|

In this episode, we discuss: 1) How Arkansas continues to grapple with the same issues decade after decade, including a broken foster care system, high poverty rates, and poor K-12 reading scores; 2) Why safety net reforms are key to Arkansas' flourishing, specifically concerning Medicaid; and 3) How more school choice would put Arkansas on the map, and why Arkansas has the potential to be the next go-to state like Texas, Florida, and Tennessee. Nic’s bio:

For show notes, thoughtful insights, media interviews, speeches, blog posts, research, and more, check out my website (https://www.vanceginn.com/) and please subscribe to my newsletter (www.vanceginn.substack.com), share this post, and leave a comment.

0 Comments

This Week's Economy Ep. 21 | Happy Birthday, Milton Friedman: Economic Wisdom That Still Applies Now8/11/2023 Today, I'm honoring what would have been the 111th birthday of Nobel prize winner and economist Milton Friedman. His economic wisdom has profoundly impacted my philosophy. By discussing some of his most famous quotes, I divulge how so much of Friedman's findings and theories still apply today, and how we could have a better economy with more human flourishing by incorporating more of his research and views. Two of my favorite books of his I recommend: You can watch this episode and others along with my Let People Prosper Show on YouTube or listen to it on Apple Podcast, Spotify, Google Podcast, or Anchor. Please share, subscribe, like, and leave a 5-star rating!

For show notes, thoughtful insights, media interviews, speeches, blog posts, research, and more, check out my website (https://www.vanceginn.com/) and please subscribe to my newsletter (www.vanceginn.substack.com), share this post, and leave a comment. Today, I'm honored to be joined by Dr. Michael Munger, director of the interdisciplinary politics, philosophy, and economics program at Duke University and professor of political science. We discuss: 1) How transaction costs, including regulations and political corruption, prolong poverty and prevent prosperity and the role of economic freedom in human flourishing; 2) Whether capitalism can work within America’s republic and the ways in which it's currently failing because of too much government; and 3) Why cutting taxes without cutting spending is futile and the need for de-regulation, especially in regards to housing. Dr. Munger’s bio:

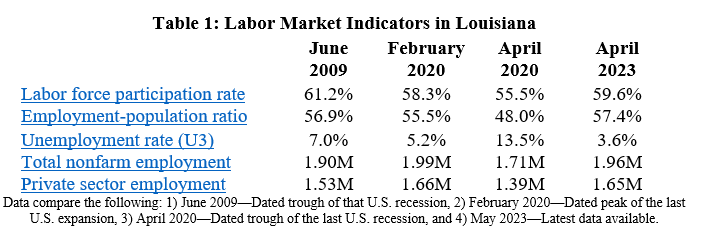

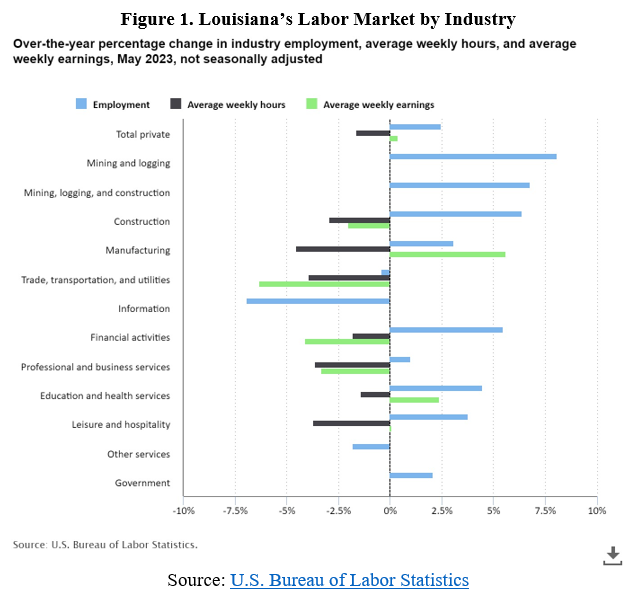

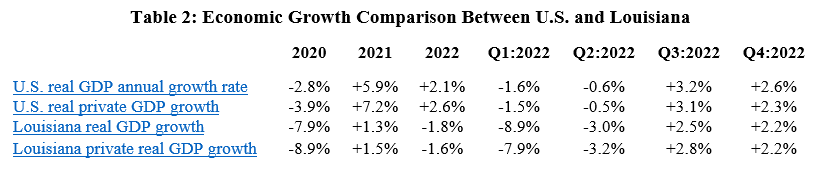

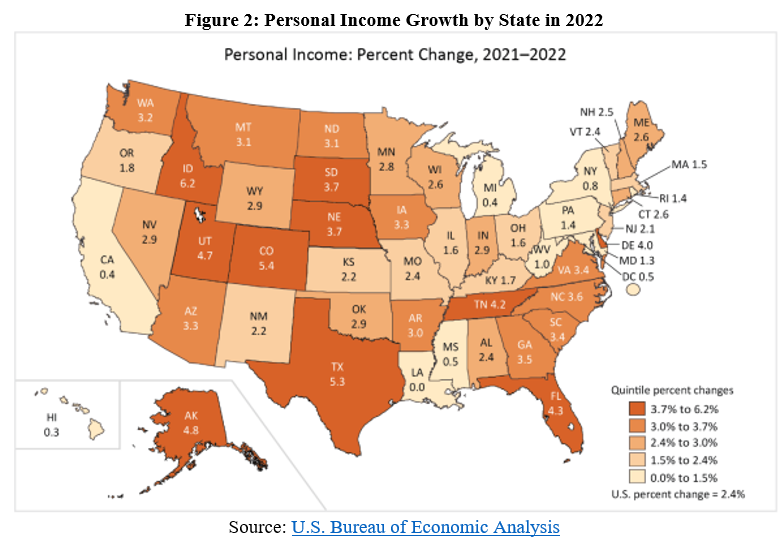

For show notes, thoughtful insights, media interviews, speeches, blog posts, research, and more, check out my website (https://www.vanceginn.com/) and please subscribe to my newsletter (www.vanceginn.substack.com), share this post, and leave a comment.  Key Point: Louisiana’s labor market shows improvement on the surface but there are underlying problems because of poor public policies which can be overcome with the Pelican Institute’s “Comeback Agenda.” Louisiana’s Labor Market: Table 1 shows Louisiana’s labor market information over time until the latest data for May 2023 which was released this month by the U.S. Bureau of Labor Statistics. The BLS report has two surveys which provide different information about the labor market. The payroll survey provides information on nonfarm employment based on responses by established employers for at least two years. The household survey provides responses from households for those who have a job and their demographics, which determines measures like the labor force participation rate and unemployment rate.  The payroll report shows that Louisiana’s net total nonfarm jobs increased by 4,600 jobs last month (+0.2%) to 1.96 million employed, which is 29,700 jobs below the pre-shutdown level in February 2020. Private sector employment was up by 4,400 jobs (+0.3%) to 1.65 million and government employment increased by 200 jobs (+0.1%) to 317,100 last month. Compared with a year ago, total employment was up by 48,400 jobs (+2.5%), with the private sector adding 41,700 jobs (+2.6%) and the government adding 6,700 jobs (+2.2%). This results in about 85% of all nonfarm jobs being in the productive private sector while 15% is in the government sector, which is the same as the share for the entire U.S. Figure 1 shows the percent changes in changes in employment, average weekly hours, and average weekly earnings by industry over the last year. The industries leading the way in increases in employment are mining and logging, construction, and financial activities while information and other services have the largest declines. Average weekly hours have declined or been flat in all industries with manufacturing, trade, and professional and business services declining the most. Average weekly earnings increased the most in manufacturing and education and health services but declined in most industries with trade and financial activities declining the most. These data show the dichotomy between those in the labor market as there are industries gaining employment but average weekly earnings are falling in most cases and are falling even further when adjusted for inflation, hurting many chances for Louisianans to make ends meet.  The household survey finds that the working-age population, defined as 16 to 64 years old, declined by another 894 people last month to 3.6 million, down 10,623 people over the last year, and down 34,106 people since February 2020. But the civilian labor force, defined as those who are working or looking for work, rose by 3,377 people to 2.1 million last month, 22,506 people over last year, and 27,910 people since February 2020. These figures result in a labor force participation rate of 59.6%, which is up from 58.8% from last year and up from 58.3% since pre-shutdown but well below the 61.2% rate in June 2009. But the number of employed has been increasing as it was up 2,363 over the last year, contributing to the slightly higher unemployment rate over the last year from 3.5% to 3.5%; but this rate remains lower than the 5.2% rate in February 2020. And a broader look at Louisiana’s labor market shows that Louisianans still face challenges with the continued decline in the working-age population which weighs on the labor-market shortage and long-term economic growth. And comparisons with neighboring states based on several labor market measures indicate concerns. Economic Growth: The U.S. Bureau of Economic Analysis (BEA) recently provided the real (inflation-adjusted) gross domestic product (GDP) and personal income for Louisiana and other states. Table 2 shows how the U.S. and Louisiana economies performed since 2020. The steep declines were during the shutdowns in 2020 in response to the COVID-19 pandemic, which was when the labor market suffered most. The increase in real GDP of +2.2% in Q4:2022 ranked 26th in the country, resulting in an annual decline in economic output by -1.8% in 2022 which was the second worst in the country.  The BEA also reported that personal income in Louisiana grew at an annualized pace of +6.0% (ranked 32nd) in Q4:2022 (below +7.4% U.S. average). This resulted in personal income growth of 0.0% in 2022, ranking 50th of the states (see Figure 2).  The growth rate for 2022 was driven by the negative $10 billion (-4.0-percentage points) in transfer payments from a decline in safety net payments as the expanded child tax credit expired and more people found jobs but increases in net earnings by $8.4 billion (+3.4-percentage points) and other income by $1.6 billion (+0.6-percentage point). Personal income per person in Louisiana increased by 0.08% to $54,622 last year, which ranked 42nd in the country but the increase was far below inflation.

Bottom Line: More Louisianans gained jobs in April, but their pay hasn’t been keeping up with inflation in a stagnant economy. While the state improved its tax code in 2021, there was an irresponsible budget passed in 2023 which excessively grew spending, busted spending caps in FY23 and FY 24 and didn’t provide tax relief even with billions in excess tax revenue. Given these results, there is little reason to believe that there will be improvements in the state’s poor business tax climate, net outmigration of Louisianans, or the 19.6% poverty rate which ranks second highest in the country. Which pro-growth policies should be pursued instead? Refer to the Pelican Institute’s “Comeback Agenda” for policy recommendations that would turn the tide and provide opportunities for people to prosper. Originally published at Pelican Institute.  Oren Cass, founder of the think tank American Compass, presents a vision of the “new right” in his recently released book, Rebuilding American Capitalism. In it, he advocates for a top-down approach to governance in response to what he perceives as free-market failures.

