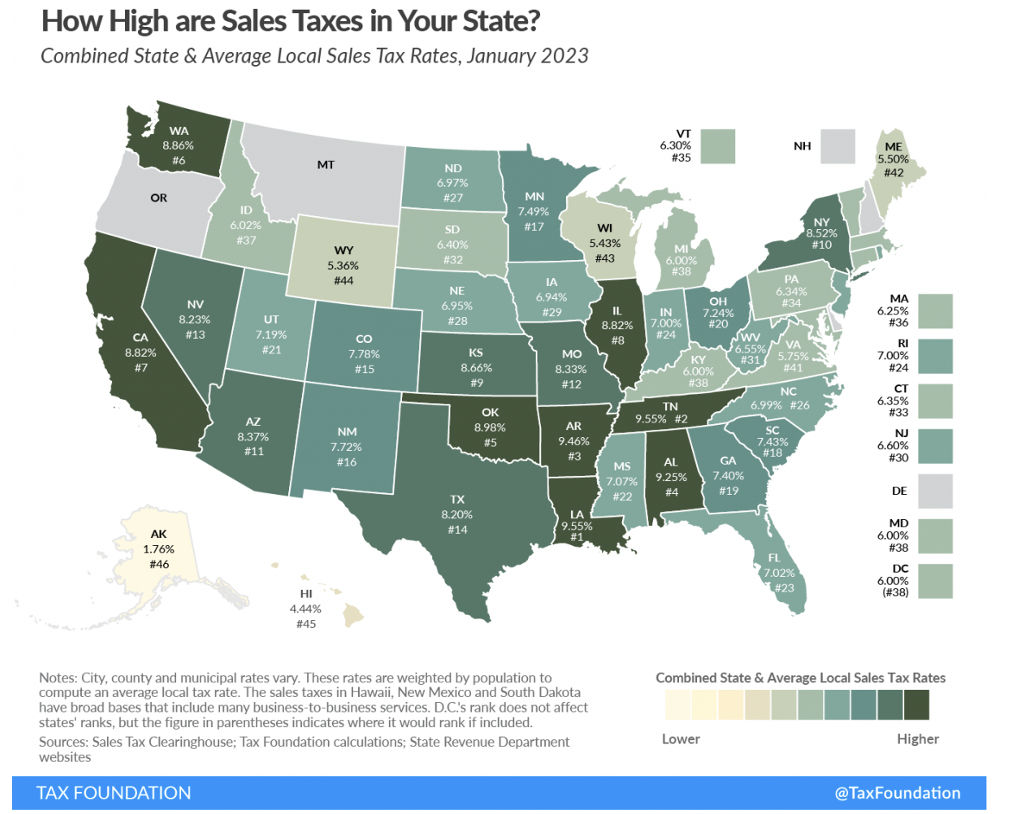

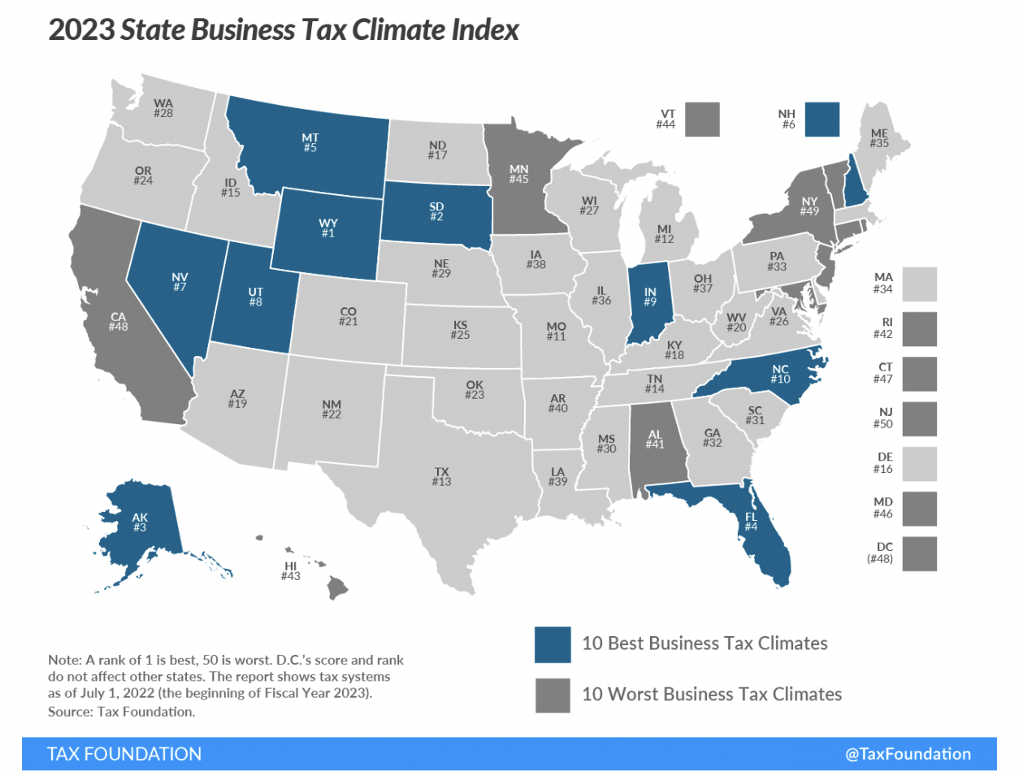

Recent data from the Tax Foundation reveals that Louisiana has the highest average combined state and local sales tax rate of all the states. The bulk of this burden comes from its local taxes, the second highest in the nation.  Pair these findings with Louisiana’s progressive income taxes of a graduated personal income tax rate of up to 4.25% and a corporate income tax rate max of 7.50%, and there’s no wonder why the Pelican State has a net out-migration problem. According to the Tax Foundation’s business tax climate index, the state ranks 12th worst in the country.  Personal income taxes disincentivize work, and sales taxes can lead consumers to shop elsewhere and businesses to relocate. Employers and consumers want to be where they can keep more of what they earn, which helps explain why Florida, a state with no personal income taxes and a combined sales and local tax rate that’s more than 2.5-percentage points lower than Louisiana’s, had the highest net in-migration last year.  Clearly, Louisiana’s tax code needs an overhaul if the growth and flourishing of Louisianans are priorities. But so does the state’s spending. To start, the Pelican State could consider joining the 14 states in the flat-income tax revolution. As more states flatten or remove their personal income taxes, Louisiana’s costly progressive income taxes will become much less appealing. Moving to flat personal and corporate income taxes would be a pro-growth step forward toward the eventual greater goal of eliminating these costly taxes, helping to compete with places like Florida and Texas, both of which don’t have personal income or corporate income taxes. Considering that the ultimate burden of government is how much it spends, reforming the tax code is just one piece of the puzzle. The excessive government spending at the state and local levels, compared with reasonable metrics like the rate of population growth plus inflation which helps measure the average taxpayer’s ability to pay for government spending, burdens Louisianans. Furthermore, Louisiana’s state and local debt is estimated to be about $7,600 per person owed by 2027, plus another nearly $28,000 per person owed in unfunded liabilities over time, so there are clearly massive barriers in the way for Louisianans to flourish. This is an issue because heavy spending leads to heavy burdens on state residents and decreased economic freedom, which Louisiana can’t afford to lose more of, considering how far it falls behind other states.  Not surprisingly, Georgia, Florida, and Texas all boast lower spending than Louisiana, with improved economic freedom and poverty rates. Meanwhile, Louisiana has the highest official poverty rate in the country. The rankings for the Pelican State aren’t quite as bad as the highly progressive states of New York and California, which are hemorrhaging population to other states. Incentives matter, so people are voting with their feet to flee high cost, low freedom states.

Louisiana should start its comeback story by adopting a stronger spending limit, similar to the one recently passed in Texas. Spending caps help governments stay limited, which is imperative for states to thrive as it forces them to narrow their scope. In turn, the private sector has more elbow room to grow and people have greater ability to prosper. This would also help provide more surplus funds to put toward cutting, flattening, and eventually eliminating personal and corporate income taxes. Louisiana has too great of a culture and too much potential for it to be squandered by burdensome spending and taxes. It’s time for serious spending restraint and major tax reforms to provide the best path forward. Originally published at Pelican Institute.

