|

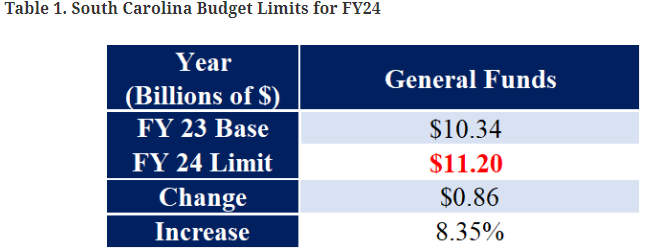

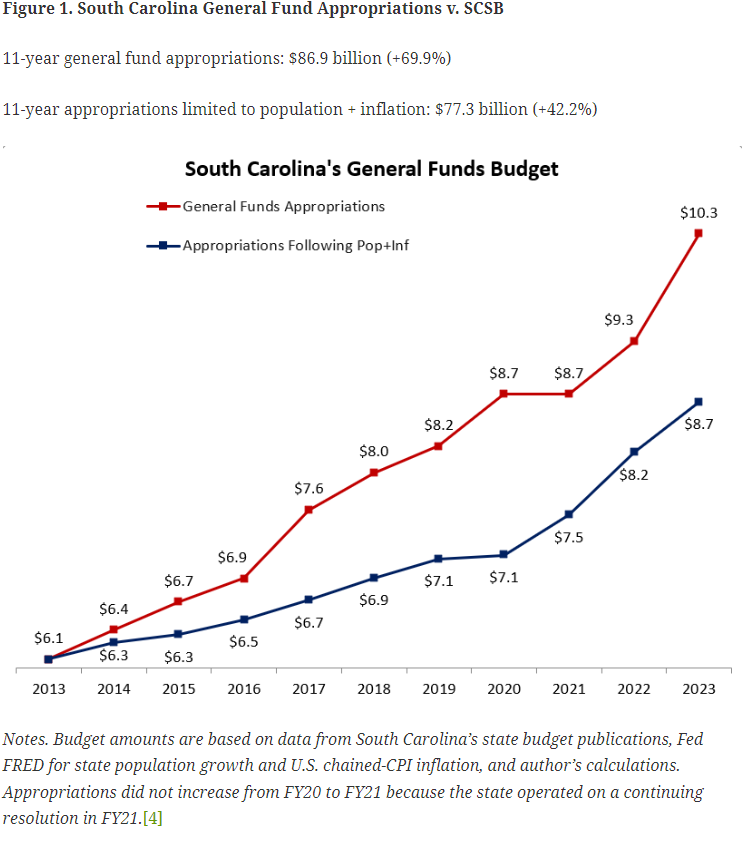

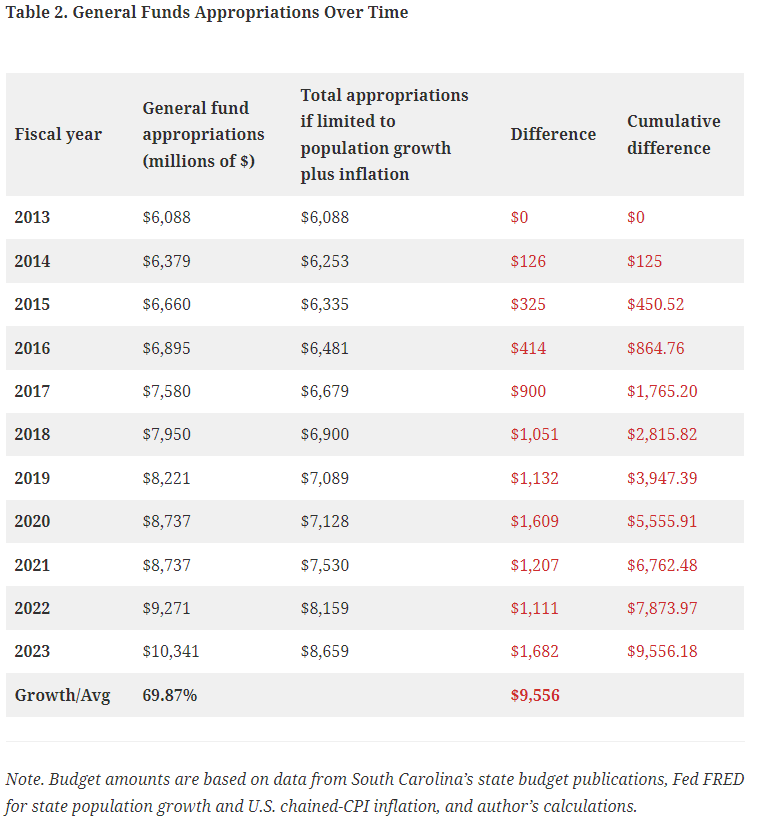

South Carolina is getting on the right track when it comes to fiscal responsibility. In 2022, state lawmakers and Gov. Henry McMaster enacted the first-ever state personal income tax cuts, letting residents keep more of their hard-earned money and making South Carolina more competitive for business. Last year, voters also approved ballot measures requiring the state government to set more money aside in the event of an economic downturn. The next step is to get state spending under control, which can be achieved by following the Policy Council’s South Carolina Sustainable Budget (SCSB). The SCSB provides a limit for annual general funds[1] appropriations using data based on the rate of state population growth plus inflation. This report provides appropriations recommendations for fiscal year (FY) 2024 and compares recent state appropriations with what spending would have looked like under a sustainable budget.  Based on population and inflation data in 2022, the recommended general funds appropriations limit[2] for South Carolina’s FY24 budget is $11.2 billion. However, with inflation reaching a 40-year high, primarily because of the errant policies in D.C., this spending ceiling is higher than it would otherwise be under normal economic circumstances. Accordingly, the S.C. Legislature should consider freezing spending at the current FY23 budget amount of $10.34 billion. This would help to correct recent overspending seen in South Carolina’s budget and put our state on a more sustainable path. At a minimum, general fund appropriations in the FY24 budget must remain below $11.2 billion. Overview A sustainable budget, sometimes called a conservative or a responsible budget, is a model for state budgeting that limits appropriations based on population growth plus inflation. This metric serves as an indicator of what the average taxpayer can afford to pay for government provisions. In particular, it accounts for: 1) More people in the state who could potentially pay taxes, 2) Wage growth that’s typically tied to inflation over time to pay taxes, and 3) Economies of scale, as not every new person or wage increase should be associated with new government spending. The SC Sustainable Budget does not make specific recommendations on how general funds should be appropriated. Rather, it gives legislators the flexibility to appropriate taxpayer dollars to government programs as determined by the General Assembly while ensuring that spending growth remains in line with what people can afford. Such a voluntary spending limit is key to putting South Carolina in a position for further tax relief. In 2022, lawmakers cut and simplified our state personal income taxes – a policy supported by the Policy Council – and set up a trigger for additional, smaller cuts in the future. But smart budgeting will help accelerate the process of reducing income taxes and fuel other tax cuts. Unsustainable spending, on the other hand, could build pressure to reverse course and raise taxes, leaving South Carolinians with fewer opportunities to flourish. SC Appropriations vs. Sustainable Budget Figure 1 compares the previous eleven years[3] of South Carolina’s general fund appropriations (FY13 to FY23) to general fund appropriations if limited to the rate of population growth plus inflation, with the following results:  Key takeaways (see Table 2):

Follow the sustainable budget

As legislators begin working on South Carolina’s next budget, we strongly encourage them to follow the SCSB, which establishes a spending limit based on what the average state taxpayer can afford to pay for government services. The SCSB does not instruct lawmakers how to spend funds, rather its purpose is to keep overall spending from rising too quickly. Such budgetary restraint will be vital going forward. In its November 2022 report, the S.C. Board of Economic Advisors forecasted $12.3 billion in general fund revenue for FY24, with expected revenue for FY23 being $12.5 billion – a 1.3% decline. Moreover, the FY23 revenue estimate is 8.7% less than actual revenues of $13.7 billion for FY22. If these estimates materialize, it will mark an end to years of major growth in state revenue collections. The good news is that South Carolina is already taking steps to prepare for a rainy day. Voters recently approved two amendments to increase contributions to the state reserve funds – raising the General Reserve Fund from 5% to 7% and the Capital Reserve Fund from 2% to 3% of the previous year’s general fund revenue. By law, the reserve funds act primarily as a shield against year-end budget deficits. By doubling down on smart policy and following the SCSB, our state will be in a much stronger position to cut taxes, avoid the tremendous cost of unchecked government growth, and allow citizens to prosper and reach their fullest potential. Originally posted by South Carolina Policy Council.

0 Comments

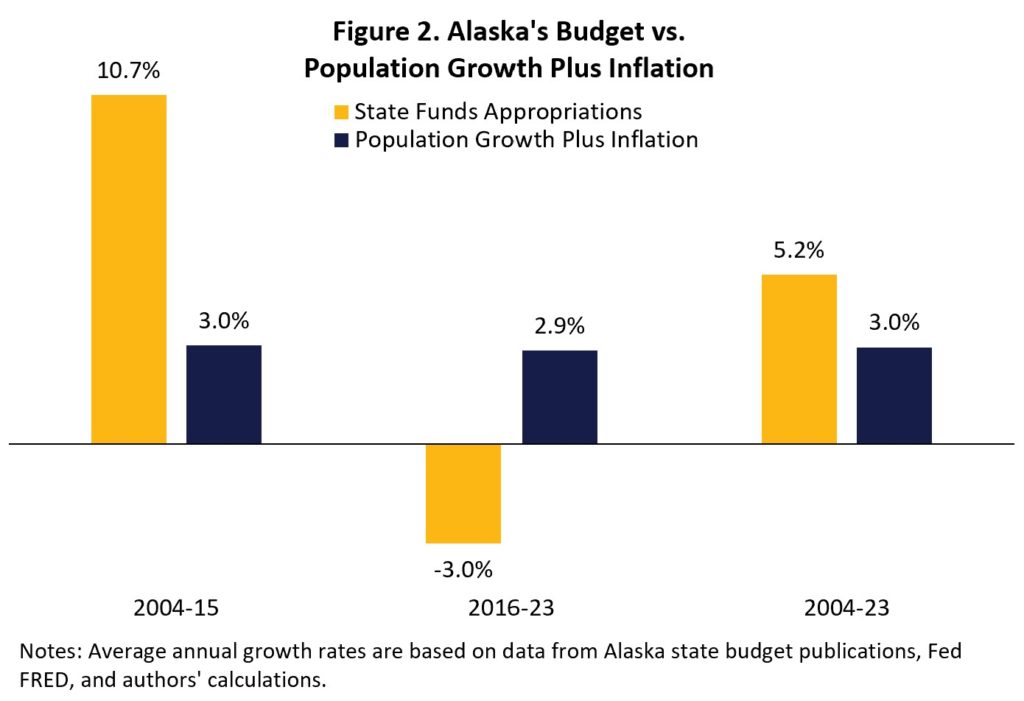

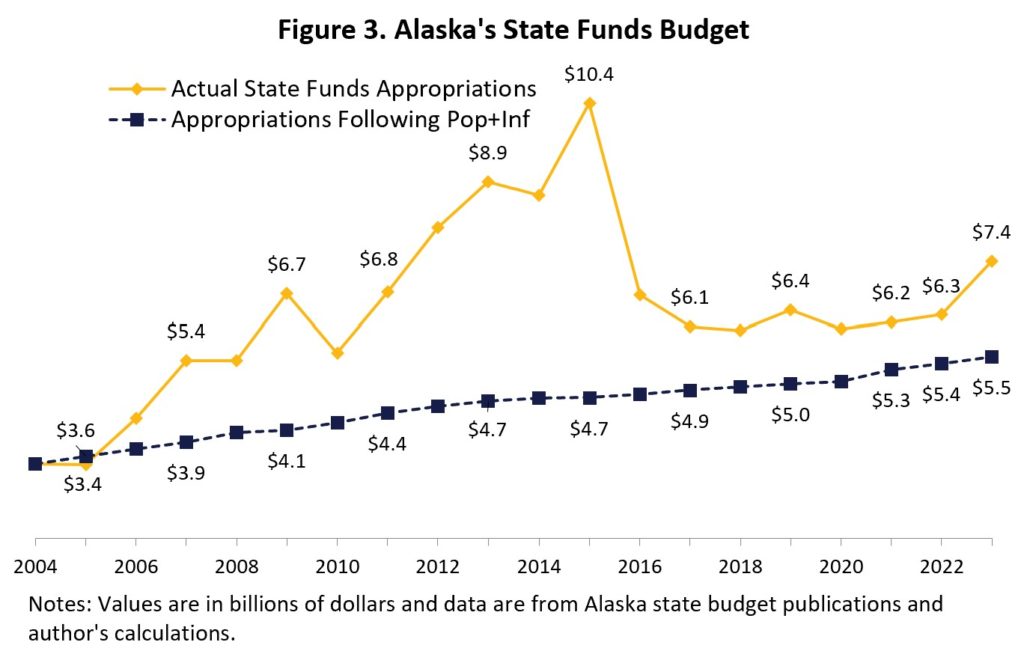

By Vance Ginn and Quinn Townsend Introduction While revenue estimates for the state of Alaska hit a record high last fiscal year, this upcoming fiscal year 2024 (July 2023 – June 2024) is another story. The Fall 2022 revenue forecast is much lower than it has been in previous years. Now more than ever, Alaskans need policymakers to show fiscal responsibility and restraint as they congregate in Juneau to discuss the next state budget. To that end, a responsible budget should not exceed $7.71 billion in state funds. Alaska Policy Forum is releasing its third annual Responsible Alaska Budget (RAB), now for FY 2024, to help effectively limit state spending and restrain the growth of government. The RAB represents a strong fiscal rule in the form of a spending limit which should be passed and added to the state’s constitution as a meaningful appropriation limit. Fiscal restraint allows the state to prioritize the needs of Alaskans without excessively growing the size of government, thus limiting the burden on the private sector where productivity advances improve opportunities for Alaskans to prosper today and for generations to come. There is a need to overcome the economic challenges the state is experiencing and the extravagant spending from 2004 to 2015 in Alaska. The RAB is an essential maximum limit for policymakers this session, and the actual budget should be well below it to help Alaskans deal with economic challenges and to correct past budgeting excesses. Responsible Alaska Budget Calculation The FY 2024 RAB sets a maximum threshold on the upcoming state appropriations based on the summed rate of the state’s resident population growth and inflation, as measured by the U.S. chained-consumer price index (CPI), over the year before the legislative session. This threshold is an upper limit for the enacted budget for all state funds, excluding federal funds, the Permanent Fund Dividend (PFD), and fund transfers. The calculation is found using the growth rate of Alaska’s resident population and adding it to the growth rate of the U.S. chained-CPI. In 2022, the U.S. chained-CPI inflation increased by 4.97%, and Alaska’s population growth declined 0.10%. The sum of these values, an increase of 4.87%, serves as the maximum growth rate for state funds appropriations in FY 2024. With a base approved state funds budget of $7.35 billion in FY 2023, Figure 1 shows that the FY 2024 RAB is a maximum of $7.71 billion. It should be noted that due to reporting consistencies, APF is now using the official budget numbers from the Office of Management and Budget rather than the Legislative Finance Division, resulting in a slightly different calculated FY 2023 RAB than what we published in 2022. And we are using chained-CPI inflation now to account for the substitution effects by consumers who choose different goods and services when there are changes in prices, which are not accounted for with just CPI inflation. The FY 2023 enacted budget was $7.35 billion — $800 million more than the published FY 2023 RAB threshold of $6.55 billion, meaning it was an irresponsible budget. This should be corrected in the FY 2024 budget. Due to higher price inflation over the past year across the country and a decrease in the state’s resident population, the FY 2024 RAB accounts for these with a ceiling growth rate of 4.87% which essentially freezes inflation-adjusted state funds appropriations per capita. In addition to high inflation, Alaskan policymakers will also be struggling with a low revenue forecast, due in part to decreased oil prices and oil production. Alaska’s Department of Revenue estimates an FY 2024 revenue of $10 billion (excluding federal funds), which does include revenue for the Permanent Fund Dividend, an appropriation we do not include in our maximum threshold calculation, as well as state restricted funds. A responsible budget passed by policymakers will take this into consideration, while not relying on the state’s savings accounts. Instead, limiting the growth of government spending to keep more money in the productive private sector will support increased opportunities for Alaskans to achieve their hopes and dreams while helping those struggling to gain the dignity of work by earning a living. Historical Budget Trends Figure 2 shows Alaska’s budget trends since FY 2004. During the period from 2004 to 2015, the average annual budget increased by almost 11%, which was nearly four times faster than the key metric of the rate of population growth plus inflation. Since then, the budget has declined annually by 3%, on average, while the rate of population growth plus inflation increased by about 3% from 2016 to 2023. This means that policymakers have done a better job budgeting in the last several years but there is more room for improvement. Additionally, these budget numbers are only the enacted budgets, not total state spending. Unfortunately, Alaska has a history of relying heavily on supplemental spending, which is above and beyond the enacted budget.  From FY 2004 to FY 2023, the budget grew on an average annual basis by 5.2%, which was substantially higher than the average 3% rate of population growth plus inflation. Figure 3 illustrates state funds appropriations over this period and the appropriations that would have happened if they had followed the rate of population growth plus inflation each period.  The budget growth excesses in the earlier period (2004-15) have compounded over time even with the improved budgeting since 2016 to lead a much larger budget over time. This results in state funds budgeted for FY 2023 $1.8 billion more than what would have been spent, which translates to the state spending an additional $2,500 per Alaskan. Or, if you take the cumulative differences between the actual budget and those if policymakers followed the rate of population growth plus inflation, the cumulative difference is $37.3 billion in overspending over time, which translates to excessive government spending of $50,000 per Alaskan. This excessive spending has resulted in a bloated state government that reduces private sector economic activity and opportunities for people to prosper.

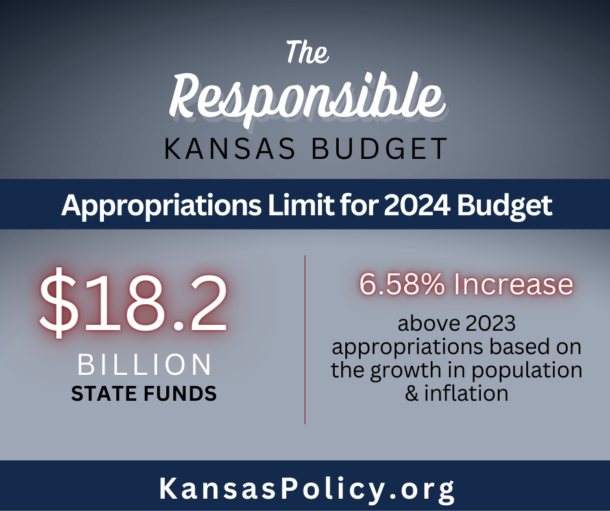

Conclusion Alaska Policy Forum’s FY 2024 RAB sets a maximum budget threshold that will help bring the state budget in check with state appropriations of less than $7.71 billion, representing a 4.87% increase based on the rate of population growth plus inflation in 2022. Working to enact a budget less than this maximum amount, particularly considering the low revenue forecast, past budget excesses, and economic headwinds, will help immensely in reducing the cost of funding limited government. Policymakers should pass an FY 2024 budget that is less than the Responsible Alaska Budget and put this spending limit in the constitution. Doing so will move the Last Frontier into the future, with a strong, steady economy and a vibrant population with opportunities for all Alaskans to flourish. Originally published at Alaska Policy Forum.  Here is The Responsible Mississippi Budget 2024 which I wrote for the Mississippi Center for Public Policy's President & CEO Douglas Carswell who wrote this to go along with the report. Mississippi recently made some significant tax cuts. Thanks to the 2022 Mississippi Tax Freedom Act, over a million Mississippi workers will be better off as the state income tax rate is reduced from around 7 percent to a flat 4 percent. In the coming legislative session, Mississippi lawmakers have to set a budget for 2024. Some will call for further tax cuts. Others will insist that we cannot afford tax cuts. What should conservative lawmakers do? To help authentic conservatives in our state, the Mississippi Center for Public Policy has published a responsible budget for our state. The key to setting a responsible budget, as every householder knows, is to get control of what we spend. We believe that Mississippi’s government spending (general fund appropriations) for 2024 should not exceed $6.75 billion. To increase spending over and above that amount would mean raising spending per person in our state faster than inflation. That would be un-conservative. When setting a budget, conservatives that are serious about limiting the size of government ought to follow a simple fiscal rule; any increase in government spending should not exceed the rate of population growth plus inflation. Before drafting our budget, we took a look at Mississippi government spending over the past decade or so. Unfortunately over the past decade state government spending (the general fund appropriations) has tended to grow rather rapidly. Between 2014 and 2019, state government spending grew faster than population change plus inflation, meaning that the relative size of the state government in Mississippi increased. The good news, however, is that since 2020 the expansion of the state government in Mississippi has slowed. Spending growth over the past three years has not exceeded changes in population plus inflation. Genuinely conservative lawmakers should aim to keep things that way in 2024, and not exceed $6.75 billion in spending. If lawmakers set a responsible budget that keeps control of spending, we estimate that there will be a budget surplus of around 800 million in 2024 – a portion of which could be used to reduce the tax burden yet further. During the last legislative session, a number of lawmakers argued that we could not afford to cut taxes. If we were not careful, they claimed, we could end up like Kansas. Kansas did indeed once cut taxes, before having to raise them again when the money ran out. But the money only ran out in Kansas because they failed to get control of spending first. Here in Mississippi, provided we limit the general fund appropriation to $6.75 billion, there will be not just a surplus, but a sustainable surplus that can be used to cut taxes. We believe that Mississippi’s budget surplus is both cyclical and structural. That is to say the surplus will not simply disappear as and when the economy slows. Provided Mississippi lawmakers keep spending under control there will be money left over to reduce taxes. Over the past few decades, the southern United States has flourished. Tennessee, Texas, Georgia and Florida have enjoyed rapid growth. Dallas and Nashville have become go-to places for ambitious young people right across America. Why are these southern states doing so well? Because they tend to be run by people who appreciate the importance of low taxes and light regulation. While those that run New York, Chicago and California have raised taxes and red tape, driving businesses away, the south has gone in a very different direction. Mississippi could be part of this southern success story too – provided we continue to cut taxes. A responsible budget for 2024 that carefully controls spending would be another big step in the right direction. Douglas Carswell is the President & CEO of the Mississippi Center for Public Policy. The Responsible Budget for Mississippi can be read HERE.  Last year, Kansas Policy Institute released its first edition of the Responsible Kansas Budget (RKB) for 2023. This model for accountable, sustainable budgeting proposed a limit on All Funds (state funds plus federal funds) appropriations in 2023 at $21.0 billion based on limiting spending increases to the combined rate of population growth and inflation. Instead, the Legislature approved an All Funds budget of $22.9 billion – nearly $2 billion more than the RKB. While the RKB is determined by previous years of appropriations, it isn’t a justification for that spending – and in fact, there was likely waste or things that could have been approved previously. This year, the RKB returns, but with a new focus on State Funds instead of All Funds. This is because State Funds more accurately represent the spending under the direct control of Kansas’s government. for 2005 to 2023, state funds appropriations have increased by 138.1%, from $7.2 billion to $17.1 billion, for an average annual increase of 5.2%. The 2024 Responsible Kansas Budget (RKB) sets a maximum threshold on the State Funds budget based on the rate of population growth and inflation during the prior year before a legislative session. This is a simple calculation of finding the growth rate of the state’s resident population and adding it to the growth rate of the US chained-CPI. In 2021, the US chained-CPI inflation increased 7.18%, and Kansas’s population growth declined 0.60%. The sum of these values, an increase of 6.58%, serves as the maximum growth rate for SGF appropriations in 2024. With a base approved State Funds budget of $17.1 billion in 2023, the 2024 RKB is a maximum of $18.21 billion. Efficiency is key to hitting the RKB’s limits: there’s potential everywhere in government to reduce costs while still providing the same service. One tool to do this is performance-based budgeting, a review system in which each program submits goals and outcome measures related to how well they are succeeding in those goals. Kansas has performance-based budgeting, yet the first report released in December 2021 was half-hearted, difficult to interpolate from, and indicative of hundreds of millions of dollars going to programs with little accountability. A KPI report on performance-based budgeting will be released Thursday of this week. 2022 showed how unpredictable the economy could be, with inflation harming thousands of families across the state. Many of the issues driving inflation are out of the hands of Kansas legislators. And yet, government spending is directly in the hands of our elected officials and could be a small way to help families currently feeling the squeeze of inflation. Responsible budgeting is a way that local leadership can shore up their governments and economies to withstand downturns. Low spending means low taxation and lower regulation, which gives people and businesses more room to flourish. View the 2024 Responsible Kansas Budget in our report below. Originally published at Kansas Policy Institute.  The 2024–25 Conservative Texas Budget limits the state’s budget to be passed by the Legislature in 2023 so that the average taxpayer can afford it and historic tax relief can happen. Key points

Original post at TPPF.  Many cities across the nation are facing a fiscal crisis. While pandemic-related problems that were self-induced or otherwise play a part, many of these issues have plagued cities for a long time. A serious cultural shift concerning finances among local governments is critical if people want to flourish in cities.

I recently interviewed Mark Moses who is a municipal government expert and author of the recently published book The Municipal Financial Crisis: A Framework for Understanding and Fixing Government Budgeting. He contends that “many local governments are on track for bankruptcy.” And this downward trajectory can be expected to continue as municipalities fail to restrain their spending and overreach, crowding out opportunities for the private sector to work. We’re seeing this play out in places like New York City, where city-funded expenses have been asked to be cut by 3% and on track to be slashed more in response to their recently reported $10 billion deficit. Moses says that “there’s a lack of economic understanding in lots of municipalities.” This absence of understanding often results in collecting more taxes to fund more “solutions” as a band-aid to the broken system and struggling local finances. As he puts it, “local governments give up trying to balance budget sheets.” But failing to assess and address the tangled economic approach that’s led them to a place where more taxes and regulations seem like the only answer leads to long-term issues and a path that’s difficult to leave. Local governments must limit their scope and focus on core issues. That means letting new initiatives and departments take a back seat while they get spending under control. This is difficult, however, especially after the 2021 American Rescue Plan Act that gave $45.6 billion to municipalities, which temporarily and artificially inflated local finances. More money under lousy management is a weak fix. And now, with rising inflation and energy costs, these municipalities are ill-equipped to thrive in a recession that wasn’t helped by the huge bailout package. A good start to overcoming these challenges would be to get government out of the way in most cases so that the the private sector can solve key issues, which has proven to be the best antidote for most problems throughout history. Overinflating their role instead of sticking to limited governing, such as property rights and a few public goods, is a trap that many cities fall into and that comes at a huge cost. But philanthropic and other private-led solutions tend to be crowded out through higher taxes and regulations when city hall makes promises they can’t fulfill. Moses describes this as municipalities “seeing themselves as an end to themselves,” which is why many local governments resist spending limits or find ways around them. This is an ongoing issue in Texas which is contributing to an affordability crisis. Texas is blessed to have constitutional amendments against state-controlled personal income taxes or property taxes, so all property taxes are local in Texas. While there have been attempts recently by the state to limit their growth, property taxes have increased by 169% in the past 20 years compared with an increase of 104% in the rate of population growth plus inflation. This indicates that property taxes are growing well above the average taxpayer’s ability to pay for them. Some argue that Texas has high property taxes because it has no personal income taxes. But the reality is that it is really from excessive local government spending. For example, Texas has the 6th most burdensome residential property tax according to the Tax Foundation but other states without a personal income tax like Florida and Tennessee rank 26th and 36th, respectively. This is because the latter two states do a better job restraining spending. The best way to get budgets and taxes back on a fiscally conservative track is through a strict spending limit that covers the entire budget and grows no more than the rate of population growth plus inflation. This would help cities, and all local governments, stick to just addressing what’s in their purview. A city’s scope shouldn’t be evaluated from one council meeting to the next but should be assessed in the long term if its local government hopes to see future success and a prosperous economy. The same principles of economic success apply to all government institutions; people flourish where liberty is preserved, and that’s best achieved under limited government whereby politicians’ interventions remain inside their limited scope so that free markets and free people can innovate and thrive. Just as we’re witnessing with this recession, there’s always a trade-off to overspending and unbalanced budgets. The sooner local governments realize that and reel in their spending, which is the ultimate burden of government, the sooner financial crises will be averted. Originally published at EconLib  Americans are facing a housing affordability crisis—and Texans are no exception.

Texas families struggle to make ends meet with high inflation, stagnating wages, and rising mortgage rates. Add high property taxes to the equation, and it is not difficult to see why 1-in-2 Texans reported that they were behind on rent or mortgage payments and that eviction or foreclosure in the next two months is likely. Property tax relief is needed more than ever to help homeowners, renters, and businesses during these challenging times. For this purpose, the Foundation proposes a way to cut local property taxes substantially next year, and cut them nearly in half over the next decade. In Texas, the housing market is cooling as there were three months of supply of homes for sale relative to demand in September 2022, which is the highest since May 2020 after a couple of years of a very tight housing market. This cooling of the housing market resulted from mortgage rates topping 7%, a 20-year high that dramatically raises borrowing costs and monthly payments. Another contributing factor to the affordability crisis in Texas is high and rising local property taxes. Texas is blessed to have constitutional bans against a personal income tax and a statewide property tax. But while Texas has a costly gross receipts-style tax called a franchise tax, which should be eliminated, the most burdensome taxes discussed during soccer practices or business events are local property taxes. These taxes have nearly tripled over the past 20 years. And it’s wrong to think that property taxes are high because there is no personal income tax, as other states like Florida and Tennessee have much lower property tax burdens. The problem is excessive local government spending that requires more taxes. Property taxes are regressive. The Texas Comptroller’s office estimates that the lowest 20% of income earners will pay 6.9% of their total income in property taxes compared with 1.9% for the highest income quintile in 2023. Moreover, the Tax Foundation ranks Texas 11th in property tax collections per capita, 6th for its burden on homeowners, and 13th most burdensome to businesses, which is ultimately passed to consumers. Consequently, property tax relief is a top priority to help relieve some of the housing affordability issues. Reducing property taxes for Texans would keep more money in their pockets to satisfy their desires during a rising affordability crisis. To do so, the Foundation proposes eliminating nearly half of total property taxes. The proposal uses state general revenue-related funds to replace the maintenance and operations (M&O) property taxes partially funding independent school districts (ISD), which is about $60 billion per biennium. Specifically, most, if not all, surplus general revenue-related funds, which the Legislature has the most control over, above the state’s new state spending limit based on the rate of population growth plus inflation would be used to replace the ISD M&O property taxes each period until they’re eliminated. We calculate that this could happen in a decade. We use the average two-year growth rates over the last decade from 2012 to 2021, given that the state has a biennial budget for general revenue-related funds of 9.3% and a rate of population growth and inflation of 6.7%. We then use a reasonable 90% of this 2.6-percentage points surplus each biennium and half of the latest 2022-23 surplus of $27 billion to find this is achievable while fully funding public schools based on the current state-determined school finance formulas. With a record $27 billion expected surplus and another $14 billion likely in the state’s rainy day fund, the state has plenty of taxpayer money to fund limited government provisions within the normal taxes collected while returning surplus money to Texans. This is a historic opportunity to provide substantial property tax relief and more opportunities for businesses to move to Texas without costly incentive deals. The result would be Texas having a more robust economy, more job creation, more investments, and more opportunities to prosper so that Texans can be more able to afford their desired livelihood. Originally posted at TPPF  A nation emerging from a significant pandemic and an economic downturn awaited President Joe Biden in early 2021. President Warren G. Harding inherited a similar situation after winning the 1920 election in a landslide. But Harding overcame it by getting government out of the way. The economy recovered quickly—whereas Biden enacted bad progressive policies that have resulted in a double-dip recession with 40-year high inflation.

Biden should learn from Harding and his successor President Calvin Coolidge to correct government failures and allow markets to heal so that we can enjoy abundant economic prosperity again. In the aftermath of the Great War, the U.S. suffered a severe economic downturn. The late economist Milton Friedman described this as one of the most “severe on record.” The depression of 1920-1921 is often forgotten because it was short-lived, but it offers policy lessons that can be applied to our current situation. Prior to and during the Great War, President Woodrow Wilson led a massive expansion of the federal government, which included the creation of the Federal Reserve and personal income tax system. After the war, markets corrected from those government failures throughout the economy triggering a steep economic downturn. The business and agriculture sectors were hit particularly hard by the depression of 1920-1921, which led to bankruptcies and farm foreclosures. Unemployment was estimated to be about 12% and the nation was hit buffered from deflation. Americans were hurting. During the presidential campaign of 1920, then-Sen. Warren G. Harding pledged a “return to normalcy” against Wilson’s progressivism. During the campaign, Harding argued that the nation needed to return to sound money, less spending, lower taxes, less debt, and limited government. This was the fiscal policy blueprint of the “normalcy” agenda. Harding understood that to revive business confidence and lower high income tax burdens, the federal government must get its fiscal house in order. In 1921, Congress passed the Budget and Accounting Act, which under the leadership of Bureau of the Budget Director Charles Dawes and later his successor, Herbert Lord, worked to reduce federal spending. Dawes would compare the task of cutting spending to having a “toothpick with which to tunnel Pike’s Peak.” Harding also understood that to lower the high tax rate, spending had to be addressed first. “The present administration is committed to a period of economy in government…There is not a menace in the world today like that of growing public indebtedness and mounting public expenditures…We want to reverse things,” explained Harding. Reducing spending was not easy. As an example, Harding vetoed a popular bonus for veterans of the Great War. Overall, Harding’s commitment to economy in government resulted in an estimated 50% reduction in federal spending. Harding also relied on Secretary of the Treasury Andrew Mellon, who also shared his views regarding limiting spending. Mellon would serve as the lead architect for Harding’s tax reform policies. The top income tax rate was over 70% and Mellon’s goal was to lower the rate. Through a series of tax reforms, the high rate would eventually be cut to 25% during the Coolidge administration. Harding and Coolidge’s fiscal conservatism of lowering spending and tax rates and paying down the national debt resulted in a quick economic recovery. The Federal Reserve also tightened the money supply. The historian Paul Johnson wrote “Harding had done nothing except cut government expenditure, the last time a major industrial power treated a recession by classic laissez-faire methods…” After the death of Harding in August 1923, Coolidge continued and strengthened the economic policies of Harding. President Coolidge, along with Secretary Mellon, continued to lower spending and tax rates. The federal budget was $3.14 billion in 1923. By 1928, when Coolidge left, the budget was $2.96 billion. Altogether, spending and taxes were cut in about half during the 1920s, leading to faster real economic growth and productivity that contributed to budget surpluses throughout the decade. The decade had started in depression and by 1923 the national economy was booming with low unemployment. And that continued throughout much of the decade. This would have continued but government expanded again. In particular, the Hoover administration ran deficits and raised taxes and the Federal Reserve had too loose and then too tight money supply. This led to the Great Depression—a phenomenon that was avoidable and was exacerbated by President Roosevelt’s large expansion of government. It’s unlikely that President Biden will follow the pro-growth economic policies of Harding and Coolidge, nor will the Fed tighten the money supply enough to reduce inflation. Published at Real Clear Policy with John Hendrickson  With its vibrant cities, relatively cheap cost of living, and thriving industries like manufacturing, healthcare and hospitality, it’s obvious why South Carolina is one of the fastest growing states in the nation. To keep its competitive edge and protect the interests of taxpayers, it is imperative that state government spending – which has seen significant growth in recent years – be brought under control. For that reason, SCPC has partnered with the Texas Public Policy Foundation (TPPF) for a new project: the South Carolina Sustainable Budget. This introductory report compares the last decade of state appropriations with what spending would have looked like under a sustainable budget. A future report will provide sustainable budget spending recommendations for fiscal year (FY) 2024. Published at South Carolina Policy Council with Bryce Fiedler and Video discussion here. Press Release for 7 Publications on Responsible Local Budgets for 7 Cities and Counties in Texas6/29/2022

Nearly every major city and county government in Texas spends well beyond what the average taxpayer can afford, according to a series of new research papers on local government spending by the Texas Public Policy Foundation. As a result, over the last decade the typical family of four has paid thousands of dollars in taxes over what the state considers to be a reasonable increase. (Individual reports linked below) “Major cities and counties in Texas are spending huge sums that are wildly out of step with what many taxpayers can afford to pay,” said Dr. Vance Ginn, TPPF’s Chief Economist and co-author of the series. “The data should be a huge red flag that we are heading toward unsustainable spending growth and tax increases that kill jobs, punish families, and drive people and businesses out of the state.” TPPF defines reasonable spending growth as no more than population growth plus inflation. The state of Texas has followed this spending limit for state budgets for several biennia and officially adopted most of it into state statute in the last legislative session. City and county budgets are currently under no obligation to follow this reasonable spending limit. “Responsible Local Budgets (RLB) would promote efficiency and prudence with taxpayer money, creating less need for higher taxes and fees, but still provide all the funding needed for critical government functions,” said James Quintero, TPPF’s Policy Director for the Government for the People campaign and co-author of the research. “Taxpayers would love to see local governments voluntarily adopt these spending limits, but, as long as cities and counties continue their spending binge, it may be necessary for state lawmakers to impose strict parameters to protect taxpayers.” Over the last decade, Dallas has been the worst offender among cities, spending more than 34% above a responsible spending growth limit. In that time, the average family of four in Dallas paid more than $10,000 in excess taxes. The cities of San Antonio and Austin spent over 16% and 14% higher, respectively, than the average taxpayer’s ability to pay. Spending growth in Texas’ major counties has been eye-popping. Lubbock County’s spending has grown 66% above a responsible limit, Bexar County by 52%, Travis County by 43%, Dallas County by 40%, and Tarrant County by 27%. Only Brownsville spent under the growth limit during the decade. Harris County takes the prize as the worst of all local governments by exceeding a responsible spending limit by 114%. “Now it is time to rein in excessive government spending growth at the local level,” Ginn and Quintero write. “We urge local governments to voluntarily adopt these taxpayer protections. Because some may not, we recommend that the Texas Legislature pass a spending limit for all other local governments that includes all spending from any revenue source, restricts expenditure growth to a maximum of state population growth plus inflation from the prior year, and requires a two-thirds supermajority vote by the local governing body to exceed the limit.” “Limiting the growth of these budgets to population growth plus inflation with the RLBs outlined here will help ensure these localities can be vibrant places for people to prosper.” https://www.texaspolicy.com/press/tppf-local-governments-spending-beyond-the-average-taxpayers-ability-to-pay  Gov. Kim Reynolds and Republican legislative leaders are making tax reform a priority for the upcoming 2022 legislative session. The path to keeping government from excessively burdening people with taxes and allowing for pro-growth tax reform starts with conservative budgeting.

Fortunately, Iowa has been practicing prudent budgeting. Iowa will end the current FY 2021 with a $1.24 billion budget surplus in its general fund, which is substantially larger than last year’s surplus of $305 million. Iowa state leadership deserves credit for their recent prudent spending and tax relief. As a result, Iowa was prepared fiscally for much of the costs related to the government shutdown in response to the COVID-19 pandemic. Truth in Accounting’s Financial State of the States 2021 report ranks Iowa in the top 10 (9 out of 50) of fiscally stable states. In addition, the legislature has been careful to avoid using the billions in COVID-19 related federal funding on ongoing expenses. The $1.24 billion surplus is not a result of these federal dollars, but rather the fiscal conservativism that has spurred economic growth. Nevertheless, policymakers will need to continue this approach to strengthen the state’s improving fiscal foundation by keeping spending from excessively burdening taxpayers to provide needed tax relief. This is a reason that the Iowans for Tax Relief (ITR) Foundation recently released the Conservative Iowa Budget (CIB) for FY 2023. This conservative budget approach helps limit spending by setting a maximum threshold on the state’s general fund based on the rate of the state’s resident population growth plus inflation. Given the 2021 rate of 4.51% and a base of $7.1B, excluding $1 billion provided in tax relief this year, the FY 2023 budget should be less than $7.44 billion. This fiscal rule of a spending limit on the general fund provides a reasonable limitation that essentially freezes inflation-adjusted spending per capita. This helps to lessen the crowding out of private sector activity and helps to stabilize expectations over time. Iowa’s Revenue Estimating Conference (REC) estimated that revenues will increase for both FYs 2022 and 2023. The REC is estimating $8.9 billion in revenue for FY 2022 and $9.1 billion for FY 2023. This projection is a healthy improvement from the previous year. These optimistic projections by the REC make it prudent to continue using budgetary caution to fund only limited roles for government instead of spending every taxpayer dollar. Therefore, it is important to keep spending reined in and will require legislators to prioritize every taxpayer dollar, which is difficult as many special interests will be arguing for either new funding or expansion of their previous allocations. Already public education (K-12, community and technical colleges, and higher education) along with Medicaid comprise 79% of the general fund budget. This creates additional pressure because spending on these items continue to increase and crowd out other priorities. Many families and businesses, especially during the pandemic and now as inflation reduces their purchasing power, must prioritize their spending. Government should also focus on priorities, even more so than families and businesses – because it is not the government’s money. Fiscal rules that limit spending help achieve this goal. While Iowa currently has a 99% spending limit in code, this limitation must be strengthened. The spending limit should be strengthened by passing a constitutional amendment or changing it in the code to be based on a maximum rate of population growth plus inflation. This is an important measure because it accounts for more people paying taxes, higher wages – which are highly correlated with inflation over time, and economies of scale. Policymakers have a historic opportunity to enact pro-growth tax reform that will benefit all Iowans and make the state more competitive. To achieve this goal policy makers must continue to practice sound budgeting by passing a Conservative Iowa Budget. https://www.texaspolicy.com/the-road-to-tax-reform-starts-with-conservative-spending/ The Conservative Iowa Budget helps limit government spending so that there are more opportunities for tax relief and for widespread prosperity for Iowans now and for generations to come.

Introduction The path to keeping government from excessively burdening people with taxes and allowing for pro-growth tax reform starts with conservative budgeting. Iowa Gov. Kim Reynolds and the Republican-led legislature have fortunately been following a policy of prudent budgeting. Iowa will end fiscal year (FY) 2021 with a $1.24 billion budget surplus in its general fund, which is substantially larger than last year’s surplus of $305 million. The large surplus is a direct result of fiscal conservatism. Nevertheless, policymakers will need to continue this approach to correct for past excesses and strengthen the state’s improving fiscal foundation to provide needed tax relief. This can be achieved by keeping government spending from excessively burdening taxpayers. The Iowans for Tax Relief (ITR) Foundation’s Conservative Iowa Budget (CIB) for FY 2023 (see Figure 1) helps do this by setting a maximum threshold on the state’s general fund based on the rate of the state’s resident population growth plus inflation, as measured by the U.S. consumer price index (CPI). This fiscal rule of a spending limit on the general fund based on population growth plus inflation provides a reasonable limitation that essentially freezes inflation-adjusted spending per capita. This helps to lessen the crowding out of private sector activity and helps to stabilize expectations over time. https://www.texaspolicy.com/the-2023-conservative-iowa-budget/ For several decades and under the control of both Republicans and Democrats, Tennessee has been known for its fiscally conservative budgeting. Years of limited spending and low taxes have kept hundreds of millions of dollars in the pockets of Tennessee taxpayers that might otherwise have gone to government bloat. In fact, according to the Tax Foundation, Tennessee residents pay less in taxes than anyone in the country. Conservative budgeting has not only helped Tennessee taxpayers, but it also positioned the state to enter the COVID-19 crisis with a relatively strong “rainy day fund” of $1.1 billion, or seven percent of the state’s general fund expenditures. Tennessee remains in a strong financial position as its economy has bounced back stronger than the national average post-pandemic. Conservative budgeting and sound policy during the pandemic contributed to such strong tax revenues that the state had an unprecedented $2.1 billion surplus in the latest fiscal year despite the crisis.

But future good times are no guarantee—and that’s why, whether in good or bad times, Tennessee families practice priority-based budgeting, making tough choices on how to spend their hard-earned dollars. If Tennessee is to remain an economic powerhouse, policymakers must also continue to make fiscally conservative choices, resist the temptation for excessive spending, and not make it overly difficult for Tennessee taxpayers to fund their state government. Ron Shultis, Director of Policy and Research for the Beacon Center, commented about the report: “Tennessee has been a fiscal leader for decades but it is important that we not rest on our laurels or take that for granted. The Conservative Tennessee Budget sets the standard for staying a national leader. By ensuring spending doesn’t grow more than population plus inflation, state government won’t become more of a burden on taxpayers.” Vance Ginn, chief economist at the Texas Public Policy Foundation and co-author of the report, stated, “Any increase in the state budget should be less than the average taxpayer’s ability to pay for it, as measured by population growth plus inflation, which is why the Conservative Tennessee Budget is essential for continued opportunities that best let people prosper. We have seen the success of this approach in Texas for a number of years so I’m excited to partner with the Beacon Center in this fruitful endeavor to keep Tennessee a great place to raise a family and start a business.” https://www.texaspolicy.com/a-conservative-budget-for-tennessee/ The national debt is rapidly nearing $29 trillion, which is 25% more than our entire economy, and is orders of magnitude higher if you consider unfunded liabilities of Social Security and Medicare. This threatens life as we know it and must be addressed now.

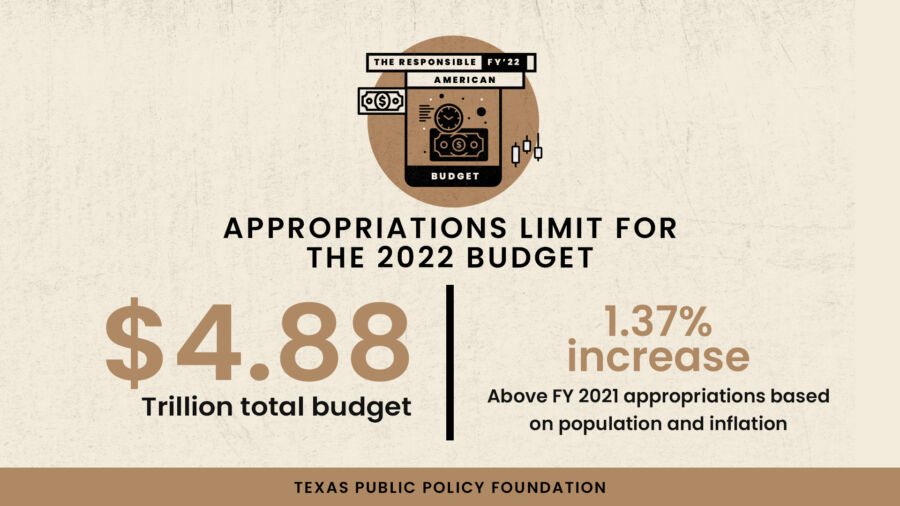

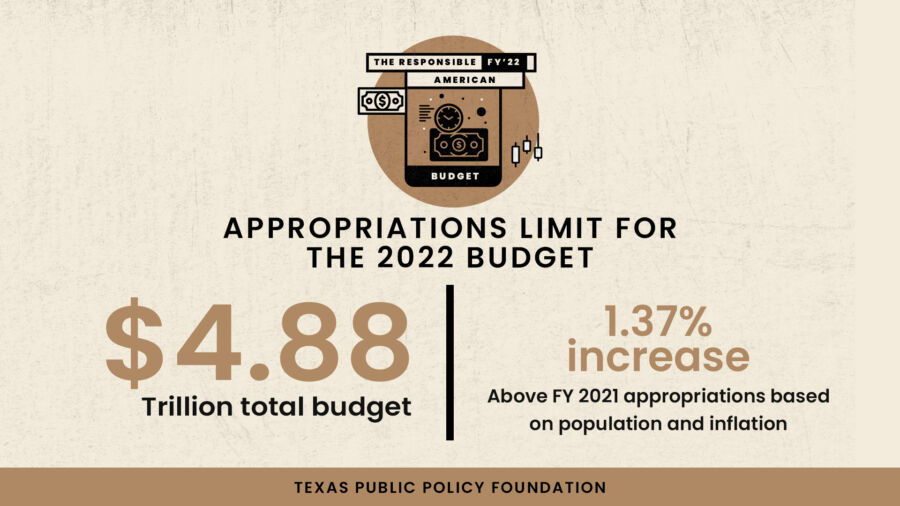

Since the start of 2020, the debt has increased by $5.2 trillion. And President Joe Biden has called for $6 trillion in new spending along with massive tax hikes that will hinder growth and add trillions more in debt. The most recent spending plans are the $1.2 trillion “infrastructure” bill, which is really a green-energy boondoggle, and the at least $3.5 trillion reconciliation package that has been described as “human infrastructure,” which greatly expands the welfare state. This expansion of the welfare state is far more than President Franklin Delano Roosevelt’s New Deal or President Lyndon B. Johnson’s Great Society. Although these initiatives likely had good intentions, the results were a disaster with the former driving the Great Depression deeper and longer and the latter contributing to greater dependency and rising structural deficits. President Biden’s Green New Deal would fundamentally transform America into something it is not, nor can it afford to be. Many progressives argue that the federal government can continue to deficit spend without consequence. While we expect this from progressives, where are the conservatives? Both political parties share the blame for the rising burden of government that comes from excessive government spending. For example, 19 Senate Republicans voted for the $1.2 trillion “infrastructure” bill that spends than 10% on conventional infrastructure such as roads and bridges. The political calculus of this maneuver by Republicans is awful and troubling as Americans need elected officials to take fiscal responsibility seriously now. A great example is that by President Calvin Coolidge, who believed in the morality of a limited government and was the ultimate budget hawk. Coolidge, along with his predecessor, President Warren Harding, made cutting government spending a priority. When Harding assumed office, he was confronted with the Depression of 1920-1921 and his response was to fight it by removing government obstacles of excessive spending and taxing, which helped get the U.S. out of that situation in a hurry. After Harding’s death, Coolidge continued Harding’s pro-growth fiscal conservatism as Coolidge regarded “a good budget as among the noblest monuments of virtue.” For Coolidge, keeping a balanced budget with spending restraint and reasonable tax rates was not just sound economic policy but moral and constitutional, as it supported increased economic prosperity along with preserving life, liberty, and the pursuit of happiness. Under President Coolidge, federal spending decreased by 0.4%, from $3.14 billion in 1923 to $3.13 billion in 1928. This means the budget declined by even more in inflation-adjusted terms and resulted in spending as a share of GDP declining from 3.7% to 3%, which compares with the astronomical $6.6 trillion for nearly one-third of GDP in 2020. As a result of cutting spending, Coolidge was able to lower the top income tax rate to 25% in 1926, as he noted that “You can’t increase prosperity by taxing success.” The spending restraint, tax cuts, and faster economic growth helped the federal government run a budget surplus every year for a cumulative cut in the national debt over those seven years of $6.1 billion. As a result of Coolidge’s fiscal conservatism, the nation experienced the Roaring ‘20s because free-market capitalism was allowed to work much more than today. “The very fact that the federal government has been able to cut down expenditures, decrease its indebtedness and reduce its taxes indicates how great is the accomplishment which you have made on behalf of the people of the nation,” noted Coolidge. Although the budget has changed since Coolidge was in office, Amity Shlaes, noted historian and Coolidge biographer, wrote that “the pressure to expand programs was as strong [then] as it is today.” Policymakers should follow Coolidge’s example and reduce spending. States such as Texas and Iowa have also proved that fiscal conservatism works, so the federal government should now do the same. The Texas Public Policy Foundation’s Responsible American Budget provides a blueprint to restoring fiscal sanity in Washington. Excessive government spending and the national debt cannot be ignored. If America doesn’t change course quick, there will be catastrophic results for Americans and Western Civilization. This is not just dangerous; it is un-American and something that will keep us from leaving a legacy to be proud of. We need Calvin Coolidge’s fiscal conservatism more than ever. Commentary President Biden and Congressional Democrats have proposed roughly $6 trillion in new spending over a decade of hard-earned taxpayer dollars. To put this into perspective, this exceeds the economic output of every country except the U.S. and China, matches the $6 trillion authorized for COVID-related items since the pandemic—with nearly $1.5 trillion unspent—and exceeds the annual federal baseline budget of $4.8 trillion.

To put it bluntly, this reckless spending will destroy America’s fiscal and economic institutions by pushing us toward insolvency, dependency, and insanity. The first proposal that the Senate, with some Republican support, recently passed a motion to proceed on is a mostly a progressive wish list of spending. It’s $1.2 trillion on “infrastructure,” with an unfunded $550 billion of it being new spending as the rest are funds previously authorized but not yet spent. But it has just $110 billion, or less than 10%, for what’s historically been considered infrastructure—roads and bridges. The other 90% is to fund mass transit waste, green energy nonsense, and more items that the states or the private sector could do. This first proposal should die or at least be cut down to actual infrastructure projects. The second proposal is a reconciliation package deemed as “human infrastructure” at an astronomical cost of likely $5 trillion over a decade (with little backing documentation on what human infrastructure is). This proposal will not only dramatically expand the federal government’s role in everyday American life but will contribute to stagflation not seen since the 1970s. It would fundamentally expand people’s dependency on the federal government and destroy the potential of Americans. Here’s how it spends money we don’t have and turns America into something she is not. Authorizing Runaway Government Spending

Commentary  The Texas Public Policy Foundation recently released the Responsible American Budget, a plan for the federal government to limit the out-of-control spending that threatens the prosperity of future generations. The key component of the proposal imposes a successful spending growth formula that has kept the budget in states like Texas from spending more than its taxpayers can afford. The Responsible American Budget has received high praise from members of Congress, top economists, state policymakers, and experts from across the country:

Originally posted at TPPF.   Irresponsible government spending damages the productive private sector through redistribution of resources, higher taxes, higher price inflation, and higher interest rates, reducing Americans’ real incomes, job opportunities, and prosperity. While there have been multiple attempts to reduce the excessive growth of federal spending in the U.S., these attempts have had limited success, if any, as noted by the $28 trillion—and quickly rising—national debt and its $350 billion—and skyrocketing—interest payments. There is debate about whether deficits matter, and these days many from across the political spectrum suggest that they do not; they are partially correct. The part of fiscal policy that matters to our daily lives is government spending, which is the fundamental source of higher taxes, more regulations, higher debt, and more crowding out of the productive private sector. Given these challenges, the time is now to address excessive government spending, and we need to promote sound fiscal rules that make the budget tangible for Americans to understand and to hold elected officials accountable for excessive spending. A bold way to do this is provided by the Responsible American Budget. Originally published at TPPF. The Responsible American Budget has received high praise from members of Congress, top economists, state policymakers, and experts from across the country:

Vance Ginn, PhD, is the chief economist at the Texas Public Policy Foundation.

