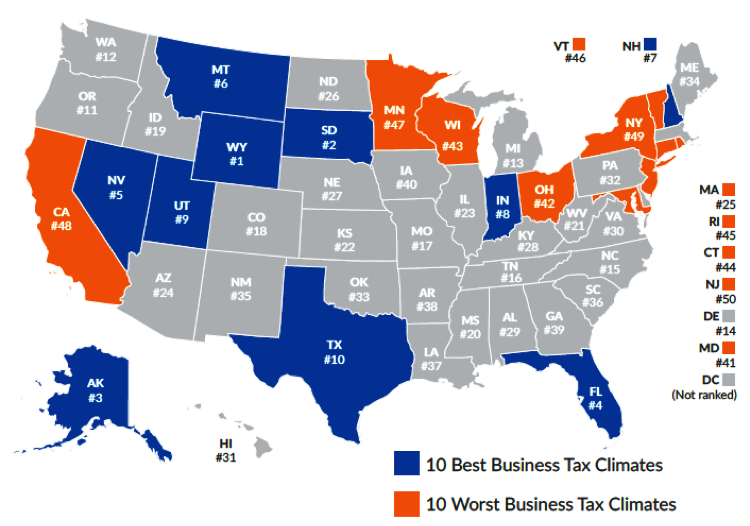

Originally published at American Institute for Economic Research.

The rise of several underdog states and the fall of previous favorites tells the story of the Tax Foundation’s new 2024 State Business Tax Climate report. The findings support how less government contributes to more flourishing, while heavy-handed taxes hinder prosperity. The scores for the 50 states in the report declined by 0.19 points from the prior report, indicating a less overall competitive business tax climate nationwide. Considering that half of all states have cut taxes over the past three years, and an increasing number are moving to flax taxes, pressure is building on states to seek tax cuts or risk getting left behind. An inspiring success story is Iowa, which has emerged as a beacon of pro-growth tax reform. Iowa reduced its top marginal individual income tax rate from 8.53 to 6.0 percent. By consolidating its previous nine tax brackets into four, the newer, more streamlined tax system is less burdensome for Iowans. Another improvement in Iowa’s reforms was reducing the marriage penalty. The state removed a longstanding tax burden by doubling the bracket amounts for married couples filing jointly. The state also shifted its previously three-bracket corporate income tax structure into just two brackets, which caused the top rate to drop by 1.4 percentage points. As a result of these changes, Iowa’s ranking improved from 38th to 33rd in just one year. While there’s room for improvement, the state is on a better path. Considering the conservative budgeting by Governor Reynolds and the legislature, and the transition to a flat 3.9 percent income tax rate by 2026 and a flat corporate income tax rate of 5.5 percent, the state could soon be on its way to 15th place. Massachusetts, on the other hand, experienced the sharpest decline of all the states, plummeting 12 places down to 46th. This regression in business tax competitiveness can be largely attributed to a new state constitutional amendment. It transitioned Massachusetts from a single-rate to a graduated-rate income tax system with a new 4 percent surtax for a top marginal tax rate of 9 percent for incomes over $1 million. This progressive policy not only represents a departure from the trend of rate reductions and bracket consolidation in other states as part of the flat tax revolution, but also introduces a significant marriage penalty. While implementing a new payroll tax further contributed to Massachusetts’s decline in tax competitiveness, the state’s individual tax component ranking fell from 11th to 44th. Unfortunately, this fall was foretold by the vast number of people fleeing the state, many of whom were no doubt searching for a more tax-friendly place of residence. After all, people vote with their feet. While Massachusetts experienced a sharp fall, Mississippi and Idaho emerged as rising stars in the world of tax reform. Mississippi’s ranking jumped from 27th to 20th thanks to three major shifts. It became the second state to implement permanent full expensing for select investment in machinery and equipment, passed a flat personal income tax, and will soon phase out its franchise tax. These forward-thinking policy changes encourage investment and economic growth, positioning Mississippi as a more competitive business destination. Likewise, Oklahoma has also made significant strides in tax reform. In addition to eliminating its marriage penalty, the state reduced its split roll ratio in property taxation and withdrew its capital stock tax. These actions propelled its property tax component ranking to substantially improve from 30th to 15th. As a result of these reforms, Oklahoma’s overall ranking has risen significantly, now at 19th. And while Governor Stitt’s recent special session was unsuccessful in making bigger strides for tax cuts, the state looks poised to do so soon, thereby improving its competitiveness. On a similar path, Idaho made a noteworthy move by transitioning from four brackets to a flat individual income tax at 5.8 percent. Additionally, the state cut its corporate income tax rate to 5.8 percent, further enhancing its tax competitiveness. These reforms boosted its individual tax component rank by two places, now at 17th. The findings from the Tax Foundation’s report underscore a fundamental economic truth: Free markets do not discriminate. They thrive where they are permitted to flourish, and that starts with sustainable budgeting and sound tax policy. States like Iowa, Oklahoma, Mississippi, and Idaho, which prioritize tax cuts and financial freedom, are poised to rise in the rankings and could quickly become some of the more sought-after states. As they continue to reduce tax burdens, they create environments where individuals and businesses can retain more of their earnings, which invites innovation, improves the quality of life, and encourages moving to those states. Meanwhile, states like Massachusetts and New Jersey, which ranks 50th in the report, choose high spending and taxes that will contribute to continued out-migration as individuals and businesses seek refuge in states prioritizing economic freedom. The message is unmistakable. Free markets work, and policymakers should heed the lessons from these tax climate rankings.

0 Comments

The rise of several underdog states and the fall of previous favorites tells the story of the Tax Foundation’s new 2024 State Business Tax Climate report. The findings support how less government contributes to more flourishing, while heavy-handed taxes hinder prosperity.

