|

In "This Week's Economy" Ep. 2, I provide brief insights on the economies of U.S., Texas, & Louisiana; talk about the TX House Budget; and note how Biden's green energy agenda results in poverty. Thank you for listening to the second episode of "This Week's Economy," a new series of the "Let People Prosper" podcast, where I quickly recap and share my insights every Friday morning on key economic news from the preceding week.

Today, I cover:

You can watch this episode on YouTube or listen to it on Apple Podcast, Spotify, Google Podcast, or Anchor (please share, subscribe, like, and leave a 5-star rating).

0 Comments

In co-dependent relationships, there’s often an enabler compounding the destructive behavior. In the case of the Silicon Valley Bank collapse and a possible crisis for the banking industry, the Federal Reserve and its fast-and-loose monetary policy is that toxic enabler. If only couples counseling could fix the muddled relationship between the Fed and the banking industry.

Over the past three years, the Fed has monetized much of Congress’s excessive deficit spending, thereby bringing inflation to a 40-year high and distorting the banking industry and economy. To take advantage of that extra liquidity, SVB (and many other banks) invested in riskier assets: interest-rate-sensitive bonds. Banks were unprepared for the Fed’s sudden pivot last year when it began increasing interest rates in an effort to control elevated inflation. To be sure, they ignored many warning signs, such as a bloated Fed balance sheet and supply chain disruptions. And when the Fed raised its target federal funds rate from near 0% to today’s range of 4.75% to 5%, bonds began losing significant value. In SVB’s case, the bank had to realize huge losses when it made its mark-to-market calculations for its balance sheet, as it shifted investments from hold-to-maturity to available-for-sale status, hoping to satisfy its depositors by selling those assets. The losses proved too substantial, rendering the bank insolvent. The actions of the Fed certainly incentivized the kind of risk-taking that led to SVB’s insolvency and failure, but the bank was far from an innocent victim as it abandoned basic risk management. It loaded its balance sheet with risky investments while prioritizing social agendas over profits, investing in ESG initiatives that performed poorly. At the time of its failure, SVB looked more like a hedge fund than a commercial bank. But instead of letting SVB and its depositors face the consequences of the bank’s mismanagement, the Federal Deposit Insurance Corporation, Federal Reserve, Department of Treasury, and White House launched coordinated rescue actions, determining that all depositors of the failed bank would be saved. The FDIC’s traditional policy of insuring accounts up to $250,000 was seemingly obliterated by this decision, establishing an entirely new regime. The Fed and FDIC justified the SVB rescue by claiming that the bank represented a “systemic risk” though it was only a mid-level-sized bank. This further muddied the waters as to how the Fed and FDIC determine which institutions are “too big to fail.” Further compounding the issue was Treasury Secretary Janet Yellen’s testimony to the Senate Finance Committee guaranteeing all deposits of “Too Big to Fail” banks. The fallout from this new regime, which focuses only on the deposits of the largest banks, creates an incentive for depositors with more than $250,000 to shift their deposits to the largest banks that will accept them. This will put pressure on mid-level and smaller banks as they must now compete for larger deposits that will be uninsured at their banks. The result of this challenge will likely be more consolidation across the banking sector, thus making the big banks that much larger. In a sane society, troubled banks such as SVB would be allowed to fail, and the depositors would lose their deposits above the $250,000 insured amount. But financial socialism is growing. Profits are privatized, losses are socialized, and everyone in government is tripping over each other to bail someone out. The current rescue actions and the promise of more are not a part of the free market capitalism that has supported wealth and prosperity throughout America’s history. These actions send a loud and clear signal to all banks: go ahead and take the risk! We’ll finance your failure with a more accommodative monetary policy. It should come as no surprise when more banks begin backsliding due to this messaging. As things stand, no sector, including the banking industry, is incentivized via market discipline to reduce risky behaviors thanks to the government’s outsize role. The ones who suffer most from this are consumers seeking services, who will inevitably be left with more mediocre options as government handouts cover competition. To avoid this and strengthen the economy, Washington needs to end bailouts. The Fed needs to keep raising its target federal funds rate and more aggressively reduce its bloated balance sheet, which it increased by $300 billion recently, to rein in inflation and let markets work. Likewise, Congress should cut spending to stop issuing so many Treasury securities that fund the more than $31 trillion national debt. This system where the Fed micromanages the free market instead of allowing the free market to work out problems on its own will continue to impoverish the economy. Indeed, Fed Chairman Jerome Powell’s suggestion last week that target rate hiking is nearing an end means Americans can expect more inflation and more economic distortions for a longer period of time. The recent events provide further evidence that it is past time to reevaluate the structure, governance, and operating rules of the Fed. Indeed, Washington’s response to the SVB failure proves the entire financial arm of the government ought to be thoroughly reformed so that market discipline can be returned to the banking sector. If significant change doesn’t happen, the troubled co-dependent relationship between the banking sector, the Fed, and Washington’s bureaucracy will never heal. For Americans, that means waiting on the next Fed-fueled boom and bust cycle. Originally published at the Washington Examiner. Overview

On today's episode of the "Let People Prosper" show, which was recorded on Feb. 24, 2023, I'm honored to be joined by Dr. Tyler Goodspeed, who is an economist, fellow at the Hoover Institution at Stanford University, and was acting chairman of the White House’s Council of Economic Advisers from 2020 - 2021.

We discuss:

You can watch this interview on YouTube or listen to it on Apple Podcast, Spotify, Google Podcast, or Anchor (please share, subscribe, like, and leave a 5-star rating). Dr. Goodspeed’s bio and other info (here):

The push to ditch reliable energy is out of control. Politicians are manipulating the energy market through subsidies, tax breaks, and environmental, social, and corporate governance (ESG) initiatives in regulations and government pensions.

