America is in the midst of an identity crisis, and it’s probably not the kind you’d think. Our nation is wrecked by an abysmal economy and unhappy people losing confidence in their country. In such unhappiness, people on both sides of the political aisle too often propose “solutions” that grant the government more control of our lives, even though that control is usually the source of the problem.

The American experiment has paved the way for millions to escape poverty and build a better life via a free-market system with a constitutional republic that encourages innovation and results in more human flourishing than ever before. We need to get back to those roots. I had the opportunity to discuss this phenomenon with Dr. Samuel Gregg, author of the book The Next American Economy and distinguished fellow at the American Institute for Economic Research, who said this country’s founding values are based on “liberty and personal responsibility.” What set America apart was a vision for commoners to determine their own future, and we continue to rank as the most entrepreneurial country in the world. American’s earliest ideals demanded liberty and responsibility, rejecting directives from a distant King. As a result, the roles of the federal and state governments were carefully managed by a system of federalism, with checks and balances to restrain overreach and protect liberty. According to Gregg, this ongoing experiment is why immigrants are continually inspired to leave their homes and venture to the United States. These core tenets of America have become less defined over the past century. America has increasingly chosen big government over individual liberties, thereby reducing the benefits of free-market capitalism. The major expansions of government started in the progressive era, with Presidents Teddy Roosevelt, Woodrow Wilson, and Herbert Hoover. Those historic expansions were put on steroids by President Franklin D. Roosevelt’s “New Deal,” which prolonged and deepened the Great Depression. Likewise, President Lyndon B. Johnson’s “Great Society” program ballooned government through the creation Medicare and Medicaid, among others. The results have been massive government spending with increased dependency on government programs. President George W. Bush’s expansion of Medicare with Part D provided some prescription drug coverage for seniors, with questionable results, at a massive cost. President Barack Obama’s Obamacare expanded government control, contributing to the high cost and declining quality of US healthcare. President Trump’s attempt to punish China with tariffs actually punished low-income Americans most. Most recently, President Biden’s 2022 “Inflation Reduction Act” further grows government, without reducing inflation and at a huge cost to taxpayers. Inflating the role of government in an attempt to solve underlying issues created by big government created a vicious cycle that continues today. Government meddling distorts the economy by blocking and confusing free people’s choices. This results from a cultural shift, where Americans increasingly seem to believe government can solve problems better than markets or individuals. This belief is contradicted by the evidence. The lack of belief in free markets is really the lack of believe in free people, as the market is nothing but people. Big government is usually the cause of economic and social problems, so trying to solve them with more government just exacerbates the issues. A severe deficit in the knowledge of history, both of culture and economics, helps explain why post-modern socialist solutions increasingly entrance younger generations. Unlike older countries, America’s identity comes from the “texts, documents, and debates” that created our founding, says Gregg. Surveys show that only 1 in 3 Americans can pass a citizenship test, because most of them aren’t familiar with the foundational ideas outlined in our texts and documents. A national identity crisis is near-inevitable, when we forget our core values of liberty and personal responsibility The further we stray from the principles that made our nation great (including free-market capitalism, a constitutional republic, and personal responsibility) the more swiftly we head down what economist Friedrich Hayek called “the road to serfdom.” Only by learning our unique history, and grasping the principles of free-market economics free from burdensome interference, can Americans embark on the next American economy. Originally published at AIER.

0 Comments

As Congress rolled out the $1.7 trillion omnibus government-funding bill, an economist broke down the effects of large federal spending amid big deficits and high debt, the impact on tuition, and the need for oversight of some of this taxpayer money. NTD spoke to Vance Ginn, the president of Ginn Economic Consulting, who warned against massive spending, given a federal deficit of over $1.3 trillion and a national debt of over $31 trillion. Ginn called on Americans to say “no” to the bill and let the next Congress draft a budget, and alleged that the omnibus bill expands social safety nets without connecting them back to people joining the workforce.

