Highlights

Overview

The Bureau of Labor Statistics recently released its U.S. jobs report for April 2023, which was another mixed report with some strengths but many weaknesses.

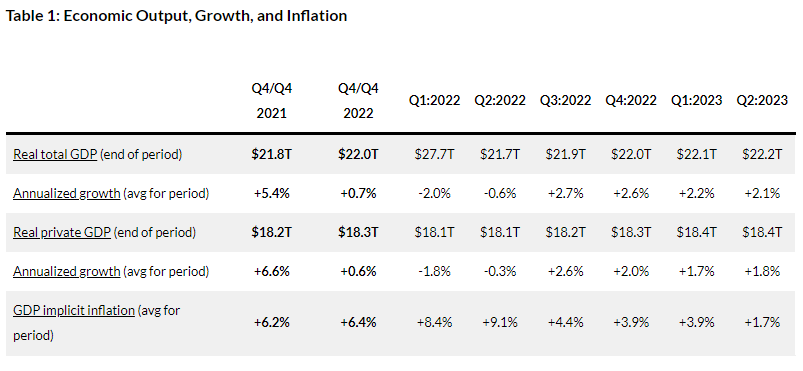

Economic Growth The U.S. Bureau of Economic Analysis recently released the third estimate for economic output for Q2:2023.