He tends to believe that certain politicians can and should shape markets to achieve desired outcomes rather than letting free markets, which are free people, work. This attempt to rebrand not only the right but capitalism itself is flawed, as history and sound economics prove. Cass pinpoints growing concerns in the economy to help bolster his arguments, like poor inflation-adjusted wage growth and lack of strong social and family units. These are problems making it harder for people to prosper, but they are not, as he suggests, evidence that free-market capitalism has failed. But these problems–if they are problems, as Scott Winship and Jeremy Horpedahl recently found that people are thriving–aren’t the results of free markets but are driven instead by government failures. These failures include bloated government spending, restrictive regulations, high tax burdens, excessive safety net programs, costly tariffs, and other barriers to entry in the marketplace. They are imposed by politicians and government bureaucrats, hindering competition, disrupting entrepreneurial endeavors, impeding wage growth, and destroying human flourishing. Cass contends that capitalism only works under the right conditions, which must be facilitated by the government to keep the labor market and the economy strong. Rather than what he calls the “Old Right’s market fundamentalism” of fewer regulations and less government intervention being best, he welcomes more government with certain politicians in power. He proudly makes markets the scapegoat and, with it, globalization and financialization. In the book’s foreword, Cass writes: "Globalization must be replaced with a bounded market that restores the mutual dependence of American capital and labor and invites the trade and immigration that benefit American workers. Financialization must be reversed so that both talent and capital in pursuit of profit find their best opportunities in productive investment rather than extraction and speculation." Believing that more opportunities in the form of globalization inhibit rather than help Americans is the same faulty basis with which people discourage immigration and trade, which are central to thriving economies. But the crux of Cass’s theory is that he believes markets must be molded, even referring to work by the father of modern economics Adam Smith. Conveniently, he fails to cite the economist Frederick Hayek, who built on Smith’s ideas, to identify spontaneous order, the basis of free-market capitalism that argues economic growth and prosperity arise from voluntary transactions by free people, not government guidance and control. This “new right” idea was debunked long before Cass came along by Hayek (and others), who also highlighted the “knowledge problem” associated with central planning. He argued that no central authority can possess the information necessary to make efficient decisions for an entire economy. The complexity of economic interactions and the constant flux of information require decentralized decision-making and market mechanisms to aggregate and incorporate local knowledge effectively. Hayek’s insights emphasize the limitations of top-down control and the importance of allowing market forces and individual actors to shape economic outcomes based on their localized knowledge and preferences from the bottom-up. But Cass would have it that government is heralded as the keeper of knowledge and the arbiter of good decisions rather than encouraging freedom and liberty in individuals, i.e., the essence of capitalism. Capitalism allows individuals to pursue their economic aspirations and make decisions based on their knowledge and preferences through voluntary exchange within rules of the game set by limited government. Through this freedom, innovation, entrepreneurship, and competition thrive, leading to greater prosperity for all. History is full of successful economic transformations driven by leaders who championed limited government and free markets. Former President Calvin Coolidge cut government spending, cut taxes, and reduced the national debt, providing more paths for human flourishing. Likewise, former President Ronald Reagan cut taxes, tried to rein in government spending, and reduced regulations, unleashing economic growth and job creation. Both of them understood that cutting spending, reducing taxes, and removing excessive regulations create an environment where businesses thrive and workers can benefit. Their approaches embraced the power of individual freedom and self-determination, not top-down control that breeds the opposite. Oren Cass’s theory of the “new right” and its embrace of government fundamentalism misunderstands the principles of capitalism and human behavior. Top-down approaches, rooted in centralized control and regulation, do not lead to economic prosperity or personal freedom no matter who is in charge but do distort the efficient allocation of resources, undermine the adaptability of markets, and reduce opportunities to let people prosper. To achieve a thriving and prosperous economy, we must adhere to and strengthen the principles of free-market capitalism, which too much of our economy today is deprived of when considering healthcare, education, transportation, manufacturing, and the labor market. This should include embracing limited government, voluntary exchange, and individual freedom as the pillars of strong families, productive workers, and profitable employers. Economist Milton Friedman noted what this debate is about decades ago. “The problem of social organization is how to set up an arrangement under which greed will do the least harm; capitalism is that kind of a system.” And while “history suggests that capitalism is a necessary condition for political freedom,” it’s clearly “not a sufficient condition.” But capitalism is the best system yet that has supported economic prosperity and political freedom. The problem is that we have had too little free-market capitalism for people to thrive because of too much government. There’s no need for a “new right” of big-government progressive policies offered by Cass and others when free-market capitalism of the “old right” is too often missing in our lives. Originally published at Econlib. Today, I'm honored to be joined by Alex Nowrasteh, Director of Immigration Studies at Cato Institute's Center for Global Liberty and Prosperity. We discuss: 1) Immigration myths, including "immigrants steal jobs," and why that isn't true; 2) What data reveal about where today's immigrants are coming from, how their life improves upon moving to America, and how America is improved by immigrants, and 3) Need for immigration reform, why one day we'll tear down the Texas border wall, and more. You can watch this interview on YouTube or listen to it on Apple Podcast, Spotify, Google Podcast, or Anchor. Please share on social media, subscribe to your favorite platform and my newsletter, like it and leave a 5-star rating.

Larry and Glenda Legler think the state should be using much of its nearly $33 billion surplus to give Texans a break on their property taxes.

Larry Legler said, "The state's got an ungodly amount of money that they need to do something with." But after months of promises to do that, Republican leaders still can't agree on the way to provide relief. "That's what's getting frustrating." Governor Greg Abbott prefers ending the school maintenance and operations or "M&O" portion of your property taxes over ten years. That portion alone is about 42% of your property tax bill. To make that happen, the state would shift sales tax, other state revenues, and surplus money to pay for public schools. That would allow the state to gradually reduce the rate for M&O property taxes until they're eliminated altogether. Vance Ginn, a conservative economist and president of Ginn Economic Consulting, has pushed this idea for years. "It's the only way that you can get to $0 school district property taxes is by buying down those rates because that rate can go to zero which zero out of a hundred-dollar valuation for a home is $0. And so that is still $0, and you've eliminated that tax." But Lt. Gov. Dan Patrick and the Texas Senate have a different plan. While it uses more state revenues and less property taxes to pay for schools, it would also increase homestead exemptions for most homeowners from $40,000 to $100,000. And for homeowners over 65, it would raise homestead exemptions from $70,000 to $110,000. Patrick said it would provide nearly double the savings for homeowners than the Governor's plan. CBS News Texas asked Patrick earlier this week if he doesn't support eliminating the school property tax. He said, "You can't get there. You only have sales tax to prop up a state of 30 to 35 to 40 million people the next decade. What happens when we have a decline and sales taxes go down? You'll have no money to pay your bills. You can't be a one-legged horse." Ginn disagreed. "The Comptroller said we're going to have about $27 billion in the rainy-day Fund. The rainy-day fund is there to cover unforeseen revenue shortfalls which would be exactly this sort of situation." Abbott said 30 business and other groups support his plan. The Leglers said because they're seniors, they prefer the plan from Patrick and the Senate. "Everything's gone sky high and when people can't get the medications they need, which is not our case, but many people we know, or they can't afford groceries, a loaf of bread at the grocery store, we got a problem." Both the House and Senate have approved different legislation, and until they pass the same bill, the Governor cannot sign it into law. Abbott will speak Friday about this, and other issues related to the regular and special legislative sessions. Originally published by CBS Texas. Today, I'm honored to be joined by Amity Shlaes, who has written four NYT bestsellers, chairs the board of the Calvin Coolidge Presidential Foundation, is winner of the Manhattan Institute's Hayek Book Prize, and serves as a scholar at the King's College. We discuss:

You can watch this interview on YouTube or listen to it on Apple Podcast, Spotify, Google Podcast, or Anchor. Please share on social media, subscribe to your favorite platform and my newsletter, like it and leave a 5-star rating.

