Originally published at Kansas Policy Institute. Recent Internal Revenue Service (IRS) data underscore a significant trend: people and income continue moving from high-tax to low-tax states. The pandemic lockdowns accelerated this movement, and even as life returns to a semblance of normalcy, the exodus continues unabated as policies matter. The IRS reports migration data between states reveal that in 2022, California topped the list of net losers in adjusted gross income (AGI), shedding $23.8 billion. Other high-tax, blue states, New York, Illinois, New Jersey, and Massachusetts, were the biggest losers, collectively losing billions in AGI. Conversely, low-tax, red states like Florida, Texas, South Carolina, Tennessee, and North Carolina emerged as the biggest net gainers, with Florida alone attracting $36 billion in AGI. According to the Wall Street Journal, the flight from blue, high-tax states far surpasses pre-pandemic levels. California’s income loss in 2022 was nearly three times that of 2019. New Jersey saw a record net income loss, largely due to fewer New Yorkers relocating across the Hudson River. Although lower than during the pandemic, New York’s AGI loss was still about 50% higher in 2022 compared to 2019. This migration pattern illustrates a clear preference for states with lower taxes, less regulation, and more business-friendly environments. The top income-gaining states share common pro-growth policies that promote economic growth, highlighting the significant impact of state policies on migration decisions as people move with their feet. Kansas: A State of Concern For Kansas, the story is one of consistent outmigration. The net loss from domestic migration in 2022 marked the 28th out of the last 30 years, with a staggering loss of over $600 million and more than $2 billion over the last five years. This represents the second-highest loss in three decades, second only to 2017 when the state imposed its highest tax increase. The average state outmigration loss in Kansas, about $76,000 per return, indicates a broad spectrum of incomes are leaving. Moreover, Kansas’ biggest gains came from higher-tax states, and its losses went to lower-tax states. Johnson County, often hailed as Kansas’s economic engine, accounted for over half of the state’s AGI loss at $357 million in 2022. This marks the fifth out of the last six years that Johnson County has experienced a net loss. Despite having about 20% of the state’s population, it has borne a disproportionate share of the AGI loss, which coincides with efforts to shift the county politically left and impose significant property tax hikes that reduce affordability. Considering data from the Kansas Policy Institute’s Green Book and the Tax Foundation, it becomes clear that Kansas is not alone in facing these challenges. However, the extent of the problem in Kansas is particularly alarming compared to other states. The IRS data indicate that while many states have rebounded or stabilized post-pandemic, Kansas continues to struggle with significant outmigration. Economic and Policy Implications for Kansas The significant outmigration from Kansas has several implications:

Kansas’s Path to Prosperity In response to these challenges, Kansas must adopt a comprehensive approach that includes responsible budgeting, tax relief, and the removal of barriers to work and education. Here are some key policy recommendations:

Addressing Migration Trends The migration trends underscore the importance of adopting free-market, pro-growth policies prioritizing economic freedom and personal responsibility. Kansas can learn from states that have successfully attracted residents and income by implementing policies that reduce the size of government, lower taxes, and eliminate burdensome regulations. The continued outmigration from Kansas highlights the urgent need for policy reforms that can reverse this trend. By learning from the successes of states that have managed to attract people and income, Kansas can chart a path toward a more prosperous future. Addressing the underlying issues driving residents away is crucial to ensuring the state’s long-term economic stability and growth.

0 Comments

Originally published at Mackinac Center.

Michigan’s economic health and fiscal policies are critical for its future prosperity. Understanding where the state stands in various economic freedom measures can help identify areas for improvement and guide policy decisions. Fraser Institute Rankings The Fraser Institute publishes the Economic Freedom of North America index, which evaluates how states' policies support economic freedom. The index considers three main areas: government spending, taxes and labor market regulations. Higher scores indicate greater economic freedom. In the latest report, Michigan ranks 31st in economic freedom among U.S. states. This ranking reflects areas where Michigan lags in supporting economic freedom and highlights opportunities for policy improvements. Government Spending: This component measures the size of government relative to the economy. Lower government spending relative to GDP indicates more economic freedom. Michigan ranks 28th, suggesting a need to control spending better. Taxes: This component assesses the impact of taxes on economic incentives. Higher tax burdens discourage investment and economic activity. Michigan ranks 19th, indicating room for tax reforms to enhance economic freedom. Labor Market Regulations: This component examines labor market regulations, such as minimum wage laws and forced membership in a labor union. Stricter regulations can reduce economic freedom by limiting the flexibility of labor markets, thereby making it more difficult for employers and employees to find the best fit for each other. Michigan ranks 38th, so improving labor market regulations can help Michigan enhance its economic freedom ranking — improving opportunities for employers and employees alike. Economic Factors Labor Market: The latest BLS data shows Michigan’s unemployment rate is 3.9%, the same as the U.S. rate. But the number of employed persons increased by only 0.9% over the past year, half the national growth rate of 1.8%. The slower hirings highlight the need for more job opportunities from faster economic growth in Michigan. Employment Trends: According to the Michigan Labor Market Information, the state has seen slow employment growth, with particular struggles in industries such as manufacturing and financial activities. This emphasizes the need for pro-growth policies to make it easier for businesses to grow, leading to more and better-paying jobs. Labor Force Participation Rate: Michigan’s labor force participation rate — the share of people ages 16 and over working or seeking work — is 61.7%. That’s lower than the national average of 62.3%. If you, as a consumer, find fewer employees when you need to talk to someone at a business, that’s an example of why the participation rate matters. Wage Growth: Wage growth in Michigan has been slower than the national average, affecting the economic well-being of its residents. Path to Improvement Tax Reform: Lowering tax rates can support economic growth and attract business investment. Reducing the state income tax and exploring other tax reforms can make Michigan more competitive with other states. A more favorable tax environment can increase business activity, job creation and wages. Regulatory Efficiency: Streamlining regulations can reduce the burdens businesses face. By simplifying regulatoryprocesses and reducing bureaucratic hurdles, Michigan can make it easier for businesses to start and grow, leading to a more vibrant economy with more goods and services available. Spending Discipline: Implementing strict budgetary controls can ensure that spending growth does not exceed the combined rate of inflation and population growth, maintaining the state government’s fiscal stability. Michigan can achieve long-term fiscal health by focusing government spending on areas with the largest impact and eliminating wasteful spending. Labor Improvement: Reinstating a right-to-work law will lead to more jobs. By addressing its economic and fiscal policy weaknesses, Michigan can improve its rankings and create a more robust and dynamic economy. Sustainable budgeting, tax reform and regulatory efficiency are key to unlocking Michigan’s economic potential. By implementing these strategies, Michigan can enhance its economic freedom, attract investment and ensure long-term prosperity for its residents.  Originally published at Econlib.

Amid a heated election year, the teachings of economist Friedrich Hayek provide a guiding beacon, urging us to transcend partisan lines and champion free-market capitalism that benefits everyone. I recently interviewed Dr. Bruce Caldwell of Duke University about his book, Hayek: A Life, 1899-1950, who helped shed light on Hayek’s views on pressing issues today. As we navigate the complex landscape of governance, we should heed Hayek’s call for market-based approaches, especially with trade and immigration, where the clash of political ideologies often obscures the path to rational decision-making. Hayek’s teachings underscore the need for policy approaches prioritizing broader economic health rather than conforming to the whims of political affiliations or interest groups. He did not advocate for simplistic labels like “left and right” but viewed political thought as a triangle, with socialism, conservatism, and liberalism representing the three points. He favored liberalism, in the classical sense. His writings compel us to consider whether policies align with our principles and values. One example is trade protectionism, with tariffs enacted while president and pushed again by Donald Trump. Hayek’s book, The Road to Serfdom, cautioned against the pitfalls of protectionism and advocated for free-market principles that embrace competition in free trade. While protectionist measures like tariffs may appeal to certain political bases, they come at the expense of economic efficiency and growth. They ultimately cost us more for purchases and inhibit our choices as competition is artificially manipulated where it would otherwise organically select the best providers of resources. A Hayekian approach to trade involves understanding that dynamic economies thrive on diversity and exchanging goods and services across borders. Another issue at the forefront of political debates that Hayek’s approach helps shed light on is immigration. He recognized that allowing the free movement of individuals fosters economic dynamism and innovation. Policies that restrict immigration solely for political gain risk stifling economic growth and impeding the exchange of ideas that fuels progress. A Hayekian perspective on immigration advocates for policies that acknowledge the economic benefits of a diverse and dynamic workforce. Instead of succumbing to populist narratives that frame immigration as a threat, Hayek prompts us to view it as an opportunity. An influx of skilled and motivated individuals can contribute to a vibrant economy, filling gaps in the labor market and injecting fresh perspectives that drive entrepreneurship. Too often, misinformation about immigration has led even conservatives to favor more government involvement in tightening borders and deportation. However, as Hayek outlined in his development of “the knowledge problem,” expecting a government of people with limited knowledge of the issue and tradeoffs from policy choices too often results in worse outcomes. The people in government do not and never will have all the answers. Instead, collecting everyone’s ideas in the market leads to having the most available knowledge and, therefore, better outcomes. In short, government failures are worse than any perceived market failures. Taking a cue from Hayek, we should strive for more free trade agreements, especially with our allies, which means an end to all tariffs and other barriers. We should also enact market-based immigration policies that balance national security concerns with the economic advantages of attracting talent from diverse backgrounds. As we prepare to select our nation’s president for the next four years, Hayek’s teachings serve as a guidepost, urging us to prioritize people’s well-being over the allure of party-centric agendas. Embracing a Hayekian perspective requires a willingness to critically evaluate policies based on their economic merit rather than their alignment with partisan ideologies. Only by doing so can we navigate the complex economic landscape and ensure a prosperous and dynamic future for all.  Argentina’s new self-described “anarcho-capitalist” President, Javier Milei, is raising eyebrows worldwide with his aggressive attempts to restore the nation’s abysmal economy. On December 20, he signed a decree to remove many government regulations stifling international trade and domestic activity.