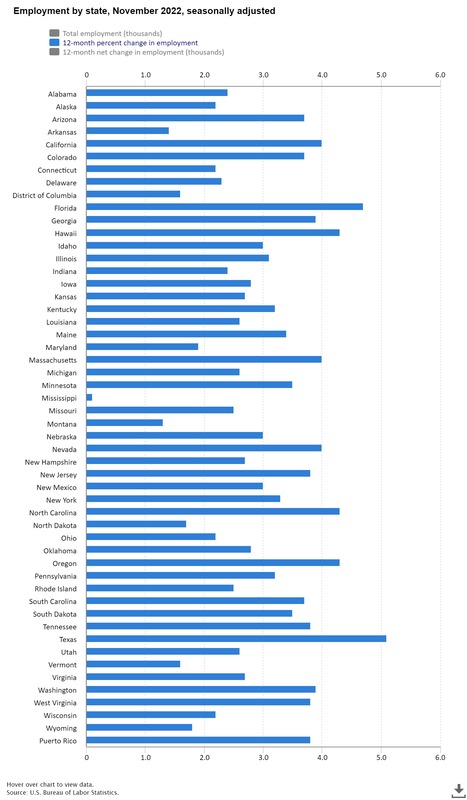

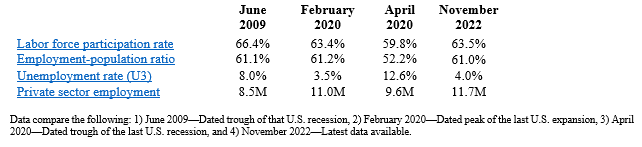

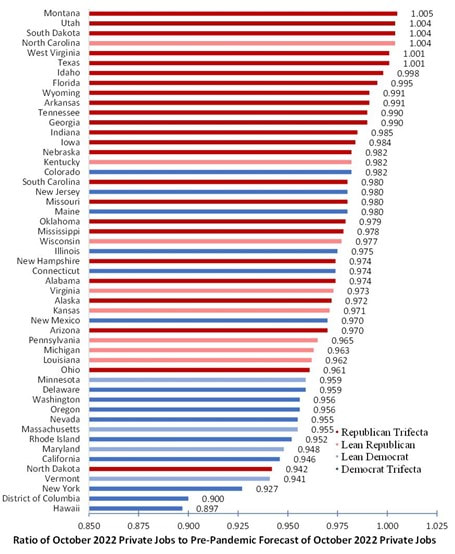

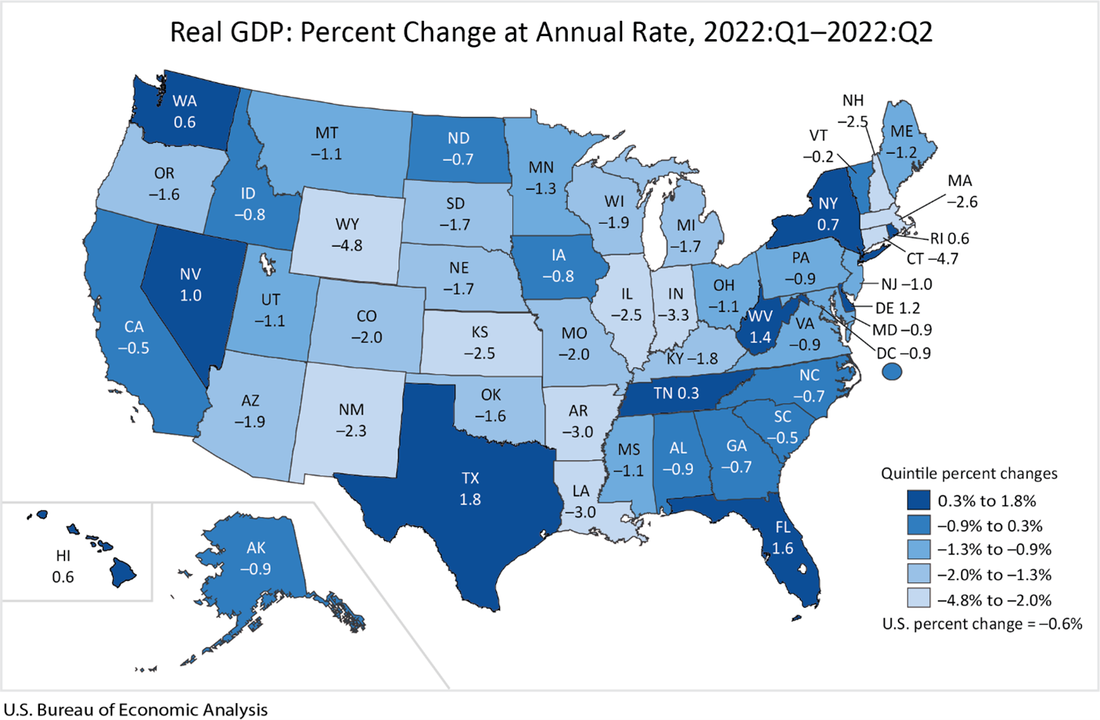

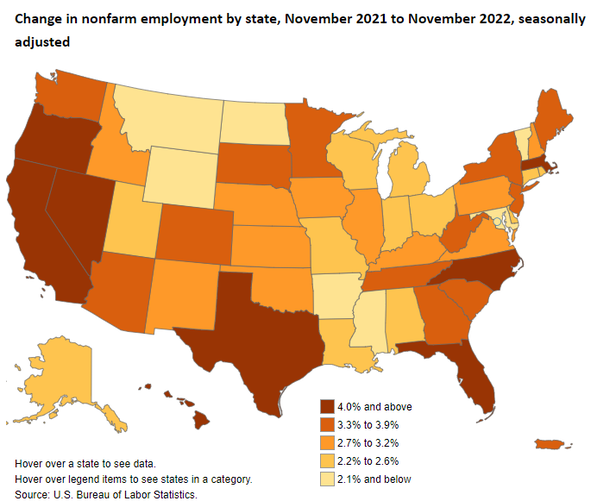

Originally posted at NTD News. Key Point: Texas leads the way in job creation over the last year and in economic growth in the latest reported quarter but there’s more to do to help struggling Texans deal with the state’s affordability crisis, especially spending less and moving further to sales taxes.  Overview: Texas has been a national leader in the economic recovery since the inappropriate shutdown recession in Spring 2020. This includes reaching a new record high in total nonfarm employment for the 13th straight month, leading exports of technology products for 20 consecutive years, and being home to 54 of the Fortune 500 companies. While the 87th Texas Legislature in 2021 supported the recovery by passing many pro-growth policies like the nation’s strongest state spending limit, there’s more to do in the session in 2023 to remove barriers placed by state and local governments. Solutions include governments passing responsible budgets and returning surplus tax dollars collected to taxpayers by reducing property taxes until they’re eliminated. Other states are cutting, flattening, and phasing out taxes, so Texas must make bold reforms to support more opportunities to let people prosper, mitigate the affordability crisis, and withstand destructive policies out of D.C. Labor Market: The best path to prosperity is a job, as it helps bring financial self-sufficiency, dignity, hope, and purpose to people so they can earn a living, gain skills, and build social capital. The table below shows the state’s labor market for November 2022. The establishment survey shows that net nonfarm jobs in Texas increased by 33,600 last month, resulting in increases for 30 of the last 31 months, to bring record-high employment to 13.7 million. Compared with a year ago, total employment was up by 657,600 (+5.1%), which was the fastest growth rate in the nation, with the private sector adding 635,100 jobs (+5.8) and the government adding 22,500 jobs (+1.1%).  