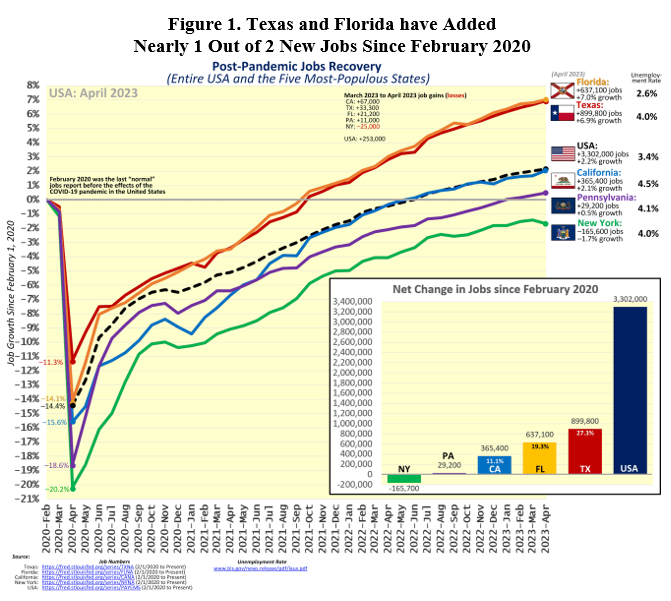

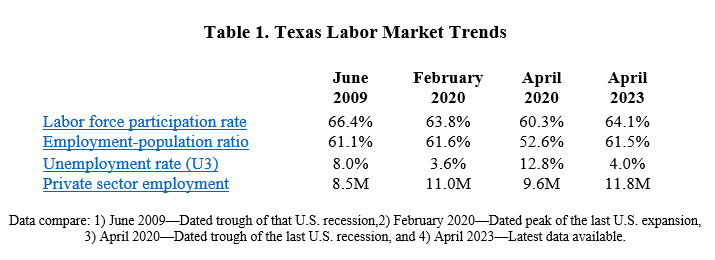

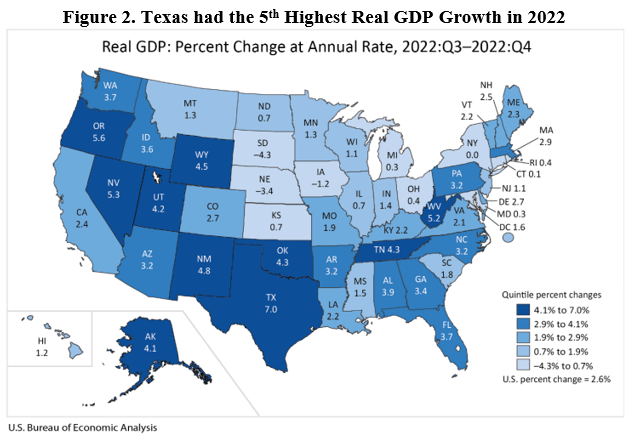

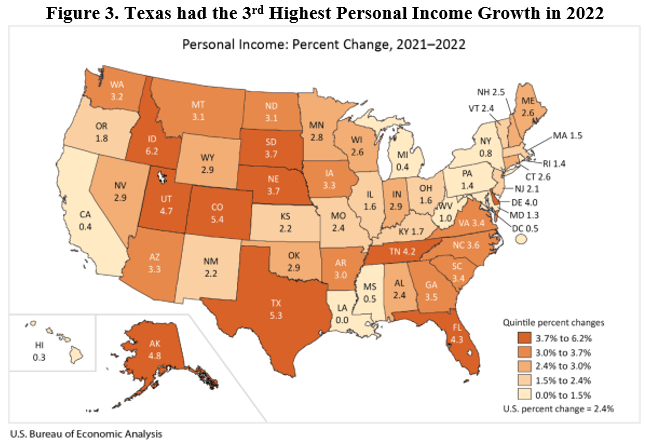

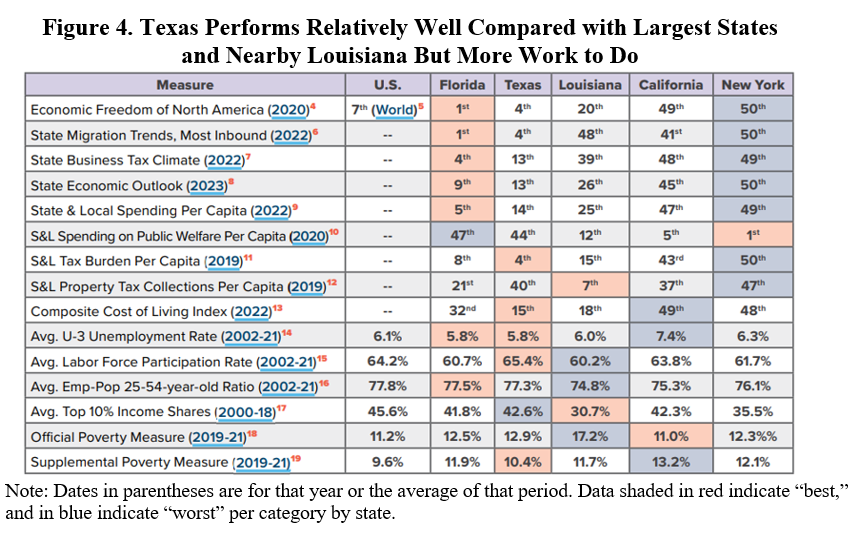

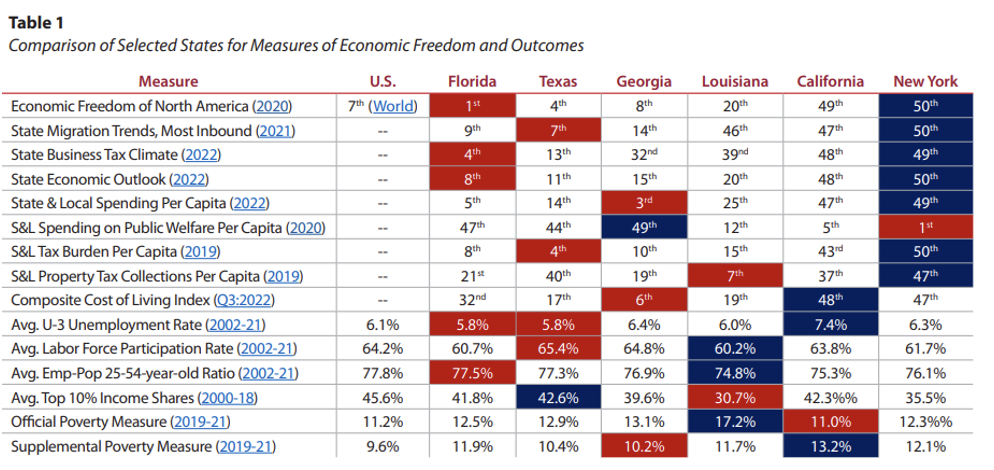

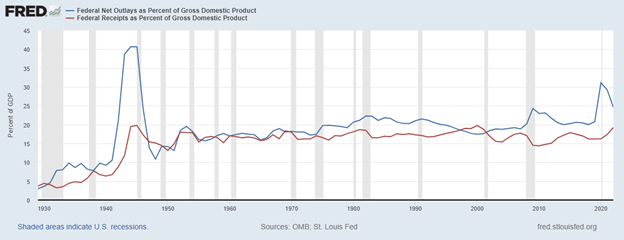

Key Point: Texas is a leader in job creation over the last year and since February 2020 (Figure 1 by @SoquelCreek). But Texas will struggle to compete with other states or prosper more as the 88th Legislature passed the largest budget increase in the state’s history, passed the largest corporate welfare increases in the state’s history, passed the largest safety net increases in the state’s history, didn’t pass property tax relief, and didn’t pass school choice. Governor Greg Abbott called a special session to tackle property tax relief and border security with more special sessions likely to come.  Overview: Texas has been a leader in the country’s economic recovery since the costly shutdown recession in Spring 2020. This includes reaching a new record high in total nonfarm employment for the 19th straight month. The current 88th Legislature ended the regular session on May 29 with a record surplus but chose to pass the largest spending and welfare increases in the state’s history without passing tax relief or school choice. This was a huge, missed opportunity for Texas that will set up a fiscal cliff with so much spending, less competition with fiscally conservative states, and less opportunity to let people prosper which combined will stop the Lone Star State from being a leader in the country. Fortunately, Governor Abbott called what is likely the first of multiple special sessions to tackle property tax relief (and border security). Labor Market: The best path to let people prosper is free-market capitalism as it is the best system that supports jobs and entrepreneurship for more people to earn a living, gain skills, and build social capital. Table 1 shows Texas’ labor market for April 2023.  The establishment survey shows net nonfarm jobs in Texas increased by 33,300 last month, resulting in increases for 35 of the last 36 months, to bring record-high employment to 13.8 million. Compared with a year ago, total employment was up by 534,600 (+4.0%)--second fastest growth rate in the country to Nevada (+4.2%)—with the private sector adding 476,800 jobs (+4.2%) and the government adding 57,800 jobs (+2.9%). The household survey shows that the labor force participation rate is higher and employment-population rate is slightly lower than in February 2020, but the former is well below June 2009 at the trough of the Great Recession. The state’s unemployment rate of 4.0% is higher than the U.S. rate of 3.4% but this is weak indicator as it’s highly volatile based on changes in the labor force. There is also continued declining inflation-adjusted average earnings in Texas. Economic Growth: The U.S. Bureau of Economic Analysis (BEA) reported the real gross domestic product (GDP) by state for 2022. Figure 2 shows Texas had the fifth fastest real GDP growth of +3.4% to $1.9 trillion (above the U.S. average of +2.1% to $20.0 trillion).  The BEA also reported that personal income in Texas grew by 5.3% to $1.9 trillion in 2022 which was the third highest in the country. This is behind Idaho (+6.2%) and Colorado (+5.4%) but well above the U.S. growth rate of 2.4% (to $21.8 trillion). Figure 3 shows personal income growth across the country.  Bottom Line: As Texans struggle from high inflation and high property taxes and an uncertain future with the U.S. economy likely in a deepening recession, they need substantial relief to help make ends meet. Other states are cutting, flattening, and phasing out taxes, passing responsible budgets, and passing school choice, so Texas must make bold reforms to support more opportunities to let people prosper, mitigate the affordability crisis, and withstand destructive policies out of D.C. Figure 4 provides a comparison of the size of government, economic freedom, and economic outcomes among the four largest states and nearby Louisiana. While Texas does relatively well, there is much more to do for more liberty and prosperity. Unfortunately, the Texas Legislature failed to achieve these needed policy objectives in the regular session of 2023 so Governor Greg Abbott is calling them back where the Legislature should spend less, provide more in property tax relief, pass school choice, and reduce or eliminate corporate welfare and expansions of safety net programs.  Free-Market Solutions: The Texas Legislature should improve the Texas Model by:

This Week's Economy Ep 10 | Is U.S. in Recession? Will TX Pass Largest Spending Increase in HISTORY?5/26/2023 Today, I cover: 1) National: What's the latest on the debt ceiling deal, why I believe that the U.S. is in a recession based on the latest GDP report, and how inflation continues to indicate more aggressive monetary tightening by the Fed; 2) State-Level Jobs: I break down the latest state-level jobs report and share reasons for optimism and more with a focus on Texas and Louisiana. 3) Texas: What's going on with the current Texas legislative session, and why the proposed budget increase would be the largest spending increase in TX history while not passing the largest property tax relief in history. Plus, massive increases in corporate welfare, and large increases in social safety net spending, which would result in a disaster for Texans and the Texas economy. You can watch this episode and others along with my Let People Prosper Show on YouTube or listen to it on Apple Podcast, Spotify, Google Podcast, or Anchor (please share, subscribe, like, and leave a 5-star rating!).

For show notes, thoughtful insights, media interviews, speeches, blog posts, research, and more, check out my website (https://www.vanceginn.com/) and please subscribe to my newsletter on Substack, share this post, and leave a comment. What REALLY Happens in the White House, Need Tax & Spending Reforms & More w Paul Winfree | Ep. 455/23/2023 Today, I'm honored to be joined by economist and trusted public policy adviser Paul Winfree, who has served in top management and policy roles in the White House, U.S. Senate, and think tanks. We discuss:

Paul Winfree is an economist and a trusted public policy advisor. He has served in top management and policy roles in the White House, the US Senate, and in think tanks.

This Week's Economy Ep 9 | New Debt Ceiling Bill, Importance of Reducing Taxes, Gov. Spending & More5/19/2023 Don't miss the 9th episode of "This Week's Economy,” where I briefly share insights every Friday on key economic and policy news across the country. Today I cover: 1) National: Breaking down the latest debt ceiling bill and the importance of restraining government spending for helping the economy to bounce back; 2) States: How states are setting an example of better spending habits with responsible budgeting and taxation in states like Florida and Iowa; and 3) Recession: Why I believe next year's data will show that we are in a recession that is set to deepen due to ongoing stagflation, and more. You can watch this episode and others along with my Let People Prosper Show on YouTube or listen to it on Apple Podcast, Spotify, Google Podcast, or Anchor (please share, subscribe, like, and leave a 5-star rating!).

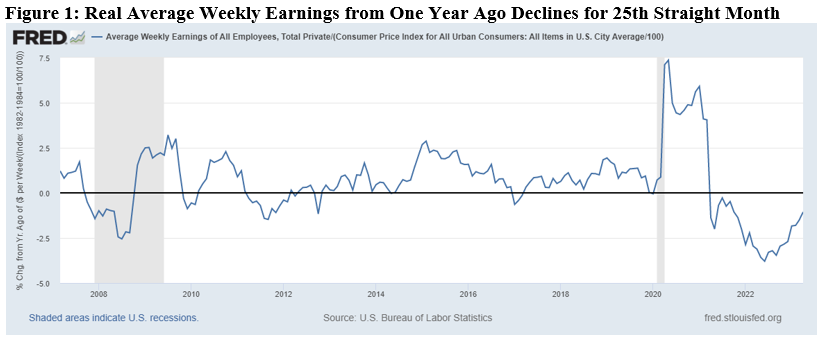

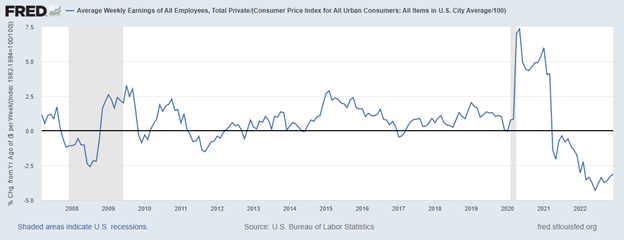

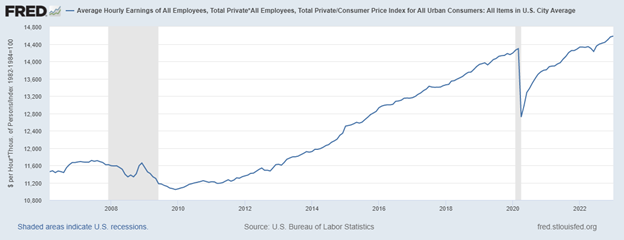

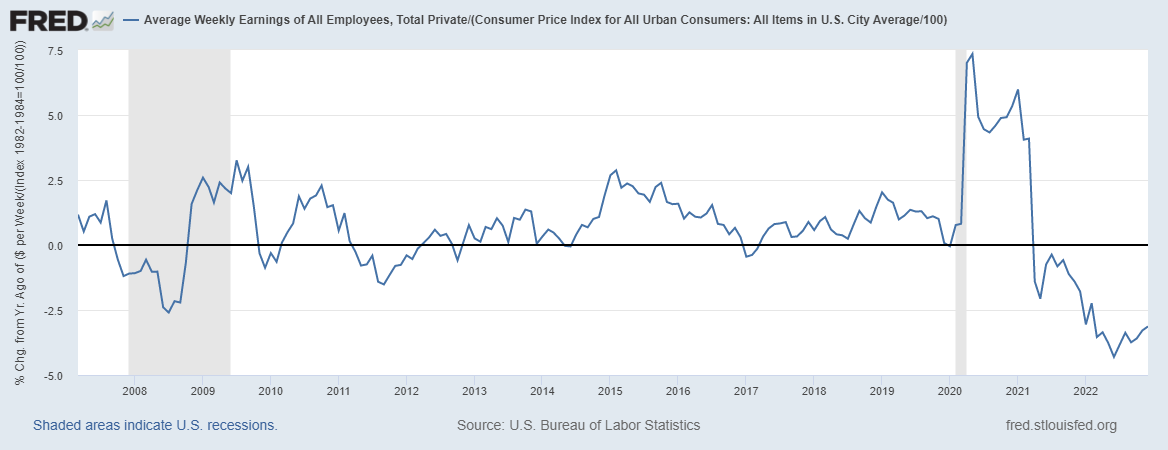

For show notes, thoughtful insights, media interviews, speeches, blog posts, research, and more, check out my website (https://www.vanceginn.com/) and please subscribe to my newsletter on Substack (vanceginn.substack.com/).  According to a recent CNBC survey, pessimism regarding the American economy is at an all-time high, with 69% of the public having a negative view. The leading reason is inflation in a weak economy. The latest report this week shows that inflation remains persistently high at near 5%, eroding slower-growing average weekly earnings year-over-year for 25 straight months.

