|

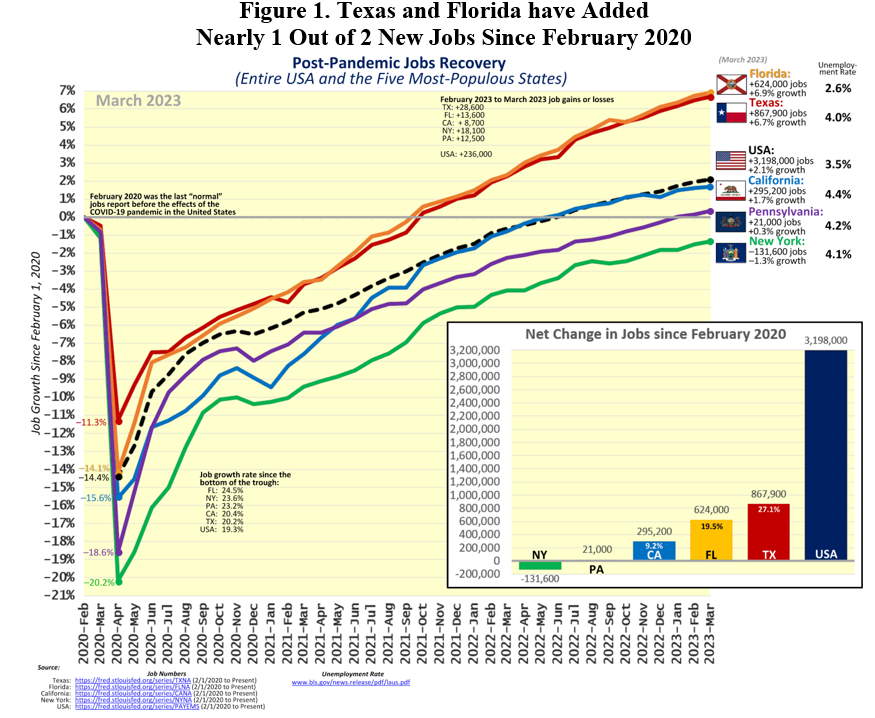

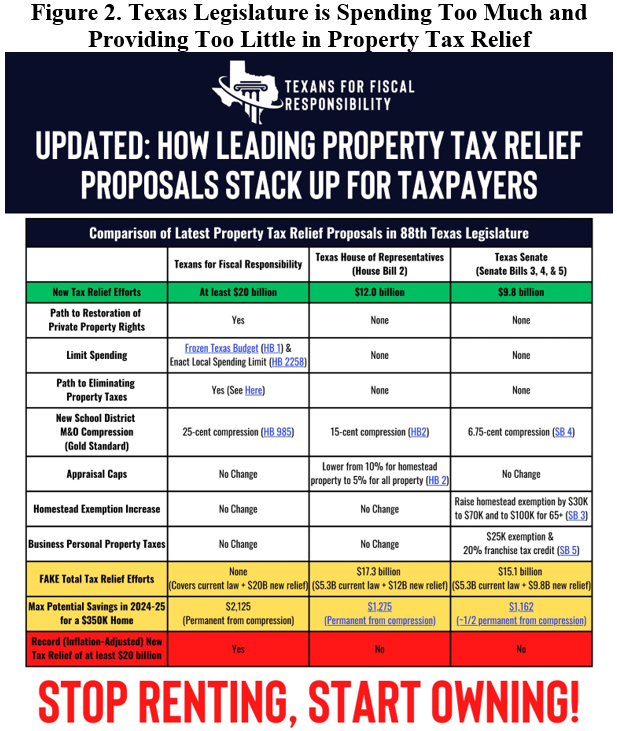

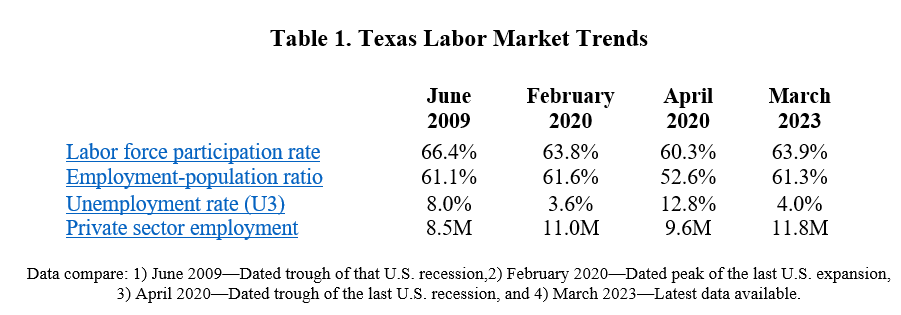

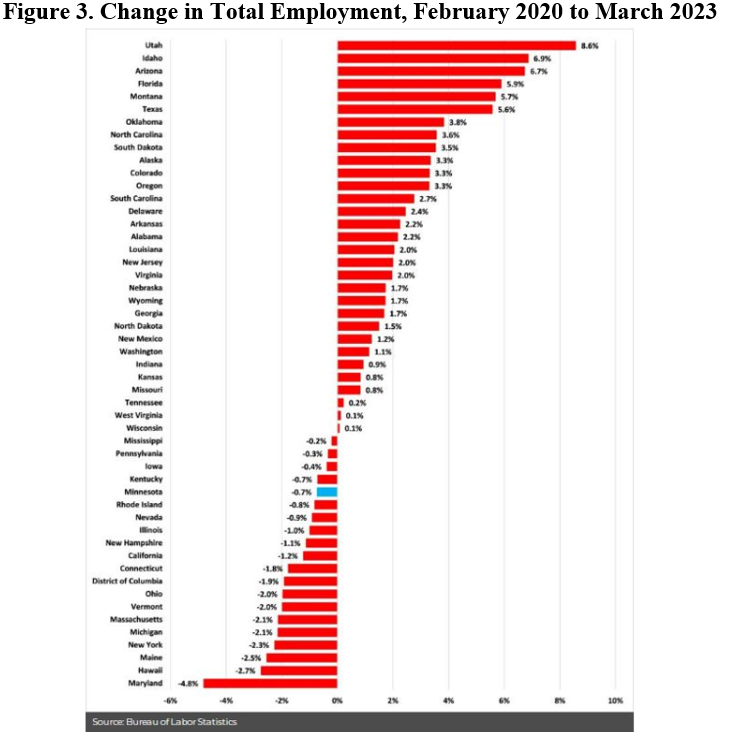

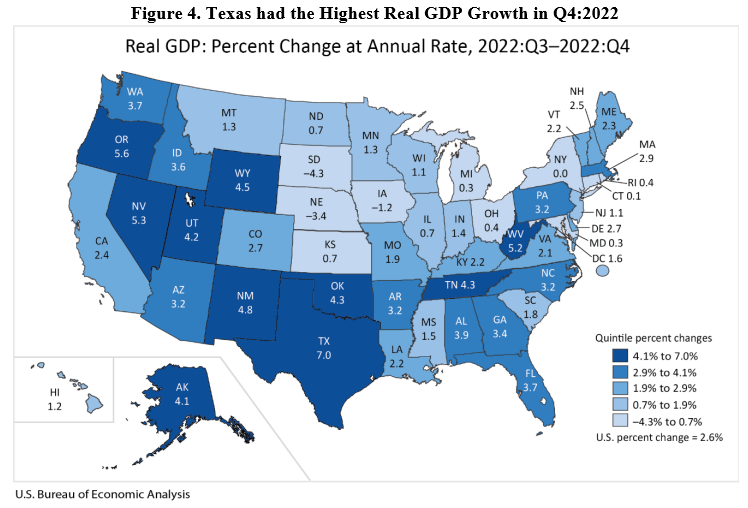

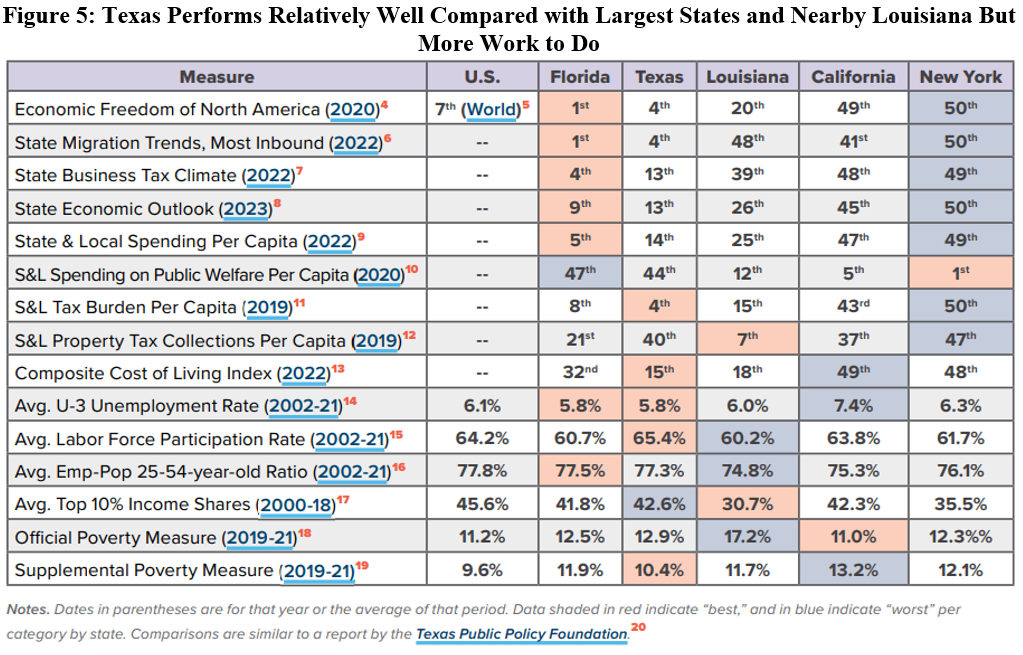

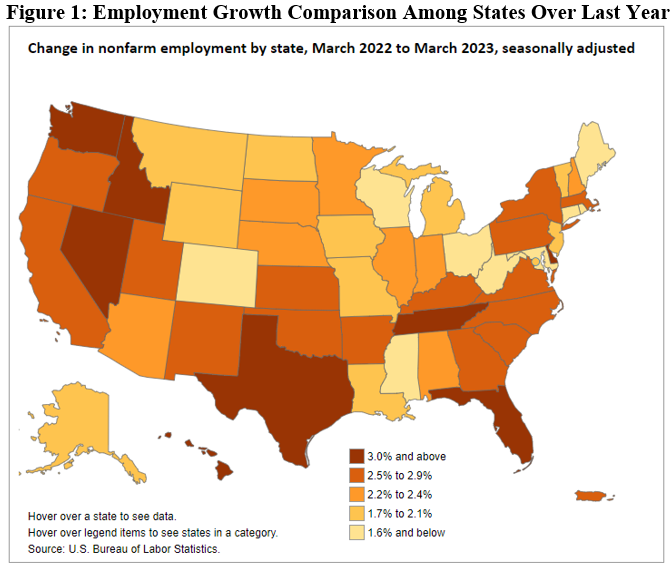

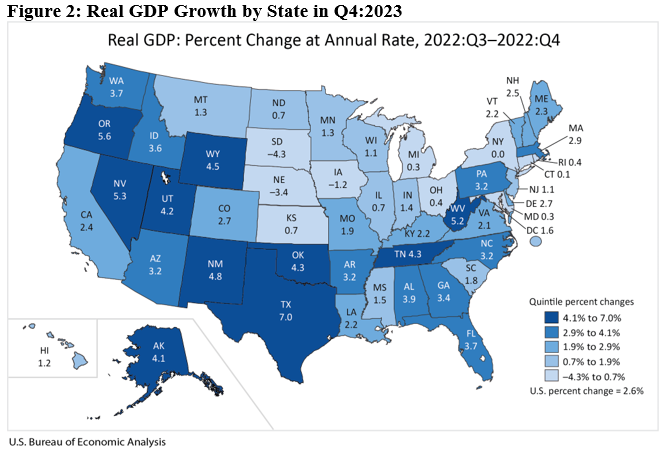

Key Point: Texas remains a leader in job creation over the last year (chart below by @SoquelCreek) and set employment records across the state (see Figure 1) but Texans who are struggling from an affordability crisis would benefit from less spending, taxes, and regulations.  Overview: Texas is a leader in the country’s economic recovery since the costly shutdown recession in Spring 2020. This includes reaching a new record high in total nonfarm employment for the 18th straight month, leading exports of technology products for 21 consecutive years, and being home to the most Fortune 500 companies in the country. The current 88th Texas Legislature is winding down as legislator are spending too much, providing too little in property tax relief (see Figure 2), throwing taxpayer money at corporate welfare, and wavering on passing universal school choice. There’s a historic opportunity to ensure taxpayers have a bright future, Texas must lead and there’s time to do it but they must act quickly.  Labor Market: The best path to let people prosper is free-market capitalism as it is the best system that supports jobs and entrepreneurship for more people to earn a living, gain skills, and build social capital. Table 1 shows Texas’ labor market for March 2023.  The establishment survey shows that net nonfarm jobs in Texas increased by 28,600 last month, resulting in increases for 34 of the last 35 months, to bring record-high employment to 13.8 million. Compared with a year ago, total employment was up by 575,100 (+4.3%)--third fastest growth rate in the country to Nevada (+5.0%) and Florida (+4.5%)—with the private sector adding 517,900 jobs (+4.6%) and the government adding 57,200 jobs (+2.9%). Figure 3 (h/t John Phelan) shows which states have created new jobs since February 2020, which red states are leading the way.  