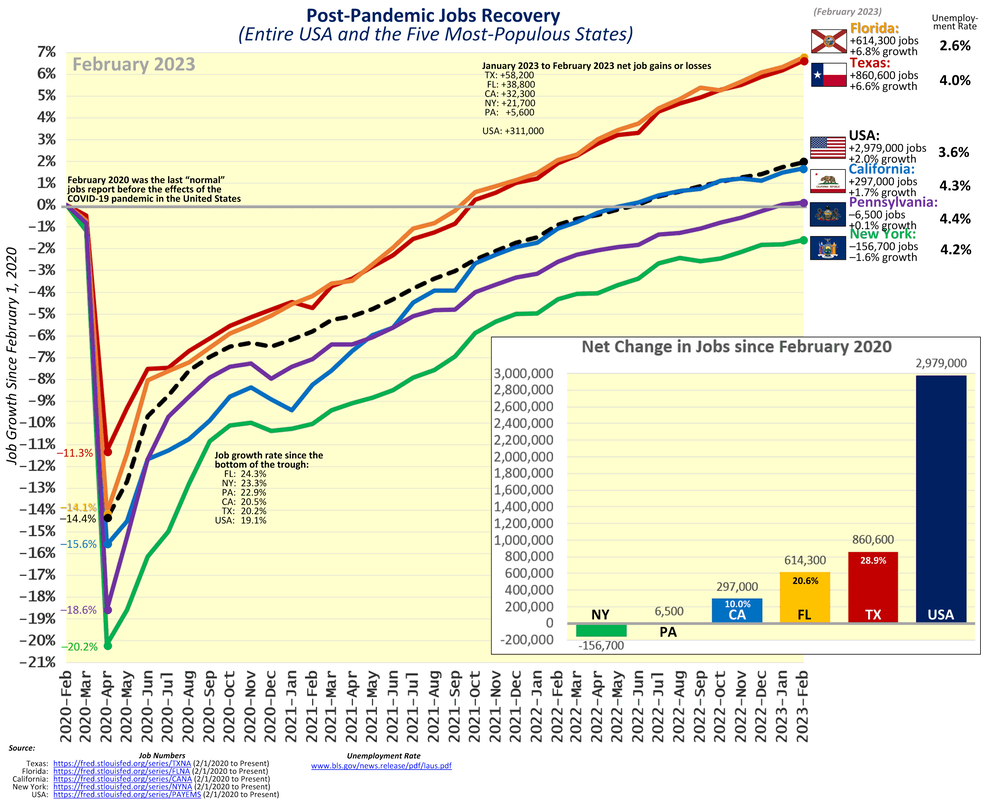

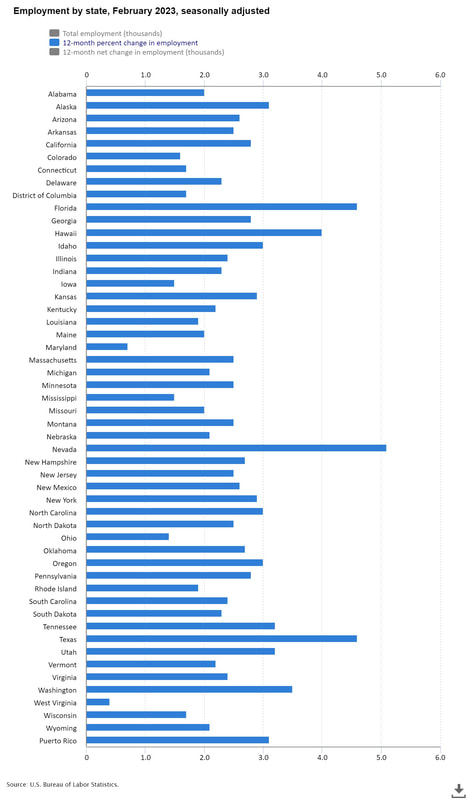

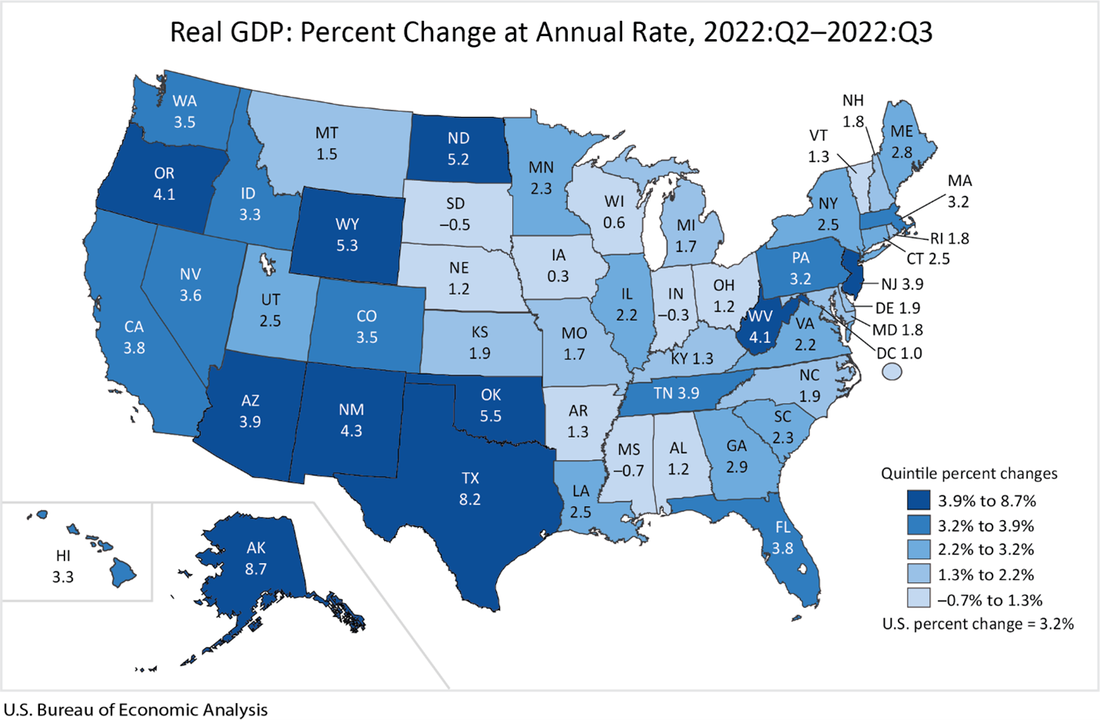

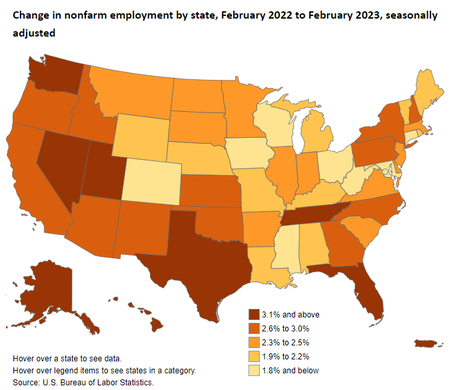

It’s also concerning that the “big three” investment institutions, which collectively hold over $20 trillion in assets, too often coerce the companies in which they have significant investments to bend the knee to their big-government political ideology, such as complying with the Paris Climate Accord. Sadly, the result of this virtue signaling to prop up unreliable wind and solar comes at high costs for little benefits—if any benefits at all. And more than hemorrhaged taxpayer dollars are at stake: this green energy agenda increases poverty. It must stop. While the media is constantly ringing alarm bells about the always-changing climate, not enough people are alarmed by the economic trade-offs these unreliable green energy initiatives create. But that requires an honest comparison of the climate change risks versus the economic costs, both of which impact future generations. The International Energy Agency (IEA) finds that there were an expected 20 million more people without electricity globally, totaling 775 million people, in 2022. Many of these people are in sub-Saharan Africa, who are facing increasing hardship due to rising costs for food, fuel and other necessities. This situation is made worse by the left’s insistence on unreliable sources of energy that have forced many Europeans to use wood for stoves and heat instead of much cleaner-burning natural gas. Forcing some of the population to depend on energy sources that don’t work ultimately pushes them into hardship and poverty when those methods fail. Texas experienced this problem in a tragic way two years ago during its historic weather event of freezing temperatures and accumulations of ice and snow that left thousands without power, contributing to an estimated 246 deaths. Such a tragedy should never have happened in America’s energy capital, but these are gambles that politicians take when offering subsidies to unreliable variable energy providers that make it difficult for reliable thermal energy to compete, even though thermal energy is the most stable and reliable form. Fortunately, Texas let a property tax break for businesses called Chapter 313 expire in December 2022. That tax break was often used by renewable energy companies to lower their tax bills (and operating costs). Still, some already want to bring Chapter 313 or something like it back. This should be a non-starter. That’s not to say that climate change couldn’t have consequences, but considering the projected minimal benefits from expensive initiatives by politicians and the need for adaptation, the trade-offs seem hardly worth it. And this says nothing of the benefits of more CO2, which is necessary for life on earth. More broadly, if every signatory of the Paris Accord, including India and China, decarbonized by 2050, the temperature differentiation by 2100 would be just 0.17 degrees. And according to climate change activists, the cost to get there could be as much as $21 trillion through 2050. Businesses attempting to go green would be forced to raise their prices significantly to make a profit, a normally tough task that’s only made harder by present-day sky-high inflation. But if subsidies and other artificial means of skewing the energy market continue, then businesses that don’t receive subsidies and can’t afford to “go green” simply won’t be able to compete. This would result in a massive reallocation of resources that will contribute to less economic growth, more poverty, and less energy stability. Not only can over-dependence on unreliables lead to hardship, but it often counteracts the green energy innovation it wants to spur. One of the reasons the U.S. is so prosperous is that it is the most responsible and efficient at producing and utilizing energy, having reduced criteria pollutants 78% in the last 50 years. And what has supported this is our wealth acquired via free-market capitalism. That’s why the best thing for activists and politicians seeking improved adaptation to climate change is to get out of the way and let the free markets, meaning free people, work. Subsidies, tax breaks, ESG initiatives, and other hindrances to a well-functioning market process should be abandoned. When politicians push funds into green energy agendas, often to win votes through virtue signaling, precious scarce taxpayer resources are wasted. Markets work, but we have to let them. Individuals and entities should be left alone when choosing which energy sources to direct their funds and business. Otherwise, the outcome is less prosperity and more poverty. There is a better way. Originally posted at Real Clear Energy. Key Point: Texas continues to be a leader in job creation over the last year (chart below by @SoquelCreek) and set employment records across the state, but Texans who are struggling from an affordability crisis would benefit from less spending, regulating, and taxing.  Overview: Texas has been a national leader in the economic recovery since the inappropriate shutdown recession in Spring 2020. This includes reaching a new record high in total nonfarm employment for the 17th straight month, leading exports of technology products for 21 consecutive years, and being home to the most Fortune 500 companies in the country with more than 50. While the 87th Texas Legislature passed a Conservative Texas Budget and passed country’s strongest state spending limit, the current 88th Texas Legislature has more to do to freeze spending and use more than $60 billion in excess taxes collected to put school district maintenance and operations on a path to elimination so Texans can stop renting and start owning their property.  Labor Market: The best path to prosperity is a job, as it helps bring financial self-sufficiency, dignity, hope, and purpose to people so they can earn a living, gain skills, and build social capital. The table below shows Texas’ labor market for February 2023.  The establishment survey shows that net nonfarm jobs in Texas increased by 58,200 last month, resulting in increases for 33 of the last 34 months, to bring record-high employment to 13.8 million. Compared with a year ago, total employment was up by 611,400 (+4.6%)—second fastest growth rate in the country to Nevada—with the private sector adding 560,100 jobs (+5.0) and the government adding 51,300 jobs (+2.6%).  The household survey shows that the labor force participation rate and employment-population rate are slightly lower than in February 2020, but the former is well below June 2009 at the trough of the Great Recession. The private sector now employs 800,000 more people than pre-pandemic. Texans face challenges with a worse unemployment rate, though historically low but higher than U.S. rate of 3.6% though many have dropped out of the labor force elsewhere. Economic Growth: The U.S. Bureau of Economic Analysis (BEA) reported the real gross domestic product (GDP) by state for Q3:2022. The figure below shows Texas had the second fastest GDP growth (first is Alaska) of +8.2% on an annualized basis to $1.89 trillion (above the U.S. average of +3.2% to $20.05 trillion). In the prior quarter, Texas had the fastest growth with +1.8% growth as the U.S. average declined by -0.6% that quarter. Of course, these followed Texas’ GDP contractions of -7.0% in Q1:2020 and -28.5% in Q2 during the depths of the shutdown recession. Fortunately, GDP rebounded in Q3 and Q4, yet declined overall in 2020 by -2.9% (less than -3.4% decline of U.S. average) but increased by +3.9% in 2021 (below the +5.9% U.S. average). The BEA also reported that personal income in Texas grew at an annualized pace of +6.9% in Q3:2022 (ranked 6th highest and faster than the U.S. average of +5.3%) but slower than the robust +8.4% in Q2:2022 (ranked 6th best and above the U.S. average of +4.9%) as job creation and inflated income measures found their way across the economy.  Bottom Line: As Texans face an affordability crisis from high inflation and high property taxes and an uncertain future with the U.S. economy likely in a recession, they need substantial relief to help make ends meet. Other states are cutting, flattening, and phasing out taxes, so Texas must make bold reforms to support more opportunities to let people prosper, mitigate the affordability crisis, and withstand destructive policies out of D.C.

