|

In the Energy News Beat - Conversation in Energy with Stuart Turley, Dr. Vance Ginn is interviewed about various pressing economic and political issues. They discuss the recent presidential debate, the state of the U.S. economy, the implications of red-state policies on job growth, and the impact of high energy costs on inflation. The conversation also covers the importance of school choice, immigration reform, Supreme Court rulings on free speech, the Chevron Supreme deference Court decision on regulatory issues, and the challenges of achieving net zero emissions amidst global economic shifts. Dr. Ginn emphasizes the need for sound financial policies and reducing government spending.

Please follow Vance on his substack HERE: https://vanceginn.substack.com/. It is a great source of finance and political insights. Vance, I would like to have you back and on the 3 Podcasters Walk into a Bar with David Blackmon and Rey Trevio. - Thanks again for your time, and talk soon - Stu

0 Comments

Originally published at AIER.

The US economy faces numerous challenges, exacerbated by policy uncertainty and excessive government intervention. Milton Friedman famously said, “If you put the federal government in charge of the Sahara Desert, in five years there’d be a shortage of sand.” This sharp observation underscores the inefficiencies often associated with government intervention. Instead, we should advocate for free-market solutions that empower individuals and businesses to drive innovation and growth. Election years heighten policy uncertainty, driving economic volatility. Businesses and investors become cautious, waiting to see which policies will prevail. This hesitation can slow economic activity, affecting job creation and investment in new projects. More than half of Americans think we are in a recession even when the headline data say otherwise, reflecting a disconnect between reported statistics and personal experiences. Policy uncertainty during election years exacerbates these issues. The upcoming elections could significantly impact economic policies, depending on the direction taken by the administration. Whether it’s Biden’s continued interventionist policies or a shift under Trump, the stakes are high. Businesses, investors, and consumers are left guessing, which stalls responsible decision-making and hampers economic growth. The recent meeting of the Business Roundtable highlighted these concerns as both Biden and Trump pitched their economic visions. According to the Tax Foundation, Biden’s tax plan, which includes increases on corporations and the wealthy, could reduce GDP by 2.2 percent and eliminate 788,000 jobs over time. On the other hand, Trump’s tariff proposals that hike taxes on Americans would have economic consequences, increasing consumer prices and reducing household incomes. The Federal Reserve’s decisions also play a crucial role in shaping the economic landscape. Recent hikes in interest rates to curb inflation have added another layer of uncertainty. Higher borrowing costs can dampen consumer spending and business investment, slowing economic growth. The Fed’s policy trajectory remains uncertain, contributing to a cautious outlook among businesses and investors. Biden’s regulatory approach further complicates matters. His administration has introduced numerous regulations affecting various sectors, from energy to finance. While intended to address climate change and market stability, these regulations often have significant compliance costs and operational challenges. The regulatory burden can stifle innovation and deter investment, particularly in industries struggling with economic headwinds. Another key aspect is the role of institutions. Friedrich Hayek, in his seminal work “The Road to Serfdom,” cautioned against the overreach of central planning. He emphasized that central planning often leads to inefficiencies and a loss of individual freedoms. His insights are particularly relevant today as we navigate the complexities of modern economies. To truly flourish, governments should embrace free-market capitalism and resist the creeping influence of socialism. This principle applies across sectors. By focusing on the efficient use of resources, reducing regulatory burdens, and fostering competition, we can build a more prosperous future. The bottom-up approach ensures better utilization of resources and empowers entrepreneurs, businesses, and local communities. Policies such as eliminating unnecessary regulations, reducing corporate tax rates, and promoting school choice are vital. These policies drive economic growth and ensure that resources are used where they are most needed. Policy uncertainty during election years can create a precarious economic environment. Given the numerous issues in Washington, states must lead the way in our system of federalism. The increasing divergence between red and blue states on taxes, labor, and education highlights this trend. Red states cut taxes and promote business-friendly policies, while blue states often expand government programs. This divergence allows states to set examples of effective governance through free-market principles. By reducing regulatory burdens, passing sustainable budgets, and fostering competition, states can mitigate some national policy uncertainties that stall economic progress. The next big step in federalism involves states innovating beyond traditional policies. For instance, states should focus on restraining government spending, eliminating bad taxes like income taxes, and reducing onerous regulations. Policies promoting school choice can also drive education reform and better outcomes, ensuring that all children have access to quality education regardless of their socioeconomic background. In addition, more freedom in technology and innovation should be ensured to support the next big revolution that improves our lives and livelihoods. To move forward, we must build from our past experiences and rise to overcome obstacles. We can foster innovation and resilience by acknowledging and learning from our failures. It’s essential to recognize that failure provides valuable lessons and opportunities for growth. Expanding government intervention in response to failures often stifles this learning process and leads to greater inefficiencies. Policy uncertainty during election years can create a precarious economic environment. States must lead the way in our system of federalism, setting examples of effective governance through free-market principles. By passing sustainable budgets, reducing regulatory burdens, and fostering competition, states can mitigate some national policy uncertainties that stall economic progress. Let’s leverage the strengths of the free market, prioritize efficiency, and ensure that our policies truly benefit Americans. By embracing free-market principles, reducing regulatory burdens, and fostering competition, we can pave the way for a stronger and more prosperous America. Together, we can build a future where smart policies and strong institutions that support life, liberty, and property pave the way for economic resilience and growth. Don’t miss the latest economic news in 9 minutes:

💸New CPI inflation report shows a 3.4% increase over the last year, while real average weekly earnings have dropped 4.4% since Biden took office. The Fed must act faster to cut its balance sheet, as I discussed on Fox Business with Cavuto. #Bidenomics #Inflation 📈Biden's tariff practices are a tax hike on those earning less than $400K, despite promises. Join me on the Sean Hannity Show, Lars Larson Show, and NTD News where I discussed the high costs and the failure of Bidenomics. #Tariffs 📚Government schools in Texas are fully funded, NOT UNDERFUNDED like some are saying! Despite declining enrollment and failing test scores, progressives still push for more funding. It's time for universal ESAs to empower parents and lower property taxes. #SchoolChoice 💬 Like, subscribe, and share my take on key economic issues every week. For more info, subscribe to my newsletter at vanceginn.substack.com and check out vanceginn.com.  Originally published at AIER.

Recently, the Biden administration handed $1.5 billion to the nation’s largest domestic semiconductor manufacturer, GlobalFoundries, the biggest payout from the CHIPS and Science Act of 2022 so far. The argument for this corporate welfare is America is too dependent on chips from China and Taiwan so more should be made domestically. Instead of seeing how America should reduce the cost of doing business for all semiconductor businesses here, some businesses will be picked as winners and others as losers. The cost of this form of socialism gives capitalism a bad rap and should be rejected. This move echoes a broader trend of governments worldwide intervening in their economies through industrial policy. A cocktail of targeted subsidies, tax breaks, and regulatory tinkering, industrial policy aims to sculpt economic outcomes by favoring specific industries or firms, all for the supposed benefit of the national economy. Industrial policy puts business “investment” decisions in the hands of government bureaucrats. What could go wrong? While its champions tout its potential to boost competitiveness and spur innovation, the reality often tells a different story, especially in light of massive deficit spending. In practice, industrial policy tends to fan the flames of higher prices and sow the seeds of economic destruction. Politicians too often meddle with voluntary market dynamics by artificially bolstering favored sectors through subsidies and tax perks, resulting in the misallocation of resources and distorted prices. Moreover, the infusion of government funds to bankroll these initiatives with borrowed money can contribute to the Federal Reserve helping finance the debt, increasing the money supply, and stoking inflation. The nexus between deficit spending and prices looms large over industrial policy. When politicians resort to deficit spending to bankroll industrial ventures, they put upward pressure on interest rates by issuing more debt and competing with scarce private funds. Elevated interest rates disturb private investment, ushering in a likely economic slowdown. Suppose deficit financing leans heavily on monetary expansion, whereby the central bank snaps up government debt. In that case, it fuels inflation by flooding the market with money that chases fewer goods and services. The national debt is above $34 trillion, and the Federal Reserve has already monetized much of the increase in recent years. Racking up even more deficits is insane: repeating the same mistakes and expecting a different result. Excessive spending and money printing have landed us with above-target inflation for over three years running. The repercussions of industrial policy ripple beyond inflation to encompass the broader economic landscape. Excessive government meddling in specific industries crowds out private investment and entrepreneurship. When particular firms enjoy subsidies and preferential treatment, it distorts the competitive landscape and deters innovation. This stifles economic vibrancy and impedes the rise of new industries or technologies crucial for sustained growth. For a cautionary tale of how Biden’s recent move could play out, look no further than Europe. Nations like Sweden, heralded by the West as a utopian example of big government yielding big benefits, spent the last year grappling with economic strife driven by dwindling private consumption and housing construction. Europe’s penchant for industrial policy, marked by subsidies, high taxes, and regulatory hoops, has contributed to its economic stagnation. To sidestep the dilemma of industrial policy missteps, policymakers should stop propping up their favorite sector or industry and instead unleash people to flourish by getting the government out of the way. Politicians should foster an environment conducive to entrepreneurship, innovation, and competition. This entails cutting government spending, reducing taxes, trimming red tape, and championing trade by removing barriers to private sector flourishing. By allowing market forces to determine resource allocation and rewarding entrepreneurship and risk-taking, people here and elsewhere can unleash their full potential and adapt to changing circumstances more effectively than under industrial policy frameworks. Biden’s billion-dollar amount to one company may seem like a lot, but that’s just a drop in the bucket of what’s to come from the CHIPS Act. Instead, these funds should be eliminated, preventing Congress from taking us further down the road to serfdom.  Originally published at Washington Times.

