, Figure 4 shows tax receipts, spending, and spending adjusted for only population growth plus chained-CPI inflation. Instead of an (updated) $19.0 trillion national debt increase, there could have been only a $500 billion debt increase for a $18.5 trillion swing in a positive direction that would have substantially reduced the cost of this debt to Americans. The Republican Study Committee recently noted the strength of this type of fiscal rule in its FY 2023 “Blueprint to Save America.” And to top this off, the Federal Reserve should follow a monetary rule so that the costly discretion stops creating booms and busts.  Bottom Line

The stagflationary destruction will continue given the “zombie economy” and the unraveling of the banking sector which will hit main street hard. Instead of passing massive spending bills, the path forward should include pro-growth policies that shrink government rather than big-government, progressive policies. It’s time for a limited government with sound fiscal and monetary policy that provides more opportunities for people to work and have more paths out of poverty. Recommendations:

This was originally posted at Texans for Fiscal Responsibility. Today, I'm joined on episode 65 of the "Let People Prosper Show" by Alexandra (Lexi) Hudson, writer, speaker, and founder of Civic Renaissance. Lexi (bio) and I discuss:

Please subscribe to my work on your favorite platform, follow me on social media, share my work, and like or leave a 5-star rating to help me spread this message to the masses!  Originally published at Texans for Fiscal Responsibility.

Texas Gov. Greg Abbott (R) is again promoting what could be universal school choice during the third special session in Texas that starts on Oct. 9th. That would be among the best actions Texas can make, the other being eliminating property taxes. School choice expert Corey DeAngelis recently noted, “Education funding is meant for educating children, not for protecting a particular institution. It’s time for Texas to fund students, not systems.” In the Texas Legislature’s regular session this year, several school choice bills were proposed, but all died. State Sen. Brandon Creighton (R-Conroe) had the best case for education savings accounts (ESA) in Senate Bill 8, and it passed the Senate with an 18-13 vote. But it died in the House Public Education Committee, where other school choice bills have died in previous sessions. Creighton’s proposal sought to establish an ESA program, the gold standard for school choice already adopted by ten states. ESAs provide parents with funds for each child, which can be used for various approved education-related and approved expenses. These expenses include traditional public schools, private school tuition, homeschooling materials, tutoring services, and more. They aren’t the derogatory word of “vouchers” thrown around by anti-school choice folks. Vouchers move funds from a government school to another school. ESAs, on the other hand, provide funds to parents for them to use for their kids, which is why they have been determined to work well within our constitutional system and provide accountability by parents on how they use the funds. This market-based, limited-government approach provides a productive path to achieving the goal of improving student outcomes at the least cost to taxpayers. But naysayers in the education system and supposed religious freedom advocacy groups are raising the alarm against school choice. Clay Robinson, spokesperson of the Texas Parent Teacher Association, recently asserted, “The more money you have to spend on private schools, the less you have to spend on public schools,” echoing a widely-held concern among rural voters. These arguments, however, are based on misleading premises. In reality, government schools wouldn’t have less spending on it unless parents chose to send their kids elsewhere because those schools didn’t meet their kids’ unique needs. This should be a concern for government school proponents, but this isn’t something that they want to address. Instead, proponents just want more funding for a flawed monopoly system. More funding should be rejected, as there is more being spent on government schools in Texas than ever before with dire outcomes. And rural school districts and their advocates who have long been the barrier to getting school choice passed have nothing to worry about. If there aren’t any other options for students, then they will continue to attend government schools. But I wonder if they know that, when there is competition in the marketplace, other options pop up meeting the demand; which would be a great outcome for families and teachers. ESAs can address a pressing issue of quality teachers. Texas teacher salaries are reported to lag behind the national average, which doesn’t account for the lower cost of living in Texas compared with many other states. However, this could contribute to a teacher shortage statewide, along with other concerns by teachers of the problems at government schools, including a large increase in funding to administrators rather than teachers. Only about 20% of every dollar going to the classroom goes to the teacher, so government schools should correct this failure before receiving any additional funding. The current government-run monopoly schooling system isn’t helping educators even as the system has received at least 16% in inflation-adjusted spending per student since 2002. Teachers in many states where government schools hold a monopoly have little to no negotiating power as they are stuck in the state’s pay schedule based on tenure and other limited factors. Moreover, lower-income families often find themselves trapped within government-run schools determined by district lines. And all of this is at a huge cost to taxpayers, threatening people of losing their homes from exorbitant property taxes, and declining student outcomes. ESAs, while not a silver bullet, substantially expand educational options, directing tax dollars to parents to do what’s best for their kids rather than to a bureaucratic, failing schooling system. States that have embraced universal school choice with ESAs are fostering competitive education markets, driving innovation, and achieving notable improvements in educational outcomes. Parents gain the power to choose the best educational options for their children, while teachers benefit from more professional opportunities and negotiating power. So, is the current government school system truly the best option for Texas? The answer will become apparent if we implement universal school choice for all children. Otherwise, the Lone Star State risks falling behind other states prioritizing educational freedom and student achievement. America’s system of free-market federalism, when allowed to function, reveals what works and what fails, resulting in a more prosperous society over time. Education deserves the same opportunities for experimentation and innovation. School choice has the potential to break the government-run schooling monopoly that stifles innovation and keeps costs high with declining outcomes. Equal funding to parents, who are taxpayers, for their kids, can reveal which schooling options truly earn parental support, thereby incentivizing educators and administrators to innovate and provide our children with the education they deserve. As the third special legislative session starts, the Texas Legislature must prioritize responsible stewardship of taxpayer funds and embrace the transformative potential of universal school choice. It’s time for Texas to lead the way, empowering parents, nurturing educational freedom, and ensuring our children have the brightest possible future. Anything less would be a disappointment, and worse, a tragedy for the future of the bright young minds of tomorrow. Thank you for listening to the 29th episode of "This Week's Economy," where I briefly recap and share my insights on key economic and policy news. Today, I cover:

1) National: No government shut down as Congress passes a continuing resolution budget, House Speaker Kevin McCarthy kicked out with a new speaker to be voted in next Wednesday, presidential candidate Nikki Haley bashes excessive government spending and signs Taxpayer Protection Pledge as all candidates should, and latest jobs report reveals overall weakness; 2) States: Americans for Tax Reform released its Sustainable Budget Project for states that I helped author and Texas will have another special legislative session this Monday to discuss passing Universal School Choice; and 3) Other: My latest op-eds, including one published by The Wall Street Journal with Grover Norquist on the national and state spending problems, and another published by The Daily Caller on why the FTC suing Amazon over antitrust concerns is a waste of time and taxpayer dollars. Please subscribe to my work on your favorite platform, follow me on social media, share my work, and like or leave a 5-star rating to help me spread this message to the masses!  In the tapestry of human history, one recurring thread stands out – the need for limited power in leadership.

As far back as the 7th century B.C., Homer explored this theme with remarkable insight in his timeless epic, "The Iliad." In modern-day America, where today’s leaders often assume too much power, Homer's lessons about the imperfections of inflated authority offer valuable insights. Recognizing the perils of excessive control, he creatively described what could be key to combating pressing issues today. In "The Iliad," the gods of ancient Greece held dominion over justice and politics, not wholly unlike today's political leaders. Yet, Homer masterfully portrayed the limitations and imperfections of these gods, revealing that even the mightiest beings are not immune to human-like foibles. These divine beings often acted out of self-interest. They were susceptible to basing actions on desires or petty grievances, making them appear more human than celestial. For instance, Zeus, the king of the gods, is reluctant to help the Trojans because of his disapproving wife, Hera, who strongly favors the Greeks. Zeus acts to maintain harmony, which is seen in Book IV of "The Iliad," when he contemplates helping the Trojans in battle but ultimately refrains from directly interfering. His hesitation reflects his complex role as the ruler of the gods, the upholder of fate, and his desire to manage the divine politics within Mount Olympus. When not hoping to maintain marital harmony as Zeus did, the other gods often behaved out of concern for personal honor, which was highly valued in ancient Greece. The discord between Agamemnon and Achilles exemplifies this theme. As the leader of the Achaean forces, Agamemnon believed he deserved the highest prize, Briseis, and was willing to oppress Achilles, a crucial warrior in the Trojan battle, to claim her. Achilles, in turn, prioritized his claim to Briseis over aiding the war efforts. Both placed their honor and pursuit of what they believed was rightfully owed to them above the collective well-being, jeopardizing the battle’s victory. In one instance, Apollo admitted that his intervention wasn't driven by compassion for the Trojans but by a desire to protect his favored hero, Hector. This acknowledgment underscores the willingness of the gods to manipulate events for personal gain as opposed to the greater good. The parallel between the gods of "The Iliad" and contemporary leadership is their susceptibility to act in self-interest. While the gods may seem all-powerful, their actions often reveal a profound concern for their agendas and favored heroes. Although not as strong a principle today, personal honor preservation reveals itself in modern leaders through rent-seeking behavior. We see elected officials sometimes prioritize their agendas, party interests, or re-election prospects over the welfare of their nations and citizens. Just as Zeus was more concerned with appeasing influential people, politicians may succumb to surrounding pressure, foregoing long-term goals of improving the country. Today's America faces numerous challenges, from mounting national debts to housing affordability, inflation, and stagnant wages. These issues often stem from government overreach and misguided policies, reminiscent of the interference of the gods in "The Iliad." It is crucial to recognize that unchecked government power can lead to a loss of personal liberties and economic prosperity. In contemplating the lessons from Homer's "The Iliad," we discover that unchecked power carries inherent risks, whether in the hands of gods or modern leaders. Pursuing self-interest, personal