Free-Market Solutions: In 2023, the Texas Legislature should improve the Texas Model by:

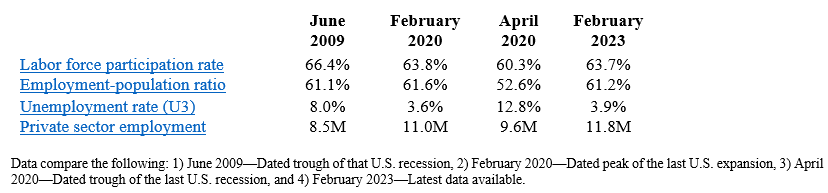

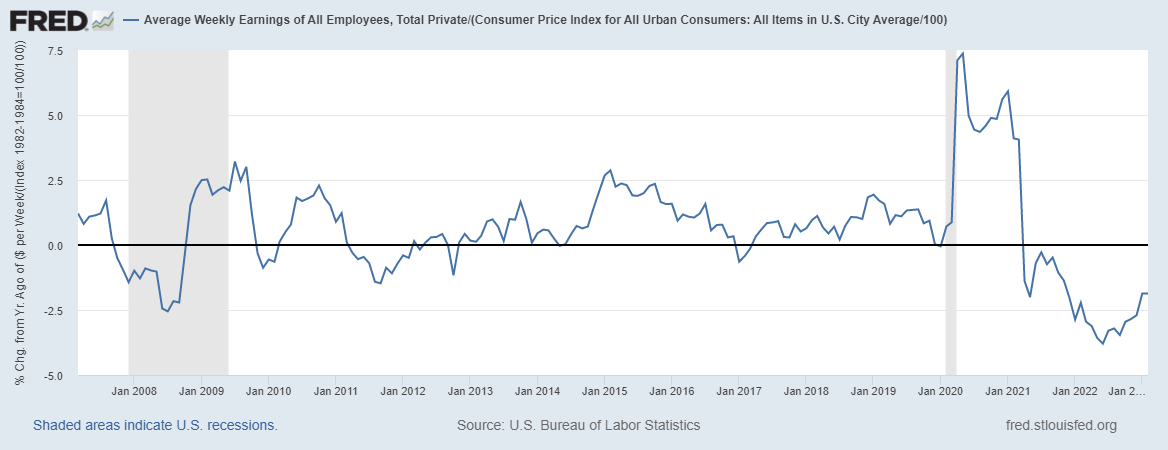

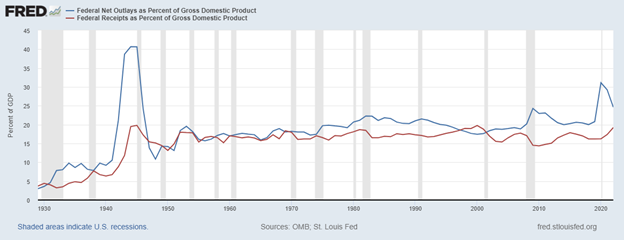

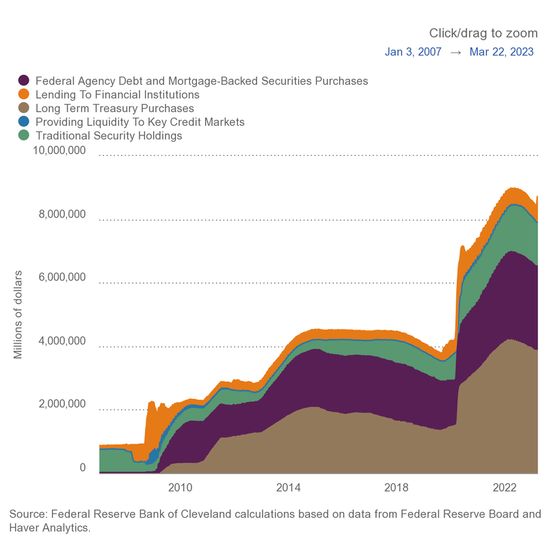

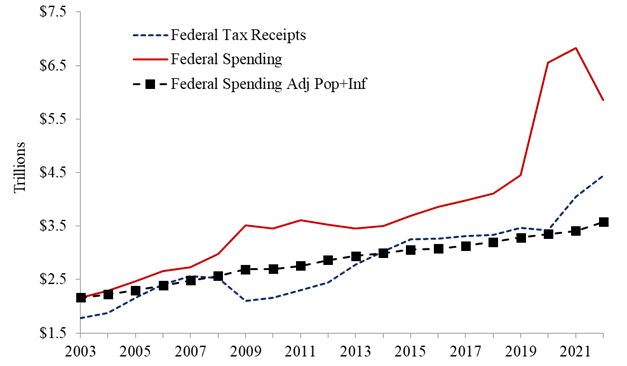

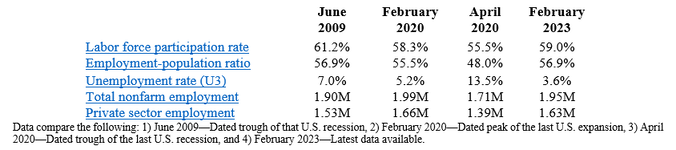

Key Point: Average weekly earnings adjusted for inflation are now down for 23 straight months year-over-year as inflation keeps roaring. But there’s hope if we give free-market capitalism a chance to let people prosper.  Overview: The government failures that drove the “shutdown recession,” high inflation, and weak economic growth over the last three years continue to plague Americans. This includes excessive federal spending leading to massive cumulative deficit spending of $7.6 trillion since January 2020 to reach $31.6 trillion in national debt—about $250,000 owed per taxpayer. This has created a fight between the Biden administration and House Republicans over the debt ceiling, as raising it must come with spending restraint. And more inflation is on the horizon as the Federal Reserve recently increased its balance sheet and the government creates rampant moral hazard by insuring what appears to be all deposits at big banks. The solution to these problems are pro-growth policies of shrinking government back to its constitutional roles. Labor Market: The Bureau of Labor Statistic recently released its U.S. jobs report for February 2023. After substantial revisions in the previous report which likely indicate bias in these data for a while, there were some signs of strength while others suggest weakness. The establishment survey shows there were +311,000 (+2.9%) net nonfarm jobs added in February to 155.4 million employees, with +265,000 (+3.0%) added in the private sector and +46,000 (+1.9%) jobs added in the government sector. Most of the private sector jobs were added in the sectors of leisure and hospitality (+105,000), private education and health services (+74,000), and retail trade (+50,100), which the first two sectors also led over the last 12 months; information (-25,000), manufacturing (-4,000), utilities (-1,100), and financial activities (-1,000) had net job declines last month and only retail trade (-2,300) declined over the last year. The household survey had another increase of +177,000 jobs to 160.3 million employed. There have been declines in net jobs in four of the last 11 months for a total increase of +2 million since March 2022, which is about half of the +3.9 million net jobs per the establishment survey. The official U3 unemployment rate rose to 3.6% and the broader U6 underutilization rate rose to 6.8%. Since February 2020 before the shutdown recession, the prime age (25-54 years old) employment-population ratio is flat at 80.5%, prime-age labor force participation rate was 0.1-percentage point higher at 83.1%, and the total labor-force participation rate was 0.8-percentage-point lower at 62.5%with millions of people out of the labor force thereby holding the U3 unemployment rate artificially low But challenges remain for Americans as inflation-adjusted average weekly earnings were down -1.9% over the last year for the 23rd straight month. Economic Growth: The U.S. Bureau of Economic Analysis’ recently released the 2nd estimate for economic output for Q4:2022. The following table provides data over time for real total gross domestic product (GDP), measured in chained 2012 dollars, and real private GDP, which excludes government consumption expenditures and gross investment. And most of the estimates for Q4:2022 and growth in 2022 were revised lower, providing more evidence that 2022 was a very weak year if not a recession.  Economic activity has had booms and busts thereafter because of inappropriately imposed government COVID-related restrictions in response to the pandemic and poor fiscal policies that severely hurt people’s ability to exchange and work. Since 2021, the growth in nominal total GDP, measured in current dollars, was dominated by inflation, which distorts economic activity. The GDP implicit price deflator was +6.1% for Q4-over-Q4 2021, representing half of the +12.2% increase in nominal total GDP. This inflation measure was +9.1% in Q2:2022—the highest since Q1:1981—for a +8.5% increase in nominal total GDP that quarter. This made two consecutive declines in real total (and private) GDP, providing a criterion to date recessions every time since at least 1950. In Q3:2022, nominal total GDP was +7.6% and GDP inflation was +4.4% for the +3.2% increase in real total GDP. But if inflation had been as high as it was in the prior two quarters or had the contribution of net exports of goods and services (driven by natural gas exports to Europe) not been 2.9%, real total GDP would have either declined or been essentially flat for a third straight quarter. In Q4:2022, there was a similar story of weakness as nominal total GDP was +6.6% and GDP inflation was +3.9% for the +2.7% increase in real total GDP. But if you consider the +2.7% real total GDP growth was driven by contributions of volatile inventories (+1.5pp), government spending (+0.6pp), and next exports (+0.5pp) which total +2.6pp, the actual growth is quite tepid like it was in Q3:2022. For all of 2022, real total GDP growth is reported +2.1% year-over-year but measured by Q4-over-Q4 the growth rate was only +0.9%, which was the slowest Q4-over-Q4 growth for a year since 2009 (last part of Great Recession). The Atlanta Fed’s early GDPNow projection on March 24, 2023 for real total GDP growth in Q1:2023 was +3.2% based on the latest data available. The table above also shows the last expansion from June 2009 to February 2020. A reason for slower real private GDP growth in the latter period is due to higher deficit-spending, contributing to crowding-out of the productive private sector. Congress’ excessive spending thereafter led to a massive increase in the national debt by nearly +$7 trillion that would have led to higher market interest rates. This is yet another example of how there is always an excessive government spending problem as noted in the following figure with federal spending and tax receipts as a share of GDP no matter if there are higher or lower tax rates.  