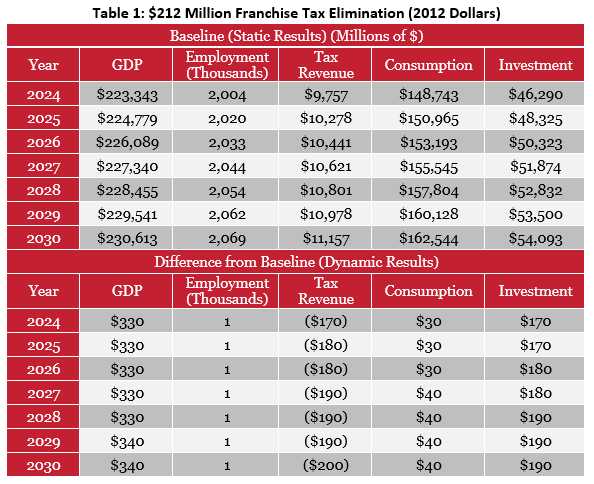

The scores for the 50 states in the report declined by 0.19 points from the prior report, indicating a less overall competitive business tax climate nationwide. Considering that half of all states have cut taxes over the past three years, and an increasing number are moving to flax taxes, pressure is building on states to seek tax cuts or risk getting left behind. An inspiring success story is Iowa, which has emerged as a beacon of pro-growth tax reform. Iowa reduced its top marginalindividual income tax rate from 8.53 to 6.0 percent. By consolidating its previous nine tax brackets into four, the newer, more streamlined tax system is less burdensome for Iowans. Another improvement in Iowa’s reforms was reducing the marriage penalty. The state removed a longstanding tax burden by doubling the bracket amounts for married couples filing jointly. The state also shifted its previously three-bracket corporate income tax structure into just two brackets, which caused the top rate to drop by 1.4 percentage points. As a result of these changes, Iowa’s ranking improved from 38th to 33rd in just one year. While there’s room for improvement, the state is on a better path. Considering the conservative budgeting by Governor Reynolds and the legislature, and the transition to a flat 3.9 percent income tax rate by 2026 and a flat corporate income tax rate of 5.5 percent, the state could soon be on its way to 15th place. Massachusetts, on the other hand, experienced the sharpest decline of all the states, plummeting 12 places down to 46th. This regression in business tax competitiveness can be largely attributed to a new state constitutional amendment. It transitioned Massachusetts from a single-rate to a graduated-rate income tax system with a new 4 percent surtax for a top marginal tax rate of 9 percent for incomes over $1 million. This progressive policy not only represents a departure from the trend of rate reductions and bracket consolidation in other states as part of the flat tax revolution, but also introduces a significant marriage penalty. While implementing a new payroll tax further contributed to Massachusetts’s decline in tax competitiveness, the state’s individual tax component ranking fell from 11th to 44th. Unfortunately, this fall was foretold by the vast number of people fleeing the state, many of whom were no doubt searching for a more tax-friendly place of residence. After all, people vote with their feet. While Massachusetts experienced a sharp fall, Mississippi and Idaho emerged as rising stars in the world of tax reform. Mississippi’s ranking jumped from 27th to 20th thanks to three major shifts. It became the second state to implement permanent full expensing for select investment in machinery and equipment, passed a flat personal income tax, and will soon phase out its franchise tax. These forward-thinking policy changes encourage investment and economic growth, positioning Mississippi as a more competitive business destination. Likewise, Oklahoma has also made significant strides in tax reform. In addition to eliminating its marriage penalty, the state reduced its split roll ratio in property taxation and withdrew its capital stock tax. These actions propelled its property tax component ranking to substantially improve from 30th to 15th. As a result of these reforms, Oklahoma’s overall ranking has risen significantly, now at 19th. And while Governor Stitt’s recent special session was unsuccessful in making bigger strides for tax cuts, the state looks poised to do so soon, thereby improving its competitiveness. On a similar path, Idaho made a noteworthy move by transitioning from four brackets to a flat individual income tax at 5.8 percent. Additionally, the state cut its corporate income tax rate to 5.8 percent, further enhancing its tax competitiveness. These reforms boosted its individual tax component rank by two places, now at 17th. The findings from the Tax Foundation’s report underscore a fundamental economic truth: Free markets do not discriminate. They thrive where they are permitted to flourish, and that starts with sustainable budgeting and sound tax policy. States like Iowa, Oklahoma, Mississippi, and Idaho, which prioritize tax cuts and financial freedom, are poised to rise in the rankings and could quickly become some of the more sought-after states. As they continue to reduce tax burdens, they create environments where individuals and businesses can retain more of their earnings, which invites innovation, improves the quality of life, and encourages moving to those states. Meanwhile, states like Massachusetts and New Jersey, which ranks 50th in the report, choose high spending and taxes that will contribute to continued out-migration as individuals and businesses seek refuge in states prioritizing economic freedom. The message is unmistakable. Free markets work, and policymakers should heed the lessons from these tax climate rankings. Originally published at AIER.  There’s much discussion in Baton Rouge about how to best allocate scarce taxpayer money that’s overflowing the state’s coffers. A problem with $3 billion in the state’s savings accounts is that everyone has their hands out to receive some of it. But the ones who should be remembered first are the taxpayers. In this discussion, one of the bright spots is tax reform, particularly eliminating the state’s corporate franchise tax. The corporate franchise tax is levied annually on the taxable capital of corporations, including capital stock, surplus, and undivided profits. Unlike corporate income taxes, which are levied on a company’s profits, these taxes are imposed on a company’s net worth. Therefore, the tax penalizes investment and requires companies to pay the tax regardless of whether they make a profit. While it’s just three percent of the state’s revenue, it’s a large burden on businesses as only 16 states have one and two of them (i.e., Connecticut and Mississippi) are phasing theirs out. Louisiana should eliminate its corporate franchise tax, too. There were improvements to the franchise tax in the state’s 2021 tax reforms that reduced the rate and increased the minimum amount needed to begin paying the tax. Those reforms also included revenue triggers which would reduce personal income taxes and corporate franchise taxes if three revenue targets are hit. This tax could be reduced substantially this session. The first two triggers are already hit so the Legislature simply needs to add about $55 million to the rainy day fund to hit the final one and there could be at least a 50 percent cut in the corporate franchise tax rate. And State Senator Bret Allain’s SB 1 could help make this phase out more certain. Eliminating this tax would result in increased productivity, faster economic growth, higher consumption, and greater investment. We’ve been working with the Economic Research Center to examine the economic effects of eliminating this tax. Their model estimates the dynamic effects of tax changes on economic variables. Table 1 includes the dollar values reported in millions of 2012 inflation-adjusted dollars and are based on the estimates in the Congressional Budget Office’s February 2023 economic projections. Employment is represented by full-time equivalent non-farm jobs, in thousands of jobs.  Removing this tax on capital would support more investment and economic output over time with the largest effect in the first year. Their results show that eliminating the costly corporate franchise tax would result in gross domestic product (GDP) increasing by $330 million, with employment increasing by at least 1,000 jobs, consumer spending increasing by $30 million, and investment jumping by $170 million in 2024.

And the inflation-adjusted value of a $212 million franchise tax cut would result in just $170 million in reduced total tax revenue because the increased economic growth, employment, and investment contributes to higher collections in other taxes, such as the personal income tax because there are more people working. Of note, the temporary reduction in tax revenue won’t affect the state’s budget. Over the last three fiscal years, the state has seen a boom in corporate income and franchise tax revenues, such that, according to law, anything collected over $600 million in this category automatically goes into a savings account—the Revenue Stabilization Fund—to help offset future decreases in revenue. This money is not even in the state’s operating budget, so it won’t be missed. Louisiana is hemorrhaging people and businesses as they move to other nearby states with better tax systems. The Legislature has a chance to stop the bleeding so the state and Louisianans can heal and become more prosperous over time. There’s a great opportunity to do so now. Lawmakers can pass a responsible budget, activate revenue triggers for tax relief, and set the state on a path toward ending this punishing tax so our state can be competitive. Originally published by Pelican Institute.  Recent data from the Tax Foundation reveals that Louisiana has the highest average combined state and local sales tax rate of all the states. The bulk of this burden comes from its local taxes, the second highest in the nation.  Pair these findings with Louisiana’s progressive income taxes of a graduated personal income tax rate of up to 4.25% and a corporate income tax rate max of 7.50%, and there’s no wonder why the Pelican State has a net out-migration problem. According to the Tax Foundation’s business tax climate index, the state ranks 12th worst in the country.  Personal income taxes disincentivize work, and sales taxes can lead consumers to shop elsewhere and businesses to relocate. Employers and consumers want to be where they can keep more of what they earn, which helps explain why Florida, a state with no personal income taxes and a combined sales and local tax rate that’s more than 2.5-percentage points lower than Louisiana’s, had the highest net in-migration last year.  Clearly, Louisiana’s tax code needs an overhaul if the growth and flourishing of Louisianans are priorities. But so does the state’s spending. To start, the Pelican State could consider joining the 14 states in the flat-income tax revolution. As more states flatten or remove their personal income taxes, Louisiana’s costly progressive income taxes will become much less appealing. Moving to flat personal and corporate income taxes would be a pro-growth step forward toward the eventual greater goal of eliminating these costly taxes, helping to compete with places like Florida and Texas, both of which don’t have personal income or corporate income taxes. Considering that the ultimate burden of government is how much it spends, reforming the tax code is just one piece of the puzzle. The excessive government spending at the state and local levels, compared with reasonable metrics like the rate of population growth plus inflation which helps measure the average taxpayer’s ability to pay for government spending, burdens Louisianans. Furthermore, Louisiana’s state and local debt is estimated to be about $7,600 per person owed by 2027, plus another nearly $28,000 per person owed in unfunded liabilities over time, so there are clearly massive barriers in the way for Louisianans to flourish. This is an issue because heavy spending leads to heavy burdens on state residents and decreased economic freedom, which Louisiana can’t afford to lose more of, considering how far it falls behind other states.  Not surprisingly, Georgia, Florida, and Texas all boast lower spending than Louisiana, with improved economic freedom and poverty rates. Meanwhile, Louisiana has the highest official poverty rate in the country. The rankings for the Pelican State aren’t quite as bad as the highly progressive states of New York and California, which are hemorrhaging population to other states. Incentives matter, so people are voting with their feet to flee high cost, low freedom states.

Louisiana should start its comeback story by adopting a stronger spending limit, similar to the one recently passed in Texas. Spending caps help governments stay limited, which is imperative for states to thrive as it forces them to narrow their scope. In turn, the private sector has more elbow room to grow and people have greater ability to prosper. This would also help provide more surplus funds to put toward cutting, flattening, and eventually eliminating personal and corporate income taxes. Louisiana has too great of a culture and too much potential for it to be squandered by burdensome spending and taxes. It’s time for serious spending restraint and major tax reforms to provide the best path forward. Originally published at Pelican Institute.  By Victor Skinner | The Center Square contributor | Feb 16, 2023