The household survey shows that the labor force participation rate is slightly higher than in February 2020 but well below June 2009 at the trough of the Great Recession. The employment-population ratio fell by 0.1% in November moving it further away from where it was in February 2020, and the private sector now employs 700,000 more people. Texans still face challenges with a worse unemployment rate, though historically low, and nonfarm private jobs just recently above its pre-shutdown trend (Figure 1). Figure 1 compares the ratio of current private employment to pre-shutdown forecast levels in red states and blue states if both chambers of the legislature and the governor are Republican (dark red), Democrat (dark blue), or some combination (lighter colors). The results show a clear distinction between red states and blue states, with the stringency of restrictions by governments during the pandemic along with pro-growth policies before and after the shutdowns playing key roles. Specifically, 22 of the 25 states with the best (highest) ratios are in red-ish states while 13 of the 15 states and D.C. with the worst (lowest) ratios are in blue-ish places as of October 2022. Figure 1 Ratios of Current Private Jobs to Pre-Shutdown Forecast of Private Jobs by Place and Political Representation, October 2022  Overall, multiple indicators should be considered as the unemployment rate is a rather weak signal of the labor market. While the labor force participation rate in Texas exceeds where it was before the shutdowns, and the 4.0% unemployment rate could be full employment, the employment-population ratio is 0.2-percentage point above the pre-shutdown ratio. Economic Growth: The U.S. Bureau of Economic Analysis (BEA) provided the real gross domestic product (GDP) by state for Q2:2022. Texas had the fastest GDP growth of +1.8%—to $1.85 trillion—on an annualized basis (above the -2.6% U.S. average). These followed Texas’ GDP growth declines of -7.0% in Q1:2020 and -28.5% in Q2 during the depths of the recession. GDP rebounded in Q3 and Q4, yet declined overall in 2020 by -2.9% (less than -3.4% decline of U.S. average) but increased by +3.9% in 2021 (below the +5.9% U.S. average). The BEA also reported that personal income in Texas grew at an annualized pace of +9.3% in Q2:2022 (ranked 3rd best and above the +5.8% U.S. average) as job creation and inflated income measures found their way across the economy.  Bottom Line: As Texas recovers from the shutdown recession and faces an uncertain future with the U.S. economy having stagflation and a likely recession, Texans need substantial relief to help make ends meet. While the Texas Model was strengthened by the 87th Legislature last year from less government spending, taxing, and regulating, more is needed for limiting government at the state and local levels.

