Originally published at Law & Liberty.

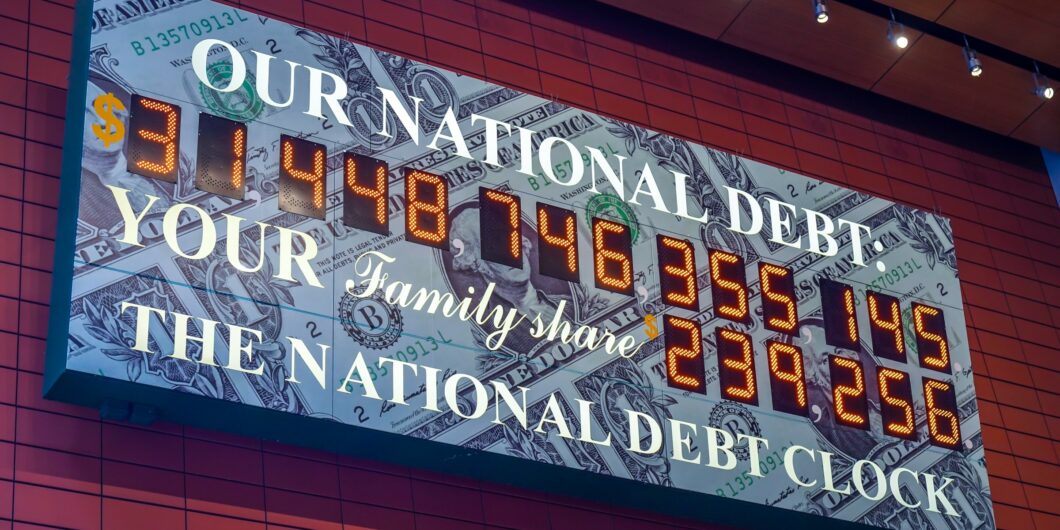

The Congressional Budget Office (CBO) just released the February 2024 Budget and Economic Outlook, and projections look grim. This year, net interest cost—the federal government’s interest payments on debt held by the public minus interest income—stands at a staggering $659 billion in 2023 and has recently soared to about $1 trillion. Unless politicians face these facts and restrain spending, Americans can expect rising inflation and painful tax hikes without improvement in public services. Some politicians quickly blamed a lack of tax revenue, calling for repealing the 2017 Trump tax cuts. But how much more money can they take? New IRS data shows that 98% of all income taxes are paid by the top 50% of income earners, those making at least $46,637. Moreover, 35% of Americans feel worse off than 12 months ago and inflation remains the primary concern for those across the income spectrum. So perhaps, rather than taking more money, the government should own up to its mistakes. The massive net interest costs result from bad spending habits, not a lack of revenue. This requires the federal government to adopt strict fiscal and monetary rules to rein in wasteful deficit spending and money printing that fuel higher interest rates and inflation. Net interest cost is the second largest taxpayer expenditure after Social Security and is higher than spending on Medicaid, federal programs for children, income security programs, or veterans’ programs. And it’s expected to grow. The CBO projects net interest to surpass Medicare spending this year and balloon to $1.6 trillion in 2034 as a result of higher debt and higher interest rates. Interest rates on Treasury debt are at the highest since 2007, paying between 4% and 5.5%, and the rates are expected to rise further. As the stockpile of gross federal debt is expected to grow by about $20 trillion to $54 trillion over the next decade, politicians will face an increasing temptation to rely on the Federal Reserve to pay for it by printing money. If the Fed does, the dollar’s value will decline, and Americans will continue to struggle financially. In an ideal world, politicians will organize the budget process to focus on funding a limited government and ensuring Americans keep their hard-earned money. They would also have plans to cut spending during times of economic downturn to reduce tax burdens on families and businesses and avoid the Keynesian fallacies of deficit spending to fill gaps in economic growth. However, America isn’t Shangri-La. As Thomas Sowell poignantly notes, a politician’s first goal is to get elected, the second goal is to get reelected, and the third goal is far behind the first two. So long as there are investors happy to purchase Treasury debt, there will be politicians who are happy to sway voters with generous spending programs financed by public debt. This must end. Instead, Washington should require strong institutional constraints with a spending limit. The limit should cover the entire budget and hold any budget growth to a maximum rate of population growth plus inflation. This growth limit represents the average taxpayer’s ability to pay for spending. Following this limit from 2004 to 2023 would have resulted in a $700 billion debt increase instead of the actual increase of $20 trillion. Such a policy has been in effect in Colorado since 1992. It is the Taxpayer’s Bill of Rights (TABOR) amendment to the Colorado Constitution. TABOR has revenue and expenditure limitations that apply to state and local governments. The revenue limitation applies to all tax revenue, prevents new taxes and fees, and must be overridden by popular vote. Expenditures are limited to revenue from the previous year plus the rate of population growth plus inflation. Any revenue above this limitation must be refunded with interest to Colorado citizens. A spending cap like TABOR is necessary but not sufficient to solve the problem because politicians in Washington can still pressure the Federal Reserve to pay for the increased debt by printing money. Therefore, it must be combined with a monetary rule to force fiscal sustainability while requiring sound money with fewer distortions in the economy. Monetary rules can come in many forms. While no rule is perfect, research shows that a rule-based monetary policy can result in greater stability and predictability in money growth than the current policy of “Constrained Discretion” whereby the Fed follows rules during “normal times” and has discretion during “extraordinary times.” Whether we are in ordinary or extraordinary times is up to policymakers, who typically don’t want to “let a good crisis go to waste,” as they say. Milton Friedman advocated for a money growth rate rule, the “k-percent rule.” This rule states that the central bank should print money at a constant rate (k-percent) every year. A variation of this rule was used by Fed Chair Paul Volcker in the late 1970s and early 1980s to tackle the Great Inflation with much success. Unfortunately, the Fed had already done too much damage with excessive money growth before then, so the cuts to the Fed’s balance sheet contributed to soaring interest rates that forced destructive corrections in the economy, resulting in a double-dip recession in the early 1980s. This led to the Fed abandoning money growth targeting in October 1982. It is important to note, though, that this “monetarist experiment” was not bound to any law, constitutional or statutory. During that time, the Fed still operated under discretion, which is why it was able to abandon the monetary growth rule just a few years after it had begun, unfortunately. There are other rules that could be applied. John Taylor proposed what’s been coined the Taylor Rule, which estimates what the federal funds rate target, which is the lending rate between banks, should be based on the natural rate of interest, economic output from its potential, and inflation from target inflation. Scott Sumner most recently popularized nominal GDP targeting, which uses the equation of exchange to allow the money supply times the velocity of money to equal nominal GDP. It has different variations, but the key is that velocity changes over time, so the money supply should change based on money demand to achieve a nominal GDP level or growth rate over time. By focusing on a rules-based approach to spending and monetary policy, Americans do not have to worry about electing the perfect candidate every election. Proper constraints will nudge even the worst politicians to make fiscally responsible choices and reduce net interest costs. Furthermore, America will be better positioned to respond to crises at home and abroad. If Congress wants to see who is to blame for the grim CBO projections, they should look in the mirror. Stop looking to take hard-earned money away from Americans and focus on sound budget and monetary reforms now.