0 Comments

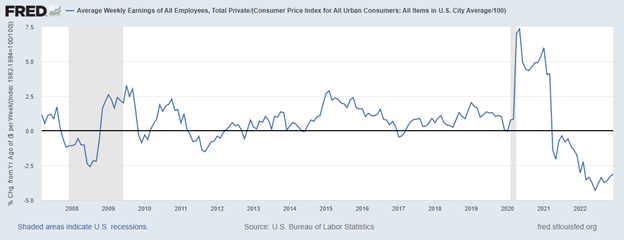

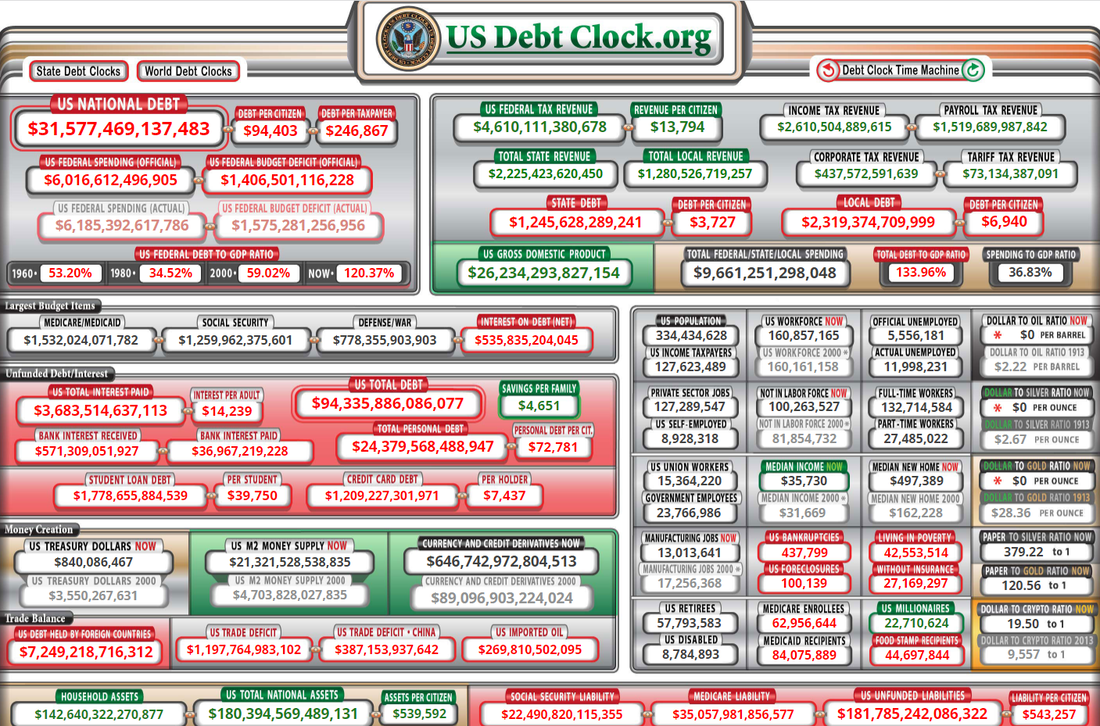

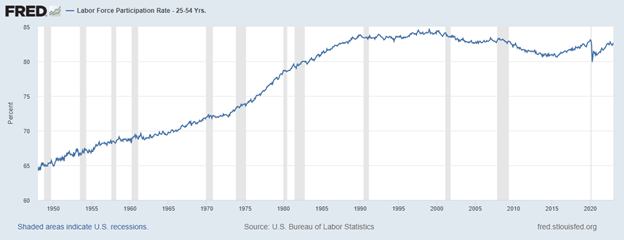

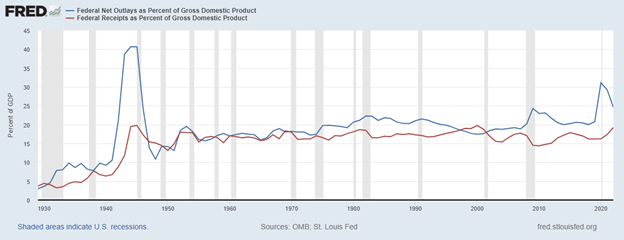

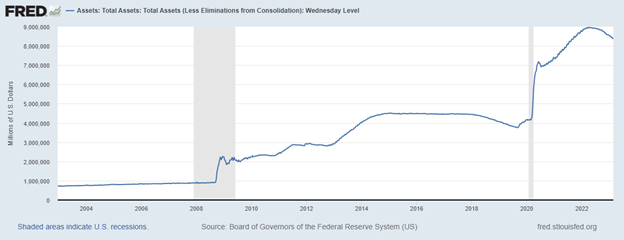

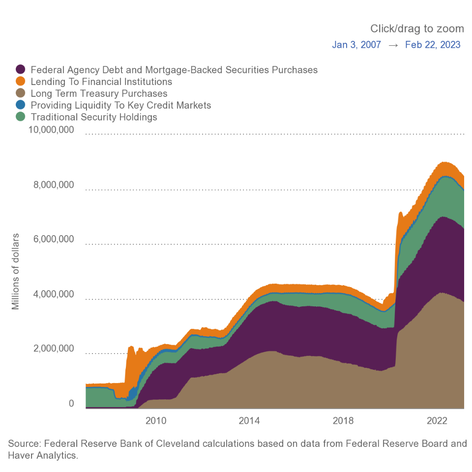

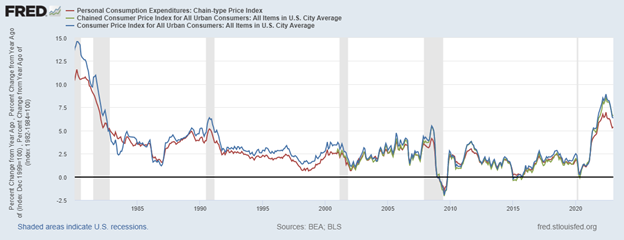

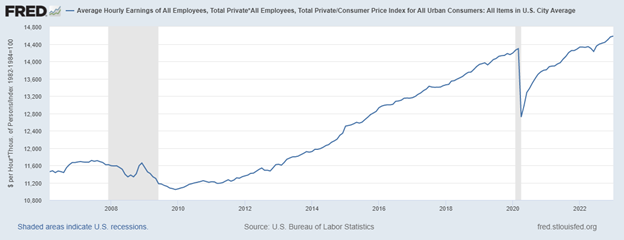

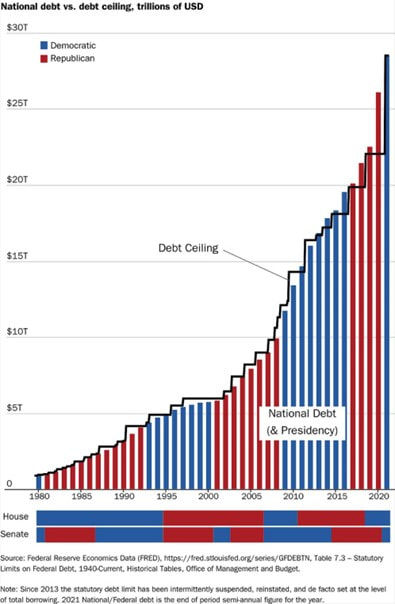

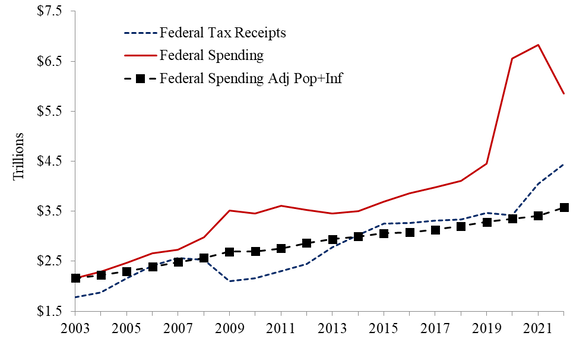

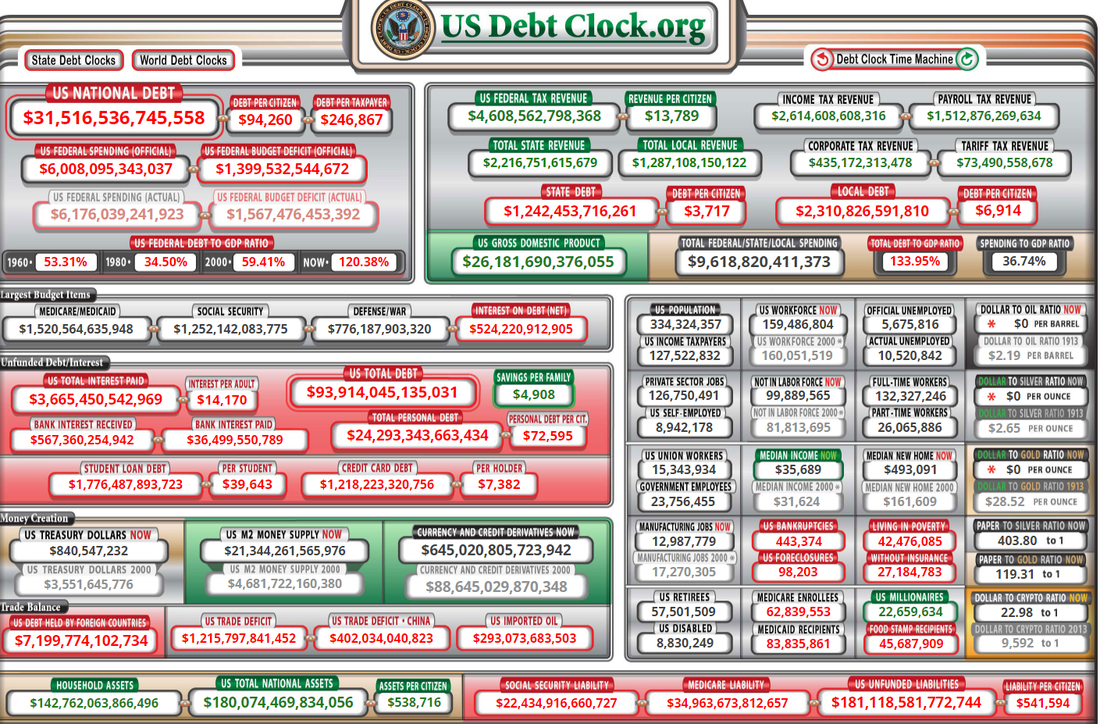

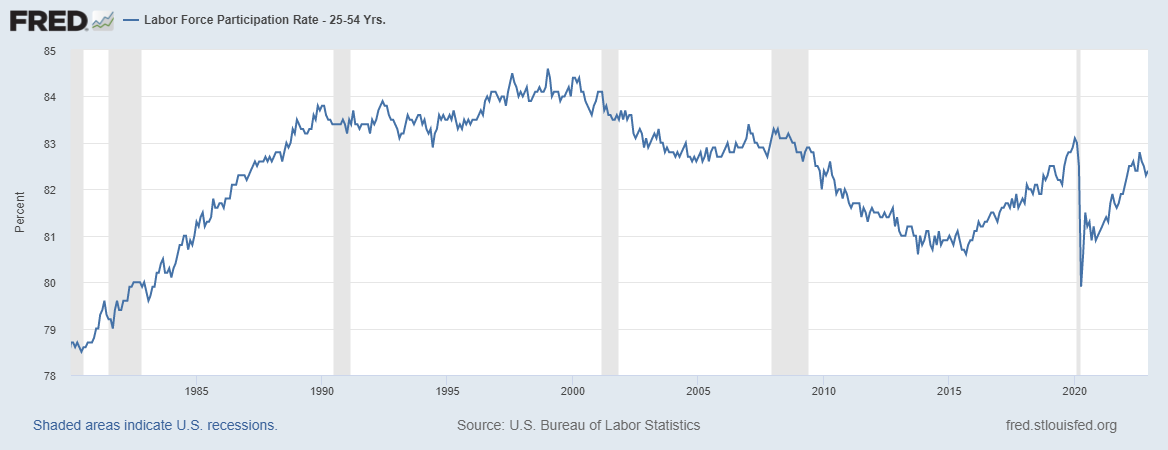

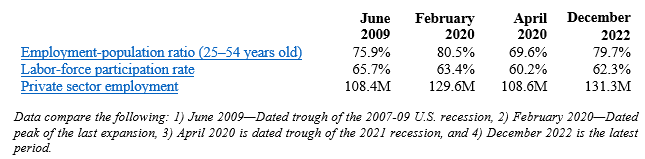

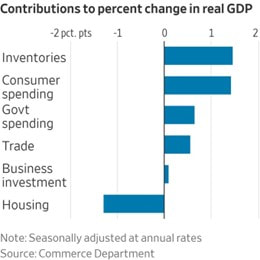

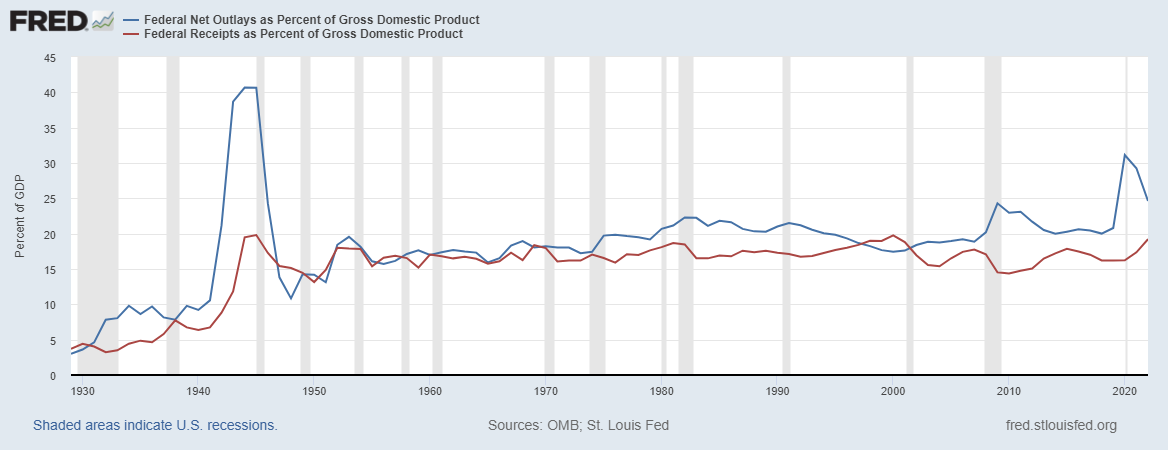

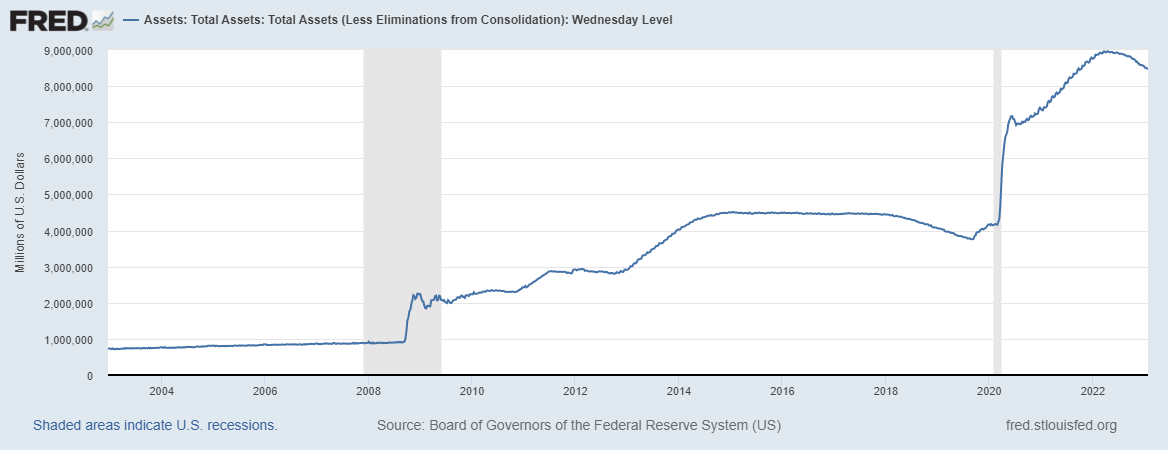

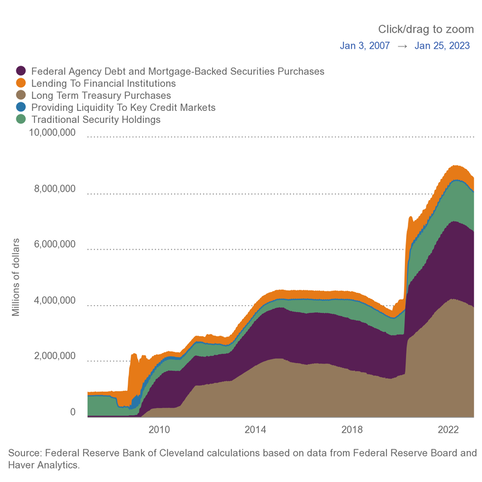

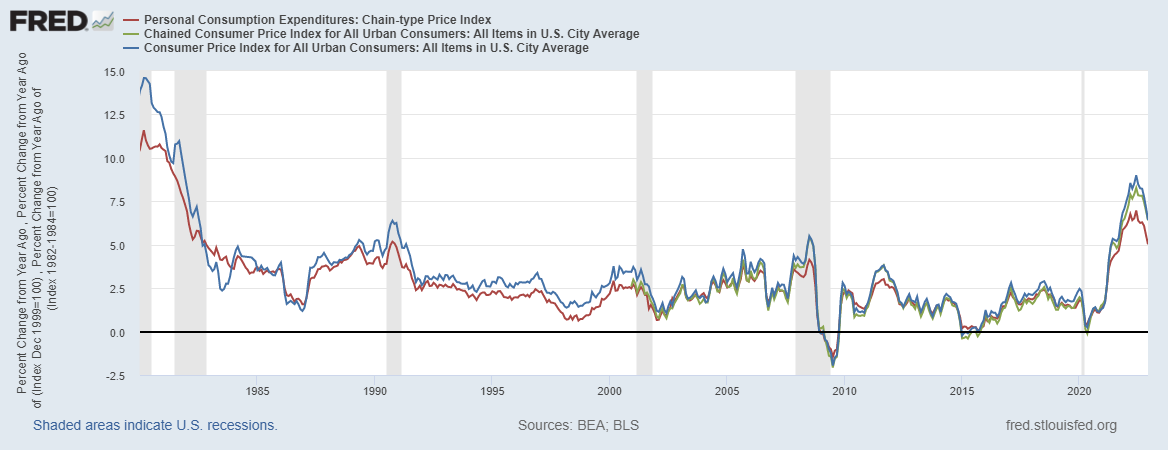

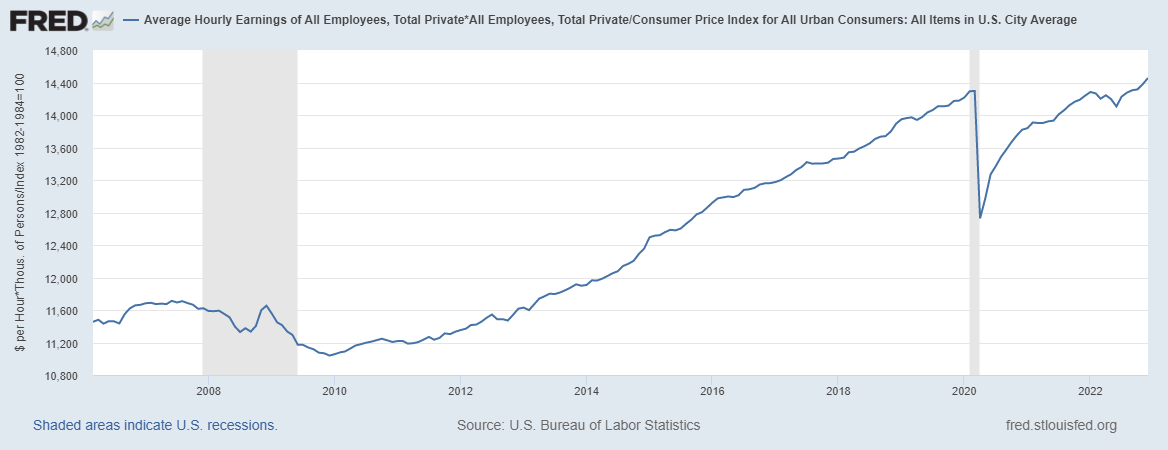

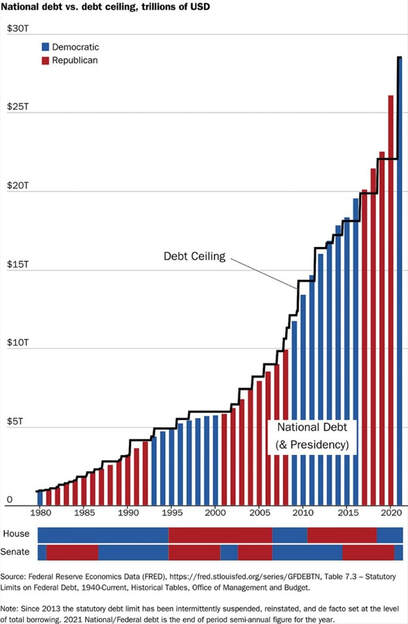

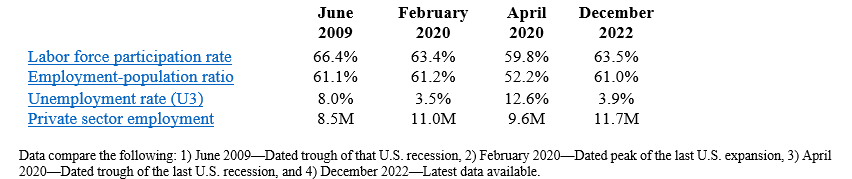

Key Point: The U.S. economy in 2022 had the slowest Q4-over-Q4 growth during a recovery since at least 2009 and average weekly earnings are now down for 22 straight months as inflation keeps roaring. But there’s hope if we just give free-market capitalism a chance to let people prosper.  Overview: Although President Biden recently tried to claim that the state of the union is strong, facts tell a different story. The government failures that drove the “shutdown recession,” high inflation, and weak economic growth over the last three years continue to plague Americans. This includes excessive federal spending leading to massive deficit spending adding up to $7 trillion since January 2020 to reach nearly $31.5 trillion in national debt—about $250,000 owed per taxpayer. This has created a fight between the Biden administration and House Republicans over the debt ceiling, as raising it must come with spending restraint to avoid some of the fiscal insanity that will lead to insolvency if nothing is changed. And more inflation could be on the horizon if the Federal Reserve chooses to monetize more more of the new debt, which past excess has already contributed to 40-year-high inflation rates. These government failures with little relief from pro-growth policies in sight mean that things will get worse before they get better.  Labor Market: The Bureau of Labor Statistic recently released its U.S. jobs report for January 2022. This report came with substantial revisions to seasonal adjustments and population estimates which could bias the data for a while given that the revised estimates include the much of the last three years of data that are highly volatile. And recall the recent report by the Philadelphia Fed finds that if you add up the jobs added in states in Q2:2022 there were just 10,500 net new jobs rather than more than 1 million reported. The establishment survey shows there were +517,000 (+3.3%) net nonfarm jobs added in January to 155.1 million employees, with +443,000 (+3.6%) added in the private sector and +74,000 (+1.4%) jobs added in the government sector. Most of the private sector jobs were added in the sectors of leisure and hospitality (+128,000), private education and health services (+105,000), and professional and business services (+82,000), which these three sectors led over the last 12 months as well; information (-5,000) and utilities (-700) were the only net job declines over the last month and no sector had net job losses over the last year. Average hourly earnings for all employees was up by 10 cents last month to $33.03, or up by +4.4% over the last year. And average weekly earnings in the private sector increased by $13.35 last month to $1,146, or up by +4.7% over the 12 months. The household survey had another large increase of +894,000 jobs added to 160.1 million employed There have been declines in net jobs in four of the last 10 months for a total increase of +1.8 million since March 2022, which is about half of the +3.6 million of the net jobs added per the establishment