The household survey shows that the labor force participation rate and employment-population rate are now slightly higher than in February 2020, but the former is well below June 2009 at the trough of the Great Recession as there aren’t as many people in the labor force as a share of the working-age population. The state’s unemployment rate of 4.0% is higher than the U.S. rate of 3.5% but this is weak indicator as it’s highly volatile based on changes in the labor force. There is also continued declining inflation-adjusted average earnings in Texas. Economic Growth: The U.S. Bureau of Economic Analysis (BEA) reported the real gross domestic product (GDP) by state for Q4:2022 and 2022. Figure 4 below shows Texas had the fastest real GDP growth of +7.0% on an annualized basis to $1.92 trillion (above the U.S. average of +2.6% to $20.18 trillion).  For the third straight quarter in 2022, Texas had one of the fastest growth rates in the country. For all of 2022, Texas’ real GDP growth rate was +3.4%, which was the fifth highest. The BEA also reported that personal income in Texas grew at an annualized pace of +7.7% in Q4:2022 (ranked 15th highest and faster than the U.S. average of +5.3%) but slower than the robust +8.4% in Q2:2022 (ranked 6th best and above the U.S. average of +7.4%) as job creation and inflated income measures found their way across the economy. Personal income growth in 2022 in Texas was +5.3% making it the third fastest in the country (Idaho with +6.2% and Colorado with +5.4%) with the U.S. growth of +2.4%. Bottom Line: As Texans face an affordability crisis from high inflation and high property taxes and an uncertain future with the U.S. economy likely in a deepening recession, they need substantial relief to help make ends meet. Other states are cutting, flattening, and phasing out taxes, so Texas must make bold reforms to support more opportunities to let people prosper, mitigate the affordability crisis, and withstand destructive policies out of D.C. Figure 5 provides a comparison of the size of government, economic freedom, and economic outcomes among the four largest states and nearby Louisiana. While Texas does relatively well, there is much more to do for more liberty and prosperity.  Free-Market Solutions: In 2023, the Texas Legislature should improve the Texas Model by:

0 Comments

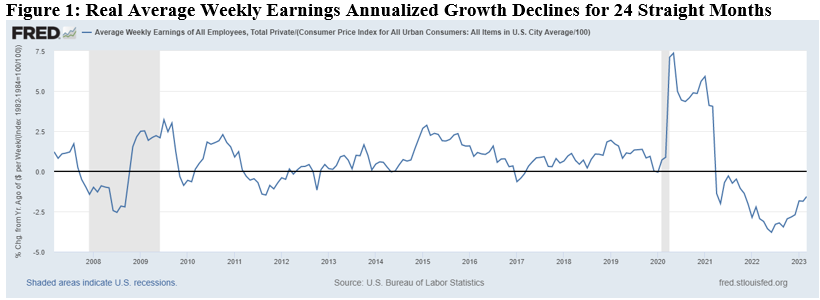

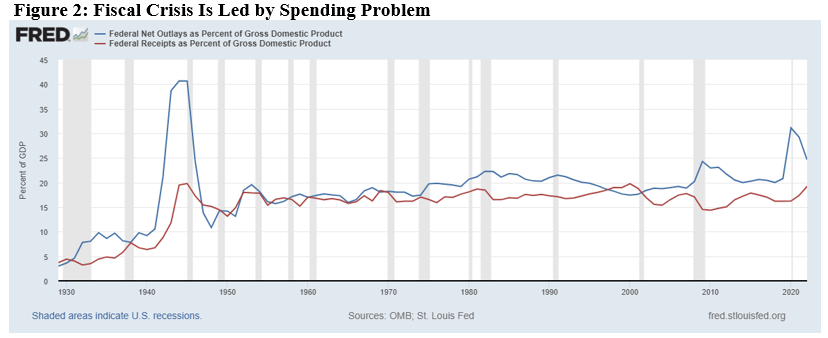

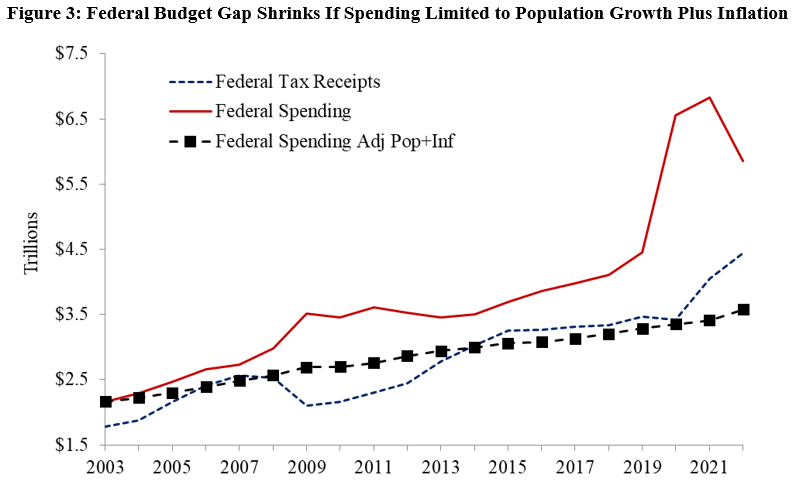

Key Point: Inflation-adjusted average weekly earnings year-over-year are down for 24 consecutive months and economic growth is anemic creating a stagflationary period at best or recessionary period at worst. The best way to let people prosper is free-market capitalism.  Overview: Government failures drove the “shutdown recession” and stagflationary period over the last three years that has plagued Americans, with more banking problems to come. This is fueled by the debt ceiling fight and likely elevate inflation for longer than many expected, with the only answers being less spending by Congress, less regulation by Biden administration, and less money printing by the Fed. The solution to these problems are pro-growth policies of shrinking government back to its constitutional roles. Labor Market: The Bureau of Labor Statistic recently released its U.S. jobs report for March 2023. The reports continue to be mixed with signs of strength though underlying weaknesses remain. The establishment survey shows there were +236,000 (+2.7%) net nonfarm jobs added in March to 155.6 million employees, which has increased by +4.1 million over the last year but just +3.2 million since February 2020 before the shutdowns. Over the last month, there were +189,000 jobs (+2.8%) added in the private sector and +47,000 jobs (+2.2%) added in the government sector. Most of the private sector jobs were added in the sectors of leisure (+72,000), private education and health services (+65,000), and professional and business services (+39,000), which the first two led over the last 12 months; retail trade (-14,600), construction (-9,000), manufacturing (-1,000), and financial activities (-1,000) had losses. Only retail trade (-15,200) declined over the last year. The household survey had another increase of +577,000 jobs to 160.9 million employed in March, which there have been declines in net employment in four of the last 12 months for a total increase of +2.6 million since March 2022 and +2.1 million since February 2020. The official U3 unemployment rate ticked down to 3.5% and the broader U6 underutilization rate fell to 6.7%. Since February 2020, the prime-age (25-54 years old) employment-population ratio is up by 0.2pp to 80.7%, prime-age labor force participation rate was 0.1-percentage point higher at 83.1%, and the total labor-force participation rate was 0.7-percentage-point lower at 62.6% with millions of people out of the labor force holding the U3 rate artificially low. Given some improvements, challenges remain for Americans as inflation-adjusted average weekly earnings were down -1.6% over the last year for the 24th straight month. Economic Growth: The U.S. Bureau of Economic Analysis’ recently released the 1st estimate for economic output for Q1:2023. Table 1 provides data over time for real total gross domestic product (GDP), measured in chained 2012 dollars, and real private GDP, which excludes government consumption expenditures and gross investment. Most of the estimates for Q4:2022 and growth in 2022 have been revised lower, providing more evidence that 2022 was a very weak economy if not a recession.  Economic activity has had booms and busts because of inappropriately imposed government COVID-related restrictions in response to the pandemic and poor fiscal and monetary policies that severely hurt people’s ability to exchange and work. In 2022, the first two quarters had declines in real total (and private) GDP, providing a reason to date recessions every time since at least 1950. While the second half of 2022 looked better, those two quarters were influenced by net exports and inventories that would have made the economy much weaker. For 2022, real total GDP growth is reported +2.1% year-over-year but measured by Q4-over-Q4 the growth rate was only +0.9%, which was the slowest Q4-over-Q4 growth during a recover on record. Then the anemic growth in Q1:2023 provides more reason that this is an extended recession or at least stagflation. The Atlanta Fed’s early GDPNow projection on April 28, 2023 for real total GDP growth in Q2:2023 was +1.7% based on the latest data available. If you consider the last expansion from June 2009 to February 2020, there was slower real private GDP growth in the latter period due to higher deficit-spending, contributing to crowding-out of the productive private sector. Congress’ excessive spending since February 2020 led to a massive increase in the national debt by nearly +$7.8 trillion that would have led to higher market interest rates. This is yet another example of how there is always an excessive government spending problem as noted in Figure 2 with federal spending and tax receipts as a share of GDP no matter if there are higher or lower tax rates.  But the Fed monetized much of the new debt to keep interest rates artificially lower thereby creating higher inflation as there has been too much money chasing too few goods and services as production has been overregulated and overtaxed and workers have been given too many handouts. The Fed’s balance sheet exploded from about $4 trillion, when it was already bloated after the Great Recession, to nearly $9 trillion and is down only about 3.5% since the record high in April 2022 after rising nearly $400 billion in March then down $180 billion in April 2023. The Fed will need to cut its balance sheet (total assets over time) more aggressively if it is to stop manipulating markets (see this for types of assets on its balance sheet) and persistently tame inflation, as may need deflation given the rampant inflation over the last two years. The resulting annual inflation measured by the consumer price index (CPI) has cooled some from the peak of +9.1% in June 2022 but remains at +5.0% in March 2023, which remains the highest since 2008 as do other key measures of inflation. After adjusting total earnings in the private sector for CPI inflation, real total earnings are up by only +2.3% since February 2020 as the shutdown recession took a huge hit on total earnings and then higher inflation hindered increased purchasing power. Just as inflation is always and everywhere a monetary phenomenon, deficits and taxes are always and everywhere a spending problem. David Boaz at Cato Institute notes how this problem is from both Republicans and Democrats. In order to get control of this fiscal crisis which is contributing to a monetary crisis, the U.S. needs a fiscal rule like the Responsible American Budget (RAB) with a maximum spending limit based on the rate of population growth plus inflation. If Congress had followed this approach from 2003 to 2022, the figure below shows tax receipts, spending, and spending adjusted for only population growth plus chained-CPI inflation. Instead of an (updated) $19.0 trillion national debt increase, there could have been only a $500 billion debt increase for a $18.5 trillion swing in a positive direction that would have substantially reduced the cost of this debt to Americans. The Republican Study Committee recently noted the strength of this type of fiscal rule in its FY 2023 “Blueprint to Save America.” And to top this off, the Federal Reserve should follow a monetary rule so that the costly discretion stops creating booms and busts.  Bottom Line: I expect stagflation will continue along with the a deeper recession this year given the “zombie economy” and the unraveling of the banking sector which will hit main street hard. Instead of passing massive spending bills, the path forward should include pro-growth policies that shrink government rather than big-government, progressive policies. It’s time for limited government with sound fiscal and monetary policy that provides more opportunities for people to work and have more paths out of poverty. There is some optimism with the House Republicans debt ceiling bill package but it’s got an uphill battle to become law with Democrats in the Senate and White House so more must be done.

