|

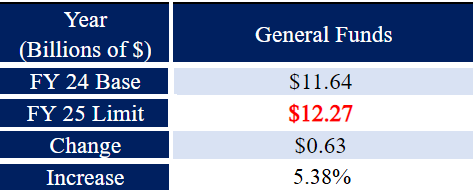

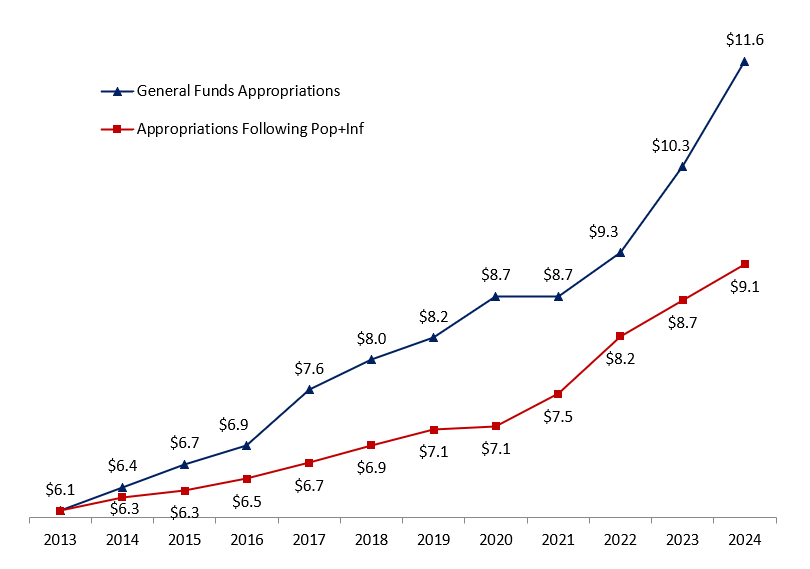

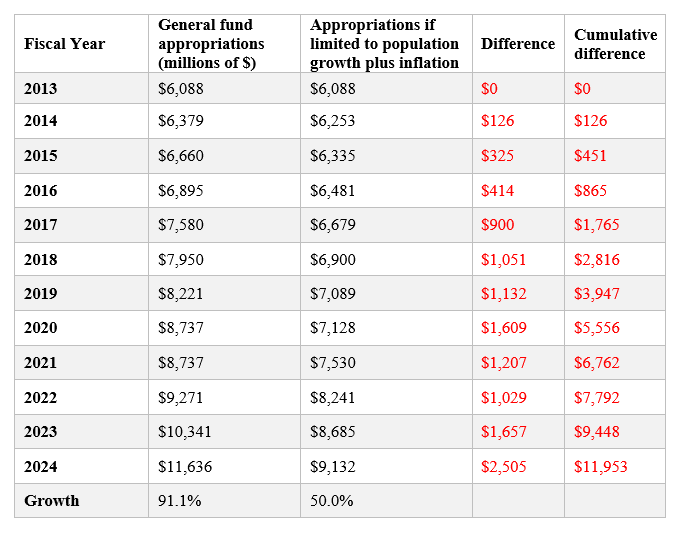

Originally posted at South Carolina Policy Council. Thanks to a robust state economy, plentiful business opportunities, and a relatively low cost of living, South Carolina remains one of the fastest-growing states in the nation. To maintain this strong position and promote further growth, it is crucial for S.C. legislators to limit state spending and reduce the government’s burden on taxpayers. The S.C. Policy Council created the South Carolina Sustainable Budget (SCSB) to assist in this effort. The SCSB is a maximum limit on annual recurring general funds[1] appropriations based on the rate of state population growth plus inflation. First published in 2022 and again in early 2023, it has served as a data-driven resource to help rein in unsustainable spending and provide more opportunities for tax relief. Unfortunately, the state did not adhere to the SCSB limit of $11.20 billion for its fiscal year (FY) 2024 budget; instead, it appropriated $11.64 billion – a 12.56% increase above the FY23 base of $10.34 billion. To turn the tide of excessive budget growth and provide more room for tax relief, the Policy Council is issuing its third SCSB. Table 1 provides the results outlined in this report for the FY25 SCSB. Table 1. The FY25 South Carolina Sustainable Budget for Appropriations of Recurring General Funds  Based on population and inflation data in 2023, the recommended recurring general funds appropriations limit[2] for South Carolina’s FY25 budget is $12.27 billion. With inflation moderating somewhat since reaching a 40-year high in 2022, primarily because of the errant policies in D.C., the SCSB ceiling is higher than it would be under normal economic circumstances. For example, the average annual rate of population growth plus inflation since 2013 has been 3.78%. Accordingly, the S.C. Legislature should consider freezing spending at the current FY24 budget of $11.64 billion. This would help correct recent overspending in the state’s budget and help put the state on a more sustainable budget path. It would also leave more money available for needed tax relief. At a minimum, recurring general fund appropriations in the FY25 budget must remain below $12.27 billion. Overview A sustainable budget – sometimes called a conservative or responsible budget – is a model for state budgeting that sets a maximum limit