But the Fed monetized much of the new debt to keep rates artificially lower thereby creating higher inflation as there has been too much money chasing too few goods and services as production has been overregulated and overtaxed and workers have been given too many handouts. The Fed’s balance sheet exploded from about $4 trillion, when it was already bloated after the Great Recession, to nearly $9 trillion and is down only about 2.6% since the record high in April 2022 after rising nearly $400 billion in March 2023. The Fed will need to cut its balance sheet (total assets over time) more aggressively if it is to stop manipulating so many markets (see figure below with types of assets on its balance sheet) and persistently tame inflation, which there’s likely a need for deflation for a while given the rampant inflation over the last two years.  The resulting inflation measured by the consumer price index (CPI) has cooled some from the peak of +9.1% in June 2022 but remains hot at +6.0% in February 2023 over the last year, which remains near 40-year highs along with other key measures of inflation. After adjusting total earnings in the private sector for CPI inflation, real total earnings are up by only +2.2% since February 2020 as the shutdown recession took a huge hit on total earnings and then higher inflation hindered increased purchasing power. Just as inflation is always and everywhere a monetary phenomenon, deficits and taxes are always and everywhere a spending problem. The figure by David Boaz at Cato Institute shows how this problem is from both Republicans and Democrats. As the federal debt far exceeds U.S. GDP, America needs a fiscal rule like the Responsible American Budget (RAB) with a maximum spending limit based on population growth plus inflation. If Congress had followed this approach from 2003 to 2022, the figure below shows tax receipts, spending, and spending adjusted for only population growth plus chained-CPI inflation. Instead of an (updated) $19.0 trillion national debt increase, there could have been only a $500 billion debt increase for a $18.5 trillion swing in a positive direction that would have substantially reduced the cost of this debt to Americans. The Republican Study Committee recently noted the strength of this type of fiscal rule in its FY 2023 “Blueprint to Save America.” And to top this off, the Federal Reserve should follow a monetary rule so that the costly discretion stops creating booms and busts.  Bottom Line: My expectation is that stagflation will continue along with the a deeper recession this year given the “zombie economy” and the unraveling of the banking sector which will hit main street. Instead of passing massive spending bills, the path forward should include pro-growth policies that get government out of the way rather than the progressive policies of more spending, regulating, and taxing. The time is now for limited government with sound fiscal and monetary policy that provides more opportunities for people to work and have more paths out of poverty.

Recommendations:

Key Point: Louisiana’s labor market looks okay on the surface, but weaknesses remain because of poor policies which hinder economic opportunity across the state. There’s need for a comeback agenda. Louisiana’s Labor Market: The table below shows Louisiana’s labor market over time until the latest data for February 2023 from the U.S. Bureau of Labor Statistics.  The establishment survey shows that net total nonfarm jobs in the state increased by 2,400 jobs last month (+0.1%), bringing total jobs to 46,600 jobs below the pre-shutdown level in February 2020. Private sector employment was up by 2,500 jobs (+0.2%) and government employment declined by 100 jobs (-0.1%) last month. Compared with a year ago, total employment was up by 35,500 jobs (+1.9%), which was the 7th lowest rate in the country, with the private sector adding 31,700 jobs (+2.0%) and the government adding 3,800 jobs (+1.2%). The household survey finds that the working-age population declined by 1,181 people (-0.03%) last month, down 12,944 people (-0.4%) over the last year, and down 31,247 people (-0.9%) since February 2020. But the civilian labor force rose by 8,240 people (+0.4%) last month, 4,312 people (+0.2%) over last year, and 9,465 people (+0.5%) since February 2020. These figures result in a labor force participation rate of 59.0% which is up from 58.3% since pre-shutdown but well below the 61.2% rate in June 2009 at the trough of the Great Recession. While the unemployment rate of 3.6% is substantially lower than the 5.2% rate in February 2020, a broader look at Louisiana’s labor market shows that Louisianans still face challenges, especially compared with neighboring states based on several measures.  Economic Growth: The U.S. Bureau of Economic Analysis (BEA) recently provided the real (inflation-adjusted) gross domestic product (GDP) in Q3:2022 for Louisiana and other states.  The following table shows how U.S. and Louisiana economies performed since 2020. The steep declines were during the shutdowns in 2020 in response to the COVID-19 pandemic, which was when the labor market suffered most. The decline in real GDP annualized growth of -3% in Q2:2022 was the 5th worst and increase of +2.5% in Q3:2022 ranked 23rd in the country.  The BEA also reported that personal income in Louisiana grew at an annualized pace of +5.8% (ranked 19th) in Q2:2022 (tied +5.8% U.S. average) and of +2.5% (ranked 47th) in Q3:2022 (below +5.3% U.S. average). Bottom Line: Louisianans gained jobs in February but continue to feel the costs of restrictive policies that reduce opportunities for them to find well-paid jobs. Institutions matter to human flourishing but they are too weak in Louisiana according to the Fraser Institute’s ranking of 20th for economic freedom. And the Tax Foundation recently ranked the Pelican State as having the 12th worst business tax climate and 15th highest corporate income tax rate. The state has improved its tax code recently and lower taxes may happen soon, but excessive government spending, highly complicated personal income tax code, and poor business tax climate contribute to a net outmigration of Louisianans and a 19.6% poverty rate that ranks highest in the country. State and local policymakers should work to reverse this trend by passing pro-growth policies.  Comeback Agenda: The Pelican Institute for Public Policy recently released “Louisiana’s Comeback Agenda” to turn things around in the Pelican State by doing the following:

This Week's Economy Ep. 1: TRUTH About the Fed Raising Rates, the SVB Collapse & Inflation3/24/2023 In "This Week's Economy" Ep. 1, I debut my brief weekly podcast on the hot button economic issues related the national, state, and local economic issues and public policy that will let people prosper. Thank you for listening to the first episode of "This Week's Economy," a new series of the "Let People Prosper" podcast, where I quickly recap and share my expertise on all the economic news from the preceding week every Friday morning. You can watch this episode on YouTube or listen to it on Apple Podcast, Spotify, Google Podcast, or Anchor (please share, subscribe, like, and leave a 5-star rating). Today, I cover:

With a debt ceiling fight and bank failures, Congress’ day of reckoning to spend less is now.

Inflation is sky-high, purchasing power is sinking, 60% of Americans live paycheck to paycheck, and credit card debt is soaring to nearly $1 trillion. To make matters worse, between the fourth quarter of 2021 to the fourth quarter of 2022, U.S. real GDP grew by just 0.9%, the slowest growth in a “recovery” since at least 2009 amid the Great Recession. The more the federal budget deficit grows because of excessive government spending, the more the budget is crowded out from funding legislative priorities. In turn, Congress is forced to find ways to pay for interest on the debt, which will soon exceed $1 trillion. It’s not just the budget that’s getting crowded out; productive activity in the private sector fueled by entrepreneurs is stifled due to too much money chasing too few goods and services at the hands of tyranny imposed by big government. The underlying culprits to these economic catastrophes are reckless, weaponized government spending, often funding tyranny against Americans, and the Federal Reserve holding a bloated balance sheet. This excess national debt and money printing contributed to the latest closure of Silicon Valley Bank and will have further consequences. These government failures should be addressed by Congress spending less. This should include reducing federal funds sent to states. Not only do federal funds diminish federalism by making states dependent on the federal government but it also comes with massive red tape. The U.S. system of federalism provides a unique laboratory of competition to see what works across the states. This is best observed and encouraged by letting states be as independent as possible. Considering that federal deficits are expected to increase by an average of $2 trillion annually over the next decade, states would be wise to prepare for fewer federal funds as Congress’ purse strings will tighten. According to Congressman Chip Roy (R-TX) in a recent interview, another major way the government drives up spending is by hiding behind so-called mandatory expenditures such as Medicare and Social Security, and discretionary spending, which is funding tyranny through the weaponization of bureaucrats. “We have to commit to not funding tyranny such as the IRS going after minorities and poor people,” said Congressman Roy. “Why should we fund the FBI labeling Scott Smith, a man who stood up for his daughter being sexually assaulted to her school board, a domestic terrorist? Likewise, military funding should go toward making us a strong defense, not to ensuring that recruits ‘stay woke’ and never say ‘sir’ or ‘ma’am.’” While it’s politically popular for the government to honor its commitments like Social Security and Medicare for current retirees, mandatory spending is excessive and needs reforms to remain solvent over time. Cutting non-defense discretionary spending–including abolishing Departments of Education and Energy–to pre-Covid levels, would mean saving $3 trillion over the next decade. But both Republicans and Democrats have to work at this as they’re equally culpable of driving up spending under many administrations. And these expenditure savings need to be closer to $8 trillion to stabilize the debt to output level per the Committee for a Responsible Federal Budget. In addition to tightening up federal funds sent to states and mandatory expenses, the government should consider adopting a Responsible American Budget, similar to what’s been practiced in Texas, Florida, and Tennessee, that’s helping their economies thrive. This would require adopting some sort of fiscal rule like a spending cap, but as Congressman Roy emphasized, without passing exceptions that would render the rule irrelevant. If such a rule based on the maximum growth rate of population growth plus inflation, which represents what the average taxpayer can afford, had been in place, then we would have accrued $500 billion in new debt rather than $19 trillion over the last 20 years. Returning the federal government to its constitutional role of preserving liberty is key to economic growth. The surest way to suffocate the productive private sector from innovating and Americans from prospering is to let spending increases continue. This is the biggest threat to the American dream today, which younger generations are already counting dead as they’ve seen such poor economic growth in their lifetimes. If the future of the nation and opportunities for upcoming generations is important, the government must earn Americans’ trust by spending less, reforming mandatory programs, cutting federal bureaucracy, and promoting other pro-growth policies. As Congressman Roy shared, “I didn’t inherit a free country to pass down an unfree one. We have to fight.” Originally posted at The Daily Caller.  Louisiana’s official poverty rate of 19.6% in 2021 was the highest in the country, according to the U.S. Census Bureau. The map below by American Progress shows that higher poverty rates tend to be in the south.  There has been $25 trillion (inflation-adjusted) spent on the “War on Poverty” since it was declared in 1964 and about $1 trillion spent nationally every year, including billions of dollars in Louisiana. In fact, state and local spending per capita on public welfare in Louisiana of $2,924 ranked the 12th highest in the country in 2020.

Given so much taxpayer money has been spent on safety nets, shouldn’t there be fewer than one of every five people in poverty in the Pelican State? We believe so! This is a reason that the Pelican Institute recently released “Louisiana’s Comeback Agenda” to help struggling Louisianans find long-term self-sufficiency through a career instead of safety nets. The failures of the current government safety net system are expensive and costly. These programs should be easy for people to navigate, produce better outcomes, and empower individuals to return to the workforce. To better understand the extent to which programs are achieving these goals, lawmakers should call for routine performance audits. Performance audits dive deeper into the programs than typical financial audits by looking at not only expenditures of taxpayer money on these programs but also examining their outcomes. They provide recommendations for improving outcomes and lowering costs by identifying waste, duplication of efforts, and opportunities for consolidation or outsourcing. Routine, independent performance audits will determine whether programs effectively serve their intended purpose and hopefully make improvements if not. Fortunately, Louisiana’s Legislative Auditor’s office already does some of this. On its website, they note: “Performance Audit Services may audit any state agency, office, department, board, commission, institution, division, committee, program, or legal entity created within the legislative or executive branch of state government. The division conducts at least one performance audit of each executive branch department over a seven year period but performance audits may also result from topics of interest to the public, or requests from legislators, agencies, and other parties. Performance audits improve the transparency of state government.” And there have been some fruit from previous audits. In 2021, the Louisiana Legislative Auditor conducted a performance audit of the Louisiana Department of Children and Family Services’ administration of the Temporary Assistance for Needy Families (TANF) program in response to a request from the Louisiana Senate. The audit report revealed that “DCFS does not collect sufficient outcome information to determine the overall effectiveness of TANF-funded programs and initiatives. The current performance measures that DCFS uses to monitor and evaluate TANF programs are mostly output and process measures which are not useful in determining whether programs are effective at meeting TANF goals.” Auditors also found that “Louisiana has the lowest Work Participation Rate (WPR) in the nation at 3.5% for the federal fiscal year 2020. Under the WPR, states must engage a certain percentage of families receiving cash assistance in specific work activities, such as employment, job searches, or vocational training.” This valuable information was provided because a one-time performance audit of the TANF program was requested. Policymakers and the public would benefit from independent reviews like this on a recurring basis to identify program strengths and weaknesses and take swift action when necessary. By doing so, we can get taxpayer-provided resources to those who need them so they can find career paths out of poverty instead of being trapped living in poverty. Originally published at Pelican Institute. In today's episode of the "Let People Prosper" podcast, which was recorded on February 24, 2023, I'm joined by Dr. Vincent Geloso, who shares his insights on:

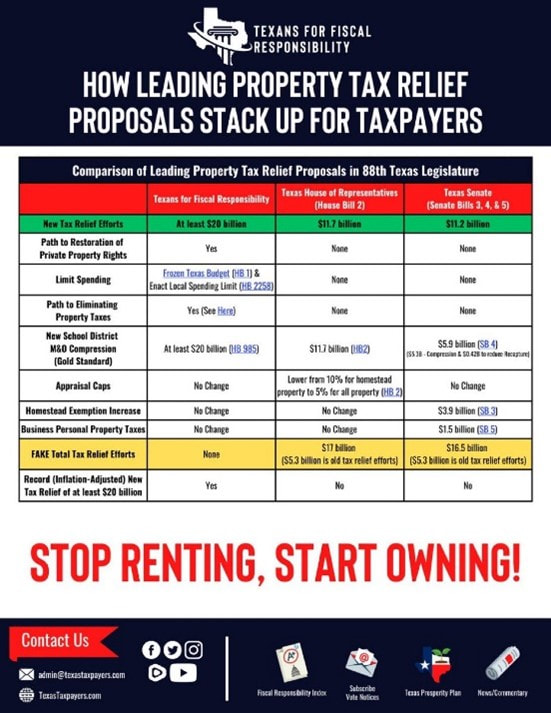

Dr. Geloso’s and other info (here):

Lt. Gov. Dan Patrick, along with several senators, announced a new bill package this week designed to reduce property taxes through several different methods.