With Argentina’s poverty rate soaring to 40.1 percent in early 2023 and its debt burden owed to the International Monetary Fund (IMF) now $45 billion along with its other mountains of debt, the time is now for a no-nonsense pro-growth approach that gets the government out of the way. Since Milei’s inauguration on December 10, he’s set out bold initiatives. These include reducing government spending by as much as five percent of the nation’s GDP, slashing the number of federal ministries by half to nine, and, most notably, declaring that he will devalue the nation’s currency, the peso, by more than 50 percent. To paint a picture, some estimate that the decision to devalue the peso and other policy changes could bring already rapid inflation of more than 160 percent up to as high as 300 percent. Onlookers have been quick to criticize these actions and their potential effects on the country, but desperate times call for desperate measures. And the US, most of all, should not point fingers. If anything, we could stand to learn a thing or two from Milei’s proactive approach. While Milei’s moves will temporarily exacerbate inflation and further strain the economy, as he’s acknowledged, it also aims to enhance the country’s future. Moving from a government-dominated, top-down economy to one built on free-market capitalism is a significant institutional shift. We already know from the work of economist Douglass North that these economic changes are what support more ways to let people prosper, but that the adjustment period will be challenging. There are currently many hindrances to the free exchange of people in the marketplace, and these inefficiencies take time to correct through a well-functioning price system. But after this “shock therapy” comes a brighter future. There will also likely be a move away from the country’s currency of the peso to the US dollar, which should help stabilize markets, inflation, and economic activity. This would provide a better anchor than the peso does today, even though the anchor of the dollar has its own troubles. It’s hard to conceive how Argentina was one of the world’s wealthiest nations only a century ago. Once surpassing European powers in its economic strength, Argentina’s standing took a nosedive in 1929 when it abandoned the gold standard. The shift began a challenging period as protectionist trade policies, influenced by former Argentina President Juan Peron, eroded its once-thriving trade status. Moreover, excessive regulations further distorted price signals, and the emergence of a military dictatorship during the 70s and 80s brought everything crashing down. But the troubles didn’t stop there. In 2001 and 2002, Argentina experienced a severe economic crisis when the government partially defaulted on its debt, froze bank accounts, and abandoned the dollar. The aftermath was characterized by economic collapse, unemployment, and widespread political and social unrest. Argentina had a rough start to the 21st century, and its challenges have only snowballed since. Rampant inflation, exacerbated by the central bank’s relentless money printing to cover mounting debts, has led to the plummeting credibility of the Argentine peso. So Milei’s strategy will likely worsen things before they can improve. Along with shrinking the government, his objective to balance the budget by the end of 2024 is a historical measure aiming to alleviate debt with spending cuts instead of tax hikes, often the go-to when more money is needed. But as the work of the late economist Alberto Alesina confirms, the best path forward for austerity is to cut government spending, not raise taxes, to avoid a deeper recession and higher debt. Cautious optimism is warranted, as the nation’s leaders have a history of abusing power, and we can’t foresee how Milei will wield his influence over time. One concerning move is his intention to raise taxes on grain, which would be a big blow to many farmers. But even so, things should look up if he sticks to what he initially set out to do and what he has done so far. As the US observes Argentina’s economic trajectory, it must take note of the cautionary tale embedded in Milei’s approach. The focus on reducing government spending and narrowing the scope of government aligns with the prescription needed to combat inflation not just there but here. America’s inflationary challenges, rooted in a bloated Federal Reserve balance sheet helping fund excessive government deficit-spending, require Congress to take decisive action. Inflation will strain household budgets until the reins are pulled on government spending, and the Fed cuts its balance sheet more aggressively. We can’t be too proud to take a tip from Argentina. The perilous outcomes of unchecked government spending can manifest anywhere; strategic policies such as responsible spending limits only become more necessary the longer their implementation is delayed. Argentina’s bold moves, though met with skepticism, could be the beacon the US needs to navigate its own economic storms successfully. But until then, let’s keep cheering what the classical liberal President Milei is doing in Argentina. Originally published at AIER.  New Hampshire has displaced Florida as the most economically free state, according to the Fraser Institute’s new Economic Freedom of North America report. The findings demonstrate that, while size and location account for some of a state’s success, free-market friendliness is everything.

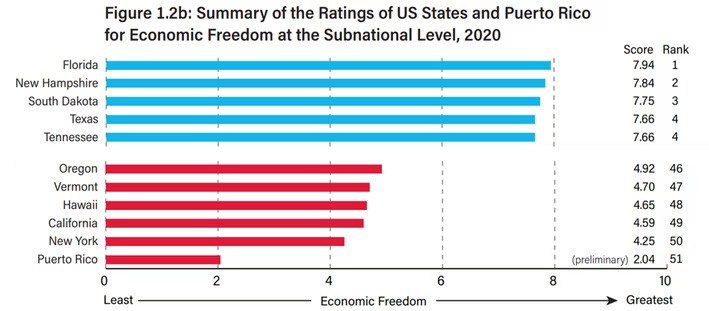

This annual report, now in its nineteenth edition (one of us is its lead author), offers a comprehensive analysis of economic freedom using 2021 data (the most recent available). The report defines economic freedom as “the ability of individuals to act in the economic sphere free of undue restrictions.” The top five states in the report are what one might expect. Unsurprisingly, these top five states tend to spend less, do not have a personal income tax, and have reasonable labor market regulations. New Hampshire improved its economic freedom score from 7.92 to 7.96 to retake the top spot after losing it in the prior year. Florida fell from the top as it dropped from 7.97 to 7.80. Tennessee declined from 7.85 to 7.73 for third place. Texas inched down from 7.67 to 7.64, and South Dakota fell from 7.73 to 7.59. Conversely, the least economically free states were New York (4.09), California (4.27), Vermont (4.27), Oregon (4.56), and Hawaii (4.58), all of which lost ground since the last report. Each state has some of the highest rates of taxation and government spending, as well as stringent labor market regulations. In the freest quartile of states, the population grew on average by one percent in 2022, compared to a 0.1 percent decline in the least free quartile. Americans are voting with their feet in favor of economic freedom, fueling the flood of California and New York refugees pouring into Texas and Florida. Furthermore, hundreds of research papers have used the index, almost universally finding that more economic freedom correlates with positive outcomes such as higher incomes, faster income growth, lower unemployment, and more entrepreneurial activity. Bluntly, states with less government spending, lower taxes, and less burdensome labor market regulations have more opportunities for people to flourish. While the report has many compelling findings, two states stand out: New Hampshire and South Dakota. New Hampshire has embarked on a journey of economic liberation in recent years. In 2021, the state had significantly reduced taxes and had begun its ongoing quest to abolish interest and dividends taxes, a huge step toward reducing the tax burden. While the state’s taxes are already relatively low, they continue to decline. New Hampshire does not have a state minimum wage, reducing labor market regulations allowing wages to be market-determined instead of government-mandated. This helps attract young people and others with less experience, training, or education. As a result, household incomes in the Granite State are among the highest in America. Consistently, states with low minimum wages draw more people than average, while states with high minimum wages — California, New York, Illinois — are experiencing out-migration. Not only businesses, but also parents and students in New Hampshire have seen their freedom expand through school choice, which will help improve economic outcomes. In its commitment to providing school choice for all, the state has implemented education freedom accounts. These accounts empower parents to make educational choices that best suit their children’s needs while promoting a competitive schooling landscape that benefits teachers and students. South Dakota, too, has made remarkable strides in economic freedom, which became particularly evident during the challenging times of the COVID-19 pandemic. In 2021, the state was an exemplar of resilience and recovery, boasting the lowest unemployment rate in the country after the pandemic hit. Its output recovered pre-pandemic levels before any other state, with its real GDP growing by nearly five percent. Fortunately, the state never issued stay-at-home orders or mask mandates. Instead, state leadership allowed individuals to make decisions concerning personal health and safety, a common theme that has assisted the state’s flourishing. One key factor contributing to South Dakota’s economic success is its unique tax policies. The state is a rare tax haven with no corporate or personal income taxes and no durational limits on trusts. By allowing families to hold wealth indefinitely within trusts, and letting earners keep more of their hard-won incomes, South Dakota has remained a top spot for entrepreneurs. This tax-friendly environment in South Dakota reaffirms a fundamental economic principle: spending and taxes influence individual choices. As evidenced by the state’s success, people gravitate toward regions with lower tax burdens and more favorable financial policies. The success stories of New Hampshire and South Dakota underscore the power of economic freedom in fostering human flourishing. In a society where consumers are free to choose, businesses must continually improve the quality and affordability of their products and services. This dynamic situation fuels increased productivity and benefits everyone in the economy. Economic freedom isn’t just about lower taxes. It encompasses a broader spectrum of policies that allow individuals to make decisions about their lives, finances, and education. It’s about governments empowering people with opportunities rather than restricting or directing activity. By following New Hampshire and South Dakota’s lead, other states can unleash the power of economic freedom to boost investment, create jobs, improve human flourishing, and make their regions more competitive and attractive places to live. In a world where economic challenges are ever-present, these states serve as beacons of hope, proving that less government spending, lower taxes, and reduced labor market regulations can pave the way to a brighter economic future, full of greater opportunity for all. Originally published at Daily Caller. Today, I'm joined on episode 68 of the "Let People Prosper" show by Dr. Carlos Carvalho who is a Professor in Statistics at the University of Texas-Austin and Director of the Salem Center.

Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. Also, subscribe and see show notes for this episode on Substack (www.vanceginn.substack.com) and visit my website for economic insights (www.vanceginn.com). We discuss: 1) Economic lessons that Dr. Carvalho learned living in Brazil during the 80s while the nation suffered from hyperinflation and how it relates to current overspending by Congress in the U.S. (see more on this in my episode with Dr. John Cochrane); 2) The importance of federalism and letting markets work; and 3) How the pandemic was mishandled and the importance of understanding tradeoffs.  The Fraser Institute recently released its annual “Economic Freedom of the World” report. While the US inched up one spot from its previous ranking to fifth-best, this ranking remains below its peak of third-best in 2000.