Recommendations: In 2023, the Texas Legislature should improve upon its past efforts by:

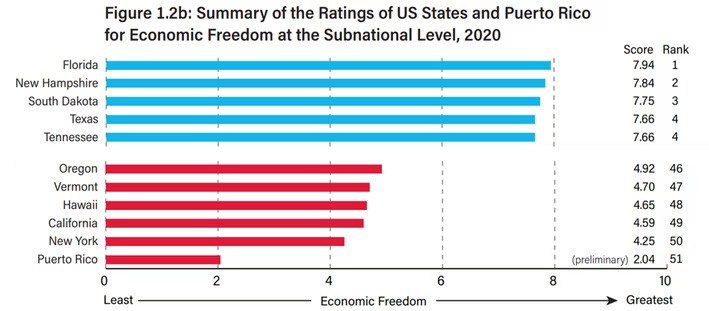

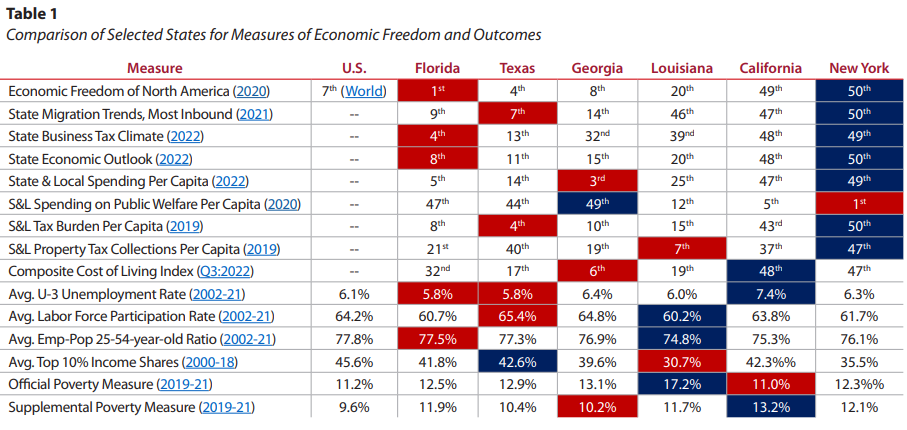

People point to tax burdens and over-regulation as the reasons for economic decline. But the reality is that high government spending is the precursor to heavy taxes and regulation. Look no further than the Fraser Institute’s latest report to see how states rank for economic freedom based on government spending, taxes, and labor market regulation. The five lowest-ranking states for economic freedom are Oregon (46th), Vermont (47th), Hawaii (48th), California (49th), and New York (50th). The most economically free states are Florida (1st), New Hampshire (2nd), South Dakota (3rd), Texas (4th), and Tennessee (4th).  I recently interviewed Dr. Dean Stansel, contributing author of the report, about his findings. He said, “anytime the government takes from you, that’s an infringement on your freedom.” And he’s right; if the government doesn’t spend, it doesn’t need to tax and it wouldn’t fund bureaucrats to regulate.