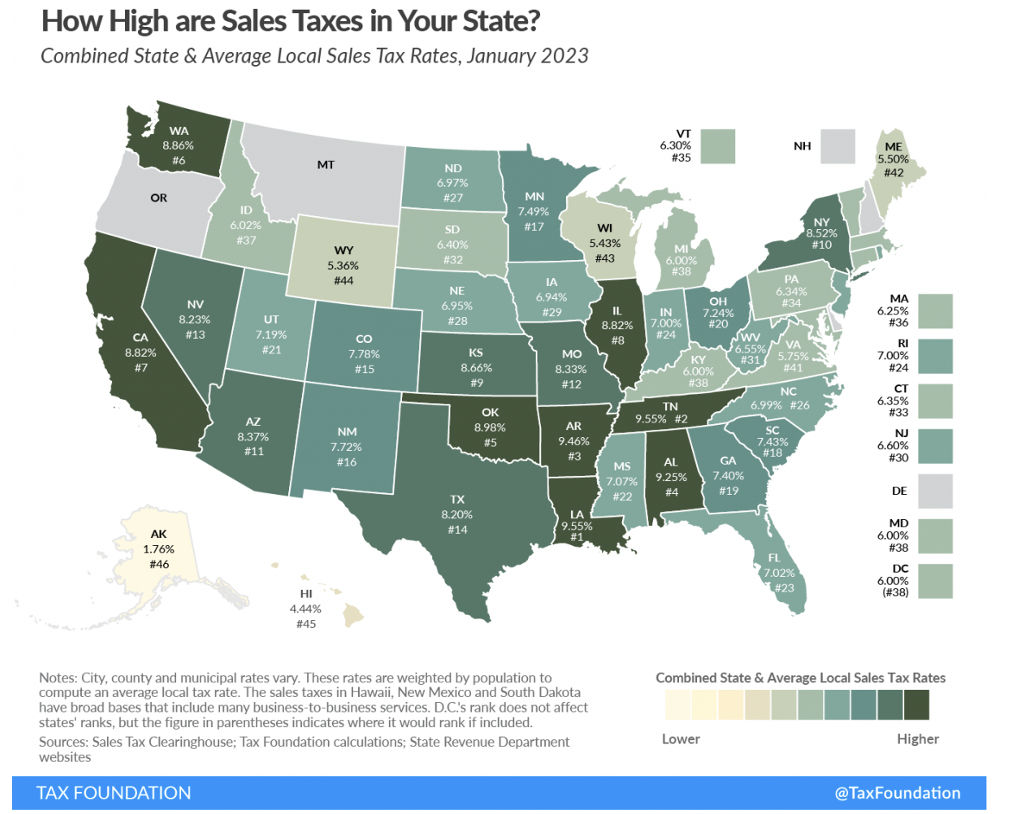

(The Center Square) – Louisiana’s combined state and local sales taxes are the highest in the nation, a reality critics contend is one of several tax and spending issues plaguing the state. The Tax Foundation released a report last week that compares state and local sales taxes across the nation, ranking states based on both the state sales tax and combined state and local rates. The research shows that as of Jan. 1, Louisiana’s state sales tax of 4.45% ranks 38th from the top. But when that figure is added to the average local tax rate of 5.10%, the state’s 9.55% combined rate becomes the highest among 50 states and the District of Columbia. "Sales taxes are just one part of an overall tax structure and should be considered in context," according to the report. "For example, Tennessee has high sales taxes but no income tax, whereas Oregon has no sales tax but high income taxes. While many factors influence business location and investment decisions, sales taxes are something within policymakers’ control that can have immediate impacts." The report comes as Louisiana lawmakers are studying potential changes to the state’s tax structure ahead of the 2023 legislative session. Vance Ginn, chief economist for the Pelican Institute, contends that excessive government spending is one factor driving higher taxes in Louisiana, though he believes personal income taxes are having the biggest impact on the state’s economy. "We have got to find a way to restrain excessive government spending at the state and local level," he said. "The sales tax is high in Louisiana … but really the focus should be on the burdensome income tax." The Pelican Institute is advocating for a flat income tax that eventually phases to zero. "That will allow for more job creation and economic growth," Ginn said. The Tax Foundation ranks Louisiana 25th nationally for income taxes, 32nd in the nation for corporate income tax, and 23rd for property taxes. Those rankings, combined with other measures, puts the state in 39th place overall in the foundation’s 2023 State Business Tax Climate Index. The foundation’s most recent report notes that sales tax rates can have a significant impact on where residents make major purchases and where businesses locate, and it cites examples of states that have increased per capita sales by maintaining rates lower than their neighbors. The analysis shows Louisiana’s 9.55% combined sales tax rate is more than 2% higher than Mississippi’s 7.07% rate, and 1.35% higher than Texas at 8.20%. Arkansas’ combined rate of 9.46% is the third highest nationally, behind Louisiana and Tennessee at 9.55%. California has the highest state sales tax rate at 7.25%, followed by four states tied for the second-highest rate, at 7%: Indiana, Mississippi, Rhode Island, and Tennessee. Five states do not have a state sales tax: Alaska, Delaware, Montana, New Hampshire and Oregon. The lowest rates for states with sales tax include Colorado at 2.9%, followed by Alabama, Georgia, Hawaii, New York and Wyoming, all at 4%. States with the highest average local sales tax rates include Alabama at 5.25%, Louisiana, Colorado at 4.88%, New York at 4.52%, and Oklahoma at 4.48%. Behind Louisiana with the highest combined state and local sales tax is Tennessee, Arkansas, Alabama at 9.25% and Oklahoma at 8.98%. States with the lowest average combined rates are Alaska at 1.76%, Hawaii at 4.44%, Wyoming at 5.36%, Wisconsin at 5.43%, and Maine at 5.5%. Originally published at The Center Square.  By Victor Skinner | The Center Square contributor | Jan 26, 2023