A first-time finding not seen in any of 27 prior years: Hong Kong fell from first place. Singapore nudged out Hong Kong for the top spot by 0.01 points. While that rating may seem minuscule, the implications of how both countries got here are not. The report, which shows comprehensive data from 2021, assesses economic freedom among nations across five major areas: size of government, legal system and property rights, sound money, freedom to trade internationally, and regulations. According to the Fraser Institute’s Matt Mitchell, “The most important component of economic freedom…is the rule of law section…you need to be able to trust that the contracts you form and the property you acquire will be protected. We found that regulatory barriers and the rule of law matter more than taxes [for economic freedom].” Given these guidelines, Hong Kong’s fall isn’t surprising. China’s special administrative region allowed to manage most of its own affairs under the “one country, two systems” precedent since 1997, Hong Kong’s independence has been seriously threatened since 2020 with the passage of China’s new security law. Today, as a result, Hong Kong has one of the fastest-growing political prisoner populations worldwide. Although the protection of Hong Kong’s independence under the system was set to last until 2047, it seems unlikely that China will keep its promise. Over the past two years, Hong Kong’s economic freedom ranking dropped by a substantial 0.40 points, a total decline of 0.64 points since its highest rating of 9.19 in 2010. This is much steeper than the average economic freedom drop worldwide following the pandemic, which is the lowest average score since 2009, pointing to China’s harsh policies as a primary factor. China’s recent security law inhibits free speech and impartial justice, integral to the rule of law which is the foundation upon which individuals can construct their economic aspirations, with trust as the indispensable glue. But trust isn’t just a legal concept. It’s deeply interwoven with a nation’s cultural fabric. Trust is the bedrock upon which economic prosperity thrives, allowing individuals and businesses to engage in voluntary exchanges with confidence. Recent developments, including China imposing significant trade barriers, limits to foreign labor employment, increased business costs, and new attempts to restrict media, tarnished Hong Kong’s overall score. The lesson from the report rings loud and clear: A small government footprint in fiscal matters alone won’t guarantee economic freedom. What’s needed is a symphony of elements: the rule of law, property rights, stable currency, open trade, and sensible regulation. High-income industrial economies like now top-ranking Singapore shine in areas related to legal systems, property rights, sound currency, and international trade while keeping their government size compact. The report is a valuable tool for deciphering economic freedom’s complexities, and the factors underlying the success story of Singapore and Hong Kong’s decline drive home the point that tax rates don’t solely determine economic prosperity. It hinges on the quality of institutions, the rule of law, and the cultural values that champion trust and voluntary exchange. As the US strives to enhance its economic freedom, the country would be wise to heed the lessons offered by Singapore’s rise and Hong Kong’s fall. In particular, this should include removing government barriers so that there are more ways for free people to prosper. Originally published at American Institute for Economic Research.  Originally published at American Institute for Economic Research.

The Fraser Institute recently released its annual “Economic Freedom of the World” report. While the US inched up one spot from its previous ranking to fifth-best, this ranking remains below its peak of third-best in 2000. A first-time finding not seen in any of 27 prior years: Hong Kong fell from first place. Singapore nudged out Hong Kong for the top spot by 0.01 points. While that rating may seem minuscule, the implications of how both countries got here are not. The report, which shows comprehensive data from 2021, assesses economic freedom among nations across five major areas: size of government, legal system and property rights, sound money, freedom to trade internationally, and regulations. According to the Fraser Institute’s Matt Mitchell, “The most important component of economic freedom…is the rule of law section…you need to be able to trust that the contracts you form and the property you acquire will be protected. We found that regulatory barriers and the rule of law matter more than taxes [for economic freedom].” Given these guidelines, Hong Kong’s fall isn’t surprising. China’s special administrative region allowed to manage most of its own affairs under the “one country, two systems” precedent since 1997, Hong Kong’s independence has been seriously threatened since 2020 with the passage of China’s new security law. Today, as a result, Hong Kong has one of the fastest-growing political prisoner populations worldwide. Although the protection of Hong Kong’s independence under the system was set to last until 2047, it seems unlikely that China will keep its promise. Over the past two years, Hong Kong’s economic freedom ranking dropped by a substantial 0.40 points, a total decline of 0.64 points since its highest rating of 9.19 in 2010. This is much steeper than the average economic freedom drop worldwide following the pandemic, which is the lowest average score since 2009, pointing to China’s harsh policies as a primary factor. China’s recent security law inhibits free speech and impartial justice, integral to the rule of law which is the foundation upon which individuals can construct their economic aspirations, with trust as the indispensable glue. But trust isn’t just a legal concept. It’s deeply interwoven with a nation’s cultural fabric. Trust is the bedrock upon which economic prosperity thrives, allowing individuals and businesses to engage in voluntary exchanges with confidence. Recent developments, including China imposing significant trade barriers, limits to foreign labor employment, increased business costs, and new attempts to restrict media,l tarnished Hong Kong’s overall score. The lesson from the report rings loud and clear: A small government footprint in fiscal matters alone won’t guarantee economic freedom. What’s needed is a symphony of elements: the rule of law, property rights, stable currency, open trade, and sensible regulation. High-income industrial economies like now top-ranking Singapore shine in areas related to legal systems, property rights, sound currency, and international trade while keeping their government size compact. The report is a valuable tool for deciphering economic freedom’s complexities, and the factors underlying the success story of Singapore and Hong Kong’s decline drive home the point that tax rates don’t solely determine economic prosperity. It hinges on the quality of institutions, the rule of law, and the cultural values that champion trust and voluntary exchange. As the US strives to enhance its economic freedom, the country would be wise to heed the lessons offered by Singapore’s rise and Hong Kong’s fall. In particular, this should include removing government barriers so that there are more ways for free people to prosper.  On September 11, 1960, a group of young conservatives gathered in the home of William F. Buckley, Jr., in Sharon, Connecticut. For decades, the timeless ideals embodied in the document they produced animated the American conservative movement.

Today’s public policy challenges are different than the ones faced by the Sharon Statement signatories in 1960. Authoritarianism is on the rise both at home and abroad. More and more people on the left and right reject the distinctive creed that made America great: that individual liberty is essential to the moral and physical strength of the nation. In order to ensure that America’s best days are ahead, we affirm the following principles:

See full list of signatories and the original post at Freedom Conservatism.  Oren Cass, founder of the think tank American Compass, presents a vision of the “new right” in his recently released book, Rebuilding American Capitalism. In it, he advocates for a top-down approach to governance in response to what he perceives as free-market failures.