1 Comment

Originally published at AIER.

Congress hasn’t done its primary job of passing a balanced budget or even a full-year budget in decades. This must change soon before the fiscal crisis gets worse. But that’s unlikely because few seem to care. Congress recently passed the third continuing resolution for fiscal year 2024 in the amount of $1.7 trillion. This budget legerdemain kicks the federal budget to March, when members will repeat the same omnibus process, one fraught with hijinks and grandstanding. Instead of an actual debate about what we should or should not spend on a department and agency basis, we get calls to “shut down the government” if any number of demands aren’t met. Now, there’s a “bipartisan tax deal” that could add more than $600 billion to the debt over a decade. Democrats don’t seem to care about the debt much, and some who adhere to the ideology of modern monetary theory even think it is helpful for economic growth. But the Republicans also seem to have little, if any, courage to restrain spending, so they just keep cutting taxes and spending us into greater levels of debt. The late, great economist Milton Friedman said, “I am in favor of reducing taxes under any circumstances, for any excuse, with any reason whatsoever because that’s the only way you’re ever going to get effective control over government spending.” But spending is the ultimate burden of government on taxpayers and must be addressed first. The Republican agenda has prioritized border security, rightly or wrongly, over everything else to deal with a humanitarian crisis along the border with Mexico. Former president and top GOP presidential contender Donald Trump has insisted on prioritizing this issue. Events at the border continue to boil with the fight between Texas Governor Greg Abbott and President Biden after a recent Supreme Court decision. The decision has limited reach as it “temporarily allows the Border Patrol agents to continue cutting and moving the razor wire installed by Texas. However, since the ruling came through the emergency docket, the case is now passed back down to the lower court, who will hear the case with oral arguments.” The Republican pursuit of an aggressive border security deal as the number one priority risks further inflating bloated spending as the issue gets subordinated. While some argue that illegal immigration costs far more than border security, compelling studies indicate that immigrants, when provided opportunities, make substantial contributions to society, enriching the economy. The more aggressive approach to border security during Trump’s term contributed to extravagant federal deficit spending. There has also been a high cost to Texans in the state’s budget to address border security issues of more than $5 billion in the current budget and at least $5 billion more since 2016. Addressing illegal immigration issues and averting an impending fiscal crisis requires substantial debate about these issues rather than the current partisan-fueled fire drill over continuing resolution funding. With budget deficits expected to be at least $2 trillion per year over the next decade and net interest payments recently surpassing $1 trillion, every scarce taxpayer dollar must be used wisely, if at all. This could be done with market-based reforms that would foster better fiscal, economic, and border situations. Economist Richard Vedder and others proposed an immigration approach that would create an international market for visas whereby the government issues some of them for refugees, and the rest are auctioned off to people willing and able to purchase them. The government could use this money to pay down deficits, and there would be better accountability for those with visas while providing necessary resources along the border. The biggest national threat continues to be Congress’ profligate spending, which the primary drivers are so-called “entitlements” and must be swiftly reformed with market-based approaches. But right behind it is the Federal Reserve’s bloated balance sheet, which must be addressed. Despite a 14 percent reduction since its peak of about $9 trillion in May 2022, the Fed’s balance sheet remains a staggering 85 percent higher than pre-pandemic levels. Lingering issues of the Fed running losses of $116.4 billion last year, propping up struggling financial institutions with its costly bank term funding program, and the ongoing cost of trying to artificially hold down market interest rates as federal budget deficits soar exacerbate a fiscal-monetary crisis. Manifestations of the underlying economic malaise are evident in falling real wages down 1.3 percent since Biden took office, inflation surpassing set targets, unattainable housing affordability, and families grappling with saving money. These symptoms, rather than isolated issues, indicate the pervasive consequences of unchecked government spending and money printing, casting a long shadow on Americans’ well-being. The latest efforts by Congress to pass the continuing resolution and propose the latest tax deal will make the fiscal situation worse. While the latest idea of a fiscal commission could do what is good in theory, there are already calls to raise taxes, which will be detrimental to the economy and the fiscal picture. The path forward must be fiscal sustainability. This includes a long-term solution of a spending limit. The limit should cover the entire budget and hold any growth to a maximum rate of population growth plus inflation. This growth limit represents the average taxpayer’s ability to pay for spending. Doing so would have resulted in just a $700 billion increase in the debt instead of the actual increase of $20 trillion from 2004 to 2023. The spending limit should be combined with a monetary rule that removes much of the discretion of central bankers. This will support sound money. It can be achieved by moving to a single price stability mandate and preferably a high-powered money growth rate rule of the Fed’s assets. Other rules include the Taylor rule or nominal GDP targeting. While each of these rules has pros and cons, the money growth rate rule advocated for by Milton Friedman is the simplest. It’s simply a rule based on how fast currency plus bank reserves grow. This would be the easiest for the public to understand, to hold officials accountable, and to tie the Fed’s balance sheet directly to inflation. John Taylor proposed what’s been coined the Taylor rule that estimates what the federal funds rate, which is the lending rate between banks, should be based on the natural rate of interest, economic output from its potential, and inflation from target inflation. Scott Sumner most recently popularized nominal GDP targeting, which uses the equation of exchange (MV=Py) to allow the money supply times the velocity of money to equal nominal GDP. There are different variations of it, but the key is that velocity changes over time, so the money supply should change based on money demand to achieve a nominal GDP level or growth rate over time. Rules over discretion, at least until we can rightfully end the Fed, should hold those in Congress and at the Fed in check because their limited knowledge will always result in bad outcomes for people in the marketplace. Such measures are pivotal in preventing further debt accumulation, safeguarding America’s credibility, and preserving the economy’s stability. The choices made today will reverberate into the future, shaping the economic landscape for future generations. This call to action is for policymakers to tread carefully, adopt prudent fiscal and monetary sustainability through a rules-based approach, and prioritize the long-term well-being of the country with market-based reforms over short-term politics. Failure on these issues will prevent us from addressing the humanitarian crisis along the border, China, or other concerns. These efforts will be challenging, but they’re essential for freedom and prosperity.  The economic shock from the shutdowns in response to the COVID-19 pandemic were unprecedented. Never had state governors imposed stay-at-home orders that cut people off from their lives and livelihoods. Those costly policies were bad enough, but then came historic increases in deficit spending and money creation.

