|

Naomi and I discuss:

1) Pros and cons of taxpayer-funded health care and whether it is a human right; 2) Problems with Medicaid and how it is putting doctors and patients at a disadvantage; and 3) The crucial roles of free market competition and technology in quality, affordable health care. Naomi’s bio:

You can watch this episode and others along with my Let People Prosper Show on YouTube or listen to it on Apple Podcast, Spotify, Google Podcast, or Anchor. Please share, subscribe, like, and leave a 5-star rating! For show notes, thoughtful insights, media interviews, speeches, blog posts, research, and more, check out my website (www.vanceginn.com) and please subscribe to my newsletter (www.vanceginn.substack.com), share this post, and leave a comment.

0 Comments

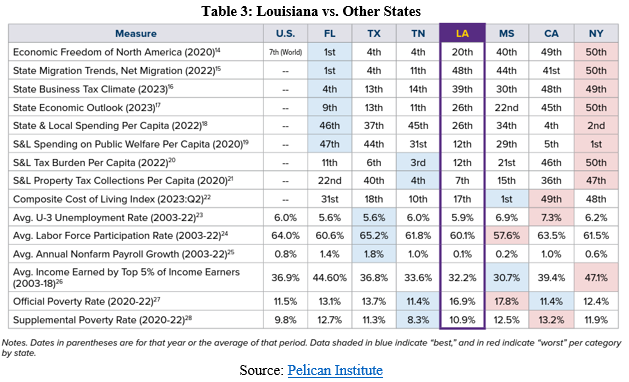

What is going on in Louisiana’s economy? How is the labor market doing for Louisianans? What you hear in the media or by politicians may not always match reality. The Pelican State has many fantastic resources with educated people, eccentric culture, robust ports, abundant oil and gas production, and much more. But Louisianans can’t reach their full potential and flourish because of failed public policies, highlighted by job losses in two of the last three months and many still out of the labor force. The Pelican Institute’s “Comeback Agenda,” which includes our recently released tax and budget reform plan, provides a prosperous path forward. Let’s dive into the data, consider myths and realities, and note which policies would help.

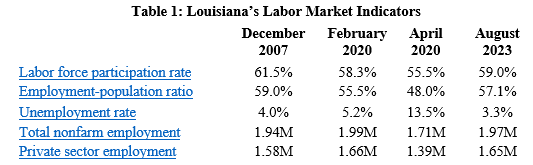

Table 1 provides Louisiana’s key labor market data during important dates from the U.S. Bureau of Labor Statistics. These dates are December 2007, when the Great Recession started; February 2020, when the last expansion peaked before the COVID-19-related shutdowns; April 2020, when the shutdown recession ended; and August 2023, for the latest data available.  These data indicate strength on the surface, but how are Louisianans really doing? In August 2023, the unemployment rate declined to 3.3%, with 68,814 people unemployed; both are the state’s record lows. Louisiana Governor John Bel Edwards cheered these points as a testament to his policies since he took office in January 2016. But are these data worthy of praise? Let’s start by looking at how the unemployment rate is calculated: unemployed divided by the labor force, which includes the employed and unemployed. This calculation can show a lower unemployment rate in multiple ways, including fewer unemployed with the same labor force or fewer unemployed and fewer in the labor force. These data are collected from a survey of households across the state. The first reason would be considered by most as a positive result, while the latter as mostly negative if people stopped looking for work because they couldn’t find it or opted to receive temporary government assistance. There were massive increases in the number of Louisianans enrolled in social safety net programs over the last three years, which likely changed people’s incentive to work. But considering what has happened in the labor market since January 2016, the result is not as rosy. Since January 2016, Louisiana’s working-age population has declined by 29,650 to 3.5 million. The labor force has declined by 40,236 to 2.1 million. The number of unemployed has declined by 59,966 to 68,814. These data reflect how Louisiana has had people leave the state for years, including the third highest net out-migration in the country last year. The situation today is much different than in January 2016. If we account for the decline of 40,236 in the labor force and say those people didn’t leave the labor force and are unemployed (understanding some of them may find employment, but we don’t know how many would), then the unemployment rate would be 5.1%. This unemployment rate is lower than the 6% in January 2016 but 55% higher than the reported 3.3% rate today. Moreover, if the working-age population hadn’t declined, the labor force participation rate would be 59.7% instead of the 59.0% rate today. Work matters, as it brings about dignity and self-sufficiency and leaves fewer people needing help from government safety net programs. These calculations show that while the labor market data can look good on the surface, there are many real problems facing Louisianans that need to be addressed by state leaders. There are obstacles imposed by the government that can be solved, and we need only look to Utah as an example of how states can do a better job of connecting citizens with employment and supportive services that lead to self-sufficiency.

