Originally published at AIER.

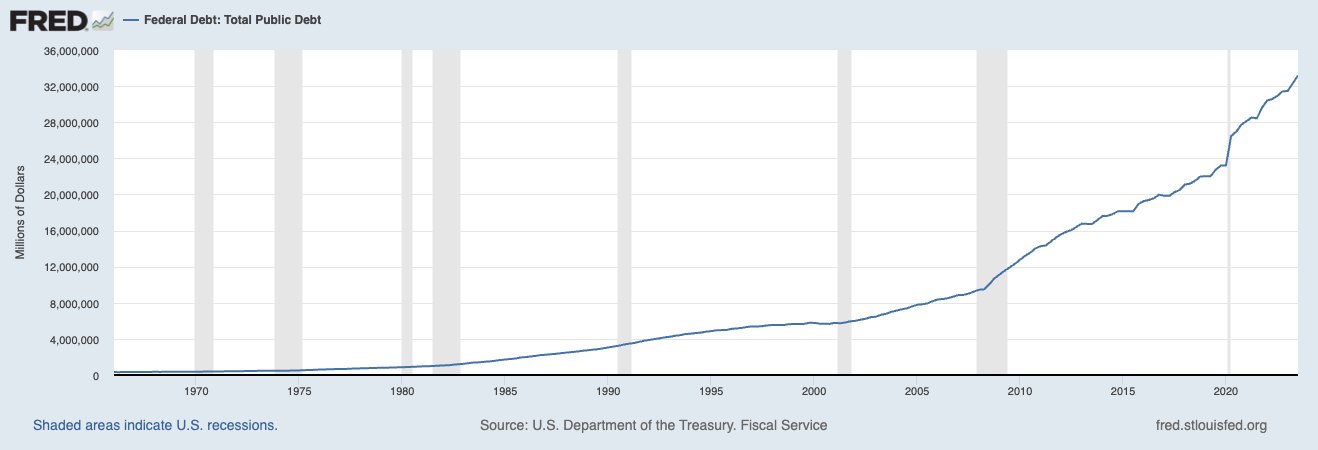

As 2025 draws near, America teeters on the brink of a fiscal abyss. This impending fiscal cliff, marked by the end of tax cut provisions and a spending crisis, calls for immediate and decisive action by Congress to avert a worse economic situation than the one Americans feel today. The national debt from excessive government spending is on track to surpass $35 trillion soon, a stark increase of nearly $10 trillion since 2020. This level of debt per citizen exceeds $100,000; per taxpayer, it is nearly $267,000. Such figures are not just numbers but represent a looming burden that future generations will bear — a burden that transcends mere fiscal policy and ventures into the realm of ethical responsibility. The gravity of this debt is exacerbated by the interest payments it necessitates, which have soared to over $1 trillion annually, surpassing what the country spends on national defense. This situation illustrates a troubling scenario where the government, to manage its debt, resorts to issuing more debt, a practice unsustainable by any standard measure of sound budgeting. The economic repercussions of this cycle of debt are profound, leading to higher interest rates, likely increased inflation, and a misallocation of resources that stifles productive private sector activity. Amidst these challenges, the Tax Cuts and Jobs Act (TCJA) provisions, set to expire in 2025, play a pivotal role. These tax cuts have been instrumental in supporting economic activity across all income brackets by reducing their tax burden. If these cuts expire, they could reverse the economic gains achieved, reducing disposable income, dampening savings and investment, and contributing to an economic downturn in an already fragile economy. The cessation of these benefits would particularly impact families who have benefited from the near doubling of the standard deduction and enhancements to the child tax credit. Furthermore, the expiration of the $10,000 cap on state and local tax (SALT) deductions could have mixed effects; while it may benefit taxpayers in primarily blue, high-tax states, it complicates the fiscal landscape significantly. A balanced approach would be to maintain the increased standard deduction while simplifying the tax code further by eliminating complex provisions like the SALT deduction and the child tax credit, promoting a flatter, more equitable tax system with one low tax rate for everyone. This would also support more economic growth that, combined with spending less, can quickly get our fiscal house in order. This fiscal predicament is further complicated by President Biden’s commitment not to raise taxes on those earning less than $400,000 annually. This promise will be difficult to keep if the TCJA provisions expire without appropriate legislative adjustments, further imperiling his dwindling reelection hopes in November. This situation and recent tariff impositions that affect all income levels would represent a double blow to American taxpayers, dampening economic prospects. As we face these fiscal upheavals, the discretionary spending caps and the debt ceiling, due to expire in 2025, add complexity to an already challenging budgetary environment. The US risks a severe budgetary crisis without thoughtful reform, particularly in the so-called “entitlement programs” like Social Security and Medicare, which consume a substantial portion of the federal budget. These areas must be addressed because both will be essentially bankrupt over the next decade, and millions of recipients will face substantial cuts in benefits. Given all these challenges, fiscal and monetary rules are paramount. Congress should implement a fiscal rule after cutting federal spending to at least the pre-lockdown level in 2019. Implementing rules like the Sustainable American Budget, which caps federal spending based on population growth plus inflation, could provide a sustainable path forward. This approach, supported by Americans for Tax Reform along with the economic insights of Alberto Alesina and John Taylor, advocates for austerity focused on spending restraint and economic growth rather than tax hikes, as some on the “new right” have recently advocated. Regarding a monetary rule, the Fed should return to a single mandate of price stability, cut its bloated balance sheet to at least the pre-lockdown level in 2019, and adopt a strict rule that ideally would be on the growth of its monetary base. These steps would help reduce persistent inflation and remove the extraordinary distortions throughout asset prices and the production process because of years of quantitative easing and low interest rates. Combining these monetary and fiscal rules would provide the necessary checks and balances to give the economy time to heal from massive government failures and help support a stronger institutional framework for economic growth and individual flourishing. Moreover, the regulatory environment has grown increasingly burdensome under the Biden administration, with an estimated $1.6 trillion in new final rules imposed since President Biden took office through May 2024. These rules have been applied across the economy, including financial decisions based on ESG factors influencing the energy sector to increase car emission standards influencing the auto sector. But these ultimately influence producers’ and consumers’ costs of many goods and services. Removing the burden on Americans would unleash economic growth, helping with the fiscal and economic headwinds. The bad policies out of DC have created a dire fiscal and economic situation moving into 2025. If the Trump tax cuts expire, excessive spending will continue unabated, and corrective monetary policy will not happen. Uncertainty and expectations alone will result in a hard landing in the economy, job losses, and elevated inflation. Given the last four years of declining purchasing power for millions of Americans, this result is unacceptable, and the idea of raising taxes to attempt to solve this is naive. Instead, the US must leverage this crisis as an opportunity for sweeping reforms. By returning to principles of fiscal responsibility and market-driven activity, America can navigate away from the fiscal abyss and toward a future of economic stability and prosperity. Though fraught with challenges, this moment offers an unparalleled chance to reshape America’s fiscal landscape, ensuring a legacy of growth and stability for future generations.

0 Comments

It's a pleasure to speak with the Texas Aggregates and Concrete Association again and enjoy the great resort here with my wife and three young kids. While aggregates and concrete may not always be in the spotlight, they are the bedrock of our infrastructure, forming the foundation upon which we build our homes, businesses, and communities.