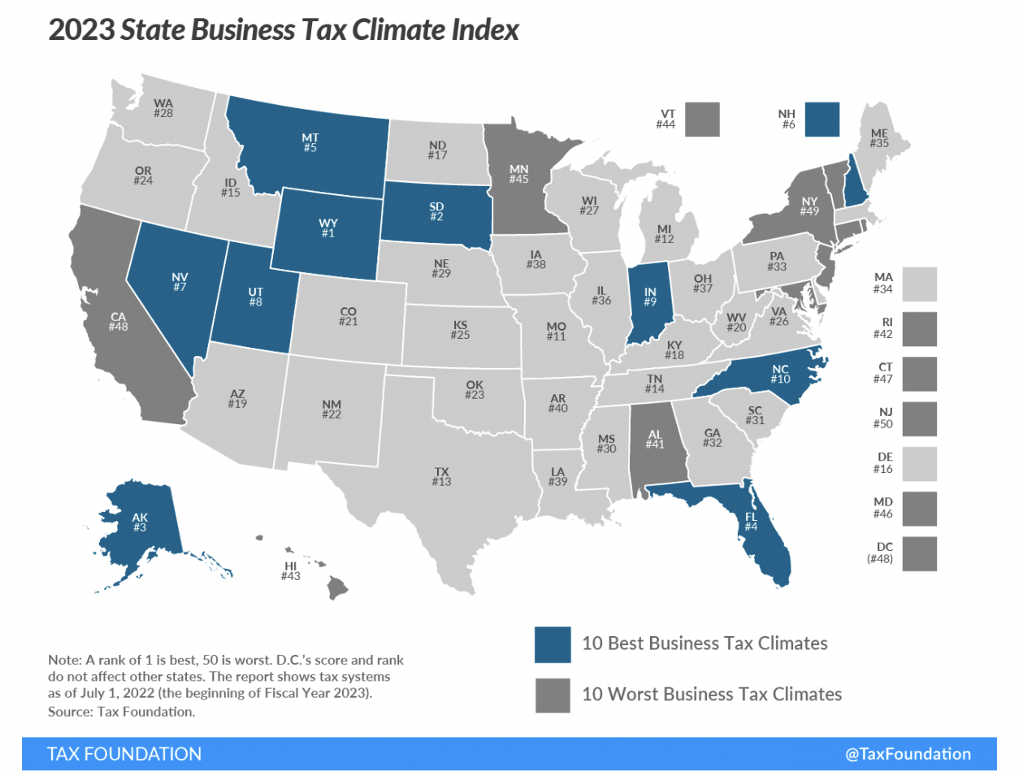

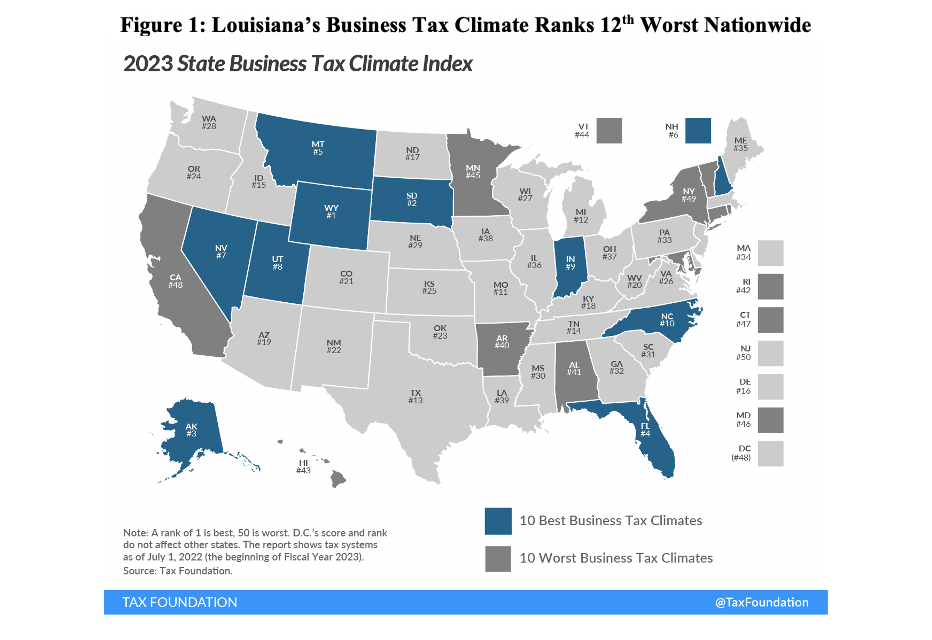

(The Center Square) — New analysis shows Louisiana’s top corporate income tax rate is the 15th highest in the nation, a reality critics contend is holding the state back. Analysis from the Tax Foundation released Tuesday shows that out of the 44 states that levy a corporate income tax, Louisiana’s top 7.5% rate ranks 15th from the top, the highest in the region. Neighboring Texas does not levy a corporate income tax and instead imposes a gross receipts tax on businesses, while Arkansas’ 5.3% rate ranked 33rd, and Mississippi’s 5% rate ranked 34th. "The rate is too high, 7.5% ranking 15th in the nation means Louisiana is less competitive, especially with its neighbors," Vance Ginn, chief economist at the Pelican Institute, told The Center Square. Ginn noted that the corporate income tax ranking follows a previous report from the Tax Foundation that ranked Louisiana as the 12th lowest state for business tax climate, a measure that takes into account other factors. He contends lawmakers can take action to improve the situation. "What we’ve been looking at is finding ways to flatten the corporate income tax," Ginn said, noting that the state’s current system has three brackets. Reducing the three brackets into one would help in the short term, he said, but the long-term focus should be on "eliminating the income tax and finding ways to limit government spending," he said. "What we’ve been looking at is using surplus funds to buy down the corporate tax," Ginn said. Louisiana "really ultimately needs to be more competitive," he said. "People are moving out. Businesses are moving out." Ginn pointed to recent U.S. Census data that shows 67,508 residents left the Pelican State between April 1, 2020 and July 1, 2022, with most of the loss through domestic migration. The Tax Foundation identified 44 states that levy a corporate income tax, which ranged from North Carolina’s 2.5% rate to 11.5% in New Jersey. Behind the Garden State is Minnesota at 9.8%, Illinois at 9.5%, and Alaska and Pennsylvania, which levy top corporate tax rates of 9.4% and 8.99%, respectively. There are 11 states with top rates at or below 5%. North Carolina is followed by Missouri and Oklahoma at 4%, North Dakota at 4.31%, Colorado at 4.55%, Utah at 4.85%, Arizona and Indiana at 4.9%, and Kentucky, Mississippi, and South Carolina at 5%. Nevada, Ohio, Texas, and Washington use a gross receipts tax instead of corporate income taxes, while Delaware, Oregon, and Tennessee impose both gross receipts taxes and corporate income taxes. "Though often thought of as a major tax type, corporate income taxes accounted for an average of just 7.07% of state tax collections and 4.04% of state general revenue in fiscal year 2021," according to the report. "And while these figures are not high, they represent a substantial increase over prior years. Corporate income taxes accounted for 2.26% of general revenue in FY 2020, which is more in line with historical norms." Originally published at The Center Square. In October, the Tax Foundation released the 2023 State Business Tax Climate Index. The report ranks all fifty states based on the collective burdens of each state’s corporate income tax, individual income tax, sales tax, unemployment insurance, and property tax. The results showed that spending restraint funded with a low rate, broad-based taxes provide the best climate for business activity, which supports more jobs, and we all know that work helps provide people with dignity, purpose, and hope, along with the long-term self-sufficiency that is essential for families to flourish. The Tax Foundation’s report notes what many entrepreneurs in Louisiana already know: the state’s business tax climate needs improving. Figure 1 shows that last year the state ranked as the 12th worst among the 50 states, which is an improvement from the 8th worst ranking in the prior year, but still well below where it needs to be to support more in-migration, economic growth, and well-paying jobs. Last year’s ranking was influenced by the corporate tax rank of 32nd, individual income tax rank of 25th, sales tax rank of 48th, property tax rank of 23rd, and unemployment insurance tax rank of 6th in the nation.  Source: Tax Foundation

Compared with nearby states, Louisiana ranked ahead of Arkansas (40th), behind Mississippi (30th), and remained well-below neighboring Texas which improved from the previous report to 13th best in the nation. Given the upcoming 2023 session in Louisiana, the state legislature has an extraordinary opportunity to learn from the Tax Foundation’s report on how to improve. For Louisiana to provide greater opportunity for entrepreneurs and families to prosper, the business tax climate must improve by limiting spending, reforming and cutting taxes, and reducing regulatory burdens. Doing so will help more Louisianans live the American Dream. Originally published at Pelican Institute.  Louisiana has many of the right characteristics for families to flourish. This includes abundant natural resources and thriving petrochemical, oil and gas, and tourism sectors. In fact, New Orleans was recently ranked as the 9th fastest-growing city for 2022 by the American Growth Project. They note that the worker shortages in New Orleans “could indicate the city has even more room to grow in coming years.”

But there’s substantial room for improvement as people and businesses are leaving the state. A big part of that is because of the poor state business tax climate that the Tax Foundation recently ranked as the 12th worst in the country. If it’s too costly to run a business, then employers and workers will go elsewhere. This is especially true when it comes to personal income taxes. Louisiana should join the many states in the flat tax revolution to avoid the negative effects this tax has on people’s livelihoods. This year, four states passed a flat personal income tax, making a soon-to-be total of 14 flat income tax states across the nation. One of them is Louisiana’s neighbor, Mississippi, currently ranked 30th in business tax climate. With a flat income tax, Mississippi's status will improve, but not as much as it could if it also eliminated the personal income tax altogether. Even the improvement of flattening income taxes won't support as much prosperity as eliminating them. The nine states without personal income taxes, including nearby Texas and Florida, show better economic growth, domestic migration, and non-farm payroll employment when compared to flat-tax states. Uncoincidentally, Florida ranked 4th best and Texas 13th in business tax climate. High personal income taxes contribute to Louisiana’s northern neighbor, Arkansas, ranking 40th in business tax climate, and the progressive darlings of California and New York ranking 48th and 49th, respectively. Personal income taxes in the business tax climate index rank 25th in Louisiana, 37th in Arkansas, 49th in California, and 50th in New York. But the marks against Louisiana don't stop there. The latest edition of the Rich States, Poor States report from the American Legislative Exchange Council, which notes the economic performance of the 50 states based on economic output, migration, and job creation from 2010 to 2020, reveals that Louisiana ranks last. The report also compares the upcoming economic outlook for all the states across 15 policy variables, which put Louisiana at 20th, still behind Texas (11th) and Florida (8th), but above Mississippi (27th), although that will likely change in the next report given Mississippi's new flat tax policy. What continues to show up as a contributing factor for Louisiana's lackluster tax policies and economic performance, when compared to its neighboring states, is a hefty burden of personal income taxes. People are fleeing states with high personal income taxes for good reason. Progressive personal income taxes disincentivize work, as people's hard-earned money, that's already being devalued by the current 40-year high inflation, decreases even more. Naturally, people gravitate toward states where they can keep more of what they make. What's a state to do for funding once personal income taxes are eliminated? One poor answer to fund government spending is with higher property taxes. This is a weak spot to the overall tax system in some states without personal income taxes, like Texas, which are a result of excessive local government spending. The better answer that many no personal income tax states primarily depend on for funding is consumption-based taxes. A flat final sales tax with the broadest base and lowest rate possible is best. Although taxing consumption results in less consumption, the benefit is that people save more, which allows for more capital and economic growth. If Louisiana hopes to see more economic growth and thriving people in its state, like the recent growth in New Orleans, flattening personal income taxes should be a top priority until their ultimate elimination. Originally published at The Center Square As if the $1.2 trillion “infrastructure” bill in Congress could not be worse, a closer look shows that among other bad ideas there is $125 million allocated to fund the creation of pilot programs to evaluate a federal vehicle miles traveled (VMT) tax.