While these may have been well-intentioned policies early on, their repercussions—amplified by misguided macroeconomic policy since January 2021—continue to plague many Americans. The antidote is pro-growth policies. There was a vibrant economy on the eve of this shock. In fact, about three quarters of the flows of people into employment were Americans returning to the workforce—the highest on record. For context, 2.3 million prime-age Americans—people between the ages of 25 and 54—returned to the labor force during Trump, after 1.6 million left during the Obama recovery. This happened with a robust private sector providing many opportunities because the Trump administration focused on removing barriers by getting the Tax Cuts and Jobs Act of 2017 through Congress and providing substantial, sensible deregulation. We often hear that these tax cuts were “trickle-down economics” or “tax cuts for the rich and big business.” But the change in real (inflation-adjusted) wages was positive across the income spectrum. The bottom 10% of the wage distribution rose by 10% while the top 10% rose half as fast. And real wealth for the bottom 50% increased by 28%, while that of the top 1% increased by just 9%. The results show those tax cuts weren’t designed for the “rich.” In 2019, the real median household income hit a record high, and the poverty rate reached a record low. Poverty rates fell to the lowest on record for Blacks and Hispanics, and child poverty fell to 14.4%—a nearly 50-year low. Clearly, Americans were doing well across the board, especially those who had historically been left behind. These stellar results were from reducing barriers by government in people’s lives—a stark contrast to what happened by state governments during the pandemic and exacerbated thereafter by Biden’s big-government policies. While there were similar spending bills passed into law during both administrations, it’s comparing apples and oranges. Trump supported congressional efforts in March and April 2020 when huge swaths of the economy were shut down, 22 million Americans were laid off, and 70% of the economy faced collapse. In contrast, Biden substantially increased regulations immediately and passed a nearly $2 trillion spending bill in March 2021—an amount equal to approximately 10% of the U.S. economy, at a moment when the U.S. economy was already 10 months into recovery. Another difference was that Trump introduced sunsets for emergency pandemic provisions so that they would expire. But Biden continued and expanded many of them, increasing dependency on government. Through March 2022, employment is back up 20.4 million but remains 1.6 million below the peak in February 2020. While Biden touts the most jobs gained in one year in 2021, more jobs were recovered in just the two months of May and June 2020 than in all 12 months of 2021, and nearly two-thirds of this jobs recovery was during Trump. Moreover, job gains of 6.7 million in 2021 were far less than the glorified projections coming from the White House of around 10 million. Just think if Biden had practiced the pro-growth policies of Trump. Instead, inflation is at a 40-year high and looks to continue to soar, fueled by a host of self-imposed costly policies in Washington. This includes Biden’s over-regulating of the oil and gas sector, massive unnecessary spending bills, and attempts to drastically raise taxes. And the Federal Reserve has more than doubled its balance sheet over the last two years, purchasing a majority of the $6 trillion increased national debt in that period, which is a 25% increase to $30 trillion. These policies, which simultaneously boost demand while constraining supply, have brought the prospect of stagflation—high inflation and low growth—back for the first time since the late 1970s. Rather than directly addressing the crisis, Biden has consistently deflected the issue by first doubting the reality of inflation to now falsely blaming it on corporate greed or Russian President Vladimir Putin. But the causes and consequences fall at his feet. It’s time to return to the proven, pro-growth policies that worked during the Trump administration, along with an essential missing factor then of spending restraint by Congress. Doing so will provide a solid foundation for more opportunities to let people prosper. This commentary was based on the remarks by Mr. Ginn and Mr. Goodspeed on a panel at the Texas Public Policy Foundation’s 2022 Policy Orientation. https://www.texaspolicy.com/biden-should-pivot-to-trumps-pro-growth-policies/  Americans have less money than they had last year—though taxes haven’t been raised. So what’s the problem? Inflation, which has increased at a 40-year high annual pace of 7.9%. It acts as a hidden tax because we don’t see it listed on our tax bills, but we sure see less money on our bank accounts.

In fact, inflation-adjusted average hourly earnings for private employees are down 2.8% over the last year. This means a person with $31.58 in earnings per hour is buying 2.8% less of a grocery basket purchased just last February. “For a typical family, the inflation tax means a loss in real income of more than $1,900 per year,” stated Joel Griffin, a research fellow at The Heritage Foundation. The hidden tax of rapid inflation has been avoided for four decades. But that’s understandable because we haven’t seen these sorts of reckless policies out of Washington since the Carter administration. The policies from the Biden administration’s excessive government spending and the Federal Reserve’s money printing must correct course now before things get worse. What’s causing inflation is being debated. One claim is “Putin’s price hikes” stem from the Russian president’s invasion of Ukraine. While this has contributed to oil and gasoline prices spiking recently, these prices—and general inflation—were already rising rapidly. This was because of the Biden administration’s disastrous war on fossil fuels through increased financial and drilling regulations, cancelation of the Keystone XL pipeline, and more. Specifically, the price of West Texas Intermediate crude oil is up about 110% since Biden took office, yet only up 21% since Russia invaded Ukraine. And to think, the U.S. was energy independent in the sense that it was a net exporter of petroleum products in 2019. Another claim is the supply-chain crisis. For example, the global chip shortage has contributed to a large shortage and subsequent increase in the average price of new vehicles—to a record high of $47,000, up 12% over the last year. This contributed to buyers switching to used cars, which has pushed the average price up to nearly $28,000, about 40% higher. These two claims will likely be transitory price increases, though not sufficient to drive down overall inflation to what we’ve experienced for the last year-plus. Inflation is persistent because of rampant government spending and money printing. Larry Kudlow, who served as the director of the National Economic Council for President Trump, stated that inflation “is destroying working folks’ pocketbooks and devaluing the wages they earn, and the root cause of the inflation is way too much government spending, too many social programs without workfare, and vastly too much money creation by the Federal Reserve.” Both political parties share the blame for too much government spending, which has caused the national debt to balloon to $30 trillion. Just over the last two years, the debt has increased by 25% or $6 trillion. While some of that may have been necessary during the (inappropriate) shutdowns in response to the COVID-19 pandemic, much of the nearly $7 trillion passed in spending bills was not, especially the trillions by the Biden administration far after the pandemic had slowed and people were returning to work. Laughably, Speaker of the House Nancy Pelosi recently argued that government spending is helping inflation and President Biden argued that he’s cutting the deficit. Both are false. Government spending doesn’t change inflation because it just redistributes money around in the economy. And the deficit would only be rising from Biden’s big-government policies but he’s taking advantage of an optical illusion: one-time COVID-19 relief funding drying up and tax revenues rising partially from the effects of inflation. Ultimately, the driver of inflation is from discretionary monetary policy by the Federal Reserve as it monetizes much of the $6 trillion in added national debt since early 2020. The Fed did this to keep its federal funds rate target from rising above the range of zero to 0.25% by more than doubling its balance sheet to $9 trillion. More money is fueling the ugly government spending and bubbly asset markets that’s resulting in dire economic consequences. Instead, we need to learn what Presidents Harding and Coolidge realized a century ago. This would mean a return to sound fiscal policy, monetary policy, and the dollar that built on the principles of America’s founding. We need binding fiscal and monetary rules to hold politicians and government officials in check of we hope to tame inflation and return to prosperity. https://www.texaspolicy.com/the-tax-increase-thats-hidden-in-plain-sight/  An MSNBC headline reporting on a recent interview of a White House economic advisor Jared Bernstein claimed that America has a “booming economy.” But that’s not what most Americans think about the economic situation.