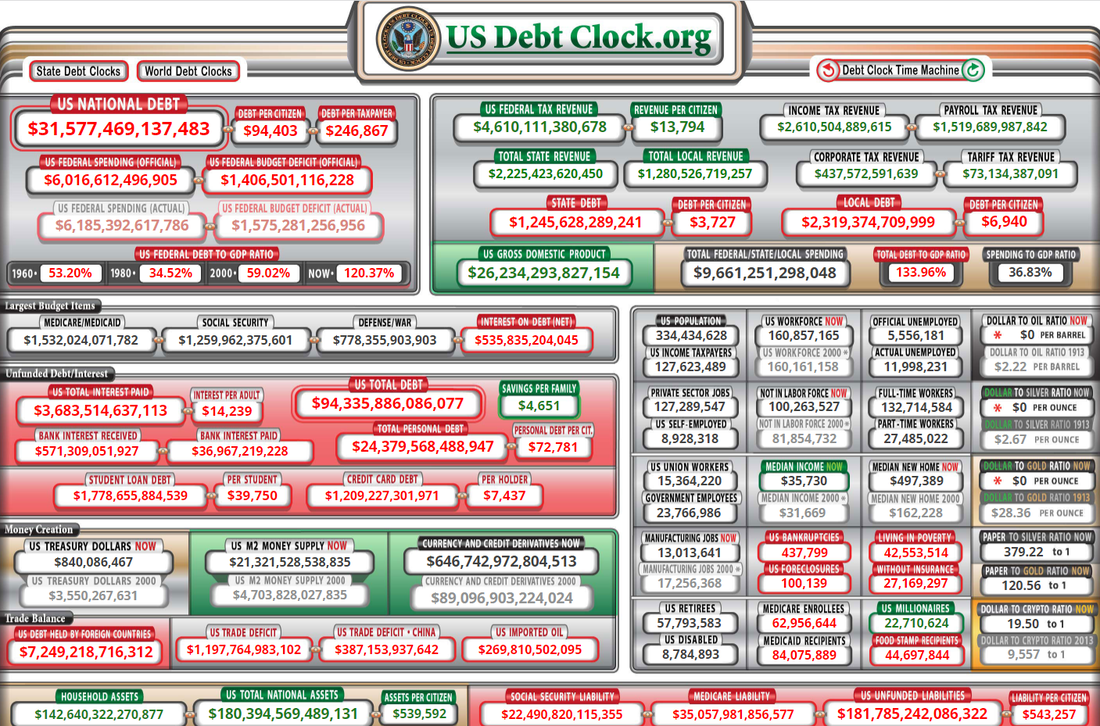

The Federal Reserve recently raised its federal funds rate target for the 10th meeting in a row to 5.25%–the highest since August 2007. While these rate hikes were anticipated in light of ongoing inflation, they could have been avoided. But excessive government spending and money printing during the “boom” led to this government-failure bust, the effects of which we’ll feel for months and even years to come. The sluggish economic growth has been rough on Americans, but inflation has been a killer. The survey also noted, “Just 5% say their household income is growing faster than inflation, 26% say it’s keeping pace, and 67% report they are falling behind.” This is devastating lower-income households’ standard of living. The trend of declining real wages is particularly harmful to low-income Americans. But even the wealthy feel the effects, as more than half of higher-income Americans surveyed report spending less on eating out and entertainment. This has contributed to the anemic annualized economic growth of just 1.1% in the first quarter of 2023 after rising by only 0.9% from the fourth quarter of 2021 to the fourth quarter of 2022. As prices increase, businesses spend more on production, making it more difficult to raise workers’ wages while remaining profitable. Employees who can’t be paid enough to fund costly goods like childcare and groceries, which have risen by 7.1% over the last year, spend less on other things or fall behind on their bills. Businesses earning less revenue will invest less, and so goes the vicious downward cycle. Another hit on Americans has been the cost of shelter, which was up 8.1% over the last year even as there are signs that housing prices are cooling across the country. Still, housing prices have been “eclipsing the inflation rate by 150% since 1970.” This means many Americans can’t afford to own a home, and that’s getting further out of reach as mortgage rates have soared. What’s to be done about inflation threatening Americans’ livelihoods? Legendary economist Milton Friedman had some advice about addressing sky-rocketing inflation that is valuable today. There is one and only one basic cause of inflation: too high a rate of growth in the quantity of money—too much money chasing the available supply of goods and services,” he argues. “These days, that cause is produced in Washington, proximately, by the Federal Reserve System, which determines what happens to the quantity of money; ultimately, by the political and other pressures impinging on the System, of which the most important are the pressures to create money in order to pay for exploding Federal spending and in order to promote the goal of ‘full employment.’ Despite raising its target interest rate to fight inflation, the Fed has a bloated balance sheet of nearly $9 trillion, which is too high for disinflation to its target of an average 2% rate. When the Fed engages in excessive money printing compared with the supply of goods and services, inflation is the result, as Friedman described. While it was appropriate for the Fed to raise its target rate, the ongoing increase to its balance sheet is just continuing to distort productive economic activity. And Congress must restrain spending. The national debt is nearly $31.5 trillion, with net interest payments on the debt set to exceed $1 trillion soon. The government must borrow to finance the deficit when it spends more than it makes, driving up interest rates. Higher interest rates increase the cost of borrowing for businesses, leading to lower investment, which reduces the supply of goods and services. Add in the Fed buying the debt that increases the money supply with less supply of goods and services, resulting in more inflation. House Republicans passed a debt ceiling bill that would return spending to 2022 levels and limit spending to just 1% growth over the next decade while eliminating other bad policies. Negotiations between the two parties continue, while a June 1 deadline looms. If they don’t reach agreement, it will make the debt issue an ongoing concern as defaulting on the debt nears, further raising interest rates that weaken the economy. This means we can expect a deeper, longer recession. The Fed and Congress have a duty to stop flawed policies of excessive printing and spending, respectively. High inflation harms Americans, and the Fed and Congress must address this. If they don’t take action soon to address these government failures, the erosion of the American dream will continue. The future of America depends on sound, pro-growth, pro-liberty policies instead that will let people prosper. Originally published at Econlib.  The U.S. dollar will likely soon lose its status as the global reserve currency. The dollar’s global reserve dominance has declined in recent years. As a result, international trade partners are hedging new connections. This will restructure the global economic order and create challenges ahead, especially for middle-class Americans.