survey. The official U3 unemployment rate declined slightly to 3.4% which is the lowest since 1969. But challenges remains as inflation-adjusted average weekly earnings were down -1.5% over the last year for the 22nd straight month, weighing on Americans budgets to make ends meet. And since February 2020 before the shutdown recession, the prime age (25-54 years old) employment-population ratio was 0.3-percentage point lower, prime-age labor force participation rate was 0.3-percentage point lower, and the total labor-force participation rate was 0.9-percentage-point lower with millions of people out of the labor force thereby holding the U3 unemployment rate much lower than otherwise.   Economic Growth: The U.S. Bureau of Economic Analysis’ recently released the 2nd estimate for economic output for Q4:2022. The following table provides data over time for real total gross domestic product (GDP), measured in chained 2012 dollars, and real private GDP, which excludes government consumption expenditures and gross investment. And most of the estimates for Q4:2022 and growth in 2022 were revised lower, providing more evidence that 2022 was a very weak year if not a recession.  The shutdown recession in 2020 had GDP contract at historic annualized rates because of individual responses and government-imposed shutdowns related to the COVID-19 pandemic. Economic activity has had booms and busts thereafter because of inappropriately imposed government COVID-related restrictions in response to the pandemic and poor fiscal policies that severely hurt people’s ability to exchange and work. Since 2021, the growth in nominal total GDP, measured in current dollars, was dominated by inflation, which distorts economic activity. The GDP implicit price deflator was +6.1% for Q4-over-Q4 2021, representing half of the +12.2% increase in nominal total GDP. This inflation measure was +9.1% in Q2:2022—the highest since Q1:1981—for a +8.5% increase in nominal total GDP that quarter. This made two consecutive declines in real total (and private) GDP, providing a criterion to date recessions every time since at least 1950. In Q3:2022, nominal total GDP was +7.6% and GDP inflation was +4.4% for the +3.2% increase in real total GDP. But if inflation had been as high as it was in the prior two quarters or had the contribution of net exports of goods and services (driven by natural gas exports to Europe) not been 2.9%, real total GDP would have either declined or been essentially flat for a third straight quarter. In Q4:2022, there was a similar story of weakness as nominal total GDP was +6.6% and GDP inflation was +3.9% for the +2.7% increase in real total GDP. But if you consider the +2.7% real total GDP growth was driven by contributions of volatile inventories (+1.5pp), government spending (+0.6pp), and next exports (+0.5pp) which total +2.6pp, the actual growth is quite tepid like it was in Q3:2022. For all of 2022, real total GDP growth is reported +2.1% year-over-year but measured by Q4-over-Q4 the growth rate was only +0.9%, which was the slowest Q4-over-Q4 growth for a year since 2009 (last part of Great Recession). The Atlanta Fed’s early GDPNow projection on February 24, 2023 for real total GDP growth in Q1:2023 was +2.7% based on the latest data available. The table above also shows the last expansion from June 2009 to February 2020. A reason for slower real private GDP growth in the latter period is due to higher deficit-spending, contributing to crowding-out of the productive private sector. Congress’ excessive spending thereafter led to a massive increase in the national debt by more than +$7 trillion that would have led to higher market interest rates. This is yet another example of how there is always an excessive government spending problem as noted in the following figure with federal spending and tax receipts as a share of GDP no matter if there are higher or lower tax rates.  