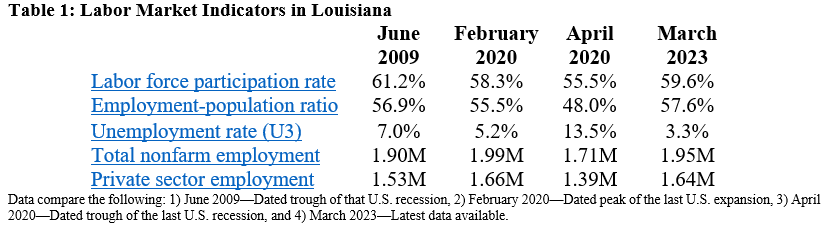

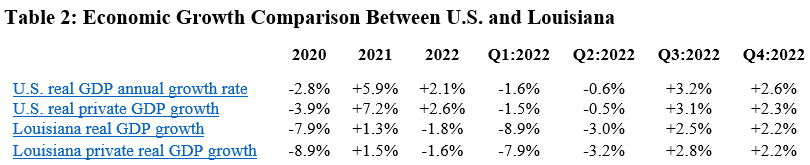

Recommendations: · Set a pro-growth policy path with less spending, regulating, and taxing at all levels of government. · Reject new spending packages that America cannot afford nor needs; pass the RAB instead. · Impose strict monetary rule with the Fed having a much smaller balance sheet and a much higher federal funds rate target until we End the Fed. · Enact return-to-work policies. Key Point: Louisiana’s economy has many weaknesses primarily because of poor policies hindering prosperity across the state, which is why there’s a need for the Pelican Institute’s “Comeback Agenda.” Louisiana’s Labor Market: Table 1 shows Louisiana’s labor market over time until the latest data for March 2023 from the U.S. Bureau of Labor Statistics.  The establishment survey shows that net total nonfarm jobs in the state increased by 4,400 jobs last month (+0.2%), bringing total jobs to 42,700 jobs below the pre-shutdown level in February 2020. Private sector employment was up by 4,800 jobs (+0.3%) and government employment declined by 400 jobs (-0.1%) last month. Compared with a year ago, total employment was up by 40,200 jobs (+2.1%), with the private sector adding 31,700 jobs (+2.0%) and the government adding 4,100 jobs (+1.3%). The household survey finds that the working-age population declined by another 1,045 people (-0.03%) last month, down 11,789 people (-0.3%) over the last year, and down 32,292 people (-0.9%) since February 2020. But the civilian labor force rose by 15,246 people (+0.7%) last month, 23,150 people (+1.1%) over last year, and 42,381 people (+2.0%) since February 2020. These figures result in a labor force participation rate of 59.6%, which is up from 58.3% since pre-shutdown but well below the 61.2% rate in June 2009 at the trough of the Great Recession. While the unemployment rate of 3.3% is substantially lower than the 5.2% rate in February 2020, a broader look at Louisiana’s labor market shows that Louisianans still face challenges (see Figure 1), as the population continues to decline and comparatively with neighboring states based on several measures.  Economic Growth: The U.S. Bureau of Economic Analysis (BEA) recently provided the real (inflation-adjusted) gross domestic product (GDP) in Q4:202 for Louisiana and other states in Figure 2.  Table 2 shows how U.S. and Louisiana economies performed since 2020. The steep declines were during the shutdowns in 2020 in response to the COVID-19 pandemic, which was when the labor market suffered most. The increase in real GDP of +2.2% in Q4:2022 ranked 26th in the country, resulting in an annual decline in economic output by -1.8% in 2022 which was the second worst in the country.  The BEA also reported that personal income in Louisiana grew at an annualized pace of +6.0% (ranked 32nd) in Q4:2022 (below +7.4% U.S. average). This resulted in personal income growth of 0.0% in 2022, ranking 50th of the states. Personal income per person in Louisiana increased by 0.8% to $54,622 last year, which ranked 42nd in the country and the increase was well below inflation. Bottom Line: Louisianans gained jobs in March, but those jobs are not paying enough to beat inflation or help expand investment in stagnant economy, resulting in costly stagflationary situation. Institutions matter to human flourishing, but they are too weak in Louisiana according to the Fraser Institute’s ranking of 20th for economic freedom and other measures. The state has improved its tax code recently and lower taxes may happen soon, but there’s a once-in-a-generation opportunity to ensure prosperity. The combination of spending restraint, not busting the spending caps, paying down debt, and putting money in the rainy day fund for future tax reforms and to hit the triggers for tax relief now are essential. These steps would help improve the state’s poor business tax climate, help curb the net outmigration of Louisianans, and help mitigate the 19.6% poverty rate that ranks second highest in the country. Which pro-growth policies be pursued? Refer to the Pelican Institute’s “Comeback Agenda” for policy recommendations related to the state’s budget and taxes, K-12 education, public safety, social safety nets and workforce development, technology and innovation, and reducing regulatory barriers.  With weeks left in the Texas Legislature’s 88th regular session, state lawmakers are working to enact the largest tax cut in the history of the nation’s second most populous state. In addition to billions of dollars worth of property tax relief, state legislators are moving to enact a number of innovative reforms before adjourning. Texas should unite to push these measures across the finish line.