The University of Michigan’s consumer sentiment index for March, which gauges how consumers feel about the economy, fell to a decade low at 59.4. This is a 5.4% drop from February and a 30% drop from March 2021. The survey reveals Americans’ pessimism and uncertainty amidst the highest levels of inflation since the 1980s. Many Americans reported that they have had to reduce their quality of life and lower their living standards amidst the inflation crisis. This crisis has been created by the Federal Reserve printing too much money to fund the overspending by Congress, and exacerbated by the Biden administration’s war against oil and gas that fueled higher energy prices and have been amplified by the Russia-Ukraine conflict. The only positive news from the survey was slight optimism for the strengthening labor market. Survey statistics revealed that there was hope that the unemployment rate would continue to decline. While there are reasons to be optimistic about the labor market’s increase in monthly nonfarm jobs—431,000 (with 426,000 in the private sector)—and the unemployment rate dropping to 3.6%, weaknesses remain. For example, since the shutdown recession ended in April 2020, total nonfarm jobs are up 20.4 million but are still down 1.6 million from February 2020. This indicates that though the labor market is improving, but it’s not as strong as it was then. And while the Biden administration touts the jobs created since he took office in January 2021, only 39% have been added since then while the other 61% were during the Trump administration. Other unaddressed labor market weaknesses remain. Inflation-adjusted wages are down by 2.3% over the last year, a depressed prime-age (25-54 years old) employment-population ratio by 0.5 percentage point since February 2020, and a broader U6 underemployment rate of 6.9%. Further adding to the concern in the labor market is a record high of 5 million more unfilled jobs (11.3 million) than unemployed people (6.3 million). These ongoing weaknesses are shedding light on the impacts of big-government policies out of D.C., such as the “stimulus” checks, enhanced unemployment insurance, expanded child tax credits, and pandemic-related mandates, that have limited and are hindering the rebound of the American economy. Instead, we must return to normalcy if we wish to give Americans more opportunities to prosper. But that’s not happening. Paired with the inflation we’re dealing with stagnating economic growth, creating a period of stagflation for the first time since the 1970s. Rising inflation is foreshadowing concerns of a future recession and economic crisis as American families are paying substantially more for products and services amidst reduced purchasing power. Why is our economy out of control, and what can be done to mitigate the economic crisis? The government imposed a “shutdown recession” from March to April 2020 that proved devastating. Amidst the shutdown, elected officials heightened Americans’ economic dependence on government through $6 trillion in deficit-spending that included programs which disincentivized working. Two years later, there must be a return to the dignity and permanent value of work — instead of the dependence on the government that the Biden administration is promoting. For example, the Biden administration’s irresponsible proposed budget of $5.8 trillion includes massive spending while raising and creating harmful taxes, such as the new “billionaire tax” that Sen. Joe Manchin already shot down. The result of this irresponsible budget would be an increase in the debt by 50% to $45 trillion over the next decade, which is highly optimistic given their unlikely rosy economic assumptions. Given the likelihood of continued trillion-dollar deficits for the foreseeable future and the Fed keeping its target overnight lending rate low even as it raises the rate by printing more money means that more inflation and economic damage are to come. But this doesn’t have to happen. Congress should choose a different path, enacting pro-growth policies like those passed from 2017 to 2019, which will better provide Americans with opportunities to improve their lives and livelihoods. This should be paired with binding fiscal and monetary rules to stop Congress from overspending hard-earned taxpayer dollars and to stop the Fed from overprinting money that’s reducing families’ purchasing power. We should stop the “booming economy” rhetoric and focus on how families are doing. The way to give them more opportunities to flourish is by removing obstacles imposed by government. https://www.texaspolicy.com/booming-economy-not-if-you-ask-most-americans/  Watching the screen on a gas pump while filling your vehicle’s tank is liable to induce a panic attack. Paying for a used car almost requires taking out a second mortgage. Speaking of mortgages, members of the middle class are being priced out of the housing market as home prices march relentlessly upward. Many price increases are out of control.