on appropriations or spending based on the rate of population growth plus inflation. This metric serves as an indicator of what the average taxpayer can afford to pay for government provisions. It accounts for 1) More people in the state who could potentially pay taxes; 2) Wage growth that’s typically tied to inflation over time to pay taxes; and 3) Economies of scale, as not every new person or wage increase should be associated with new government spending. The SCSB does not make specific recommendations on how general funds should be appropriated in the budget. Instead, it gives legislators the flexibility to appropriate taxpayer dollars to government programs as determined by the General Assembly, while ensuring that spending growth remains in line with what people can afford. Such a voluntary spending limit is key to putting South Carolina in a position for further tax relief. In 2022, Gov. Henry McMaster and lawmakers enacted the first-ever state personal income tax cut, which immediately reduced the top rate from 7% to 6.5% and collapsed the lower bracket to 3%. It also scheduled additional yearly 0.1% cuts to the top rate until it reaches 6%, though general fund revenues must project at least 5% annual growth for the cuts to trigger. The problem with this approach is that it relies on continued revenue growth to deliver incremental tax relief. Following the SCSB would help to accelerate this process, freeing up revenue to buy down the top rate to 6% immediately and fueling other tax cuts. On the other hand, unsustainable spending could build pressure to reverse course and raise taxes, leaving South Carolinians with fewer opportunities to flourish. SC Appropriations vs. Sustainable Budget Figure 1 compares the previous twelve years[3] of South Carolina’s recurring general fund budget appropriations (FY13 to FY24) to those appropriations when limited each year to the rate of population growth plus inflation. Figure 1. South Carolina General Fund Appropriations v. SCSB 12-year GF appropriations: $98.5 billion (+91.1%) 12-year GF appropriations limited to population growth + inflation: $86.5 billion (+50.0%)  Notes. Budget amounts are based on data from South Carolina’s state budget publications, Fed FRED for state population growth and U.S. chained-CPI inflation, and authors’ calculations. Appropriations did not increase from FY20 to FY21 because the state operated on a continuing resolution in FY21.[4] Key takeaways (see Table 2):