The data in the report are two years behind, so these findings reflect 2020, which include only a few months of the pandemic-related shutdowns and excessive policy restrictions. Given the continued excess of spending since then, there is good reason to believe that the scores will look worse in the following reports, even if the relative rankings don’t change much. The lowest-ranking states for economic freedom spend excessively and raise taxes to fund self-imposed expenses instead of limiting spending to what the average taxpayer can afford. Given this, there’s no surprise that New York is 50th. The state’s extreme spending has led it to what’s been estimated as a $10 billion deficit. It also ranks last in individual income taxes and second to last in property taxes, according to the Tax Foundation’s latest rankings of state business tax climate, which ranks the state 49th. Florida, on the other hand, ranks first in economic freedom with no personal income taxes, and ranks fourth among states in business tax climate. The trend is similar among the more and less economically free states: those with lower spending, taxes, and regulations boast better economic freedom rankings, while states like New York and California with egregious tax burdens and regulations are the least economically free. According to Stansel, the top states remained at the top even after pandemic-related shutdowns slowed state economies because they more successfully kept spending, taxes, and labor market regulations under control. But the real question is: why should we care about economic freedom? Economic freedom is the measure of how much people can decide for themselves on how to meet their needs, given that we live in a world where resources, especially time, are scarce. In free-market capitalism, people own and direct the means of capital and labor. But with socialism, politicians own and direct the means of capital and labor. Government interference, whether in the form of excessive government spending that distorts economic activity, or heavy taxation and barriers to work and capital growth through regulation, reduces means and opportunities for voluntary exchange that supports greater human flourishing. The more regulations state governments impose, the less incentive people have to work and be entrepreneurial. The more the state taxes, the less money people have to contribute to the savings, investment, and capital growth that provides for the wealth of nations’ investment. People are fleeing less economically free states toward the freer. There is greater potential for personal flourishing where there are fewer barriers to individual decisions that support economic growth. While tax and regulation reforms are reasonable steps for states seeking more economic freedom, it won’t help much if state spending remains unrestrained. According to the late economist and originator of the ideas for the EFNA report, Milton Friedman, the ultimate burden of government is not how much it taxes, but how much it spends. Balancing the budget is one thing, but that’s a short-term fix for an ideological problem too many states seem to have made, about the expanded role of government. Taxpayers must fund government programs when instead, the government should be limited to its constitutional roles so more money stays in the pockets of taxpayers and the productive private sector. Until states decide to impose a strict spending limit based on a maximum rate of population growth plus inflation, cut and eliminate burdensome taxes, and scrap burdensome regulations, economic freedom will continue to collapse. And, more importantly, people will suffer. States must not let that happen. Instead, state governments should get out of the way so that economic freedom can empower people to prosper. Originally published at AIER.  Key Point: We need pro-growth policies to unleash economic prosperity.  Overview: The irresponsible “shutdown recession” from February to April 2020 and subsequent government failures of excessive spending, regulation, and printing of money have led to a longer, deeper recession with high inflation that will have long-lasting consequences for many Americans’ livelihoods now and in the future. This includes excessive federal spending redistributing scarce private sector resources with deficit spending of more than $7 trillion since January 2020 to reach the new high of $31.4 trillion in national debt—about $95,000 owed per American or $250,000 owed per taxpayer. This new debt added fuel to the fire as the Federal Reserve monetized most of the new debt, leading to a 40-year-high inflation rates, substantially reducing our purchasing power even when accounting for increases in earnings. The inflated transitory boom continues to bust into a long, deep recession with high inflation, which hasn’t happened since Joan Jett and the Blackhearts was the top-ranked rock band in 1982. The failed policies of the Biden administration, Congress, and the Fed must be replaced with a liberty-preserving, free-market, pro-growth approach so there are more opportunities to let people prosper. Labor Market: The U.S. Bureau of Labor Statistics recently released the U.S. jobs report for November 2022. The establishment report shows there were 263,000 net nonfarm jobs added last month, with 221,000 added in the private sector. Interestingly, while there have appeared to be a relatively robust number of jobs created, a recent report by the Philadelphia Fed find that if you add up the jobs added in states in Q2:2022 there were just 10,500 net new jobs rather than more than 1 million initially estimated. This further indicates that the recession started earlier this year, likely in March. The official U3 unemployment rate increased to what remains a historically low rate of 3.7%, but challenges remain. These challenges include a 3.0% decline in average weekly earnings (inflation-adjusted) over the last year, a 0.8-percentage point lower prime-age (25–54 years old) employment-population ratio than in February 2020, and a 1.3-percentage-point lower labor-force participation rate with millions of people out of the labor force. Things look worse when you consider the household survey, which employment declined by 138,000 jobs last month and has declined in four of the last eight months for a total increase of just 12,000 jobs since March 2022 (when I would date the 2022 recession). This goes along with my warnings for months of a “zombie economy.” This includes “zombie labor” as many workers are sitting on the sidelines and others are “quiet quitting” while there’s a declining number of unfilled jobs than unemployed people to 4.3 million And that demand for labor is likely inflated from many “zombie firms,” which run on debt and could make up at least 20% of the stock market and will likely lay off workers with rising debt costs.  Economic Growth: The U.S. Bureau of Economic Analysis’ released economic output data for Q3:2022. The following provides data for real total gross domestic product (GDP), measured in chained 2012 dollars, and real private GDP, which excludes government consumption expenditures and gross investment.  The shutdown recession contracted at historic annualized rates because of individual responses and government-imposed shutdowns related to the COVID-19 pandemic. Economic activity has had booms and busts thereafter because of inappropriately imposed government COVID-related restrictions in response to the pandemic that severely hurt people’s ability to exchange and work. In 2021, the growth in nominal total GDP, measured in current dollars, was dominated by inflation, which distorts economic activity. The GDP implicit price deflator was up 6.1% for Q4-over-Q4 2021, representing half of the 12.2% increase in nominal total GDP. This inflation measure was up by 9.1% in Q2:2022—the highest since Q1:1981—for an 8.5% increase in nominal total GDP. This made two consecutive declines in real total (and private) GDP, providing a criterion to date recessions every time since at least 1950. Nominal total GDP was 7.3% and GDP inflation was 4.3% for the 2.9% increase in real total GDP in Q3:2022. But if inflation had been as high as it was in the prior two quarters or had the contribution of net exports of goods and services not been 2.9%, real total GDP would have either declined or been flat for a third straight quarter. The Atlanta Fed’s early GDPNow projection on December 15, 2022, for real total GDP growth in Q4:2022 was down to 2.8% based on the latest data available. The table above also shows a historical comparison of the last expansion from June 2009 to February 2020. The earlier part of the expansion had slower real total GDP growth but had faster real private GDP growth. A reason for this difference is higher deficit-spending in the latter period, contributing to crowding-out of the productive private sector. Congress’ excessive spending thereafter led to a massive increase in the national debt that would have led to higher market interest rates. But the Fed monetized much of it to keep rates artificially lower thereby creating higher inflation as there has been too much money chasing too few goods and services as production has been overregulated and overtaxed and workers have been given too many handouts. The resulting inflation measured by the consumer price index (CPI) has cooled some from the peak of 9.1% in June 2022 but remains hot at 7.1% in November 2022 over the last year, which remains at a 40-year high. After adjusting total earnings in the private sector for CPI inflation, real total earnings are up only 0.9% in November 2022 since February 2020 as inflation has limited people’s purchasing power. Elevated inflation will continue until the Fed more sharply reduces its balance sheet to stop distorting market activity and there is a positive real federal funds rate target.  Just as inflation is always and everywhere a monetary phenomenon, high deficits and taxes are always and everywhere a spending problem. As the federal debt far exceeds U.S. GDP, and President Biden proposed an irresponsible FY23 budget and Congress never passed one, America needs a fiscal rule like the Responsible American Budget (RAB) with a maximum spending limit based on population growth plus inflation. If Congress had followed this approach from 2002 to 2021, the (updated) $17.7 trillion national debt increase would instead have been a $1.1 trillion decrease (i.e., surplus) for a $18.8 trillion swing to the positive that would have reduced the cost to Americans. The Republican Study Committee recently noted the strength of this type of fiscal rule in its FY 2023 “Blueprint to Save America.” And the Federal Reserve should follow a monetary rule.  Bottom Line: Americans are struggling from bad policies out of D.C., which have resulted in a recession with high inflation. Instead of passing massive spending bills, like passage of the “Inflation Reduction Act” that will result in higher taxes, more inflation, and deeper recession, the path forward should include pro-growth policies. These policies ought to be similar to those that supported historic prosperity from 2017 to 2019 that get government out of the way rather than the progressive policies of more spending, regulating, and taxing. The time is now for limited government with sound fiscal and monetary policy that provides more opportunities for people to work and have more paths out of poverty.