How did we get here? A little over a year ago, and in the years before the Covid-19 pandemic, most prices were relatively stable. But more recently, general price inflation is at a 40-year high. The late economist Milton Friedman helped explain the inflation and stagflation of the 1970s. His explanation helped shape the strong economic recovery of the 1980s, built on the principles of limited government, with sound monetary policy that resulted in a steep decline in what had been rampant, double-digit inflation. Inflation Is a Monetary Phenomenon Friedman pointed out that “inflation is always and everywhere a monetary phenomenon.” The seemingly force majeure is actually a manmade problem, caused by the Federal Reserve (Fed) creating too much money. These principles of money and inflation aren’t new. But those lessons are being disregarded by some in the economics profession. People like Stephanie Kelton have been promoting Modern Monetary Theory (MMT), which is virtually a complete reversal of what Friedman espoused and history demonstrated. This theory contends that the federal government’s current deficit spending isn’t an issue — it can, and should, be solved by the Fed creating money to fund it without concern about inflation as long as the U.S. dollar is the world’s reserve currency. President Joe Biden has not openly endorsed MMT, but he’s no fan of Friedman either. Instead, he seems content to have many mostly younger congressional Democrats advocate for MMT, which provides convenient and seemingly academic reasoning for financing more federal spending without explicitly raising taxes. It has a similar political appeal that Keynesianism presented almost a century ago, and MMT is just as flawed. But proponents of MMT do get one thing correct — the Fed can create money to service the debt and avoid a default. But in real terms, meaning adjusting for inflation, this assertion is false. Creating money to service the debt devalues the currency. Investors then receive a lower real return on their holdings of federal debt. Furthermore, everyone is hurt by inflation, whether they own government bonds or not. Inflation is essentially a tax, as it robs people of their purchasing power at no fault of their own. Everyone who received a 7.5 percent raise over the last year probably thought they would be able to afford more stuff, but they were deceived. Inflation rose just as much — so there was no real raise. False Claims That Taxes Are the Solution But MMT proponents claim that the massive budget deficits are what allow people to save money. Were it not for those deficits, they contend, people would have no cash to save. At first glance, the pandemic seemed to support that. People received transfer payments from the government and saved much of them due to uncertainty. But more recently, people’s savings are being depleted as this dependency on government dries up and prices soar. Now that inflation is running amok, MMT adherents believe tax increases are the primary (if not only) cure. They claim inflation is not caused by the Fed creating too much money, but by people having too much money to spend; taxation will remove that excess liquidity and stop inflation. However, MMT doesn’t explain why it’s only inflationary when people spend money, but not when the government spends it. Somehow the Fed creating money by purchasing government debt miraculously doesn’t bid up prices for scarce resources. The theory sounds more like a belief than science — something that must be trusted rather than demonstrated. Specifically, MMT ideology is built on mathematical relationships between economic variables like private and public savings and debt rather than a strong theoretical construct, and breaks down quickly when analyzed with sound economic theory. Moreover, these relationships seem to be used to derive a funding mechanism for their big-government policy goals, such as a federal jobs guarantee, universal healthcare, and other costly initiatives. How Taxation Might Stop Inflation But MMT is not entirely wrong on using taxation to stop inflation. If those taxes are used to pay for deficit spending — which really should be done by spending less — rather than the Fed financing it, then higher taxes can lower inflation. But that is far too nuanced of an explanation for MMT, which paints in much broader brushstrokes. Regardless, MMT cannot dispel the hard truths of monetary policy, which is inflation comes from one place — the Fed. When the Fed creates money faster than the real economy grows, prices will rise; it’s that simple. To alleviate the uncertainty and distortions across the economy of bad policies in Washington, there should be binding fiscal and monetary rules based on sound economics instead of ideology. This should include changing government spending by less than the growth in personal incomes and only changing the money supply to keep prices stable. Almost two years after President Biden declared “Milton Friedman isn’t running the show anymore,” the late economist is clearly the one with the last laugh. Perhaps next time, the president will think twice before speaking ill of the dead. https://www.texaspolicy.com/the-real-cause-of-inflation-is-insane-government-spending/  Even though Sen. Joe Manchin says the Build Back Better Act is “dead,” we all know that spending plans in the D.C. swamp have a disturbing tendency to rise from the grave. There’s already speculation (on CNN and elsewhere) about what a new big-government spending bill will contain.