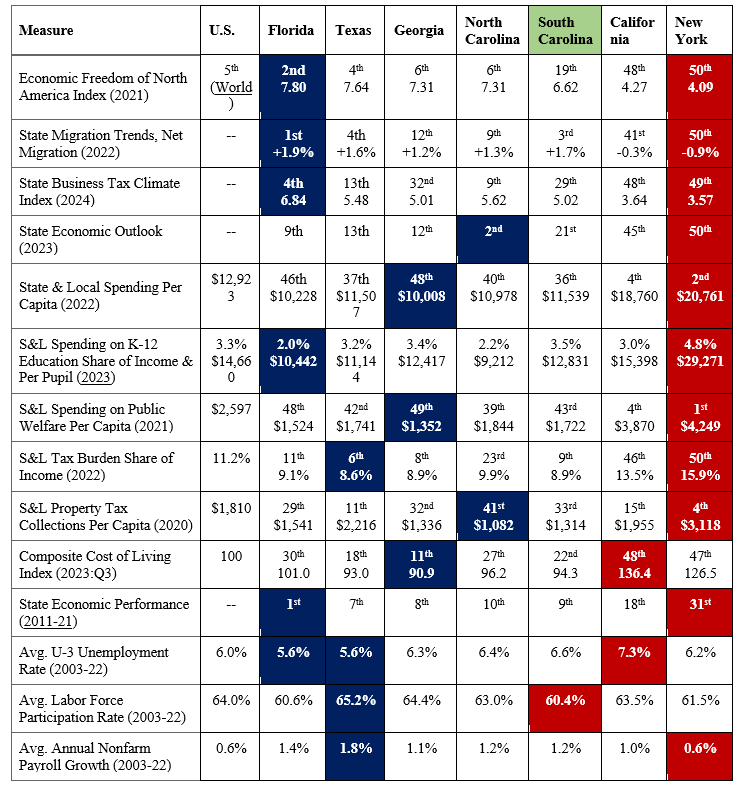

Note. Budget amounts are based on data from South Carolina’s state budget publications, Fed FRED for state population growth and U.S. chained-CPI inflation, and authors’ calculations. These data provide clear evidence that there is room for the state to limit spending growth to reduce taxes substantially. South Carolina has been one of the 25 states in the last three years to cut income taxes, which has helped the state improve compared to its neighbors. However, North Carolina recently passed legislation that could eventually bring their income tax rate to 2.49%, which would be the lowest in the country, excluding the seven states without personal income taxes. On that list are Florida and Tennessee, two major competitors for jobs and investment in the Southeast. South Carolina could improve its position by passing sustainable budgets and using the surplus revenue to cut taxes, especially income taxes. See Table A in the Appendix for more comparisons of South Carolina with other states. Follow the SC Sustainable Budget We strongly encourage legislators to follow the SCSB when drafting South Carolina’s FY25 budget. As a data-driven resource, the SCSB sets a clear spending limit based on what the average taxpayer can afford to pay for government services. Surpassing this limit will fuel excessive government growth and promote unsustainable spending, leaving less revenue that can be used to lower taxes. Recent budget projections show a historic opportunity for tax relief – if legislators are willing to take it. In its November 2023 forecast, the S.C. Board of Economic Advisors (BEA) estimates a recurring budget surplus of $673.1 million for FY25. It also projects the cost of lowering South Carolina’s top personal income tax rate from 6.4% to 6.3% to be roughly $100 million (which is accounted for by BEA prior to their $673.1 million projection). Based on current data, we estimate[1] it would cost an additional $300 million in revenue to cut the top rate immediately to 6% in the new budget. Accordingly, this all-at-once cut could be achieved using less than half of the projected recurring surplus. Passing a sustainable budget would be easier if state agencies followed South Carolina’s legal budget process. Under current law, agencies are supposed to justify every dollar they are requesting when submitting their annual budget plans to the governor – explaining why both new and current programs deserve taxpayers’ money. The law follows a concept known as zero-based budgeting, where all expenses need to be justified annually based on need and performance without regard to previous budgets. Despite this legal mandate, agencies only provide details for new spending requests each year. Fortunately, South Carolina is decently prepared for a rainy day should it occur. Voters in 2022 approved two amendments to increase contributions to the state reserve funds – raising the General Reserve Fund from 5% to 7% (over several years) and the Capital Reserve Fund from 2% to 3% of the previous year’s general fund revenue. By law, the reserve funds act primarily as a shield against year-end budget deficits. While these reserve funds are important to withstand volatility in the budget, lawmakers should focus on limiting or cutting the budget for it to be sustainable over time. Conclusion Following the SCSB will put South Carolina in a better position to reduce taxes, avoid the cost of excessive government growth, and give citizens more opportunities to flourish. Had this been done since 2013, the state could have substantially lowered personal income taxes, if not eliminated them. Fortunately, the upcoming budget provides state leaders with another crucial opportunity to rein in spending and deliver much-needed relief. South Carolina taxpayers are counting on it. Appendix: How Does South Carolina Compare with Other States? Table A shows how South Carolina compares with the largest four states in the country (i.e., California, Texas, Florida, New York) and neighboring states (i.e., Arkansas and Mississippi) based on measures of economic freedom, government largesse, and economic outcomes. Table A. Comparison of States for Measures of Economic Freedom and Outcomes  Notes. Dates in parentheses are for that year or the average of that period. Data shaded in blue indicate “best,” and in red indicate “worst” per category by state.

These rankings show that South Carolina is better than most states in terms of economic freedom, but is substantially less economically free than its neighbors of Georgia and North Carolina. South Carolina does better than others in this comparison in terms of having the lowest supplemental poverty rate and near the best in net migration. South Carolina has the highest state and local government spending per capita among its neighbors and a substantially worse business tax climate than North Carolina. The data show that states with less economic freedom (e.g., New York, California, and South Carolina) tend to perform economically worse. On the other hand, those states with more economic freedom (e.g., Florida, Texas, Georgia, and North Carolina) tend to perform economically better. Given these comparisons, South Carolina has much room for improvement to be more competitive and, more importantly, provide more opportunities for human flourishing.

0 Comments

Leave a Reply. |

Vance Ginn, Ph.D.

|

RSS Feed

RSS Feed

Proudly powered by Weebly