Reflecting on my journey, I realize how essential the right direction and strong institutions are in shaping our paths. Much like the solid foundation of concrete, institutions give us the stability to build and grow. Like the economy, my life has been a series of peaks and troughs. In my younger years, I grew up in a low-income, single-mother household in South Houston as my dad had epilepsy, and they divorced when I was five years old. I went to private school from K-2 grades, public school from 3-6 grades, and home school from 7-12. Unlike many of you, I took many risks during my teenage years and began playing drums in a band called "Sindrome," living the rockstar life. But a near-fatal car accident in 2002 was my wake-up call, one of several but the one that turned me toward a brighter path. Through this experience, a month in bed with many bumps and bruises, and a lot of prayer, I found my purpose: to help others through my calling to let people prosper. We find ourselves at a pivotal point in our country and in Texas. The recent elections tell us that there is a clear call for change in the Lone Star State. The upcoming November elections will be another opportunity for the country to steer towards a path of prosperity or continue down a troubling road. As an optimist, I believe in our potential, but I also recognize our country and state's many economic, political, and cultural issues. Policy Uncertainty and Economic Volatility At the national level, we face several economic challenges. The Biden administration has been keen on infrastructure spending, which includes the $1.2 trillion Infrastructure Investment and Jobs Act. While this aims to rejuvenate our infrastructure, it also raises concerns about efficiency and the role of government in these projects, and the fact that we are running deficits higher than that per year with the national debt at nearly $35 trillion and net interest payments of $1 trillion exceeding national defense expenditures of about $860 billion. Excessive government spending, increased regulation, and interventionist policies often lead to inefficiencies and distortions in the market. Milton Friedman, my favorite economist, warned about the dangers of heavy government involvement, advocating instead for free-market solutions that empower individuals and businesses. Election years heighten policy uncertainty, which can drive economic volatility. Businesses and investors become cautious, waiting to see which policies will prevail. This hesitation can slow economic activity, affecting everything from job creation to investment in new projects. For the aggregates and concrete industry, this means potential delays in infrastructure projects and fluctuations in demand. Milton Friedman once said, "If you put the federal government in charge of the Sahara Desert, in five years, there’d be a shortage of sand." This sharp but insightful remark underscores the inefficiency that often accompanies government intervention. In his view, infrastructure projects should be managed by private entities with a direct stake in the outcome and can respond more agilely to changes and needs. Here in Texas, we are not immune to these challenges. Our state is known for its robust economy and low taxes, but we're grappling with excessive government spending and high property taxes. The Texas Comptroller's report highlights how our spending on transportation is around $10 billion annually. While infrastructure is crucial, we must be mindful of how these funds are used to ensure they generate real value for taxpayers. Weak Labor Market Amid Headlines of Strength Despite headlines showing strength, the U.S. labor market reveals underlying weaknesses. Nearly half of Americans think we are in a recession, reflecting a disconnect between reported statistics and personal experiences. Real average weekly earnings have declined by nearly 4% since January 2021, squeezing household budgets and diminishing purchasing power. The labor force participation rate remains low at 62.5%, significantly below the February 2020 level. If participation were the same as it was then, the unemployment rate would be closer to 6% rather than the reported 4% today. Texas, however, leads in job gains, which is a testament to our state's resilient economy. Yet, we must acknowledge that the 25% increase in the two-year state budget last year was excessive. This surge in spending did not provide sufficient property tax relief, which is critical for maintaining economic vitality and keeping Texas attractive for businesses and residents alike. Moreover, we must prioritize universal school choice next year to ensure educational opportunities that meet diverse needs and drive future economic growth. Election Year Volatility During election years, the stakes are even higher. Uncertainty about future policies can cause volatility in markets and economic performance. For instance, debates over infrastructure funding, environmental regulations, and tax policies can create an unstable business environment. Companies may delay or cancel projects, affecting the demand for aggregates and concrete. This uncertainty trickles down, impacting jobs, investments, and overall economic health. Aggregates and concrete are essential for the development and maintenance of our infrastructure. These materials for things like highways and homes are our physical landscape's backbone. However, it's crucial to approach their use smartly. We don't need to resort to industrial policies with high costs and trade-offs, burdening taxpayers. Instead of a top-down approach, which often fails due to bureaucratic inefficiencies, we should consider a bottom-up approach to transportation projects. This includes government projects, public-private partnerships, and private projects. A significant portion of infrastructure could be managed through private toll roads. While my ideal vision leans heavily on privatization and tax cuts, I recognize that a balanced approach is more realistic in the current environment. Public-private partnerships can bring innovation and efficiency, reducing the burden on taxpayers while still delivering essential infrastructure. Let me share an example from my work. My research finds that private toll roads can often be built faster and cheaper than public projects. Private companies are directly incentivized to minimize costs and maximize efficiency. For instance, the LBJ Express project in Dallas, a public-private partnership, was completed ahead of schedule and under budget, demonstrating the potential benefits of such collaborations. There is also a need to move to design-build for projects in Texas rather than today's more costly and time-consuming design-bid-build approach. Additionally, Texas is experiencing significant population growth, with more people moving to the state, increasing the demand for our infrastructure. The Texas Department of Transportation (TxDOT) is investing in expanding highways and improving ports to accommodate this growth. Projects like the $7.5 billion North Houston Highway Improvement Project aim to address these demands. However, we must ensure that these investments are managed efficiently and effectively. Role of Institutions and Central Planning Another key aspect is the role of institutions. Friedrich Hayek, in his book "The Road to Serfdom," cautioned against the overreach of central planning. He emphasized that central planning often leads to inefficiencies and a loss of individual freedoms. His insights are particularly relevant today as we navigate the complexities of modern infrastructure development. To truly flourish, Texas needs to embrace more free-market capitalism and resist the creeping influence of socialism in our economy. This applies to transportation and beyond. By focusing on the efficient use of resources, reducing regulatory burdens, and fostering competition, we can build a more prosperous future. The bottom-up approach not only ensures better utilization of resources but also empowers local communities to take charge of their development, aligning projects more closely with the actual needs and priorities of the people. Consider the example of toll roads in other states. Using private toll roads in Virginia has significantly improved traffic flow and reduced congestion in previously bottleneck areas. This model can be replicated in Texas, where traffic congestion is growing, especially in urban areas. By allowing private companies to manage and maintain these roads, we can ensure they are kept in optimal condition without continuously draining public funds. Furthermore, private toll roads can be a source of innovation. Companies can introduce advanced technologies for traffic management and toll collection, making the entire system more efficient. For example, using electronic toll collection systems in Florida has greatly reduced vehicles' time at toll booths, enhancing the overall travel experience. However, this doesn't mean we should eliminate public involvement in infrastructure projects. There are instances where government intervention is necessary, especially in projects that may not be immediately profitable but are crucial for public access and economic activity. This is where public-private partnerships come into play, allowing us to leverage the strengths of both sectors. The government should act as a facilitator rather than a direct manager of projects. By setting clear regulations and standards, it can ensure that private companies operate fairly and efficiently while also protecting the interests of the public. This approach can help us avoid the pitfalls of excessive government control while still reaping the benefits of private sector efficiency. Paul Krugman and other progressives might argue that significant government intervention is necessary to address market failures and ensure equitable outcomes. They believe that without government oversight, critical infrastructure could suffer from underinvestment, and social inequalities could worsen. While these points are worth considering, history has shown us that excessive government control often leads to inefficiencies, higher costs, and reduced innovation. Learning from Failures and Future Outlook My journey from poverty to rockstar to entrepreneurial economist taught me the value of strong institutions and the importance of aligning personal purpose with societal needs. This principle applies to our infrastructure as well. Just as a solid foundation is critical for a stable building, a robust institutional framework is essential for a thriving economy. We must ensure that our policies and investments in infrastructure reflect this understanding. As we look toward the future, we must remain vigilant against the encroachment of socialist policies that threaten to undermine the free-market principles that have made Texas a beacon of prosperity. Instead, we should champion policies that promote individual liberty, economic freedom, and responsible stewardship of resources. Failure provides us with valuable lessons, and too often, people want to mitigate this by expanding government intervention, which can be detrimental to our learning and growth. We are at a critical juncture in our state's history. The recent elections have shown us that Texans are ready for a change. The upcoming November elections present another opportunity to reaffirm our commitment to the principles that have made Texas great. While I am optimistic about our future, we must address the economic, political, and cultural challenges that threaten our way of life. Election Year Volatility and Policy Uncertainty One of the most pressing issues is the rise of big government. Across the political spectrum, there is a growing tendency to rely on government intervention to solve problems. This trend is particularly concerning in Texas, where we have traditionally prided ourselves on independence and self-reliance. Many of you might be demanding the government give you handouts or reap the benefits of federal, state, or local spending, but all this comes from taxpayers' pockets. We must try a different approach. Election year volatility adds another layer of complexity. Businesses and investors are left guessing about the future as policies swing with the political tide. This uncertainty can stall projects, delay investments, and increase costs. The aggregates and concrete industry, heavily reliant on long-term planning and stability, feels these effects acutely. Conclusion In conclusion, aggregates and concrete are vital for Texas's growth, but their smart use is paramount. Let's leverage the strengths of the free market, prioritize efficiency, and ensure that our infrastructure investments truly benefit Texans. As we progress, I am eager to collaborate with any of you on projects aligning with these principles. Together, we can build a stronger, more prosperous Texas. For those interested in further discussions on economic policy and free-market solutions, I invite you to check out my podcast, the Let People Prosper Show on all major platforms, and my Substack newsletter at vanceginn.substack.com, where I delve into these topics in greater detail. You can also visit my website, VanceGinn.com, for more information and resources. Thank you for your time and attention. Let's work together to build a future where smart infrastructure investment and strong institutions pave the way for a prosperous Texas.  Originally published at Texans for Fiscal Responsibility.