But the Fed monetized much of the new debt to keep rates artificially lower thereby creating higher inflation as there has been too much money chasing too few goods and services as production has been overregulated and overtaxed and workers have been given too many handouts. The Fed’s balance sheet exploded from about $4 trillion, when it was already bloated after the Great Recession, to nearly $9 trillion and is down only about 6.5% since the record high in April 2022. The Fed will need to cut its balance sheet (see first figure below with total assets over time) more aggressively if it is to stop manipulating so many markets (see second figure with types of assets on its balance sheet) and persistently tame inflation, which there’s likely a need for deflation for a while given the rampant inflation over the last two years.   The resulting inflation measured by the consumer price index (CPI) has cooled some from the peak of +9.1% in June 2022 but remains hot at +6.4% in January 2023 over the last year, which remains at a 40-year high (highest since July 1982) along with other key measures of inflation (see figure below). After adjusting total earnings in the private sector for CPI inflation, real total earnings are up by only +2.2% since February 2020 as the shutdown recession took a huge hit on total earnings and then higher inflation hindered increased purchasing power.   Just as inflation is always and everywhere a monetary phenomenon, deficits and taxes are always and everywhere a spending problem. The figure below (h/t David Boaz at Cato Institute) shows how this problem is from both Republicans and Democrats.  As the federal debt far exceeds U.S. GDP, and President Biden proposed an irresponsible FY23 budget and Congress never passed one until the ridiculous $1.7 trillion omnibus in December, America needs a fiscal rule like the Responsible American Budget (RAB) with a maximum spending limit based on population growth plus inflation. If Congress had followed this approach from 2003 to 2022, the figure below shows tax receipts, spending, and spending adjusted for only population growth plus chained-CPI inflation. Instead of an (updated) $19.0 trillion national debt increase, there could have been only a $500 billion debt increase for a $18.5 trillion swing in a positive direction that would have substantially reduced the cost of this debt to Americans. Of course, part of this includes the Great Recession and the Shutdown Recession, so these periods would have likely been good reason to exceed the limit, but regardless we would be in a much better fiscal and economic situation with this fiscal rule. The Republican Study Committee recently noted the strength of this type of fiscal rule in its FY 2023 “Blueprint to Save America.” And to top this off, the Federal Reserve should follow a monetary rule so that the costly discretion stops creating booms and busts.  Bottom Line: While there appears to be a strengthening labor market in January, let’s see if this continues as my guess is that these were biased from the data adjustments, and we will see a weaker labor market in the months to come. My expectation is that stagflation will continue along with the a deeper recession this year given the “zombie economy” with “zombie labor” of many workers sitting on the sidelines and others are “quiet quitting” along with the failures of many “zombie firms” that live on debt. Ultimately, Americans are struggling from bad policies out of D.C.. Instead of passing massive spending bills, the path forward should include pro-growth policies. These policies ought to be similar to those that supported historic prosperity from 2017 to 2019 that get government out of the way rather than the progressive policies of more spending, regulating, and taxing. The time is now for limited government with sound fiscal and monetary policy that provides more opportunities for people to work and have more paths out of poverty.