But with the national debt recently surpassing $30 trillion, we can’t allow even more irresponsible spending. The time for a Responsible American Budget is now. Another big-government bill making its way down the pike is The America COMPETES Act of 2022, which the House passed last week. It contains up to $350 billion more in deficit spending, all in the name of making us more competitive with China. This includes billions and billions of dollars in corporate giveaways, such as sending $50 billion in taxpayer money to the semiconductor industry, another $50 billion to the Energy Department as a slush fund for “science purposes” and $8 billion to the U.N. Green Climate Fund. That fiscal cost plus the bill’s regulatory cost will make the nation substantially less competitive. The truth is, what Americans and Texans need is relief, not more debt and higher prices. The last two years have been increasingly difficult on our wallets. With inflation hitting a 40-year high, prices of everyday consumer goods continue to increase compared to years past, thereby reducing our purchasing power. As the nation continues to recover economically, now is not the time to continue discussing increasing the burden of federal government spending and taxing on Americans. Should it pursue fiscal excesses like those included in the Build Back Better Act, each American would be saddled with an additional $24,000 of national debt, raising the total debt owed by each taxpayer to $111,000. Over the past couple of years, we’ve seen major Texas metropolitan markets like in Dallas, Austin, and Houston become the new home to many companies in industries like technology and manufacturing. As quickly as Texas begins to see these new job opportunities, there is the potential for them to vanish should Congress raise taxes. While the Tax Cuts and Jobs Act helped to increase the competitive advantage for businesses through cutting the corporate tax rate from 35% to 21%, there is movement to raise this rate and raise the global intangible low-taxed income (GILTI) rate on businesses. This would follow a disruptive trend of imposing a global minimum tax rate of 15% that was agreed to by more than 130 countries in October 2021, which would hit Texans hard. Much like our business community, Texans could find themselves struggling to get by as they see things like their inflation-adjusted wages decline, making it difficult to afford things like childcare or increasing challenges in saving for retirement. There should be a united voice in opposing additional hikes in spending and taxes and help refocus Congress toward supporting a stronger economy and more opportunities with fiscal restraint and deregulation that have been proven to work for all. A good start is making the Trump tax cuts permanent. Of course, America doesn’t have a revenue problem, but a spending problem. So, the primary way to provide Texans and all Americans with relief is by passing a Responsible American Budget. This budget would freeze government spending per person so that there is less of a burden on taxpayers. This budget approach has received high praise from members of Congress, top economists, state policymakers, and experts from across the country. Here are three of the many takes: Art Laffer: “Government spending is taxation, and we cannot spend and tax our way into prosperity. The Responsible American Budget is a terrific way to rein in this government waste by imposing fiscal limitations on the profligate spenders in Washington.” Steve Moore: “Spending in D.C. is simply out of control, and we have to act now to stop it. Fiscal restraints like the Responsible American Budget will go a long way to preserving our freedom and unleashing prosperity.” Grover Norquist: “There has been success in reducing federal tax rates in recent years, which President Biden and congressional Democrats are now trying to undo. Where we’ve yet to make sufficient progress is reining in federal spending. With the Responsible American Budget, the Texas Public Policy Foundation has laid out plan to get federal spending under control.” If we can have less spending, taxing, and regulating, we can compete and return to the real prosperity earned in 2019 rather than the increased dependency on government today. Otherwise, America can’t compete. https://www.texaspolicy.com/the-u-s-needs-a-responsible-american-budget/  Government spending is at the heart of sound public policy. But out-of-control spending for decades has created substantial economic destruction and ongoing threats that must be remedied before things get worse. Fortunately, we have examples of how fiscal rules can solve this problem. We must put these rules into place before our economy gets any worse.