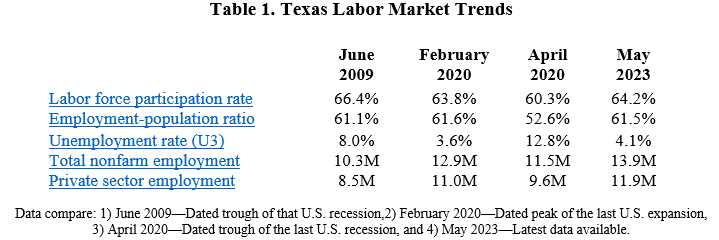

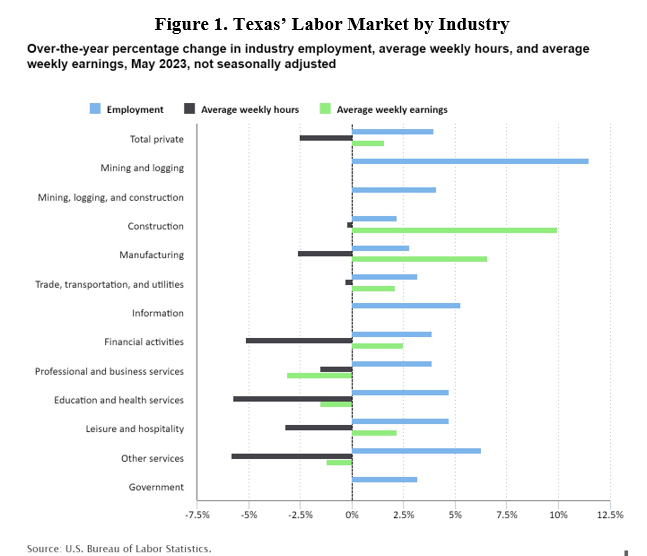

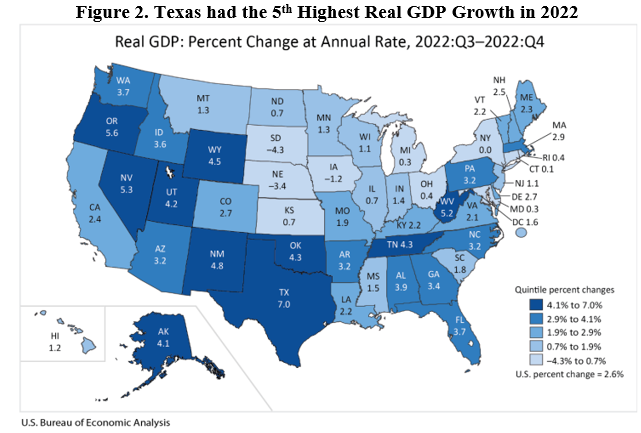

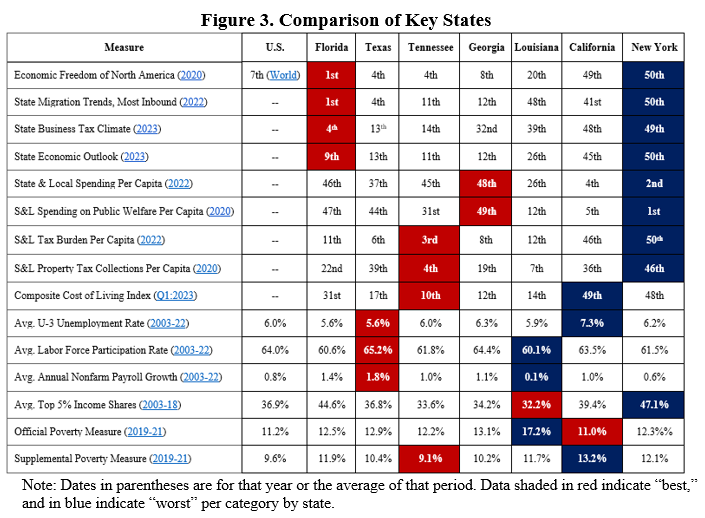

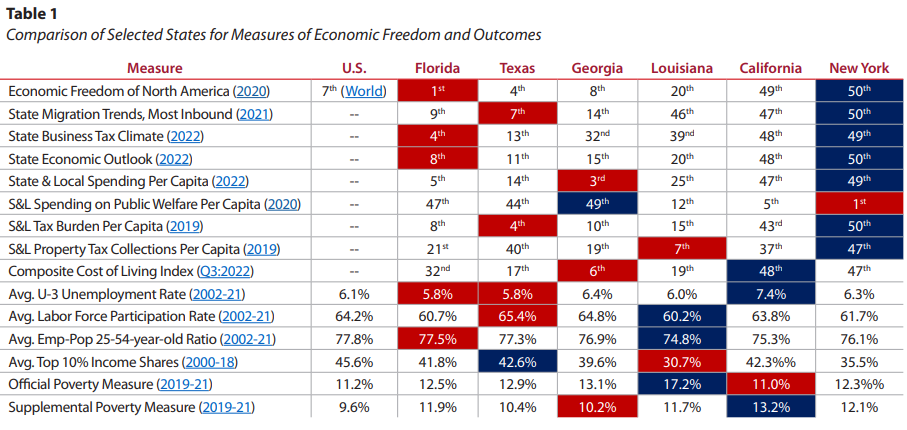

He tends to believe that certain politicians can and should shape markets to achieve desired outcomes rather than letting free markets, which are free people, work. This attempt to rebrand not only the right but capitalism itself is flawed, as history and sound economics prove. Cass pinpoints growing concerns in the economy to help bolster his arguments, like poor inflation-adjusted wage growth and lack of strong social and family units. These are problems making it harder for people to prosper, but they are not, as he suggests, evidence that free-market capitalism has failed. But these problems–if they are problems, as Scott Winship and Jeremy Horpedahl recently found that people are thriving–aren’t the results of free markets but are driven instead by government failures. These failures include bloated government spending, restrictive regulations, high tax burdens, excessive safety net programs, costly tariffs, and other barriers to entry in the marketplace. They are imposed by politicians and government bureaucrats, hindering competition, disrupting entrepreneurial endeavors, impeding wage growth, and destroying human flourishing. Cass contends that capitalism only works under the right conditions, which must be facilitated by the government to keep the labor market and the economy strong. Rather than what he calls the “Old Right’s market fundamentalism” of fewer regulations and less government intervention being best, he welcomes more government with certain politicians in power. He proudly makes markets the scapegoat and, with it, globalization and financialization. In the book’s foreword, Cass writes: "Globalization must be replaced with a bounded market that restores the mutual dependence of American capital and labor and invites the trade and immigration that benefit American workers. Financialization must be reversed so that both talent and capital in pursuit of profit find their best opportunities in productive investment rather than extraction and speculation." Believing that more opportunities in the form of globalization inhibit rather than help Americans is the same faulty basis with which people discourage immigration and trade, which are central to thriving economies. But the crux of Cass’s theory is that he believes markets must be molded, even referring to work by the father of modern economics Adam Smith. Conveniently, he fails to cite the economist Frederick Hayek, who built on Smith’s ideas, to identify spontaneous order, the basis of free-market capitalism that argues economic growth and prosperity arise from voluntary transactions by free people, not government guidance and control. This “new right” idea was debunked long before Cass came along by Hayek (and others), who also highlighted the “knowledge problem” associated with central planning. He argued that no central authority can possess the information necessary to make efficient decisions for an entire economy. The complexity of economic interactions and the constant flux of information require decentralized decision-making and market mechanisms to aggregate and incorporate local knowledge effectively. Hayek’s insights emphasize the limitations of top-down control and the importance of allowing market forces and individual actors to shape economic outcomes based on their localized knowledge and preferences from the bottom-up. But Cass would have it that government is heralded as the keeper of knowledge and the arbiter of good decisions rather than encouraging freedom and liberty in individuals, i.e., the essence of capitalism. Capitalism allows individuals to pursue their economic aspirations and make decisions based on their knowledge and preferences through voluntary exchange within rules of the game set by limited government. Through this freedom, innovation, entrepreneurship, and competition thrive, leading to greater prosperity for all. History is full of successful economic transformations driven by leaders who championed limited government and free markets. Former President Calvin Coolidge cut government spending, cut taxes, and reduced the national debt, providing more paths for human flourishing. Likewise, former President Ronald Reagan cut taxes, tried to rein in government spending, and reduced regulations, unleashing economic growth and job creation. Both of them understood that cutting spending, reducing taxes, and removing excessive regulations create an environment where businesses thrive and workers can benefit. Their approaches embraced the power of individual freedom and self-determination, not top-down control that breeds the opposite. Oren Cass’s theory of the “new right” and its embrace of government fundamentalism misunderstands the principles of capitalism and human behavior. Top-down approaches, rooted in centralized control and regulation, do not lead to economic prosperity or personal freedom no matter who is in charge but do distort the efficient allocation of resources, undermine the adaptability of markets, and reduce opportunities to let people prosper. To achieve a thriving and prosperous economy, we must adhere to and strengthen the principles of free-market capitalism, which too much of our economy today is deprived of when considering healthcare, education, transportation, manufacturing, and the labor market. This should include embracing limited government, voluntary exchange, and individual freedom as the pillars of strong families, productive workers, and profitable employers. Economist Milton Friedman noted what this debate is about decades ago. “The problem of social organization is how to set up an arrangement under which greed will do the least harm; capitalism is that kind of a system.” And while “history suggests that capitalism is a necessary condition for political freedom,” it’s clearly “not a sufficient condition.” But capitalism is the best system yet that has supported economic prosperity and political freedom. The problem is that we have had too little free-market capitalism for people to thrive because of too much government. There’s no need for a “new right” of big-government progressive policies offered by Cass and others when free-market capitalism of the “old right” is too often missing in our lives. Originally published at Econlib. Key Point: Texas is a leader in job creation over the last year and since February 2020. But Texas faces major headwinds as the recently ended 88th Legislature looked more like California than what is expected from the free-market bastion of hope and prosperity in Texas, which could change during special sessions but nothing certain yet. The path forward must be one of free-market capitalism instead of expanding the size and scope of government to let people prosper. Overview: Texas has reached a new record high in total nonfarm employment for the 20 straight months. The 88th Legislature ended on May 29 and went straight into a special session to provide property tax relief but that hasn’t happened yet, and the second special session ends on June 27. Instead, the Legislature passed the largest spending increase in the state’s history, the most money for corporate welfare, one of the largest expansions of safety nets, and no school choice. This was a huge, missed opportunity for Texas that will set up a fiscal cliff with so much spending, less competition with fiscally conservative states, and less opportunity for flourishing which combined will stop the Lone Star State from being a leader in the country. Labor Market: The best path to let people prosper is free-market capitalism as it is the best system that supports jobs and entrepreneurship for more people to earn a living, gain skills, and build social capital. Table 1 shows Texas’ labor market for May 2023.  The payroll survey shows net nonfarm jobs in Texas increased by 51,000 last month, resulting in increases for 36 of the last 37 months, to bring record-high employment to 13.9 million. Compared with a year ago, total employment was up by 529,800 (+4.0%)--fastest growth rate in the country—with the private sector adding 472,000 jobs (+4.1%) to 11.9 million and the government adding 57,800 jobs (+2.9%) to 2.0 million. But there continued declining inflation-adjusted average weekly earnings in most industries in Texas (see Figure 1).  The household survey shows that the labor force participation rate is higher and employment-population rate is slightly lower than in February 2020, but the former is well below June 2009 at the trough of the Great Recession. The state’s unemployment rate of 4.1% is higher than the U.S. rate of 3.7% but this is weak indicator as it’s highly volatile based on changes in the labor force. Economic Growth: The U.S. Bureau of Economic Analysis (BEA) reported the real gross domestic product (GDP) by state for 2022. Figure 2 shows Texas had the fifth fastest real GDP growth of +3.4% to $1.9 trillion (above the U.S. average of +2.1% to $20.0 trillion).  The BEA also reported that personal income in Texas grew by 5.3% to $1.9 trillion in 2022 which was the third highest in the country. This is behind Idaho (+6.2%) and Colorado (+5.4%) but well above the U.S. growth rate of 2.4% (to $21.8 trillion). Bottom Line: As Texans face an affordability crisis from high inflation and high property taxes and an uncertain future with the U.S. economy likely in a deepening recession, they need substantial relief to help make ends meet. Other states are cutting, flattening, and phasing out taxes, passing responsible budgets, and passing school choice, so Texas should have made bold reforms to support more opportunities to let people prosper, mitigate the affordability crisis, and withstand destructive policies out of D.C. Figure 3 provides a comparison of the size of government, economic freedom, and economic outcomes among the four largest states, Tennessee, Georgia, and Louisiana.  While Texas does relatively well, there is much more to do for more liberty and prosperity. Unfortunately, the Texas Legislature failed to achieve these needed policy objectives in the regular session of 2023 so Governor Greg Abbott (R) called them back to provide property tax relief which hasn’t yet so will have to call them back again for this along with passing school choice and should bring them back to eliminate corporate welfare and expansion of safety net programs.

Free-Market Solutions: The Texas Legislature should improve the Texas Model by:

In our system of federalism, competition matters among the states. This reality has been on full display the past few years as people fled big-government states like California and New York to more limited government states like Texas and Florida. But what works best?

The American Legislative Exchange Council’s (ALEC) “Rich States, Poor States” report is a recent comparison of states. Utah, a politically red state, ranks second best in economic performance and first in economic outlook for 2023. Texas, the largest red state, ranks seventh in performance and 13th in outlook. On the surface, this looks pretty straightforward, but a closer look shows that Texas is a leader but needs much improvement. The report measures performance based on the growth of state gross domestic product, absolute domestic migration, and non-farm payroll from 2011 to 2021. The economic outlook is based on 15 state policy variables, including tax burden, debt and other factors. Utah beats Texas for state GDP and nonfarm payroll growth rates, while Texas wins for absolute domestic migration. This is thanks to people leaving states like California and New York, which rank 45th and 50th, respectively, in outlook, and coming to Texas in search of more economic freedom. Should Utah be a model for Texas? Not necessarily. Note that Utah’s population is about 3.4 million. Texas has more than 30 million people or nearly nine times more people than Utah. Utah is also less diverse, with 77.2% of its population being white, 14.8% Hispanic, and 1.5% black, compared with Texas’ population being 40.3% white, 40.2% Hispanic, and 13.2% Black. Texas also has twice the share of foreign-born residents, with 17.0%, whereas Utah has just 8.5%. Utah has a much lower poverty rate at 8.6% compared with 14.2% in Texas. Clearly, there are significant differences between these two red states. And what works well in Utah likely may not fit well in Texas, given their substantially different demographics and economies. While the ALEC report is insightful, a cursory glance at the two ranks is just that. Considering all the metrics it provides along with state population and diversity, there’s a more holistic picture of which states are thriving. A more reasonable comparison for Texas based on economic and population sizes and diversity is the second largest red state of Florida. Florida has a population of about 22 million, with 52.7% white, 26.8% Hispanic, and 17.0% Black, while 21.0% is foreign-born, and the poverty rate is 13.1%. According to ALEC’s report, Florida ranks first for performance, better than Utah and Texas, and 9th for outlook, better than Texas. Texas and Florida boast business-friendly policy climates, typically spend responsibly, have no state income tax, and are right-to-work states. And the performances of their economies are robust based on multiple indicators. But two of the biggest factors that put Florida above Texas are the same ones that help put Utah above Texas now and for the foreseeable future: lower property tax burden and universal school choice. According to the Tax Foundation, individuals have the 6th highest property tax burden in Texas, 26th in Florida, and 43rd in Utah. Texas’ outrageous property taxes, which are high in large part due to too much local spending, is causing an affordability crisis as home and property values have risen faster than wages for too long. If businesses perceive the cost of doing business as too high due to high property taxes, they may choose to locate elsewhere, which results in less investment, economic growth, and job creation. This is why Texas should spend responsibly and use the at least $33 billion surplus to compress the school district maintenance and operations property taxes that are essentially controlled by the state’s school finance formulas. Combine this with spending restraint at the state and local levels and Texas could put property taxes on a path to elimination within a decade so that Texans can finally fulfill their right to own property while ending a bad wealth tax. Finally, when it comes to school choice, Utah and Florida joined the universal school choice revolution this year, while Texas is still fighting for it. Universal school choice is critical for improved state economies as it’s linked to improved student outcomes and increased teacher pay, both essential to becoming more competitive and producing a population with less criminal activity and higher economic earnings, to name just a few benefits. In short, competition matters! While it’s misleading to declare that Utah or Florida economically outperform Texas overall based on the differences outlined here, they do put pressure on Texas to improve or risk falling behind. Decreased property taxes and universal school choice mean more freedom, which empowers people to prosper. Time is running out this session so the Texas Legislature must act promptly. Originally published at The Center Square. In today's episode of the "Let People Prosper" podcast, which was recorded on February 24, 2023, I'm joined by Dr. Vincent Geloso, who shares his insights on:

Dr. Geloso’s and other info (here):

Louisiana is one of the most federally dependent states in the country, ranking 10th in a recent analysis.