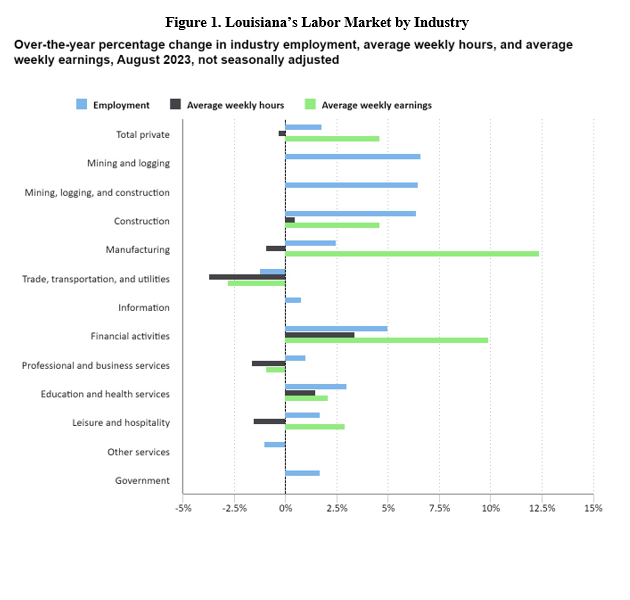

Nonfarm employment is what economists most often report because the data are considered more consistent with the health of the labor market. This is collected from established businesses instead of households across the state. There was an increase in nonfarm employment by 7,400 jobs in August (9th most in percentage terms of any state). But this was after cumulative losses of 3,600 jobs during the prior two months for an increase of just 3,800 jobs over the last three months. Considering nonfarm employment over a longer period, it is up by 34,200 jobs from a year ago (23rd most in the country). But it is down by 20,900 since January 2016 and down by 28,000 since February 2020 (one of only ten states not to have regained all jobs since then). We can see where jobs are added in Louisiana by diving deeper into these data. Jobs in the private sector increased by 6,700 last month to 1.65 million, and government employment increased by 700 jobs to 316,600 last month. Compared with a year ago, the private sector added 29,600 jobs, and the government added 4,600 jobs. But the private sector is down by 8,700 since January 2016 and down by 13,600 jobs since February 2020. There is growing weakness in the labor market, with job losses and average weekly earnings not rising as fast as CPI inflation of 3.7% in many industries (Figure 1).  Overall, these data show the hardship that many Louisianans are facing across the state.

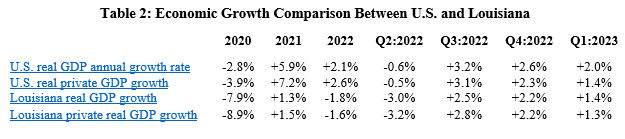

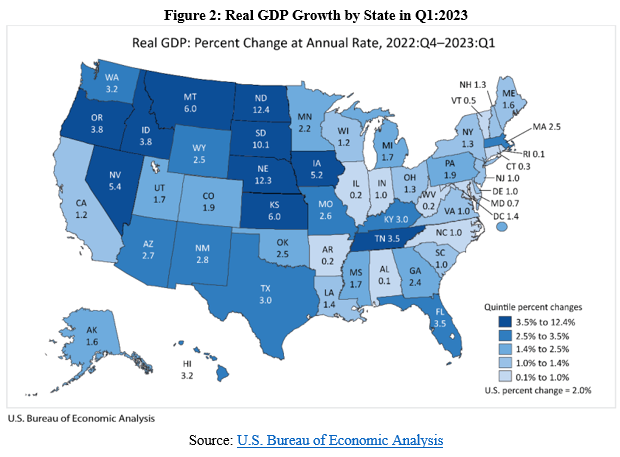

Table 2 shows how the U.S. and Louisiana economies performed since 2020, as reported by the U.S. Bureau of Economic Analysis.  The steep declines were during the shutdowns in 2020 in response to the COVID-19 pandemic, which was when the labor market suffered most. Figure 2 shows how the increase in real GDP in Louisiana of +1.4% in Q1:2023 ranked 31st in the country to $289.9 billion, after an annual decline in economic output by -1.8% in 2022 which was the second worst in the country.  The BEA also reported that personal income in Louisiana grew at an annualized pace of +6.2% (ranked 27th) to $258.5 billion in Q1:2023 (above +5.1% U.S. average). There was personal income growth of 0.0% in 2022, ranking 50th of the states.

Bottom Line: Louisiana’s economy is weak when it comes to the labor market; economic growth and reforms can unleash the potential of Louisianans and make the state more competitive.

Originally posted at Pelican Institute. |

Vance Ginn, Ph.D.

|

RSS Feed

RSS Feed

Proudly powered by Weebly