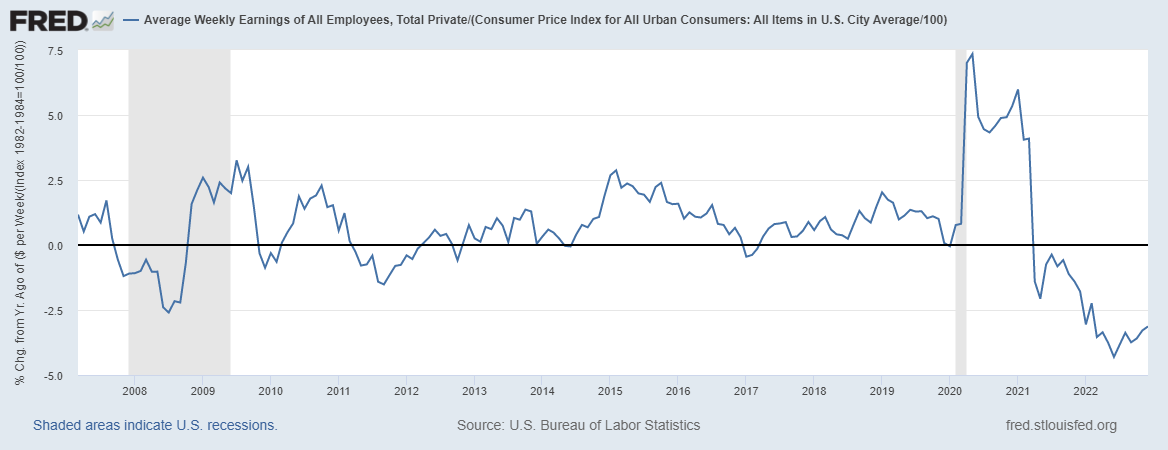

In President Biden‘s recent State of the Union address, he painted a rosy economic picture, touting what he called “Bidenomics” as the driving force behind what he claims is a robust economy. He pointed to a low unemployment rate, the absence of a recession, and a lower inflation rate as evidence of success. Reality, however, tells a different story. And Mr. Biden’s recently released irresponsible budget sends the federal government and America further toward bankruptcy. Despite the president’s assertions, the economy and inflation remain top concerns for most Americans. The disconnect between the headlines and the lives of ordinary citizens underscores the profound challenges facing the nation’s economic landscape. This sense of malaise can be directly attributed to the flawed principles underlying Bidenomics, as outlined in his latest budget. These include excessive spending, taxation and regulation. Each is destructive, but together, they are catastrophic. The result has been stagflation and less household employment in four of the last five months. There have also been lower inflation-adjusted average weekly earnings by 4.2% since January 2021, when Mr. Biden took office. Rather than fostering economic growth and prosperity, Bidenomics has stifled innovation, investment and job creation. At its core, Bidenomics represents a misguided attempt to address complex economic issues through heavy-handed government intervention. While the administration may tout short-term gains, the long-term consequences of such policies are far-reaching and unaffordable. The reality is that excessive government spending has led to unsustainable levels of debt, burdening future generations with the consequences of fiscal irresponsibility. Similarly, excessive taxation is stifling entrepreneurship and dampening economic activity, limiting opportunities for individuals and businesses alike. Excessive regulation serves only to hamper innovation and drive up costs, exacerbating the challenges facing working families. Unfortunately, Mr. Biden’s latest budget proposal doubles down on these bad policies. Even with rosy assumptions of tax collections being a higher share of economic output over time as the tax hikes will reduce growth and, therefore, lower taxes as a share of gross domestic product, the budget continues massive deficits every year. This will result in higher interest rates, higher inflation, more investment These results have been highlighted in economic theory by economists such as Alberto Alesina and John B. Taylor. Their research has found that raising taxes doesn’t help close budget deficits because of the reduction in growth from higher taxes in a dynamic economy. The way forward should be cutting or at least better-limiting government spending — the ultimate burden of government on taxpayers. Amid these challenges, America also needs a return to optimism and flourishing. This includes leadership that inspires confidence, fosters innovation, and empowers people to pursue their dreams. We need out-of-the-box policies prioritizing economic freedom and individual opportunity, allowing the entrepreneurial spirit to thrive and driving growth and prosperity. More specifically, this means reducing the burden of government intervention through lower spending and taxes, streamlining regulations, and fostering an environment where entrepreneurship can thrive. By embracing fiscal sustainability and making tough choices, we can ensure the long-term stability and prosperity of our nation. In short, while Mr. Biden tries to spin a positive narrative about the economy, the facts speak for themselves. We cannot afford Bidenomics, no matter the headlines, what was touted in the State of the Union address, or the latest budget. The stakes are too high, and the consequences too grave, to ignore the reality of our economic situation. We need leadership that is willing to confront the hard truths and enact policies that prioritize the well-being of all Americans, fostering an environment where optimism and flourishing can thrive.  Originally published at James Madison Institute.

America’s Antitrust laws have been essential to the legal landscape for over a century. They were designed to protect competition and consumer welfare. However, the Biden administration’s onslaught on competition through flawed antitrust efforts has threatened consumer welfare and profitability. This is especially true for “Big Tech” companies that generate substantial consumer welfare and billions of dollars in economic activity. While these efforts are purportedly aimed at safeguarding the interests of consumers, they pose a major threat to free-market capitalism and, thereby, the nation’s prosperity. Understanding the origins of antitrust laws illuminates why current antitrust accusations are far from their original purpose. Antitrust laws trace back to the Sherman Anti-Trust Act’s enactment in 1890. The landmark legislation was aimed to curb anticompetitive practices. Section 1 prohibits contracts in restraint of trade, regardless of the size of the firms participating. Section 2 prohibits monopolization or the abuse of monopoly power by firms with substantial market shares. Further reinforcement came with the Clayton Act in 1914, which focused on preventing mergers that could substantially lessen competition or tend to create a monopoly. However, applying antitrust laws lacked consistency and often yielded ambiguous results, especially during the mid-20th century. Fast forward to the 1970s, legal scholars proposed a paradigm shift. Figures like Aaron Director, Robert Bork, and others delved into the legislative history of the Sherman Act, concluding that its primary purpose was to protect consumers from the harm caused by cartels without undermining economic efficiency. This approach laid the foundation for what we now call the consumer welfare standard, a critical development in antitrust enforcement. In the late 1970s, the U.S. Supreme Court recognized this standard in several cases, asserting that business conduct raising antitrust concerns must be evaluated based on demonstrable economic effects. This standard has since guided antitrust law, emphasizing a simple question: does the conduct make consumers better or worse off? If the conduct improves or does not harm consumers, the conduct is allowed; otherwise, the government can intervene. The consumer welfare standard is a seemingly straightforward approach that has been a guiding light to antitrust cases. But it has failed to hold those currently at the Federal Trade Commission (FTC) and Department of Justice accountable for their excessive efforts. In recent years, calls to wield antitrust laws to address the conduct of prominent technology companies like Amazon and Google, which some pejoratively call “Big Tech,” have gained momentum. However, these movements are misguided and pose significant risks to the principles of free-market capitalism. Expanding the enforcement powers of antitrust agencies, as advocated by some on the left and right, revives an old “big is bad” approach reminiscent of a bygone era when antitrust enforcement was highly politicized. Instead of fostering competition, such a progressive approach undermines the competitive market process. This destroys the instrumental activity that provides innovation, affordable prices, and high-quality goods and services, all critical for human flourishing. This lawsuit purports to challenge Amazon’s management of its online marketplace, alleging that sellers are forced to charge high prices and lose profit by using Amazon’s add-on services and advertisements. The FTC contends that these choices are obligatory and accuses Amazon of operating as a monopoly, leading to higher prices for lower-quality products. Numerous surveys and studies reveal that consumers are pleased with Amazon’s services, so this attack against the consumer welfare standard does not appear to be about what is best for customers despite the claims of progressive antitrust enforcers. Moreover, consumers have the agency to take their dollars elsewhere, as Amazon is hardly the only online seller. The principles that drive capitalism are rooted in competition; when competition is stifled, consumers and entrepreneurs lose. Another example of abusing antitrust is the Department of Justice’s (DOJ) lawsuit against Google. The suit contends that Google has dominated the market as the default browser on popular devices through monopolistic means and must be stopped. However, Google is the default browser via legal marketing tactics, which the consumer can easily change, as numerous search engine options can be implemented on any device. Therefore, the case fails to meet the standard of a solid antitrust law violation of making consumers worse off. Consumers still have many options when selecting a default browser, but most choose Google because they like it best. This lawsuit is emblematic of a broader issue – applying antitrust laws to preserve competition. Antitrust laws should protect consumers by evaluating whether they are better or worse off due to a company’s actions. It should not be a mechanism to stifle competition to level the playing field. Enforcing such laws without considering the diverse preferences of consumers is a disservice to the very principles on which capitalism–and antitrust laws–were founded. If we’re going to have antitrust laws rather than just letting market forces work, the consumer welfare standard is an essential framework for evaluating antitrust cases. It ensures that the focus remains on improving people’s lives rather than manipulating the market based on antitrust enforcers’ interests or political persuasions. This standard can help keep regulators from blocking innovation and economic growth by limiting their ability to pick winners and losers. While concerns about the size of large tech companies and their censorship practices may be warranted, granting more power and discretion to government bureaucrats is not the solution. Expanding antitrust laws and enforcement powers will lead to politicized enforcement, often aimed at serving the interests of big government, with a disregard for the effects on consumers and the broader economy. Such a big-government approach would curtail entrepreneurship, freedom of speech, job creation, investment, and economic prosperity. Proposals to create new antitrust laws are unlikely to address concerns related to censorship and bias in tech companies. Instead, they will usher in uncertainty as legal standards evolve, causing companies to settle such cases to avoid costly legal battles. Such settlements may not necessarily benefit consumers or the economy and will drive up entry costs, creating a high barrier for startups. At a time of elevated inflation, the labor market faces challenges, and the economy is in turmoil. Pursuing lawsuits against successful companies diverts resources from critical issues and misuses taxpayer money. The time is now to refocus on what genuinely matters, acknowledge the limitations of government intervention in regulating markets, and allow the principles of free-market capitalism to flourish. This approach should recognize that dispersed, decentralized information through people in markets is much better than through central planning. Free-market capitalism is not the enemy but the best path to prosperity and freedom. We would be wise to have more of it, not destruction by the radical Biden administration.  Originally published at American Institute for Economic Research.