The personal finance website WalletHub released a report Wednesday that ranked states’ dependency on the federal government based on three metrics: return on taxes paid to the federal government, share of federal jobs, and federal funding as a share of state revenue. The study ranked Louisiana in 10th overall with a score of 57.46, though the state government’s dependency ranked third. Residents’ dependency was ranked 22nd. Vance Ginn, chief economist at the Pelican Institute, told The Center Square much of Louisiana’s dependency derives from the state’s high poverty rate — 19.6% in 2022 — and the federal funds from various programs that flow into the state as a result. Forty-four percent of all state funding in Louisiana comes from Congress, and the Pelican Institute is working on “finding ways for Louisiana to have a comeback” that boosts businesses and employment, which in turn reduces poverty. “Louisiana is overly dependent on the federal government and the way to reduce that depends on getting more Louisianans back to work,” he said. “The way to get people back to work is removing barriers in the private sector, restraining government spending, providing tax relief, and reducing regulations.” The WalletHub analysis shows only state governments in Alaska and Wyoming receive more funding as a share of state revenues than Louisiana. Neighboring Mississippi ranked third overall in the study, while Arkansas was ranked 28th and Texas 29th. Other states in the top 10 most dependent on federal funding include Alaska in first, followed by West Virginia, Mississippi, Kentucky, New Mexico, Wyoming, South Carolina, Arizona, and Montana. New Jersey was ranked as the least dependent state, followed by Washington, Utah, Kansas, Illinois, California, Massachusetts, Iowa, Delaware, Nevada, and Colorado. The analysis also derived an average ranking for red and blue states, based on how residents voted in the 2020 presidential election. Democratic states produced an average ranking of 30.68, compared to the average ranking of 20.32 in Republican states, suggesting Republican states are generally more dependent than Democratic states. The study also examined how tax rates factor into the equation. Louisiana fell into the “high dependency, low tax” category, with a tax rate that’s ranked 25th in the country. Other analysis compared gross domestic product per capita compared to dependency on the federal government, and WalletHub placed Louisiana in the “high dependency, low GDP” category with a GDP per capita ranking of 40th. Originally published at The Center Square.  On a stifling July day, Elon Musk sat across from the governor of Oklahoma under a small white pop-up tent, a red Tesla flag waving from a short pole in an otherwise unadorned field.

That the billionaire was even in Oklahoma, seriously considering putting a gigantic new Tesla factory outside of Tulsa, was a major turning point for the frequently overlooked state. Suddenly, Oklahoma could boast of being on par with its much larger neighbor and rival, Texas. The only other city still in the running for the plant, by that point in 2020, was Austin. The wide shadow of Texas has long fallen over Oklahoma. Despite offering the same red-state promise of open land, a cowboy ethos and limited government regulations, Oklahoma has found itself a perennial also-ran, especially in recent decades as Texas cities became magnets for new companies and workers from around the country. In the end, Mr. Musk chose Austin. But the long-shot bid put Oklahoma on the map for relocating companies and workers, and inspired a new resolve to make the state a more appealing place to work and live. Since 2018, Tulsa has been offering remote workers $10,000 to move to the city for at least a year. In its first year, 70 people took the city up on the offer. In 2021, 950 people made the move. Many stayed. “I can’t believe I live in Oklahoma — it’s like even weird to say,” said Chris Bland, who took the $10,000 and moved in 2021 from an apartment in Harlem, working remotely as an environmental scientist at New York’s Mount Sinai Health System. Since then, Mr. Bland, 29, has been selling his friends and family on Tulsa — restaurants, bars, $895 a month for a studio apartment downtown — and he has already stayed longer than the single year required by the program, which is funded by the Tulsa-based George Kaiser Family Foundation. Oklahoma City has taken a different tack, raising money from residents and visitors — in the form of a dedicated 1 percent sales tax — and spending hundreds of millions of dollars in recent decades on things like new parks, a canal, a streetcar system and a basketball arena. The city remade its downtown, and new shops and restaurants replaced those that had long ago vanished. Many American cities have been spending to improve their downtown amenities, and other states also offer tax breaks and other incentives to try to lure businesses. But Oklahoma City is now one of the country’s fastest-growing large cities, climbing past Boston and Washington to become the 20th largest by population, with 687,000 people. Still, the state’s growth has been dwarfed by the roaring boom in Texas, which has welcomed a rush of transplants from other states and new immigrants from around the world. The Texas economy is second in the United States only to California, and it has been growing faster. But Oklahoma officials now see a chance to draft off that boom, selling their state as a place that is just as business-friendly, at a more affordable entry point. “We hope it’s the next Texas,” said Lt. Gov. Matt Pinnell of Oklahoma, sitting in a Houston seafood restaurant for a series of recent meetings to entice more international energy investment in his state. More than 100 companies have come to Oklahoma in the last five years, including 29 last year, and another 200 have announced expansions, according to the state Commerce Department, resulting in more than $10 billion in promised new investments. Six companies moved their headquarters to the state. The rivalry with Texas nonetheless remains a bit one-sided. Oklahoma has three Fortune 500 companies headquartered in the state, all in the oil and gas industry; Texas has more than 50. Asked about the threat posed by their neighbor, Texas officials did not see one. “Texas is dominating for the 18th year in a row as the Best State for Business,” Andrew Mahaleris, the press secretary to Gov. Greg Abbott, said in a statement, citing a ranking in Chief Executive magazine. “Texas will continue to remain number one because of the unmatched competitive advantages we offer: no corporate or personal income taxes, a predictable regulatory climate, and a young, growing and skilled work force.” But soaring housing prices in Austin and other Texas cities are undermining some of the state’s competitive advantage. “There are a lot of states around here that are a lot cheaper to live,” said Vance Ginn, an economist in the Trump administration and a former chief economist at the Texas Public Policy Foundation, a conservative think tank. “That is a concern.” Don Ward, a Texas native and entrepreneur, is moving his small technology business, Laundris, to Tulsa from Austin. Mr. Ward, 53, said he worried about the rapid rise of housing and other costs, and Tulsa offered some of the small-city feel that he said had been vanishing from Austin, whose population is now just under 1 million. “Austin has been more focused on working with the Elon Musks of the world,” Mr. Ward said. “Tulsa gave me an opportunity to be a big fish in a smaller pond again.” Reliable electricity is another issue Oklahoma is using as a selling point. The failure of the Texas electrical grid during a brutal winter storm in February 2021 fueled new interest in states, like Oklahoma, with energy infrastructure seen as more reliable. Gov. Kevin Stitt, a Republican, boasted in a recent interview about not only the state’s “affordable, reliable energy grid” but his effort to do away with 25 percent of the state’s regulations on businesses. Seated in his office in the Capitol, Mr. Stitt conceded that Texas has long had a reputation as a good place for business. “But it’s getting overcrowded,” he said, noting that commute times around Oklahoma City are far shorter than those in Dallas-Fort Worth. It has long been easy to drive around Oklahoma City. The problem was a lack of things to drive to. The need became apparent decades ago, when the city lost out to Indianapolis for a United Airlines maintenance center. Company executives had visited Oklahoma City and found they simply could not make their employees live there. “It was terrible,” said David Holt, 43, who grew up in Oklahoma City in the 1990s and is now in his second term as mayor. “All my peers who had any wherewithal went to Dallas or Houston or the more adventurous off to California or New York.” The city began a long process to make itself more attractive, one that continues. On a recent weekday, a billboard across from the Oklahoma City Thunder arena proclaimed “Always Onward” over a newly opened park of spindly young trees. (The state, for its part, has been trying a different tagline: “Imagine That.”) The city has also been transforming politically. Once reliably red, Oklahoma City is now solidly purple, having narrowly favored former President Donald J. Trump in 2020 but voting by a wide margin for the losing Democratic candidate for governor last year. Governor Stitt, a businessman and political newcomer when first elected in 2018, said that he did not worry that efforts to attract newcomers to the state’s urban centers would alter its political identity. “We’re finding people moving here from the quote unquote liberal states because of their policies,” he said, adding that he and other state leaders were clear about their conservative principles. “It’s not for everybody. If this is not who you are, great, you don’t have to live in our state.” Tulsa has similarly been shifting politically, and in its attitude about itself, said Mayor G.T. Bynum, also a Republican in a nonpartisan office. He said the amount of investment in the city was akin to the 1920s oil boom and, because of Tesla’s interest, the city was hearing from other electric vehicle and battery companies. “Elon Musk netted us tens of thousands of dollars in free advertising,” Mr. Bynum said. Even so, by the time he visited, Mr. Musk may have already made his decision against Oklahoma, for many of the same old reasons. “The fundamental problem I have is getting people to move out of California,” Mr. Musk told the head of work force development in Oklahoma in 2020, according to documents obtained by The Associated Press. “Austin is one of the few places to which they will move.” The population of Austin has grown more than 20 percent in the last decade. But Oklahoma City has also grown by nearly that much during that time period, roughly 18 percent, a fact Mayor Holt attributes in part to his city’s ability to appeal to those seeking what Austin used to be. “We have a lot of the things that you would expect to find in a large American city, but without the hassle,” he said. “I think that’s a combination that maybe only has a finite window. It’s the combination Austin offered 20 years ago, and then everybody took them up on it, and now it’s too crowded.” Originally published at The New York Times.  President Biden recently visited the humanitarian crisis along the U.S.-Mexico border but mostly used it as a political stunt to offer more failed policies and chastise Republicans. Republicans have also had years to solve immigration issues, but the situation continues. Meanwhile, Biden and former President Trump have similar protectionist trade policies, which have come at a cost to Americans.

