|

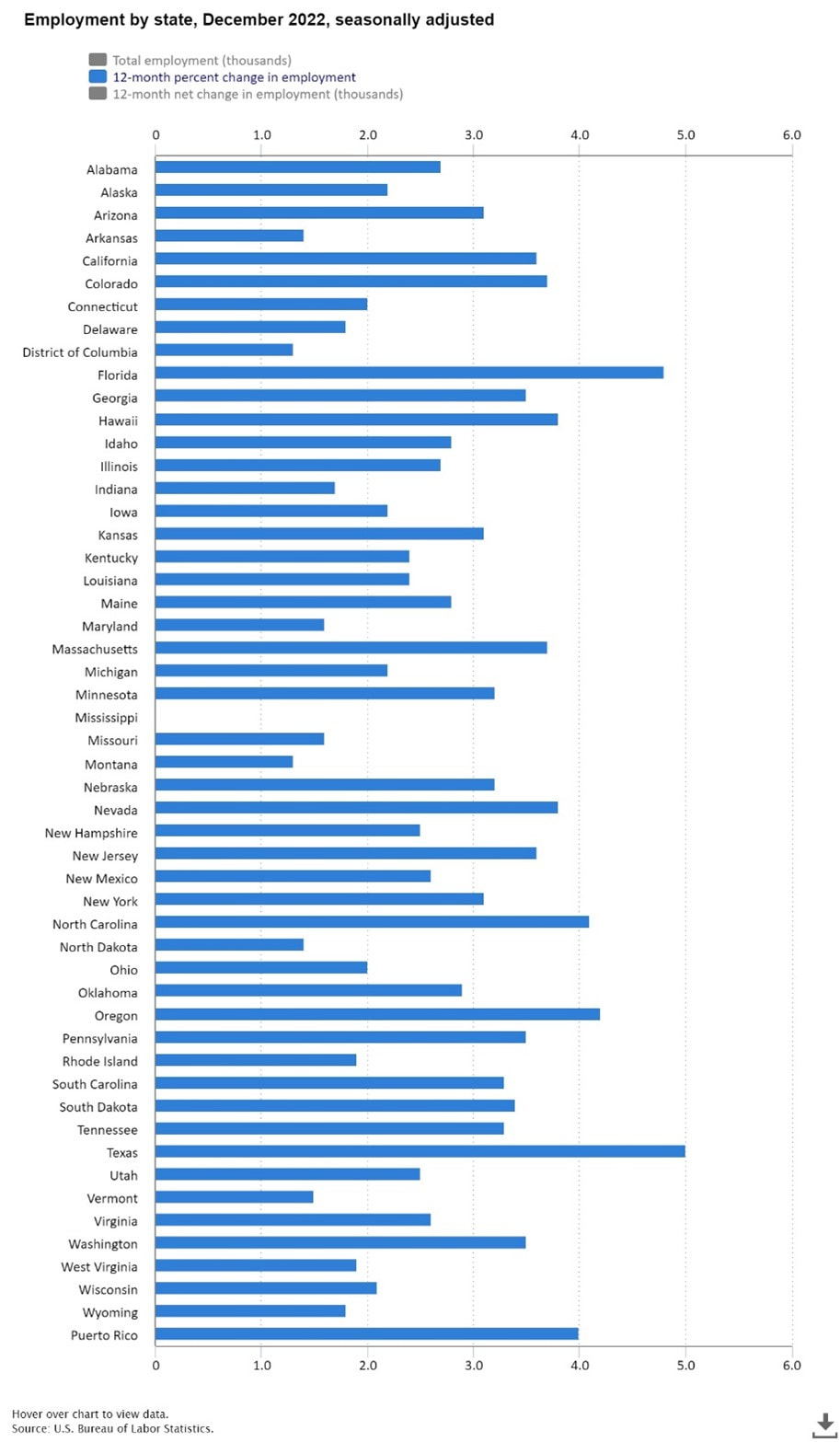

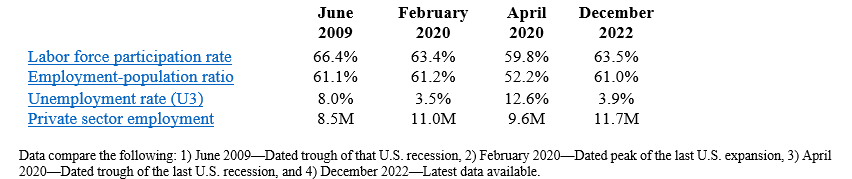

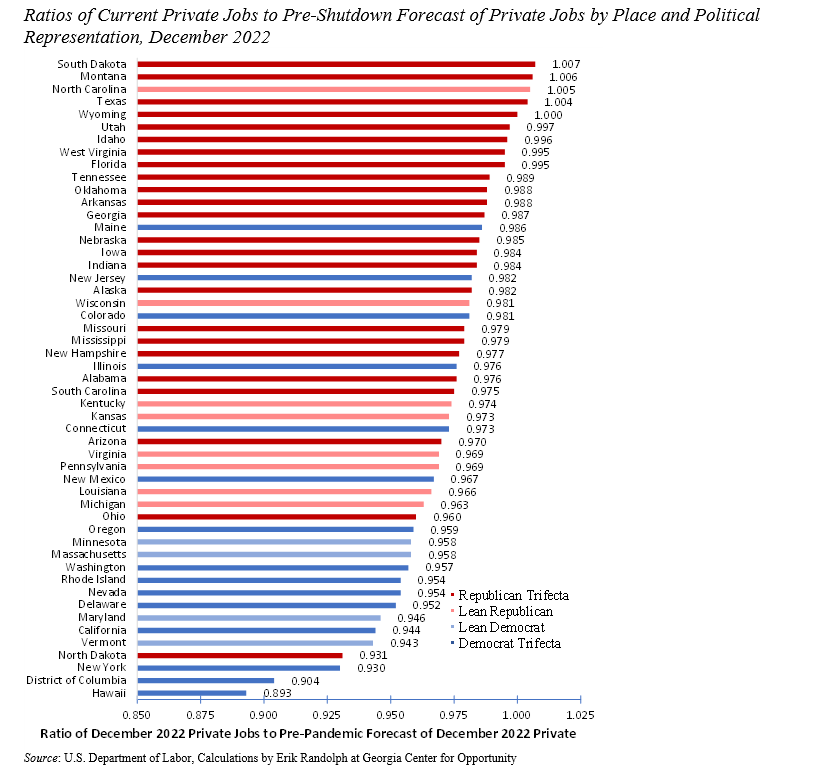

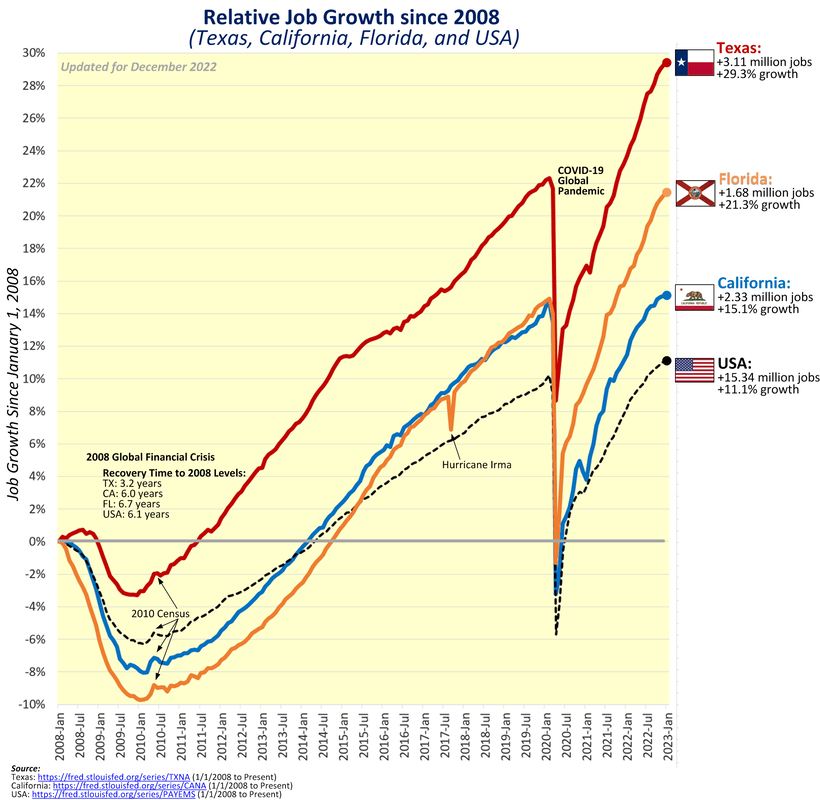

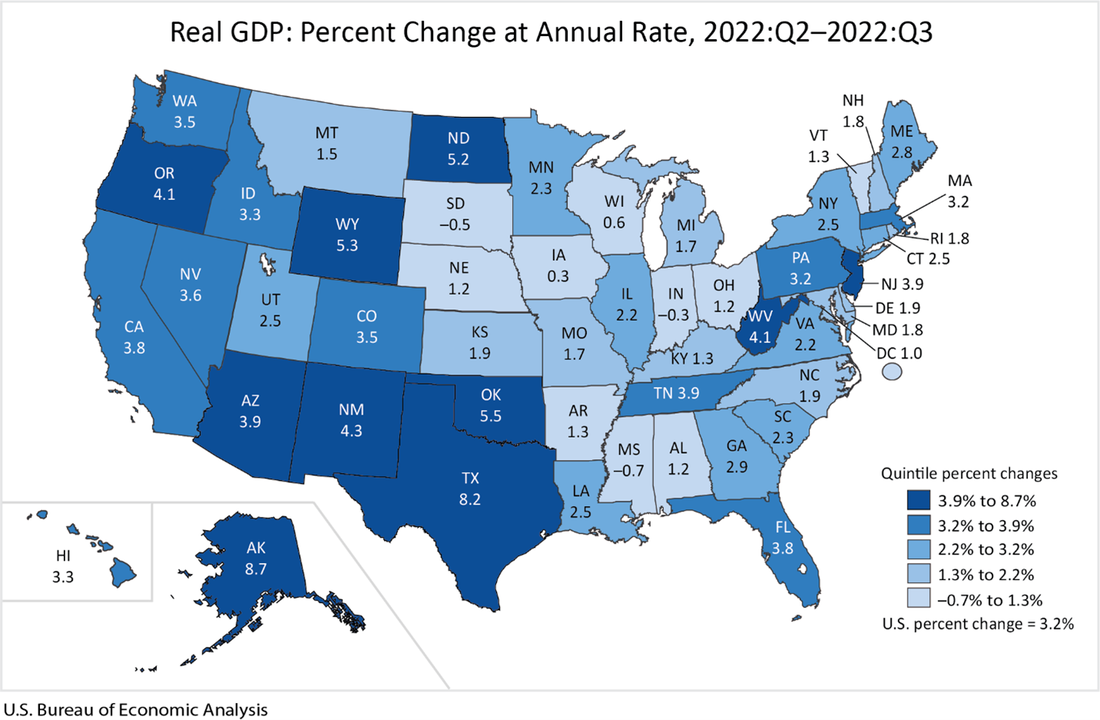

Key Point: Texas continues to lead the way in job creation over the last year (see first figure) and second in economic growth in the third quarter of 2023 (see last figure), but there’s more to do to help struggling Texans deal with the state’s affordability crisis, especially spending, regulating, and taxing less.  Overview: Texas has been a national leader in the economic recovery since the inappropriate shutdown recession in Spring 2020. This includes reaching a new record high in total nonfarm employment for the 14th straight month, leading exports of technology products for 20 consecutive years, and being home to more than 50 of the world’s Fortune 500 companies. While the 87th Texas Legislature in 2021 supported the recovery by passing many pro-growth policies like the nation’s strongest state spending limit, there’s more to do in the ongoing 2023 session to remove barriers placed by state and local governments. Labor Market: The best path to prosperity is a job, as it helps bring financial self-sufficiency, dignity, hope, and purpose to people so they can earn a living, gain skills, and build social capital. The table below shows the state’s