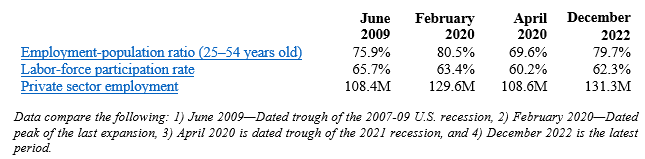

Recent headlines for the January jobs report indicate a robust economy. But a more thorough look reveals challenges for Americans. One recent headline proclaimed “Voters are finally noticing that Bidenomics is working.” But just 30 percent of Americans think the economy is doing well. When asked who would handle the economy better, people give former president Donald Trump a 22-point advantage over President Biden. Challenges include increasing part-time employment in recent months, declining household employment in three of the last four months for a net decline of 398,000 job holders, mounting public debt burdens, and declining real wages, which have fallen by 4.4 percent since January 2021. Why these results? Bidenomics is based on costly Keynesian boom-and-bust policies. With so much whiplash, it’s no wonder people are conflicted about the economy. In the latest jobs report for January, a net increase of 353,000 nonfarm jobs from the establishment survey appears robust, as it was well above the consensus estimate of 185,000 new jobs. But let’s dig deeper. Last month, household employment declined by 31,000, contradicting the headlines. The divergence of jobs added between the household survey and the establishment survey has widened since March 2022. This period coincides with declining real gross domestic product in the first and second quarters of 2022 (usually that’s deemed a recession, but it hasn’t been yet). Indexing these two employment levels to 100 in January 2021, they were essentially the same until March 2022, but nonfarm employment was 2.5 percent higher in January 2024. While this divergence mystifies some, a primary reason is how the surveys are conducted. The establishment survey reports the answers from businesses and the household survey from individual citizens. The establishment survey often counts the same person working in multiple jobs, while the household survey counts each person employed. This likely explains much of the divergence, as many people work multiple jobs to make ends meet. The surge in part-time employment and more discouraged workers underscores the fragility of the labor market. Though average weekly earnings increased by 3 percent in January over a year prior, this is below inflation of 3.1 percent. Real average weekly earnings had increased for seven months before falling last month. And there had been declines in year-over-year average weekly earnings for 24 of the prior 25 months before June 2023. These real wages are down 4.4 percent since Biden took office in January 2021. As purchasing power declines, mounting debts become more urgent. Total US household debt has reached unprecedented levels, with credit card debt soaring by 14.5 percent over the last year to a staggering $1.13 trillion in the fourth quarter of 2023. Such substantial growth in debt raises concerns about the current (unsustainable?) consumption trends, business investment, and a looming financial crisis. The surge in mortgage rates to over seven percent for the first time since December and rising home prices exacerbate housing affordability challenges, particularly for aspiring homeowners. An integral component of what some consider the “American Dream,” housing affordability is a major factor discouraging Americans. The euphoria surrounding the January 2024 jobs report is misplaced. Policymakers should heed these warning signs and enact meaningful reforms to address root causes. Biden’s policy approach undergirds most of these difficulties. Bidenomics focuses on his Build Back Better agenda that picks winners and losers by redistributing taxpayer money for supposed economic gains through large deficit spending. We haven’t seen an agenda of this magnitude since LBJ’s Great Society in the 1960s or possibly since FDR’s New Deal in the 1930s. Both were damaging, as the Great Society dramatically expanded the size and scope of government, contributing to the Great Inflation in the 1970s, and the New Deal contributed to a longer and harsher Great Depression. Just since January 2021, Congress passed the following major spending bills upon request of the Biden administration:

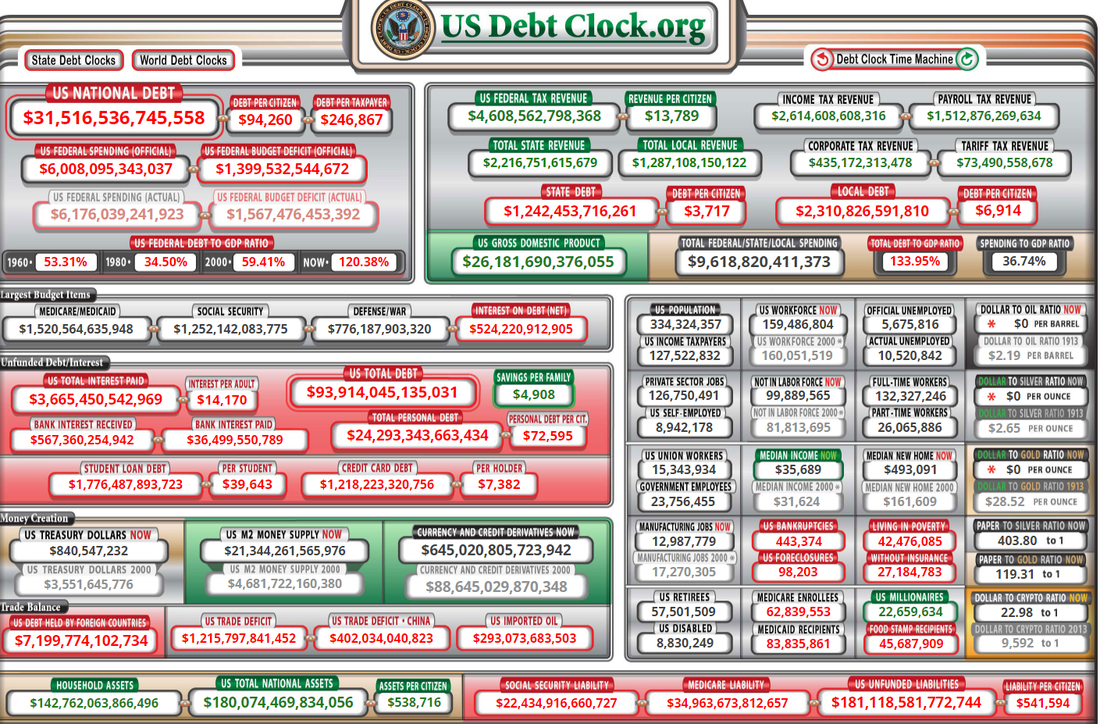

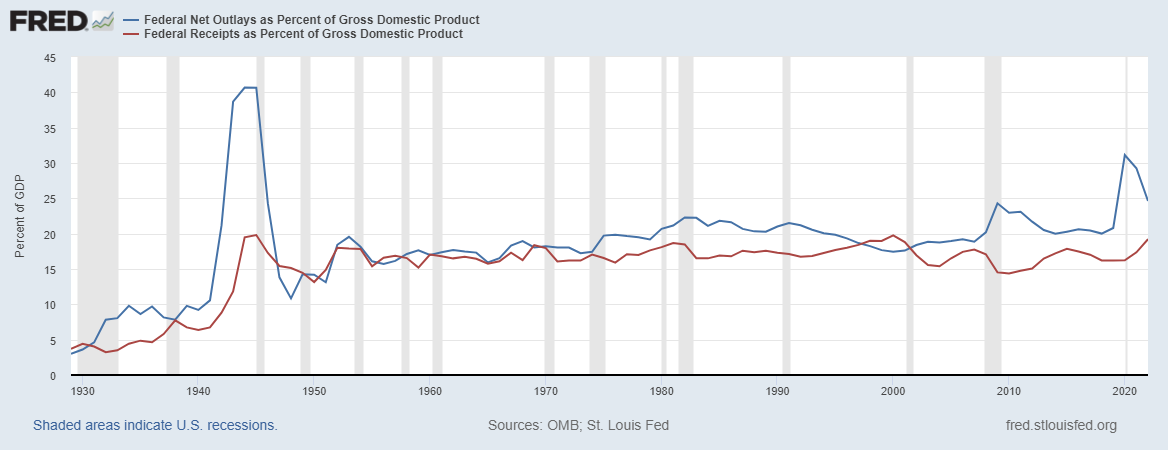

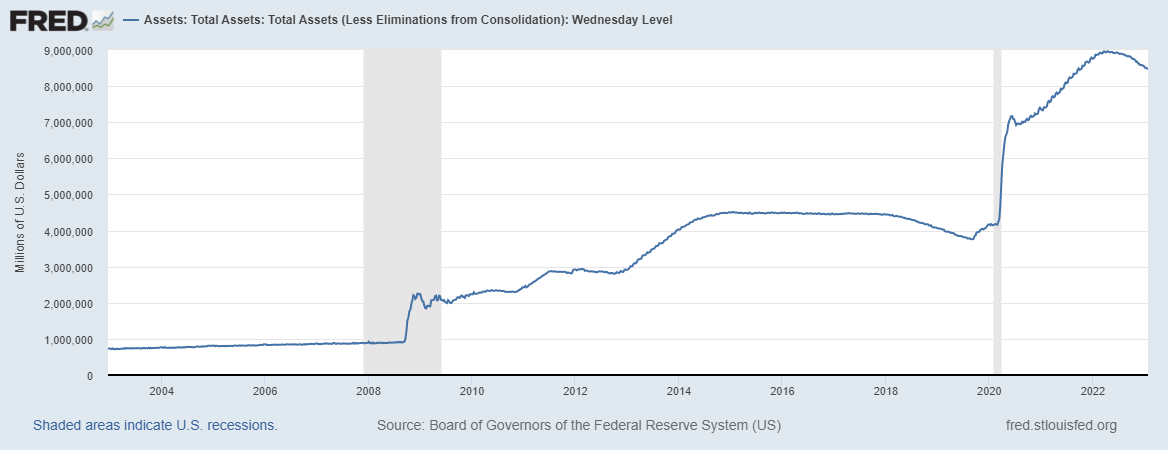

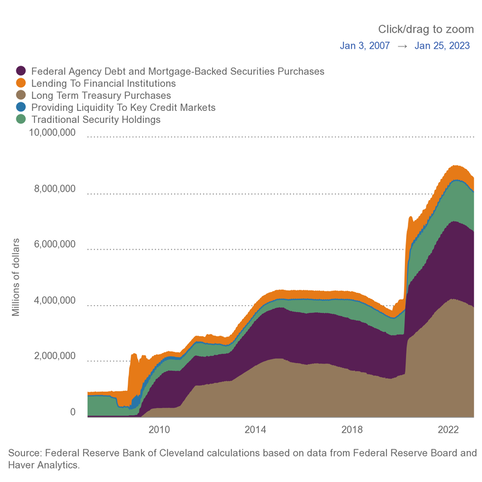

These four bills will add nearly $4.3 trillion to the national debt. But at least another $2.5 trillion will be added to the national debt for student loan forgiveness schemes, SNAP expansions, net interest increases, Ukraine funding, PACT Act, and more. In total over the past three years, excessive spending will lead to more than $7 trillion added to the national debt, which now totals $34 trillion — a 21 percent increase since 2021. There seems to be no end to soaring debt with the recent discussions of more taxpayer money to Ukraine, Israel, the border, and the “bipartisan tax deal,” collectively adding at least another $700 billion to the debt over a decade. Record debts accrued by households and by the federal government (paid by households) are not signs of a robust economy. This will likely worsen before it improves, as household savings dry up. And with interest rates likely to stay higher for longer because of persistent inflation, debts will crowd out household finances and the federal budget. The Federal Reserve has monetized much of this increased national debt over the last few years by ballooning its balance sheet from $4 trillion to $9 trillion and back down to a still-bloated $7.6 trillion. This helps explain persistent inflation, massive misallocation of resources, and costly malinvestments across the economy, keeping the economy afloat yet fragile. Excessive deficit spending weighs heavily on future generations, saddling them with unsustainable debt levels they have no voice in. Today, everyone owes about $100,000, and taxpayers owe $165,000, toward the national debt. Of course, these amounts don’t include the hundreds of trillions of dollars in unfunded liabilities for the quickly-going-bankrupt welfare programs of Social Security and Medicare. Future generations will be on the hook for even more national debt if Bidenomics continues and Congress doesn’t reduce government spending now. This is why the national debt is the biggest national crisis for America. We’re robbing current and future generations of their hopes and dreams. Fortunately, there’s a better path forward if politicians have the willpower. This path should be chosen before we reap the major costs of a bigger crisis. I’ve recently outlined what this should look like at AIER. In short, we need a fiscal rule of a spending limit covering the entire budget based on a maximum rate of population growth plus inflation. There should also be a monetary rule that ideally reduces and caps the Fed’s current balance sheet to at least where it was before the lockdowns. My work with Americans for Tax Reform shows that had the federal government used this spending limit over the last 20 years, the debt would have increased by just $700 billion instead of the actual $20.2 trillion. That’s much more manageable and would point us in a more sustainable fiscal and monetary direction. Together, fiscal and monetary rules that rein in government will help reduce the roles that politicians and bureaucrats have in our lives so we can achieve our unique American dreams. If not, we will have wasted many dreams on Bidenomics that can make things look good on the surface, but cause rot underneath. Healthcare Costs Are Straining Federal And Household Budgets. Here’s How Biden Can Rein Them In2/14/2024  Originally published at Daily Caller.

Soaring health care spending continues to spiral up, tightening the financial noose on households and government coffers. Families are forced to make difficult choices between paying for essential medical care and meeting basic needs while the federal government struggles to rein in spending amid mounting debt. These soaring health care costs must be addressed with market-based approaches before it’s too late. When the Affordable Care Act (ACA) was passed in 2010, it was heralded as the panacea for reining in healthcare costs. However, the law’s complex regulations and mandates have contributed to administrative bloat and increased overhead costs, ultimately driving up premiums and out-of-pocket patient expenses. Unfortunately, since then, subsequent politicians have failed to correct course. In 2024, federal spending on Medicare, Medicaid, and ACA subsidies will likely exceed the discretionary budget, posing a significant threat to long-term fiscal sustainability. Compulsory spending on health coverage in the private sector infringes upon household earnings. This exacerbates economic challenges for families whose purchasing power is already reduced, as inflation-adjusted average weekly earnings are down 3.1 percent since Jan. 2021. Moreover, the growing burden of health care spending poses a significant threat to long-term fiscal sustainability, as rising debt levels raise concerns about future economic prosperity. The Congressional Budget Office (CBO) recently released its annual Budget and Economic Update, painting a grim budget picture. The trajectory is alarming, with expenditures expected to be $6.4 trillion this fiscal year before soaring to a staggering $10.1 trillion by 2034. Also, net interest spending is poised to balloon from $1 trillion to $1.6 trillion by 2034. These projections underscore the urgent need for meaningful reforms to rein in healthcare costs and put the federal budget on a more sustainable path. To address these challenges, policymakers must prioritize fiscal responsibility and adopt measures to remove government as much as possible from healthcare. This would help to quickly get healthcare back to a relationship between a doctor and patient. Today, too many middle layers rob time between the doctor and patient and raise healthcare prices. Policymakers should make market-based reforms. It won’t be done overnight, so there will need to be some steps to get there. It would be great if just making healthcare prices transparent would solve the problem. But the healthcare system is much more dysfunctional than that, unfortunately. Many reimbursement rates are set between doctors and private insurance companies or government programs like Medicaid and Medicare. Those reimbursement rates are so different depending on which entity is negotiating that the prices won’t tell us much, other than how screwed up the system is, but we already know that. A market-based approach should remove obstacles on the demand and supply sides of the market. This should include ending the tax exclusion for employer-sponsored health insurance. There’s a long history of this exclusion, which started during WWII. But while it had good intentions, the result has been a major distortion to the healthcare market. There should also be consideration of a voucher program for Medicare and block grants to states for Medicaid with limited growth each year. These would help reduce the moral hazard and over-subsidization on the demand side. On the supply side, the federal and state governments should remove rules that restrict the supply of doctor offices by removing certificate of need laws. They can also boost the supply of physicians by reducing or eliminating occupational licenses. Unleashing supply and imposing market forces on demand will result in more innovative, affordable, and accessible care for everyone. The resulting reduction in government spending and improved timely access to quality care can help support more prosperity. This would reduce the need for people on government safety net programs. It would also help mitigate higher prices, alleviate strain on household budget burdens, and safeguard the nation’s economic future. These steps will require difficult choices and bipartisan cooperation at the federal and state levels, but the stakes are too high to ignore the issue any longer.  Originally published at Econlib.

Amid a heated election year, the teachings of economist Friedrich Hayek provide a guiding beacon, urging us to transcend partisan lines and champion free-market capitalism that benefits everyone. I recently interviewed Dr. Bruce Caldwell of Duke University about his book, Hayek: A Life, 1899-1950, who helped shed light on Hayek’s views on pressing issues today. As we navigate the complex landscape of governance, we should heed Hayek’s call for market-based approaches, especially with trade and immigration, where the clash of political ideologies often obscures the path to rational decision-making. Hayek’s teachings underscore the need for policy approaches prioritizing broader economic health rather than conforming to the whims of political affiliations or interest groups. He did not advocate for simplistic labels like “left and right” but viewed political thought as a triangle, with socialism, conservatism, and liberalism representing the three points. He favored liberalism, in the classical sense. His writings compel us to consider whether policies align with our principles and values. One example is trade protectionism, with tariffs enacted while president and pushed again by Donald Trump. Hayek’s book, The Road to Serfdom, cautioned against the pitfalls of protectionism and advocated for free-market principles that embrace competition in free trade. While protectionist measures like tariffs may appeal to certain political bases, they come at the expense of economic efficiency and growth. They ultimately cost us more for purchases and inhibit our choices as competition is artificially manipulated where it would otherwise organically select the best providers of resources. A Hayekian approach to trade involves understanding that dynamic economies thrive on diversity and exchanging goods and services across borders. Another issue at the forefront of political debates that Hayek’s approach helps shed light on is immigration. He recognized that allowing the free movement of individuals fosters economic dynamism and innovation. Policies that restrict immigration solely for political gain risk stifling economic growth and impeding the exchange of ideas that fuels progress. A Hayekian perspective on immigration advocates for policies that acknowledge the economic benefits of a diverse and dynamic workforce. Instead of succumbing to populist narratives that frame immigration as a threat, Hayek prompts us to view it as an opportunity. An influx of skilled and motivated individuals can contribute to a vibrant economy, filling gaps in the labor market and injecting fresh perspectives that drive entrepreneurship. Too often, misinformation about immigration has led even conservatives to favor more government involvement in tightening borders and deportation. However, as Hayek outlined in his development of “the knowledge problem,” expecting a government of people with limited knowledge of the issue and tradeoffs from policy choices too often results in worse outcomes. The people in government do not and never will have all the answers. Instead, collecting everyone’s ideas in the market leads to having the most available knowledge and, therefore, better outcomes. In short, government failures are worse than any perceived market failures. Taking a cue from Hayek, we should strive for more free trade agreements, especially with our allies, which means an end to all tariffs and other barriers. We should also enact market-based immigration policies that balance national security concerns with the economic advantages of attracting talent from diverse backgrounds. As we prepare to select our nation’s president for the next four years, Hayek’s teachings serve as a guidepost, urging us to prioritize people’s well-being over the allure of party-centric agendas. Embracing a Hayekian perspective requires a willingness to critically evaluate policies based on their economic merit rather than their alignment with partisan ideologies. Only by doing so can we navigate the complex economic landscape and ensure a prosperous and dynamic future for all.  We must learn from history or be doomed to repeat it. This includes honestly assessing the economy in 2023 so that we have better information for making decisions in 2024.

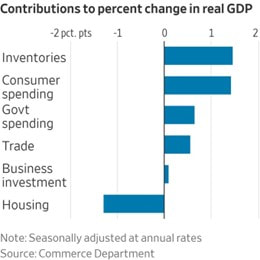

Starting with a bang on many people’s minds is housing affordability. The year commenced with a surge in the average 30-year fixed mortgage rate from 6.5% in January to nearly 8% in October but has declined recently to about 6.6%. These higher mortgage rates and record-high housing prices contributed to an unaffordable housing market. While existing home sales were up 0.8% in November, they are down 7.3% over the last year, indicating a struggling housing market for families that will unlikely improve much in 2024. Another concern is costly inflation. Rampant hikes in the cost of a typical basket of goods and services have meant less purchasing power for us. This contributes to making housing, food, education, and other expenses for that basket less comfortable or worse for many families. As of November 2023, the core consumption personal expenditures increase was 3.2% year-over-year. This price measure of a basket of goods and services excludes food and energy and is what the Federal Reserve prefers to watch. While core PCE inflation has moderated from close to 6% in 2022, the recent 3.2% inflation rate remains 60% higher than the Fed’s average inflation target of 2%. Although moderating inflation represents some relief for many Americans, the challenge is that average weekly earnings adjusted for core inflation declined in 23 of the last 35 months since January 2021. In total, these real average weekly earnings are down 0.8% since then, indicating why inflation is a top concern. An additional problem is debt. Because earnings haven’t been keeping up with inflation, credit card debt soared to more than $1 trillion as people struggled to make ends meet, which is a bad sign for 2024. And many people have been going through their savings and retirement funds quickly. What about jobs? The White House recently celebrated “total job gains achieved under the Biden administration reached 14.1 million through November 2023.” But this metric becomes less impressive considering that 9.4 million of those jobs were just recovering jobs lost during the pandemic lockdowns. So, there have been 4.7 million new jobs added since January 2021, which is 134,000 per month. While this is positive, it is not record-breaking. The weaker labor market in recent months indicates that 2024 could be tough for many workers. Most people’s pocketbooks did not grow but diminished this year, and the job market similarly lags. But what about the nation’s overall growth? Hasn’t GDP soared? Not exactly. In the third quarter of 2023, the annualized real GDP growth hit 4.9%, which appears robust. But when you dig into the details, it’s more complicated. Government spending, which is a drag on the economy as it must take taxes from the private sector and distort market activities, threw in 0.99 percentage points. And private inventories, influenced by the whims of fluctuating interest rate expectations, chipped in 1.27 percentage points. When you exclude those contributions to consider stable real private GDP, there was just a 2.6% bump up. This slower pace didn’t just pop out of nowhere. It’s been a saga since early 2022, when we hit a two-quarter decline in real gross domestic product, waving a big red flag for a recession. And when you consider the valuable metric of real gross domestic output, which is the average or real gross domestic product and real gross domestic income, the economy has declined in three out of the last seven quarters. While these economic issues suggest stagflation triggered by misguided pandemic lockdowns and subsequent trillions of new money printing of deficit-spending, there may be some relief. The Fed’s slow correction to its bloated assets of $9 trillion at its peak to $7.7 trillion contributed to interest rates soaring since March 2022. But with Congress continuing to deficit spend of about $2 trillion per year and net interest payments soaring to $1 trillion per year, there are massive economic challenges ahead. These deficits will make it more difficult for the Fed to correctly normalize its assets quickly to get them back to at least the pre-pandemic $4 trillion. This is because the budget deficits would contribute to higher interest rates, so the Fed will likely monetize the debt more to help Congress avoid needed spending restraint. While these truths are tough to swallow, many beacons of hope also emerged throughout the year that should be noted. In 2023, a momentous shift unfolded with a transformative surge in educational choice. Twenty states expanded school choice, and a record-breaking 10 states passed some form of universal school choice, making 36% of American students eligible for a private choice program. Some states have been slow to increase educational freedom, but this revolution’s overall impact is historical. Recognizing that children are the cornerstone of our nation’s future and acknowledging that improved education is a pivotal predictor of their success, the catalyst for change is undeniably rooted in more universal school choice. The second bright light is the flat state tax revolution. Many states took bold steps to enhance their economic landscapes. Notably, prominent states like California and New York faced ongoing out-migration as individuals sought refuge from progressive policies, and less heralded states embraced free-market principles, propelling them onto the national stage. More conservative Florida and Texas continued to lead the way in places where people moved in 2023. The third thing to cheer is a responsible movement toward a sustainable state budget revolution. Some states are pushing toward improving their spending limits to one that covers more of the budget, limits budget growth to no more than population growth plus inflation, and has a supermajority vote to bust the limit or raise taxes. The synergy of these reforms demonstrates the power of federalism as states experiment with policies, revealing effective strategies and fostering a healthy laboratory of competition. We need lawmakers at the federal, state, and local governments to recognize what works and implement them. The trajectory in 2024 and beyond hinges on embracing free-market capitalism, which is the best path to let people prosper. This includes less government spending, less money printing, more school choice, and more tax relief. In short, less government. That’s how we get a more prosperous 2024. Happy New Year! Originally published at Econlib.  Originally published at Real Clear Policy.

During the fourth Republican presidential candidate debate the four participating candidates were asked to name a past president who would serve as an inspiration for their administration. In his response, Governor Ron DeSantis stated that he would take inspiration from President Calvin Coolidge. Coolidge, stated DeSantis, is “one of the few presidents that got almost everything right.” Further, DeSantis argued that “Silent Cal” understood the federal government’s role and “the country was in great shape” under his administration. To say that the federal budget process is broken is an understatement. The national debt continues to grow driven by out-of-control spending. The budget hawk within the Republican Party is an endangered species. Governor DeSantis is correct that the Republican Party needs to rediscover the principle of limited government. The best way to do this is to take inspiration from the Republican Party’s best known budget hawks and champions of limited government, Presidents Warren G. Harding, and Calvin Coolidge. President Harding assumed office in 1921 when the nation was suffering a severe economic depression. Hampering growth were high-income tax rates and a large national debt after World War I. Congress passed the Budget and Accounting Act of 1921 to reform the budget process, which also created the Bureau of the Budget (BOB) at the U.S. Treasury Department (later changed in 1970 to the Office of Management and Budget). President Harding’s chief economic policy was to rein in spending, reduce tax rates, and pay down debt. Harding, and later Coolidge, understood that any meaningful cuts in taxes and debt could not happen without reducing spending. Harding selected Charles G. Dawes to serve as the first BOB Director. Dawes shared the Harding and Coolidge view of “economy in government.” In fulfilling Harding’s goal of reducing expenditures, Dawes understood the difficulty in cutting government spending as he described the task as similar to “having a toothpick with which to tunnel Pike’s Peak.” To meet the objectives of spending relief, the Harding administration held a series of meetings under the Business Organization of the Government (BOG) to make its objectives known. “The present administration is committed to a period of economy in government…There is not a menace in the world today like that of growing public indebtedness and mounting public expenditures…We want to reverse things,” explained Harding. Not only was Harding successful in this first endeavor to reduce government expenditures, his efforts resulted in “over $1.5 billion less than actual expenditures for the year 1921.” Dawes stated: “One cannot successfully preach economy without practicing it. Of the appropriation of $225,000, we spent only $120,313.54 in the year’s work. We took our own medicine.” Overall, Harding achieved a significant reduction in spending. “Federal spending was cut from $6.3 billion in 1920 to $5 billion in 1921 and $3.2 billion in 1922,” noted Jim Powell, a senior fellow at CATO Institute. Harding viewed a balanced budget as not only good for the economy, but also as a moral virtue. Dawes’s successor was Herbert M. Lord, and just as with the Harding Administration, the BOG meetings were still held on a regular basis. President Coolidge and Director Lord met regularly to ensure their goal of cutting spending was achieved. Coolidge emphasized the need to continue reducing expenditures and tax rates. He regarded “a good budget as among the most noblest monuments of virtue.” Coolidge noted that a purpose of government was “securing greater efficiency in government by the application of the principles of the constructive economy, in order that there may be a reduction of the burden of taxation now borne by the American people. The object sought is not merely a cutting down of public expenditures. That is only the means. Tax reduction is the end.” “Government extravagance is not only contrary to the whole teaching of our Constitution but violates the fundamental conceptions and the very genius of American institutions,” stated Coolidge. When Coolidge assumed office after the death of Harding in August 1923, the federal budget was $3.14 billion and by 1928 when he left, the budget was $2.96 billion. Altogether, spending and taxes were cut in about half during the 1920s, leading to budget surpluses throughout the decade that helped cut the national debt. The decade had started in depression and by 1923, the national economy was booming with low unemployment. Both Harding and Coolidge were committed to reining in spending, reducing tax rates, and paying down the national debt. Both also used the veto as a weapon to ensure that increased spending and other poor public policies were stopped. The results of the Harding-Coolidge economic plan created one of the strongest periods of economic growth in American history. Unemployment remained low, the middle class was expanded, and the economy expanded. From 1920 to 1929 manufacturing output increased over 50 percent and the United States was a global leader in many key industries. In our current era marked by dangerous debt levels and high inflation whoever becomes the Republican presidential nominee should take inspiration from Harding and Coolidge. Economic Reality Check: What Do Falling Mortgage Rates & Jobs+Inflation Signal for the 2024 Economy?12/15/2023 Thank you for tuning into the 39th episode of “This Week’s Economy.”

Much information is packed into today’s newsletter, including my new podcast episode revealing the economic news you need to know in less than 14 minutes! Today, I cover: 1) National: -Why the new U.S. jobs report (my latest commentary) is not as strong as some say -Inflation rates have moderated but still remain well above the Fed’s 2% rate target -Federal Reserve paused again with its federal funds rate target in the range of 5.25-5.5%, supporting a boost in the stock market and likely lower mortgage rates 2) States: -Sustainable Colorado Budget was released that I authored with Ben Murrey at Independence Institute, which provides a path forward for the Centennial state to return to its TABOR roots and buy down the income tax -School choice challenges face Texas as many state leaders are against it, and they keep spending too much -California’s deficit reaches crazy highs, proving why spending is the ultimate government burden 3) Other: -Don't miss my latest LPP episode with Jennifer Huddleston discussing problems with regulating technology, including AI -One of my latest op-eds argues why China is not our biggest threat…what is? -Argentina's new president makes significant strides that could set an example for the U.S.  Recent polling data from CNN reveals a grim reality: 84 percent of Americans are concerned about the national economy. Despite President Biden’s efforts to highlight seemingly positive metrics as indicators of the success of his progressive policies, a closer look at the data reveals why most Americans remain dissatisfied.

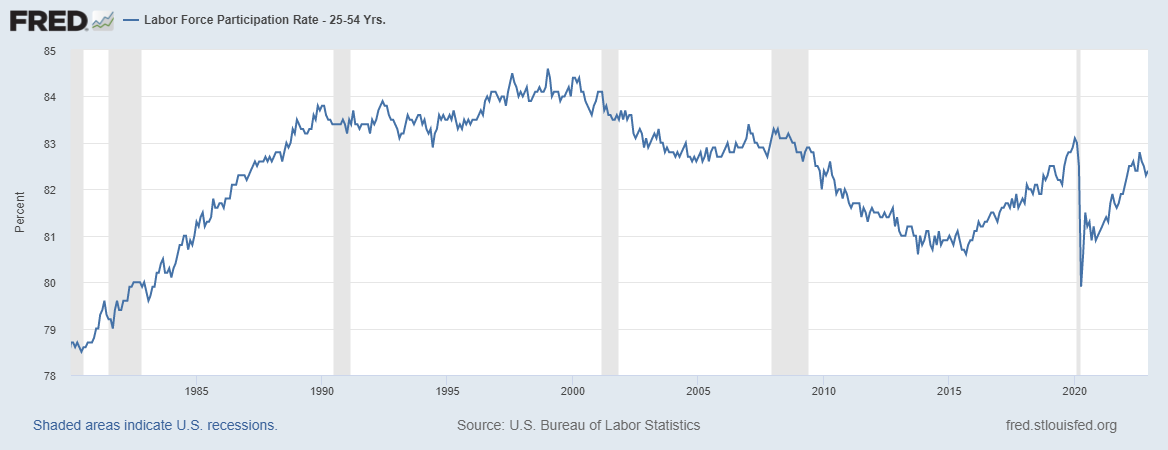

Biden’s claim of adding 14 million jobs since taking office would be impressive if it were true. The reality is that, since he took office in Jan. 2021, 13 million private sector jobs have been added. This appropriately excludes the unproductive addition of one million government jobs that will soon set a record under his watch. But the bigger point negating his rosy scenario is that the vast majority of this touted “job growth” stems from restoring job losses from the pandemic lockdowns. When we accurately tally the new jobs added since the shutdowns began in Feb. 2020, the count stands at 4.5 million private sector jobs added in three years. While this is a positive, it’s an average of 1.5 million jobs yearly, far from qualifying as record-breaking job creation. The latest U.S. jobs report for November provides additional data, reaffirming the mixed nature of the labor market. The payroll report indicates a feeble performance. There was a headline number of 199,000 jobs added. But there were revisions in October of 35,000 fewer jobs added. So, net additions stand at 164,000 jobs. When government jobs are correctly subtracted, the count is just 115,000 new productive private jobs last month. On a more positive note, the household report shows a substantial increase of 532,000 in the labor force, resulting in a 62.8 percent participation rate. Employment experienced robust growth of 747,000, contributing to a decline in the unemployment rate to 3.7 percent. But the broader unemployment rate that includes underemployed and discouraged workers is nearly twice as high at seven percent. However, it’s crucial to note that the average weekly earnings show a 3.7 percent increase over the last year, though this has been overshadowed by the elevated inflation. Fresh data on inflation as measured by the chained consumer price index (chained-CPI), which accounts for the substitution effect of changes in individual prices not accounted for by the headline CPI, reveals signs of moderation. The latest core chained-CPI inflation rate, which excludes food and energy and is watched by the Federal Reserves, for Nov. 2023 was up 3.7 percent year-over-year. Not only is this 85 percent higher than the Fed’s average inflation rate target of two percent, it also nearly matches the increase in earnings, negating any increase in purchasing power. In fact, real average weekly earnings have declined for 24 straight months. No wonder people are concerned about the economy. The ongoing reduction of the Fed’s balance sheet contributes to this inflation moderation, but further cuts to its bloated balance sheet are necessary to stabilize prices across the economy. Their balance sheet currently hovers around $8 trillion, nearly double its pre-pandemic figure, having increased tenfold in fifteen years from $800 billion in 2007. While some blame the national debt crisis on not having enough tax revenue from slower-than-optimal GDP growth, the truth is excessive government spending. Inflation is not your fault, as The Atlantic recently claimed. It’s the fault of excessive government spending by Congress that led to rising national debt which the Fed purchased and printed money. Too much money chasing too few goods is the classic definition of inflation, and it fits this time, too. A better way to solve this would be to slash government spending and taxes like President Calvin Coolidge did a century ago. During the Roaring 20s, the national debt declined, and the economy supported more opportunities for people to flourish. In light of the evidence, the question arises: Is Bidenomics working? The answer, drawn from the data, suggests it is not. To guide the economy back on course, recalibration is imperative. This includes prioritizing fiscal responsibility, pruning the Fed’s ballooning balance sheet, and reining in excessive government spending. Only through such pro-growth measures can we hope to unlock genuine economic recovery and chart a course toward lasting prosperity.  Originally published at Econlib.

President Biden signed a sweeping executive order to “harness” and “keep” artificial intelligence, two words you never want to hear from the government. This new regulation will inhibit Americans’ flourishing because restricting free markets never works. The EO is reported to ensure safety, equity, and responsible development. While these goals may appear laudable, delving deeper reveals that this motion will hinder economic progress and stifle the innovation it aims to promote. That’s why policies must always be judged by their results rather than their intentions. Details of the order’s objectives include safety tests, industry standards, and government oversight to address potential risks associated with AI. Forcing AI companies to conduct safety tests before going public, known as “red teaming,” will significantly slow the development and deployment of AI technologies. It’s well-established that innovation thrives in an environment of minimal regulatory interference called “permissionless innovation.” So introducing these bureaucratic hurdles will hinder fast-growing AI and all the industries that have begun to rely on it. Medicine and biotech, in particular, have realized remarkable potential with AI that has life-saving ramifications. But Biden’s overreaching EO wants to harness that. As is the case with many regulations, the EO comes at not just a cost to the individuals it affects but to the government’s pocketbook as well. As part of its endeavor to “preserve individuals’ privacy,” the administration will fund the Research Coordination Network. At a time when wages aren’t keeping pace with inflation and the average American family is losing real money due to a suffering economy, the government adding an expense like this is an insult to injury. Congress needs to reduce spending, and the Fed needs to slash its bloated balance sheet now more than ever. One of the most troubling aspects of the EO is its emphasis on regulating AI in the workforce out of concern for the technology displacing workers. Although there has been some uproar out of concern over AI destroying jobs, research shows that only 34% of Americans fear job displacement due to AI. And for good reason. Not only now but historically, concerns about new technologies displacing workers have been overblown. A Harvard paper published in 2013 predicted that by 2023, almost half of all American jobs would be replaced by AI. Clearly, the calculation has not come to pass. That’s because technology is a tool, not a threat. Frequently, implementing AI and technology like it allows humans to do more complex or human-facing jobs that AI can’t do or that people don’t want AI to do. AI is a transformative technology that has the potential to revolutionize various industries, from healthcare to finance and beyond. In a free market, competition drives innovation and efficiency, benefiting consumers and businesses. Restricting AI through excessive regulations and government oversight threatens this dynamic. While the intention behind Biden’s EO on AI may be to ensure responsible development and safe use, the economic consequences could be dire. To maintain America’s leadership in AI and foster economic growth, lawmakers and leaders must avoid overregulation and unnecessary restrictions on this transformative technology. Instead, we should encourage innovation, protect intellectual property, and ensure that AI remains a powerful tool for driving economic prosperity and improving the lives of all Americans. In the fast-paced world of technology, the last thing we need is government interference that hampers progress. Thank you for listening to the 32nd episode of "This Week's Economy," where I briefly recap and share my insights on key economic and policy news.

Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. Also, subscribe and see show notes for this episode on Substack (www.vanceginn.substack.com) and visit my website for economic insights (www.vanceginn.com). Today, I cover: 1) National: The newly appointed House Speaker Mike Johnson, how President Biden's student loan "forgiveness" plan will disadvantage lower-income earners while making higher education more expensive, and while the latest GDP report may seem promising at first, but is less impressive when considering details; 2) States: Texas has a new roughly $18 billion surplus that should be put toward buying down property taxes until they are zero, but that likely won't happen given what's on Texas' ballot, and Louisiana's GDP and personal income rates show that aggressive improvement is needed in The Pelican State; and 3) Other: Why you don't want to miss last week's podcast with Texas State Representative Brian Harrison and the upcoming episode with Former U.S. Senator Phil Gramm on the myth of American inequality.  This commentary was originally published at EconLib here.

Americans say the economy is the most important problem facing the country. But major headlines covering the latest jobs report for August do their best to downplay this concern. The New York Times’ headline covering the news was, “August Jobs Report: U.S. Jobs Growth Forges On,” but the economic reality is far less cheerful. Sure, the jobs report beat the consensus estimate by economists. But that high-level look at the data fails to address underlying issues keenly felt by many Americans that are apparent with more scrutiny. And these problems won’t be over unless policies out of D.C. substantially and quickly improve. Last month, 187,000 jobs were added, according to the payroll survey, compared with the anticipated 170,000. But the jobs added in the prior two months were revised lower by a cumulative 110,000 jobs, bringing the net jobs added in August to just 77,000. This extends an ongoing trend of downward revisions over the last several months. According to the household survey, the unemployment rate, a weak indicator of the labor market’s strength, jumped substantially from 3.5% to 3.8%. Coupled with news of slow wage growth of just 0.2% last month, there is growing concern among Americans trying to make ends meet. We know the higher unemployment rate isn’t from too few jobs available. The number of job openings has been nearly double that of those unemployed for a long time, though decreasing quickly. Instead, the higher rate suggests a sluggish economy in which there are more unemployed or ghost job openings from companies that do not intend to hire but want to gauge interest and competition. There is some good news. The labor force increased by 736,000, which raised the participation rate to 62.8% in August. This is the highest rate since February 2020, just before the shutdowns in response to the COVID-19 pandemic. More people entering the labor force and higher participation rates appear promising. However, the increase in the labor force was a combination of 222,000 more people employed, with the other 514,000 people becoming unemployed. And diving deeper, 4.2 million more adults remain not in the labor force compared with February 2020. Many of these individuals have been unemployed for years, so obtaining employment could be difficult due to a lack of productivity signals in their resume on top of employers dealing with a stagnant economy. The rise in the unemployment rate, lackluster wage growth, and the possibility of unfilled job openings all point to a weak labor market. Add in ongoing stagflation, as too-high inflation continues, and Americans are rightly concerned about the future. Some blame the Federal Reserve for this weakness because of its fight to bring down inflation after creating it. However, Milton Friedman debunked this tradeoff between lower inflation and a higher unemployment rate decades ago. Specifically, there’s no long-run tradeoff between the two, so the Fed must focus on the single mandate of price stability instead. The Fed has been working to combat inflation by hiking its interest rate target to a multi-decade high of 5.5% and slowly reducing its bloated balance sheet. This is why you’ve seen car loan and mortgage rates soar to multi-decade highs. These higher rates significantly disrupt the new car and housing markets. But this is the resulting bust after the artificial post-pandemic “boom” as new money moves throughout the economy and manipulated interest rates create malinvestments. We felt the higher inflation rate last year from the Fed’s actions of close to 9%, and now it’s about one-third of that rate, but this remains about 50% higher than its 2% flexible average inflation target. The Fed has stated that it may raise interest rates further. And I believe that it will be forced to raise its target rate to about 6% before this hiking cycle is over. But just raising this rate won’t be enough to curb inflation for long if Congress’ deficit spending remains unchecked. This will force the Fed to monetize it to avoid putting more pressure on Congress to get their irresponsible fiscal house in order. President Biden and Democrats in Congress made this situation worse with the passage of the misnamed Inflation Reduction Act, which is likely to cost about four times the initial $300 billion estimate over a decade. Their wasteful spending, along with Republicans’ excessive spending before them, has led to a fiscal crisis, the most significant national threat. Congress will unlikely make the needed reforms to the primary drivers of the deficit of mandatory spending programs like Social Security and Medicare because of rent-seeking in politics. This will likely result in the Fed not sufficiently cutting its balance sheet to stop inflation. Rather, the Fed will probably choose to increase its balance sheet, putting more inflationary pressure on the economy when that’s the last thing it needs. A vital measure of the economy known as real gross domestic output, the real average of gross domestic product and gross domestic income, has declined in three of the last six quarters. While I don’t want there to be a hard landing, this is the situation that central planners by Congress spending and taxing too much, President Biden regulating too much, and the Fed printing too much have left us. There will be efforts by the government to correct these government failures, but we shouldn’t double down on past mistakes. Let’s learn from these failures and remember the most recent lesson in the 1980s: President Reagan cutting regulations, Congress passing tax cuts (but spending too much), and Fed Chairman Paul Volcker cutting the balance sheet. Initially, the cuts to the Fed’s balance sheet contributed to soaring double-digit interest rates, and the economy suffered a double-dip recession. However, afterward, the economy was able to heal from the prior hindrances of past presidents, congressional members, and the Fed, resulting in a long period of economic prosperity, which is often called the Great Moderation. What we have today is an economy where the government is growing, and markets aren’t as much. This must be reversed. When workers, entrepreneurs, and employers are free to engage in voluntary transactions, competition thrives, innovation flourishes, and resources are allocated efficiently. Moreover, free markets promote consumer choice and personal freedom. When government interventions, such as wasteful spending, excessive regulations, and high taxes, are removed, markets can function more efficiently and respond dynamically to changing economic conditions. Striking the right balance between constitutionally limited government functions and preserving the freedom of markets is crucial for achieving a vibrant and prosperous economy. Rising unemployment, stagnant wages, and the specter of inflation require a multifaceted approach. Raising interest rates hasn’t been enough. The government must focus on responsible fiscal and monetary policies, including reducing government spending, addressing burdensome regulations and taxes, and substantially cutting the Fed’s balance sheet. Americans are still suffering, and there is no time to waste in aggressively assessing these measures that cause economic strain so that people can get back to flourishing instead of merely “making it.” Today, I cover: 1) National:

3) Other: My thoughts on the DOJ lawsuit against Google for violating antitrust laws and why I believe it's an attack on consumers and capitalism. You can watch this TWE episode and others along with my Let People Prosper Show on YouTube or listen to it on Apple Podcast, Spotify, Google Podcast, or Anchor. Please share, subscribe, like, and leave a 5-star rating!

For show notes, thoughtful insights, media interviews, speeches, blog posts, research, and more, please check out my website (www.vanceginn.com) and subscribe to my newsletter (www.vanceginn.substack.com), share this post, and leave a comment.  Inflation might be cooling some, but recent reports suggest many Americans aren’t economically optimistic. Despite President Biden continuing to celebrate the success of his “Bidenomics” approach, the reality is that purchasing power is still down, and job market weaknesses remain. So, why is the current administration so proud? It seems deficit spending is the reason.

A poll from Monmouth University found that only one in four Americans believe the country is headed in the right direction, and a significant 62% disapprove of how Biden is handling inflation. And it’s no wonder, considering that real wages have failed to keep up with inflation for a staggering 26 consecutive months. Understandably, people are becoming weary. The latest CPI report shows a moderate decline in headline inflation to 3% in June 2023 from the previous month’s 4%. However, core inflation, which excludes food and energy prices, remains stubbornly high at 4.8% year over year. This improvement shows some relief, but to get the economy back on track, we must address the underlying inflationary pressures caused by deficit-spending of more than $6 trillion funded by a bloated Federal Reserve balance sheet, which is declining too slowly. Turning to the latest jobs report for June, the figures are disappointing, falling well below expectations. Only 99,000 net jobs were added after accounting for downward revisions in the two prior months. Moreover, many of these jobs were government jobs, straining the productive private sector that pays for those jobs. According to the household survey, employment has remained nearly stagnant since March, indicating a lack of substantial job creation. To make matters worse, the labor force participation rate has yet to return to its pre-pandemic rate, indicating millions of Americans are uncertain about their job prospects. Even for employed people, their purchasing power is down, and renters and individuals from low socio-economic backgrounds are struggling. If this is the outcome of “Bidenomics,” it’s clear that a different approach is necessary to restore the American economy. The government must rein in spending, and the Federal Reserve should be more aggressive in cutting its balance sheet. Despite the lackluster evidence that his initiatives are helping, President Biden continues to approve increased deficit spending through initiatives like the Inflation Reduction Act, which is estimated to cost over $1 trillion. The national debt has surpassed $32 trillion, translating to roughly $95,000 owed per American or almost $250,000 per taxpayer, far exceeding the country’s economic output. This continuous increase in spending, coupled with kicking the problem down the road for future generations to tackle, as seen in the latest debt ceiling deal, won’t effectively lower inflation or provide the economic relief Americans desperately need. A different direction is essential, involving responsible budgeting to curb excessive spending and align expenditures with means. Congress should consider passing a strict spending limit with a growth rate that better matches the average taxpayer’s ability to fund government spending, calculated based on the maximum rate of population growth plus inflation. If Congress had adhered to this maximum spending growth rate from 2003 to 2022, there could have been a cumulative $500 billion debt increase instead of the actual $19 trillion increase, resulting in $18 trillion in static savings for taxpayers. In essence, restraining spending now is pro-growth and will foster greater economic prosperity. The latest inflation and jobs reports suggest that the touted “Bidenomics” approach leaves much to be desired. To secure a brighter economic future, current economic strategies need serious reevaluation that focus on fiscal responsibility and sustainable growth. Originally published at The Daily Caller. Research: The Inflation Reduction Act's Costly New Tax Credits for Electric Vehicle Batteries4/10/2023  Executive Summary The U.S. Congress passed and President Biden signed into law the so-called “Inflation Reduction Act” (IRA) in August 2022. The IRA includes many provisions which are now estimated to cost $1.2 trillion over a decade per Goldman Sachs’ more recent analysis compared with the Congressional Budget Office’s (CBO) initial estimate of $391 billion. Part of this substantially higher estimated cost is because of the new cost estimates for tax credits for electric vehicle (EV) battery cells and modules manufactured in the U.S. Instead of the initially estimated cost of $30.6 billion by the CBO, new estimates based on more precise projections and growth in the EV market indicate that this could be as high as $196.5 billion (540% higher than initially estimated) per the Mercatus Center and Goldman Sachs. This higher estimate appears more accurate than the original CBO estimate given the large increase in the EV market and the expanding use of these tax credits. Given that the cost of these subsidies passed by Congress and communicated to the public appears to be substantially undervalued, the CBO and other nonpartisan agencies and committees responsible for providing Congress with accurate revenue estimates and sound economic analysis should reexamine their calculations. Originally published at Americans for Tax Reform.  The push to ditch reliable energy is out of control. Politicians are manipulating the energy market through subsidies, tax breaks, and environmental, social, and corporate governance (ESG) initiatives in regulations and government pensions.