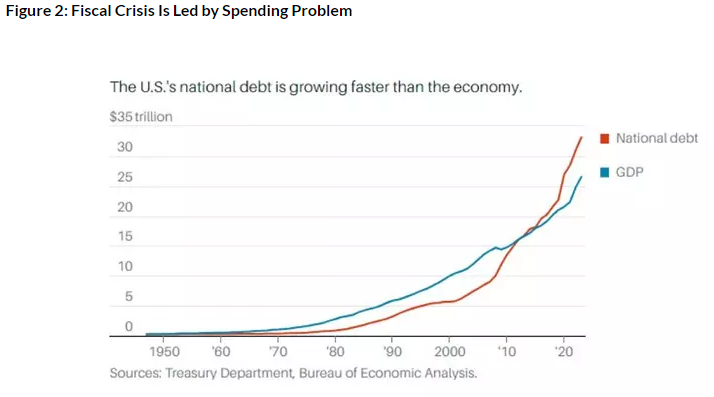

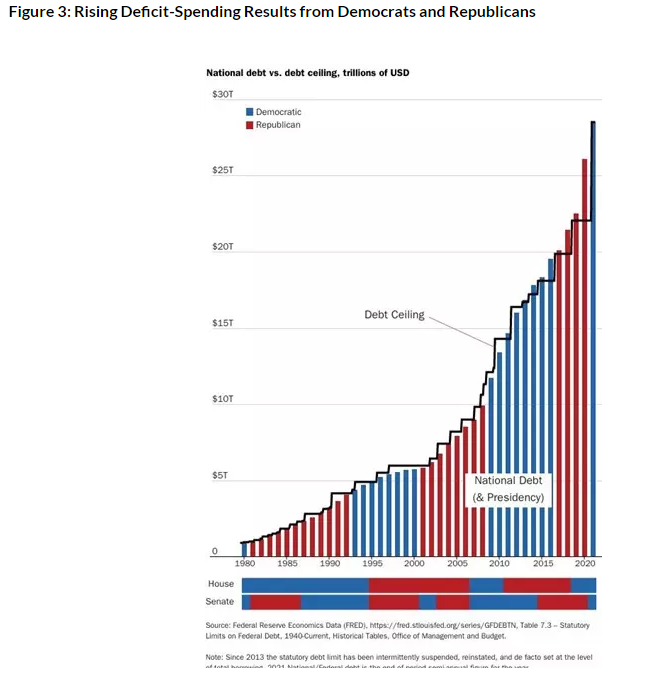

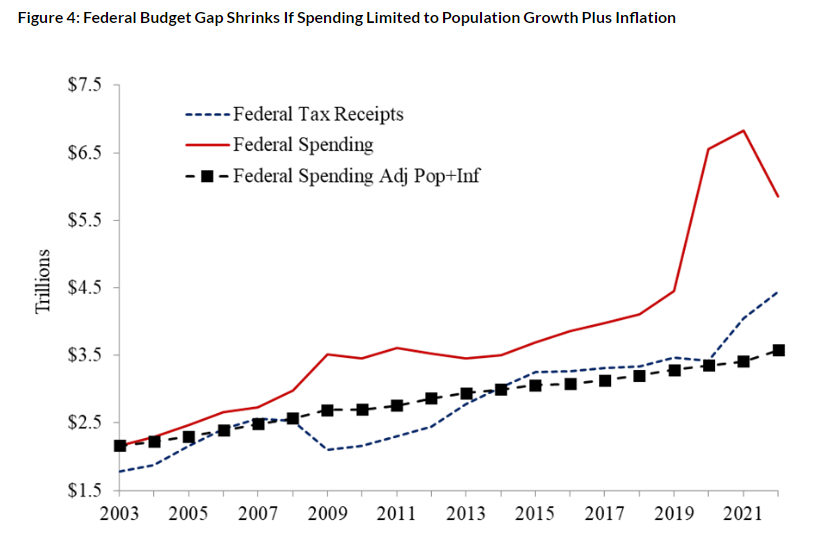

The latest indicator of this concern is U.S. real GDP was revised lower to just a 2.1% increase last quarter. Moreover, previous quarters were revised lower and there continue to be indications of a recession in early 2022 from two consecutive quarters of declining economic activity and relatively weak thereafter. Another measure of economic activity is the real average of GDP and GDI which accounts for domestic production and income. It increased by just 1.4% to $22.1 trillion. This important measure has declined in half of the last six quarters, increasing this value by only 1.2% since the first quarter of 2022, which is likely when the recession started. Meanwhile, the federal budget deficit is growing faster because of overspending and declining tax collections from a weak economy (See Figure 2). The national debt has ballooned to $33.5 trillion, and net interest payments on the debt will soon be a top federal expenditure of at least $1 trillion. Adding to these fiscal challenges are other large, unnecessary expenditures of taxpayer money.  The Fed has monetized, or printed, much of the new debt to keep interest rates artificially lower than where the market would have them. This created higher inflation as there was too much money chasing too few goods and services. And this has been exacerbated as production has been overregulated and overtaxed and workers have been given too many handouts. The Fed will need to cut its balance sheet (total assets over time) more aggressively if it is to stop manipulating markets (see this for types of assets on its balance sheet) and persistently tame inflation. The current annual inflation rate of the consumer price index (CPI) has been cooling since a peak of +9.1% in June 2022 but remains elevated at 3.7% in September 2023, which remains too high as are other key measures of inflation. Just as inflation is always and everywhere a monetary phenomenon, deficits and taxes are always and everywhere a spending problem. David Boaz at Cato Institute has noted how this problem is from both Republicans and Democrats (See Figure 3).  In order to get control of this fiscal crisis which is contributing to a monetary crisis, the U.S. needs a fiscal rule like the Responsible American Budget (RAB) with a maximum spending limit based on the rate of population growth plus inflation. This was recently released as part of Americans for Tax Reform’s Sustainable Budget Project. If Congress had followed this approach from 2003 to 2022, Figure 4 shows tax receipts, spending, and spending adjusted for only population growth plus chained-CPI inflation. Instead of an (updated) $19.0 trillion national debt increase, there could have been only a $500 billion debt increase for a $18.5 trillion swing in a positive direction that would have substantially reduced the cost of this debt to Americans. The Republican Study Committee recently noted the strength of this type of fiscal rule in its FY 2023 “Blueprint to Save America.” And to top this off, the Federal Reserve should follow a monetary rule so that the costly discretion stops creating booms and busts.  Bottom Line

The stagflationary destruction will continue given the “zombie economy” and the unraveling of the banking sector which will hit main street hard. Instead of passing massive spending bills, the path forward should include pro-growth policies that shrink government rather than big-government, progressive policies. It’s time for a limited government with sound fiscal and monetary policy that provides more opportunities for people to work and have more paths out of poverty. Recommendations:

This was originally posted at Texans for Fiscal Responsibility.

0 Comments

Leave a Reply. |

Vance Ginn, Ph.D.

|

RSS Feed

RSS Feed

Proudly powered by Weebly