Sens. Paul Bettencourt (R-Houston), Tan Parker (R-Flower Mound), Bob Hall (R-Rockwall), Joan Huffman (R-Houston), and Charles Perry (R-Lubbock) joined Patrick in a press conference on March 14. The package included three bills that would offer a combined estimated $16.5 billion in property tax relief. Lt. Gov. Patrick opened the press conference and invited Sen. Bettencourt to walk through the proposals, saying, “No one knows more about property taxes.” “What we have is tremendously good news for Texas taxpayers today,” Bettencourt said. “It’s important to know that we’re touching every taxpayer, every homeowner, every business owner, with needed tax relief,” Bettencourt claimed. “We’re spending the money as wisely as we can to get the maximum tax relief possible — and this plan has eye-popping numbers.” Senate Bill 3, filed by Bettencourt, would increase the homestead exemption for property taxes from $40,000 to $70,000 and allow seniors to deduct an additional $30,000. Bettencourt claimed the increases would save homeowners $800 to $1,000 over the course of the next two years. Bettencourt was also responsible for SB 4, which would contribute another $5.38 billion to buy down or “compress” school district property taxes, as explained in the bill analysis. The final bill in the property tax reduction package was SB 5, filed by Parker. The proposal would increase the “business personal property exemption from a $2,500 de minimis exemption to a $25,000 universal exemption.” Additionally, Parker’s bill would “provide eligible taxable entities a credit equal to 20% of the amount of ad valorem taxes paid during the period on which the report is based.” In the press conference, Parker claimed the bill would deliver $1.5 billion of relief to business owners. All of these measures were included in Lt. Gov. Patrick’s legislative priorities, as reported by The Dallas Express. Several of the property tax reduction measures have already garnered bipartisan support in the Senate. “We’ve never had $16.5 billion dollars to throw at property tax relief, and that is a record number, and it is well spent, and I believe it will be well received by the citizens and taxpayers of the great state of Texas,” noted Bettencourt. Patrick also explained, “The real key to save Texans’ taxes is to limit the size of government. That’s the key.” However, the proposals have disappointed some economic policy experts and taxpayer advocacy groups, who had hoped for different approaches to the tax burden. Vance Ginn, the president of Ginn Economic Consulting, directed The Dallas Express to a statement where he claimed, “[T]he Senate’s overly-complicated property tax package (#SB4, #SB4, #SB5) of $16.5B won’t put any property taxes on a path to elimination so Texans will continue to not have their right to own property.” Instead, Ginn urged that Texas needs to “[s]pend less and use surpluses to reduce school M&O [maintenance and operations] property taxes by state and other property taxes by local [governments] until all are ZERO so Texans can finally have the right to own their property and ultimately stop renting and start owning.” Similarly, Noah Betz, the executive director at the Huffines Liberty Foundation, explained to The Dallas Express, “We strongly believe this package falls short of being real property tax relief.” A statement from former Texas Senator Don Huffines added that “[a] major shortcoming of the Senate bills is that they do nothing to limit future increases in rates and levies by local governments, including school districts.” Tim Hardin, the president of Texans for Fiscal Responsibility, told The Dallas Express, “although we support any property tax relief we do not feel as though the Senate package goes far enough. … We would like to see property taxes be put on a path towards elimination.” Originally published at Dallas Express.  Louisiana is one of the most federally dependent states in the country, ranking 10th in a recent analysis.

The personal finance website WalletHub released a report Wednesday that ranked states’ dependency on the federal government based on three metrics: return on taxes paid to the federal government, share of federal jobs, and federal funding as a share of state revenue. The study ranked Louisiana in 10th overall with a score of 57.46, though the state government’s dependency ranked third. Residents’ dependency was ranked 22nd. Vance Ginn, chief economist at the Pelican Institute, told The Center Square much of Louisiana’s dependency derives from the state’s high poverty rate — 19.6% in 2022 — and the federal funds from various programs that flow into the state as a result. Forty-four percent of all state funding in Louisiana comes from Congress, and the Pelican Institute is working on “finding ways for Louisiana to have a comeback” that boosts businesses and employment, which in turn reduces poverty. “Louisiana is overly dependent on the federal government and the way to reduce that depends on getting more Louisianans back to work,” he said. “The way to get people back to work is removing barriers in the private sector, restraining government spending, providing tax relief, and reducing regulations.” The WalletHub analysis shows only state governments in Alaska and Wyoming receive more funding as a share of state revenues than Louisiana. Neighboring Mississippi ranked third overall in the study, while Arkansas was ranked 28th and Texas 29th. Other states in the top 10 most dependent on federal funding include Alaska in first, followed by West Virginia, Mississippi, Kentucky, New Mexico, Wyoming, South Carolina, Arizona, and Montana. New Jersey was ranked as the least dependent state, followed by Washington, Utah, Kansas, Illinois, California, Massachusetts, Iowa, Delaware, Nevada, and Colorado. The analysis also derived an average ranking for red and blue states, based on how residents voted in the 2020 presidential election. Democratic states produced an average ranking of 30.68, compared to the average ranking of 20.32 in Republican states, suggesting Republican states are generally more dependent than Democratic states. The study also examined how tax rates factor into the equation. Louisiana fell into the “high dependency, low tax” category, with a tax rate that’s ranked 25th in the country. Other analysis compared gross domestic product per capita compared to dependency on the federal government, and WalletHub placed Louisiana in the “high dependency, low GDP” category with a GDP per capita ranking of 40th. Originally published at The Center Square. On today's episode of the "Let People Prosper" show, which was recorded on March 6, 2023, I'm honored to be joined by Dr. Arthur Laffer, legendary economist and 2019 recipient of the Presidential Medal of Freedom. We discuss:

Dr. Arthur Laffer’s bio and other info (here):

It was a pleasure to help write this report with the Pelican Institute for Public Policy! Check it out. Today, the Pelican Institute for Public Policy released “Louisiana’s Comeback Agenda,” a bold vision for policy change in Louisiana and a statewide campaign to support the effort. The agenda is intended to serve as a guide for lawmakers, candidates, and community leaders to spark discussion and debate toward proven policies to bring jobs and opportunity to Louisiana. “Poor public policy decisions have caused Louisiana families to suffer for too long, and yet our southern neighbors like Texas, Florida, Tennessee, and North Carolina are thriving,” said Daniel Erspamer, CEO of the Pelican Institute. “Given our unmatched natural resources and cultural assets, Louisiana should be an economic powerhouse, and with the right policy decisions moving forward, it can be.” Louisiana’s Comeback Agenda focuses on six priority policy areas, outlining specific problems and offering specific solutions:

The plan was released just before the gubernatorial forum at the Pelican Institute’s annual Solutions Summit, where candidates were asked questions that dealt with the policy issues outlined in the plan. “We’ve spent months focused on finding real solutions to correct Louisiana’s poor decisions of the past and create increased opportunity for Louisiana’s people going forward,” said Erin Bendily, Vice President for Policy and Strategy at the Pelican Institute. “We’ve reviewed research, examined what other states are doing, and identified where our state can be more competitive. This agenda is the result of that work. We hope that this will help shape the policy discussions in Louisiana in the upcoming legislative session and as voters make important decisions about our state’s leadership and future this fall.” The agenda is the policy centerpiece of a major campaign that aims to bring transformational policy change to the Pelican State. The policy recommendations will be supported by a statewide speaking tour, an ambitious advertising campaign, grassroots activation and education, and legislative engagement and advocacy. “Ultimately, we want Louisiana to flourish, and the policy solutions in the Comeback Agenda are how we will get there,” said Erspamer. “The courage to make these crucial changes will require leadership, bold action, and a groundswell of support from every corner of Louisiana. Working together, we can write the next chapter of Louisiana’s story.” You can read the full paper here. Originally published here.