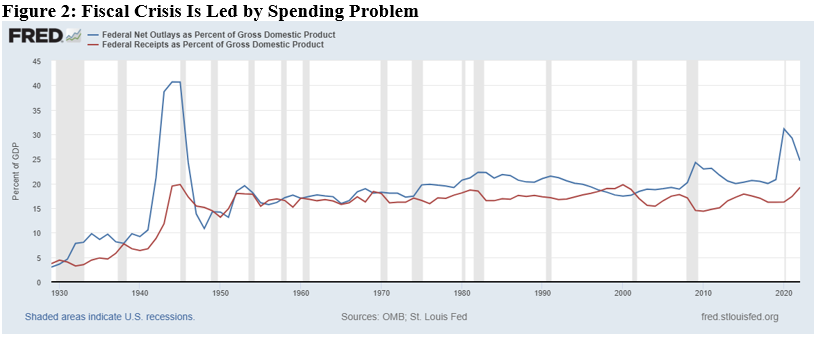

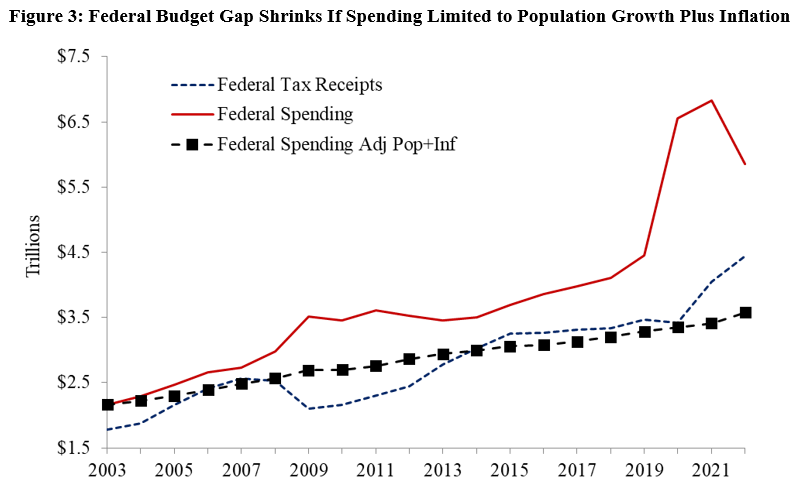

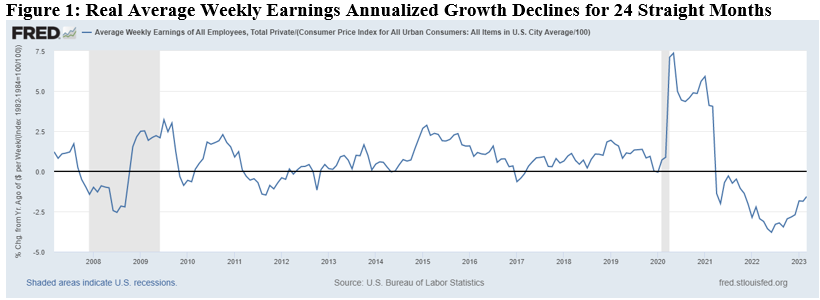

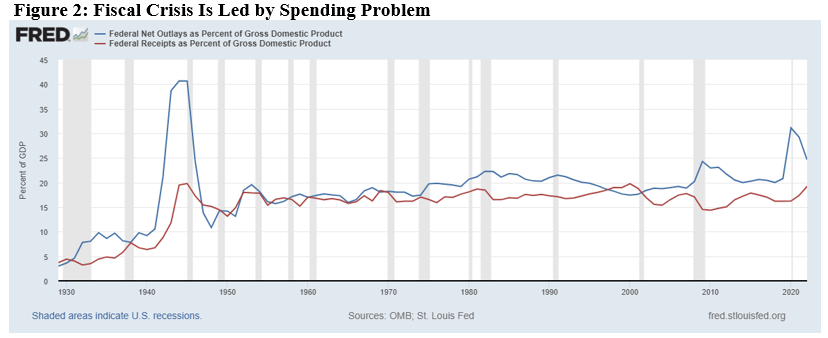

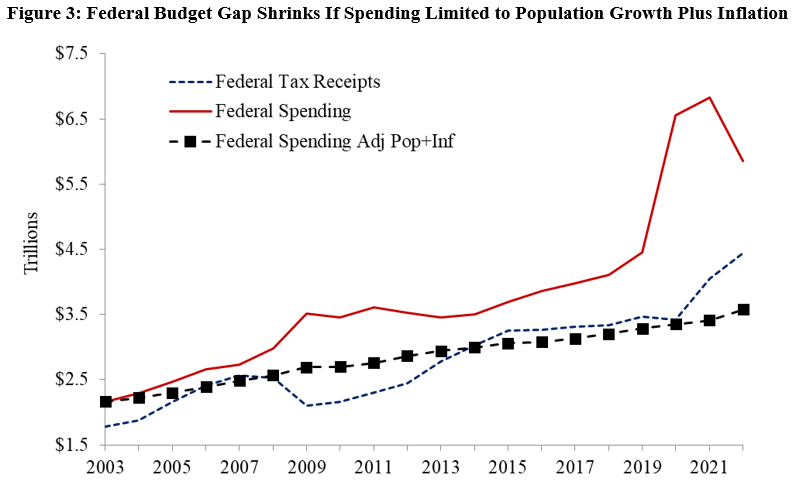

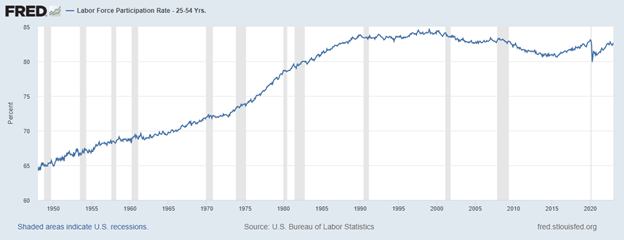

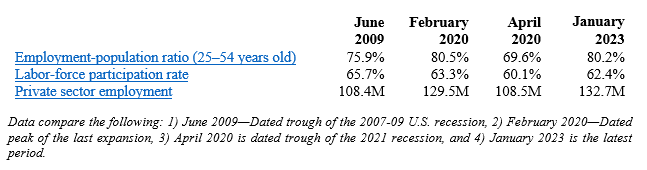

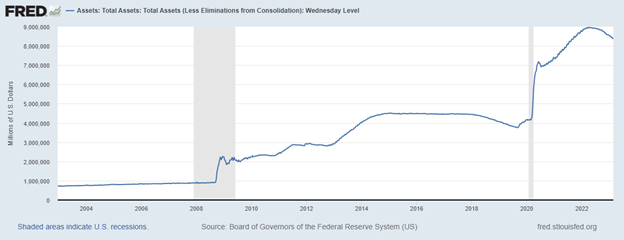

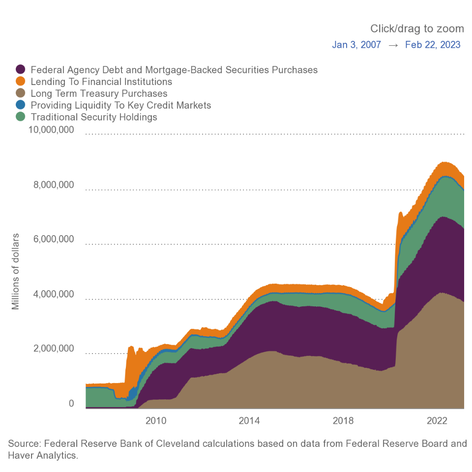

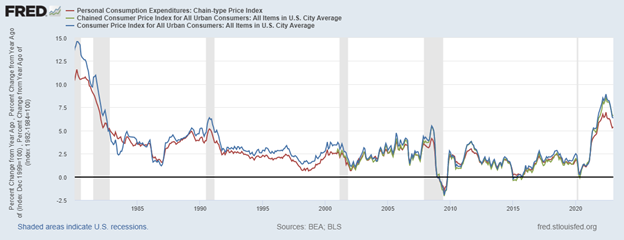

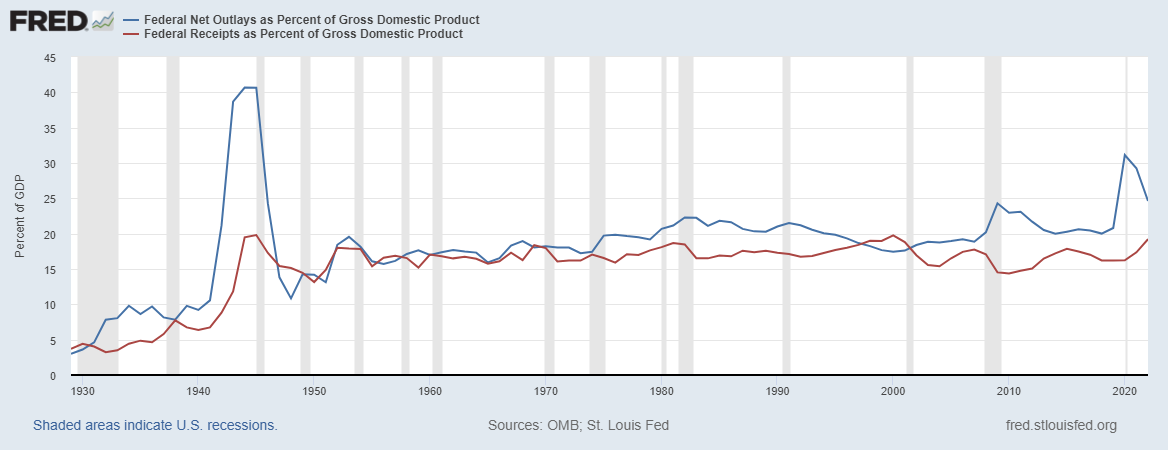

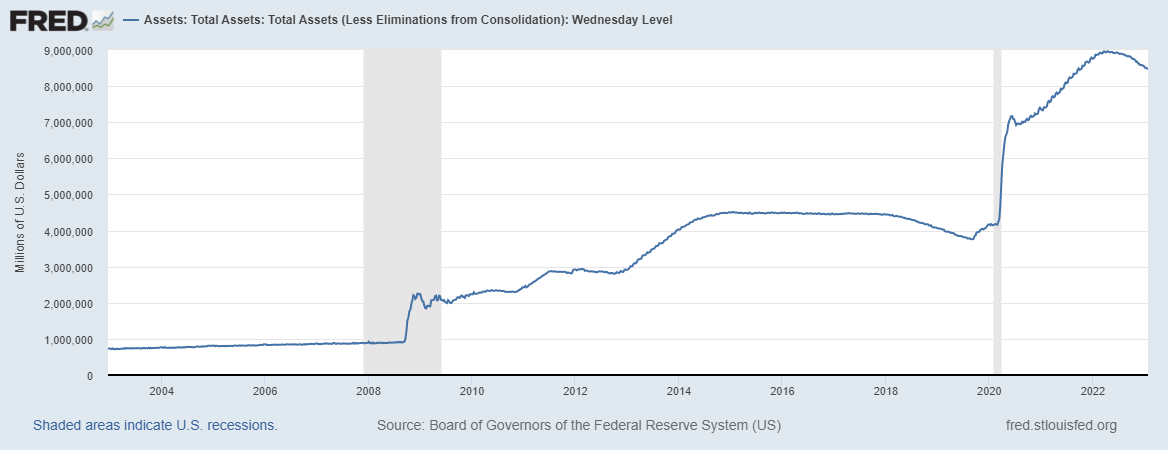

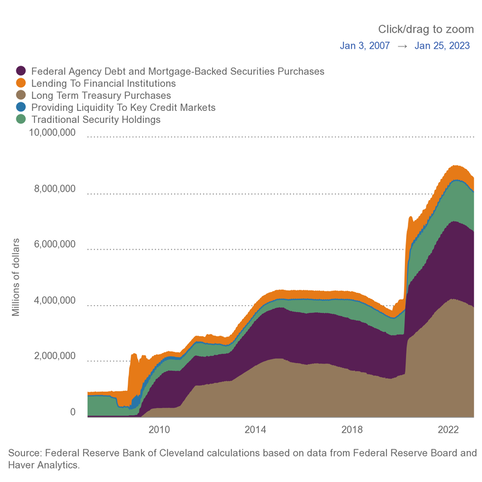

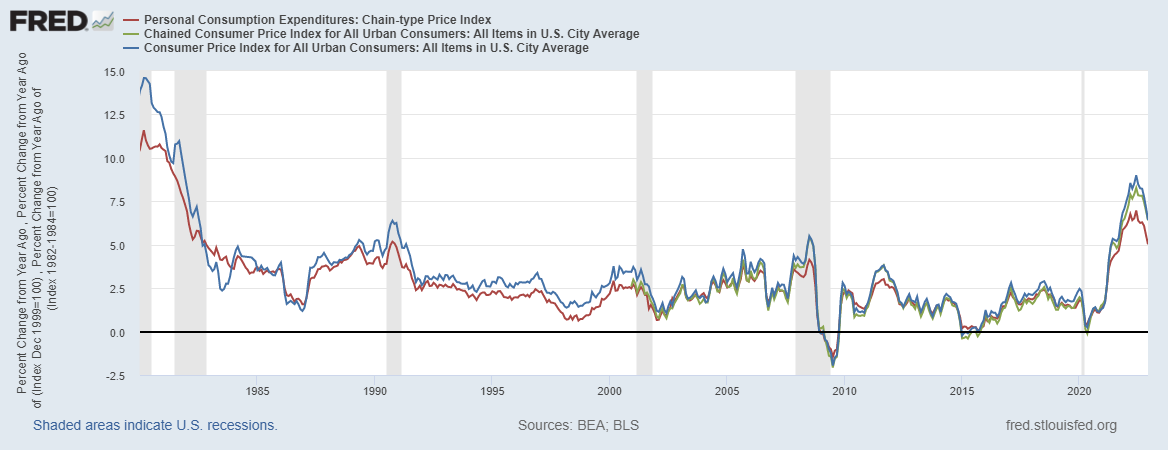

Americans should know what’s happening and how they can prepare for this possibility. But first, what does it mean to be the world’s global reserve currency, and why does it matter? The U.S. Dollar is the dominant global reserve currency. It’s widely accepted and is the preferred medium of exchange for international transactions. The dollar has enjoyed this status for the past 80 years due to its strong reputation acquired across a long history of America’s rising military prowess, fulfilling its financial obligations, and maintaining a strong economy. These institutional foundations of the dollar created high demand among foreign entities. One of the most important transactions utilizing the dollar is the purchase of oil. Oil is currently priced in dollars globally and other dollar-denominated assets. Losing or weakening the dollar’s position and value results in higher oil prices. The dollar’s elevated demand has helped keep its value high relative to other currencies. This prompted many countries to tie their currency directly to our dollar. The U.S. benefited by leveraging foreign demand for dollars into loans to the U.S. federal government. Foreign investors lend the U.S. high volumes of money because of the debt’s dollar denomination. The higher demand for U.S. Treasury securities pushes down domestic interest rates. This influences lower rates on mortgages and business loans, which help provide increased investment and economic growth. Losing or weakening the dollar’s reserve position will result in increased interest rates, decreased investment, and weak to negative economic growth. The dollar’s reserve status has also meant an increased volume of international trade. Ultimately, international trade helps keep interest rates and inflation moderately low. Losing or weakening the dollar’s reserve position will result in increased inflation. Trouble for the dollar is on the horizon. The once-givens about the dollar have come into question recently due prominently to excessive deficit spending. Foreign investors are reducing their demand for dollars as they diversify their portfolios. This combination contributed to the ballooning of the debt, depreciated the dollar, led to higher inflation and falling year-over-year real average weekly earnings for 25 straight months, and drove up interest rates, thereby slowing economic activity. Of course, this will have tradeoffs and many of them won’t be good. As mentioned, the major tradeoffs will be higher inflation and interest rates. The latter will trigger a move by the Federal Reserve to attempt to lower interest rates. But if its target rate is held below what markets dictate, the Fed will monetize the debt, increase the money supply, and drive inflation higher. The long-term result will be even higher interest rates to tame inflation. Unfortunately, the consequences of higher interest rates and inflation would be severe. People should expect higher mortgage rates than the already rising average rate of 6.4%. This is the highest in 15 years. Ultimately, higher interest rates would result in a steeper contraction in the housing market, exacerbate economic weakness, increase job losses, and worsen poverty. But maybe more importantly, it would likely crush middle-class Americans and the lifestyle that they’ve been accustomed to having for decades. The higher cost of shelter, food, gasoline, and energy as the dollar loses its reserve currency status would wreck havoc on their budgets and force major decisions about what’s best for their families. This could mean having to put off saving for college, going on vacations, and living in much smaller homes. All because our government couldn’t spend our money wisely. Therefore, the government should take serious steps to restore confidence in the dollar before a bad situation for Americans becomes worse or irreconcilable. To start, the federal government should reduce deficit spending. The long-term goal should be a balanced budget and an eventual start to paying down the debt. This will be pro-growth as the government stops redistributing taxpayer money from productive to unproductive activities. It will also strengthen the fiscal and economic situation of the U.S. The result will be an improvement in foreigners’ outlook on the dollar that would help preserve the dollar’s status. Dollar-focused policies should be tied to reducing the money in circulation. This should occur as the Federal Reserve reduces its balance sheet. Doing so tames inflationary pressures and could even result in some disinflation. This would allow the hard-earned dollars of Americans to go further than they do today. These policy improvements should be put into law with fiscal and monetary policy rules. The rules should remove the discretion of big-government spenders and printers. This would enable people’s livelihoods to get back on track and improve for generations. The potential loss of the dollar’s reserve currency status could have significant economic consequences, and there are even more than highlighted here. There is, however, reason for optimism: The U.S. economy is resilient and adapts well to challenges. But will those in D.C. allow for that to happen in the dynamic marketplace? Time will tell. But let’s hope so before it’s too late for middle-class Americans and everyone else to have the opportunity to fulfill their hopes and dreams. Originally published at The Daily Caller with Chuck Beauchamp, Ph.D. Key Point: The best way to let people prosper is free-market capitalism. Unfortunately, government has created a situation where inflation-adjusted average weekly earnings are down year-over-year for 25 straight months and economic growth is anemic.  Overview: Government failures drove the “shutdown recession” and stagflationary period over the last three years that has plagued Americans, with more banking problems to come. This is fueled by the debt ceiling fight and elevated inflation that has also rocked the U.S. dollar. The answer are pro-growth policies of less spending by Congress, less regulation by the Biden administration, and less money printing by the Fed. Labor Market: The Bureau of Labor Statistic recently released its U.S. jobs report for April 2023, which was another mixed report with some strengths but many weaknesses. The establishment survey is the most reported shows there were +253,000 (+2.6%) net nonfarm jobs added in April to 155.7 million employees, which has increased by +4.0 million over the last year but just +3.3 million since February 2020. However, there were cumulative revisions in the prior two months of 149,000, so on net for that reduced the net increase to just +104,000 jobs indicating a weakening labor market. Over the last month, there were +230,000 jobs (+2.7%) added in the private sector and +23,000 jobs (+2.1%) added in the government sector. Most of the private sector jobs were added in the sectors of private education and health services (+77,000), professional and business services (+43,000), and leisure and hospitality (+31,000), which these three also led over the last 12 months. But wholesale trade lost -2,200 jobs last month while no industry had job losses over the last year. The household survey increased by +139,000 jobs to 161.0 million employed in April. There have been declines in net employment in four of the last 13 months for a total increase of +3 million since April 2022 and +2.3 million since February 2020, which both are 1 million below the jobs reported in the establishment survey. This could be because of reporting issues or the number of jobs each person has in the market. The official U3 unemployment rate ticked down to 3.4% and the broader U6 underutilization rate fell to 6.6%, which both are near or at historic lows. Since February 2020, the prime-age (25-54 years old) employment-population ratio is up by 0.3pp to 80.8%, prime-age labor force participation rate was 0.3-percentage point higher at 83.3%, and the total labor-force participation rate was 0.7-percentage-point lower at 62.6% with millions of people out of the labor force holding the U3 rate artificially low. Given some improvements, challenges remain for Americans as inflation-adjusted average weekly earnings were down (-1.1%) over the last year for the 25th straight month. Economic Growth: The U.S. Bureau of Economic Analysis’ recently released the 1st estimate for economic output for Q1:2023. Table 1 provides data over time for real total gross domestic product (GDP), measured in chained 2012 dollars, and real private GDP, which excludes government consumption expenditures and gross investment. Most of the estimates for Q4:2022 and growth in 2022 have been revised lower, providing more evidence that 2022 was a very weak economy if not a recession.  Economic activity has had booms and busts since the government-imposed COVID-related restrictions in response to the pandemic and poor fiscal and monetary policies that severely hurt people’s ability to exchange and work. In 2022, the first two quarters had declines in real total (and private) GDP, providing a reason to date recessions every time since at least 1950. While the second half of 2022 looked better, those two quarters were influenced by net exports and inventories that would have made the economy much weaker. For 2022, real total GDP growth is reported +2.1% year-over-year but measured by Q4-over-Q4 the growth rate was only +0.9%, which was the slowest Q4-over-Q4 growth during a recover on record. Then the anemic growth of just +1.1% in Q1:2023 provides more reason that this is an extended recession or at least stagflation. The Atlanta Fed’s early GDPNow projection on May 8, 2023 for real total GDP growth in Q2:2023 was +2.7% based on the latest data available, but this rate has been lowered in recent quarters. Considering the last expansion from June 2009 to February 2020, there was slower real private GDP growth in the latter part of that period due to higher deficit-spending, contributing to crowding-out of the productive private sector. Congress’ excessive spending since February 2020 led to a massive increase in the national debt by nearly +$7.6 trillion that would have led to higher market interest rates. This is yet another example of how there is always an excessive government spending problem as noted in Figure 2 with federal spending and tax receipts as a share of GDP no matter if there are higher or lower tax rates.  