Unlocking Prosperity: Steering America Back to Free-Market Fundamentals As the latest economic indicators from April 2024 unfold, it’s becoming alarmingly clear that America’s path to prosperity is at a critical juncture. A steadfast return to free-market capitalism with limited government is not just a choice but an urgent necessity. In the face of fluctuating, weakening economic conditions, a pivot towards policies that promote market-driven growth rather than big-government socialism is imperative. This shift is crucial to counteract the current trend of governmental overreach, which is stifling innovation, profitability, and efficiency. April’s labor market update provided a mixed bag of results. While an increase of 175,000 in nonfarm payroll employment was reported, the government added 8,000 jobs, bringing the increase to 618,000 (+2.7%) over the last year. This underscores a continuing trend of government expansion faster than the productive private sector by 2.2 million or by just 1.6%. Furthermore, the household employment figures tell a concerning story of a stagnant labor force participation rate of 62.7%. This stagnation indicates that a large part of the potential workforce remains on the sidelines, artificially lowering the unemployment rate and obscuring deeper systemic issues. The latest GDP data for Q1 2024 revealed a growth rate of just 1.6% on an annualized basis, indicating that the economic recovery is still on shaky ground. When government spending was excluded, real private sector growth was even more lackluster at 1.4%. There is a critical need for genuine market-driven growth rather than relying on fiscal or monetary ‘stimulus’ that fails to ignite real economic dynamism. It’s a clear call for a return to free-market capitalism. Inflation continues to erode the economic landscape, with the Consumer Price Index rising by 3.5% year-over-year for April. This persistent inflation is coupled with a troubling decline in inflation-adjusted average weekly earnings, which have fallen by a large 4.4% since January 2021, when Biden took office. This decline in purchasing power strains American households, making the case for immediate inflation control measures more compelling than ever. The regulatory environment under the current administration has also become a significant burden. An estimated $1.6 trillion in new regulations have been added since President Biden took office, further hindering economic activity. This increase across various sectors, including banking and anti-trust enforcement by the Federal Trade Commission, Federal Deposit Insurance Corporation, Federal Reserve, and Consumer Financial Protection Bureau, has introduced considerable uncertainty and constrained economic vitality. The nation’s fiscal situation is also a growing concern, with the Monthly Treasury Statement for April 2024 showing significant budget deficits that continue to burden future generations. Coupled with the Federal Reserve’s latest meeting minutes, which reveal ongoing concerns about inflation and economic stability, and the size of the bloated Federal Reserve’s balance sheet, it’s clear that fiscal and monetary policies are distorting and destroying sustainable growth. The U.S. must champion policies that reduce government intervention to navigate these turbulent waters. This involves cutting government spending, easing regulatory burdens, and reforming and simplifying taxes to foster economic growth and innovation. Adopting a fiscal rule such as Americans for Tax Reform’s Sustainable Budget Project and advocating for a monetary policy rule that curtails the Federal Reserve’s market interventions would help pave the way for a more stable and prosperous economic future. The time is ripe for America to recommit to the principles that have historically underpinned its economic success: trust in market mechanisms, empowerment of individuals, and a significant reduction in government’s coercive roles. By advocating for a return to these fundamentals, we can ensure that the economy not only recovers but also thrives in a manner that benefits the broadest swath of society. As we look forward, let’s rally behind policies repeatedly proven to be the bedrock of prosperous, resilient economies.  Listen to the interview with Sean Hannity here.

Vance Ginn, former Chief Economist for the OMB, currently founder and president of Ginn Economic Consulting and host of the Let People Prosper Podcast and EJ Antoni, a Public Finance Economist at the Heritage Foundation, discuss Biden’s dismal economy. Just yesterday while speaking in Wisconsin, Biden did everything he could to convince the audience that things are actually going really well. My Path from Rockstar to Entrepreneur Economist with John Hendrickson | Let People Prosper Bonus Ep5/8/2024 Check out this bonus episode of the Let People Prosper Show. My good friend, John Hendrickson of Iowans for Tax Relief Foundation, who has been a previous guest on my show, interviews me for one of his graduate courses about my role as an entrepreneur. We had a great discussion about how I got to where I am today, my faith, and the failures that have led to my success as an entrepreneur.

I hope you’ll watch it as I share my testimony and insights as a rockstar to an economist. Don’t forget to subscribe and share it. The document below is the syllabus for a course that I teach on free-market economics and the importance of institutions. Please provide feedback. Thanks! Originally published at Texans for Fiscal Responsibility.

Navigating Economic Challenges: A Call for Pro-Growth Policies in America As we navigate the complexities of the U.S. economy, the recent data from March 2024 underscores a pivotal truth: we must return to free-market principles that foster abundant prosperity. Amidst current economic fluctuations, it’s crucial that American policy strongly pivots towards nurturing a market-driven economy. With its potential for innovation and efficiency, this approach challenges the status quo of governmental overreach and champions policies that propel, rather than impede, prosperity. This is a beacon of hope for a brighter economic future. Labor Market Dynamics: A Complex Outlook The labor market presents a complex picture. The latest data from March 2024 reveals an increase of 303,000 net nonfarm jobs, a significant portion of which 71,000 were in the government sector. This disproportionate job creation in the government sector, particularly in healthcare and education, is a cause for concern as it hampers productive private-sector activity, thereby impeding economic growth. Adding to the complexity of the labor market, household employment has seen a decline in four of the last six months, resulting in a net decrease of 84,000 jobs over that period. Despite the low unemployment rate of about 3.5%, the labor force participation rate remains subdued at 62.7%. This is a clear indication that many individuals are still not part of the labor force, artificially keeping the unemployment rate low and masking deeper economic issues. Moreover, part-time employment increased by 600,000 last month while full-time employment declined by 100,000, continuing an ongoing trend. These labor market data signal weaknesses, even as the headlines claim they are strong. Economic Growth and Inflationary Pressures Real GDP growth for the first quarter of 2024 was well below expectations at just a 1.6% annualized growth rate. When excluding government expenditures, the real private sector growth was a mere 1.4%, revealing the fragility of an economy buoyed by flawed government actions. This tepid growth underscores the limited effectiveness of fiscal “stimulus” absent of genuine market-driven expansions. Inflation continues as a significant concern, with the Consumer Price Index (CPI) for March 2024 rising by 3.5% year-over-year. This increase, alongside real average hourly earnings declining by about 4% since January 2021, exacerbates the economic pressures on American households. This situation advances the urgency for pro-growth policies to support sustainable economic growth. Charting a Pro-Growth Path for America The persistent high inflation suggests that this issue will likely endure longer than many anticipate. The Federal Reserve’s slow pace in reducing its bloated balance sheet implies that interest rates will remain elevated for an extended period, contributing to slower growth and stagflation until the bubble bursts and the recession hits. To effectively address these challenges, it is essential to advocate for reduced government spending, fewer regulations, and lower taxes. Implementing stringent monetary guidelines and adopting fiscal policies that align spending with economic benchmarks, such as population growth and inflation, would significantly stabilize and potentially reduce the national debt burden. The U.S. needs a fiscal rule like the Responsible American Budget (RAB) to control this fiscal and monetary crisis. This was recently released as part of Americans for Tax Reform’s Sustainable Budget Project and the Republican Study Committee’s Budget, highlighting this approach’s federal, state, and local benefits. If Congress had followed this approach from 2004 to 2023, instead of a $20.2 trillion national debt increase, it could have increased by just $700 billion for a $19.5 trillion improvement for taxpayers. To top this off, the Federal Reserve should follow a monetary rule so that the costly discretion stops creating booms and busts. Conclusion The current economic situation demands a firm shift towards policies that remove government intervention and support more economic growth. These strategies represent policy imperatives and moral obligations, unlocking the potential of the American economy and ensuring a prosperous future. Aligning policies with economic realities is crucial for fostering sustainable growth and prosperity, creating an environment where businesses can thrive, and individuals find more avenues out of poverty. By reducing the role of government and giving more space to the entrepreneurial spirit, we can ensure that our economy not only grows but does so in a way that benefits the broadest number of people. Let’s advocate for a return to policies that have proven time and again to be the bedrock of prosperous societies: those that trust the market, empower individuals, and reduce the coercive role of politicians and bureaucrats in economic affairs. Today, I am joined by David Bahnsen, founder, managing partner, and chief investment officer of The Bahnsen Group and author of his latest book, Full-Time Work and the Meaning of Life.

David provides valuable insights on these issues and more on the following: How does full-time work provide meaning in life? What does the Bible say about work and a free and virtuous society? How does the government create barriers to work, and how should we remove them? Please like this video, subscribe to the channel, share it on social media, and rate and review it. I would appreciate it if you would subscribe to my Substack newsletter so you’ll receive my episodes, show notes, and other valuable insights in your inbox twice weekly at https://vanceginn.substack.com/. You can also find this information and more at https://vanceginn.com/ . Originally published at Texans for Fiscal Responsibility. Highlights

Figure 1: Real Average Weekly Earnings Remain Down 4.2% Since January 2021  Source: Fed FRED Labor Market The Bureau of Labor Statistics recently released its U.S. jobs report for February 2024, which was another mixed report with some strengths but many weaknesses.