The idea behind the VMT tax is to tax drivers for every mile they drive, which could address both traffic congestion and the increasing supposed shortfall in the Highway Trust Fund. This shortfall is caused in part by lower gas tax revenue (lower than some desire, that is) due to more fuel-efficient vehicles and the increased use of electric vehicles (EVs) that don’t pay fuel taxes, as well as by inflated costs of building and maintaining roads and bridges. How would a VMT work? In short, it won’t. But let’s play along with the fantasy. One method would be to require a GPS device in every vehicle which would transmit your vehicle’s data to the federal government. Thankfully, in 2012, the Supreme Court ruled that such a requirement would be unconstitutional. A second method would be annual odometer readings done at vehicle inspections; this would likely just incentivize fraud. The IRS would have to assume the responsibility of auditing the odometers of roughly 289.5 million registered vehicles. Doesn’t that sound fun? Oregon and Utah are two of the first states to launch state-level pilot programs. Oregon’s VMT tax trial participants have three options to sign up for—two privately run systems and one administered by the state’s Department of Transportation. The private companies allocate devices to drivers which log location and distance travelled, then send out tax bills and remit the taxes to the state. State programs operate on a small scale, while the proposed national system would require the feds to track hundreds of millions of vehicles. Remember, the federal government does not have $1.2 trillion available, as some of the bill is being funded with unspent, previously authorized funds, but the new spending could add at least $250 billion to an already bloated national debt. Despite President Biden’s call to ease the financial burden on America’s lower-income earners, these policies will prove to be most detrimental to them. Consider the ongoing 2018 Two-Hundred lawsuit against the California Air Resources Board (CARB) aimed at stopping the implementation of its multi-billion dollar “scoping plan.” The plan’s goals included a “net zero” emissions requirement, a numeric per capita threshold, a mandated VMT tax, and a “vibrant communities appendix.” The costs to fund this plan disproportionately harm low- and moderate-income families and negatively influence the state’s economy. Such policies continue to drive up housing costs, contributing to their homelessness problem. VMT taxes will place an additional financial penalty on low-income families who can’t afford to—or choose not to—live in urban centers. Urban inhabitants are forced to move out of urban areas, then charged even more for doing so by imposing a tax on lengthy commutes. Gas and VMT taxes create an unnecessary burden on taxpayers, as they are funneled through third-party channels, increasing the costs. They also discourage driving, which will inevitably hurt employment and upward mobility. Both taxes increase the price of consumer goods and have a negative impact on economic growth. The U.S. shouldn’t impose a VMT tax to make up for a lower gas taxes collected. Instead, transportation spending should come from general revenue, which it has since 2008. Also, more affordable ways of providing transportation should be considered instead of repeating the same costly mistakes. The federal government needs to quit piling on new taxes and subsidies that hurt those most who can least afford less opportunities available to flourish. Instead, Congress should focus on unleashing the power of the free market to make energy (which affects everything we do) more affordable. It is time to reexamine why such a large transportation-related deficit is automobile-centered and face the fact that it is unsustainable. Adding and raising taxes thrusts our constitutional republic towards an autocratic order, which along with irresponsible spending should be rejected in favor of responsible spending that better helps all Americans, especially low-income earners. Commentary  The Tax Foundation recently published a map of the country illustrating the property taxes paid in each state as a percentage of owner-occupied housing value in 2018. Of all 50 states, Texas had the seventh highest property tax burden in the country, with an effective rate of 1.69% of occupied housing value. This burden is something that Texans across the state know too well.

The article accompanying the map acknowledges that Texas to some extent relies on high property taxes in lieu of other tax categories – i.e., income taxes – though other states without an income tax do not necessarily have a high property tax burden (e.g., Florida). Regardless, in an economy hampered by COVID-19 and government lockdowns and with homeowners under substantial financial and mental stress, local governments have a responsibility to reduce the burden on taxpayers. The Texas Public Policy Foundation has put forward proposals to reduce burdensome property taxes by focusing on Texas embracing final sales taxes over property taxes and governments implementing sound budget practices. A final sales tax system is a more attractive alternative to a property tax. Property taxes are calculated on oftentimes subjective property values, which can rise without a change in homeowners’ ability to pay; Texans can adjust their spending habits to a sales tax, however. This results in a compounding effect of property taxes on holders of property every year that reduces their ability to pay them, forcing many to lose their property and to never truly own it. One way to ease the property tax burden across Texas is to buy down school districts’ maintenance and operations (M&O) property taxes, which is about half of the property tax burden. This could be done by limiting state spending and using any surplus funds to cut the local property tax until it is eliminated, which could take roughly a decade, moving Texas towards sales taxes as they are the state’s top revenue source. However, this could be difficult to maintain session after session with the limitations on state and local government spending to achieve this in a timely manner, if at all. Another way is for the state to immediately replace school M&O property taxes with higher sales taxes. An immediate swap would eliminate the risk that the switch to a final sales tax would be only temporary, a failure common to past property tax relief efforts. However, an immediate switch may be politically challenging to implement, so a way to mitigate this is to limit state spending and use surplus funds to cut the sales tax rate over time. Switching M&O costs to sales taxes is not the only measure local (or state) governments should adopt. The other, and possibly even more fundamental to reducing barriers for opportunities to let people prosper, is implementing sound budgetary practices. By reducing government spending through things like freezing new hires and pay raises and placing a moratorium on incurring any new taxpayer-funded debt, there are plenty of opportunities to cut taxes. Local governments should volunteer for third-party audits to determine where areas of waste can be eliminated along with expensive lobbying contracts and longevity pay. Ultimately, practicing zero-based-budgeting, whereby local governments must justify every expenditure, could help achieve setting budget priorities that support effective government programs. Any government approach to supporting an economic recovery in the wake of COVID-19 must begin with easing the burden on Texas taxpayers, and that approach must include reducing the burden of soaring property taxes and implementing sound budgeting at all levels of government.  Texans appreciate living in a state that values liberty, sensible business policy, and, perhaps most importantly, a strong dislike for taxes, which inevitably infringe on the first two values.

But, in comparison with other states, Texas is beginning to lose its competitive edge in business climate as noted in the Tax Foundation’s recently released 2019 State Business Tax Climate Index. The report ranks all fifty states based on the burdens of each state’s corporate income tax, individual income tax, sales tax, unemployment insurance, and property tax. Figure 1 presents the ranking of each state whereby the top-ranked states include either states without at least one major tax, such as the individual income tax, or states that have all major taxes with low rates and broad bases. Meanwhile, poorly ranked states share similar shortcomings such as complex non-neutral taxes and comparatively high tax rates, such as in the three worst ranked states: California (48th), New York (49th), and New Jersey (50th). In this year’s report, Texas’ overall rank took a hit, sliding from 13th best nationwide in 2018 to 15th best for 2019. Yet, the drop is not due to new policy as the state’s individual category scores remained unchanged and actually improved by 8 ranks for Unemployment Insurance. Rather, the new lower overall rank highlights Texas’ stagnation in decreasing its tax burden as other states jump on the opportunity to increase their prosperity from lower burdens. While Texas excels in the category of individual income tax because as it doesn’t have one, the state is consistently held back by its corporate income tax portion of the index, which remains unchanged at 49th, or second worst! This is because Texas’ business tax is a gross receipts-style tax that is costly to comply with and pay. If Texas eliminated this onerous tax, the Tax Foundation has found the state’s business tax climate overall rank could improve to 3rd best. And the Texas Public Policy Foundation and the Legislative Budget Board (LBB) have estimated large economic gains. Texans have been hurt by burdensome local property taxes for too long, with that ranking in the report being 14th worst in the last three years. We know all too well about complexity, high rates, and lack of voter oversight of Texas’ local property tax system. To overcome this over-burdensome system, the Foundation has recently released a report detailing a strategy to slow the growth of state and local government spending in order to use surplus state funds to permanently reduce the school maintenance and operations (M&O) property tax until its eliminated. This would end nearly half of the property tax burden in Texas within about a decade while increasing funding for school districts over time with state taxes that would eventually fund 100 percent of schools M&O. Moving forward, Texas’ elected officials should consider these rankings by the Tax Foundation and other reports when looking for ways to improve the state’s business tax climate so Texans have the best chance to start a new business or gain employment. The Texas model of limited government has contributed to human flourishing, where 24 percent of new civilian jobs created nationwide have been since December 2007, but there’s always room for improvement. https://www.texaspolicy.com/blog/detail/texas-business-tax-climate-needs-improving Read blog post with figures here.