glory, and re-election can overshadow the well-being of nations, leaving citizens to bear the consequences of misguided decisions. We must limit government power, embrace free markets, and prioritize the greater good derived from individual gain to mitigate these risks. As the characters in Homer's epic grappled with the consequences of self-interested gods, we, too, must seek to promote paths that seek to empower the people and limit the government as our forefathers intended. By doing so, we can create a world where the lessons of "The Iliad" guide us toward better governance and a brighter future. In heeding these ancient warnings, we can navigate the complexities of contemporary leadership and secure a more prosperous future for all. Originally published by Online Library of Liberty's Banned Books series.  The Fraser Institute recently released its annual “Economic Freedom of the World” report. While the US inched up one spot from its previous ranking to fifth-best, this ranking remains below its peak of third-best in 2000.

A first-time finding not seen in any of 27 prior years: Hong Kong fell from first place. Singapore nudged out Hong Kong for the top spot by 0.01 points. While that rating may seem minuscule, the implications of how both countries got here are not. The report, which shows comprehensive data from 2021, assesses economic freedom among nations across five major areas: size of government, legal system and property rights, sound money, freedom to trade internationally, and regulations. According to the Fraser Institute’s Matt Mitchell, “The most important component of economic freedom…is the rule of law section…you need to be able to trust that the contracts you form and the property you acquire will be protected. We found that regulatory barriers and the rule of law matter more than taxes [for economic freedom].” Given these guidelines, Hong Kong’s fall isn’t surprising. China’s special administrative region allowed to manage most of its own affairs under the “one country, two systems” precedent since 1997, Hong Kong’s independence has been seriously threatened since 2020 with the passage of China’s new security law. Today, as a result, Hong Kong has one of the fastest-growing political prisoner populations worldwide. Although the protection of Hong Kong’s independence under the system was set to last until 2047, it seems unlikely that China will keep its promise. Over the past two years, Hong Kong’s economic freedom ranking dropped by a substantial 0.40 points, a total decline of 0.64 points since its highest rating of 9.19 in 2010. This is much steeper than the average economic freedom drop worldwide following the pandemic, which is the lowest average score since 2009, pointing to China’s harsh policies as a primary factor. China’s recent security law inhibits free speech and impartial justice, integral to the rule of law which is the foundation upon which individuals can construct their economic aspirations, with trust as the indispensable glue. But trust isn’t just a legal concept. It’s deeply interwoven with a nation’s cultural fabric. Trust is the bedrock upon which economic prosperity thrives, allowing individuals and businesses to engage in voluntary exchanges with confidence. Recent developments, including China imposing significant trade barriers, limits to foreign labor employment, increased business costs, and new attempts to restrict media, tarnished Hong Kong’s overall score. The lesson from the report rings loud and clear: A small government footprint in fiscal matters alone won’t guarantee economic freedom. What’s needed is a symphony of elements: the rule of law, property rights, stable currency, open trade, and sensible regulation. High-income industrial economies like now top-ranking Singapore shine in areas related to legal systems, property rights, sound currency, and international trade while keeping their government size compact. The report is a valuable tool for deciphering economic freedom’s complexities, and the factors underlying the success story of Singapore and Hong Kong’s decline drive home the point that tax rates don’t solely determine economic prosperity. It hinges on the quality of institutions, the rule of law, and the cultural values that champion trust and voluntary exchange. As the US strives to enhance its economic freedom, the country would be wise to heed the lessons offered by Singapore’s rise and Hong Kong’s fall. In particular, this should include removing government barriers so that there are more ways for free people to prosper. Originally published at American Institute for Economic Research.  Originally published at American Institute for Economic Research.