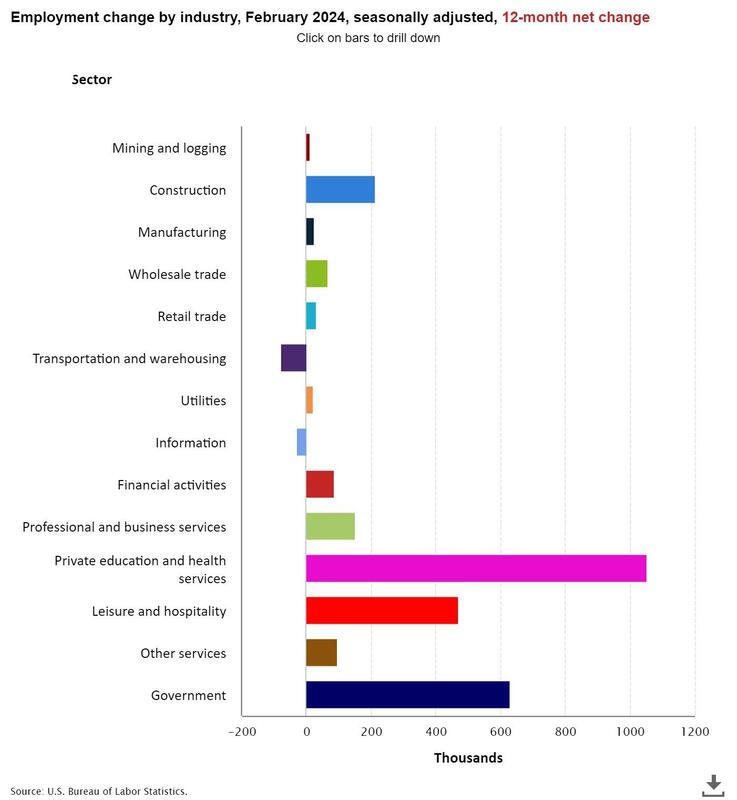

Figure 2. Changes in Employment by Industry Over the Last Year  Source: Fed FRED

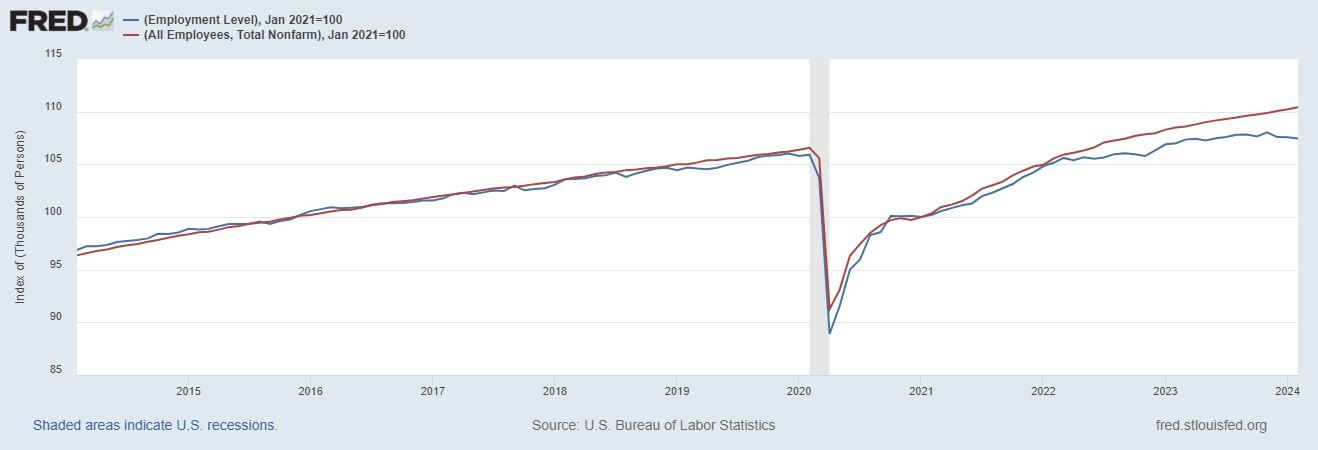

Figure 3. Establishment Nonfarm Jobs Far Outpace Household Employment Level Since March 2022  Source: Fed FRED

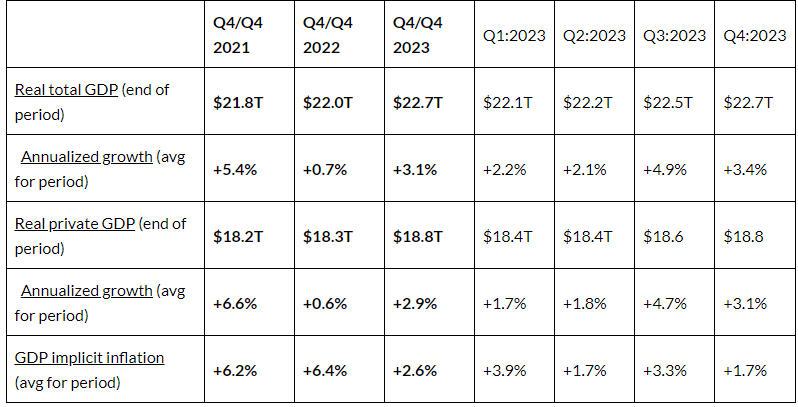

Economic Growth The U.S. Bureau of Economic Analysis recently released the third estimate for economic output in the fourth quarter of 2023.