David is joined by former Trump-era OMB economist, Dr. Vance Ginn, to discuss the history of economic thought; the strengths and weaknesses of the classical, Chicago, and Austrian schools of thought; whether or not we need a Fed; and what to do about excess debt and economic growth. Yes, it is a busy hour, but one you will not want to miss!

Iowa’s fiscal foundation remains strong despite national economic uncertainty because of the state’s fiscal conservatism and prudent budgeting.

Governor Kim Reynolds has made Iowa a leader in conservative fiscal policy. This approach has already left more money in taxpayers’ pockets, and set the state on course to implement a low, flat income tax by 2026. In its Fiscal Policy Report Card on America’s Governors for 2022, the Cato Institute “grades governors on their fiscal policies from a limited-government perspective.” On this basis, Cato ranked Governor Reynolds as the best in the nation, writing that she “has been a lean budgeter and dedicated tax reformer since entering into office in 2017.” Last year, Governor Reynolds and the Iowa legislature continued to place a priority on prudent budgeting. The $8.2 billion budget for fiscal year 2023 represented a mere 1 percent increase from the prior year. And for FY 2024, Reynolds has proposed an $8.5 billion budget, with the extra funds meant to cover the universal school-choice plan that the legislature recently passed. Iowa’s anticipated $1.6 billion budget surplus for FY 2023 is nearly as much as the $1.9 billion surplus recorded in FY22, with another $2.2 billion surplus expected in FY 2024. The state should have $895.2 million in reserve funds in FY 2023 and $962.5 million in FY 2024 — the statutory maximum for those years. The state’s Taxpayer Relief Fund — the fund into which excess tax revenue is placed so that it can be returned to taxpayers by the legislature — was worth $1.1 billion in FY 2022, and is on track to grow to $2.7 billion in FY 2023 and then to $3.4 billion in FY 2024. In 2022, Iowa also enacted the most comprehensive income-tax-reform package in the nation. Over four years, the nine-bracket income tax will transform into a flat income tax with a 3.9 percent rate. The corporate tax has also already been reduced from 9.8 percent to 8.4 percent, and is set to gradually shrink until it reaches a flat 5.5 percent rate. These measures constitute a sound, pro-growth tax policy that will create incentives to work, save, and invest, and will make Iowa’s economy more competitive on the national stage. Prudent budgeting is essential for ensuring that these income-tax cuts can be responsibly implemented. And on Governor Reynolds’ watch, Iowa’s tax revenues continue to grow, reducing the degree to which the tax cuts must be “paid for” through spending cuts. The most recent numbers, released in February, showed that revenues are at $35.9 million, or 5.7 percent higher than they were at the same time last fiscal year. That said, in addition to proposing a fiscally prudent FY 2024 budget, Governor Reynolds is also proposing to rein in Iowa’s administrative state. It has been 40 years since Iowa made any major reforms to state government, and in that time the size and scope of government have increased. Reynolds is proposing to streamline the executive branch and reverse some of that growth. Currently, Iowa has 37 cabinet agencies. The governor’s proposal calls for a 16-agency cabinet. She argues that government is both too big and too expensive, and streamlining it will result in more efficiency and better services for taxpayers. She estimates that if enacted, this consolidation plan would save taxpayers over $214 million in the next four years. Although Governor Reynolds and the legislature have placed a priority on prudent budgeting, there is more that could be done. Iowa statute currently allows legislators to spend up to 99 percent of projected tax revenues. This rule should be replaced with one that would limit most spending to the rate of population growth plus inflation, which could have saved Iowans as much as $2.9 billion — or $3,700 for the average family of four — in taxes had it been in place since 2013. Meanwhile, Governor Reynolds has already signaled that she does not want to stop at a flat income-tax rate of 3.9 percent. She has said she aims to lower the rate to a flat 2 percent, and to eventually eliminate the tax altogether while continuing to cut state-government spending. Governor Reynolds should be applauded for putting Iowa on the path to a robust economy, and providing a model of sound fiscal policy for the federal government and other states to emulate. Now, she just has to keep at it, because there is more work still to be done. Originally published at National Review Online.  Despite the on-going, sky high, Biden-flation, American's are spending like crazy. And it's a little bit puzzling. But then again, it really isn't, because we want what we want when we want it, and we want it now!

"But that is gonna start to come to a halt very quickly, as inflation continues to take a bite out of their consumption habits" said Dr. Vance Ginn, president of Ginn economic consulting, "And part of the spending numbers that we see are really just from inflation. If you adjust a lot of these for inflation, we're actually seeing declining retail sales." The other reality is, too many Americans are charging up their credit cards, and living beyond their means. "A lot of people are also racking up a lot on their credit cards" Dr. Ginn told KTRH, "Credit card debt is up to a record high of over a trillion dollars across the economy, and we've seen that soar just over the last year." And looking ahead to this year, the clock will eventually strike midnight, and the U.S. will officially be in another recession. Originally posted at KTRH News. In today's episode of the "Let People Prosper" podcast, which was recorded on February 27, 2023, I'm joined by Randan Steinhauser, who shared her insights on School Choice, including:

Randan Steinhauser’s bio and other info (here):

On a stifling July day, Elon Musk sat across from the governor of Oklahoma under a small white pop-up tent, a red Tesla flag waving from a short pole in an otherwise unadorned field.