The Fraser Institute recently released its annual “Economic Freedom of the World” report. While the US inched up one spot from its previous ranking to fifth-best, this ranking remains below its peak of third-best in 2000. A first-time finding not seen in any of 27 prior years: Hong Kong fell from first place. Singapore nudged out Hong Kong for the top spot by 0.01 points. While that rating may seem minuscule, the implications of how both countries got here are not. The report, which shows comprehensive data from 2021, assesses economic freedom among nations across five major areas: size of government, legal system and property rights, sound money, freedom to trade internationally, and regulations. According to the Fraser Institute’s Matt Mitchell, “The most important component of economic freedom…is the rule of law section…you need to be able to trust that the contracts you form and the property you acquire will be protected. We found that regulatory barriers and the rule of law matter more than taxes [for economic freedom].” Given these guidelines, Hong Kong’s fall isn’t surprising. China’s special administrative region allowed to manage most of its own affairs under the “one country, two systems” precedent since 1997, Hong Kong’s independence has been seriously threatened since 2020 with the passage of China’s new security law. Today, as a result, Hong Kong has one of the fastest-growing political prisoner populations worldwide. Although the protection of Hong Kong’s independence under the system was set to last until 2047, it seems unlikely that China will keep its promise. Over the past two years, Hong Kong’s economic freedom ranking dropped by a substantial 0.40 points, a total decline of 0.64 points since its highest rating of 9.19 in 2010. This is much steeper than the average economic freedom drop worldwide following the pandemic, which is the lowest average score since 2009, pointing to China’s harsh policies as a primary factor. China’s recent security law inhibits free speech and impartial justice, integral to the rule of law which is the foundation upon which individuals can construct their economic aspirations, with trust as the indispensable glue. But trust isn’t just a legal concept. It’s deeply interwoven with a nation’s cultural fabric. Trust is the bedrock upon which economic prosperity thrives, allowing individuals and businesses to engage in voluntary exchanges with confidence. Recent developments, including China imposing significant trade barriers, limits to foreign labor employment, increased business costs, and new attempts to restrict media,l tarnished Hong Kong’s overall score. The lesson from the report rings loud and clear: A small government footprint in fiscal matters alone won’t guarantee economic freedom. What’s needed is a symphony of elements: the rule of law, property rights, stable currency, open trade, and sensible regulation. High-income industrial economies like now top-ranking Singapore shine in areas related to legal systems, property rights, sound currency, and international trade while keeping their government size compact. The report is a valuable tool for deciphering economic freedom’s complexities, and the factors underlying the success story of Singapore and Hong Kong’s decline drive home the point that tax rates don’t solely determine economic prosperity. It hinges on the quality of institutions, the rule of law, and the cultural values that champion trust and voluntary exchange. As the US strives to enhance its economic freedom, the country would be wise to heed the lessons offered by Singapore’s rise and Hong Kong’s fall. In particular, this should include removing government barriers so that there are more ways for free people to prosper.  A recent survey found that 25 out of 100 Americans buy items on Amazon at least once per week. But the Biden administration’s Federal Trade Commission’s (FTC) decision to sue Amazon in federal court for supposedly violating antitrust law last week could change that for consumers.