Recommendations:

Key Point: Americans are suffering under big-government policies as average weekly earnings adjusted for inflation are down for 21 straight months. It's time for pro-growth policies to unleash economic potential to let people prosper.  Overview: The irresponsible “shutdown recession” and subsequent government failures have led to a longer, deeper recession with high inflation that are having persistent consequences for many Americans’ livelihoods. This includes excessive federal spending redistributing scarce private sector resources with deficit spending of more than $7 trillion since January 2020 to reach the new high of $31.4 trillion in national debt—about $95,000 owed per American or $250,000 owed per taxpayer. This new debt has hit its limit and needs to be addressed with spending restraint as the Federal Reserve monetized most of the new debt, leading to a 40-year-high inflation rates. The failed policies of the Biden administration, Congress, and the Fed must be replaced with a liberty-preserving, free-market, pro-growth approach by the new majority by House Republicans so there are more opportunities to let people prosper.  Labor Market: The U.S. Bureau of Labor Statistics recently released the U.S. jobs report for December 2022. The BLS’s establishment report shows there were 223,000 net nonfarm jobs added last month, with 220,000 added in the private sector. Interestingly, while there have appeared to be a relatively robust number of jobs created, a recent report by the Philadelphia Fed find that if you add up the jobs added in states in Q2:2022 there were just 10,500 net new jobs rather than more than 1 million initially estimated. This further indicates that the recession started in (likely) March 2022 (more on this below). That expected revision to the establishment report supports the weak data in the BLS’s household survey, which employment increased by 717,000 jobs last month but had declined in four of the last nine months for a total increase of 916,000 jobs since March 2022. This number of net jobs added since then is much lower than the report 2.9 million payroll jobs in the establishment. The official U3 unemployment rate declined slightly to 3.5%, but challenges remain, including: 3.1% decline in average weekly earnings (inflation-adjusted) over the last year, 0.4-percentage point lower prime-age (25–54 years old) employment-population ratio than in February 2020, 0.6-percentage point below prime-age labor force participation rate, and 1.0-percentage-point lower total labor-force participation rate with millions of people out of the labor force.   These data support my warnings for months of stagflation, recession, and a “zombie economy.” This includes “zombie labor” as many workers are sitting on the sidelines and others are “quiet quitting” while there’s a declining number of unfilled jobs than unemployed people to 4.5 million And that demand for labor is likely inflated from many “zombie firms,” which run on debt and could make up at least 20% of the stock market and will likely lay off workers with rising debt costs. Economic Growth: The U.S. Bureau of Economic Analysis’ released economic output data for Q4:2022. The following provides data for real total gross domestic product (GDP), measured in chained 2012 dollars, and real private GDP, which excludes government consumption expenditures and gross investment.  The shutdown recession in 2020 had GDP contract at historic annualized rates because of individual responses and government-imposed shutdowns related to the COVID-19 pandemic. Economic activity has had booms and busts thereafter because of inappropriately imposed government COVID-related restrictions in response to the pandemic and poor fiscal policies that severely hurt people’s ability to exchange and work. Since 2021, the growth in nominal total GDP, measured in current dollars, was dominated by inflation, which distorts economic activity. The GDP implicit price deflator was +6.1% for Q4-over-Q4 2021, representing half of the +12.2% increase in nominal total GDP. This inflation measure was +9.1% in Q2:2022—the highest since Q1:1981—for a +8.5% increase in nominal total GDP that quarter. This made two consecutive declines in real total (and private) GDP, providing a criterion to date recessions every time since at least 1950. In Q3:2022, nominal total GDP was +7.6% and GDP inflation was +4.4% for the +3.2% increase in real total GDP. But if inflation had been as high as it was in the prior two quarters or had the contribution of net exports of goods and services (driven by natural gas exports to Europe) not been 2.9%, real total GDP would have either declined or been essentially flat for a third straight quarter. In Q4:2022, there was a similar story of weaknesses as nominal total GDP was +6.4% and GDP inflation was +3.5% for the +2.9% increase in real total GDP. But if you consider the +2.9% real total GDP growth was driven by contributions of volatile inventories (+1.5pp), government spending (+0.6pp), and next exports (+0.6pp) which total +2.7pp, the actual growth is quite tepid. For all of 2022, real total GDP growth is reported +2.1% year-over-year but measured by Q4-over-Q4 the growth rate was only +0.96%, which was the slowest Q4-over-Q4 growth for a year since 2009 (last part of Great Recession).  The Atlanta Fed’s early GDPNow projection on January 27, 2023 for real total GDP growth in Q1:2023 was +0.7% based on the latest data available. The table above also shows the last expansion from June 2009 to February 2020. The earlier part of the expansion had slower real total GDP growth but had faster real private GDP growth. A reason for this difference is higher deficit-spending in the latter period, contributing to crowding-out of the productive private sector. Congress’ excessive spending thereafter led to a massive increase in the national debt that would have led to higher market interest rates. This is yet another example of how there is always an excessive government spending problem as noted in the following figure with federal spending and tax receipts as a share of GDP.  But the Fed monetized much of it to keep rates artificially lower thereby creating higher inflation as there has been too much money chasing too few goods and services as production has been overregulated and overtaxed and workers have been given too many handouts. The Fed’s balance sheet exploded from about $4 trillion, when it was already bloated after the Great Recession, to nearly $9 trillion and is down only about 6% since the record high in April 2022. The Fed will need to cut its balance sheet (see first figure below with total assets over time) more aggressively if it is to stop manipulating so many markets (see second figure with types of assets on its balance sheet) and persistently tame inflation.   The resulting inflation measured by the consumer price index (CPI) has cooled some from the peak of 9.1% in June 2022 but remains hot at 6.5% in December 2022 over the last year, which remains at a 40-year high (highest since June 1982) along with other key measures of inflation (see figure below). After adjusting total earnings in the private sector for CPI inflation, real total earnings are up by only 1.1% since February 2020 as the shutdown recession took a huge hit on total earnings and then higher inflation hindered increased purchasing power.   Just as inflation is always and everywhere a monetary phenomenon, high deficits and taxes are always and everywhere a spending problem. The figure below (h/t David Boaz at Cato Institute) shows how this problem is from both Republicans and Democrats.  As the federal debt far exceeds U.S. GDP, and President Biden proposed an irresponsible FY23 budget and Congress never passed one until the ridiculous $1.7 trillion omnibus in December, America needs a fiscal rule like the Responsible American Budget (RAB) with a maximum spending limit based on population growth plus inflation. If Congress had followed this approach from 2002 to 2021, the (updated) $17.7 trillion national debt increase would instead have been a $1.1 trillion decrease (i.e., surplus) for a $18.8 trillion swing to the positive that would have reduced the cost to Americans. The Republican Study Committee recently noted the strength of this type of fiscal rule in its FY 2023 “Blueprint to Save America.” And the Federal Reserve should follow a monetary rule.

Bottom Line: Americans are struggling from bad policies out of D.C., which have resulted in a recession with high inflation. Instead of passing massive spending bills, like passage of the “Inflation Reduction Act” that will result in higher taxes, more inflation, and deeper recession, the path forward should include pro-growth policies. These policies ought to be similar to those that supported historic prosperity from 2017 to 2019 that get government out of the way rather than the progressive policies of more spending, regulating, and taxing. The time is now for limited government with sound fiscal and monetary policy that provides more opportunities for people to work and have more paths out of poverty. Recommendations:

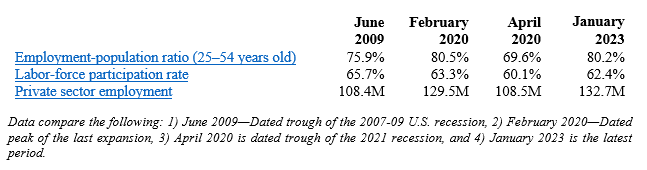

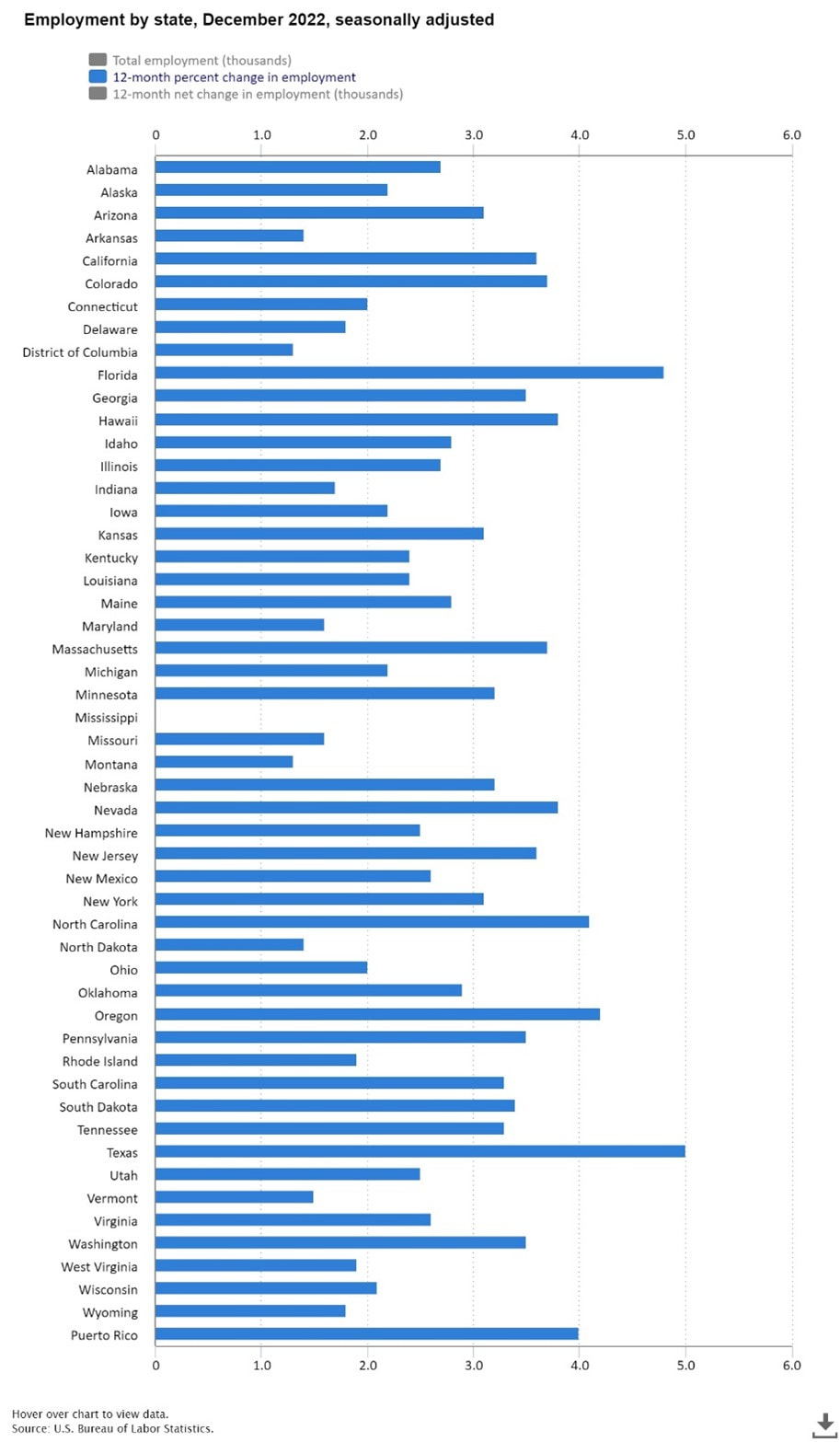

Key Point: Texas continues to lead the way in job creation over the last year (see first figure) and second in economic growth in the third quarter of 2023 (see last figure), but there’s more to do to help struggling Texans deal with the state’s affordability crisis, especially spending, regulating, and taxing less.  Overview: Texas has been a national leader in the economic recovery since the inappropriate shutdown recession in Spring 2020. This includes reaching a new record high in total nonfarm employment for the 14th straight month, leading exports of technology products for 20 consecutive years, and being home to more than 50 of the world’s Fortune 500 companies. While the 87th Texas Legislature in 2021 supported the recovery by passing many pro-growth policies like the nation’s strongest state spending limit, there’s more to do in the ongoing 2023 session to remove barriers placed by state and local governments. Labor Market: The best path to prosperity is a job, as it helps bring financial self-sufficiency, dignity, hope, and purpose to people so they can earn a living, gain skills, and build social capital. The table below shows the state’s labor market for December 2022. The establishment survey shows that net nonfarm jobs in Texas increased by 29,500 last month, resulting in increases for 31 of the last 32 months, to bring record-high employment to 13.7 million. Compared with a year ago, total employment was up by 650,100 (+5.0%)—fastest growth rate in the country—with the private sector adding 628,800 jobs (+5.7) and the government adding 21,300 jobs (+1.1%).  The household survey shows that the labor force participation rate is slightly higher than in February 2020 but well below June 2009 at the trough of the Great Recession. The employment-population ratio fell was unchanged in November and nearly where it was in February 2020, and the private sector now employs 700,000 more people than then. Texans still face challenges with a worse unemployment rate, though historically low, and nonfarm private jobs just recently above its pre-shutdown trend (Figure 1). The figure below compares the ratio of current private employment to pre-shutdown forecast levels in red states and blue states if both chambers of the legislature and the governor are Republican (dark red), Democrat (dark blue), or some combination (lighter colors).  The results show a clear distinction between red states and blue states, with the stringency of restrictions by governments during the pandemic along with pro-growth policies before and after the shutdowns playing key roles. Specifically, 21 of the 25 states with the best (highest) ratios are in red-ish states while 13 of the 15 states and D.C. with the worst (lowest) ratios are in blue-ish places as of December 2022. The following figure from Soquel Creek on Twitter tells the story even more directly: those states with more economic freedom prosper more than those with less economic freedom (see rankings in Fraser Institute's Economic Freedom of North America report: FL ranks #1, Texas ranks #4, California ranks #49, and New York ranks #50).  Overall, multiple indicators should be considered in this nuanced labor market, such as the fact that the unemployment rate is a weak indicator as many have dropped out of the labor force. While the labor force participation rate in Texas slightly exceeds where it was before the shutdowns, and the 3.9% unemployment rate could be considered full employment, the employment-population ratio is 0.2-percentage point below the pre-shutdown ratio. Economic Growth: The U.S. Bureau of Economic Analysis (BEA) recently provided the real gross domestic product (GDP) by state for Q3:2022. The Figure below Texas had the second fastest GDP growth (first is Alaska) of +8.2% on an annualized basis to $1.89 trillion (above the U.S. average of +3.2% to $20.05 trillion). In the prior quarter, Texas had the fastest growth with +1.8% growth as the U.S. average declined by -0.6% that quarter. Of course, these followed Texas’ GDP contractions of -7.0% in Q1:2020 and -28.5% in Q2 during the depths of the shutdown recession. Fortunately, GDP rebounded in Q3 and Q4, yet declined overall in 2020 by -2.9% (less than -3.4% decline of U.S. average) but increased by +3.9% in 2021 (below the +5.9% U.S. average). The BEA also reported that personal income in Texas grew at an annualized pace of +6.9% in Q3:2022 (ranked 6th highest and faster than the U.S. average of +5.3%) but slower than the robust +8.4% in Q2:2022 (ranked 6th best and above the U.S. average of +4.9%) as job creation and inflated income measures found their way across the economy.  Bottom Line: As Texas recovers from the shutdown recession and faces an uncertain future with the U.S. economy having stagflation and a likely recession, Texans need substantial relief to help make ends meet. Other states are cutting, flattening, and phasing out taxes, so Texas must make bold reforms to support more opportunities to let people prosper, mitigate the affordability crisis, and withstand destructive policies out of D.C.

Free-Market Solutions: In 2023, the Texas Legislature should improve the Texas Model by:

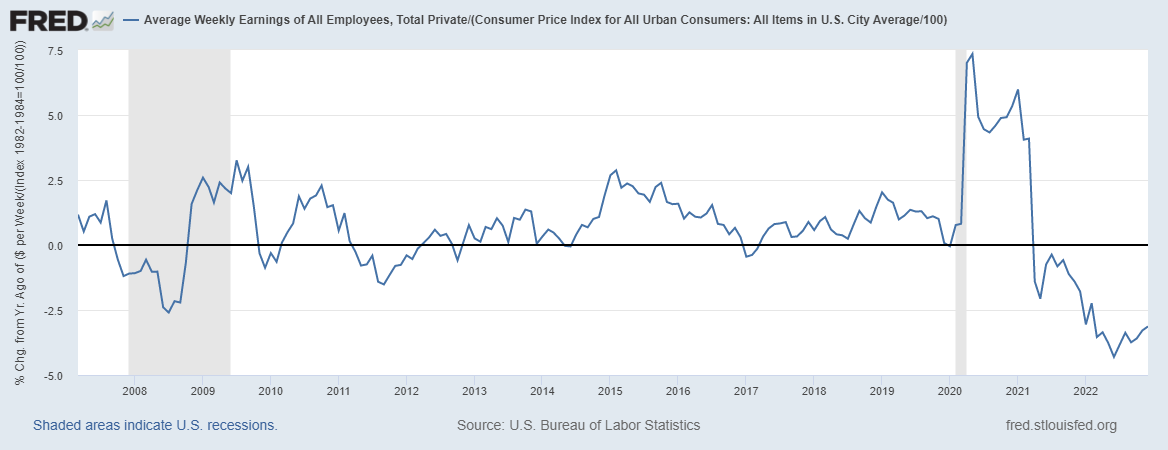

Our country’s economic journey throughout 2022 is one for the books. We had the highest inflation in 40 years , the highest mortgage rates in 20 years , and the worst stock market declines in 14 years . People are still struggling to pay bills, reduce debt, and save money, with average weekly earnings adjusted for inflation down 3% year over year .

The dismal state of the economy blindsided many people last year, but we don’t have to be caught so unaware in 2023. Knowledge is power, and knowing what could happen this year might make a difference in your finances. I believe that the burden of the inflationary recession will intensify this year. Expect to see the economy continue to correct from the consequences of Congress’s excessive deficit-spending that simply moved our money around, Biden’s overregulation that stifled energy production and other markets, and the Federal Reserve’s monetary mischief that manipulated markets through its bloated balance sheet. Currently, the Fed’s balance sheet remains well over $8.5 trillion , not falling nearly fast enough after it peaked at $8.9 trillion in April 2022. Much of this stems from when the Fed’s balance sheet more than doubled due to pandemic-related shutdowns to help Congress afford massive spending that ballooned the national debt by more than $7 trillion over the last three years. Now, the debt sits at about $31.5 trillion . Adding to the perfect storm is a regulation-happy president, Joe Biden, who hinders the ability of the free market to flourish, particularly in the areas of oil and gas, with his flawed green-energy agenda. The vital ingredients for a suffering economy with continually high inflation and high interest rates are present. The popular misery index (a measurement of economic distress on the everyday person), which uses the unemployment rate plus inflation, was above 10% in December — the highest rate since before the shutdowns in 2012. Given the projection of the economy in 2023, we can expect rising unemployment and elevated inflation as employers cut costs or raise prices to stay afloat. We’ve already seen employment take hits in the household survey, which has shown net employment declined in four of the last nine months for a total increase of just 916,000 jobs added since March 2022. In short, we’re looking at a continued inflationary recession with higher interest rates in 2023. It won’t be pretty, but there’s a reason for hope: a divided Congress. Republicans now have control of the House, and Democrats have control of the Senate and the White House. That division can create roadblocks to poor policies being pushed out of the Biden administration and the Democrat-controlled Senate, which has destroyed economic opportunities over the last two years. But the other possibility is more costly executive orders from Biden as he seeks to push more green energy policies, such as the ESG investing scam or stopping permits for oil and gas, and other flawed initiatives. This would mean more blockades to free-market flourishing. If the economy is prohibited from growing due to excessive regulation, taxation, and spending, we can anticipate that things will get worse before they get better. We’re in this mess because of 2020’s “shutdown recession” and subsequent government failures. The way out is the proven recipe of pro-growth, liberty-enhancing policies of less spending, taxation, and regulation while the Fed aggressively cuts its balance sheet. This would unleash the economic potential of the productive private sector and get people working well-paid jobs while substantially reducing inflation. In the meantime, hardworking people should minimize expenses, save for the storms ahead, and stay connected to family and the community for the smoothest possible sailing throughout what is sure to be a bumpy ride in 2023. Originally published at Washington Examiner.  Economics is the new American religion. Disagree with the mainstream narrative surrounding it, and you’re a heathen needing quick conversion. No longer is it seen as a social science requiring unbiased scrutiny: it’s about giving people what they think they want, no matter the cost.