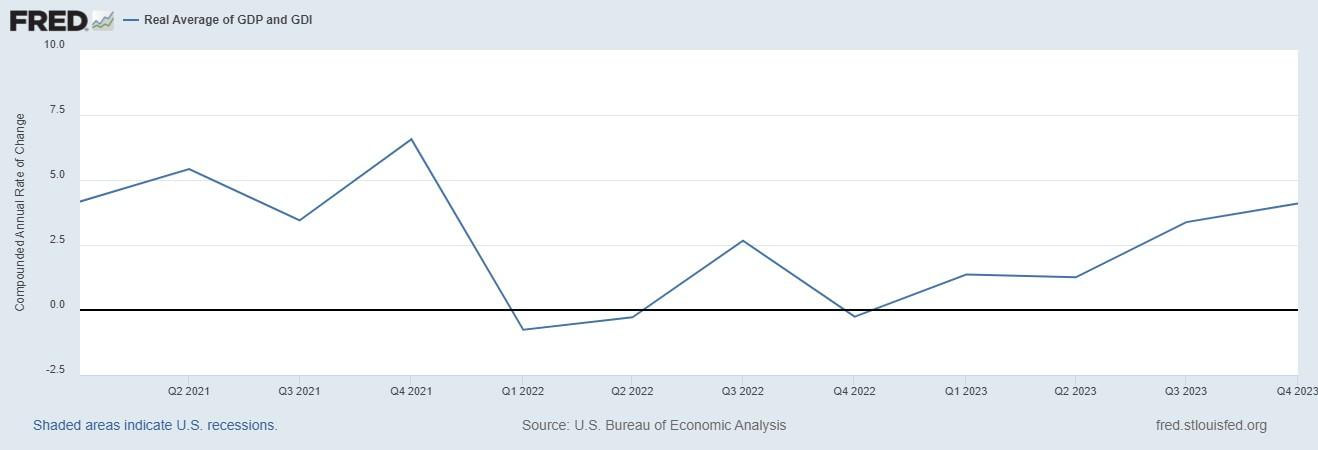

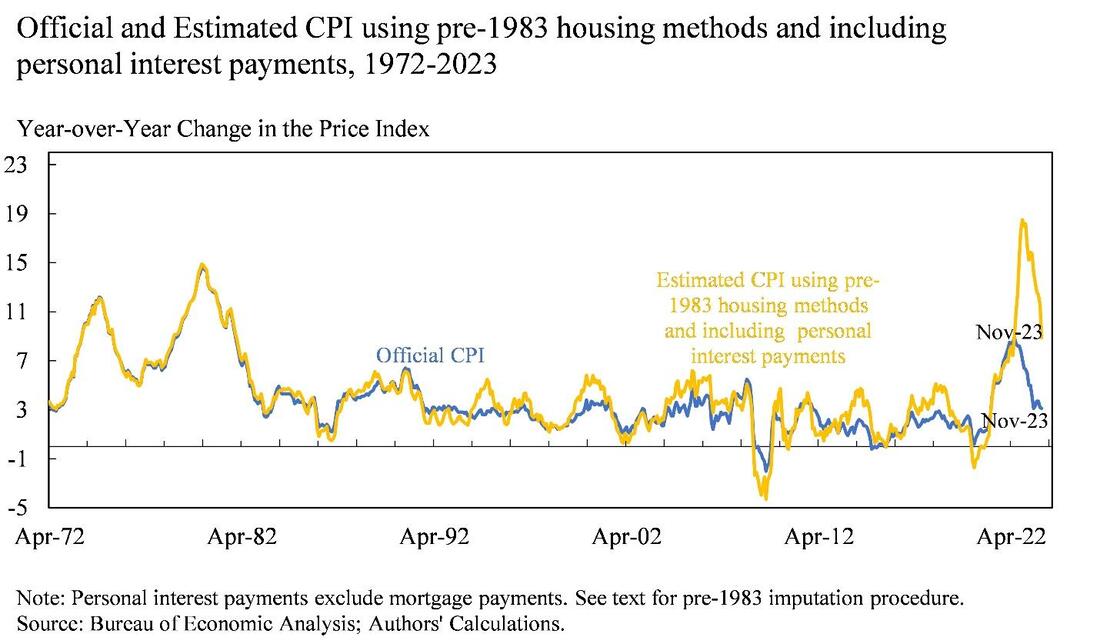

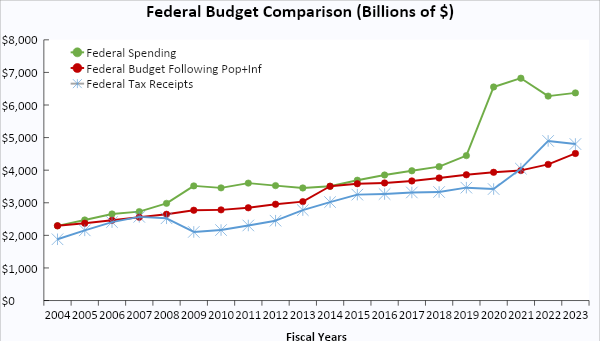

Table 1: Economic Output, Growth, and Inflation  Another key measure of economic activity is the real average of GDP and GDI, which accounts for domestic production and income and is known as real gross domestic output. Real GDO in the third quarter increased by 3.4%, and in the fourth quarter increased by 4.1% to $22.5 trillion. Figure 4 shows how this measure has declined on an annualized basis in three of the last eight quarters, increasing this value by only 2.9% since the fourth quarter of 2021 before the two consecutive quarters of declines in the first and second quarters of 2022. Figure 4. Annualized Real Gross Domestic Output Growth  Meanwhile, the federal budget deficit continues unabated because of overspending and declining tax collections from a weaker economy. The national debt has ballooned to $34.6 trillion, and net interest payments on the debt will soon be a top federal expenditure, rising to above $1 trillion. The Federal Reserve has monetized, or printed, much of the new Treasury debt to keep interest rates artificially lower than where the market would suggest. The Fed will need to cut its balance sheet (total assets over time) more aggressively if it is to stop manipulating markets (see this for types of assets on its balance sheet) and persistently tame inflation. The current annual inflation rate of the consumer price index (CPI) has been moderating since a peak of 9.1% in June 2022 but remains elevated at 3.2% in February 2024. Compared with the Fed’s average inflation rate target of 2%, which really should be 0%, the current CPI inflation rate is too high, as are other key measures of inflation. A recent paper by Larry Summers, who was the 71st Secretary of the Treasury for President Clinton and Director of the National Economic Council for President Obama, and co-authors notes that if the calculation of CPI kept housing calculation methods and personal interest payments in, then the latest peak in inflation would have been 18% instead of 8.1%. Figure 5 shows their chart with these data that also highlights how the method-adjusted inflation would be closer to 10% instead of the reported 3.1%. Figure 5. CPI Inflation Differences When Methods Are Similar Over Time  Just as inflation is always and everywhere a monetary phenomenon, deficits and high taxes are always and everywhere a spending problem. David Boaz at Cato Institute has noted how this problem is caused by both Republicans and Democrats. To control this fiscal and monetary crisis, the U.S. needs a fiscal rule like the Responsible American Budget (RAB) with a maximum spending limit based on the rate of population growth plus inflation. This was recently released as part of Americans for Tax Reform’s Sustainable Budget Project, highlighting this approach’s benefits at the federal, state, and local levels. If Congress had followed this approach from 2004 to 2023, Figure 4 shows tax receipts, spending, and spending adjusted for only population growth plus chained-CPI inflation. Instead of an (updated) $20.2 trillion national debt increase, there could have been only a $700 billion debt increase for a $19.5 trillion swing in a positive direction that would have substantially reduced the cost of this debt to Americans. The Republican Study Committee recently noted the strength of this type of fiscal rule in its FY 2025 “Fiscal Sanity to Save America.” To top this off, the Federal Reserve should follow a monetary rule so that the costly discretion stops creating booms and busts. Figure 6: Federal Budget Gap Shrinks If Spending Limited to Population Growth Plus Inflation  Bottom Line

Bidenomics has been a failure and the policy approach must be redirected to pro-growth policies that shrink government rather than big-government, progressive policies. It’s time for a limited government with sound fiscal and monetary policy that provides more opportunities for people to work and have more paths out of poverty. Recommendations:

In the wake of the Baltimore bridge collapse, a major U.S. port has come to a standstill. The Port of Baltimore is the top U.S. port for vehicle imports and exports, as well as for farm and construction machinery. U.S. Transportation Secretary Pete Buttigieg told MSNBC on Wednesday that while there are many ports on the U.S. East Coast, “there is no substitute for the Port of Baltimore being up and running.”

How will this affect the U.S. economy—and even global supply chains? NTD spoke to Vance Ginn, the president of Ginn Economic Consulting and the former chief economist at the U.S. Office of Management and Budget, to find out more.  Last week, the Texas Association of Business, Fort Worth Chamber of Commerce, Longview Chamber of Commerce, U.S. Chamber of Commerce, and American Bankers Association sued to block the Consumer Financial Protection Bureau’s (CFPB) final rule to lower the credit card late fees cap to $8.

This lawsuit challenges the Biden Administration's terrible price control idea that would hurt Texans. Given the entities that sued to block this rule and the effect on Texans, the case should continue in Texas instead of moving it elsewhere as the CFPB would like. Credit card late fees, what some call “junk fees,” are the cost of someone paying their bill late. Nothing is free, so there’s a charge for paying late, as it also influences the expected cash flow of credit card companies. It’s not a price gouging scheme; it’s simply a way to take the risk of giving credit to those in need while keeping cash flow for profitability. This is not only important for businesses, but it also provides an incentive for people to pay their bill online. Without a market-based credit card fee, the cost will be on those who need credit the most as they won’t be able to get it or pay much higher interest rates. The Wall Street Journal Editorial Board wrote: “Even the CFPB acknowledges, the lower penalty may cause more borrowers to pay late, and as a result incur higher ‘interest charges, penalty rates, credit reporting, and the loss of a grace period.” Many Texans depend on credit card access to pay their living expenses. There are more than 3 lines of credit per user in Texas. More than 3 million small businesses also rely on access to credit to grow and expand. Some card issuers most impacted by this rule, including Citi, Chase, and Synchrony, have extensive operations in Texas. JCPenney, based in Plano, offers one of the country's most popular co-branded credit cards through its partnership with Synchrony. The retailer, which employs more than 2,000 Texans, is just a few years removed from bankruptcy and stands to lose big if this misguided rule is allowed to stand. Reports indicate late fees account for 14 to 30 percent of department store credit card revenue. Given the current state of credit card delinquencies at a 10-year high, the CFPB’s rule would exacerbate an already dire situation. This would have far-reaching effects on our community and economy, particularly as consumers and small businesses increasingly rely on credit to navigate lower inflation-adjusted average weekly earnings by 4.2% since January 2021. Most of the plaintiffs in this lawsuit are local organizations that recognize the importance of defending and preserving access to credit. Texas is the rightful venue for this battle.  Originally published at AIER.