But the Fed monetized much of the new debt to keep interest rates artificially lower thereby creating higher inflation as there has been too much money chasing too few goods and services as production has been overregulated and overtaxed and workers have been given too many handouts. The Fed’s balance sheet exploded from about $4 trillion, when it was already bloated after the Great Recession, to nearly $9 trillion and is down only about 5.2% to $8.5 trillion since the record high in April 2022 after rising nearly $400 billion in March 2023 then down $200 billion since then. The Fed will need to cut its balance sheet (total assets over time) more aggressively if it is to stop manipulating markets (see this for types of assets on its balance sheet) and persistently tame inflation, as we may need deflation which hasn’t happened since 2009 given the rampant inflation over the last two years. The current annual inflation rate of the consumer price index (CPI) has been cooling since a peak of +9.1% in June 2022 but remains elevated at +4.9% in April 2023, which remains the highest since 2008 as do other key measures of inflation. After adjusting total earnings in the private sector for CPI inflation, real total earnings are up by only +2.6% since February 2020 as the shutdown recession took a huge hit on total earnings and then higher inflation hindered increased purchasing power. Just as inflation is always and everywhere a monetary phenomenon, deficits and taxes are always and everywhere a spending problem. David Boaz at Cato Institute notes how this problem is from both Republicans and Democrats. In order to get control of this fiscal crisis which is contributing to a monetary crisis, the U.S. needs a fiscal rule like the Responsible American Budget (RAB) with a maximum spending limit based on the rate of population growth plus inflation. If Congress had followed this approach from 2003 to 2022, the figure below shows tax receipts, spending, and spending adjusted for only population growth plus chained-CPI inflation. Instead of an (updated) $19.0 trillion national debt increase, there could have been only a $500 billion debt increase for a $18.5 trillion swing in a positive direction that would have substantially reduced the cost of this debt to Americans. The Republican Study Committee recently noted the strength of this type of fiscal rule in its FY 2023 “Blueprint to Save America.” And to top this off, the Federal Reserve should follow a monetary rule so that the costly discretion stops creating booms and busts.  Bottom Line: Stagflation will continue with the a deeper recession this year given the “zombie economy” and the unraveling of the banking sector which will hit main street hard. Instead of passing massive spending bills, the path forward should include pro-growth policies that shrink government rather than big-government, progressive policies. It’s time for limited government with sound fiscal and monetary policy that provides more opportunities for people to work and have more paths out of poverty. There is some optimism with the House Republicans debt ceiling bill package, but it’s got an uphill battle to become law with Democrats in the Senate and White House so more must be done.

Recommendations:

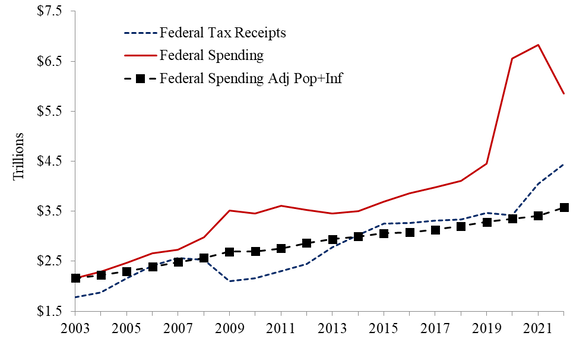

Key Point: Inflation-adjusted average weekly earnings year-over-year are down for 24 consecutive months and economic growth is anemic creating a stagflationary period at best or recessionary period at worst. The best way to let people prosper is free-market capitalism.  Overview: Government failures drove the “shutdown recession” and stagflationary period over the last three years that has plagued Americans, with more banking problems to come. This is fueled by the debt ceiling fight and likely elevate inflation for longer than many expected, with the only answers being less spending by Congress, less regulation by Biden administration, and less money printing by the Fed. The solution to these problems are pro-growth policies of shrinking government back to its constitutional roles. Labor Market: The Bureau of Labor Statistic recently released its U.S. jobs report for March 2023. The reports continue to be mixed with signs of strength though underlying weaknesses remain. The establishment survey shows there were +236,000 (+2.7%) net nonfarm jobs added in March to 155.6 million employees, which has increased by +4.1 million over the last year but just +3.2 million since February 2020 before the shutdowns. Over the last month, there were +189,000 jobs (+2.8%) added in the private sector and +47,000 jobs (+2.2%) added in the government sector. Most of the private sector jobs were added in the sectors of leisure (+72,000), private education and health services (+65,000), and professional and business services (+39,000), which the first two led over the last 12 months; retail trade (-14,600), construction (-9,000), manufacturing (-1,000), and financial activities (-1,000) had losses. Only retail trade (-15,200) declined over the last year. The household survey had another increase of +577,000 jobs to 160.9 million employed in March, which there have been declines in net employment in four of the last 12 months for a total increase of +2.6 million since March 2022 and +2.1 million since February 2020. The official U3 unemployment rate ticked down to 3.5% and the broader U6 underutilization rate fell to 6.7%. Since February 2020, the prime-age (25-54 years old) employment-population ratio is up by 0.2pp to 80.7%, prime-age labor force participation rate was 0.1-percentage point higher at 83.1%, and the total labor-force participation rate was 0.7-percentage-point lower at 62.6% with millions of people out of the labor force holding the U3 rate artificially low. Given some improvements, challenges remain for Americans as inflation-adjusted average weekly earnings were down -1.6% over the last year for the 24th straight month. Economic Growth: The U.S. Bureau of Economic Analysis’ recently released the 1st estimate for economic output for Q1:2023. Table 1 provides data over time for real total gross domestic product (GDP), measured in chained 2012 dollars, and real private GDP, which excludes government consumption expenditures and gross investment. Most of the estimates for Q4:2022 and growth in 2022 have been revised lower, providing more evidence that 2022 was a very weak economy if not a recession.  Economic activity has had booms and busts because of inappropriately imposed government COVID-related restrictions in response to the pandemic and poor fiscal and monetary policies that severely hurt people’s ability to exchange and work. In 2022, the first two quarters had declines in real total (and private) GDP, providing a reason to date recessions every time since at least 1950. While the second half of 2022 looked better, those two quarters were influenced by net exports and inventories that would have made the economy much weaker. For 2022, real total GDP growth is reported +2.1% year-over-year but measured by Q4-over-Q4 the growth rate was only +0.9%, which was the slowest Q4-over-Q4 growth during a recover on record. Then the anemic growth in Q1:2023 provides more reason that this is an extended recession or at least stagflation. The Atlanta Fed’s early GDPNow projection on April 28, 2023 for real total GDP growth in Q2:2023 was +1.7% based on the latest data available. If you consider the last expansion from June 2009 to February 2020, there was slower real private GDP growth in the latter period due to higher deficit-spending, contributing to crowding-out of the productive private sector. Congress’ excessive spending since February 2020 led to a massive increase in the national debt by nearly +$7.8 trillion that would have led to higher market interest rates. This is yet another example of how there is always an excessive government spending problem as noted in Figure 2 with federal spending and tax receipts as a share of GDP no matter if there are higher or lower tax rates.  But the Fed monetized much of the new debt to keep interest rates artificially lower thereby creating higher inflation as there has been too much money chasing too few goods and services as production has been overregulated and overtaxed and workers have been given too many handouts. The Fed’s balance sheet exploded from about $4 trillion, when it was already bloated after the Great Recession, to nearly $9 trillion and is down only about 3.5% since the record high in April 2022 after rising nearly $400 billion in March then down $180 billion in April 2023. The Fed will need to cut its balance sheet (total assets over time) more aggressively if it is to stop manipulating markets (see this for types of assets on its balance sheet) and persistently tame inflation, as may need deflation given the rampant inflation over the last two years. The resulting annual inflation measured by the consumer price index (CPI) has cooled some from the peak of +9.1% in June 2022 but remains at +5.0% in March 2023, which remains the highest since 2008 as do other key measures of inflation. After adjusting total earnings in the private sector for CPI inflation, real total earnings are up by only +2.3% since February 2020 as the shutdown recession took a huge hit on total earnings and then higher inflation hindered increased purchasing power. Just as inflation is always and everywhere a monetary phenomenon, deficits and taxes are always and everywhere a spending problem. David Boaz at Cato Institute notes how this problem is from both Republicans and Democrats. In order to get control of this fiscal crisis which is contributing to a monetary crisis, the U.S. needs a fiscal rule like the Responsible American Budget (RAB) with a maximum spending limit based on the rate of population growth plus inflation. If Congress had followed this approach from 2003 to 2022, the figure below shows tax receipts, spending, and spending adjusted for only population growth plus chained-CPI inflation. Instead of an (updated) $19.0 trillion national debt increase, there could have been only a $500 billion debt increase for a $18.5 trillion swing in a positive direction that would have substantially reduced the cost of this debt to Americans. The Republican Study Committee recently noted the strength of this type of fiscal rule in its FY 2023 “Blueprint to Save America.” And to top this off, the Federal Reserve should follow a monetary rule so that the costly discretion stops creating booms and busts.  Bottom Line: I expect stagflation will continue along with the a deeper recession this year given the “zombie economy” and the unraveling of the banking sector which will hit main street hard. Instead of passing massive spending bills, the path forward should include pro-growth policies that shrink government rather than big-government, progressive policies. It’s time for limited government with sound fiscal and monetary policy that provides more opportunities for people to work and have more paths out of poverty. There is some optimism with the House Republicans debt ceiling bill package but it’s got an uphill battle to become law with Democrats in the Senate and White House so more must be done.