Specifically, the FTC claims that “Amazon’s ongoing pattern of illegal conduct blocks competition, allowing it to wield monopoly power to inflate prices, degrade quality, and stifle innovation for consumers and businesses.” This federal case will waste a lot of time and taxpayer money as it has no basis. In the Pelican Institute’s recent research, we highlighted the radicalism by those looking to make political points regarding antitrust enforcement instead of following the half-century, objective consumer welfare standard. As history has proven, empowering people in the marketplace rather than bureaucrats in government results in more efficient and effective outcomes and better supports liberty and prosperity. The FTC’s Chair, Lina Khan, and Assistant Attorney General Jonathan Kanter of the Department of Justice’s antitrust division, have been doubling down on the administration’s aggressive approach to antitrust enforcement. This is the latest example, and they haven’t had a good track record. Antitrust laws were designed to protect consumers and promote fair competition but rarely achieve these goals. Inevitably, businesses become the antitrust enforcement targets, resulting in less economic growth, innovation, and job creation, leading to higher prices and hindered prosperity. In short, consumers and employers are hurt by antitrust overreach, which will result from this sham case against Amazon by the FTC. And it will mean other companies must increase their legal team because they may be next. Protecting consumer welfare, which refers to the value consumers receive above the price they pay for goods and services, should be the driving force behind antitrust enforcement. This acknowledges that consumers have the sovereignty to make decisions supporting the competitive market process. If not, we will have much less consumer satisfaction, which would be unfortunate because of the administration’s radical approach in the Amazon case. Instead, common sense should lead the way so that Amazon can continue to provide the satisfaction demanded by consumers rather than be directed by government. Originally posted at Pelican Institute. Federal and state layouts are vastly outpacing the combined rate of inflation and population growth.  The U.S. national debt recently passed $33 trillion, more than 120% of gross domestic product. Left-wing politicians assert that Americans are undertaxed, but the data show that the government spends too much.

Americans for Tax Reform launched the Sustainable Budget Project in September to document the rise in government spending over the past decade. The results are clear: Overspending is the problem. Between 2013 and 2022, aggregate annual spending by the 50 state governments, excluding federal funds, increased 51.7%. Total annual federal spending rose 69.4% during the decade, more than three times as fast as the 21.6% increase in the rate of population growth plus inflation. If government grows faster than this rate, then it is growing faster than what the average taxpayer can afford. Had the federal government limited the growth in spending to a maximum of the population growth rate plus inflation during that decade, in 2022 the federal government would have spent $1.6 trillion less than it did, resulting in at least a $200 billion surplus. If the federal government had done this over the past two decades, the national debt would have increased by less than $500 billion instead of $19 trillion. If state governments had limited spending growth to the rate of population growth plus inflation during the last decade, they would have spent $1.39 trillion in 2022, $344 billion less than the $1.74 trillion they actually spent. Had federal and state governments simply grown no faster than the rate of population growth plus inflation, taxpayers could have been spared at least $2 trillion in taxes and debt in 2022 and trillions of dollars more over time. The U.S. hasn’t needed drastic budget cuts, just slower, more sustainable debt growth. Our project defines each state’s overspending problem by providing a dollar-figure spending ceiling and allowing anyone to see how government spending in a state has grown relative to the rate of population growth plus inflation. It will publish and promote an annual benchmark spending level for every state, which lawmakers must not exceed if they want to keep state spending in check. Limiting state spending to the Sustainable Budget Project benchmark isn’t impossible. Lawmakers in more states are beginning to implement the sorts of structural reforms necessary to slow the rate of government spending to a sustainable clip. During the past decade, Colorado and Texas have demonstrated that this can be done. Colorado spent a cumulative $12.8 billion less over the past decade than what could have been available under the benchmark. State lawmakers could have dramatically cut the state’s individual income tax. Instead, there is a push in Colorado to raise taxes and destroy the Taxpayer’s Bill of Rights, the state’s constitutional requirement that all tax increases be subject to voter approval and revenue collected in excess of the state spending cap be refunded to taxpayers. Texas spent $16.4 billion less than the benchmark over the past decade, savings that could have been used to eliminate its gross-receipts-style franchise tax and other bad taxes. Rather than continuing to keep state spending in check, Texas lawmakers instead passed the largest state budget in the state’s history this year. Excessive spending at the federal, state and local levels of government deserves more attention. Tax hikes are easy to identify, but there has been no objective, binary metric to determine whether a state government spends too much. By focusing on the rate of population growth plus inflation, the Sustainable Budget Project provides such a standard. Governors and state legislators need to implement reforms and practice restraint to slow the steep upward trajectory of government spending. That lawmakers in large, politically important states have already demonstrated this ability has shown their counterparts in other states and in Washington that sustainable budgeting is possible. With more modest growth in state government spending, lawmakers can lower taxes and Americans can keep more of what they earn. Mr. Norquist is president of Americans for Tax Reform. Mr. Ginn, a senior fellow at ATR, served as chief economist of the White House’s Office of Management and Budget, 2019-20. Originally published at Wall Street Journal.  Just weeks after launching its pointless lawsuit against Google, Biden’s Federal Trade Commission set its sights on Amazon, beginning the process of suing one of Americans’ favorite companies.