Gov. Greg Abbott and leadership in the Texas House and Senate all want to pass a massive property tax relief bill but differ over the best approach. The Senate would like to raise the homestead exemption. The House, however, would rather cut the appraisal cap in half, taking it from 10% to 5%, and put more money toward rate compression than is called for by the Senate plan. Disagreements over these key details threaten to squelch planned relief. Lawmakers should work out a deal before the session ends. “Texas has a historic opportunity to provide much-needed property tax relief with nearly $33 billion in surplus for the current biennium plus extra taxpayer money available in the upcoming biennium, which should be returned to taxpayers,” noted Texas-based economist Vance Ginn, a senior fellow at Americans for Tax Reform. In addition to reducing property tax payments in a state that is home to the nation’s sixth highest average property tax burden, Texas lawmakers are also taking action to reduce regulatory costs. The House passed House Bill 2127 by a 92-55 vote on April 19. HB 2127, introduced by Rep. Dustin Burrows, R-Lubbock, and Sen. Brandon Creighton, R-Conroe, prohibits local governments from regulating products, activities, or industries in a manner that exceeds or conflicts with state law. Proponents of HB 2127, such as the National Federation of Independent Business, which represents small businesses, say it will rectify the patchwork of regulations that currently exist in Texas, which is making it more difficult for a business to operate and create jobs. “There are dozens of reasons why Texas is the best state in the country for business, but its convoluted, unpredictable, and inconsistent patchwork regulatory system is not one of them,” said James Quintero, policy director at the Texas Public Policy Foundation. Quintero says HB 2127 “brings some much-needed common sense to the system, unifying the rules for conducting business in a predictable, reliable, and efficient way to promote compliance.” Lastly, Texas lawmakers have the opportunity to make Texas the first state to ban taxpayer-funded lobbying by enacting Senate Bill 175. SB 175, introduced by Sen. Mayes Middleton, R-Galveston, would bar local governments and other political subdivisions from using taxpayer funds to hire contract lobbyists. Supporters of SB 175 note that contract lobbyists hired with taxpayer dollars frequently work against the interests of taxpayers. In previous sessions, for example, taxpayer-funded lobbyists have worked to kill property tax relief and block reforms that would have government spending grow at a more sustainable clip. This resistance to conservative priorities continues to this day, with taxpayer dollars currently being spent to lobby against Education Savings Accounts. That is why many view SB 175 as a root reform that will beget many other pro-growth reforms. Proponents of SB 175 believe it will help facilitate the future passage of tax relief, ESAs, greater spending restraint, and other pro-taxpayer reforms. As we saw with the criminal justice reform movement that started in Texas and has since swept the nation, enactment of a given reform in Texas makes it easier to pass that same proposal in other states. That’s because lawmakers in many state capitals look to Texas as a model for sound governance. As such, while passage of the aforementioned reforms would benefit Texans, their enactment will also have a positive effect nationally. Hopefully Texas lawmakers can capitalize on these opportunities before them in the remaining weeks of session and send these groundbreaking reforms to the desk of Abbott, who has made clear he wants to sign them. Grover Norquist is president of Americans for Tax Reform. He wrote this for The Dallas Morning News. Originally published at Dallas Morning News. This Week's Economy Ep. 6: NEW GDP Report, Debt Ceiling Bill, School Choice & State Budgets4/28/2023 In today's episode of "This Week's Economy," I discuss the latest GDP report, the House Republicans passing a new debt ceiling bill, School Choice, state budgets, social media bans, and more. Thank you for listening to the 6th episode of "This Week's Economy,” where I briefly share my insights every Friday morning on key economic and policy news at the U.S. and state levels.

Today, I cover: 1) National: Findings from the latest GDP report released yesterday (April 27th) and the debt ceiling bill passed by House Republicans; 2) States: Updates on Universal School Choice and budgets across states, especially Texas and Louisiana; and 3) Other: Bills circulating on restricting social media, and more. You can watch this episode on YouTube or listen to it on Apple Podcast, Spotify, Google Podcast, or Anchor (please share, subscribe, like, and leave a 5-star rating). For show notes, thoughtful economic insights, media interviews, speeches, blog posts, research, and more at my Substack directly in your inbox.  J.P. Morgan CEO Jamie Dimon is making international headlines with his recent claim that the current U.S. banking crisis is “not yet over, and even when it is behind us, there will be repercussions from it for years to come.” With Congress’s ongoing excessive spending and the Federal Reserve’s continued monetary mischief, Dimon’s prediction seems pretty safe.

Following the collapse of Silicon Valley Bank (SVB), Signature Bank and Silvergate shut down shortly thereafter. Depositors with uninsured amounts above the Federal Deposit Insurance Corporation’s (FDIC) insured amount of $250,000 at both banks withdrew large sums, forcing the banks to sell assets that had lost significant value. Silvergate voluntarily liquidated itself, while bank regulators forcibly closed Signature Bank. While the specific circumstances of SVB’s collapse may be unique, the factors contributing to its failure are not. SVB, Signature, and countless other banks that have yet to make headlines invested in risky assets such as environmental, social, and governance (ESG) initiatives and less risky assets such as government securities. These actions were fueled by government interventions in the economy that pumped excess liquidity into the market, creating an artificial “boom.” Since early 2020, Congress has added more than $7 trillion to the national debt, and the Federal Reserve helped keep interest rates artificially low. This resulted in a flood of liquidity that found its way into the banking system, which led to banks taking on those less profitable investments, particularly interest-rate-sensitive government bonds. But banks weren’t prepared for the Fed to change its interest rate tune, raising its target for the federal funds rate from 0 percent to the latest range of 4.75 percent to 5 percent, and for those assets to lose significant value so quickly. This made these banks take a huge hit to their balance sheet when they marked-to-market those assets, and they didn’t have sufficient capital in a fractional reserve banking system to fund deposit withdrawals, hence bank runs. Now, we’re witnessing the beginnings of the inevitable bust that follows a prolonged “boom” fueled by government actions that just redistributed resources while distorting markets. Perhaps the worst part in all of this is that the Treasury, Fed, and FDIC are creating moral hazard for banks by insuring many deposits at big, “systemically important” banks. This has created a shift of deposits from smaller regional banks to bigger banks, given this guarantee for now. Therefore, there’s more reason for bigger banks to take on more risks with this backstop and flood of new deposits at the expense of smaller banks and the economy. To make matters worst, the Fed recently added even more liquidity to the market. After reducing its balance sheet by about $700 billion from its peak of $9 trillion in April 2022, the Fed added $400 billion to provide loans to financial institutions. Its balance sheet is now down about $100 billion since then to $8.6 trillion, or only 4.4 percent below its record high last year, when it should be down substantially more to get ahold of inflation. The Fed’s balance sheet provides a good indicator of inflation, which has started to improve, but including the aberrations in the Fed’s balance sheet and underlying inflationary indicators in the food and services sectors, inflation could easily stay elevated at a much higher rate than the Fed’s preferred 2 percent average for much longer. Adding to the pressure on the banking sector includes how the Atlanta Fed’s GDPNow estimate for inflation-adjusted GDP in the first quarter of 2023 is only 2.5 percent (and Blue Chip consensus estimate is 1.5 percent) as of April 14. This is after less than 1 percent growth from the fourth quarter of 2021 to the fourth quarter of 2022, which is the slowest growth during a year of recovery in decades. This will exacerbate problems at banks if Americans can’t pay their bills. And we’re likely to see even higher interest rates soon, even though the Fed expects to raise rates just one more time this year. Based on the well-respected Taylor rule, which calculates a federal funds rate target based on inflation and output gaps, the Cleveland Fed’s Taylor rule utility suggests at least a 6 percent federal funds rate target. This would further devalue the government securities on banks’ balance sheets. So strap up, Americans, as we’re in for a bumpy ride in the banking sector and overall economy. Only by allowing people to exchange freely with limited government interference that simply sets the rules of the game but is a referee thereafter, not a participant, can we better avoid these boom and bust cycles in the banking sector and across the economy that threaten our freedom and prosperity. A big part of this will be to unleash the banking sector from excessive regulations like those imposed by Dodd-Frank after the financial crisis. There should also be an effort to not increase the FDIC’s insured amount by $250,000, as depositors should also take losses if they’re not doing their due diligence to research where they deposit their funds. And there should be support for increasing capital requirements by banks in the marketplace rather than policy avoiding some of the problems with fractional reserve banking. Finally, the Fed should be led by a monetary rule, like the Taylor rule, and Congress by a fiscal rule, like the Responsible American Budget, to remove the discretion that plagues our economic activity and future. If not, there will be many more “booms” and busts and many more failures from government actions over time. We must let free people succeed and fail, as failure is essential for us to learn lessons, or we will keep making the same mistakes. But we should be eliminating government failures by ultimately shrinking government and ending the Fed. Originally published at Econlib. In Let People Prosper episode #41, I talk w Dan Mitchell, Ph.D., about the need government spending limits, benefit of flat tax revolution, Fed's booms and bust cycles, and more to let people prosper. On today's episode of the "Let People Prosper" show, which was recorded on March 24, 2023, I'm thankful to be joined by Dr. Dan Mitchell, President of the Center for Freedom and Prosperity and blogger at International Liberty.