Excessive federal government spending has created mounting budget deficits that have driven the national debt to $30 trillion. This debt has given the Federal Reserve ammunition to use to excessively print money, resulting in the highest inflation in 40 years. And inflation destroys our purchasing power as it is a hidden tax that erodes our livelihood. Controlling spending takes discipline, and applying fiscal rules can help. Policymakers should follow the examples a century ago of Presidents Warren G. Harding and Calvin Coolidge, who demonstrated that controlling spending and cutting the debt is possible. President Harding assumed office in 1921 when nation was suffering an overlooked severe economic depression. Hampering growth were high income tax rates and a large national debt after WWI. Congress passed the Budget and Accounting Act of 1921 to reform the budget process, which also created the Bureau of the Budget (BOB) at the U.S. Treasury Department (which was changed in 1970 to the Office of Management and Budget in the Executive Office of the President). President Harding’s chief economic policy was to rein in spending, reduce tax rates, and pay down debt. Harding, and later Coolidge, understood that any meaningful cuts in taxes and debt couldn’t happen without reducing spending. Charles G. Dawes was selected by Harding to serve as the first BOB Director. Dawes shared the Harding and Coolidge view of “economy in government.” In fulfilling Harding’s goal of reducing expenditures, Dawes understood the difficulty in cutting government spending as he described the task as similar to “having a toothpick with which to tunnel Pike’s Peak.” To meet the objectives of spending relief, the Harding administration held a series of meetings under the Business Organization of the Government (BOG) to make its objectives known. “The present administration is committed to a period of economy in government…There is not a menace in the world today like that of growing public indebtedness and mounting public expenditures…We want to reverse things,” explained Harding. Not only was Harding successful in this first endeavor to reduce government expenditures, his efforts resulted in “over $1.5 billion less than actual expenditures for the year 1921.” Dawes stated: “One cannot successfully preach economy without practicing it. Of the appropriation of $225,000, we spent only $120,313.54 in the year’s work. We took our own medicine.” Overall Harding achieved a significant reduction in spending. “Federal spending was cut from $6.3 billion in 1920 to $5 billion in 1921 and $3.2 billion in 1922,” noted Jim Powell, a Senior Fellow at CATO Institute. Harding and the Republican Party viewed a balanced budget as not only good for the economy, but also as a moral virtue. Dawes’s successor was Herbert M. Lord, and just as with the Harding Administration, the BOG meetings were still held on a regular basis. President Coolidge and Director Lord met regularly to ensure their goal of cutting spending was achieved. Coolidge emphasized the need to continue reducing expenditures and tax rates. He regarded “a good budget as among the most noblest monuments of virtue.” Coolidge noted that a purpose of government was “securing greater efficiency in government by the application of the principles of the constructive economy, in order that there may be a reduction of the burden of taxation now borne by the American people. The object sought is not merely a cutting down of public expenditures. That is only the means. Tax reduction is the end.” “Government extravagance is not only contrary to the whole teaching of our Constitution, but violates the fundamental conceptions and the very genius of American institutions,” stated Coolidge. When Coolidge assumed office after the death of Harding in August 1923, the federal budget was $3.14 billion and by 1928 when he left, the budget was $2.96 billion. Altogether, spending and taxes were cut in about half during the 1920s, leading to budget surpluses throughout the decade that helped cut the national debt. The decade had started in depression and by 1923 the national economy was booming with low unemployment. If this conservative budgeting approach—which was tied with sound monetary policy for most of the period—had been continued, the Great Depression wouldn’t have happened. Officials at every level of government today should learn from this extraordinary lesson that fiscal restraint supports more economic activity as more money stays in the productive private sector. With spending out of control at the federal level and in many states and local governments, the time is now for spending restraint and strong fiscal rules to set the stage for more economic prosperity today and for generations to come. https://www.texaspolicy.com/learning-from-the-champions-of-fiscal-conservatism/  “May you live in interesting times,” goes an old saying—usually meant as a curse. When it comes to economics, “interesting” usually means the sky is falling.