And the cost they take in doing so is a big one: people’s prosperity. I recently sat down with Dr. Peter Boettke, professor of economics and philosophy at George Mason University, to discuss what needs to happen to reverse the problem of people turning “to politics for a sense of truth,” as he puts it. He explains the problem this way: “When my truth is not being listened to, my only recourse is to impose truth on others who are peddling in falsehood.” He’s correct. This desperate need to control is what leads to the government being placed on a pedestal as the Almighty solution rather than being viewed as a tool to preserve liberty. And there’s a need to use economics to tradeoffs of proposed solutions. When people aren’t allowed to disagree concerning economics and more policies are pushed on them as gospel, Americans are left with less opportunity for accomplishing extraordinary things. Instead of getting caught up by culture concerning economics, we need to return to the four pillars as defined by Boettke that substantiate this social science and contain the basis to achieve prosperity. Pillar One: Truth and Light The truth is that we live in a world of scarcity. This reality sheds light on the truth that because of scarcity, we must make tradeoffs to attain our goals. For most, this looks like trading your scarce time to work and earn money for scarce goods. Many today argue that not everyone can work or should be required to do so, which leads to petitioning Capitol Hill to pass policies that reduce the need to work. Lawmakers can pass one policy after another, but that will never change the inherent “dignity of work” as Boettke puts it. And respecting people’s agency gives them dignity. Pillar Two: Beauty and Awe We live in a world of spontaneous order. In every century, it’s beautiful and awe-inspiring to see how voluntary activity results in the spontaneous order that leads the way to the formation of global markets through which we thrive today. To achieve this phenomenon, it’s essential that individuals are empowered to work and contribute to society. Governmental policies that impose economic barriers cannot produce the same orderly result that emerge when people are permitted to achieve their hopes and dreams through a system of free markets and limited government. By latching onto the cultural ideology that the government and not the individual must work to solve all economic woes, we move further away from personal responsibility and deeper into the crippling dependency mindset. A mindset that convinces people they are powerless instead of possessing the tools required to flourish. Pillar Three: Hope Economics gives us hope of changing our circumstances. Through capitalism and entrepreneurship, we can have hope in civil society as the first resort while the government is the last resort in reducing poverty by encouraging long-term self-sufficiency. This was one of the major downfalls of governments across the country in 2020. By shutting down the economy and deciding which businesses were essential, small business owners and entrepreneurs were sidelined, leaving them fewer opportunities and less hope of climbing out of the government-imposed economic crisis. And less hope for those locked into their road to serfdom. Pillar Four: Compassion Economics at its core takes compassion on the impoverished and disadvantaged, seeking to lift them up. “It’s not about making the wealthy better off but about how we can lift up the poor [so that] the poor get richer even faster than the rich get richer,” Boettke explains. If people understood economics under these four pillars, rather than viewing it as a list of technicalities with which to police people, more progress would prevail. Governmental barriers imposed in our lives may be in popular demand but they are not the proposed solution among the American entrepreneurs fueling the economy. As Matt Ridley writes, “Innovation is the child of freedom and the parent of prosperity.” When seeking economic solutions for the nation, the path forward should be about how best to provide opportunities to let people prosper by removing barriers, respecting individual agency, and allowing hope and compassion to be cultivated in communities. That’s achieved by enhancing and preserving liberty through limited government and a flourishing civil society. Otherwise, we’re destined to fail the lessons of economics. Originally posted by Econlib In LPP Episode #10, I talk with Dr. Boettke, who is a professor at George Mason University, about why he chose economics, his books on economics and rules-based policy, COVID, and No Due Date group. You can find the YouTube video and links to the Apple Podcast and Spotify for this episode in my newsletter here. Please excuse any spelling or grammatical errors as this transcript is from an online converter and it and I may not have caught everything. For those that remain, I take all credit for those errors. I hope you'll read, watch, and listen to the episode, and please subscribe to my newsletter and other avenues for more episodes like this one. The Washington Post called them President Biden’s “wins in Congress.” But Democrats shouldn’t take that victory lap yet, as the Post admits—there’s little in the so-called Inflation Reduction Act that will do anything of the sort.

Despite the Biden administration’s claims to the contrary, the U.S. is in a recession. And despite its claims that everything else is to blame for the 40-year high in inflation, the blame is on the bad policies of excessive spending, taxing, regulating, and money-printing out of Washington. And the progressive fiscal policy pursued by this administration and Democrats in Congress is only making it worse. Signing the IRA was only throwing gasoline on the raging economic fire. In the first two quarters of 2022, the U.S. had two consecutive quarters of declining real economic output, historic declines in productivity, and rapid inflation contributing to half of companies planning to cut jobs. Every time there have been two declining quarters of real economic output since 1950, the period has been called a recession. So why should this time be different? Clearly, the economy is floundering and American families are struggling to make ends meet. No wonder, we’re all dealing with lower economic output and high inflation not seen in four decades. The IRA will result in higher taxes, more debt, more inflation, and deeper recession at exactly the worst time for the American people. The policy solutions aren’t complicated; we must limit government and maximize liberty by reducing spending, cutting taxes, removing regulations, and tightening the money supply. The policy mistakes in Washington over the last year prove that rules-based policies that rein in the failures of government are needed now maybe more than ever. Originally posted at TPPF.  While a stagnating economy with high inflation is what economists usually call stagflation, the current situation is worse, as the real economy is declining. So there’s much less to go around for everyone—making us poorer in the process.

This inflation-recession could be resolved by Washington reversing course, but President Joe Biden and Democrats in Congress are doing the opposite. Their new bill, called the “Inflation Reduction Act” (IRA), will spend more, raise taxes, increase debt, and contribute to more inflation, resulting in a deeper recession. The IRA includes estimated hikes in taxes with a new 15% corporate minimum tax rate, 87,000 new Internal Revenue Service (IRS) agents to audit more taxpayers, and new closure of “carried interest loophole.” These are each bad policies, but especially during a recession. These add up to an estimated tax hike of about $730 billion compared with current policy over the next 10 years. The main tax hike is the new alternative minimum tax (AMT) of 15% on book income for corporations with net income exceeding $1 billion. This proposal has a rosy revenue projection of $313 billion. But businesses don’t pay taxes; they just submit them. People pay them, through higher costs, lower wages, and fewer jobs. The dynamic effects will result in less tax revenue collected from this hike. According to a recent study by the Tax Foundation, this tax hike alone would contribute to killing 23,000 jobs, a 0.1% cut in wages, and 0.1% less in economic output. If we consider other provisions like the tax hikes on carried interest and reinstatement of the federal Superfund program, the total number of jobs killed is 30,000 with every income group having a reduction in after-tax income. Clearly, this wouldn’t reduce inflation or help the economy recover. But there’s more. While the IRA is aimed at taxing the rich and corporations more, the Congressional Joint Committee on Taxation finds that every income group except those with income between $10,000 to $20,000 per year would face a higher average tax rate. This would mean President Biden’s pledge to not tax anyone earning less than $400,000 per year would be broken, with about half of the burden falling on those earning less than $200,000 per year. And the $80 billion in additional funding for 87,000 new IRS agents to increase tax enforcement and compliance is expected to bring in a phony amount of about $200 billion over a decade. But this will just increase more bureaucracy in an already overly bureaucratic federal government that will make Americans’ lives worse as they put more costs on taxpayers. Specifically, there could be 1.2 million more individual audits per year, and you can bet when the IRS doesn’t increase tax collections from legal tax returns they will come after every tax group, not just those making more than $400,000 per year. On the spending side, the IRA provides tax incentives and subsidies for unreliable wind and solar energy, an expansion of Obamacare subsidies until 2025, and other expenditures to the tune of about $430 billion. Using these rosy assumptions, there is a projected deficit reduction of $300 billion over 10 years. However, more conservative estimates suggest that the IRA will have less deficit reduction and will likely increase the deficit. The Tax Foundation, Penn Wharton Budget Model (PWBM), and Congressional Budget Office (CBO) calculate a $178 billion, $247.8 billion, and $101.5 billion in deficit reduction over the next decade, respectively. But assuming the Obamacare subsidies are extended over the full 10-year period for an apples-to-apples comparison, the PWBM estimates that would bring that deficit reduction down by $158.9 billion to just $88.9 billion over the decade, which is the same amount of the deficit in just June 2022. But recall that these estimates are compared with current policy assumptions over the next decade, which already have massive deficits because of reckless spending, so the IRA will most likely make the deficit worse. Spending will be permanent and is on the front end of the bill, while taxes will likely be temporary and are more on the back end—so the deficit will be higher in the first few years, which will give the Federal Reserve more debt to purchase thereby creating more inflation. And the higher taxes, more debt, and more inflation will stifle economic growth so a deeper recession will result. The IRA does the opposite of what the name implies. This is now too common with Democrats in Congress as they like to keep redefining things that don’t match their narrative. They should instead name this bill the “Inflation Recession Act” because we will get more of both. This far-left agenda must be rejected. Kill the bill. Published at TPPF with Daniel Sanchez-Pinol  Americans are sacrificing their savings to keep up with soaring inflation.