ohn Cochrane’s The Fiscal Theory of the Price Level examines the relationship between fiscal policy and inflation, which many consider to be the increase in the price level of a basket of goods and services. An influential and accomplished economist at the Hoover Institution, Cochrane is one of the most forward-thinking economists today. His approach challenges conventional wisdom and presents a compelling case for reevaluating our understanding of the economy. I learned much from reading the book and while interviewing him about it on my Let People Prosper Show podcast. I highly recommend reading this extensive book, though I have reservations about fiscal policy trumping monetary policy when considering the influence on inflation. Cochrane begins by laying out the foundational principles of his theory. He emphasizes the roles of government debt, taxes, and inflation expectations on prices. He argues that traditional economic models, which focus primarily on the role of central banks in controlling inflation through monetary policy, such as those by Milton Friedman, overlook the substantial effect of fiscal variables on prices. By uniquely integrating fiscal considerations and the public’s expectations about those factors into economic analysis, Cochrane aims to provide a more robust framework for understanding and predicting inflationary trends. He delves into various theoretical and empirical aspects of fiscal theory, drawing on a wide range of literature and evidence to support his arguments. He explores the implications of government budget constraints, the role of Ricardian equivalence that assumes a balanced budget over time, and the potential limitations of conventional monetary tools in controlling inflationary pressures. His thorough examination of these issues provides readers with a comprehensive understanding of the complexities of studying the relationship between fiscal policy and inflation. Cochrane’s arguments are persuasive and well-supported, but some aspects of his analysis warrant scrutiny. One area of contention is Cochrane’s emphasis on the primacy of fiscal policy in driving inflationary dynamics, particularly his assertion that the Federal Reserve plays a secondary role compared to Congress in shaping inflation outcomes. While Cochrane makes a compelling case for the importance of fiscal variables, the penultimate creator of inflation is the Fed when it creates more money than the goods and services produced. Milton Friedman, who extensively studied the role of the Fed in economic activity and inflation, said: “Inflation is always and everywhere a monetary phenomenon. It is a result of a greater increase in the quantity of money than in the output of goods and services which is available for spending.” The Fed controls what’s called “high-powered money” of various assets on its balance sheet. These assets include mostly Treasury securities from the tens of trillions of dollars in debt issued by the federal government. It also includes mortgage-backed securities, lending to financial institutions, federal agency debt, and other lending facilities. I agree with Cochrane that federal deficits give ammunition to the Fed when it purchases Treasury debt, grows high-powered money, contributes to more money chasing too few goods and services, and results in inflation. But other assets on the Fed’s balance sheet also matter, especially since the Great Financial Crisis in 2008 when the Fed started quantitative easing. Cochrane’s framework overlooks the significant role of monetary policy in influencing inflation expectations and shaping the broader economic environment. While fiscal policy can play a role in determining long-term inflation trends, as the debt distorts interest rates in the market, the Fed’s control of the money supply to target the federal funds rate and influence other rates along the yield curve remains a potent tool for managing expectations. While we should challenge Congress to adopt a fiscal rule for sustainable budgets to relieve excessive spending that drives up the national debt, this does not undermine the source of inflation: the Fed. But if Congress could balance its budget, which hasn’t happened since 2001, it would remove a bullet the Fed could shoot at the economy. In other words, a sustainable fiscal policy, wherein Congress passes balanced budgets by limiting government spending — the ultimate burden of government and the source of budget deficits — would help control inflation. While this could mitigate the assets available for the Fed to add to high-powered money, it would not solve the inflation problem because of many other available assets. Another issue that arises from considering fiscal policy the prime mover of inflation is how it works in practice. Fiscal policy is not directly expansionary or contractionary, as it is just taking funds from some people to give to others, with many of the takers being politicians and bureaucrats in government. These actions move money around in the economy without increasing productive activity that creates goods and services. There are roles for the federal, state, and local governments, but those should be limited to those outlined in constitutions. If Congress would abide by the Constitution, whereby it funded only limited government instead of the bloated federal government today, then fiscal policy would not be so burdensome. Fiscal policy would also not fall into the Keynesian trap of trying to “stabilize economic activity,” as the only thing that governments typically stimulate is more government because of the created failures due to the limited knowledge and rent seeking by politicians and bureaucrats. The underlying problem is usually government failures that cannot be resolved by more government. When Congress returns to its limited, constitutional roles, the federal budget will be drastically cut, resulting in lower taxes and opportunities to pay down and retire the national debt. This would also help reduce the massive distortions throughout the economy from government spending, taxes, and regulations. It would also decrease the Fed’s influence on the economy, but not entirely because of the other assets available for its disposal. The Fed also distorts economic activity through its ability to influence each stage of the production process with the assets on its balance sheet and its effect on interest rates. When the Fed purchases Treasury debt and increases high-powered money, the new money does not go to everyone simultaneously. Instead, the money trickles down from the financial sector to other sectors based on credit availability and other factors, in what is called the Cantillon effect. The manipulation of different markets throughout the production process of goods by the new money and the influence the purchase of assets by the Fed has on interest rates create boom and bust cycles. There is ample evidence about these economic steps, especially from the Austrian business cycle theory. Fiscal policy influences many steps in the production process through subsidies, tax breaks, and regulations, which hinder the voluntary production of individual goods and services through a well-functioning price system. But Congress cannot increase the money supply, which only the Fed can do, nor influence the general price level nor the resulting inflation. All things considered, Cochrane’s comprehensive exploration of fiscal theory and extensive analysis of its implications for the price level riveted me. His methodical dissection of economic concepts and pragmatic approach to examining fiscal policy offered a fresh perspective on economic dynamics. In conclusion, the Fiscal Theory of the Price Level offers a valuable contribution to the ongoing debate surrounding the determinants of inflation and the role of fiscal policy in the economy. While I’m sympathetic to Cochrane’s arguments, it is essential to recognize the importance of a central bank’s monetary policy in causing inflation through its balance sheet. Additionally, we should acknowledge the distortions caused by government policy, whether fiscal or monetary, and recognize the secondary role of fiscal policy compared to monetary policy in addressing inflationary pressures. To ensure sound economic outcomes, it is imperative to establish strong fiscal and monetary rules that provide an institutional framework limiting the burdens of government actions on our lives and livelihoods. Despite my dissent on the emphasis placed on fiscal policy’s role in inflation, the book’s productive discourse on the delicate dynamics of key economic elements make this an important contribution to inflation studies.  Originally published at Washington Times.

In President Biden‘s recent State of the Union address, he painted a rosy economic picture, touting what he called “Bidenomics” as the driving force behind what he claims is a robust economy. He pointed to a low unemployment rate, the absence of a recession, and a lower inflation rate as evidence of success. Reality, however, tells a different story. And Mr. Biden’s recently released irresponsible budget sends the federal government and America further toward bankruptcy. Despite the president’s assertions, the economy and inflation remain top concerns for most Americans. The disconnect between the headlines and the lives of ordinary citizens underscores the profound challenges facing the nation’s economic landscape. This sense of malaise can be directly attributed to the flawed principles underlying Bidenomics, as outlined in his latest budget. These include excessive spending, taxation and regulation. Each is destructive, but together, they are catastrophic. The result has been stagflation and less household employment in four of the last five months. There have also been lower inflation-adjusted average weekly earnings by 4.2% since January 2021, when Mr. Biden took office. Rather than fostering economic growth and prosperity, Bidenomics has stifled innovation, investment and job creation. At its core, Bidenomics represents a misguided attempt to address complex economic issues through heavy-handed government intervention. While the administration may tout short-term gains, the long-term consequences of such policies are far-reaching and unaffordable. The reality is that excessive government spending has led to unsustainable levels of debt, burdening future generations with the consequences of fiscal irresponsibility. Similarly, excessive taxation is stifling entrepreneurship and dampening economic activity, limiting opportunities for individuals and businesses alike. Excessive regulation serves only to hamper innovation and drive up costs, exacerbating the challenges facing working families. Unfortunately, Mr. Biden’s latest budget proposal doubles down on these bad policies. Even with rosy assumptions of tax collections being a higher share of economic output over time as the tax hikes will reduce growth and, therefore, lower taxes as a share of gross domestic product, the budget continues massive deficits every year. This will result in higher interest rates, higher inflation, more investment These results have been highlighted in economic theory by economists such as Alberto Alesina and John B. Taylor. Their research has found that raising taxes doesn’t help close budget deficits because of the reduction in growth from higher taxes in a dynamic economy. The way forward should be cutting or at least better-limiting government spending — the ultimate burden of government on taxpayers. Amid these challenges, America also needs a return to optimism and flourishing. This includes leadership that inspires confidence, fosters innovation, and empowers people to pursue their dreams. We need out-of-the-box policies prioritizing economic freedom and individual opportunity, allowing the entrepreneurial spirit to thrive and driving growth and prosperity. More specifically, this means reducing the burden of government intervention through lower spending and taxes, streamlining regulations, and fostering an environment where entrepreneurship can thrive. By embracing fiscal sustainability and making tough choices, we can ensure the long-term stability and prosperity of our nation. In short, while Mr. Biden tries to spin a positive narrative about the economy, the facts speak for themselves. We cannot afford Bidenomics, no matter the headlines, what was touted in the State of the Union address, or the latest budget. The stakes are too high, and the consequences too grave, to ignore the reality of our economic situation. We need leadership that is willing to confront the hard truths and enact policies that prioritize the well-being of all Americans, fostering an environment where optimism and flourishing can thrive.  Originally published at Texans for Fiscal Responsibility. Thank you for listening to the 45th episode of "This Week's Economy."

Today, I cover: 1) National: -DeSantis drops out of the race, and New Hampshire primary results put Trump and Haley fairly close, so what happens next? -Real GDP for Q4 2023 was up 3.3%, but the contribution of costly, unproductive government spending makes the real private GDP rate lower. -The stock market has been better under Trump than Biden through three years of their terms, but Trump can’t necessarily take the credit. Will he try? -Grocery prices have moderated but have still outpaced earnings since 2019; what does it mean to you? -Why the tax code shouldn’t serve as social engineering, but why does Congress try? 2) States: -National School Choice Week highlights which states need to provide universal education freedom. Is your state next? -My new paper with Sal Nuzzo of the James Madison Institute notes how Florida can reduce its sales tax burden, but will they do it? -State-level jobs report reveals that job growth is slow across most states, but Texas leads in job creation. How does your state do? 3) My Media Hits & Other: -My recent commentary reveals what’s really going on in the labor market. -My latest bonus LPP episode with Brad Swail of Texas Talks shares my thoughts on the economy, Texas, property taxes, immigration, and more. -Last week’s LPP episode with Matt Mitchell reveals how Estonia is freer than the U.S. -Set your alarms for Monday so you don’t miss my upcoming episode with Dr. Bruce Caldwell on Friedrich Hayek and much more. Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. Also, subscribe and see show notes for this episode on Substack (www.vanceginn.substack.com) and visit my website for economic insights (www.vanceginn.com).  Originally published at Daily Caller.