Recommendations:

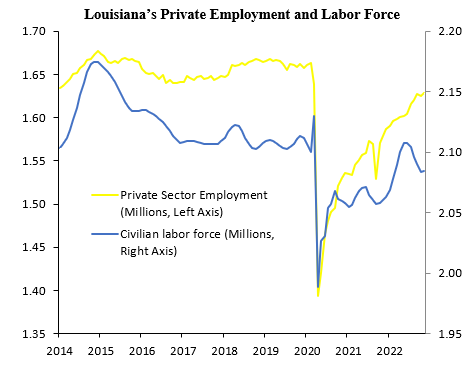

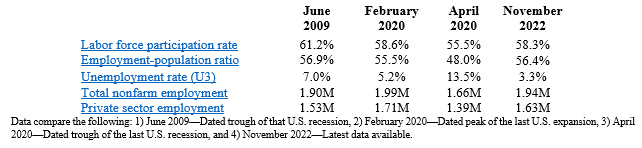

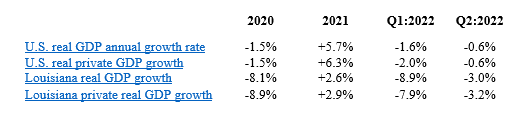

Key Point: Louisiana’s labor market looks okay with a 3.3% unemployment rate but the labor force has 15,617 (-0.7%) fewer people in it than pre-shutdown in February 2020 and private sector employment is 34,400 (-2.1%) below then, indicating a much weaker labor market and economy.  Labor Market: A job is the best path to prosperity as work brings dignity, hope, and purpose to people through life-long benefits of earning a living, gaining skills, and building social capital. The table below shows Louisiana’s labor market over time until the latest data for October 2022 by the U.S. Bureau of Labor Statistics.  The establishment survey shows that net total nonfarm jobs in the state increased by 3,800 jobs last month, bringing this to 55,900 jobs below the pre-shutdown level in February 2020. Private sector employment was up by 3,700 jobs and government employment rose by 100 jobs last month. Compared with a year ago, total employment was up by 49,200 (+2.6%) with the private sector adding 49,700 jobs (+3.1%) and the government cutting 500 jobs (-0.2%). The household survey finds that the civilian labor force rose by 840 people last month and is down 1058 people since February 2020, which results in the labor force participation rate of 58.3% being 0.3-percentage point lower than it was in February 2020 but well below June 2009 at the trough of the Great Recession. The employment-population ratio is 0.9-percentage point above where it was in February 2020. While the unemployment rate of 3.3% is substantially lower than the 5.2% rate in February 2020, a broader look at Louisiana’s labor market rather than this weak indicator shows that Louisianans still face challenges, especially compared with neighboring states based on several measures.  Economic Growth: The U.S. Bureau of Economic Analysis (BEA) recently provided the real (inflation-adjusted) gross domestic product (GDP) for Louisiana and others states. The following table shows how U.S. and Louisiana economies performed since 2020. The steep declines were during the shutdowns in 2020 in response to the COVID-19 pandemic, which was when the labor market suffered most. The decline in real GDP annualized growth in Q2:2022 of 3% was the 5th worst in the nation. The BEA also reported that personal income in Louisiana grew at an annualized pace of 5.8% (19th best) in Q2:2022 (tied +5.8% U.S. average).  Bottom Line: Louisianans gained jobs in November but continue to feel the costs of the shutdowns in 2020 and other restrictive policies that reduce opportunities for them to find well-paid jobs. Institutions matter to human flourishing in countries and states, which is floundering in Louisiana compared with many other states. The Fraser Institute recently ranked Louisiana 20th for economic freedom based on 2020 data for government spending, taxes, and labor market regulation. And the Tax Foundation recently ranked the Pelican State as having the 12th worst business tax climate. While the state has improved its tax code recently and lower taxes may happen soon from an expected budget surplus, this lack of economic freedom and poor business tax climate are contributing to a net outmigration of Louisianans to other states, which is a drain on the state’s economic potential now and in the future. State and local policymakers should work to reverse this trend by passing pro-growth policies.