While government regulation is often portrayed as a means to protect consumers, this lawsuit appears to be another attempt to control the marketplace, with potentially detrimental consequences for consumers, competition and innovation. The Amazon lawsuit is part of the FTC’s ongoing tirade against businesses, including “Big Tech,” that they accuse of violating antitrust law. But the real “violation” here is against free-market capitalism and human flourishing. The FTC takes issue with how Amazon manages its online marketplace for sellers, claiming that sellers are forced to charge high prices and lose profit by using Amazon’s add-on services and advertisements. Both of which are optional. It’s not unlike how popular media platforms employ algorithms to favor certain types of content, which some people may try to circumvent by purchasing ad campaigns. But the FTC claims these choices are optional “in name only” and that Amazon is operating like a monopoly, forcing customers to pay higher prices for lower quality products. And just like with the Google lawsuit, the real problem reveals itself with this complaint. Antitrust laws were established to preserve competition and protect consumers. They focus on the consumer welfare standard, which evaluates whether consumers are better or worse off due to a company’s actions. Research, however, shows that Amazon’s consumers are pleased with the service. Otherwise, they’d stop using it. According to the latest American Customer Satisfaction Index, Amazon takes first place for its selection, value and online shopping experience. And what’s more, NetChoice polling shows a staggering 84 percent of Americans and 92 percent of Republicans view the FTC’s lawsuit against Amazon as a waste of resources. If the FTC prevails, the result could be fewer product choices, higher prices, slower deliveries and fewer opportunities for small businesses — an outcome contrary to the intended purpose of antitrust laws. This lawsuit threatens to waste taxpayers’ dollars that could be better utilized elsewhere, particularly when the economy faces challenges like the labor shortage, high housing costs and inflation, to say nothing of Congress’ refusal to avoid accruing more debt. It also highlights the knowledge problem that economist Friedrich Hayek pointed out. Central planners lack the dispersed knowledge necessary to determine market dynamics effectively. Manipulating markets through government intervention often leads to unintended consequences, undermining the principles of free-market capitalism. The FTC’s lawsuit against Amazon raises serious concerns about its true intentions and potential negative consequences. Rather than stifling free markets and wasting resources, government should focus on getting out of the way of productive activities that benefit consumers, workers and employers alike. Originally posted Daily Caller. dailycaller.com/2023/10/03/ginn-ftc-amazon-big-tech-tirade-free-market/ |

Vance Ginn, Ph.D.

|

RSS Feed

RSS Feed

Proudly powered by Weebly