A new study from the International Monetary Fund (IMF) has ruffled assumptions, asserting that “40% of global employment is exposed to AI.” The study also predicts that high-skilled jobs will bear the brunt of this transformation, disproportionately influencing roles that traditionally require higher education and professional experience. Among advanced economies, the IMF estimates that the share of jobs affected by AI could be 60 percent. Half of them could benefit from increased productivity, and the other half hurt by replacement. The IMF concludes that the impending shift should compel countries, particularly those well-prepared for AI integration like the U.S., to implement “robust regulatory frameworks.” They argue this would help cultivate a safe and responsible AI environment with safety nets to help those whose jobs are AI “vulnerable.” But we don’t have to look too far back to realize how attempting to harness AI innovation and its results would be disastrous for people and prosperity. The rise of AI presents a unique chance for society to better adapt to challenges and capitalize on new opportunities. Humanity has always adapted to new technological possibilities, turning most disruptions into positive outcomes. For instance, dedicated professionals called “calculators” once performed complex calculations. With the emergence of pocket-sized calculators in 1971, the computing revolution began, showcasing the transformative potential of technological innovation. Those human calculators, who would today be considered high-skilled, highly vulnerable individuals, went behind the machines and created and perfected better computational technologies. Whether or not they felt threatened by the technology, they adapted nevertheless and made their skills indispensable to the technology. As the electronic calculator removed much busy work, their minds were more available to focus on tasks machines couldn’t perform. The emergence of health-related diagnostic tools like X-rays and MRIs did not render doctors less valuable but widened the breadth of their jobs. Tractors did not displace farmers but made aspects of the role significantly more accessible, allowing for higher output. The examples of technology helping humans by making their jobs easier are endless. High-skilled professionals facing AI exposure should view this revolution as an opportunity to learn and grow. Rather than advocating for regulatory barriers, individuals can proactively enhance their skills, pursue further education, earn certificates, or even explore career transitions. The power of spontaneous order in free markets lies in allowing people to innovate when not restricted by government overreach. The IMF study’s conclusion urging countries to hurriedly embrace AI regulation overlooks the resilience and adaptability inherent in free societies. Attempting to pause AI innovation is impractical in the face of rapid advancements by other nations. Our big tech competitors like China and the UAE will not inhibit progress with red tape, so why would we? We’ve already seen demonstrative instances. Recall that in June 2023, Meta launched what was, at the time, the largest open-source language model ever, Llama 2. For almost two months after that, America was the global AI leader due to this technology, only to be eclipsed by the UAE government with their release of Falcon 180b, which has more than double the parameters of Llama 2. In a matter of weeks, America lost its top spot in AI innovation. Imagine what would happen if we introduced more regulatory barriers, as suggested by the IMF, or required a pause in AI advancement, as suggested by Elon Musk and others last year. It’s not just the U.S. reputation as a world leader at stake but our very security, as we could quickly be overtaken by nations who embrace the power of AI in technology, cybersecurity, and beyond. To maintain leadership in the AI landscape, the U.S. must welcome disruptive changes and cultivate an environment encouraging competitiveness. The future belongs to those who can adapt and innovate, and AI, as a tool created by humans, should be embraced rather than feared.  We must learn from history or be doomed to repeat it. This includes honestly assessing the economy in 2023 so that we have better information for making decisions in 2024.

Starting with a bang on many people’s minds is housing affordability. The year commenced with a surge in the average 30-year fixed mortgage rate from 6.5% in January to nearly 8% in October but has declined recently to about 6.6%. These higher mortgage rates and record-high housing prices contributed to an unaffordable housing market. While existing home sales were up 0.8% in November, they are down 7.3% over the last year, indicating a struggling housing market for families that will unlikely improve much in 2024. Another concern is costly inflation. Rampant hikes in the cost of a typical basket of goods and services have meant less purchasing power for us. This contributes to making housing, food, education, and other expenses for that basket less comfortable or worse for many families. As of November 2023, the core consumption personal expenditures increase was 3.2% year-over-year. This price measure of a basket of goods and services excludes food and energy and is what the Federal Reserve prefers to watch. While core PCE inflation has moderated from close to 6% in 2022, the recent 3.2% inflation rate remains 60% higher than the Fed’s average inflation target of 2%. Although moderating inflation represents some relief for many Americans, the challenge is that average weekly earnings adjusted for core inflation declined in 23 of the last 35 months since January 2021. In total, these real average weekly earnings are down 0.8% since then, indicating why inflation is a top concern. An additional problem is debt. Because earnings haven’t been keeping up with inflation, credit card debt soared to more than $1 trillion as people struggled to make ends meet, which is a bad sign for 2024. And many people have been going through their savings and retirement funds quickly. What about jobs? The White House recently celebrated “total job gains achieved under the Biden administration reached 14.1 million through November 2023.” But this metric becomes less impressive considering that 9.4 million of those jobs were just recovering jobs lost during the pandemic lockdowns. So, there have been 4.7 million new jobs added since January 2021, which is 134,000 per month. While this is positive, it is not record-breaking. The weaker labor market in recent months indicates that 2024 could be tough for many workers. Most people’s pocketbooks did not grow but diminished this year, and the job market similarly lags. But what about the nation’s overall growth? Hasn’t GDP soared? Not exactly. In the third quarter of 2023, the annualized real GDP growth hit 4.9%, which appears robust. But when you dig into the details, it’s more complicated. Government spending, which is a drag on the economy as it must take taxes from the private sector and distort market activities, threw in 0.99 percentage points. And private inventories, influenced by the whims of fluctuating interest rate expectations, chipped in 1.27 percentage points. When you exclude those contributions to consider stable real private GDP, there was just a 2.6% bump up. This slower pace didn’t just pop out of nowhere. It’s been a saga since early 2022, when we hit a two-quarter decline in real gross domestic product, waving a big red flag for a recession. And when you consider the valuable metric of real gross domestic output, which is the average or real gross domestic product and real gross domestic income, the economy has declined in three out of the last seven quarters. While these economic issues suggest stagflation triggered by misguided pandemic lockdowns and subsequent trillions of new money printing of deficit-spending, there may be some relief. The Fed’s slow correction to its bloated assets of $9 trillion at its peak to $7.7 trillion contributed to interest rates soaring since March 2022. But with Congress continuing to deficit spend of about $2 trillion per year and net interest payments soaring to $1 trillion per year, there are massive economic challenges ahead. These deficits will make it more difficult for the Fed to correctly normalize its assets quickly to get them back to at least the pre-pandemic $4 trillion. This is because the budget deficits would contribute to higher interest rates, so the Fed will likely monetize the debt more to help Congress avoid needed spending restraint. While these truths are tough to swallow, many beacons of hope also emerged throughout the year that should be noted. In 2023, a momentous shift unfolded with a transformative surge in educational choice. Twenty states expanded school choice, and a record-breaking 10 states passed some form of universal school choice, making 36% of American students eligible for a private choice program. Some states have been slow to increase educational freedom, but this revolution’s overall impact is historical. Recognizing that children are the cornerstone of our nation’s future and acknowledging that improved education is a pivotal predictor of their success, the catalyst for change is undeniably rooted in more universal school choice. The second bright light is the flat state tax revolution. Many states took bold steps to enhance their economic landscapes. Notably, prominent states like California and New York faced ongoing out-migration as individuals sought refuge from progressive policies, and less heralded states embraced free-market principles, propelling them onto the national stage. More conservative Florida and Texas continued to lead the way in places where people moved in 2023. The third thing to cheer is a responsible movement toward a sustainable state budget revolution. Some states are pushing toward improving their spending limits to one that covers more of the budget, limits budget growth to no more than population growth plus inflation, and has a supermajority vote to bust the limit or raise taxes. The synergy of these reforms demonstrates the power of federalism as states experiment with policies, revealing effective strategies and fostering a healthy laboratory of competition. We need lawmakers at the federal, state, and local governments to recognize what works and implement them. The trajectory in 2024 and beyond hinges on embracing free-market capitalism, which is the best path to let people prosper. This includes less government spending, less money printing, more school choice, and more tax relief. In short, less government. That’s how we get a more prosperous 2024. Happy New Year! Originally published at Econlib. Thank you for tuning into the FINAL Let People Prosper podcast episode 76 of 2023! Today, I have a brief but informative podcast for you, recapping the highlights of the economy and my business, Ginn Economic Consulting, LLC.

As a Christmas gift, I am giving away a complimentary subscription to the paid version of my newsletter and a copy of Lexi Hudson’s fantastic book, “The Soul of Civility: Timeless Principles to Heal Society and Ourselves.” To enter this giveaway, simply fill out the information at the link and rate my podcast on either Apple Podcasts or Spotify. Is there anyone whom you would like for me to interview in 2024? Leave them in the comments. Today, I cover:

Originally published at Real Clear Policy.