Recommendations: In 2023, the Louisiana Legislature should provide the state’s comeback story by:

Those states that practice more free-market capitalism with limited government tend to have better economic performance, providing an economy and civil society with opportunities to help the neediest among us achieve long-lasting prosperity. Key points – Comparing institutional frameworks in states and their outcomes provides key factors that encourage thriving states, families, and entrepreneurs. – Measures of economic freedom and government burden are useful indicators of which states have growing economies and more jobs over time. – The results for these states demonstrate how institutions that encourage individual liberty, free enterprise, and civil society support prosperous outcomes, particularly in relieving poverty. – States ought to pursue policies that advance more of these lessons to provide a robust economy and flourishing civil society that will best help the neediest among us. Original post at TPPF.

Dec. 15, 2022 - 4:24 - Former chief White House Budget Office economist Vance Ginn addresses the nation's rising debt issue as the Fed continues to raise rates on 'Cavuto: Coast to Coast.'

Vance Ginn sits down with Newsmakers to discuss the battle against inflation and the rising interest rates the Fed is imposing yet again. He touches on major economic benchmarks and explains what the numbers are really showing. Watch here: https://www.youmaker.com/video/482a32b6-d37b-47bb-b6db-0ed3d975f04f   Is the flat income tax revolution underway across the states enough? No, but it must be advanced.

This extraordinary feat includes four states passing a flat personal income tax in 2022 after only four did over the last century. Now 14 states have or will soon have flat income taxes. But if you consider how the nine states without personal income taxes outperform, on average, the nine states with flat income taxes in economic growth, domestic migration, and nonfarm payroll employment over the last decade, more is necessary. While flattening income taxes is important, eliminating them is best. And this should be tied to spending restraint to avoid the infamous Kansas problem of excess spending while cutting taxes. The five states always with a flat income tax were Massachusetts (1917), Indiana (1965), Michigan (1967), Illinois (1969), and Pennsylvania (1971). The next four states initially with progressive income taxes before improving to a flat income tax were Colorado (1987), Utah (2007), North Carolina (2014), and Kentucky (2019). The four states that passed a flat income tax in 2022 were Idaho (starts in 2023), Mississippi (2023), Georgia (2024), and Iowa (2026). After a recent court decision, Arizona will also have a flat income tax in 2023 at the lowest rate in the nation at 2.5%. This will support greater economic growth as progressive personal income taxes disincentivize people to work and live in those states. This is happening in California, where even its wealthy citizens are fed up with sky-high personal income taxes that will worsen when the top marginal tax rate rises to 14.4% in 2024. According to the American Legislative Exchange Council’s 15th edition of the Rich States, Poor States report that compares the economic performance of the 50 states, the nine states already with a flat income tax rank mostly in the middle of the pack from 2010 to 2020. This includes an average overall ranking for those nine states of 24th based upon three key economic variables with average rankings of 23rd in state gross domestic product (GDP), 29th in absolute domestic migration, and 22nd in nonfarm payroll. The highest overall rankings for these states are Utah (2nd) and Colorado (6th), lowest are Illinois (43rd) and Pennsylvania (45th). States should seek better outcomes that ultimately help people flourish. The nine states without a personal income tax are Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming. These states have average rankings in ALEC’s report of 19th overall, 22nd in GDP, 14th in migration, and 21st in jobs. The highest overall rankings are Florida (3rd) and Washington (5th), with Texas (8th) and Tennessee (10th) also in the top 10, and lowest are Wyoming (41st) and Alaska (49th). Historically, the nine states with the highest personal income tax rates, including California (ranks 19th) and New York (36th), have underperformed in these economic measures and have dire outlooks ranking 48th and 50th, respectively, in ALEC’s report. Progressive, high-income tax structures produce undesirable outcomes, and states should work toward eliminating personal income taxes. Other taxes and policies matter. The Tax Foundation’s latest report on state business tax climates shows how other taxes influence business activity, and thus economic performance. States without a personal income tax or lower tax burdens overall rank the highest in business tax climate with Wyoming (1st), South Dakota (2nd), Alaska (3rd), and Florida (4th) leading the way. And those states with the highest personal income rates perform worst with California (48th), New York (49th), and New Jersey (50th) being last. What many of these states without personal income taxes tend to use to fund their spending are consumption-based taxes. The least burdensome form of taxation tends to be a flat final sales tax with the broadest base and lowest rate possible. Whatever you tax, you get less of it. Taxing consumption results in less consumption but more savings, which can support greater capital accumulation and economic growth while taxing the underground economy, such as drug dealers and undocumented workers. But the ultimate burden of government is not how much it taxes but how much it spends. Jonathan Williams, who is a co-author of the ALEC report, correctly noted, “There are nine states with no income taxes, and they spend substantially less per capita than states with an income tax.” When there’s already heavy headwinds imposed by policymakers in Washington and across many states, it’s time to build on the flat tax revolution by cutting or even freezing state budgets, strengthening state spending limits, and eliminating personal income taxes. Original post at EconLib.  The 2024–25 Conservative Texas Budget limits the state’s budget to be passed by the Legislature in 2023 so that the average taxpayer can afford it and historic tax relief can happen. Key points