labor market for December 2022. The establishment survey shows that net nonfarm jobs in Texas increased by 29,500 last month, resulting in increases for 31 of the last 32 months, to bring record-high employment to 13.7 million. Compared with a year ago, total employment was up by 650,100 (+5.0%)—fastest growth rate in the country—with the private sector adding 628,800 jobs (+5.7) and the government adding 21,300 jobs (+1.1%).  The household survey shows that the labor force participation rate is slightly higher than in February 2020 but well below June 2009 at the trough of the Great Recession. The employment-population ratio fell was unchanged in November and nearly where it was in February 2020, and the private sector now employs 700,000 more people than then. Texans still face challenges with a worse unemployment rate, though historically low, and nonfarm private jobs just recently above its pre-shutdown trend (Figure 1). The figure below compares the ratio of current private employment to pre-shutdown forecast levels in red states and blue states if both chambers of the legislature and the governor are Republican (dark red), Democrat (dark blue), or some combination (lighter colors).  The results show a clear distinction between red states and blue states, with the stringency of restrictions by governments during the pandemic along with pro-growth policies before and after the shutdowns playing key roles. Specifically, 21 of the 25 states with the best (highest) ratios are in red-ish states while 13 of the 15 states and D.C. with the worst (lowest) ratios are in blue-ish places as of December 2022. The following figure from Soquel Creek on Twitter tells the story even more directly: those states with more economic freedom prosper more than those with less economic freedom (see rankings in Fraser Institute's Economic Freedom of North America report: FL ranks #1, Texas ranks #4, California ranks #49, and New York ranks #50).  Overall, multiple indicators should be considered in this nuanced labor market, such as the fact that the unemployment rate is a weak indicator as many have dropped out of the labor force. While the labor force participation rate in Texas slightly exceeds where it was before the shutdowns, and the 3.9% unemployment rate could be considered full employment, the employment-population ratio is 0.2-percentage point below the pre-shutdown ratio. Economic Growth: The U.S. Bureau of Economic Analysis (BEA) recently provided the real gross domestic product (GDP) by state for Q3:2022. The Figure below Texas had the second fastest GDP growth (first is Alaska) of +8.2% on an annualized basis to $1.89 trillion (above the U.S. average of +3.2% to $20.05 trillion). In the prior quarter, Texas had the fastest growth with +1.8% growth as the U.S. average declined by -0.6% that quarter. Of course, these followed Texas’ GDP contractions of -7.0% in Q1:2020 and -28.5% in Q2 during the depths of the shutdown recession. Fortunately, GDP rebounded in Q3 and Q4, yet declined overall in 2020 by -2.9% (less than -3.4% decline of U.S. average) but increased by +3.9% in 2021 (below the +5.9% U.S. average). The BEA also reported that personal income in Texas grew at an annualized pace of +6.9% in Q3:2022 (ranked 6th highest and faster than the U.S. average of +5.3%) but slower than the robust +8.4% in Q2:2022 (ranked 6th best and above the U.S. average of +4.9%) as job creation and inflated income measures found their way across the economy.  Bottom Line: As Texas recovers from the shutdown recession and faces an uncertain future with the U.S. economy having stagflation and a likely recession, Texans need substantial relief to help make ends meet. Other states are cutting, flattening, and phasing out taxes, so Texas must make bold reforms to support more opportunities to let people prosper, mitigate the affordability crisis, and withstand destructive policies out of D.C.

Free-Market Solutions: In 2023, the Texas Legislature should improve the Texas Model by:

0 Comments

Leave a Reply. |

Vance Ginn, Ph.D.

|

RSS Feed

RSS Feed

Proudly powered by Weebly