We discuss: 1) Lessons from history on government spending and why strong spending limits are needed at every level of government; 2) Issues with the Fed creating artificial cycles of booms and busts; and 3) Reasons to be optimistic about the flat tax & and school choice revolutions happening in states across the country. You can watch this interview on YouTube or listen to it on Apple Podcast, Spotify, Google Podcast, or Anchor (please share, subscribe, like, and leave a 5-star rating). Dan Mitchell’s bio:

For show notes, thoughtful economic insights, media interviews, speeches, blog posts, research, and more, check out my personal website and subscribe to my Substack newsletter where you can get every episode in your inbox.  ATR Senior Fellow Vance Ginn provided remarks at the Tax Day press conference at the House Triangle. Video of Ginn’s remarks can be viewed here. Ginn said: “It is often said that we don’t have a revenue problem, we have a spending problem. And that’s true. But also here on Tax Day, we have a tax problem. What we really need is for free market capitalism, which is the best path to let people prosper, to be able to flourish again. For people to get jobs and higher wages so they could pay for the higher inflation that’s come out of the Biden administration. And it’s just one thing after another. The latest account of this was the Inflation Reduction Act which does no such thing. It continues to raise inflation, raises the debt, and the latest estimates on this show that it will be about four times higher than what the CBO reported just last year. And a lot of this has to do with the tax credits for electric vehicle batteries, which are going to cost nearly $200 billion plus over time. This is another way that they’re infiltrating the overall size of the government through our economy throughout our lives. And fortunately, we have another way that we should go, that’s led by a lot of states that are leading the sustainable state budgets across the nation, that they should look at by spending less, and finding ways to provide tax relief and regulatory reform.“ Originally published Americans for Tax Reform. This Week's Economy Ep. 5: LATEST On Debt Ceiling, Rich/Poor States, Inflation Recession Act & More4/21/2023 In "This Week's Economy" episode 5, I discuss the latest news on the federal debt ceiling, findings from ALEC's "Rich States, Poor States" report, and exciting personal updates from this past week. Thank you for listening to the fifth episode of "This Week's Economy,” where I briefly share my insights every Friday morning on key economic and policy news at the U.S. and state levels. Today, I cover:

There's a lot of talk about the harms of social media on teens. Notable experts on both sides of the issue struggle to reach consensus. But state lawmakers are moving ahead with legislation to ban teens from social media.

The issue is, even if we assume the worst, a ban is a short-term fix to a potentially longer-term problem. Worse, it will likely do more to avoid dealing with teens’ underlying problems by taking control away from parents. And it could shortchange teens of many benefits online for education, networking, and more. If these issues are truly due to social media, when teens turn 18 and become “legal adults,” the issues will continue. The only difference a ban will make is that when teens become adults, and move away to start their lives, they won't have their parents to guide them online. They’ll have missed out on the opportunity to have productive discussions about safe practices with their parents. Despite what legislators are claiming, bans aren’t a pro-parent approach. Legislation to ban minors from social media gives the government (politicians and bureaucrats) the power to decide what’s best for children. And as usual, it's set to do a poor job of it. Earlier this year, Utah became the first state to ban teens from social media. The pair of bills ban teens under 16 completely and impose heavy-handed restrictions for sites allowing teens 16 to 18. Those restrictions include state-mandated curfews, intrusive age verification, punitive fines on companies with sites subjectively considered to be too appealing, and a presumption that any harm a child experiences is the result of social media. Parental consent is required for teens 16 to 18 to create an account, but that’s the end of a parent’s input into what they want for their teen. Now Texas, Arkansas, and other states are following suit. While legislators praise these bills as a solution to the mental health crisis facing teens, these provisions don’t address the underlying problems from many factors. Adding to the debate about whether social media is a significant cause of depression, experts are also grappling with how to reduce cyberbullying, curb exploitation, and protect teens from predators online. State efforts have done more to gloss over the problems teens are facing in the name of parental choice, missing opportunities to address specific issues and avoiding the unintended consequences of such actions. What’s more, the specifics in these bills, like state-imposed curfews and civil penalties, constitute a draconian approach that removes parents from choosing what’s best for their kids. Rather than banning teens from engaging in our connected world, we should separate the concerns into actionable items. Experts, stakeholders and parents alike should be given time to propose solutions with meaningful input that prepare teens to safely and responsibly enter the technology-integrated world. The hard part, of course, is reaching a consensus. To some, that’s why an all-out ban on allowing teens on the Internet would do the trick. But that would ignore the reality that teens will one day become adults and find themselves unequipped to contend with an online world, less productive, and more at risk of the concerns given for bans. It also takes the power out of the hands of parents, who are the ones best positioned to find what’s best for their kids, and puts it in the hands of bureaucrats. Government meddling in the parent-child relationship rarely works well, and there’s little reason to believe this time will be different. That goes for Utah, Texas, Arkansas, and any other state that tries to help kids by disempowering parents. If the warning signs are true, and social media is creating all the harm talked about in the news, we can’t simply ban the problems away. We’ll need to address them head-on with solutions that balance liberty, free speech, privacy, and parenting. Without these, we will fail to set up the next generation for offline and online success. Originally published at The Center Square. Commentary: States Must Join School Choice Revolution or Have Students and Economies Be Left Behind4/20/2023  The school choice revolution in the form of universal ESAs is sweeping the nation. This is extraordinary news for students, parents, teachers, and the economy.

Florida recently became the fourth state to adopt universal school choice in 2023. Earlier this year, Iowa, Utah, and Arkansas joined the rebellion against “public” school monopolies by passing universal school choice after West Virginia and Arizona ignited the revolution last year. There are now more than 10 states with education savings accounts (ESAs), and more likely coming soon. But Texas, Louisiana, Ohio, Alabama, and other states must follow their lead or have their students and economies be left behind. Although there are still naysayers slowing progress, the tide for school choice is growing as more parents and teachers are persuaded that school choice empowers them and their students. But an often overlooked benefit of school choice is it supports a stronger economy. Evidence shows that school choice is connected to improved student outcomes, increased teacher pay, and growing economic opportunity, to name a few of its benefits. School choice’s positive effects on these measures counter the problems in the “public” school system, which is an oxymoron. “Public” schools can exclude students, which a public good can’t do. Also, any positive benefit of this so-called “public good” is questionable at best, given declining test scores and long waiting lines for charter schools. More accurately named, government schools are funded by taxpayers and operated by government employees. As the only “free” option and a monopoly in states without school choice, government schools have little incentive to improve the flawed one-size-fits-few approach. This also contributes to many high-quality teachers being underpaid. Government schools have few reasons to efficiently manage funds because they keep getting more taxpayer money regardless of their outcomes. This helps explain why too much money goes to over-paid administrators instead of teachers, and taxpayers don’t get what they pay for regarding academic and work outcomes. Taxpayers pay about $16,000 per student per year, and that continues to increase over time even after adjusting for inflation. And yet, our students are underperforming academically, falling behind kids in other countries. These outcomes were exacerbated by school shutdowns during the pandemic that left students even less equipped, but this has been a longer-term trend. More school choice is needed to motivate government schools to stop promoting mediocrity. In states like Arizona, where all students above the age of five who live in the state are allotted the same amount of funds, parents of all types now have a range of options, no matter their demographic or socioeconomic status. School choice is finally letting free markets, meaning free people, work in an arena that’s been monopolized by the government for too long. Yes, taxpayers would still fund ESAs. But until states decide to get out of the schooling market, the next best alternative is to allow competition whereby the dollars follow the child instead of to a system. In states like Florida with ESAs, parents can vote with their dollars on the best schooling options for their children, forcing all schools, including government schools, to stay competitive if they hope to attract and keep students by providing the best educational outcomes and extracurricular activities. Giving families more freedom to choose schools, tutoring, and other resources for their unique kids will better equip them to perform better academically and in their careers. Instead of most students — and almost all underprivileged students — being shuffled through the same one-size-fits-few government schooling system, ESAs allow students to flourish into well-rounded adults, leading to better careers, a more productive workforce, and a faster-growing economy. The positive economic ripple effects of a society with more access to better education are myriad. More educated societies tend to experience less crime, decreasing burdens on public services and increasing social trust, which is crucial for the economy. Additionally, more education is linked to higher incomes and improved health. These reduce the number of people in poverty, which reduces the number of people dependent on safety nets funded by taxpayer money, thereby reducing government spending and taxes, resulting in even better economic outcomes. All these elements are conducive to happier, healthier people with more means to prosper, produce, and innovate, which in many ways is the bedrock of a better economy and livelihoods. With more than 10 states providing the option of ESAs, including four states providing universal ESAs this year, why not take it to all 50? Texas, Louisiana, Ohio, Alabama, and others ought to be next or risk their students and economies being left behind. Originally posted at the Daily Caller.  Budgeting responsibly is key to Louisiana’s Comeback Agenda, and Pelican’s Chief Economist, Dr. Vance Ginn, has released a plan to rein-in state spending. Check out the proposed Responsible Louisiana Budget, below. This plan gives Louisiana a competitive advantage and is similar to those used in other states, like Texas and Florida, limiting the amount of funding appropriated at the beginning of each fiscal year, which has made lower taxes possible. Originally posted at Pelican Institute.  Louisiana doesn’t exist in a vacuum, and neither does opportunity. When it comes to the harsh reality of attracting entrepreneurs, creating new jobs and keeping our kids and grandkids home, Louisiana must reckon with the reality that we’re competing against other states in a national — and global — race for a brighter future.

That’s why Louisiana’s economic environment matters, and why eliminating the state’s income tax is so critical — no matter how difficult it might be — before more employers and families flee our state. Naysayers try to shoot down reforms with scare tactics, as if it’s a zero-sum game in which tax cuts and a strong state can’t coexist. That’s why taking a holistic view of the state’s tax and budget policies is necessary. Eliminating the state’s income tax doesn’t have to mean massive cuts or a big tax swap. The Pelican Institute has proposed a plan to flatten personal income taxes, phase them out using extra taxpayer dollars collected above a stronger spending limit and budget responsibly to meet the needs of the state. When we’re talking about taxes, don’t forget whose money it is. Those are hard-earned dollars that belong to Louisianans, and taxes leave them with less money in their pocket for putting food on the table, gas in their tanks and capital for starting a business. Is it any wonder that so many Louisianans leave for states where they can keep more of their money? When families gather around their kitchen table or businesses look at their balance sheets, take-home pay makes a difference. That’s why Louisiana should phase out income taxes as soon as possible. This is fundamental to ensuring that Louisiana can compete with our neighbors, attract and retain talent and become an economic powerhouse. This is the comeback story we can write together. Originally published at The Advocate.  The hearing is scheduled for today at 10 am ET at Longworth House Office Building: Hearing on the U.S. Tax Code Subsidizing Green Corporate Handouts and the Chinese Communist Party. Below is the video of the full hearing (my statement starts at time 27:30 with other comments throughout the 4-hour-long hearing). And below that is my written testimony based on this recent research on The Inflation Reduction Act's Costly New Tax Credits for Electric Vehicle Batteries and the policy brief. In Let People Prosper episode #40, I talk with Max Gulker, Ph.D., about whether Big Tech is a monopoly, FTC's overreach with regulations, & benefits of network effects to let people prosper. On today's episode of the "Let People Prosper" show, which was recorded on March 21, 2023, I'm thankful to be joined by Dr. Max Gulker, Senior Policy Analyst at Reason Foundation.

We discuss:

Dr. Gulker’s bio and other info (here):

Louisiana’s budget at the beginning of fiscal year 2023 was $47 billion, which is an increase of 63 percent over the last decade. With a state population of 4.6 million, and shrinking, this is a spending burden of more than $10,000 per person. While nearly half of the money in the state budget comes from the federal government, Louisiana’s taxpayers are still on the hook for the total. This growth in state spending is unsustainable given the lack of growth in the state’s economy and a history of net outmigration. This report offers an overview and brief history of Louisiana’s operating and capital budgets and outlines how the state can begin to create a more responsible, sustainable budget over time that remains adaptable to the needs of citizens. Originally published at Pelican Institute. This Week's Economy Ep. 4: TRUTH On Inflation, Real Wages, Housing Market, TX Senate Budget, & CBDC4/14/2023 In "This Week's Economy" Ep. 4, I talk about new CPI inflation report, slowing housing market, Texas Senate Budget & tax relief efforts, school choice, & threats of central bank digital currency. Today, I cover:

An Overview

In Let People Prosper episode #39, I talk with Daniel Erspamer, CEO of Pelican Institute in Louisiana, about LA's economic issues, need for tax and budget reforms, and ways that let people prosper. Thank you for listening to the Let People Prosper Show podcast and for reading the newsletter for show notes and key economic insights.

On today's episode of the "Let People Prosper" show, which was recorded on March 31, 2023, I'm thankful to be joined by Daniel Erspamer, CEO of the Pelican Institute for Public Policy in Louisiana. We discuss the Pelican Institute’s “Louisiana’s Comeback Agenda” which includes:

Please like this video and subscribe to the channel if you enjoyed this podcast! Research: The Inflation Reduction Act's Costly New Tax Credits for Electric Vehicle Batteries4/10/2023  Executive Summary The U.S. Congress passed and President Biden signed into law the so-called “Inflation Reduction Act” (IRA) in August 2022. The IRA includes many provisions which are now estimated to cost $1.2 trillion over a decade per Goldman Sachs’ more recent analysis compared with the Congressional Budget Office’s (CBO) initial estimate of $391 billion. Part of this substantially higher estimated cost is because of the new cost estimates for tax credits for electric vehicle (EV) battery cells and modules manufactured in the U.S. Instead of the initially estimated cost of $30.6 billion by the CBO, new estimates based on more precise projections and growth in the EV market indicate that this could be as high as $196.5 billion (540% higher than initially estimated) per the Mercatus Center and Goldman Sachs. This higher estimate appears more accurate than the original CBO estimate given the large increase in the EV market and the expanding use of these tax credits. Given that the cost of these subsidies passed by Congress and communicated to the public appears to be substantially undervalued, the CBO and other nonpartisan agencies and committees responsible for providing Congress with accurate revenue estimates and sound economic analysis should reexamine their calculations. Originally published at Americans for Tax Reform.  A new report by Dr. Vance Ginn, senior fellow at The James Madison Institute and president of Ginn Economic Consulting recommends that the state continue to limit the burden of government spending. The Conservative Florida Budget (CFB) sets a maximum threshold in all funds appropriations for FY 2024 of $116.2 billion. This maximum threshold is based on the 5.5% rate of the 3-year average of population growth plus inflation over the last three years from 2020 to 2022, which reasonably represents the average taxpayer’s ability to pay for government spending. “Legislators should use the CFB as a guide this session. Given the economic headwinds from the poor fiscal and monetary policies out of D.C. contributing to elevated inflation and risks of a deep recession along with past state budget excesses, the Legislature should pass a budget well below the CFB, similar to the Governor’s budget. Doing so will ensure a conservative budget that will help keep more money in taxpayers’ pockets through larger tax relief, so families and entrepreneurs have the most opportunities to flourish.” — Dr. Vance Ginn, Senior Fellow, The James Madison Institute; President, Ginn Economic Consulting. Originally published by James Madison Institute. This Week's Economy Ep. 3: TRUTH About New U.S. Jobs Report, Banking CRISIS Effects, & State Actions4/7/2023 In "This Week's Economy" Ep. 3, I note the weaker labor market in the latest U.S. jobs report, the continued banking crisis issues, and state actions in Texas and Louisiana. Today, I cover:

You can watch this episode on YouTube or listen to it on Apple Podcast, Spotify, Google Podcast, or Anchor (please share, subscribe, like, and leave a 5-star rating).

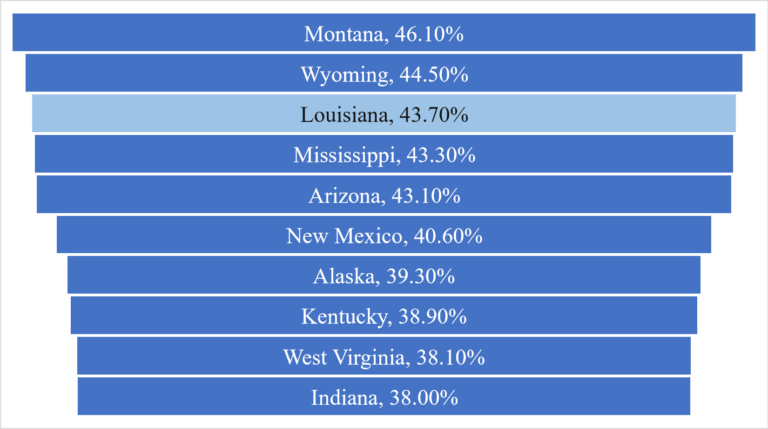

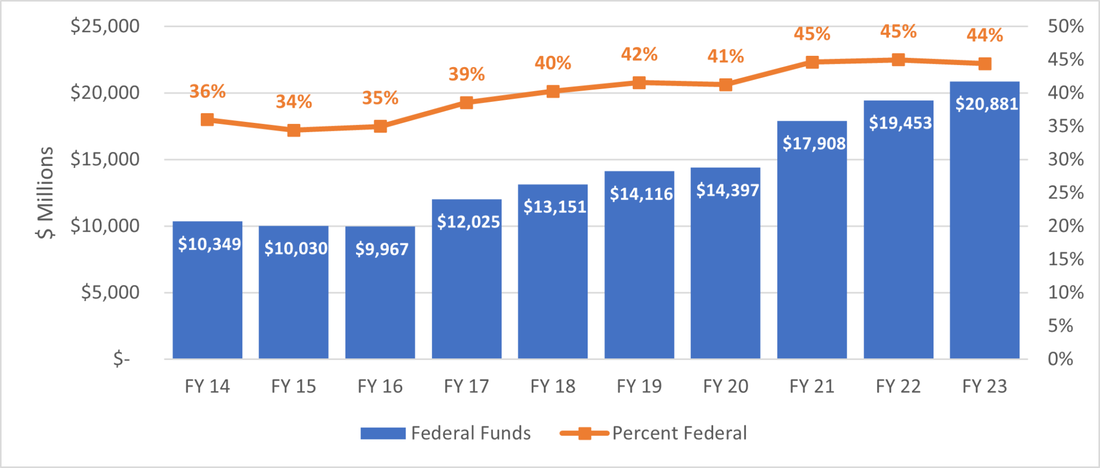

Louisiana’s state government is the third most dependent state on federal funding. This is according to a report recently released by WalletHub that shows state rankings, with Alaska and Wyoming coming in at first and second. This follows another report release by the Tax Foundation that also ranks Louisiana as the third most dependent on federal funds, with only Montana and Wyoming ahead.  This trend doesn’t appear to be getting any better. In 2014, federal funding comprised just 36% of the state’s total budget, whereas today, that percentage rises to 44%. The substantial increase in Louisiana’s use of federal funds from 2016 to 2017 is primarily due to Medicaid expansion. This program expanded the number of individuals eligible to receive Medicaid, and therefore increased the amount of money in the state’s general fund needed to match the additional federal funding. The match rate ranges from 30% to 40% per year based on personal income in the state. Disaster-related recovery has also contributed to the increased use of federal funds. Beginning in 2020 and 2021, Congress sent a large amount of federal funds due mostly to the COVID-19 pandemic response. There were also two major hurricanes, Laura and Ida, and numerous smaller hurricanes that also occurred in those fiscal years, which prompted an additional influx of federal funding from FEMA, HUD, and other agencies. Every program that is either partially or fully funded by the federal government comes with restrictions on its use – the “strings attached.” The substantial increase in Louisiana’s use of federal funds from 2016 to 2017 is primarily due to Medicaid expansion. This program expanded the number of individuals eligible to receive Medicaid, and therefore increased the amount of money in the state’s general fund needed to match the additional federal funding. The match rate ranges from 30% to 40% per year based on personal income in the state. Disaster-related recovery has also contributed to the increased use of federal funds. Beginning in 2020 and 2021, Congress sent a large amount of federal funds due mostly to the COVID-19 pandemic response. There were also two major hurricanes, Laura and Ida, and numerous smaller hurricanes that also occurred in those fiscal years, which prompted an additional influx of federal funding from FEMA, HUD, and other agencies Every program that is either partially or fully funded by the federal government comes with restrictions on its use – the “strings attached.”  Most of the federal funding is used for social safety-net programs. Louisiana has the highest poverty rate in the nation, with nearly 20% of the population in poverty and even more on at least one safety-net program. State and local spending on these programs create an annual burden of nearly $3,000 per person.

To reduce the state’s dependence on federal funds for large line-items such as social safety net programs, the state must empower more individuals to realize their own self-sufficiency and ability to flourish. Work must once again become a priority. WalletHub’s report also compared states using their gross domestic product, or GDP, per capita compared to the amount of federal funds flowing into each state. Louisiana is placed in the “high dependency, low GDP” category, with a GDP ranking of 40th in the nation. Louisiana’s economy is not growing as fast as the rest of the country. With the highest poverty rate in the country, lawmakers need to pursue reforms that will make the state more economically competitive and increase opportunity for all Louisianans. Research has shown that more responsible state budgeting and spending, tax relief, and removing barriers for employers to start businesses and workers to work help reduce the number of people in poverty and reduce the dependency on the federal government by individuals and the state. According to WalletHub and the Tax Foundation, Utah is one of the least dependent states on federal funding. This is because the state reformed its social safety-net system decades ago, linking assistance with employment opportunities. This made Utah the state with the fastest economic and job recovery post pandemic. Louisiana should take a page out of Utah’s playbook and achieve the same. It’s time to reduce the state’s and individuals’ dependence on Congress and the national debt, which exceeds $31 trillion and is shared by all states including our own. And it’s time to get Louisiana off the top of another bad list and into a comeback story that we know is achievable. Originally published at Pelican Institute. In Let People Prosper episode #38, I talk with Annie Spilman, Texas State Director of NFIB-Texas, about regulatory consistency and tax reforms which will help businesses thrive and let people prosper. On today's episode of the "Let People Prosper" show, which was recorded on March 31, 2023, I'm thankful to be joined by Annie Spilman, Texas State Director at the National Federation of Independent Business (NFIB) in Austin, Texas.

We discuss:

|

Vance Ginn, Ph.D.

|

RSS Feed

RSS Feed

Proudly powered by Weebly