Original post at TPPF.  In the last two decades, local property taxes in Texas have grown far faster than the average taxpayer’s ability to pay for them. Moreover, high property taxes are aggravating the housing affordability crisis by increasing the overall out-of-pocket cost of keeping a property. Therefore, we propose a buydown plan for property tax relief. Our simulation shows that the state can limit spending and use the resulting surplus state taxes collected to buy down school district maintenance and operations (M&O) property taxes until they are eliminated over the next decade. If, in addition, all local governments in Texas were to also limit spending and use the resulting surplus funds to reduce their property taxes, Texans could have substantial tax relief to mitigate this affordability crisis. Key Points

The latest inflation report reveals that inflation is slowing, but it remains at a 40-year high.

The stock market rose, as softer-than-expected inflation rate gave investors hope the Federal Reserve may not have to raise its target rate quite as fast. A 7.7-percent increase in prices over the last year shouldn’t make people hopeful. Many Americans can’t afford soaring living expenses, however, and the economy will worsen before there’s any relief. Adding to this struggle are inflation-adjusted average weekly earnings, which are down 4 percent over the last year, and have been declining for nearly two years. This deflating of the American Dream is the result of big-government policies, creating too much money chasing too few goods. Just the necessity of food is a struggle. Food prices at work and school are up 95 percent. Eggs are up 43 percent, and chicken, 15 percent. Gasoline to drive to the store is up nearly 18 percent and electricity, 14 percent, so even making meals at home can rock the budget. To cope with less purchasing power, Americans are not only saving less, they’re also accruing credit card debt, to a record high of nearly $1 trillion. Even in states with comparatively low cost of living, like Texas, people with full-time jobs can’t make ends meet for their families and are showing up at food banks for help. Unfortunately, the worst is yet to come. The Fed’s meager strategy for fighting inflation hasn’t included aggressively cutting its $8.6 trillion balance sheet. The balance sheet is only about 3.8 percent less than its record high in April 2022, after more than doubling during the pandemic. This overprinting of money affects many markets, as those dollars aren’t evenly distributed across the economy, resulting in distorted price signals. The Federal reserve adding assets to its balance sheet (by buying Treasury debt, agency debt, and mortgage-backed securities) kept interest rates artificially low. Those markets are starting to correct, as mortgage rates have risen to 20-year highs of around 7 percent. The Fed created the current inflationary situation (too much money), which was fueled by Congress’s deficit spending, and exacerbated by Biden’s overregulation (too few goods and services). Now, the false “boom” is busting. Hardworking families and entrepreneurs bear the brunt. To combat the problem it helped create, the Fed is raising its target federal funds rate, which has grown at the fastest pace since Paul Volcker was Chairman in the early 1980s. Volcker understood that the Fed’s balance sheet mattered most, which seems to be overlooked by the Fed and many economists today. The Fed’s hike of 75 basis points on November 2 brought the top of the target range to 4 percent, which was the fourth consecutive 75-basis-point hike, after rates were held at essentially zero for two years. The Fed signaled that it will slow target rate hikes to likely 50 basis points in December, pushing the top rate to 4.5 percent by the end of 2022. This would be the highest rate in 15 years. The Fed’s attempt to correct elevated inflation comes too late to avert the economic consequences of keeping the target rate too low for too long. As a result, Americans are suffering from persistent inflation, higher interest rates, and a prolonged, deeper economic recession. What should be done? We need pro-growth policies. The executive branch should focus on cutting regulations. Congress should prioritize making the Trump-era tax cuts permanent, cutting the corporate tax rate, and passing spending limits to help balance the budget. The Fed, the source of so much money mischief, should adhere to a monetary rule that will cut its balance sheet as much as possible, hopefully down to nothing. These pro-growth, liberty-oriented policies will unleash the economic potential of the productive private sector and get people back working again at well-paid jobs, while substantially reducing inflation. Big-government policies must end before they send us further down the road to serfdom. Our newly elected officials have a responsibility to prioritize fighting inflation, and restoring the American Dream. Originally posted at AIER. |

Vance Ginn, Ph.D.

|

RSS Feed

RSS Feed

Proudly powered by Weebly