Inflation reached 7% at the end of 2021, a rate not seen in 40 years. The Federal Reserve’s balance sheet more than doubled to $8.8 trillion since early 2020. And Uncle Sam’s fiscal house is in shambles. The 2021 budget deficit was almost $2.8 trillion, putting the national debt at $28.5 trillion—nearly 130% of U.S. gross domestic product. To call this imprudent would be a massive understatement. We need fiscal and monetary rules now. Money mischief and fiscal follies are intimately related. This isn’t because deficit spending causes inflation—things aren’t that simple. Instead, profligate spending and careless money-printing reinforce each other. When politicians and bureaucrats have too much leeway, they pursue short-run benefits at the expense of long-run viability. Whether it’s easy money from the Fed or stimulus checks from Congress, papering over unsustainable financial practices is easier than enacting sustainable reforms. To improve Americans’ livelihood, we must break the cycle. Because policymakers have demonstrated they can’t be trusted with discretion, it’s time to give binding rules a try. We can’t reform fiscal or monetary policy alone. Economic flourishing for Americans depends on tackling both. In the past two years, the Fed purchased more than $3.3 trillion in government debt. Over that same period, Uncle Sam’s deficit totaled almost $6 trillion. That means our central bank indirectly covered more than half of the federal government’s fiscal splurge. Also, Congress authorized spending of roughly $7 trillion since the pandemic started. Even the latest $1.9 trillion American Rescue Plan Act, sold to Americans as a “stimulus,” merely promoted more government. These programs contributed to fewer jobs added last year than the Congressional Budget Office’s baseline. All that wasteful spending drags down the economy. This is worryingly close to what economists call “fiscal dominance”—monetary policymakers paving the way for spending binges with cheap liquidity. Adam Smith, the godfather of economics, wrote about the continuous cycle of deficits, debt accumulation, and currency debasement that ruins nations. We should work diligently and quickly to ensure the U.S. doesn’t follow. The solution is a rules-based approach for fiscal and monetary policies. We need strong guardrails around runaway spending and money-printing. A rules-based framework can ensure fiscal and monetary policies work better, both independently and with each other. For example, we should consider a spending limit that covers the entire budget, capping spending increases at population growth plus inflation. This essentially freezes per capita government spending. By limiting total expenditures, we can minimize the burden on current and future taxpayers. Had this been in place from 2002 to 2021, the cumulative effect on the budget would be a net surplus (debt decline) of $2.8 trillion. This is in stark contrast to the $19.8 trillion in net debt we actually got. Cutting the national debt means the Fed would have fewer assets to purchase in its open market operations, thereby reducing its ability to manipulate markets and the overall economy. It could then focus on what it can control: price stability. A rule should help achieve this. The Fed drifted off course by needlessly broadening its inflation rule in August 2020. The Fed’s mandate currently includes price stability, maximum employment, and moderate interest rates. But the second and third of these are beyond the competence of central bankers. It’s time to focus the Fed on controlling the dollar’s value. Congress and the Fed harmed the vibrancy and robustness of the U.S. economy by their poor decisions. Unfortunately, there’s been a bipartisan consensus for irresponsible fiscal and monetary policies in recent years. It’s time for this to change. We need rules-based fiscal and monetary policy to get our economic affairs in order and leave post-pandemic malaise behind for good. https://www.texaspolicy.com/out-of-control-congress-and-fed-need-binding-rules/ |

Vance Ginn, Ph.D.

|

RSS Feed

RSS Feed

Proudly powered by Weebly