|

Check out episode 71 of This Week's Economy. Today, I discuss key items that touch on everything from inflation, Space X, Austin, carbon taxes, KOSA, taxes on tips, and more.

Listen, like, share, and subscribe. Show notes here: https://vanceginn.substack.com.

0 Comments

Originally published at The Hill.

Former President Donald Trump’s proposal to exempt tips from federal income and payroll taxes might sound like a windfall for service workers, but it’s a costly illusion that undermines fair tax policy and economic efficiency. This plan, proposed as legislation by Sen. Ted Cruz (R-Texas), designed to appeal to a crucial voter base, exacerbates inequities and distorts the tax system. There’s a better way. The core problem with exempting tips from taxes is that it narrows the tax base, leading to potential hikes in overall tax rates on tipped workers and everyone else to compensate for deficit spending. A broad tax base with low rates is essential for minimizing economic distortions and spreading the tax burden fairly. Narrowing the base by exempting tips would shift the burden to non-exempt income earners, creating an uneven playing field and violating sound tax policy. This proposal picks tipped workers as winners over everyone else, incentivizing more tipped jobs and payments. Today, nearly every payment app prompts users for tips, a practice that could proliferate further under such a tax exemption. This disrupts consumer behavior and distorts the labor market by artificially boosting the attractiveness of tipped positions over other roles, regardless of the actual economic value they generate. Moreover, this policy would discourage employers from raising the base wages of tipped employees. The federal minimum wage for tipped workers has stagnated at $2.13 per hour since 1991, and making tips tax-exempt might reduce the pressure to increase this base wage by employers, harming the workers it aims to help. Fiscal implications are significant. Estimates suggest exempting tips could reduce federal revenue by $150 to $250 billion over a decade. This shortfall requires higher taxes on other income forms or cuts to public services. Additionally, the potential for increased tax avoidance, as employers and employees reclassify wages as tips, would complicate tax administration and enforcement. A more effective approach would be to make the individual income tax cuts from the 2017 Tax Cuts and Jobs Act permanent, as they expire next year. Coupled with broadening the tax base and lowering rates, this would create a more efficient and equitable tax system. Reducing or eventually eliminating corporate income taxes could stimulate investment and economic growth, benefiting a broader range of Americans. Milton Friedman, the renowned free-market economist, advocated for a broad-based tax system with low rates and minimal exemptions. His philosophy centered on minimizing government intervention and ensuring tax policies do not distort economic decisions. Focusing on permanent tax cuts and broader reforms can create a more robust and fair economic environment that truly benefits all workers. Addressing excessive government spending, which has contributed significantly to our fiscal crisis, is also crucial and missing from Trump’s proposal. Neither Trump nor many Republicans seem to be advocating for significant spending cuts these days. Committing to reducing government expenditures would help manage the fiscal crisis and boost economic growth and prosperity by leaving more resources in the hands of individuals and businesses. While Trump’s proposal might seem appealing, it fails to address deeper issues within the tax system and the labor market for service workers. A broad-based tax system with low rates and minimal exemptions and less government spending is a more equitable and efficient approach that would support more prosperity than exempting tips from federal taxes. Economic Freedom Empowers Women’s Careers with Dr. Meg Tuszynski | Let People Prosper Show Ep. 1067/23/2024 Join me for Episode 106 of the Let People Prosper Show to learn about the importance of economic freedom and what it means for women and men with Dr. Meg Tuszynski, Managing Director of the Bridwell Institute for Economic Freedom in the Cox School of Business at Southern Methodist University and a Research Assistant Professor at the Cox School.

Subscribe, share, and rate the Let People Prosper Show, and visit vanceginn.com for more insights from me, my research, and ways to invite me on your show, give a speech, and more.  Originally published at Kansas Policy Institute. Recent Internal Revenue Service (IRS) data underscore a significant trend: people and income continue moving from high-tax to low-tax states. The pandemic lockdowns accelerated this movement, and even as life returns to a semblance of normalcy, the exodus continues unabated as policies matter. The IRS reports migration data between states reveal that in 2022, California topped the list of net losers in adjusted gross income (AGI), shedding $23.8 billion. Other high-tax, blue states, New York, Illinois, New Jersey, and Massachusetts, were the biggest losers, collectively losing billions in AGI. Conversely, low-tax, red states like Florida, Texas, South Carolina, Tennessee, and North Carolina emerged as the biggest net gainers, with Florida alone attracting $36 billion in AGI. According to the Wall Street Journal, the flight from blue, high-tax states far surpasses pre-pandemic levels. California’s income loss in 2022 was nearly three times that of 2019. New Jersey saw a record net income loss, largely due to fewer New Yorkers relocating across the Hudson River. Although lower than during the pandemic, New York’s AGI loss was still about 50% higher in 2022 compared to 2019. This migration pattern illustrates a clear preference for states with lower taxes, less regulation, and more business-friendly environments. The top income-gaining states share common pro-growth policies that promote economic growth, highlighting the significant impact of state policies on migration decisions as people move with their feet. Kansas: A State of Concern For Kansas, the story is one of consistent outmigration. The net loss from domestic migration in 2022 marked the 28th out of the last 30 years, with a staggering loss of over $600 million and more than $2 billion over the last five years. This represents the second-highest loss in three decades, second only to 2017 when the state imposed its highest tax increase. The average state outmigration loss in Kansas, about $76,000 per return, indicates a broad spectrum of incomes are leaving. Moreover, Kansas’ biggest gains came from higher-tax states, and its losses went to lower-tax states. Johnson County, often hailed as Kansas’s economic engine, accounted for over half of the state’s AGI loss at $357 million in 2022. This marks the fifth out of the last six years that Johnson County has experienced a net loss. Despite having about 20% of the state’s population, it has borne a disproportionate share of the AGI loss, which coincides with efforts to shift the county politically left and impose significant property tax hikes that reduce affordability. Considering data from the Kansas Policy Institute’s Green Book and the Tax Foundation, it becomes clear that Kansas is not alone in facing these challenges. However, the extent of the problem in Kansas is particularly alarming compared to other states. The IRS data indicate that while many states have rebounded or stabilized post-pandemic, Kansas continues to struggle with significant outmigration. Economic and Policy Implications for Kansas The significant outmigration from Kansas has several implications:

Kansas’s Path to Prosperity In response to these challenges, Kansas must adopt a comprehensive approach that includes responsible budgeting, tax relief, and the removal of barriers to work and education. Here are some key policy recommendations:

Addressing Migration Trends The migration trends underscore the importance of adopting free-market, pro-growth policies prioritizing economic freedom and personal responsibility. Kansas can learn from states that have successfully attracted residents and income by implementing policies that reduce the size of government, lower taxes, and eliminate burdensome regulations. The continued outmigration from Kansas highlights the urgent need for policy reforms that can reverse this trend. By learning from the successes of states that have managed to attract people and income, Kansas can chart a path toward a more prosperous future. Addressing the underlying issues driving residents away is crucial to ensuring the state’s long-term economic stability and growth.   Originally published at AIER.

The push for a carbon tax has regained popularity as the fiscal storm in 2025 and climate change debates intensify. Advocates claim it’s a solution to pay for spending excesses while reducing greenhouse gas (GHG) emissions. But a carbon tax is a misguided, costly policy that must be rejected. A carbon tax functions more like an income tax than a consumption tax, capturing all forms of work, including capital goods production and building construction. These sectors are heavy on carbon emissions, meaning the tax disproportionately burdens them, stifling investment and innovation — much like a progressive income tax, but with broader economic repercussions. For example, in the US, the construction sector alone accounts for about 40 percent of carbon emissions. A carbon tax would heavily penalize this industry, reducing its capacity to grow, generate new housing, and create jobs. Moreover, implementing a carbon tax involves massive administrative costs. The federal tax code is already complex and costly; a carbon tax would exacerbate these issues. Determining net carbon emissions is a nuanced process subject to ever-changing and arbitrary federal definitions, increasing compliance costs for businesses and consumers. A study by the Tax Foundation found that a carbon tax would cost billions of dollars annually in administrative costs, a burden that would ultimately fall on consumers through higher prices, less economic activity, and fewer jobs. The US economy is already suffering from regulatory costs of $3 trillion annually, including many energy-related restrictions, and the Biden administration has added more than $1.6 trillion in regulatory costs since taking office. One core principle of free-market capitalism is that it comes with limited government. A carbon tax contradicts this principle by expanding governmental regulation of everyday economic activities. The tax revenues would also enable further overspending, though that’s questionable given the supposed purpose of the tax is to reduce carbon emissions and, therefore, the taxes collected. Furthermore, a carbon tax could favor certain production methods over others, disrupting the level playing field that free markets thrive on and leading to inefficiencies and market distortions. The government picks winners and losers by favoring specific methods, undermining competition and economic growth. Renewable energy projects are likely to receive preferential political treatment, skewing investments away from the market’s more efficient, practical technologies. Pigouvian taxes, aimed at correcting negative externalities, are often cited to support a carbon tax. These taxes are named after economist Arthur Pigou and are designed to correct the negative effects of externalities by imposing costs equivalent to the external damage. But they can be counterproductive as they are bound to be the wrong tax rate, distorting economic activity. Carbon taxes fail to account for complex economic interactions and unintended consequences. The PROVE It Act, for instance, proposes a new carbon tax framework but lacks a clear, consistent, and scientifically sound basis for implementation. This uncertainty raises the stakes for economic disruption and consumer cost increases. Another critical issue in the carbon tax debate is ‘who decides?’ Climate science is ever evolving, and economic models predicting the outcomes of carbon taxes are fraught with uncertainties. Placing high costs on consumers based on unsettled science and unpredictable economic impacts is not a prudent policy approach. We should promote voluntary measures and technological advancements that naturally reduce emissions through market activity. Importantly, the EPA does not consider carbon dioxide a harmful pollutant in the traditional sense, as it is essential for life. We need carbon dioxide to breathe and enjoy a fulfilling life. This further questions the rationale behind taxing carbon emissions, as it imposes undue economic strain in an attempt to regulate a naturally occurring and necessary element. Even if America hadn’t been doing better than other countries that joined the Paris Treaty for goals on carbon emissions, China (and India) aren’t interested, thereby putting more of the unnecessary cost of reducing these emissions on Americans. Moreover, the cost of carbon taxes can be significant. Increasing production costs leads to higher prices for goods and services, disproportionately affecting low- and middle-income households — especially when they already suffer from high inflation. This regressive nature undermines its purported environmental benefits, placing a heavier burden on those least able to afford it. For example, a $50-per-ton carbon tax could increase household energy costs by up to $300 annually, hitting hardest those who can least afford it. Countries implementing carbon taxes, like some in Europe, have seen mixed results. Emissions reductions have been minimal, while economic growth has been hampered. These policies often result in job losses and decreased global competitiveness, showcasing the unintended consequences of such interventions. For instance, France’s carbon tax led to widespread protests and economic disruption, illustrating such policies’ social and economic challenges. While the intention behind a carbon tax — to reduce American GHG emissions in an effort to combat global climate change — is questionable in itself, the economic realities and principles of free-market economics prove it is a flawed approach. With the fiscal storm likely coming next year, Congress should just say no to the PROVE It Act and the carbon tax in general. The bottom line is that increasing the government’s footprint through such a tax is neither conservative nor market-oriented. Instead, we should focus on market-driven solutions that encourage innovation and efficiency without imposing heavy-handed regulations. Removing Government Barriers to Work with Dr. Liya Palagashvili | Let People Prosper Show Ep. 1057/16/2024 Join me for Episode 105 of the Let People Prosper Show to learn how to remove barriers to work and prosperity so people can have good jobs and fulfilling careers with Dr. Liya Palagashvili, a senior research fellow and director of the Labor Policy Project at the Mercatus Center at George Mason University.

Like, subscribe, and share the Let People Prosper Show, and visit vanceginn.com for more insights from me, my research, and ways to invite me on your show, give a speech, and more.  Originally published at Kansas Policy Institute.

Kansas has been simmering in economic stagnation for decades, trailing behind national averages in job growth, population increases, and economic growth. Like a poorly tended grill, high taxes and selective business subsidies have smoked out potential growth, leaving stagnation rather than sustenance. From 1979 to 2022, Kansas’s private job growth was just 53% compared to the national average of 88%. Imagine the vibrancy of having an additional 451,000 jobs in the state—jobs that could have been fostered with more competitive tax policies. Kansas has seen a net exodus of nearly 198,000 residents since 2000, driven away by an unwelcome tax environment. The states with the lowest tax burdens saw an influx of 4.6 million people from domestic migration during the same period, while the high-tax states watched 10.7 million residents pack up and leave. According to recent IRS data, Kansas lost $2.1 billion in adjusted gross income due to people moving elsewhere since 2017. The Kansas Policy Institute’s Green Book shows per capita spending of $4,941 in 2022 was substantially higher than in states with no personal income taxes ($3,283) and the ten best economic performance ($3,543). States with lower tax burdens have had better job growth and economic activity. Between 1998 and 2022, the ten states with the lowest state and local tax burdens averaged 51% growth in private-sector employment versus 34% for the ten states with the highest burdens. Kansas, ranked 44th during this period, achieved just 16% growth. Furthermore, Kansas’s high spending per person translates to higher taxes, ultimately burdening its citizens and hampering economic growth. More recently, Kansas’s unemployment rate ticked up to 2.9% in May 2024, a slight increase but a revealing one. The total nonfarm payroll employment saw a marginal uptick by 100 jobs. Beneath this weak report, there was more weakness as the private sector lost 300 jobs while the government added 400 jobs. This isn’t growth; it’s a reshuffle at a high cost to private-sector workers. Over the past year, Kansas has seen an overall increase of 24,000 jobs, with the private sector contributing 18,700 and the government sector adding 5,300, or about 20% of the total. During the recent special session, the Legislature passed several measures to boost the state’s economic prospects. One notable legislative action was passing a multi-billion dollar STAR bond to attract major sports franchises, especially the Chiefs and Royals from Missouri, just a few miles away. Investing in sports is like predicting Kansas weather—unpredictable and always exciting. There is potential for economic rain, but this will likely put you in a financial storm instead. Moreover, the recent special session saw efforts to provide broad tax relief, with the key being reducing tax brackets from three to two, which is a correct step toward a flat income tax. These changes could significantly impact Kansas’s economic landscape, reducing the tax burden and potentially helping grow the economy. However, the effectiveness of these measures will depend heavily on their implementation and the accompanying fiscal restraint. Flattening the income tax would transform Kansas from a flyover state into a destination. This move would simplify the tax code, making it fairer and less of a headache—because the only thing Kansans should worry about rising are the sunflowers. Kansas has also flirted with property tax relief with KPI promoting a constitutional amendment to limit appraisal valuation increases, which has broad support. The same or separate constitutional amendments should limit property tax levies, which cover the product of appraisals and tax rates, and cap state and local government spending to the rate of population growth plus inflation. The latter would best limit the true burden of government in the form of spending, providing predictability and stability for homeowners and businesses alike. Kansas is sitting on a $4 billion reserve—it’s like having a savings account when you’re deep in credit card debt. Responsible budgeting ensures fiscal sustainability and prevents the state from falling into the cycles of budget shortfalls and hasty tax hikes that have plagued it in the past. By following this approach, over-collected taxpayer money called a “surplus,” can be returned by cutting a flat income tax rate. This can be achieved by spending on essential services outlined in the state’s constitution, providing opportunities for strategic budget cuts and growth of no more than the rate of population growth plus inflation. This balanced approach helps ensure fiscal sustainability without compromising essential services. By implementing bold tax reforms and adopting a disciplined approach to spending, Kansas can pave the way for a prosperous future. These measures will create an environment conducive to job creation and economic competitiveness, ensuring that Kansas becomes a place where businesses thrive, and residents enjoy a higher quality of life. 3 Lessons on Why Free-Market Capitalism is the Best Path to Prosperity | This Week's Economy Ep. 697/12/2024 Join me as I discuss the following on how free-market capitalism:

💼 Fosters innovation by allowing entrepreneurs to create and compete, driving economic growth. 📈 Allocates resources efficiently through supply and demand, meeting consumer needs effectively. 🏡 Promotes liberty and economic freedom, enabling people to pursue their interests and improve living standards, even among those who disagree. Listen, like, share, and subscribe. Exploring Entrepreneurship and Federalism with John Tillman | Let People Prosper Show Ep. 1047/9/2024 Join me for Episode 104 of the Let People Prosper Show to dive into a discussion on the liberty movement in Illinois, the importance of federalism, and the benefits of entrepreneurship with John Tillman, CEO of the American Culture Project and chairman of the board at the Illinois Policy Institute.

Like, subscribe, and share the Let People Prosper Show, and visit vanceginn.com for more insights from me, my research, and ways to invite me on your show, give a speech, and more.  Originally published at Dallas Morning News.

More conservatives are likely to be elected to the statehouse in November. This is a historic opportunity in 2025 to enact a new budget that provides property tax relief, empowers all families with universal school choice and puts state spending in Texas on a more sustainable trajectory in 2025. Texas, in a nation grappling with unsustainable government spending, stands out for its relative fiscal restraint and economic dynamism. However, despite historically prudent budgetary policies, Texas lawmakers enacted the largest two-year budget increase last year and the second-largest property tax relief measure (though many claimed it was the largest). According to the Sustainable Budget Project by Americans for Tax Reform, Texas, unlike the federal government and the vast majority of states, has done better at aligning its budget growth with the average taxpayer’s ability to pay for government spending, as measured by the rate of population growth plus inflation. Over the past decade, federal spending has escalated by an astonishing 81.7%, nearly quadrupling the 23.2% rate of population growth plus inflation, according to Americans for Tax Reform data. In stark contrast, Texas has exhibited fiscal restraint, ensuring its spending did not spiral out of control. The implications of such fiscal prudence are profound. If the federal government had followed the sustainable budget approach from 2014 to 2023, it could have saved taxpayers an estimated $2.1 trillion in 2023 alone. Texas’ measured approach during this period allowed the state to spend and tax $22.0 billion less than it might have otherwise, benefiting taxpayers and the broader economy. The recent and uncharacteristic budgetary excesses in Texas diminish the capacity for property tax relief. Further property tax reform is crucial. Property taxes are unfair, burdensome, and they keep people renting from the government by paying property taxes forever. The competitive landscape is also evolving, with states like North Carolina and Florida thriving by implementing aggressive tax cuts and regulatory reforms. Texas must respond by intensifying its commitment to pro-growth policies and fiscal conservatism if the Lone Star State is to maintain economic leadership. A constitutional spending limit, similar to Colorado’s Taxpayer Bill of Rights, would help put state spending in Texas on a sustainable trajectory. Even in a blue state where progressives are in charge, this measure has effectively kept state and local spending in check. Its adoption in Texas would ensure that state and local budgets grow in line with the average taxpayer’s ability to pay. To truly distinguish itself, Texas should consider a strategic overhaul of its tax system, particularly in property taxes. With no personal income tax, Texas could relieve property holders of a significant financial burden by eliminating school district maintenance and operations property taxes. This shift, funded through better-controlled state and local government spending, could transform the economic landscape for homeowners and businesses. The state could achieve this monumental feat by using the resulting surpluses from spending restraint to reduce school district M&O property tax rates, aiming to phase them out over the next decade. The Texas Legislature already controls the school finance formulas so this property tax is mostly “local” in name only, and legislators have been phasing it down in recent years. It’s possible to reduce and even eliminate truly local property taxes by cities, counties, and special purpose districts through spending restraint that would produce surpluses, which can then be used to drive property tax rates down to zero over time. Some localities would take longer than others to accomplish this, but as people vote with their feet to places without property taxes, other local governments would look for ways to eliminate theirs. The result would be less government spending and little to no property taxes in Texas. This shift in a pro-growth direction would enhance homeowners’ financial freedom and support more economic growth through increased personal savings and business investment. Texas’ economic policies have historically positioned the state as a leader in job creation and financial freedom, helping to achieve record economic growth, job growth and in-migration. However, the path forward requires conserving and enhancing these policies. Texas must adapt to the changing economic landscapes by fostering a more favorable business climate, reducing governmental interference, and revamping its tax system to maintain and strengthen its competitive status. By prioritizing spending restraint, strategic tax relief and universal school choice, Texas can secure a prosperous economic future and set a standard for budgetary sustainability. Grover Norquist is president of Americans for Tax Reform, a taxpayer organization founded in 1985 at the request of President Ronald Reagan. Vance Ginn is a senior fellow at ATR, president of Ginn Economic Consulting, and previously served in the White House’s Office of Management and Budget. In the Energy News Beat - Conversation in Energy with Stuart Turley, Dr. Vance Ginn is interviewed about various pressing economic and political issues. They discuss the recent presidential debate, the state of the U.S. economy, the implications of red-state policies on job growth, and the impact of high energy costs on inflation. The conversation also covers the importance of school choice, immigration reform, Supreme Court rulings on free speech, the Chevron Supreme deference Court decision on regulatory issues, and the challenges of achieving net zero emissions amidst global economic shifts. Dr. Ginn emphasizes the need for sound financial policies and reducing government spending.

Please follow Vance on his substack HERE: https://vanceginn.substack.com/. It is a great source of finance and political insights. Vance, I would like to have you back and on the 3 Podcasters Walk into a Bar with David Blackmon and Rey Trevio. - Thanks again for your time, and talk soon - Stu  Originally published at National Review Online.

States must restrain spending growth while cutting and flattening income-tax rates. Economist Milton Friedman famously said, “I am in favor of cutting taxes under any circumstances and for any excuse, for any reason, whenever it’s possible. The reason I am is because I believe the big problem is not taxes, the big problem is spending.” This sentiment encapsulates the driving force behind the tax-cut revolution transforming the American economic landscape. This movement toward lower, flatter, and, in some cases, no income taxes is reshaping state fiscal policies to relieve taxpayers from funding excessive government. For instance, Georgia’s reduction of the state income-tax rate from 5.49 percent to 5.39 percent and Idaho’s shift to a flat income-tax rate of 5.8 percent enhance competitiveness and support more economic activity. Iowa’s adoption of a flat income tax rate of 3.8 percent, one of the lowest in the nation, further exemplifies this trend. Arkansas reduced individual and corporate tax rates, providing tax relief for the third time in 15 months. Hawaii’s substantial increase in standard deductions and adjustment of tax brackets aims to provide relief to low- and middle-income families. Kansas included property-tax relief alongside consolidating its income tax from three to two brackets. The tax-cut revolution represents a shift towards more efficient and equitable tax systems. By adopting flatter, lower tax rates, states can enhance their economic competitiveness and improve the quality of life for their residents. However, these tax cuts must be accompanied by sustainable budgeting practices that limit government spending. In 2023, Americans for Tax Reform (ATR) launched The Sustainable Budget Project, which monitors state government spending and tracks which states have or have not enacted sustainable budgets. The project defines a sustainable budget as one that limits the pace of state government spending to lower than the rate of population growth plus inflation. This approach ensures that government growth is kept in check, preventing excessive taxation and debt accumulation. Examining spending trends from 2014 to 2023 reveals the crux of the problem. Aggregate 50-state spending, excluding funding from taxpayers through the federal government, increased by 59.1 percent during this period. If states had restrained their spending to the rate of population growth plus inflation, they would have spent $1.44 trillion in 2023, $430 billion less than the $1.87 trillion spent. Over the entire decade, this would have saved $1.4 trillion, leaving more money in taxpayers’ pockets. Some states have demonstrated the benefits of sustainable budgeting. ATR found that six states held total spending growth below population growth plus inflation: Alaska, Colorado, North Dakota, Oklahoma, Texas, and Wyoming. Additionally, six other states held growth in state funds, which excludes federal funds, below the rate of population growth plus inflation: Louisiana, Massachusetts, Montana, North Carolina, Ohio, and Rhode Island. Sustainable budgeting is the key to ensuring long-term prosperity. By focusing on responsible budgeting and reducing obstacles to economic growth, such as high spending, taxes, and regulations, states can create an environment where everyone can prosper. Why Liberty Is Worth Celebrating on July 4th with Stephanie Slade | Let People Prosper Show Ep. 1037/2/2024 Join me for Episode 103 of the Let People Prosper Show to hear a deep discussion about fusionism, liberty, and more with the delightful Stephanie Slade, a senior editor at Reason, the magazine of "free minds and free markets"; a fellow in liberal studies at the Acton Institute; and a media fellow at the Institute for Human Ecology at Catholic University of America.

Like, subscribe, and share the Let People Prosper Show, and visit vanceginn.com for more insights from me, my research, and ways to invite me on your show, give a speech, and more. Originally published at American Energy Institute.

Post Debate: 7 Things The Presidential Candidates Should Know | This Week's Economy Ep. 676/28/2024 With the 2024 election approaching quickly and last night’s first presidential debate, I give a rundown on the top 7 things the candidates and those wanting to make a difference should know. The key is that states should lead the way by getting the federal government out of the way and returning power to the people.

Listen, like, share, and subscribe: vanceginn.substack.com.  Originally published at AIER.

The US economy faces numerous challenges, exacerbated by policy uncertainty and excessive government intervention. Milton Friedman famously said, “If you put the federal government in charge of the Sahara Desert, in five years there’d be a shortage of sand.” This sharp observation underscores the inefficiencies often associated with government intervention. Instead, we should advocate for free-market solutions that empower individuals and businesses to drive innovation and growth. Election years heighten policy uncertainty, driving economic volatility. Businesses and investors become cautious, waiting to see which policies will prevail. This hesitation can slow economic activity, affecting job creation and investment in new projects. More than half of Americans think we are in a recession even when the headline data say otherwise, reflecting a disconnect between reported statistics and personal experiences. Policy uncertainty during election years exacerbates these issues. The upcoming elections could significantly impact economic policies, depending on the direction taken by the administration. Whether it’s Biden’s continued interventionist policies or a shift under Trump, the stakes are high. Businesses, investors, and consumers are left guessing, which stalls responsible decision-making and hampers economic growth. The recent meeting of the Business Roundtable highlighted these concerns as both Biden and Trump pitched their economic visions. According to the Tax Foundation, Biden’s tax plan, which includes increases on corporations and the wealthy, could reduce GDP by 2.2 percent and eliminate 788,000 jobs over time. On the other hand, Trump’s tariff proposals that hike taxes on Americans would have economic consequences, increasing consumer prices and reducing household incomes. The Federal Reserve’s decisions also play a crucial role in shaping the economic landscape. Recent hikes in interest rates to curb inflation have added another layer of uncertainty. Higher borrowing costs can dampen consumer spending and business investment, slowing economic growth. The Fed’s policy trajectory remains uncertain, contributing to a cautious outlook among businesses and investors. Biden’s regulatory approach further complicates matters. His administration has introduced numerous regulations affecting various sectors, from energy to finance. While intended to address climate change and market stability, these regulations often have significant compliance costs and operational challenges. The regulatory burden can stifle innovation and deter investment, particularly in industries struggling with economic headwinds. Another key aspect is the role of institutions. Friedrich Hayek, in his seminal work “The Road to Serfdom,” cautioned against the overreach of central planning. He emphasized that central planning often leads to inefficiencies and a loss of individual freedoms. His insights are particularly relevant today as we navigate the complexities of modern economies. To truly flourish, governments should embrace free-market capitalism and resist the creeping influence of socialism. This principle applies across sectors. By focusing on the efficient use of resources, reducing regulatory burdens, and fostering competition, we can build a more prosperous future. The bottom-up approach ensures better utilization of resources and empowers entrepreneurs, businesses, and local communities. Policies such as eliminating unnecessary regulations, reducing corporate tax rates, and promoting school choice are vital. These policies drive economic growth and ensure that resources are used where they are most needed. Policy uncertainty during election years can create a precarious economic environment. Given the numerous issues in Washington, states must lead the way in our system of federalism. The increasing divergence between red and blue states on taxes, labor, and education highlights this trend. Red states cut taxes and promote business-friendly policies, while blue states often expand government programs. This divergence allows states to set examples of effective governance through free-market principles. By reducing regulatory burdens, passing sustainable budgets, and fostering competition, states can mitigate some national policy uncertainties that stall economic progress. The next big step in federalism involves states innovating beyond traditional policies. For instance, states should focus on restraining government spending, eliminating bad taxes like income taxes, and reducing onerous regulations. Policies promoting school choice can also drive education reform and better outcomes, ensuring that all children have access to quality education regardless of their socioeconomic background. In addition, more freedom in technology and innovation should be ensured to support the next big revolution that improves our lives and livelihoods. To move forward, we must build from our past experiences and rise to overcome obstacles. We can foster innovation and resilience by acknowledging and learning from our failures. It’s essential to recognize that failure provides valuable lessons and opportunities for growth. Expanding government intervention in response to failures often stifles this learning process and leads to greater inefficiencies. Policy uncertainty during election years can create a precarious economic environment. States must lead the way in our system of federalism, setting examples of effective governance through free-market principles. By passing sustainable budgets, reducing regulatory burdens, and fostering competition, states can mitigate some national policy uncertainties that stall economic progress. Let’s leverage the strengths of the free market, prioritize efficiency, and ensure that our policies truly benefit Americans. By embracing free-market principles, reducing regulatory burdens, and fostering competition, we can pave the way for a stronger and more prosperous America. Together, we can build a future where smart policies and strong institutions that support life, liberty, and property pave the way for economic resilience and growth. Improve Immigration by Strengthening American Values with Dr. Veronique de Rugy| LPP ep. 1026/25/2024 Join me for Episode 102 of the Let People Prosper Show to hear a deep discussion with the fantastic Dr. Veronique (Vero) de Rugy, the George Gibbs Chair in Political Economy and Senior Research Fellow at the Mercatus Center at George Mason University, who migrated from France to America.

We Explore: -How the entrepreneurial spirit contributes to immigration between countries. - What the differences are between national conservatism and classical liberalism. - Which policies would improve the economic and fiscal picture. Like, subscribe, and share the Let People Prosper Show, and visit vanceginn.substack.com and vanceginn.com for more insights from me, my research, and ways to invite me on your show, give a speech, and more.  Hello everyone,

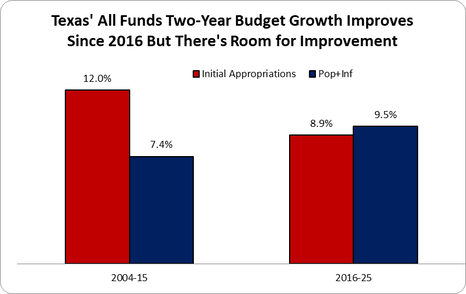

It’s a pleasure to be with you today. As one who believes strongly in free markets and individual liberty and has served as the chief economist of multiple think tanks and at the White House’s Office of Management and Budget, I’ve come from Texas not with barbecue, as you also have delicious barbecue, but with a recipe for economic prosperity that I hope you’ll find equally savory. It’s great to visit Kansas and contribute to the fantastic work at the Kansas Policy Institute. My business at Ginn Economic Consulting works with KPI and 14 other think tanks nationwide. In these capacities, I hear of the attention that Kansas receives for its past tax cuts without spending restraint and current efforts for tax relief. Kansas has been in an economic slow cook for decades, trailing behind national averages in job growth, population increases, and economic output. Much like a poorly tended grill, high taxes, and selective business subsidies have smoked out potential growth, leaving behind more stagnation than sustenance. Let’s chew over some numbers: From 1979 to 2022, Kansas's job growth limped along at just 53% compared to the national average of 88%. Imagine the vibrancy of having an additional 451,000 jobs in the state—jobs that could have been fostered with more competitive tax policies. Moreover, Kansas has seen a net exodus of nearly 198,000 residents since 2000, driven away by a tax environment as welcoming as a blizzard in May. The states with the lowest tax burdens saw an influx of 4.6 million people from domestic migration during the same period, while the high-tax states watched 10.7 million residents pack up and leave. In the most recent IRS data, Kansas lost $2.1 billion in adjusted gross income due to people moving out since 2017. In May 2024, Kansas's unemployment rate ticked up to 2.9%, a slight increase from 2.8% but a revealing one. The total nonfarm payroll employment saw a marginal uptick by 100 jobs last month. Beneath this weak report, there was more weakness as the private sector lost 300 jobs while the government added 400 jobs. This isn’t job growth; it’s a reshuffle at a high cost to private-sector workers. And this is a trend we've seen before. Over the past year, Kansas has seen an overall increase of 24,000 jobs, with the private sector contributing 18,700 and the government sector adding 5,300, or about 20% of the total. Milton Friedman once quipped, “If you put the federal government in charge of the Sahara Desert, in five years there’d be a shortage of sand.” In Kansas, if you continue to rely on excessive taxing and spending for growth, you will find yourself short on more than just jobs and people but on opportunity that drives prosperity. During the recent special session, the Legislature passed several measures to attempt to boost the state’s economic prospects. One notable legislative action was passing a $3 billion STAR bond to attract major sports franchises. Investing in sports is like predicting Kansas weather—unpredictable and always exciting. There is potential for economic rain, but you might be in a financial storm without careful budgeting and rigorous oversight. While what is seen is the possible construction, new jobs around, and new tax revenue, the unseen is costly. This includes the poor precedence for other wasteful acts by the government, higher taxes on those nearby and over time, and the lack of knowledge about what will happen over the next 30 years to the teams, the community, or other costs that come with government planning. Moreover, the recent special session saw positive efforts for broad tax relief, with the key being reducing income tax brackets from three to two, which is a step toward a much-needed flat income tax. Starting in tax year 2024, married Kansans filing jointly would have their taxable income taxed at 5.2% up to $46,000 and at 5.58% above that amount. The changes should significantly impact Kansas by reducing the tax burden and unleashing economic growth as people are incentivized to save, invest, and work. However, the effectiveness of these measures will depend heavily on accompanying spending restraint. Let’s talk about property taxes. Kansas has started the pit on property tax relief, but it’s time to cook it. Tentative tax relief discussions this year hinted at significant cuts, but Kansas should solidify this with a constitutional amendment to limit levy increases. Think of it as putting a leash on a dog prone to running off—you ensure it’s safe and always in sight. The amendment should cap annual increases as low as possible if property taxes increase at all, providing predictability and stability for homeowners and businesses alike. Regarding income taxes, flattening the income tax would turn Kansas from a flyover state into a destination. This move would simplify the tax code, making it fairer and less of a headache—because the only thing Kansans should worry about rising are the sunflowers. While the Legislature tried it this year, you should keep this as part of the approach next time. The reason why is easy to see. States with lower tax burdens consistently show superior economic growth trends; between 1998 and 2022, the ten states with the lowest tax burdens averaged 51% growth in private-sector employment, compared to 34% for the states with the highest burdens. Kansas managed a modest 16% growth during this period, ranking 44th. Kansas is sitting on a $4 billion reserve—it's like having a savings account when you’re deep in credit card debt. You should use this wisely with a responsible budget model that KPI has put forward for years now, allowing spending to grow no more than by population growth plus inflation, preferably by much less to overcome past spending excesses. This isn’t just tightening the belt; it’s ensuring you can still afford it in the future. Responsible budgeting ensures fiscal sustainability and prevents the state from falling into the cycles of budget shortfalls and hasty tax hikes that have plagued Kansas in the past. By following this approach, over-collected taxpayer money, called a “surplus,” can be returned by cutting a flat income tax rate to zero as quickly as possible. Kansas has seen its share of financial missteps, but now is the time for bold action. The legislative decisions made today will determine the state’s economic future. Legislative candidates, you are positioned to lead Kansas into a new era of fiscal responsibility and economic growth. The decisions made in the coming years will determine whether Kansas continues along the path of stagnation or redirects toward prosperity. Consider these policy recommendations not just as suggestions but as necessary steps toward securing a thriving economic future for Kansas. Kansas must also embrace responsible budgeting for these tax cuts to be sustainable. The state should learn from the lesson of excessive spending during the last decade’s troubles, which led to deficits and foolish tax hikes. In fact, the 2025 General Fund budget is 69% higher than in 2017 when Governor Kelly took office, or $3.7 billion higher than inflation over this period. Reining in this excessive use of taxpayer money to spend it on only limited roles outlined in the state’s constitution would provide opportunities for strategic budget cuts and increases of less than the rate of population growth plus inflation. This responsible approach helps ensure fiscal sustainability without compromising essential services. Thank you for your dedication to Kansas and your commitment to principles that enhance not just the economy but also liberty. You can help ensure Kansas becomes a beacon of fiscal responsibility and economic success, where every resident wants to stay and others are eager to join. Roll up your sleeves, sharpen your pencils, and get to work on policies that let Kansans prosper. After all, as Friedman would say, "Nothing is so permanent as a temporary government program"—aim for long-term policies with fewer tradeoffs to support the most opportunities. Thank you, and if you’d like to continue this conversation, I invite you to connect with me at [email protected] and subscribe to my newsletter at www.vanceginn.substack.com. Let’s work together along with the great folks at KPI to create a future where Kansans can truly prosper.  Government Spending Is The Problem The late, great economist Milton Friedman said, "The real problem is government spending." This is true as spending comes before taxes or regulations. In fact, if people didn't form a government or politicians didn’t create new programs, then there would be no need for government spending and no need for taxes. And if there was no government spending nor taxes to fund spending then there would be no one to create or enforce regulations. While this might sound like a utopian paradise, which I agree, there are essential limited roles for governments outlined in constitutions and laws. Of course, most governments are doing much more than providing limited roles that preserve life, liberty, and property. This is why I have long been working diligently for more than a decade to get a strong fiscal rule of a spending limit enacted by federal, state, and local governments promptly under my calling to "let people prosper," as effectively limiting government supports more liberty and therefore more opportunities to flourish. Fortunately, there have been multiple state think tanks that have championed this sound budgeting approach through what they've called either the Responsible, Conservative, or Sustainable State Budget. I recently worked with Americans for Tax Reform to publish the Sustainable Budget Project, which provides spending comparisons and other valuable information for every state. This groundbreaking approach was outlined recently in my co-authored op-ed with Grover Norquest of ATR in the Wall Street Journal. When Did This Budget Approach Begin? I started this approach in 2013 with my former colleagues at the Texas Public Policy Foundation with work on the Conservative Texas Budget. The approach is a fiscal rule based on an appropriations limit that covers as much of the budget as possible, ideally the entire budget, with a maximum amount based on the rate of population growth plus inflation and a supermajority (two-thirds) vote to exceed it. A version of this approach was started in Colorado in 1992 with their taxpayer's bill of rights (TABOR), which was championed by key folks like Dr. Barry Poulson and others. (picture below is from a road sign in Texas)  Why Population Growth Plus Inflation? While there are many measures to use for a spending growth limit, the rate of population growth plus inflation provides the best reasonable measure of the average taxpayer's ability to pay for government spending without excessively crowding out their productive activities. It is important to look at this from the taxpayer’s perspective rather than the appropriator’s view given taxpayers fund every dollar that appropriators redistribute from the private sector. Population growth plus inflation is also a stable metric reducing uncertainty for taxpayers (and appropriators) and essentially freezes inflation-adjusted per capita government spending over time. The research in this space is clear that the best fiscal rule is a spending limit using the rate of population growth plus inflation, not gross state product, personal income, or other growth rates. In fact, population growth plus inflation typically grows slower than these other rates so that more money stays in the productive private sector where it belongs. To get technical for a moment, personal income growth and gross state product growth are essentially population growth plus inflation plus productivity growth. There's no reasonable consideration that government is more productive over time, so that term would be zero leaving population growth plus inflation. And if you consider the productivity growth in the private sector, then more money should be in that sector at the margin for the greatest rate of return, leaving just population growth plus inflation. Population growth plus inflation becomes the best measure to use no matter how you look at it. Given the high inflation rate more recently, it is wise to use the average growth rate of population growth plus inflation over a number of years to smooth out the increased volatility (ATR's Sustainable Budget Project uses the average rate over the three years prior to a session year). And this rate of population growth plus inflation should be a ceiling and not a target as governments should be appropriating less than this limit. Ideally, governments should freeze or cut government spending at all levels of government to provide more room for tax relief, less regulation, and more money in taxpayers' pockets. Overview of Conservative Texas Budget Approach Figure 1 shows how the growth in Texas’ biennial budget was cut by one-fourth after the creation of the Conservative Texas Budget in 2014 that first influenced the 2015 Legislature when crafting the 2016-17 budget along with changes in the state’s governor (Gov. Greg Abbott), lieutenant governor (Lt. Gov. Dan Patrick), and some legislators. The 8.9% average growth rate of appropriations since then was below the 9.5% biennial average rate of population growth plus inflation since then, which this was drive substantially higher after the latest 2024-25 budget that is well above this key metric (before this biennial budget the growth rate was 5.2% compared with 9.4% in the rate of population growth plus inflation).  This approach was mostly put into state law in Texas in 2021 with Senate Bill 1336, as the state already has a spending limit in the constitution. The bill improved the limit to cover all general revenue ("consolidated general revenue") or 55% of the total budget rather than just 45% previously, base the growth limit on the rate of population growth times inflation instead of personal income growth, and raise the vote from a simple majority to three-fifths of both chambers to exceed it instead of a simple majority. There are improvements that should be made to this recent statutory spending limit change in Texas, such as adding it to the constitution and improving the growth rate to population growth plus inflation instead of population growth times inflation calculated by (1+pop)*(1+inf). But this limit is now one of the strongest in the nation as historically the gold standard for a spending limit of the Colorado's Taxpayer Bill of Rights (TABOR) has been watered down over the years by their courts and legislators, as it currently covers just 43% of the budget instead of the original 67%. My Work On The Federal Budget In The White House From June 2019 to May 2020, I took a hiatus from state policy work to serve Americans as the associate director for economic policy ("chief economist") at the White House's Office of Management and Budget. There I learned much about the federal budget, the appropriations process, and the economic assumptions which are used to provide the upcoming 10-year budget projections. In the President's FY 2021 budget, we found $4.6 trillion in fiscal savings and I was able to include the need for a fiscal rule which rarely happens (pic of President Trump's last budget).  Sustainable Budget Work With Other States and ATR When I returned to the Texas Public Policy Foundation in May 2020, as I wanted to get back to a place with some sense of freedom during the COVID-19 pandemic and to be closer to family, I started an effort to work on this sound budgeting approach with other state think tanks. This contributed to me working with many fantastic people who are trying to restrain government spending in their states and the federal levels. Here are the latest data on the federal and state budgets as part of ATR's Sustainable Budget Project. From 2014 to 2023, the following happened: Federal spending increased by 81.7%, nearly four times faster than the 23.1% increase in the rate of population growth plus inflation.

Result: American taxpayers could have been spared more than $2.5 trillion in taxes and debt just in 2023 if federal and state governments had grown no faster than the rate of population growth plus inflation during the previous decade. And this would be even more if we considered the cumulative savings over the period.  My hope is that if we can get enough state think tanks to promote this budgeting approach, get this approach put into constitutions and statutes, and use it to limit local government spending as well, there will be plenty of momentum to provide sustainable, substantial tax relief and eventually impose a fiscal rule of a spending limit on the federal budget. This is an uphill battle but I believe it is necessary to preserve liberty and provide more opportunities to let people prosper. Sustainable State Budget Revolution Across The Country Below are the states and think tanks which I'm working with and this revolution is going, which you can find an overview of this budgeting approach in Louisiana and should be applied elsewhere. I update these periodically, successful versus not successful budgeting attempts being 20-7 so far.

If you're interested in doing this in your state, please reach out to me. For more details, check out these write-ups on this issue by Grover Norquist and I at WSJ, Dan Mitchell at International Liberty, and The Economist. Don’t miss Episode 66 with 6 things you didn’t read in the news this week:

📊 April's BLS State JOLTS report shows varied job market dynamics with Texas and Florida leading growth. Less government intervention is key to prosperity. 🏫 Louisiana's new universal education savings account program expands K-12 options, showcasing the benefits of school choice. 📉 The latest CBO report highlights a dire fiscal situation, projecting $3 trillion deficits and $51 trillion debt by 2034. Pro-growth policies are crucial. 📈 Michigan needs improvements to sustainable budgeting and economic freedom to boost job creation and living standards. Get the show notes here: https://vanceginn.substack.com #EconomicGrowth #SchoolChoice #FiscalPolicy #JobMarket #ThisWeeksEconomy  Originally published at Mackinac Center.

Michigan’s economic health and fiscal policies are critical for its future prosperity. Understanding where the state stands in various economic freedom measures can help identify areas for improvement and guide policy decisions. Fraser Institute Rankings The Fraser Institute publishes the Economic Freedom of North America index, which evaluates how states' policies support economic freedom. The index considers three main areas: government spending, taxes and labor market regulations. Higher scores indicate greater economic freedom. In the latest report, Michigan ranks 31st in economic freedom among U.S. states. This ranking reflects areas where Michigan lags in supporting economic freedom and highlights opportunities for policy improvements. Government Spending: This component measures the size of government relative to the economy. Lower government spending relative to GDP indicates more economic freedom. Michigan ranks 28th, suggesting a need to control spending better. Taxes: This component assesses the impact of taxes on economic incentives. Higher tax burdens discourage investment and economic activity. Michigan ranks 19th, indicating room for tax reforms to enhance economic freedom. Labor Market Regulations: This component examines labor market regulations, such as minimum wage laws and forced membership in a labor union. Stricter regulations can reduce economic freedom by limiting the flexibility of labor markets, thereby making it more difficult for employers and employees to find the best fit for each other. Michigan ranks 38th, so improving labor market regulations can help Michigan enhance its economic freedom ranking — improving opportunities for employers and employees alike. Economic Factors Labor Market: The latest BLS data shows Michigan’s unemployment rate is 3.9%, the same as the U.S. rate. But the number of employed persons increased by only 0.9% over the past year, half the national growth rate of 1.8%. The slower hirings highlight the need for more job opportunities from faster economic growth in Michigan. Employment Trends: According to the Michigan Labor Market Information, the state has seen slow employment growth, with particular struggles in industries such as manufacturing and financial activities. This emphasizes the need for pro-growth policies to make it easier for businesses to grow, leading to more and better-paying jobs. Labor Force Participation Rate: Michigan’s labor force participation rate — the share of people ages 16 and over working or seeking work — is 61.7%. That’s lower than the national average of 62.3%. If you, as a consumer, find fewer employees when you need to talk to someone at a business, that’s an example of why the participation rate matters. Wage Growth: Wage growth in Michigan has been slower than the national average, affecting the economic well-being of its residents. Path to Improvement Tax Reform: Lowering tax rates can support economic growth and attract business investment. Reducing the state income tax and exploring other tax reforms can make Michigan more competitive with other states. A more favorable tax environment can increase business activity, job creation and wages. Regulatory Efficiency: Streamlining regulations can reduce the burdens businesses face. By simplifying regulatoryprocesses and reducing bureaucratic hurdles, Michigan can make it easier for businesses to start and grow, leading to a more vibrant economy with more goods and services available. Spending Discipline: Implementing strict budgetary controls can ensure that spending growth does not exceed the combined rate of inflation and population growth, maintaining the state government’s fiscal stability. Michigan can achieve long-term fiscal health by focusing government spending on areas with the largest impact and eliminating wasteful spending. Labor Improvement: Reinstating a right-to-work law will lead to more jobs. By addressing its economic and fiscal policy weaknesses, Michigan can improve its rankings and create a more robust and dynamic economy. Sustainable budgeting, tax reform and regulatory efficiency are key to unlocking Michigan’s economic potential. By implementing these strategies, Michigan can enhance its economic freedom, attract investment and ensure long-term prosperity for its residents.  Originally published at AIER.

As 2025 draws near, America teeters on the brink of a fiscal abyss. This impending fiscal cliff, marked by the end of tax cut provisions and a spending crisis, calls for immediate and decisive action by Congress to avert a worse economic situation than the one Americans feel today. The national debt from excessive government spending is on track to surpass $35 trillion soon, a stark increase of nearly $10 trillion since 2020. This level of debt per citizen exceeds $100,000; per taxpayer, it is nearly $267,000. Such figures are not just numbers but represent a looming burden that future generations will bear — a burden that transcends mere fiscal policy and ventures into the realm of ethical responsibility. The gravity of this debt is exacerbated by the interest payments it necessitates, which have soared to over $1 trillion annually, surpassing what the country spends on national defense. This situation illustrates a troubling scenario where the government, to manage its debt, resorts to issuing more debt, a practice unsustainable by any standard measure of sound budgeting. The economic repercussions of this cycle of debt are profound, leading to higher interest rates, likely increased inflation, and a misallocation of resources that stifles productive private sector activity. Amidst these challenges, the Tax Cuts and Jobs Act (TCJA) provisions, set to expire in 2025, play a pivotal role. These tax cuts have been instrumental in supporting economic activity across all income brackets by reducing their tax burden. If these cuts expire, they could reverse the economic gains achieved, reducing disposable income, dampening savings and investment, and contributing to an economic downturn in an already fragile economy. The cessation of these benefits would particularly impact families who have benefited from the near doubling of the standard deduction and enhancements to the child tax credit. Furthermore, the expiration of the $10,000 cap on state and local tax (SALT) deductions could have mixed effects; while it may benefit taxpayers in primarily blue, high-tax states, it complicates the fiscal landscape significantly. A balanced approach would be to maintain the increased standard deduction while simplifying the tax code further by eliminating complex provisions like the SALT deduction and the child tax credit, promoting a flatter, more equitable tax system with one low tax rate for everyone. This would also support more economic growth that, combined with spending less, can quickly get our fiscal house in order. This fiscal predicament is further complicated by President Biden’s commitment not to raise taxes on those earning less than $400,000 annually. This promise will be difficult to keep if the TCJA provisions expire without appropriate legislative adjustments, further imperiling his dwindling reelection hopes in November. This situation and recent tariff impositions that affect all income levels would represent a double blow to American taxpayers, dampening economic prospects. As we face these fiscal upheavals, the discretionary spending caps and the debt ceiling, due to expire in 2025, add complexity to an already challenging budgetary environment. The US risks a severe budgetary crisis without thoughtful reform, particularly in the so-called “entitlement programs” like Social Security and Medicare, which consume a substantial portion of the federal budget. These areas must be addressed because both will be essentially bankrupt over the next decade, and millions of recipients will face substantial cuts in benefits. Given all these challenges, fiscal and monetary rules are paramount. Congress should implement a fiscal rule after cutting federal spending to at least the pre-lockdown level in 2019. Implementing rules like the Sustainable American Budget, which caps federal spending based on population growth plus inflation, could provide a sustainable path forward. This approach, supported by Americans for Tax Reform along with the economic insights of Alberto Alesina and John Taylor, advocates for austerity focused on spending restraint and economic growth rather than tax hikes, as some on the “new right” have recently advocated. Regarding a monetary rule, the Fed should return to a single mandate of price stability, cut its bloated balance sheet to at least the pre-lockdown level in 2019, and adopt a strict rule that ideally would be on the growth of its monetary base. These steps would help reduce persistent inflation and remove the extraordinary distortions throughout asset prices and the production process because of years of quantitative easing and low interest rates. Combining these monetary and fiscal rules would provide the necessary checks and balances to give the economy time to heal from massive government failures and help support a stronger institutional framework for economic growth and individual flourishing. Moreover, the regulatory environment has grown increasingly burdensome under the Biden administration, with an estimated $1.6 trillion in new final rules imposed since President Biden took office through May 2024. These rules have been applied across the economy, including financial decisions based on ESG factors influencing the energy sector to increase car emission standards influencing the auto sector. But these ultimately influence producers’ and consumers’ costs of many goods and services. Removing the burden on Americans would unleash economic growth, helping with the fiscal and economic headwinds. The bad policies out of DC have created a dire fiscal and economic situation moving into 2025. If the Trump tax cuts expire, excessive spending will continue unabated, and corrective monetary policy will not happen. Uncertainty and expectations alone will result in a hard landing in the economy, job losses, and elevated inflation. Given the last four years of declining purchasing power for millions of Americans, this result is unacceptable, and the idea of raising taxes to attempt to solve this is naive. Instead, the US must leverage this crisis as an opportunity for sweeping reforms. By returning to principles of fiscal responsibility and market-driven activity, America can navigate away from the fiscal abyss and toward a future of economic stability and prosperity. Though fraught with challenges, this moment offers an unparalleled chance to reshape America’s fiscal landscape, ensuring a legacy of growth and stability for future generations.  Originally published at Mackinac Center.

Michigan’s economic and fiscal future hinges on adopting sustainable budgeting practices. Insights from other states show the tangible benefits of fiscal restraint, efficiency, and lower taxes. By examining how other states have managed their budgets, Michigan can learn valuable lessons in improving its fiscal health and thus secure a prosperous future. In 2023, Americans for Tax Reform launched its Sustainable Budget Project. This project monitors state government spending and tracks which states have enacted “sustainable budgets.” The Sustainable Budget Project defines a sustainable budget as one that grows no more than a specific rate: the inflation rate plus population growth, as expressed as a percentage. This project is similar to Mackinac Center’s Sustainable Michigan Budget. For comparison, Texas has focused on fiscal discipline and low taxes, creating a business-friendly environment that attracts investment. It has kept government spending in check, which fosters an environment conducive to economic growth. As a result, it projects a $21 billion surplus next year despite the recent large budget increase. In contrast, California faces a significant economic challenge due to high taxes and heavy spending habits. With the state facing an upcoming budget deficit of at least $45 billion, Gov. Gavin Newsom has proposed painful spending cuts to various social programs. This development highlights the risks of unsustainable budgeting. California relies on volatile revenue sources (especially a progressive income tax with high rates) and has failed to implement spending discipline, leaving it in a precarious fiscal situation. Other states, such as Alaska, Colorado, North Dakota, Oklahoma, Texas and Wyoming have kept spending growth below the rate of population growth plus inflation over the last decade. They’ve maintained lower taxes and enjoyed better economic health even though most of these depend partially on volatile oil and gas activity. These states have demonstrated that sustainable budgeting can lead to greater economic stability and improved quality of life for residents. Their commitment to fiscal discipline has allowed them to weather economic downturns more effectively and avoid severe budget shortfalls. Implications for Michigan Michigan's budget growth outpaces both inflation and population growth, placing a heavy burden on taxpayers. Officials can reduce this burden by adopting sustainable budgeting practices like those of successful states. This will support more economic growth and attract businesses. Sustainable budgeting can also enhance Michigan’s economic resilience, making it less susceptible to economic shocks and fiscal crises, which have historically burdened oil and gas states. The benefits of sustainable budgeting extend beyond fiscal stability. By reducing unnecessary spending and lowering taxes, Michigan can increase disposable income for families, encourage consumer spending, and boost total economic activity. This can lead to more jobs, higher wages and improved living standards for all Michiganders. To achieve sustainable budgeting, Michigan should implement strict budgetary controls, such as spending caps and mandatory budget reviews. Additionally, the state should focus on long-term fiscal and economic health by eliminating wasteful spending, increasing spending prudently and reducing tax burdens. Transparency and accountability in the budget process are also crucial for spending taxpayer money wisely. Sustainable budgeting is not just about balancing the budget — it's about ensuring a brighter future for all Michiganders. By adopting best practices from other states, Michigan can become a model of fiscal discipline and economic vitality, providing a stable and prosperous environment for its residents and future generations. How the Fed Destroys the Economy with Dr. Robert Gmeiner | Let People Prosper Show Ep. 1016/17/2024 Join me for Episode 101 of the Let People Prosper Show, where I discuss with the insightful Dr. Robert Gmeiner how the Federal Reserve's actions affect our economy. Dr. Gmeiner is an Assistant Professor of Financial Economics at Methodist University.

We Explore: 📉 How the Federal Reserve distorts market activity and creates inflation. 📊 How the Fed’s actions harm economic growth and manipulate interest rates. 💡 Why fiscal policy is not the primary cause of inflation. 🔮 How you should plan to deal with elevated inflation for years to come. Like, subscribe, and share the Let People Prosper Show, and visit vanceginn.substack.com for more insights from me, my research, and ways to invite me on your show, give a speech, and more. Don’t miss the latest economic news in 11 minutes:

🎙️ Inflation Concerns & Fed’s Bloated Balance Sheet 🌱 ESG Divestment & Bank Regulation Issues 💸 Biden’s New Tariffs: A Step Backwards! Thank you for watching! Please like, share, and subscribe for more insights. For more info, subscribe to my newsletter at vanceginn.substack.com and check out vanceginn.com. |

Vance Ginn, Ph.D.

|

RSS Feed

RSS Feed

Proudly powered by Weebly