This burden has contributed to consumer sentiment reaching its lowest level in June since the University of Michigan started the survey in January 1978. And the progressive policies in D.C. could soon make this bad situation worse. The personal saving rate, which is the share of after-tax income not used for consumption, declined again to 5.1% in June. This is after it reached 33.8% in April 2020, which was a record high since January 1959, after the first round of “stimulus” checks sent by Congress during the shutdowns. There were two more rounds of checks sent by Congress, along with enhanced unemployment payments and other handouts that weren’t connected to work, which kept the saving rate historically high as many places were shut down and people made more from handouts than they did while working. Remember, nothing is free. Those handouts and other government spending contributed to more than $6 trillion in additional national debt, which the Federal Reserve then mostly monetized—leading to the generational high in inflation. The higher inflation outpaced saving and income growth since then, as the costly policies came home to roost and cut the saving rate to 5.1%—the lowest since August 2009. What will happen when Americans run out of savings? But there’s little reprieve in sight as inflation looks to keep rising or at least not abating soon from bad policies in D.C. Inflation, which is the loss of purchasing power of your dollar, continues upward to 6.8% in June 2022 as measured by the personal consumption expenditure (PCE) price index—the highest since January 1982. The PCE inflation measure accounts for the substitution effect from high priced goods to lower priced goods. This isn’t reflected in the often-reported measure of the consumer price index (CPI) inflation rate of 9.1%, which is the highest since November 1981. Both measures show Americans’ money isn’t going nearly as far as it did a year ago. In fact, families’ purchasing power is set to be cut in half in just 10 years at the pace of PCE inflation and even faster for CPI inflation. This implies that in order to maintain the same consumption levels, households have to allocate more income to consumption than to savings. And many Americans are turning to increased debt as their savings dry up. Household debt increased to a record high of $16 trillion in the second quarter of 2022. Not surprisingly, credit card debt grew the most by 13%, which is the fastest increase in 20 years. Moreover, household debt to real economic output passed the 80% mark at the end of 2021. It’s up to 82% in the second quarter of 2022, a historically high rate, as debt increased and the real economy declined for two straight quarters. This share will likely get worse in the following quarters as Americans go through their savings and dip further into debt. And interest rates going up means the amount to pay interest on the debt will contribute to higher balances and more pressure to meet their financial obligations. No wonder people don’t feel secure about their economic future. Bad policies by Congress and the Federal Reserve contributed to this destruction and could even make things worse. Congress spent too much, leading to massive deficits, which gave the Fed debt to purchase to inject money into the economy over the last two years. That inflated “boom” had to eventually “bust.” And that’s what is happening now as the redistribution by Congress has slowed some and the Fed is finally raising its target interest rate allowing markets to correct. But Congress should be spending much less and the Fed should be more aggressive in tightening the money supply and raising its interest rate target. The famous Taylor rule suggests a rate of at least 6%, which is substantially higher than the current range between 2.5% to 2.75%. Ultimately, what’s needed now are pro-growth policies of spending, taxing, regulating, and printing cuts instead of what’s coming out of Washington. President Biden and Democrats in Congress aren’t helping the situation with the “Inflation Reduction Act,” as it will lead to more debt and more inflation that will further deplete savings, thereby making a bad situation worse for Americans. Things must change. Published at TPPF with Daniel Sanchez-Pinol  The U.S. government is bankrolling favored businesses at the expense of taxpayers and other businesses. Again. By continually involving itself in the market, government is impeding economic growth and the potential of industries to reach their full potential. That must change.

Congress recently passed the CHIPS Act, which is a $280 billion spending boondoggle that will provide funding of $52.2 billion to computer chip manufacturers. To sweeten the pot, Congress is also offering a 25% tax credit for semiconductor fabrication, which could cost an estimated $24 billion over five years. And these subsidies could support production in other regions, such as China and Europe. President Joe Biden will sign this obscene corporate welfare scheme into law soon. Congress claims this will strengthen domestic semiconductor production and help the U.S. compete with China, but that rhetoric is wrong. Domestic production of these technologies has been slowing since 1990. The U.S. still has valuable domestic producers, like Texas Instruments and Intel, but these corporations recently accounted for 12% of global chip production in 2021, down from 37% in 1990, according to the Boston Consulting Group. While the federal government might seem smart for attempting to help this industry compete, its methodology is flawed. Expanding corporate welfare will only serve to degrade competition and diminish the free-market principles that uphold the U.S. economy. This flawed approach is apparent when considering the data around prices of chip production. The total 10-year cost of ownership of a new semiconductor fabrication plant in the U.S. is 30% higher than in Taiwan, South Korea, or Singapore, and 37% to 50% higher than in China—or $10 to $40 billion dollars depending on the product. Anywhere from 40% to 70% of the difference in price is directly attributable to the incentives government provides that contribute to reduced competition. Throwing taxpayer money at the problem is a solution in search of a problem. In 2021, the U.S. semiconductor industry had substantial growth. In the closing months of 2021, American sales increased by 5.2%. That year the market had the largest share of growth worldwide, expanding 27.4%. While recessions in the U.S. and elsewhere have reduced consumption of goods that use semiconductor chips and as production increases, there has been a reduction in shortages and lower chip prices—contributing to lower stock prices. While the U.S. lags China in semiconductor production, the U.S. industry is growing faster, and we still lead by large margins in research, development, and design. The U.S. industry is a leader in chip design, and accounts for roughly 60% of all global fabless firm sales, and some of the largest integrated device manufacturers. The U.S. accounts for the largest share of the global design workforce, speaking to our leadership and development prowess. Earmarking $76 billion of taxpayer money for an already growing industry while in the midst of a recession is politically irresponsible and economically destructive. Moreover, spending to this degree fuels the bloated national debt during a recession and puts upward pressure on inflation if the Federal Reserve monetizes the debt. While President Biden will likely sign the CHIPS Act, Congress ought not use this as a precedent to subsidize more industries. The outsourcing of semiconductor production should be a wake-up call to the burdensome overregulation, overspending, and over-taxation domestically on businesses; not a license to spend more taxpayer money. With more subsidies going to specific companies, less investment and the further fleeing of business from America to places with more attractive and beneficial economic circumstances will continue. Advocates like U.S. Sen. Tom Cotton tried to justify this bill by claiming that “by ceding semiconductor manufacturing and development to countries like China, the United States has fallen behind and given the Chinese Communist Party dangerous leverage over our nation.” While China has leverage over America in that department for now, this corporate welfare is economically harmful. In the process of providing cash to businesses, corporate welfare takes money from taxpayers and consumers, reducing economic growth and increasing the debt that has many risks—including economic and national security. Because corporate welfare disrupts natural market processes, it shifts money from the most productive economic actors to those less productive—but more politically connected. This creates economic inefficiency and stunts competition, making the situation worse. The U.S. government ought to instead cut the cost of doing business domestically by reducing government spending, taxes, and regulations. By correcting the current government failures in this market in this way, Americans will flourish more. Published at TPPF with Noah Busbee  Two and two make five. This non-truth is one of the small phrases at the heart of George Orwell’s “1984.” It is used to demonstrate the ruling party’s focus on the absolute domination of its citizens, often subverting or rejecting truth in order to maintain its power.

Orwell’s phrase is often invoked in political discourse to indicate that the government, or someone else in power, is subverting, rejecting, or attempting to redefine the truth in order to serve their political ends. As previously noted in the Ginn Economic Brief, the economy is experiencing the deadly combination of stagnation and high inflation—stagflation. Families across America are getting hit by a massive hike in the cost of living, driving them to struggle to make ends meet, dip into savings to pay for basic necessities, or turn to government handouts in the form of safety nets. Despite clear evidence to the contrary, the Biden administration and its media lapdogs (or perhaps, the other way around—the radical leftist media and its lapdog, the Biden administration) refuse to assume responsibility for the actions that have brought on this rapidly-worsening economy. Instead, they deflect: “inflation is transitory,” “inflation is not as bad as it looks,” “the issue’s we’re facing are a result of supply chain issues from COVID,” and “Make no mistake: The current spike in gas prices is largely the fault of Vladimir Putin.” However, this refusal to assume responsibility is par for the course for the Biden administration—it’s not so much a subversion of the truth as it is simply a string of false excuses. The statements strike a dishonest, but not Orwellian, chord. They’re not why we invoke Orwell’s “two and two make five.” That dubious honor, instead, goes to the recent string of press releases, tweets, and news articles arguing, in various ways, that no, the economy is not headed into—or is already in—a recession. Either because the “numbers are not what they seem,” “the definition of recession is far more nuanced than just two quarters of negative growth,” or “the traditional definition of recession is outdated and needs to be updated to reflect modern monetary theory.” This is the true Orwellian speak—ahead of a second consecutive report of negative inflation-adjusted economic growth, which came out this morning, the generators of that contracting economy are out in force arguing that no, you shouldn’t believe your eyes, your bigger bills, or your dwindling savings account—the economy is actually fine! The rationale for this attempt to deflect on how a recession is typically defined is fairly straightforward: The Biden administration is already flagging in polls, and an official declaration of recession would be a confirmation of what most Americans are already feeling—a complete and total lack of confidence in the Biden administration’s ability to lead America or implement policies that lead to human flourishing. This is the truth that must be remembered amidst the deluge of people and organizations trumpeting that idea that recession is either not what we think it is or not as bad as we think it is. The current administration’s radically progressive, half-baked policies are slowly, but surely, destroying our economy and the American dream. Published at TPPF with Austin Prochko |

Vance Ginn, Ph.D.

|

RSS Feed

RSS Feed

Proudly powered by Weebly