Recommendations: · Set a pro-growth policy path with less spending, regulating, and taxing at all levels of government. · Reject new spending packages that America cannot afford nor needs; pass the RAB instead. · Impose strict monetary rule with the Fed having a much smaller balance sheet and a much higher federal funds rate target until we End the Fed. · Enact return-to-work policies. This Week's Economy Ep. 6: NEW GDP Report, Debt Ceiling Bill, School Choice & State Budgets4/28/2023 In today's episode of "This Week's Economy," I discuss the latest GDP report, the House Republicans passing a new debt ceiling bill, School Choice, state budgets, social media bans, and more. Thank you for listening to the 6th episode of "This Week's Economy,” where I briefly share my insights every Friday morning on key economic and policy news at the U.S. and state levels.

Today, I cover: 1) National: Findings from the latest GDP report released yesterday (April 27th) and the debt ceiling bill passed by House Republicans; 2) States: Updates on Universal School Choice and budgets across states, especially Texas and Louisiana; and 3) Other: Bills circulating on restricting social media, and more. You can watch this episode on YouTube or listen to it on Apple Podcast, Spotify, Google Podcast, or Anchor (please share, subscribe, like, and leave a 5-star rating). For show notes, thoughtful economic insights, media interviews, speeches, blog posts, research, and more at my Substack directly in your inbox.  J.P. Morgan CEO Jamie Dimon is making international headlines with his recent claim that the current U.S. banking crisis is “not yet over, and even when it is behind us, there will be repercussions from it for years to come.” With Congress’s ongoing excessive spending and the Federal Reserve’s continued monetary mischief, Dimon’s prediction seems pretty safe.

Following the collapse of Silicon Valley Bank (SVB), Signature Bank and Silvergate shut down shortly thereafter. Depositors with uninsured amounts above the Federal Deposit Insurance Corporation’s (FDIC) insured amount of $250,000 at both banks withdrew large sums, forcing the banks to sell assets that had lost significant value. Silvergate voluntarily liquidated itself, while bank regulators forcibly closed Signature Bank. While the specific circumstances of SVB’s collapse may be unique, the factors contributing to its failure are not. SVB, Signature, and countless other banks that have yet to make headlines invested in risky assets such as environmental, social, and governance (ESG) initiatives and less risky assets such as government securities. These actions were fueled by government interventions in the economy that pumped excess liquidity into the market, creating an artificial “boom.” Since early 2020, Congress has added more than $7 trillion to the national debt, and the Federal Reserve helped keep interest rates artificially low. This resulted in a flood of liquidity that found its way into the banking system, which led to banks taking on those less profitable investments, particularly interest-rate-sensitive government bonds. But banks weren’t prepared for the Fed to change its interest rate tune, raising its target for the federal funds rate from 0 percent to the latest range of 4.75 percent to 5 percent, and for those assets to lose significant value so quickly. This made these banks take a huge hit to their balance sheet when they marked-to-market those assets, and they didn’t have sufficient capital in a fractional reserve banking system to fund deposit withdrawals, hence bank runs. Now, we’re witnessing the beginnings of the inevitable bust that follows a prolonged “boom” fueled by government actions that just redistributed resources while distorting markets. Perhaps the worst part in all of this is that the Treasury, Fed, and FDIC are creating moral hazard for banks by insuring many deposits at big, “systemically important” banks. This has created a shift of deposits from smaller regional banks to bigger banks, given this guarantee for now. Therefore, there’s more reason for bigger banks to take on more risks with this backstop and flood of new deposits at the expense of smaller banks and the economy. To make matters worst, the Fed recently added even more liquidity to the market. After reducing its balance sheet by about $700 billion from its peak of $9 trillion in April 2022, the Fed added $400 billion to provide loans to financial institutions. Its balance sheet is now down about $100 billion since then to $8.6 trillion, or only 4.4 percent below its record high last year, when it should be down substantially more to get ahold of inflation. The Fed’s balance sheet provides a good indicator of inflation, which has started to improve, but including the aberrations in the Fed’s balance sheet and underlying inflationary indicators in the food and services sectors, inflation could easily stay elevated at a much higher rate than the Fed’s preferred 2 percent average for much longer. Adding to the pressure on the banking sector includes how the Atlanta Fed’s GDPNow estimate for inflation-adjusted GDP in the first quarter of 2023 is only 2.5 percent (and Blue Chip consensus estimate is 1.5 percent) as of April 14. This is after less than 1 percent growth from the fourth quarter of 2021 to the fourth quarter of 2022, which is the slowest growth during a year of recovery in decades. This will exacerbate problems at banks if Americans can’t pay their bills. And we’re likely to see even higher interest rates soon, even though the Fed expects to raise rates just one more time this year. Based on the well-respected Taylor rule, which calculates a federal funds rate target based on inflation and output gaps, the Cleveland Fed’s Taylor rule utility suggests at least a 6 percent federal funds rate target. This would further devalue the government securities on banks’ balance sheets. So strap up, Americans, as we’re in for a bumpy ride in the banking sector and overall economy. Only by allowing people to exchange freely with limited government interference that simply sets the rules of the game but is a referee thereafter, not a participant, can we better avoid these boom and bust cycles in the banking sector and across the economy that threaten our freedom and prosperity. A big part of this will be to unleash the banking sector from excessive regulations like those imposed by Dodd-Frank after the financial crisis. There should also be an effort to not increase the FDIC’s insured amount by $250,000, as depositors should also take losses if they’re not doing their due diligence to research where they deposit their funds. And there should be support for increasing capital requirements by banks in the marketplace rather than policy avoiding some of the problems with fractional reserve banking. Finally, the Fed should be led by a monetary rule, like the Taylor rule, and Congress by a fiscal rule, like the Responsible American Budget, to remove the discretion that plagues our economic activity and future. If not, there will be many more “booms” and busts and many more failures from government actions over time. We must let free people succeed and fail, as failure is essential for us to learn lessons, or we will keep making the same mistakes. But we should be eliminating government failures by ultimately shrinking government and ending the Fed. Originally published at Econlib. In Let People Prosper episode #40, I talk with Max Gulker, Ph.D., about whether Big Tech is a monopoly, FTC's overreach with regulations, & benefits of network effects to let people prosper. On today's episode of the "Let People Prosper" show, which was recorded on March 21, 2023, I'm thankful to be joined by Dr. Max Gulker, Senior Policy Analyst at Reason Foundation.

We discuss:

Dr. Gulker’s bio and other info (here):

David is joined by former Trump-era OMB economist, Dr. Vance Ginn, to discuss the history of economic thought; the strengths and weaknesses of the classical, Chicago, and Austrian schools of thought; whether or not we need a Fed; and what to do about excess debt and economic growth. Yes, it is a busy hour, but one you will not want to miss!

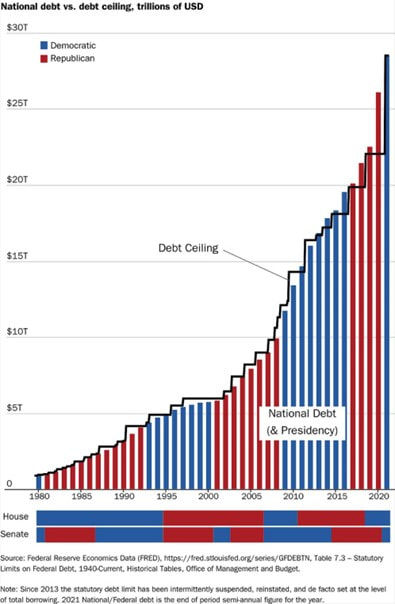

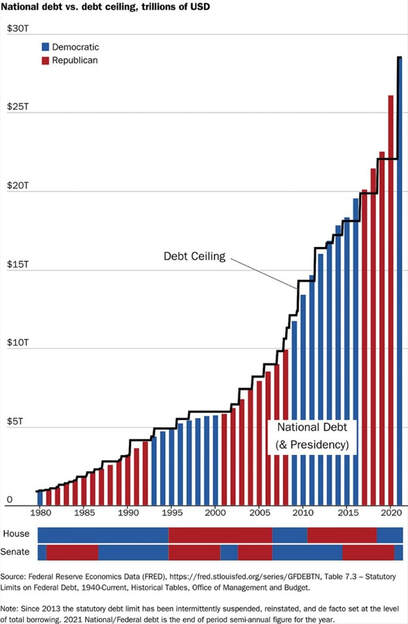

The debt ceiling standoff between President Biden and the Republican-controlled US House of Representatives indicates Republicans care about government spending and deficits again, allegedly.

But history tells a different story. Since 1980, the national debt has risen substantially each year, regardless of whether the presidency, House, or Senate was red or blue. In my recent interview with financial expert David Bahnsen, he said, “[Conservatives] are losing their moral credibility…we can’t only be fiscal conservatives when there’s a Democrat in the White House.” Proving Bahnsen’s point, two-thirds of the national debt was added just since 2009: $9.3 trillion during President Obama’s eight years, $7.8 trillion over President Trump’s four years (more than half of which was added during the COVID-19 pandemic and related shutdowns), and already $3.7 trillion in President Biden’s two years, with much more to come. During the Obama and Trump terms, both Republicans or Democrats controlled Congress. Neither put the breaks on borrowing. Spending restraint is necessary. Spending less would help avoid default on the debt, and help reduce expected massive deficits. If deficits continue to accelerate, as the Congressional Budget Office projects with a current policy baseline, the Federal Reserve will, at some point, be forced to monetize this new debt at such a scale that the post-pandemic inflation will seem mild by comparison. Moreover, higher deficits and interest rates will result in higher net interest payments, which will soon surpass $1 trillion per year, thereby crowding out Congressional budgets and likely necessitate more spending, taxes, and inflation. In early 2021, inflation escalated quickly after President Biden and Democrats passed the $2 trillion American Rescue Plan Act, handing out additional, unnecessary, blanket tax rebates and ratcheting up payouts to state and local governments and wasteful programs. And then there were the other costly legislative offerings of the “infrastructure” bill: the CHIPS Act, and the (inappropriately named) Inflation Reduction Act. Then, much of this substantial new debt generated by more than $7 trillion in excessive spending since early 2020 was purchased by the Fed, more than doubling the monetary base. Burdensome regulations imposed by the Biden administration, particularly on oil and gas production, along with tax hikes, resulted in a 40-year-high inflation rate and the slowest year of economic growth during a recovery in decades. The monetary base has finally started declining – down 6.5 percent since its peak of nearly $9 trillion in April 2022–and inflation has come down slightly but remains persistently high at 6.4 percent. Despite President Biden’s claims in his recent State of the Union address, deficits under his administration have remained near historic highs. While it’s true that the deficit has declined, it remains well above $1 trillion, and the decline was from expiring pandemic relief measures. The Congressional Budget Office finds the deficit will remain elevated well above $1 trillion and “averages $2 trillion per year from 2024 to 2033.” That’s far from balancing the budget or, better yet, achieving a surplus that could reduce the national debt, a feat achieved in only 6 years since 1940 (1947, 1948, 1951, 1956, 1957, and 1969). And it hasn’t been sustained in a century, since Presidents William Harding then Calvin Coolidge effectively restrained government spending. Cutting total spending is necessary. But trimming discretionary spending alone is not enough, as that will only temporarily address America’s fiscal crisis. To get out of this national crisis, we need perpetual spending restraint, like that championed by President Coolidge, which will require key reforms to “mandatory” programs like Social Security and Medicare. While a balanced budget amendment sounds good (and would be much better than our lack of a fiscal rule at the federal level today) it would likely result in rising taxes, which would be detrimental to growth and deficit-reduction efforts. A federal spending limit tackles the ultimate burden of government: spending. This principle works at the state level in places like Texas, where the Legislature has held the budget in check over the last decade, contributing to a $32.7 billion surplus that could provide historic tax relief. Other state think tanks are weighing this responsible-budgeting approach, limiting spending to a maximum rate of population growth plus inflation. This rate is too high now, but typically provides a stable metric that reasonably accounts for the average taxpayer’s ability to pay for government spending while growing less than the economy. Instituting a federal spending limit would encourage Congress to narrow its scope to constitutional duties. This could be done with the Responsible American Budget, which has been supported by economists, politicians, and thought leaders, by limiting federal budget growth to correspond with population growth plus inflation. This approach would help remove failed programs from our lives, while allowing for more free-market capitalism to support human flourishing. Had this limit been followed over the past 20 years, the US could have added just $500 billion to the national debt on a static basis, instead of the $19 trillion we got. The more likely result would have been paying down the debt, given the dynamic effects of such a pro-growth policy. While House Republicans are trying to restrain spending for the moment, both sides of the political aisle need to encourage a bigger shift that embraces spending limits and pro-growth policies. We must cut government spending. The negotiations around raising the debt ceiling should be that opportunity to provide fiscal sanity. If not, we will have more costly consequences that Americans can’t afford. Originally published at American Institute for Economic Research.