That the billionaire was even in Oklahoma, seriously considering putting a gigantic new Tesla factory outside of Tulsa, was a major turning point for the frequently overlooked state. Suddenly, Oklahoma could boast of being on par with its much larger neighbor and rival, Texas. The only other city still in the running for the plant, by that point in 2020, was Austin. The wide shadow of Texas has long fallen over Oklahoma. Despite offering the same red-state promise of open land, a cowboy ethos and limited government regulations, Oklahoma has found itself a perennial also-ran, especially in recent decades as Texas cities became magnets for new companies and workers from around the country. In the end, Mr. Musk chose Austin. But the long-shot bid put Oklahoma on the map for relocating companies and workers, and inspired a new resolve to make the state a more appealing place to work and live. Since 2018, Tulsa has been offering remote workers $10,000 to move to the city for at least a year. In its first year, 70 people took the city up on the offer. In 2021, 950 people made the move. Many stayed. “I can’t believe I live in Oklahoma — it’s like even weird to say,” said Chris Bland, who took the $10,000 and moved in 2021 from an apartment in Harlem, working remotely as an environmental scientist at New York’s Mount Sinai Health System. Since then, Mr. Bland, 29, has been selling his friends and family on Tulsa — restaurants, bars, $895 a month for a studio apartment downtown — and he has already stayed longer than the single year required by the program, which is funded by the Tulsa-based George Kaiser Family Foundation. Oklahoma City has taken a different tack, raising money from residents and visitors — in the form of a dedicated 1 percent sales tax — and spending hundreds of millions of dollars in recent decades on things like new parks, a canal, a streetcar system and a basketball arena. The city remade its downtown, and new shops and restaurants replaced those that had long ago vanished. Many American cities have been spending to improve their downtown amenities, and other states also offer tax breaks and other incentives to try to lure businesses. But Oklahoma City is now one of the country’s fastest-growing large cities, climbing past Boston and Washington to become the 20th largest by population, with 687,000 people. Still, the state’s growth has been dwarfed by the roaring boom in Texas, which has welcomed a rush of transplants from other states and new immigrants from around the world. The Texas economy is second in the United States only to California, and it has been growing faster. But Oklahoma officials now see a chance to draft off that boom, selling their state as a place that is just as business-friendly, at a more affordable entry point. “We hope it’s the next Texas,” said Lt. Gov. Matt Pinnell of Oklahoma, sitting in a Houston seafood restaurant for a series of recent meetings to entice more international energy investment in his state. More than 100 companies have come to Oklahoma in the last five years, including 29 last year, and another 200 have announced expansions, according to the state Commerce Department, resulting in more than $10 billion in promised new investments. Six companies moved their headquarters to the state. The rivalry with Texas nonetheless remains a bit one-sided. Oklahoma has three Fortune 500 companies headquartered in the state, all in the oil and gas industry; Texas has more than 50. Asked about the threat posed by their neighbor, Texas officials did not see one. “Texas is dominating for the 18th year in a row as the Best State for Business,” Andrew Mahaleris, the press secretary to Gov. Greg Abbott, said in a statement, citing a ranking in Chief Executive magazine. “Texas will continue to remain number one because of the unmatched competitive advantages we offer: no corporate or personal income taxes, a predictable regulatory climate, and a young, growing and skilled work force.” But soaring housing prices in Austin and other Texas cities are undermining some of the state’s competitive advantage. “There are a lot of states around here that are a lot cheaper to live,” said Vance Ginn, an economist in the Trump administration and a former chief economist at the Texas Public Policy Foundation, a conservative think tank. “That is a concern.” Don Ward, a Texas native and entrepreneur, is moving his small technology business, Laundris, to Tulsa from Austin. Mr. Ward, 53, said he worried about the rapid rise of housing and other costs, and Tulsa offered some of the small-city feel that he said had been vanishing from Austin, whose population is now just under 1 million. “Austin has been more focused on working with the Elon Musks of the world,” Mr. Ward said. “Tulsa gave me an opportunity to be a big fish in a smaller pond again.” Reliable electricity is another issue Oklahoma is using as a selling point. The failure of the Texas electrical grid during a brutal winter storm in February 2021 fueled new interest in states, like Oklahoma, with energy infrastructure seen as more reliable. Gov. Kevin Stitt, a Republican, boasted in a recent interview about not only the state’s “affordable, reliable energy grid” but his effort to do away with 25 percent of the state’s regulations on businesses. Seated in his office in the Capitol, Mr. Stitt conceded that Texas has long had a reputation as a good place for business. “But it’s getting overcrowded,” he said, noting that commute times around Oklahoma City are far shorter than those in Dallas-Fort Worth. It has long been easy to drive around Oklahoma City. The problem was a lack of things to drive to. The need became apparent decades ago, when the city lost out to Indianapolis for a United Airlines maintenance center. Company executives had visited Oklahoma City and found they simply could not make their employees live there. “It was terrible,” said David Holt, 43, who grew up in Oklahoma City in the 1990s and is now in his second term as mayor. “All my peers who had any wherewithal went to Dallas or Houston or the more adventurous off to California or New York.” The city began a long process to make itself more attractive, one that continues. On a recent weekday, a billboard across from the Oklahoma City Thunder arena proclaimed “Always Onward” over a newly opened park of spindly young trees. (The state, for its part, has been trying a different tagline: “Imagine That.”) The city has also been transforming politically. Once reliably red, Oklahoma City is now solidly purple, having narrowly favored former President Donald J. Trump in 2020 but voting by a wide margin for the losing Democratic candidate for governor last year. Governor Stitt, a businessman and political newcomer when first elected in 2018, said that he did not worry that efforts to attract newcomers to the state’s urban centers would alter its political identity. “We’re finding people moving here from the quote unquote liberal states because of their policies,” he said, adding that he and other state leaders were clear about their conservative principles. “It’s not for everybody. If this is not who you are, great, you don’t have to live in our state.” Tulsa has similarly been shifting politically, and in its attitude about itself, said Mayor G.T. Bynum, also a Republican in a nonpartisan office. He said the amount of investment in the city was akin to the 1920s oil boom and, because of Tesla’s interest, the city was hearing from other electric vehicle and battery companies. “Elon Musk netted us tens of thousands of dollars in free advertising,” Mr. Bynum said. Even so, by the time he visited, Mr. Musk may have already made his decision against Oklahoma, for many of the same old reasons. “The fundamental problem I have is getting people to move out of California,” Mr. Musk told the head of work force development in Oklahoma in 2020, according to documents obtained by The Associated Press. “Austin is one of the few places to which they will move.” The population of Austin has grown more than 20 percent in the last decade. But Oklahoma City has also grown by nearly that much during that time period, roughly 18 percent, a fact Mayor Holt attributes in part to his city’s ability to appeal to those seeking what Austin used to be. “We have a lot of the things that you would expect to find in a large American city, but without the hassle,” he said. “I think that’s a combination that maybe only has a finite window. It’s the combination Austin offered 20 years ago, and then everybody took them up on it, and now it’s too crowded.” Originally published at The New York Times.  The debt ceiling standoff between President Biden and the Republican-controlled US House of Representatives indicates Republicans care about government spending and deficits again, allegedly.

But history tells a different story. Since 1980, the national debt has risen substantially each year, regardless of whether the presidency, House, or Senate was red or blue. In my recent interview with financial expert David Bahnsen, he said, “[Conservatives] are losing their moral credibility…we can’t only be fiscal conservatives when there’s a Democrat in the White House.” Proving Bahnsen’s point, two-thirds of the national debt was added just since 2009: $9.3 trillion during President Obama’s eight years, $7.8 trillion over President Trump’s four years (more than half of which was added during the COVID-19 pandemic and related shutdowns), and already $3.7 trillion in President Biden’s two years, with much more to come. During the Obama and Trump terms, both Republicans or Democrats controlled Congress. Neither put the breaks on borrowing. Spending restraint is necessary. Spending less would help avoid default on the debt, and help reduce expected massive deficits. If deficits continue to accelerate, as the Congressional Budget Office projects with a current policy baseline, the Federal Reserve will, at some point, be forced to monetize this new debt at such a scale that the post-pandemic inflation will seem mild by comparison. Moreover, higher deficits and interest rates will result in higher net interest payments, which will soon surpass $1 trillion per year, thereby crowding out Congressional budgets and likely necessitate more spending, taxes, and inflation. In early 2021, inflation escalated quickly after President Biden and Democrats passed the $2 trillion American Rescue Plan Act, handing out additional, unnecessary, blanket tax rebates and ratcheting up payouts to state and local governments and wasteful programs. And then there were the other costly legislative offerings of the “infrastructure” bill: the CHIPS Act, and the (inappropriately named) Inflation Reduction Act. Then, much of this substantial new debt generated by more than $7 trillion in excessive spending since early 2020 was purchased by the Fed, more than doubling the monetary base. Burdensome regulations imposed by the Biden administration, particularly on oil and gas production, along with tax hikes, resulted in a 40-year-high inflation rate and the slowest year of economic growth during a recovery in decades. The monetary base has finally started declining – down 6.5 percent since its peak of nearly $9 trillion in April 2022–and inflation has come down slightly but remains persistently high at 6.4 percent. Despite President Biden’s claims in his recent State of the Union address, deficits under his administration have remained near historic highs. While it’s true that the deficit has declined, it remains well above $1 trillion, and the decline was from expiring pandemic relief measures. The Congressional Budget Office finds the deficit will remain elevated well above $1 trillion and “averages $2 trillion per year from 2024 to 2033.” That’s far from balancing the budget or, better yet, achieving a surplus that could reduce the national debt, a feat achieved in only 6 years since 1940 (1947, 1948, 1951, 1956, 1957, and 1969). And it hasn’t been sustained in a century, since Presidents William Harding then Calvin Coolidge effectively restrained government spending. Cutting total spending is necessary. But trimming discretionary spending alone is not enough, as that will only temporarily address America’s fiscal crisis. To get out of this national crisis, we need perpetual spending restraint, like that championed by President Coolidge, which will require key reforms to “mandatory” programs like Social Security and Medicare. While a balanced budget amendment sounds good (and would be much better than our lack of a fiscal rule at the federal level today) it would likely result in rising taxes, which would be detrimental to growth and deficit-reduction efforts. A federal spending limit tackles the ultimate burden of government: spending. This principle works at the state level in places like Texas, where the Legislature has held the budget in check over the last decade, contributing to a $32.7 billion surplus that could provide historic tax relief. Other state think tanks are weighing this responsible-budgeting approach, limiting spending to a maximum rate of population growth plus inflation. This rate is too high now, but typically provides a stable metric that reasonably accounts for the average taxpayer’s ability to pay for government spending while growing less than the economy. Instituting a federal spending limit would encourage Congress to narrow its scope to constitutional duties. This could be done with the Responsible American Budget, which has been supported by economists, politicians, and thought leaders, by limiting federal budget growth to correspond with population growth plus inflation. This approach would help remove failed programs from our lives, while allowing for more free-market capitalism to support human flourishing. Had this limit been followed over the past 20 years, the US could have added just $500 billion to the national debt on a static basis, instead of the $19 trillion we got. The more likely result would have been paying down the debt, given the dynamic effects of such a pro-growth policy. While House Republicans are trying to restrain spending for the moment, both sides of the political aisle need to encourage a bigger shift that embraces spending limits and pro-growth policies. We must cut government spending. The negotiations around raising the debt ceiling should be that opportunity to provide fiscal sanity. If not, we will have more costly consequences that Americans can’t afford. Originally published at American Institute for Economic Research. |

Vance Ginn, Ph.D.

|

RSS Feed

RSS Feed

Proudly powered by Weebly