Texans pay state and local taxes in one form or another. Given Texans desire prosperity and liberty, an optimal tax system creates the least burden on economic activity while funding limited government spending. While the details of taxation can get complicated quickly, core principles of sound taxation include a tax that’s simple, flat, and broad-based. Taxes may redirect you from consuming with a sales tax, push you out of your home with a property tax, or incentivize you to purchase less gasoline with an excise tax to fund government spending. Fortunately, Texas is one of only nine states without a costly state or local personal income tax. The table below shows that the 9 states without this tax perform much better economically than those states with the highest personal income tax rates. State taxes in Texas include the dominant sales and use tax, but there are also the franchise tax, motor fuels tax, and other taxes. The more than 4,100 local taxing jurisdictions statewide collect primarily property taxes, but cities, counties, and special purpose districts can also collect a sales tax. Achieving an optimal tax system begins with the derivation of taxation. First, politicians determine government provisions from voter demand and rent-seeking activity to win votes. Second, those provisions require government spending. Third, government spending requires some form of funding mechanism, hence taxation. Therefore, a key to an optimal tax system is to educate voters on the costs and benefits of government provisions while effectively limiting government spending, which can be done by putting laws in place to add budget transparency and reduce rent-seeking behaviors while strengthening limitson government spending. While the Texas Legislature has appropriately restrained government spending below the key measure of population growth plus inflation in the last two budgets, the state budget is up 7.9 percent above this measure since 2004, meaning taxes are higher and economic growth is lower today than otherwise. So, further spending restraint is necessary to help Texans be more prosperous and Texas more competitive. This could be achieved by limiting state spending to 4 percent and using state surplus dollars to provide tax relief, such as eliminating school M&O property taxes over time, until we can get to an efficient sales tax. According to the Tax Foundation and noted in the figure below, Texas has the 10th highest reliance on sales taxes in the nation, but the 5th least burdensome state-local tax burden. While a sales tax should apply to the broadest base possible, Texas has sales tax loopholes of about $45 billion in FY 2018. These loopholes should be reduced or eliminated to follow sound taxation with the broadest base and lowest rate possible. The Texas Comptroller notes that sales and property taxes in Texas are regressive. A flat tax rate results in higher income people paying a lower share of their income on taxes than lower-income people, but higher income people pay much more in taxes. The costs of property taxes are substantial, with businesses and individuals each paying about half for school M&O property taxes, and they hurt lower-income property owners and even renters as these taxes subjectively skyrocket. Sales taxes, on the other hand, allow people freedom with their money to spend or save, do not have to tax capital, and are transparent. Individuals pay about 60 percent of sales taxes collected while businesses submit the rest, but businesses don't ultimately pay taxes as they pass costs along to people through higher prices, lower wages, and fewer jobs. An example of this is the recent U.S. Supreme Court ruling that allows Texas to expand the sales tax base to all online transactions, which most are already taxed online at places like Amazon and WalMart, but any additional tax revenue should be used for tax relief because Texas state and local governments already spend too much. A sales tax is pro-growth because it allows individuals to choose what’s best for themselves. Other forms of taxes that try to socially engineer behavior, such as a gas tax or carbon tax, end up distorting economic activity and hurting lower-income households most. In conclusion, by effectively limiting government spending that allows a move to an optimal tax system based on a sales tax of final goods and services, Texans will flourish and other states will have an optimal system to follow.  BY VANCE GINN AND DREW WHITE, OPINION CONTRIBUTORS

Original can be found at The Hill The good news keeps coming. Since the passage of the Tax Cuts and Jobs Act, announcements about increased investment in the U.S. and various companies offering employees bonuses haven’t stopped. The vast majority of Americans will prosper from the Tax Cuts and Jobs Act. As an economist and policy analyst, we’ve been skeptical of the Trump administration’s direction on some issues, like NAFTA renegotiations, but we’re encouraged by the results of regulatory and tax reforms because they let people prosper, the flipside of what’s been stifling us. This first major rewrite of the federal tax code in a generation is a historic moment for our republic. The institutional framework that stifled Americans can again work for We the People instead of for bloated governments. We admit that the bill isn’t perfect and encourage Congress to follow this massive $5.5 trillion gross tax cut with spending restraint. That’s especially important because without spending reductions roughly $500 billion could be added to the national debt in the next decade. Also, doing so will help keep the roughly $112 trillion in federal IOUs from requiring government to further infiltrate our lives. We’ve experienced government’s overreach during the worst recovery since WWII of about two percent annual growth while the national debt almost doubled under the Obama administration’s high tax and spend policies. This reshaping of institutions increased barriers to prosperity through excessive regulations, like ObamaCare, and higher taxes that redistributed resources among people. America voted for a new institutional direction in 2016. Regarding regulations, the Trump administration has already repealed 67 of them while creating only three. Entrepreneurs can now budget lower costs longer which contributes to more investments in workers and capital. The result is faster economic growth with a three percent average annualized growth the last three quarters of 2017 matching GDP’s long-term average, which has lifted consumer sentiment. The tax bill’s most sweeping changes include cutting the corporate tax rate and individual income tax rates for most Americans. Sixty percent of the gross tax cuts go to families while the rest goes to businesses. As expected, critics claim these changes benefit the rich. Interestingly, the corporate tax rate cut once had bipartisan support, as President Obama proposed cutting it to 28 percent, and progressives passed and extended much of President Bush’s personal income tax cuts. Regardless, permanently cutting the corporate tax rate from 35 percent, the highest in the developed world, to 21 percent, slightly below the worldwide average, drastically improves employment prospects. Often missed in the discussion is that corporations simply submit taxes to the government because people pay them through higher prices, lower wages, and fewer jobs available. Cutting the corporate tax rate means corporations can pass those savings along to people. Businesses are reporting they will pay bonuses and higher wages, immediate pay increases to let people freely prosper. On the individual income tax side, most taxpayers will pay less tax until at least 2026. According to good tax policy, the tax bill doesn’t flatten as it leaves seven income tax brackets, but it broadens the base by eliminating many exemptions and deductions and simplifies the code by doubling the standard deduction. Critics claim that these changes could increase income inequality. But history shows that the tax code is not the place to deal with supposed income inequality as it fluctuates whether taxes are high or low. By changing the institutional incentives through this tax bill, more people can move up the income ladder. But, do only the rich get a tax cut? No. The Tax Foundation calculated the changes in tax liability for multiple households and found that each of them would pay less tax. An individual earning $30,000 with no kids could pay $379 less in taxes. An individual earning $50,000 with two kids could pay $1,892 less in taxes. A married couple filing jointly earning $165,000 with two kids could pay $2,224 less in taxes. And a married couple filing jointly earning $2 million could pay $18,904 less in taxes. All income groups receive a tax cut. Higher income people pay fewer dollars than those with lower income, but that’s because they pay more in income taxes. For example, the top 10 percent of income earners pay 70 percent of federal income taxes collected. However, the share of income taxes paid could become more progressive under these tax changes. It’s not just more money in people’s pocket, but doubling the standard deduction lets many people spend less time on their taxes and more time with their families. This is great news for working Americans. Icing on the cake would be for Congress to restrain government spending, the ultimate burden of government. Bipartisan welfare reform in the 1990s helped cut spending but more importantly improved the lives of many Americans as they returned to work or received better assistance. The amount of waste, fraud, and abuse in these programs along with too many dollars to bureaucracy and not to people make welfare a good place to start. Reforms to the major drivers of Medicaid, Medicare, and Social Security must be on the table to restrain spending growth while improving them for the truly needy. Until then, let’s celebrate the Trump administration’s new institutional direction that has long supported prosperity. Skepticism is healthy to provide proper checks and balances on government. But when pro-growth policies like regulatory and tax reforms improve human flourishing, we’re much more optimistic about the future. Vance Ginn, Ph.D., is director of the Center for Economic Prosperity and senior economist and Drew White is senior federal policy analyst, both at the nonprofit Texas Public Policy Foundation. Here are my thoughts on the border adjustment and federal tax reform in general as they could influence the U.S. economy, especially Texas.

I disagree with some of the analysis and findings by Kotlikoff (see full article below), whom is a highly respected economist regarding life cycle economic modeling and analysis, but he tends to be Keynesian in his approach, as you can see throughout his piece. Much of what he states about the border adjustment, also known as the border adjustment tax (BAT) though it is not technically a tax, is reflected in the Tax Foundation’s (TF) talking points. TF claims that the border adjustment will be more efficient than our current corporate income tax system by leveling the playing field for goods that are consumed in the U.S. Moreover, TF argues that it is not a tax but rather a “border adjustment” of the current corporate income tax such that corporations report consumption of their imported goods as income since it is consumed here instead of exports that are consumed elsewhere. TF and Kotlikoff also put a lot of emphasis on the far-reaching assumption that the dollar value will adjust accordingly to not make the border adjustment cause increases in consumer and producer prices. While theoretically TF is correct on several points, the BAT argument fails on at least the following levels:

Tax revenue neutrality is a failed argument that has been tried multiple times (e.g., Kennedy-Johnson tax cuts, Reagan tax cuts, Bush tax cuts); tax reform should focus on budget neutrality such that the economic drain of a rising $20 trillion in federal debt is plugged as soon as possible. The vision, like in Texas, should be to not tax businesses that simply submit taxes to the government while people pay the actual cost through the form of higher prices, lower wages, and fewer jobs available. In economic terms, the tax incidence is ultimately on people. Ending the corporate income tax would eliminate whether we are taxing income based on imports or exports, removing the concern over the border adjustment. Considering we are unlikely to eliminate federal taxes on businesses today, reducing the corporate tax rate to as low as possible while not changing the tax base, thereby distorting the marketplace more than it should, balancing the budget should be based on economic growth and slowing and cutting government spending so budget neutrality is achieved. There’s no need to add a “new tax,” though it’s not technically a new tax, in the form of the border adjustment. The Texas Public Policy Foundation (TPPF) recently commissioned a study with the R Street Institute that highlights the cost increase of $3.4 billion in Texas' property-casualty insurance premiums over the next decade from the border adjustment, which is just a small portion of the potential costs to Texas and other states. TPPF's research also shows that taxes on income and higher taxes in general are detrimental to economic activity among states; therefore, shrinking the size and scope of government by cutting government spending is the best path toward prosperity, not providing revenue neutrality with a new border adjustment. Fortunately, President Trump’s announced tax plan does not include the BAT. While I have concerns about the contribution of Trump’s tax plan to the already estimated increases in the national debt from current policy, economic growth will reduce some of the static analysis revenue losses. Considering that neither President Trump's nor the GOP tax plan will pay for itself, as some economists suggest, the focus must be on budget neutrality as Congress cuts and restrains government spending. At this point, I prefer the Trump tax plan and think it would best reduce tax burdens to allow more incentives by entrepreneurs to produce—the driver of economic activity. However, this is an opportunity to highlight that there shouldn’t be taxes on businesses, like TPPF argues to eliminate Texas' business franchise tax, and that the federal government should continue to simplify the tax code to provide more efficiency in the code by moving to a flat tax, which I prefer a flat consumption tax, and subsequent increased economic activity. This is also an opportunity for the U.S. to increase its economic competitiveness through tax reform to counter the unfortunate protectionist arguments in D.C. that could lead to potentially worse negotiated trade deals and fewer beneficial trade agreements, which is very disconcerting. Below are two recent WSJ articles that provides different views on this issue. I hope the debate will continue so that the appropriate institutional framework for fiscal policy will prevail. In general, this framework should be based on the core principles of taxation, which includes simplicity, efficiency, and competitiveness. By following these principles and focusing on budget neutrality without shifting to a new tax base, the U.S. can be more prosperous and Texans will benefit in the process. __________________________________ On Tax Reform, Ryan Knows Better The House proposal beats Trump’s plan, which is more regressive and would induce huge tax avoidance. By Laurence Kotlikoff May 11, 2017 6:58 p.m. ET 172 COMMENTS As Republicans push toward a major rewrite of the U.S. tax code, they must evaluate two competing proposals: the House GOP’s “Better Way” plan and President Trump’s framework, introduced last month. Either would greatly simplify personal and business taxation, but pro-growth reformers should hope that the final package looks more like the House’s proposal. Let’s begin the analysis with personal taxes. Both plans eliminate the alternative minimum tax, deductions for state and local taxes, and the estate tax. The House plan eliminates exemptions, while Mr. Trump’s outline is unclear. Both raise the standard deduction, reduce the number of income-tax brackets, lower the top marginal tax rate, and provide a big break to those with pass-through business income. On this last point the Trump plan is particularly generous. It taxes pass-through income at 15%—far below its proposed top rate of 35% for regular income. The large gap between these rates would induce massive tax avoidance by the rich. The Better Way’s proposed rates are much closer: 25% and 33%, respectively. Another criterion to judge tax reform is its effect on the budget. Absent any economic response, the Better Way proposal would lower federal tax revenue by $212 billion a year, according to a recent study I conducted with Alan Auerbach, an economist at Berkeley. But some economic response is likely. The House plan would cut the U.S. corporate tax rate from one of the highest among developed countries to one of the lowest. Computer simulations—which will be included in a forthcoming journal article I am writing with Seth Benzell and Guillermo Lagarda —suggest that increased dynamism could raise U.S. wages and output by up to 8%. Under this optimistic scenario, federal tax revenue would rise by $38 billion a year. We are in the process of simulating the Trump plan, and it is too early to say whether it produces less revenue. The plan’s potential for tax avoidance, however, is a major red flag. Which plan is more regressive? Both personal tax reforms appear to help the rich. But the Better Way’s business tax reform actually appears highly progressive. Despite the popular perception that the corporate income tax is paid by the rich, my research suggests it represents a hidden levy on workers. This causes American companies and capital to flee the country, reducing demand for U.S. workers, whose wages consequently shrink. The Better Way plan transforms the corporate income tax into something different: a business cash-flow tax with a border adjustment. Notwithstanding innumerable mischaracterizations by the press, politicians and business leaders, the cash-flow tax implements a standard value-added tax, plus a subsidy to wages. Every developed country has a VAT, which is an indirect way to tax consumption. All of these levies have border adjustments, which ensure that domestic consumption by domestic residents is taxed whether the goods in question are produced at home or imported. Unlike the Better Way, Mr. Trump’s plan does not include a border adjustment, which means it effectively taxes exports and subsidizes imports. This undermines his goal of reducing the U.S. trade deficit. Where is the progressive element to the cash-flow tax? It’s in the subsidy to wages, which insulates workers from the brunt of the VAT. They will pay VAT consumption taxes when they spend their paychecks, but they also will have higher wages thanks to the subsidy. The folks who truly pay the cash-flow tax are the rich, because they pay the VAT when they spend wealth that was earned years or decades ago. As my study with Mr. Auerbach shows, this quiet but large wealth tax makes the overall House plan almost as “fair” as the current system. Our analysis—in contrast with studies done by congressional agencies and D.C. think tanks—assesses progressivity based on what people of given ages and economic means get to spend over the rest of their lives. Consider the present value of remaining lifetime spending for 40-year-olds. The richest quintile of this cohort accounts for 51% of the group’s spending, and the poorest quintile for 6.3%. Under the House tax plan, those figures move only modestly, to 51.6% and 6.2%. And the Trump plan? Hard to say, given how easily the rich could transform otherwise high-tax wage income into low-taxed pass-through business income. The Trump tax plan strikes out on all counts. Whoever knew tax reform could be this complicated? We specialists in public finance did. The bottom line is that the U.S. needs more revenue and less spending to close the long-term fiscal gap. The nation’s true debt—the present value of all projected spending, including the cost of servicing the $20 trillion in official debt, minus the present value of all current taxes—has been estimated by Alan Auerbach and Brookings’s William Gale to be as high as $206 trillion. The Better Way plan moves in the right direction, but if the economy doesn’t respond as hoped, there’s a risk of larger deficits. One way to prevent that would be to eliminate the ceiling on earnings subject to the Social Security payroll tax. That could add $300 billion to the Treasury each year, according to our calculations. But even without that adjustment, the House plan seems far superior to both the current system and the Trump plan. The press, politicians, and business leaders should get things straight, including this key point: The Better Way tax plan is indeed a better way. Mr. Kotlikoff, an economist at Boston University, is director of the Fiscal Analysis Center. ______________________________ Economists Say President Donald Trump’s Agenda Would Boost Growth — a Little The WSJ’s monthly survey of economists gauges the impact of a fully implemented Trump plan By Josh Zumbrun Updated May 11, 2017 10:34 a.m. ET 17 COMMENTS One of the most-watched economic forecasts in Washington will come later this month when the White House releases its budget. Here is what it would look like if done by economists surveyed by The Wall Street Journal. Over the course of the next decade, the estimated cost of many items on President Donald Trump’s wish list will depend critically on his own team’s projections for economic growth, unemployment and interest rates. Per the longstanding custom, however, the White House budget differs from most economic forecasts in one crucial way. Most forecasters estimate the path for the economy they believe is most likely, taking into account that many political promises will never come to fruition. But White House forecasts are an estimate of what the economy would be like if the president’s full agenda were implemented. To establish a baseline of what a reasonable forecast might look like under Mr. Trump, respondents to The Wall Street Journal’s monthly survey of forecasters provided their own estimates of the economy if all of Mr. Trump’s initiatives were enacted. If the president’s agenda were enacted, forecasters on average think long-run gross domestic product growth could rise to 2.3%, an 0.3 percentage point increase from their 2% baseline. Unemployment would average 4.4% under this scenario, instead of 4.5%. Interest rates set by the Federal Reserve would be about a quarter-point higher. Short-term rates would be about 3.1%. So an improvement, but a modest one. Early on, White House officials have reportedly considered penciling in growth rates as high as 3.2% a year. But the respondents to the Journal’s survey—a mix of academic, financial and business economists who regularly produce professional forecasts—say numbers so high will be hard to attain, because the policies under consideration just might not pack that punch. Key Trump initiatives, which face a challenging road through Congress, include overhauling the health-care system, simplifying the corporate tax code, cutting income taxes, rewriting regulation and investing in the nation’s infrastructure. “If you were to assume that such initiatives get passed later this year, there should be positive economic benefits, especially for 2018,” said Chad Moutray, chief economist of the National Association of Manufacturers. Over the course of a decade, 3.2% growth would leave the economy nearly $2 trillion larger than 2.3% growth. So the lower estimates of economists are significant. “Fewer regulations may raise long-term growth 0.1% to 0.2% by stimulating productivity growth,” said Nariman Behravesh of IHS Markit Economics. “It should have hardly any effect on the long-term unemployment rate and inflation rates.” It is “hard to quantify, but measures would not boost long-term productivity,” said Ian Shepherdson of Pantheon Macroeconomics. “But they probably would push up both short and long-term interest rates.” The White House always has some incentive to put forth overly optimistic numbers. For one thing, the White House staff generally believe in the wisdom and benefits of the president’s agenda. And if growth rates are boosted and unemployment comes down, it does wonders for budget projections. Tax revenue climbs and spending on programs such as unemployment or Medicaid may dwindle. In recent months, economists’ forecasts for the coming year haven’t changed much. They expect growth for this year of 2.2%, down from 2.4% in the March survey. They place the odds of recession in the next year at just 15%, compared with 20% at this time a year ago. For now, many are waiting to see more detail in Mr. Trump’s agenda and retain doubts about how much he will be able to accomplish. “Infrastructure spending is great, but it has to be paid for and that creates drag at some point,” said Amy Crews Cutts, the chief economist of Equifax. “The proposed tax breaks won’t stimulate the economy nearly enough to pay for themselves let alone fund other new initiatives, which leads to deep cuts in the long run." The survey of 59 economists was conducted from May 5 to May 9. Not every economist answered every question. The Tax Foundation recently released their 2017 State Business Tax Climate Index report detailing the rankings of all fifty states. The overall score is determined by the burdens of each state’s corporate income tax, individual income tax, sales tax, unemployment insurance, and property tax. The purpose of the report is to “show how well states structure their tax systems, and provides a roadmap for improvement.”

Chart 1 shows the ranking of each state. A common factor between a majority of the top performing states is the absence of at least one major tax, such as the individual income tax, and for states that do levy all the major taxes, they do so with low rates and broad bases. States ranked in the bottom bracket share similar shortcomings such as complex non-neutral taxes and comparatively high tax rates. Texas’ overall ranking declined one position to 14th nationwide. While Texas excels in the unemployment insurance and individual income tax categories, the overall ranking decline can be attributed to poor scores for corporate income and property taxes. Although the 2015 Texas Legislature cut the business franchise (margin) rates by 25 percent for a total value of $2.6 billion, the relative ranking of the corporate income tax remained unchanged at 49th, or second worst! This is due to the fact that the business tax is a gross receipts-style tax that is costly to comply with and pay. The Tax Foundation published a previous paper that finds the state’s overall business tax climate would increase to 3rd if the margin tax was eliminated. Moreover, the Texas Public Policy Foundation and the Legislative Budget Board (LBB) have estimated large economic gains from eliminating this onerous tax. The Tax Foundation also notes that Texas’ local property taxes is a thorn in taxpayers’ side as the relative ranking of property taxes declined from 33rd to 37th, or 14th worst! Its structural complexity, unwarrantedly high rates, and lack of voter oversight continue to confuse and burden taxpayers. The 84th Legislature took steps to lower this burden by increasing the homestead exemption for school districts by $10,000 to $25,000. However, as the LBB recently noted, although homeowners paid a lower property tax amount than without the exemption increase, most homeowners paid more for their property taxes this year. To overcome the overwhelming burden of local property taxes statewide, the Texas Public Policy Foundation published a paper highlighting key reforms that should be made in the short run and long run. Specifically, structural reforms should be made in the short run by giving voters a stronger voice in the growth of property taxes by requiring an automatic election for any local government whose revenues increase above a certain limit in any one year. In the longer run, we imagine Texas with substantially more economic growth and job creation from replacing the inefficient property tax system with a higher, broader-based efficient sales tax. The 85th Legislature should take these rankings by the Tax Foundation and other reports into consideration to improve the state’s business tax climate. The goal is not necessarily to beat other states, but to give Texans the best chance to prosper, which can happen if we improve our rankings to encourage more new businesses and job creation.  By Dr. Vance Ginn & Kiara Pillay

April 15th is the day few of us look forward to: Federal Individual Income Tax Day. Fortunately, there is a day we can reluctantly look forward to: Tax Freedom Day. Tax Freedom Day is the day when the nation has worked long enough to pay for federal, state, and local taxes for the year, according to the Tax Foundation. This year, Americans will spend 31 percent of the nation’s income on all taxes, including $3.3 trillion in federal taxes and $1.6 trillion in state and local taxes. This means that Americans will not pay almost $5 trillion until the Tax Freedom Day of April 24th. To put it bluntly, we work for governments for the first 114 days of the year—one day earlier than last year, due to lower federal tax collections. Texas’ more friendly tax code keeps Texans working only until April 17th to pay all taxes. Although Texans lost four work days compared with last year when the Tax Freedom Day was April 13th, Chart 1 shows that Texas ranks 20th for having the shortest period of work days to pay federal, state, and local taxes. Mississippi has the earliest Tax Freedom Day of April 5th and Connecticut has the latest day of May 21st. Chart 1: The Average American Works 114 Days to Pay for All Taxes—Tax Freedom Day is April Source: Tax Foundation The report notes the following: “The latest ever Tax Freedom Day was May 1, 2000, meaning Americans paid 33.0 percent of their total income in taxes. A century earlier, in 1900, Americans paid only 5.9 percent of their income in taxes, meaning Tax Freedom Day came on January 22.” The more time we work for the taxman (as noted by the Beatles), the less time we have to do productive activities. The 85th Texas Legislature should pass fiscal reforms that reduce the bottom line of the budget, such as the STaR Fund, so that less revenue is needed to fund government expenditures. If this is done effectively, then the Legislature can improve the tax system by eliminating the business margin tax and providing meaningful property tax relief. These reforms and more are supported by the Conservative Texas Budget Coalition comprised of 13 member organizations. In addition, the U.S. Congress must reform the complex, bloated federal tax code to free us from paying too much taxes. By collectively limiting the size and scope of federal, state, and local governments, Texans and all Americans will have a reason to celebrate an earlier Tax Freedom Day!

Don't miss this video of a panel I moderated recently on advancing the Texas model with a simple tax system.

The Texas model of low taxes, no individual income tax, moderate regulation, and a good lawsuit climate has generated prosperity for many Texans. Despite these gains, is the state’s tax system with an onerous business franchise tax and burdensome local property taxes the most efficient? Join us as the panel discusses potential improvements to the state’s tax structure so that the budget meets the needs of Texans while providing an environment conducive to the greatest economic opportunity for them to succeed. Featuring Sen. Paul Bettencourt, Chairman, Select Committee on Property Tax Reform and Relief, Texas State Senate | Presentation Scott Drenkard, Economist and Director of State Projects, Tax Foundation |Presentation Sen. Craig Estes, Texas State Senate Rep. Chris Turner, Texas House of Representatives Moderated by Dr. Vance Ginn, Economist, Center for Fiscal Policy, Texas Public Policy Foundation http://www.texaspolicy.com/multimedia/video/advancing-the-texas-model-will-a-simple-tax-system-drive-prosperity-po2016  By Dr. Vance Ginn and Nozim Ishankulov

The Tax Foundation recently released the 2016 State Business Tax Climate Index report that estimates relative state tax burdens nationwide. The authors define the Index as the following: “The Index deals with such questions by comparing the states on over 100 different variables in the five major areas of taxation (corporate taxes, individual income taxes, sales taxes, unemployment insurance taxes, and property taxes) and then adding the results up to yield a final, overall ranking. This approach rewards states on particularly strong aspects of their tax systems (or penalizes them on particularly weak aspects), while also measuring the general competitiveness of their overall tax systems. The result is a score that can be compared to other states’ scores.” According to the report, Texas tax system ranks as the 10th best for doing business. Despite substantial burdens of property (34th), sales (37th), and corporate (41st) taxes, the absence of an individual income tax (6th) and a low unemployment insurance tax (15th) contribute to the Lone Star State’s favorable ranking, as shown in Chart 1. Chart 1: Texas has the 10th best business tax climate Source: Tax Foundation Although there are no corporate income taxes in Texas, the authors account for the existence of a “complicated gross receipts tax, styled the Margin Tax” that reduces businesses ability to reach their full potential. This onerous tax is a complicated tax to file contributing to a high cost of compliance along with the amount paid, making it a complete failure of good public policy. The Tax Foundation estimates in another report that if the margin tax was eliminated Texas’ business climate would rank 3rd best making it more competitive and advancing more job growth and economic prosperity. This is supported by a Texas Public Policy Foundation report that finds Texas forgoes billions of dollars in new real personal income and hundreds of thousands of new private sector jobs during the next five years if it’s not eliminated. Texas has been the bastion of free enterprise and economic opportunity for almost two decades. To advance the Texas model and improve its competitive advantage by having the best possible business tax climate, the Tax Foundation’s report provides evidence that the margin tax has to go. If it did so, Texas would join only Wyoming and South Dakota, which are the top two ranked states, as the only states without personal income and business taxes, improving the outlook for all Texans. http://www.texaspolicy.com/blog/detail/texas-business-tax-climate-ranks-10thbest |

Vance Ginn, Ph.D.

|

RSS Feed

RSS Feed

{kind=link}

Proudly powered by Weebly