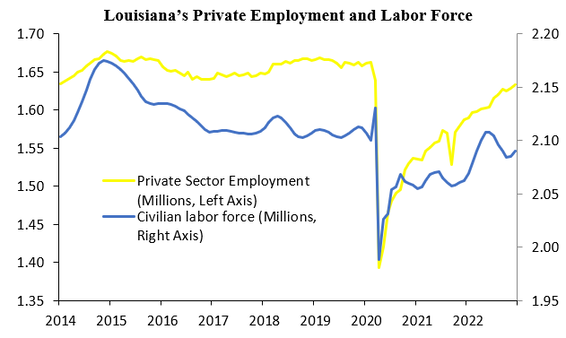

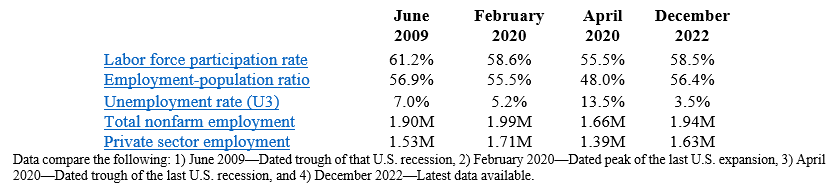

Given the gains from immigration and trade in a globally connected economy, many on the left and the right overlook how government failures of a broken visa system and costly big-government are the source of these problems. And this oversight leads to many of their big-government solutions that aren’t rooted in sound economics but rather winning votes. Immigration and trade overlap in many ways as they are exchanges with people across international borders. Given the rule of law and private property rights are essential in our republic, there are roles for government to enforce the rules of the game but otherwise politicians should address bad policies in the U.S. before trying to blame tangential problems on other countries or “market failures.” For instance, have you ever heard that “immigrants and trade steal jobs”? It’s a myth. The notion that immigrants “steal jobs” supposes that adding more people and different kinds of knowledge and innovation to the economic pie somehow prohibits the native-born population from prospering. Simply put, the aversion to immigrants joining the American workforce is rooted in fear of competition. Moreover, much of the skepticism fueling fear of more working immigrants tends to also be directed at international trade. But the gains to be acquired from immigration and trade outweigh the suspected costs. We would be wise to let markets work within the rule of law instead of imposing arbitrary restrictions and growing government. Working immigrants do not steal jobs. But, as economist Ben Powell recently noted in my conversation with him, they do change the mix of jobs as they expand the capacity of the economy with more workers. Similarly, when young people graduate college and enter the labor market each year, they don’t “steal jobs” but often accept the lower-skilled positions while increasing productivity. These groups support increased competition, fuel the creation of new jobs, and permit the native-born population to work in positions in which they’re more productive. They also increase demand for goods and services provided by lower-skilled workers. So, immigrants and new graduates alike can increase net jobs. When I hire a contractor to install my ceiling fan, I don’t view it as them stealing my job because someone else is better at it. Even though I pay for the service, it’s a trade that ultimately benefits me or I wouldn’t do it, as not learning how to install the fan gives me more time to do things which I enjoy. The contractor and I mutually benefit, just like with all exchanges with people whether in the same community, same state, same country, or another country. Barriers to immigration and trade, such as visa limitations, border walls, tariffs, and quotas, are barriers to human cooperation enforced by politicians with limited knowledge. A more productive path forward would be pursuing immigration reform that improves the visa system, making it easier for immigrants to come legally. Border walls, such as the one in Texas, are a scapegoat and far cry from addressing the real issues needing reform. Similar to the fear of immigration, proponents of trade protectionism often fail to understand that the exchange is as economically simple as it is non-threatening. Whether a Texan is trading with a New Yorker or someone from China, it’s individuals, not places or entities, trading for mutual benefit. A greater exchange of goods and services through trade promotes competition as the expanded pool of resources for consumers encourages producers to innovate to stay competitive or risk closing. International trade doesn’t steal U.S. profits any more than immigrants steal jobs. But, like immigration, it allows people to focus on producing the goods they have a comparative advantage instead of being pressured to supply everything for themselves. The goal should be to reduce costs of doing business so there are abundant opportunities for American workers and businesses to flourish by cutting government spending, taxes, and regulations. Restricting trade and immigration ultimately restricts the prosperity supported by free-market capitalism by keeping out an influx of knowledge, skills, and goods and services that made the American melting pot so great for so long. Anti-trade and anti-immigration are anti-growth. Free markets are really free people. We ought to find free-market solutions to advance freedom and opportunity rather than impose costly barriers that hinder them. As economist Peter Boettke recently in my conversation with him: when ordinary people are given elbow room to grow, economies thrive and people can prosper. Originally published at Econlib. Key Point: Louisiana’s labor market looks okay even as the unemployment rate increased by 0.2-percentage point to 3.5% unemployment rate. But the labor force has 10,622 (-0.5%) fewer people in it than pre-shutdown in February 2020 and private sector employment is 30,000 (-1.8%) below then, indicating a much weaker labor market and economy overall.  Labor Market: A job is the best path to prosperity as work brings dignity, hope, and purpose to people through life-long benefits of earning a living, gaining skills, and building social capital. The table below shows Louisiana’s labor market over time until the latest data for December 2022 by the U.S. Bureau of Labor Statistics.  The establishment survey shows that net total nonfarm jobs in the state increased by 4,800 jobs last month (+0.2%), bringing this to 50,700 jobs below the pre-shutdown level in February 2020. Private sector employment was up by 4,400 jobs (+0.3%) and government employment rose by 400 jobs (+0.1%) last month. Compared with a year ago, total employment was up by 46,200 jobs (+2.4%) with the private sector adding 45,600 jobs (+2.9%) and the government adding 600 jobs (+0.2%). The household survey finds that the civilian labor force rose by 5,028 people last month and is down 10,622 people since February 2020, which results in the labor force participation rate of 58.5% being 0.1-percentage point lower than it was in February 2020 but well below the 61.2% rate in June 2009 at the trough of the Great Recession. The employment-population ratio is 0.9-percentage point above where it was in February 2020 and nearly back to where it was in June 2009. While the unemployment rate of 3.5% is substantially lower than the 5.2% rate in February 2020, a broader look at Louisiana’s labor market rather than this weak indicator shows that Louisianans still face challenges, especially compared with neighboring states based on several measures.  Economic Growth: The U.S. Bureau of Economic Analysis (BEA) recently provided the real (inflation-adjusted) gross domestic product (GDP) in Q3:2022 for Louisiana and other states.  The following table shows how U.S. and Louisiana economies performed since 2020. The steep declines were during the shutdowns in 2020 in response to the COVID-19 pandemic, which was when the labor market suffered most. The decline in real GDP annualized growth of -3% in Q2:2022 was the 5th worst and increase of +2.5% in Q3:2022 ranked 23rd in the country.  The BEA also reported that personal income in Louisiana grew at an annualized pace of +5.8% (ranked 19th) in Q2:2022 (tied +5.8% U.S. average) and of +2.5% (ranked 47th) in Q3:2022 (below +5.3% U.S. average). Bottom Line: Louisianans gained jobs in December but continue to feel the costs of the shutdowns in 2020 and other restrictive policies that reduce opportunities for them to find well-paid jobs. Institutions matter to human flourishing in countries and states, which is floundering in Louisiana compared with many other states. The Fraser Institute recently ranked Louisiana 20th for economic freedom based on 2020 data for government spending, taxes, and labor market regulation. And the Tax Foundation recently ranked the Pelican State as having the 12th worst business tax climate and 15th highest corporate income tax rate. While the state has improved its tax code recently and lower taxes may happen soon from an expected budget surplus, this lack of economic freedom and poor business tax climate are contributing to a net outmigration of Louisianans to other states, which is a drain on the state’s economic potential now and in the future. State and local policymakers should work to reverse this trend by passing pro-growth policies.  Free-Market Solutions: In 2023, the Louisiana Legislature should provide the state’s comeback story by:

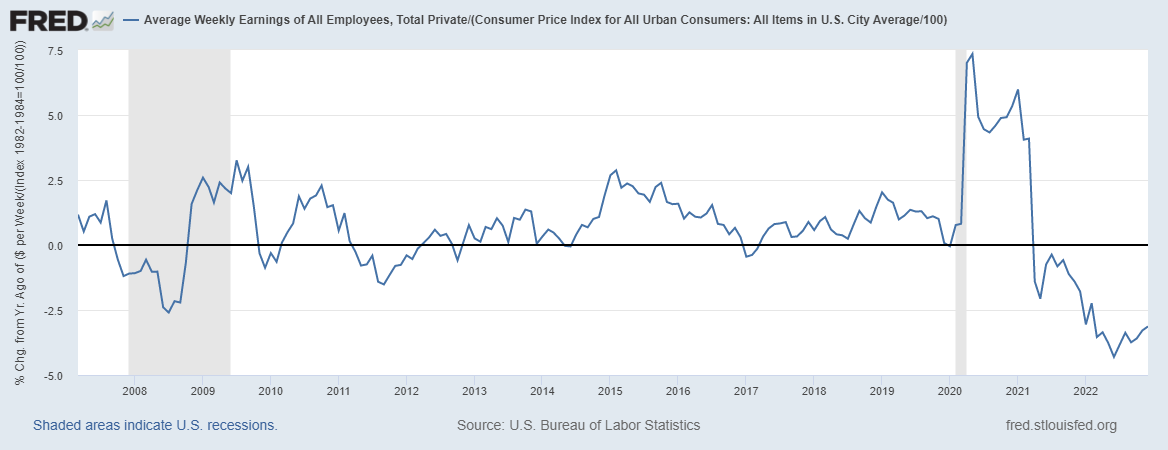

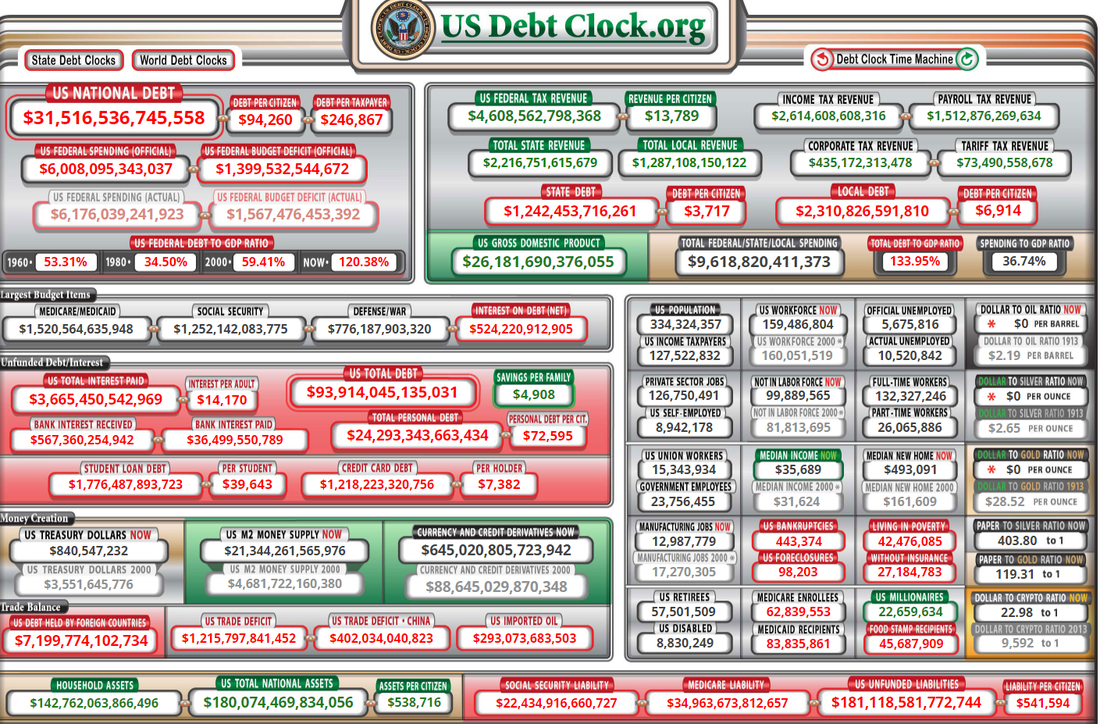

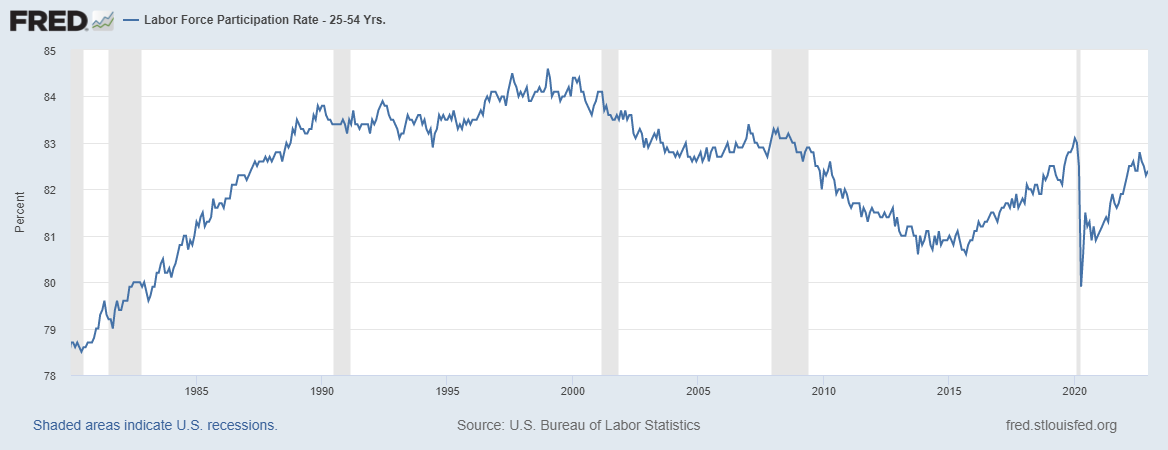

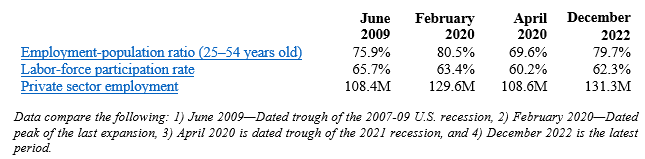

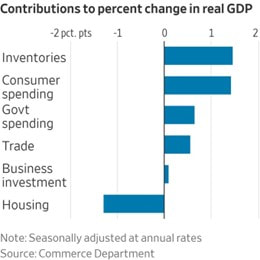

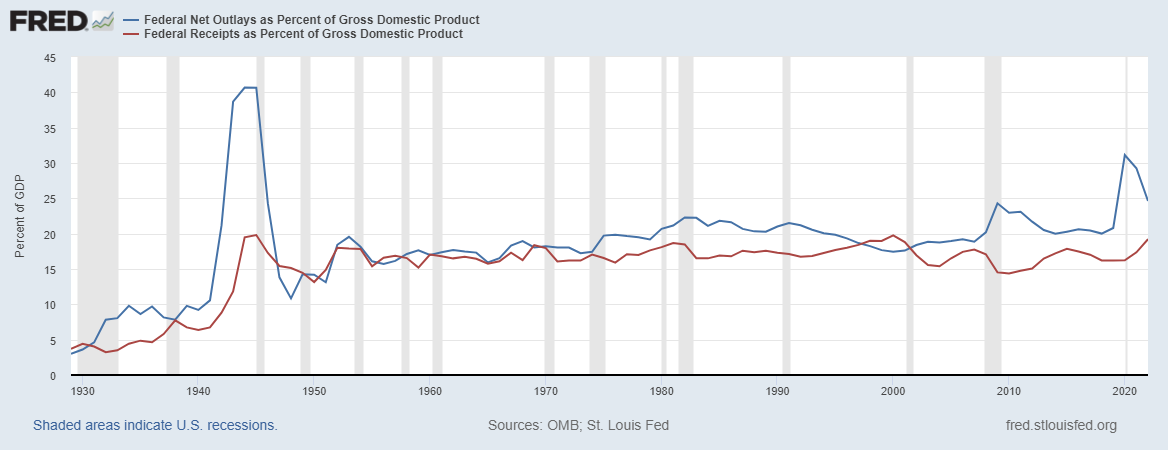

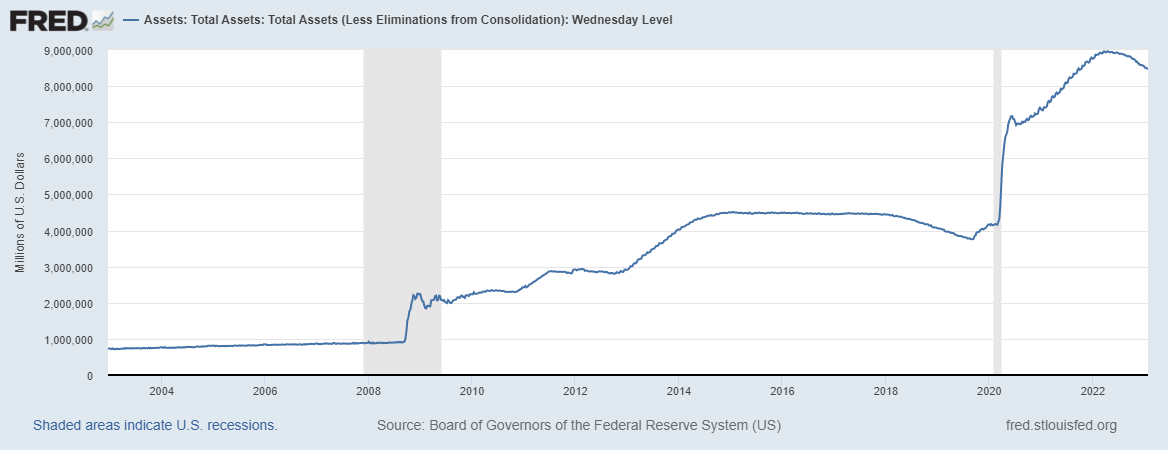

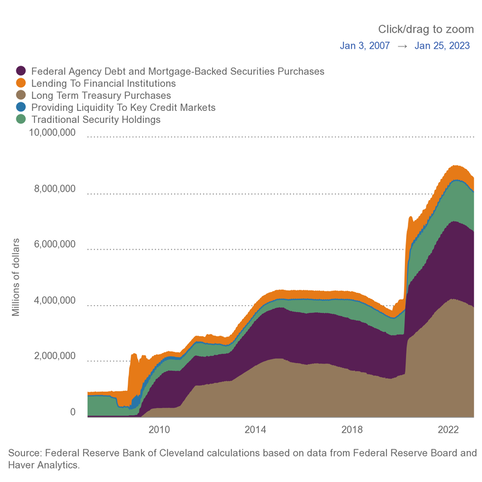

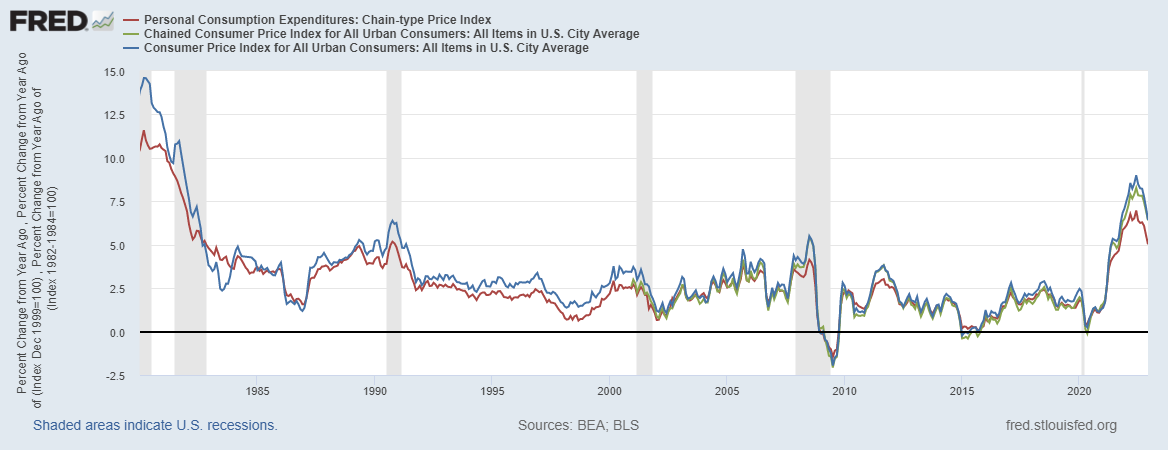

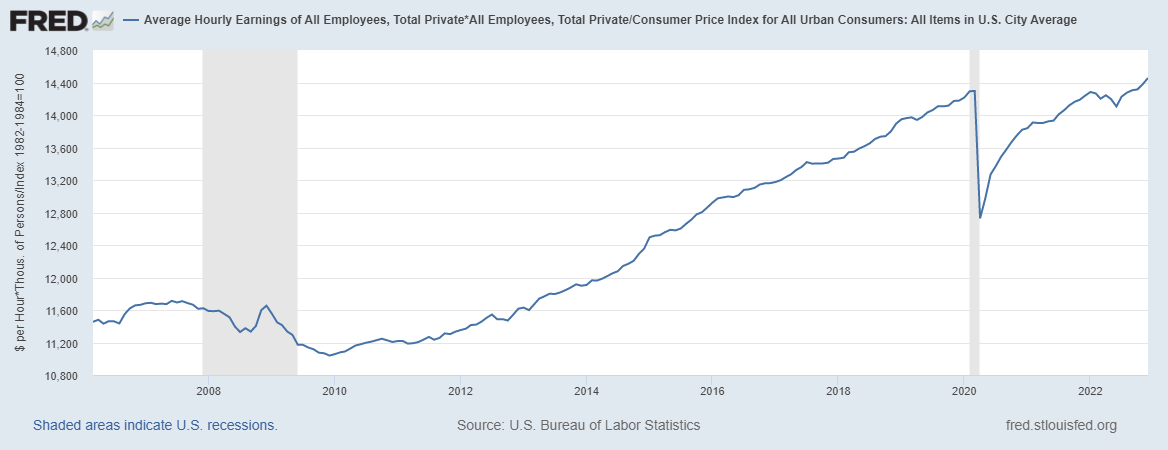

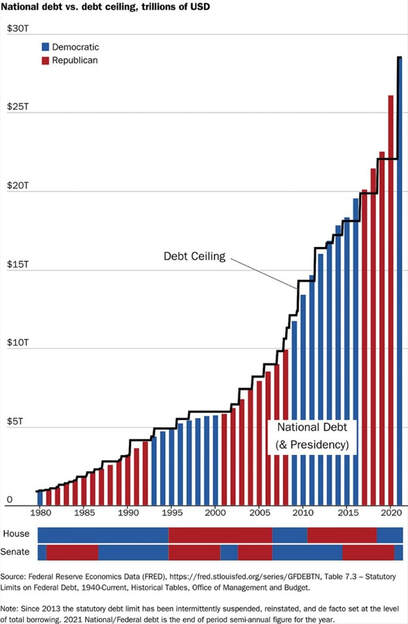

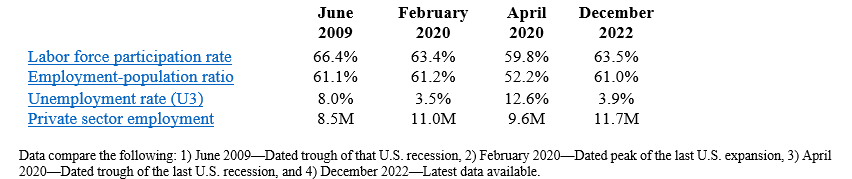

Key Point: Americans are suffering under big-government policies as average weekly earnings adjusted for inflation are down for 21 straight months. It's time for pro-growth policies to unleash economic potential to let people prosper.  Overview: The irresponsible “shutdown recession” and subsequent government failures have led to a longer, deeper recession with high inflation that are having persistent consequences for many Americans’ livelihoods. This includes excessive federal spending redistributing scarce private sector resources with deficit spending of more than $7 trillion since January 2020 to reach the new high of $31.4 trillion in national debt—about $95,000 owed per American or $250,000 owed per taxpayer. This new debt has hit its limit and needs to be addressed with spending restraint as the Federal Reserve monetized most of the new debt, leading to a 40-year-high inflation rates. The failed policies of the Biden administration, Congress, and the Fed must be replaced with a liberty-preserving, free-market, pro-growth approach by the new majority by House Republicans so there are more opportunities to let people prosper.  Labor Market: The U.S. Bureau of Labor Statistics recently released the U.S. jobs report for December 2022. The BLS’s establishment report shows there were 223,000 net nonfarm jobs added last month, with 220,000 added in the private sector. Interestingly, while there have appeared to be a relatively robust number of jobs created, a recent report by the Philadelphia Fed find that if you add up the jobs added in states in Q2:2022 there were just 10,500 net new jobs rather than more than 1 million initially estimated. This further indicates that the recession started in (likely) March 2022 (more on this below). That expected revision to the establishment report supports the weak data in the BLS’s household survey, which employment increased by 717,000 jobs last month but had declined in four of the last nine months for a total increase of 916,000 jobs since March 2022. This number of net jobs added since then is much lower than the report 2.9 million payroll jobs in the establishment. The official U3 unemployment rate declined slightly to 3.5%, but challenges remain, including: 3.1% decline in average weekly earnings (inflation-adjusted) over the last year, 0.4-percentage point lower prime-age (25–54 years old) employment-population ratio than in February 2020, 0.6-percentage point below prime-age labor force participation rate, and 1.0-percentage-point lower total labor-force participation rate with millions of people out of the labor force.   These data support my warnings for months of stagflation, recession, and a “zombie economy.” This includes “zombie labor” as many workers are sitting on the sidelines and others are “quiet quitting” while there’s a declining number of unfilled jobs than unemployed people to 4.5 million And that demand for labor is likely inflated from many “zombie firms,” which run on debt and could make up at least 20% of the stock market and will likely lay off workers with rising debt costs. Economic Growth: The U.S. Bureau of Economic Analysis’ released economic output data for Q4:2022. The following provides data for real total gross domestic product (GDP), measured in chained 2012 dollars, and real private GDP, which excludes government consumption expenditures and gross investment.  The shutdown recession in 2020 had GDP contract at historic annualized rates because of individual responses and government-imposed shutdowns related to the COVID-19 pandemic. Economic activity has had booms and busts thereafter because of inappropriately imposed government COVID-related restrictions in response to the pandemic and poor fiscal policies that severely hurt people’s ability to exchange and work. Since 2021, the growth in nominal total GDP, measured in current dollars, was dominated by inflation, which distorts economic activity. The GDP implicit price deflator was +6.1% for Q4-over-Q4 2021, representing half of the +12.2% increase in nominal total GDP. This inflation measure was +9.1% in Q2:2022—the highest since Q1:1981—for a +8.5% increase in nominal total GDP that quarter. This made two consecutive declines in real total (and private) GDP, providing a criterion to date recessions every time since at least 