During the fourth Republican presidential candidate debate the four participating candidates were asked to name a past president who would serve as an inspiration for their administration. In his response, Governor Ron DeSantis stated that he would take inspiration from President Calvin Coolidge. Coolidge, stated DeSantis, is “one of the few presidents that got almost everything right.” Further, DeSantis argued that “Silent Cal” understood the federal government’s role and “the country was in great shape” under his administration. To say that the federal budget process is broken is an understatement. The national debt continues to grow driven by out-of-control spending. The budget hawk within the Republican Party is an endangered species. Governor DeSantis is correct that the Republican Party needs to rediscover the principle of limited government. The best way to do this is to take inspiration from the Republican Party’s best known budget hawks and champions of limited government, Presidents Warren G. Harding, and Calvin Coolidge. President Harding assumed office in 1921 when the nation was suffering a severe economic depression. Hampering growth were high-income tax rates and a large national debt after World War I. Congress passed the Budget and Accounting Act of 1921 to reform the budget process, which also created the Bureau of the Budget (BOB) at the U.S. Treasury Department (later changed in 1970 to the Office of Management and Budget). President Harding’s chief economic policy was to rein in spending, reduce tax rates, and pay down debt. Harding, and later Coolidge, understood that any meaningful cuts in taxes and debt could not happen without reducing spending. Harding selected Charles G. Dawes to serve as the first BOB Director. Dawes shared the Harding and Coolidge view of “economy in government.” In fulfilling Harding’s goal of reducing expenditures, Dawes understood the difficulty in cutting government spending as he described the task as similar to “having a toothpick with which to tunnel Pike’s Peak.” To meet the objectives of spending relief, the Harding administration held a series of meetings under the Business Organization of the Government (BOG) to make its objectives known. “The present administration is committed to a period of economy in government…There is not a menace in the world today like that of growing public indebtedness and mounting public expenditures…We want to reverse things,” explained Harding. Not only was Harding successful in this first endeavor to reduce government expenditures, his efforts resulted in “over $1.5 billion less than actual expenditures for the year 1921.” Dawes stated: “One cannot successfully preach economy without practicing it. Of the appropriation of $225,000, we spent only $120,313.54 in the year’s work. We took our own medicine.” Overall, Harding achieved a significant reduction in spending. “Federal spending was cut from $6.3 billion in 1920 to $5 billion in 1921 and $3.2 billion in 1922,” noted Jim Powell, a senior fellow at CATO Institute. Harding viewed a balanced budget as not only good for the economy, but also as a moral virtue. Dawes’s successor was Herbert M. Lord, and just as with the Harding Administration, the BOG meetings were still held on a regular basis. President Coolidge and Director Lord met regularly to ensure their goal of cutting spending was achieved. Coolidge emphasized the need to continue reducing expenditures and tax rates. He regarded “a good budget as among the most noblest monuments of virtue.” Coolidge noted that a purpose of government was “securing greater efficiency in government by the application of the principles of the constructive economy, in order that there may be a reduction of the burden of taxation now borne by the American people. The object sought is not merely a cutting down of public expenditures. That is only the means. Tax reduction is the end.” “Government extravagance is not only contrary to the whole teaching of our Constitution but violates the fundamental conceptions and the very genius of American institutions,” stated Coolidge. When Coolidge assumed office after the death of Harding in August 1923, the federal budget was $3.14 billion and by 1928 when he left, the budget was $2.96 billion. Altogether, spending and taxes were cut in about half during the 1920s, leading to budget surpluses throughout the decade that helped cut the national debt. The decade had started in depression and by 1923, the national economy was booming with low unemployment. Both Harding and Coolidge were committed to reining in spending, reducing tax rates, and paying down the national debt. Both also used the veto as a weapon to ensure that increased spending and other poor public policies were stopped. The results of the Harding-Coolidge economic plan created one of the strongest periods of economic growth in American history. Unemployment remained low, the middle class was expanded, and the economy expanded. From 1920 to 1929 manufacturing output increased over 50 percent and the United States was a global leader in many key industries. In our current era marked by dangerous debt levels and high inflation whoever becomes the Republican presidential nominee should take inspiration from Harding and Coolidge. Thank you for tuning into the 75th episode of the Let People Prosper Show podcast!

Today, I’m joined by Dr. Chris Coyne, professor of economics at George Mason University and author of the book, “In Search of Monsters to Destroy: The Folly of American Empire and the Paths to Peace.” Today, we discuss: 1) The economic impact of war and the many consequences of engaging in it; 2) What Friedrich Hayek's principle of "fatal conceit" reveals about America's involvement with war; and 3) The truth about terrorism, what the U.S. got wrong with Afghanistan and Iraq, and Chris' thoughts of how Russia-Ukraine and Israel-Hamas can be at peace. Economic Reality Check: What Do Falling Mortgage Rates & Jobs+Inflation Signal for the 2024 Economy?12/15/2023 Thank you for tuning into the 39th episode of “This Week’s Economy.”

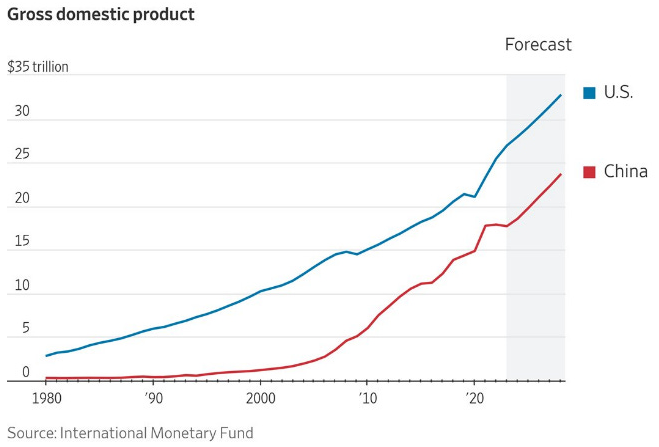

Much information is packed into today’s newsletter, including my new podcast episode revealing the economic news you need to know in less than 14 minutes! Today, I cover: 1) National: -Why the new U.S. jobs report (my latest commentary) is not as strong as some say -Inflation rates have moderated but still remain well above the Fed’s 2% rate target -Federal Reserve paused again with its federal funds rate target in the range of 5.25-5.5%, supporting a boost in the stock market and likely lower mortgage rates 2) States: -Sustainable Colorado Budget was released that I authored with Ben Murrey at Independence Institute, which provides a path forward for the Centennial state to return to its TABOR roots and buy down the income tax -School choice challenges face Texas as many state leaders are against it, and they keep spending too much -California’s deficit reaches crazy highs, proving why spending is the ultimate government burden 3) Other: -Don't miss my latest LPP episode with Jennifer Huddleston discussing problems with regulating technology, including AI -One of my latest op-eds argues why China is not our biggest threat…what is? -Argentina's new president makes significant strides that could set an example for the U.S.  Originally published at American Institute for Economic Research. Rating agency Moody’s just downgraded China’s credit outlook from stable to negative after doing the same to the US about a month ago. Does this mean that China is on equal footing with us? Worse? Better off? An economic analysis suggests that China is not our biggest threat, nor are we theirs. In fact, the biggest problem we face is completely self-inflicted and found on our home soil. Apprehensions about China’s military actions and trade strategies maintain resonance, especially among middle-aged and older Americans. While caution is warranted, especially concerning their censorship and the treatment of Hong Kong and Taiwan, an economic comparison settles many doubts.  Regarding economic might, the US outshines China with a GDP of $27 trillion compared to China’s $18 trillion. The contrast is stark on a per-capita basis. Americans enjoy an average income of $79,000, six times more than their Chinese counterparts. One alarming similarity stands out though: Both nations have weathered credit downgrades mainly due to escalating budget deficits and national debts. The United States’ national debt is shaping up to be this decade’s hallmark. Now nearly $34 trillion, the deficit spiked in 2020, with trillions of dollars more added since. Net interest payments on the debt climbed by 39 percent and recently surpassed $1 trillion annually.  The repercussions of the national debt crisis are not merely theoretical – they are tangible, affecting the everyday lives of citizens.

In 2023, the dollar has significantly depreciated. Fitch (and now Moody’s) downgraded our creditworthiness. Home sales hit their slowest pace since 2010. Average 30-year fixed mortgage rates reached their highest point since 2000. And real median household income dipped to its lowest level since 2018, to name just a few of our recent economic woes. These findings shed new light on our competition with China. They should prompt America’s leaders to reevaluate our priorities and consider whether the enemy across the Pacific is as pressing as the ones we face at home. While some argue the government spending that drove the deficits was necessary, especially during the pandemic’s peak, it underscores the broader problem – a lack of fiscal discipline and a predisposition to rely on debt as a quick fix. It is high time the US adopted a spending-limit rule. Without one, we’ve only made things worse and failed to reach budget agreements. A reasonable spending limit of no more than the rate of population growth plus inflation has worked at the state level, and it would work at the federal level. While the US points the finger at China, we have three other fingers pointing back at us. Excessive government spending and a burgeoning national debt are eroding the foundation of our economic stability. Now is not the time to allocate excessive resources to confront external foes, but to address the fundamental issue plaguing us: a government that refuses to rein in spending of taxpayer money. America should also correct the errors in recent years of trade protectionism. There is reason to counter those countries who don’t play by the same rules, like China, but that should be done by joining free trade agreements with allies. This would be a more effective and affordable approach for Americans instead of raising taxes on them through tariffs, appreciating the dollar thereby increasing the trade deficit and contributing to trade wars that often lead to military wars. Let’s refocus our efforts, fortify our economic foundation, and confront the genuine threat within our borders. If not, governments will not be able to do their job of preserving liberty. This is of utmost importance. Today, I cover the following:

Check out the short from the episode below if you want a quick recap before watching the full episode. |

Vance Ginn, Ph.D.

|

RSS Feed

RSS Feed

{kind=link}

Proudly powered by Weebly