In 2021, a bipartisan coalition ended school property tax abatements for corporations and renewable energy companies. On this week’s Liberty Cafe, Vance Ginn and Tim Hardin join me to discuss how Big Government Texas Republicans are attempting to restore this program for their friends in Big Business.

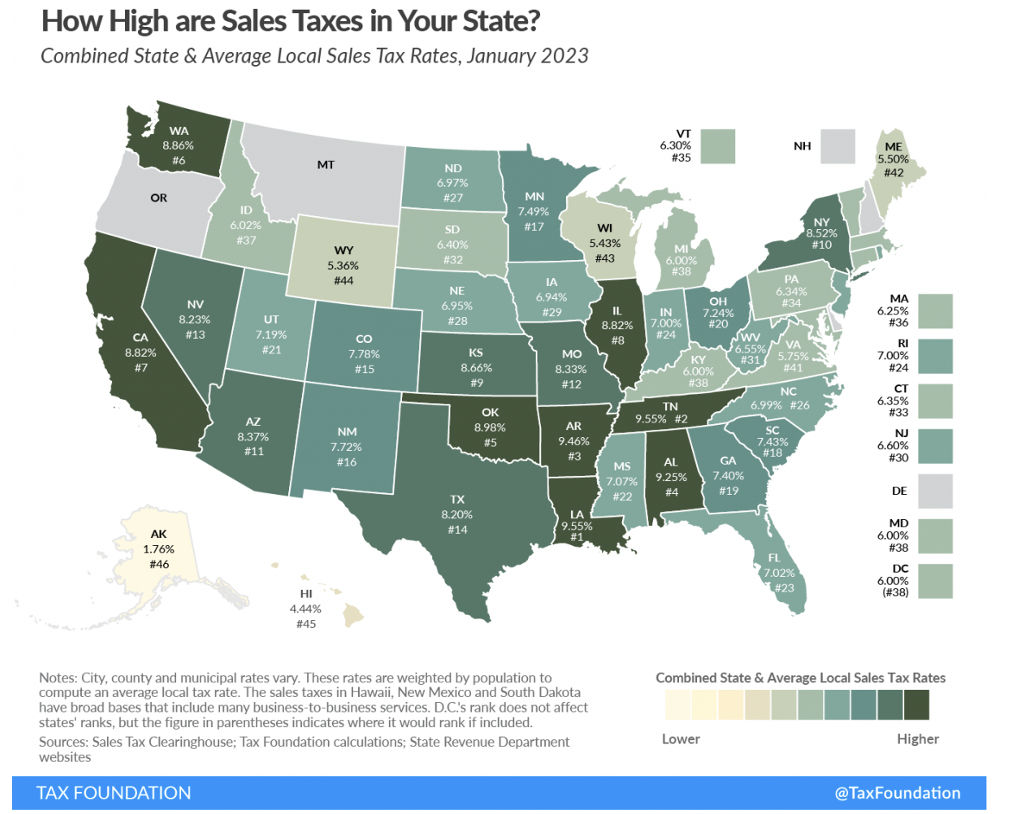

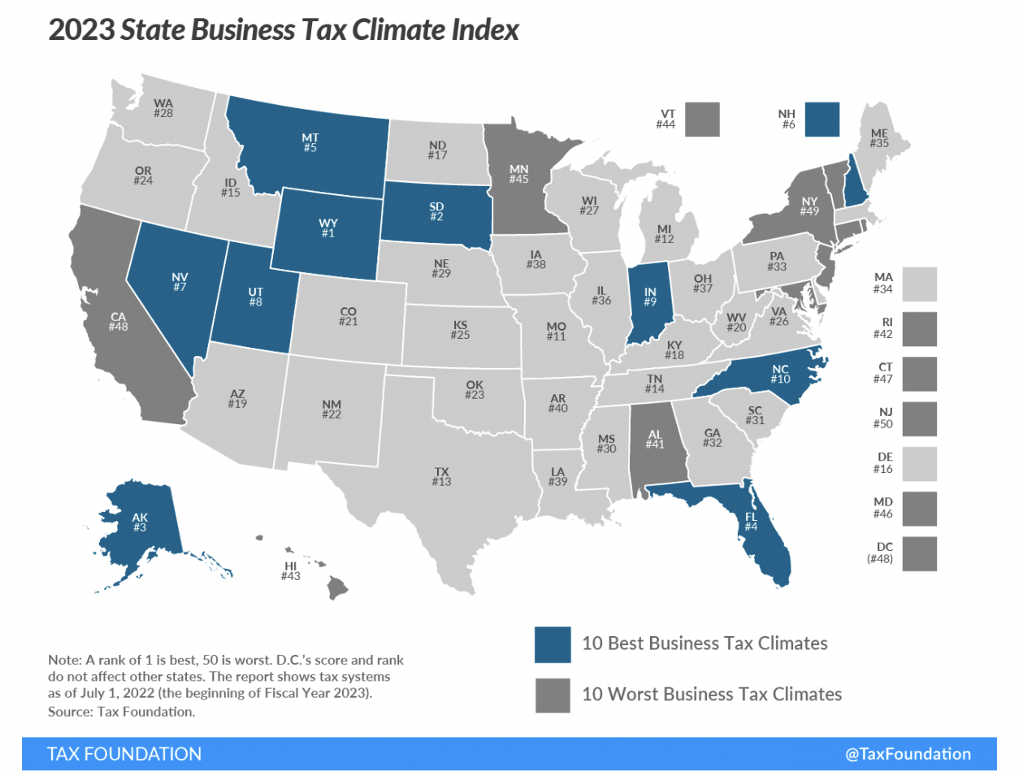

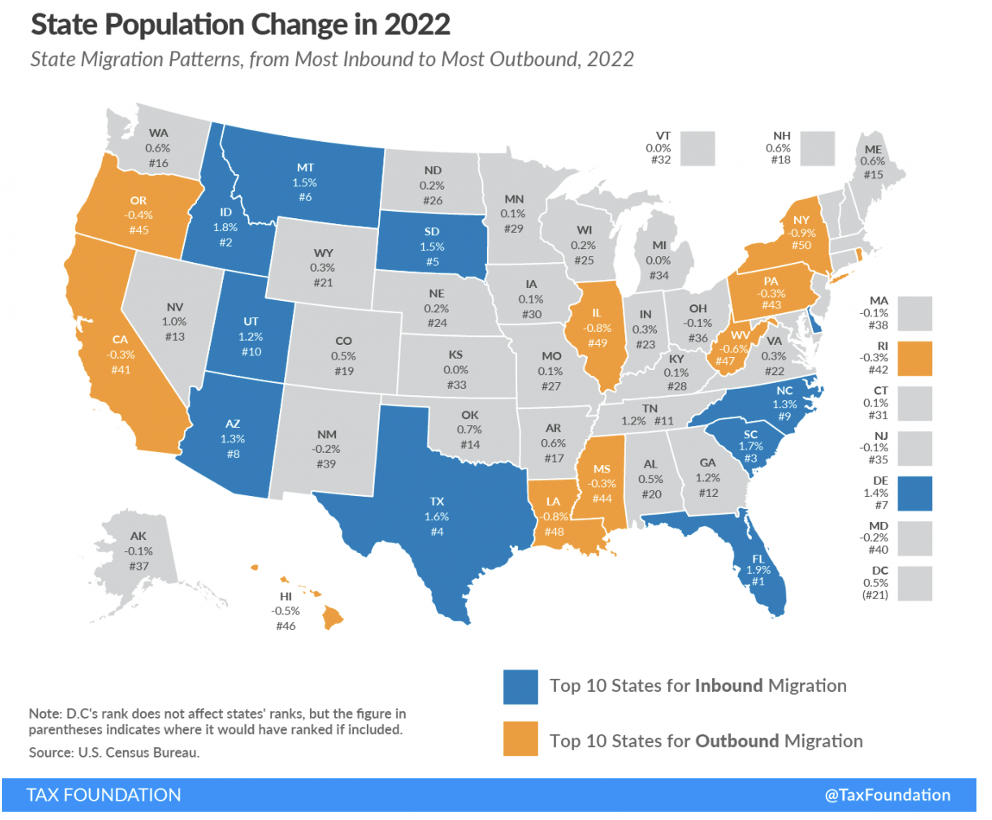

Recent data from the Tax Foundation reveals that Louisiana has the highest average combined state and local sales tax rate of all the states. The bulk of this burden comes from its local taxes, the second highest in the nation.  Pair these findings with Louisiana’s progressive income taxes of a graduated personal income tax rate of up to 4.25% and a corporate income tax rate max of 7.50%, and there’s no wonder why the Pelican State has a net out-migration problem. According to the Tax Foundation’s business tax climate index, the state ranks 12th worst in the country.  Personal income taxes disincentivize work, and sales taxes can lead consumers to shop elsewhere and businesses to relocate. Employers and consumers want to be where they can keep more of what they earn, which helps explain why Florida, a state with no personal income taxes and a combined sales and local tax rate that’s more than 2.5-percentage points lower than Louisiana’s, had the highest net in-migration last year.  Clearly, Louisiana’s tax code needs an overhaul if the growth and flourishing of Louisianans are priorities. But so does the state’s spending. To start, the Pelican State could consider joining the 14 states in the flat-income tax revolution. As more states flatten or remove their personal income taxes, Louisiana’s costly progressive income taxes will become much less appealing. Moving to flat personal and corporate income taxes would be a pro-growth step forward toward the eventual greater goal of eliminating these costly taxes, helping to compete with places like Florida and Texas, both of which don’t have personal income or corporate income taxes. Considering that the ultimate burden of government is how much it spends, reforming the tax code is just one piece of the puzzle. The excessive government spending at the state and local levels, compared with reasonable metrics like the rate of population growth plus inflation which helps measure the average taxpayer’s ability to pay for government spending, burdens Louisianans. Furthermore, Louisiana’s state and local debt is estimated to be about $7,600 per person owed by 2027, plus another nearly $28,000 per person owed in unfunded liabilities over time, so there are clearly massive barriers in the way for Louisianans to flourish. This is an issue because heavy spending leads to heavy burdens on state residents and decreased economic freedom, which Louisiana can’t afford to lose more of, considering how far it falls behind other states.  Not surprisingly, Georgia, Florida, and Texas all boast lower spending than Louisiana, with improved economic freedom and poverty rates. Meanwhile, Louisiana has the highest official poverty rate in the country. The rankings for the Pelican State aren’t quite as bad as the highly progressive states of New York and California, which are hemorrhaging population to other states. Incentives matter, so people are voting with their feet to flee high cost, low freedom states.