1950. In Q3:2022, nominal total GDP was +7.6% and GDP inflation was +4.4% for the +3.2% increase in real total GDP. But if inflation had been as high as it was in the prior two quarters or had the contribution of net exports of goods and services (driven by natural gas exports to Europe) not been 2.9%, real total GDP would have either declined or been essentially flat for a third straight quarter. In Q4:2022, there was a similar story of weaknesses as nominal total GDP was +6.4% and GDP inflation was +3.5% for the +2.9% increase in real total GDP. But if you consider the +2.9% real total GDP growth was driven by contributions of volatile inventories (+1.5pp), government spending (+0.6pp), and next exports (+0.6pp) which total +2.7pp, the actual growth is quite tepid. For all of 2022, real total GDP growth is reported +2.1% year-over-year but measured by Q4-over-Q4 the growth rate was only +0.96%, which was the slowest Q4-over-Q4 growth for a year since 2009 (last part of Great Recession).  The Atlanta Fed’s early GDPNow projection on January 27, 2023 for real total GDP growth in Q1:2023 was +0.7% based on the latest data available. The table above also shows the last expansion from June 2009 to February 2020. The earlier part of the expansion had slower real total GDP growth but had faster real private GDP growth. A reason for this difference is higher deficit-spending in the latter period, contributing to crowding-out of the productive private sector. Congress’ excessive spending thereafter led to a massive increase in the national debt that would have led to higher market interest rates. This is yet another example of how there is always an excessive government spending problem as noted in the following figure with federal spending and tax receipts as a share of GDP.  But the Fed monetized much of it to keep rates artificially lower thereby creating higher inflation as there has been too much money chasing too few goods and services as production has been overregulated and overtaxed and workers have been given too many handouts. The Fed’s balance sheet exploded from about $4 trillion, when it was already bloated after the Great Recession, to nearly $9 trillion and is down only about 6% since the record high in April 2022. The Fed will need to cut its balance sheet (see first figure below with total assets over time) more aggressively if it is to stop manipulating so many markets (see second figure with types of assets on its balance sheet) and persistently tame inflation.   The resulting inflation measured by the consumer price index (CPI) has cooled some from the peak of 9.1% in June 2022 but remains hot at 6.5% in December 2022 over the last year, which remains at a 40-year high (highest since June 1982) along with other key measures of inflation (see figure below). After adjusting total earnings in the private sector for CPI inflation, real total earnings are up by only 1.1% since February 2020 as the shutdown recession took a huge hit on total earnings and then higher inflation hindered increased purchasing power.   Just as inflation is always and everywhere a monetary phenomenon, high deficits and taxes are always and everywhere a spending problem. The figure below (h/t David Boaz at Cato Institute) shows how this problem is from both Republicans and Democrats.  As the federal debt far exceeds U.S. GDP, and President Biden proposed an irresponsible FY23 budget and Congress never passed one until the ridiculous $1.7 trillion omnibus in December, America needs a fiscal rule like the Responsible American Budget (RAB) with a maximum spending limit based on population growth plus inflation. If Congress had followed this approach from 2002 to 2021, the (updated) $17.7 trillion national debt increase would instead have been a $1.1 trillion decrease (i.e., surplus) for a $18.8 trillion swing to the positive that would have reduced the cost to Americans. The Republican Study Committee recently noted the strength of this type of fiscal rule in its FY 2023 “Blueprint to Save America.” And the Federal Reserve should follow a monetary rule.

Bottom Line: Americans are struggling from bad policies out of D.C., which have resulted in a recession with high inflation. Instead of passing massive spending bills, like passage of the “Inflation Reduction Act” that will result in higher taxes, more inflation, and deeper recession, the path forward should include pro-growth policies. These policies ought to be similar to those that supported historic prosperity from 2017 to 2019 that get government out of the way rather than the progressive policies of more spending, regulating, and taxing. The time is now for limited government with sound fiscal and monetary policy that provides more opportunities for people to work and have more paths out of poverty. Recommendations: