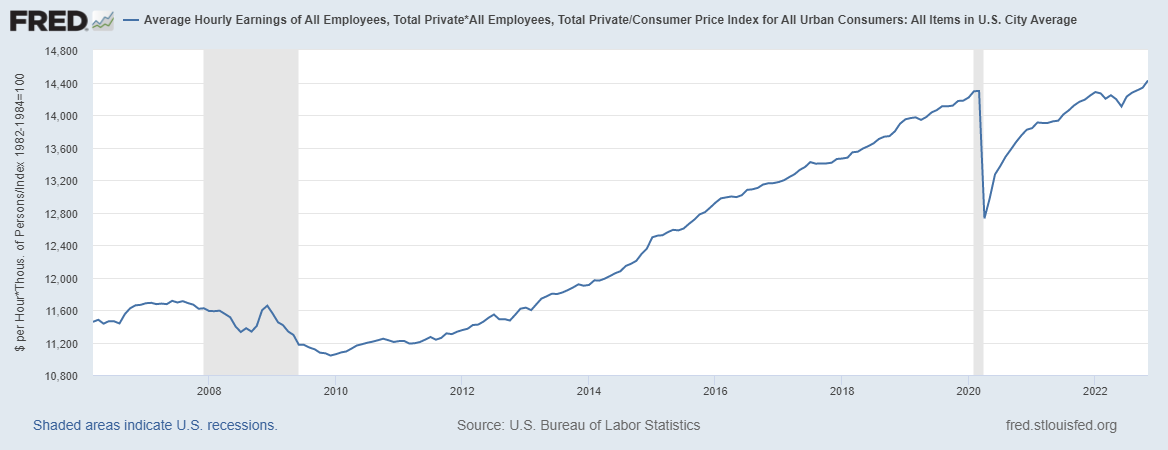

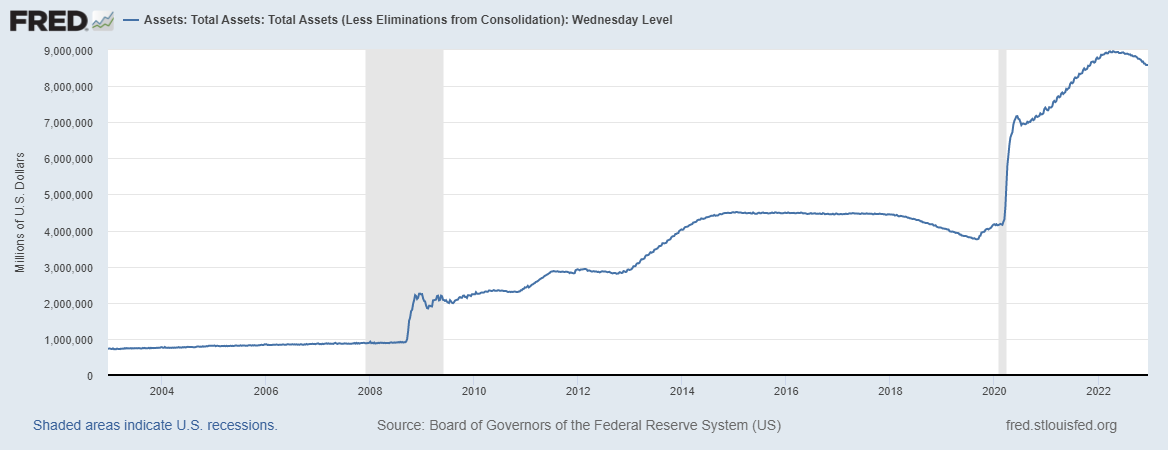

Key Point: We need pro-growth policies to unleash economic prosperity.  Overview: The irresponsible “shutdown recession” from February to April 2020 and subsequent government failures of excessive spending, regulation, and printing of money have led to a longer, deeper recession with high inflation that will have long-lasting consequences for many Americans’ livelihoods now and in the future. This includes excessive federal spending redistributing scarce private sector resources with deficit spending of more than $7 trillion since January 2020 to reach the new high of $31.4 trillion in national debt—about $95,000 owed per American or $250,000 owed per taxpayer. This new debt added fuel to the fire as the Federal Reserve monetized most of the new debt, leading to a 40-year-high inflation rates, substantially reducing our purchasing power even when accounting for increases in earnings. The inflated transitory boom continues to bust into a long, deep recession with high inflation, which hasn’t happened since Joan Jett and the Blackhearts was the top-ranked rock band in 1982. The failed policies of the Biden administration, Congress, and the Fed must be replaced with a liberty-preserving, free-market, pro-growth approach so there are more opportunities to let people prosper. Labor Market: The U.S. Bureau of Labor Statistics recently released the U.S. jobs report for November 2022. The establishment report shows there were 263,000 net nonfarm jobs added last month, with 221,000 added in the private sector. Interestingly, while there have appeared to be a relatively robust number of jobs created, a recent report by the Philadelphia Fed find that if you add up the jobs added in states in Q2:2022 there were just 10,500 net new jobs rather than more than 1 million initially estimated. This further indicates that the recession started earlier this year, likely in March. The official U3 unemployment rate increased to what remains a historically low rate of 3.7%, but challenges remain. These challenges include a 3.0% decline in average weekly earnings (inflation-adjusted) over the last year, a 0.8-percentage point lower prime-age (25–54 years old) employment-population ratio than in February 2020, and a 1.3-percentage-point lower labor-force participation rate with millions of people out of the labor force. Things look worse when you consider the household survey, which employment declined by 138,000 jobs last month and has declined in four of the last eight months for a total increase of just 12,000 jobs since March 2022 (when I would date the 2022 recession). This goes along with my warnings for months of a “zombie economy.” This includes “zombie labor” as many workers are sitting on the sidelines and others are “quiet quitting” while there’s a declining number of unfilled jobs than unemployed people to 4.3 million And that demand for labor is likely inflated from many “zombie firms,” which run on debt and could make up at least 20% of the stock market and will likely lay off workers with rising debt costs.  Economic Growth: The U.S. Bureau of Economic Analysis’ released economic output data for Q3:2022. The following provides data for real total gross domestic product (GDP), measured in chained 2012 dollars, and real private GDP, which excludes government consumption expenditures and gross investment.  The shutdown recession contracted at historic annualized rates because of individual responses and government-imposed shutdowns related to the COVID-19 pandemic. Economic activity has had booms and busts thereafter because of inappropriately imposed government COVID-related restrictions in response to the pandemic that severely hurt people’s ability to exchange and work. In 2021, the growth in nominal total GDP, measured in current dollars, was dominated by inflation, which distorts economic activity. The GDP implicit price deflator was up 6.1% for Q4-over-Q4 2021, representing half of the 12.2% increase in nominal total GDP. This inflation measure was up by 9.1% in Q2:2022—the highest since Q1:1981—for an 8.5% increase in nominal total GDP. This made two consecutive declines in real total (and private) GDP, providing a criterion to date recessions every time since at least 1950. Nominal total GDP was 7.3% and GDP inflation was 4.3% for the 2.9% increase in real total GDP in Q3:2022. But if inflation had been as high as it was in the prior two quarters or had the contribution of net exports of goods and services not been 2.9%, real total GDP would have either declined or been flat for a third straight quarter. The Atlanta Fed’s early GDPNow projection on December 15, 2022, for real total GDP growth in Q4:2022 was down to 2.8% based on the latest data available. The table above also shows a historical comparison of the last expansion from June 2009 to February 2020. The earlier part of the expansion had slower real total GDP growth but had faster real private GDP growth. A reason for this difference is higher deficit-spending in the latter period, contributing to crowding-out of the productive private sector. Congress’ excessive spending thereafter led to a massive increase in the national debt that would have led to higher market interest rates. But the Fed monetized much of it to keep rates artificially lower thereby creating higher inflation as there has been too much money chasing too few goods and services as production has been overregulated and overtaxed and workers have been given too many handouts. The resulting inflation measured by the consumer price index (CPI) has cooled some from the peak of 9.1% in June 2022 but remains hot at 7.1% in November 2022 over the last year, which remains at a 40-year high. After adjusting total earnings in the private sector for CPI inflation, real total earnings are up only 0.9% in November 2022 since February 2020 as inflation has limited people’s purchasing power. Elevated inflation will continue until the Fed more sharply reduces its balance sheet to stop distorting market activity and there is a positive real federal funds rate target.  Just as inflation is always and everywhere a monetary phenomenon, high deficits and taxes are always and everywhere a spending problem. As the federal debt far exceeds U.S. GDP, and President Biden proposed an irresponsible FY23 budget and Congress never passed one, America needs a fiscal rule like the Responsible American Budget (RAB) with a maximum spending limit based on population growth plus inflation. If Congress had followed this approach from 2002 to 2021, the (updated) $17.7 trillion national debt increase would instead have been a $1.1 trillion decrease (i.e., surplus) for a $18.8 trillion swing to the positive that would have reduced the cost to Americans. The Republican Study Committee recently noted the strength of this type of fiscal rule in its FY 2023 “Blueprint to Save America.” And the Federal Reserve should follow a monetary rule.  Bottom Line: Americans are struggling from bad policies out of D.C., which have resulted in a recession with high inflation. Instead of passing massive spending bills, like passage of the “Inflation Reduction Act” that will result in higher taxes, more inflation, and deeper recession, the path forward should include pro-growth policies. These policies ought to be similar to those that supported historic prosperity from 2017 to 2019 that get government out of the way rather than the progressive policies of more spending, regulating, and taxing. The time is now for limited government with sound fiscal and monetary policy that provides more opportunities for people to work and have more paths out of poverty.

Recommendations:

0 Comments

Leave a Reply. |

Vance Ginn, Ph.D.

|

RSS Feed

RSS Feed

Proudly powered by Weebly