Considering that high taxes and debt are always and everywhere a government spending problem, the state’s current weak spending limit has contributed to excessive government spending that has resulted in less economic prosperity for Texans. Fortunately, the Legislature has taken strides to improve the budget picture during the last three budgets by better following the Conservative Texas Budget, which is why it is crucial to put this responsible, conservative fiscal management in statute. Testimony in Support Before the Texas House Appropriations Committee “Hey Florida! Help is Here.”

That’s how Vice President Kamala Harris recently put a 21st Century spin on Ronald Reagan’s famous quote, “The nine most terrifying words in the English language are: I’m from the Government, and I’m here to help.” What does this have to do with the Texas budget and House Bill 3548? Let me explain. The premise of the Vice President’s tweet is that government’s job is to swoop in and solve all of our problems. The premise of Reagan’s quote is that too often, government is the problem—or at least standing in the way of solutions. Reagan was right, of course; government fulfills some necessary functions, but in most cases, more government means less freedom. That’s why we at the Texas Public Policy Foundation have labored for years to chisel the idea of a Conservative Texas Budget into the hard granite at the Texas state capitol. Our reasoning is clear — people don’t need more government; they need more opportunity. And our simple formula reflects that: The state’s total budget, which is the footprint of government funded by taxpayers, ought not to grow faster than our population growth plus price inflation. This spending limit is reflected in Rep. Matt Krause’s committee substitute for HB 594, which has been referred to the House Appropriations Committee. Growth beyond that equation is an excessive growth of government—meaning bigger state agencies, which inevitably assume more and more regulatory powers to themselves. And a bigger budget also means more taxes, since states (unlike the federal government) can’t hide behind deficit spending. Government shouldn’t grow faster than the citizens’ ability to pay for it. Now, state Rep. Greg Bonnen, who chairs the House Appropriations Committee, has had his HB 3548 referred to that committee. And Sen. Kelly Hancock, a member of the Senate Finance Committee, has the companion SB 1336 that will be heard before the Senate Finance Committee (of which he is a member). This legislation would improve the state’s current weak spending limit by expanding the base to all general revenue funds and by changing the growth limit to one closely related to ours of population growth times inflation. It’s important to note that the Conservative Texas Budget is a ceiling, not a floor. It’s a limit on how much the budget can increase, not a target. There’s no limit on shrinking government, cutting taxes and reducing regulations. That course would be best for Texans, and TPPF has outlined many ways in which lawmakers should do so. Our top 10 legislative priorities for this Session, which we call our Liberty Action Agenda, provides a clear path for legislators to shift power and prosperity back to the people of Texas. While Chairman Bonnen’s and Sen. Hancock’s legislation would set an improved formula closer to ours into stone and ensure that future Legislatures comply, we are pleased to see that both the House’s and the Senate’s introduced (proposed) budgets fit within our guidelines. Our math says that a total of $246.8 billion in all funds for 2022-2023 would represent a 5% increase over the last biennium, matching the growth in population plus inflation. Both proposed budgets came in under that number after excluding $6 billion toward maintaining property tax relief from last session instead of growing government. Historically, lawmakers have been too ready to increase the Texas budget and grow government. But in 2015, we introduced the Conservative Texas Budget, giving legislators a clear bar. Prior to this, the average growth rate of the biennial budget from 2004 to 2015 was 12%. With the Conservative Texas Budget in place, the average growth rate was just 5.5%. More importantly, before 2015, the average growth rate of appropriations exceeded that of population plus inflation by almost 5 percentage points, while since then, growth has been limited to an average of almost a full percentage point below population and inflation. The Conservative Texas Budget provides a path toward responsible state spending. It has proven to be successful at restraining excessive growth in government in the past, and it will continue to do so in the future if followed each session. That’s why Chairman Bonnen’s and Sen. Hancock’s legislation, which codifies much of the Conservative Texas budget, is so important. It’s the help Texas families truly need. https://thecannononline.com/hey-texas-help-is-here/  Today, the Texas Public Policy Foundation released five papers that together form a responsible strategy for the state’s immediate and long-term economic growth.

“These five approaches make for good economic policy anytime,” said TPPF Chief Economist Vance Ginn, Ph.D. “But they are especially important as the state recovers from government-imposed shutdowns. Together, these strategies will help return Texas to the prosperity we saw before COVID-19 and help get us there fast.” The Five-Step Strategy is:

“During the shutdown, the state suspended some rules and regulations, proving they weren’t essential for health and safety in the first place,” said Rod Bordelon, TPPF’s Policy Director for the Remember the Taxpayer Campaign. “Instead of waiting for the crisis to end to re-evaluate these regulations, we should repeal them now and review others in an ongoing basis so that Texans aren’t held back by unnecessary restrictions.” The Responsible Recovery Agenda also stresses that budget writers should avoid seeking additional state revenue through increased fees and taxes. “Raising taxes is a costly endeavor — even more so in a recession because it distorts behavior at a time when the economy is weak, delaying recovery and leading to even greater economic stress,” said Benjamin Priday, Ph.D., Economist at TPPF. “Legislators should close budget gaps first by strategically employing the Rainy Day Fund and by trying to find ways to reduce spending. The Responsible Recovery Agenda is a comprehensive approach to addressing the budget challenges Texas faces in the wake of COVID-19 shutdowns while also preserving the success of the Texas Model, which has strengthened the state’s economy. For a historical look at the budget and other ways to improve the budget process, the Foundation also released The Real Texas Budget report. In this Let People Prosper episode, we discuss how to unveil government excess whether it be with pension obligation bonds, bail (register for upcoming TPPF event), occupational licensing burdens reduced for military spouses, TRS pension structural problems, and the Texas House budget that increases far more than the average taxpayer's ability to pay.

#letpeopleprosper In this Let People Prosper episode 70, I chat with James Quintero and Dr. Derek Cohen about the recently released bills that would both provide property tax reform with the same language (Senate Bill 2 & House Bill 2). Read TPPF's press release here.

The press conference attended by Governor Greg Abbott, Lt. Governor Dan Patrick, Speaker Dennis Bonnen, Chairman Paul Bettencourt, and Chairman Dustin Burrows shows the unity of this particular measure. These bills would provide property tax reforms to increase transparency, change up the appraisal system, and impose a revenue trigger of an automatic rollback election: (1) if revenue is set to grow by more than 8% for local tax jurisdictions with less than $15 million in total revenue from sales and property taxes, and (2) if revenue is set to grow by more than 2.5% for all other taxing entities. This is a step in the right direction to slowing the growth of skyrocketing property taxes and we look forward to working with leadership and legislators to lower tax bills by limiting state spending as well. We also discuss the benefits of SB 523, which would restructure occupational licenses for those with particular criminal records. #letpeopleprosper In this Let People Prosper episode 69, I sit down with James Quintero, director of the Think Local Liberty project, and Dr. Derek Cohen, director of the Right On Crime project, to discuss the Texas budget, ban-the-box, and annexation.

You don't want to miss this first episode of many where we'll address a number of good, bad, and pretty good bills that influence our prosperity throughout session while giving you a heads up on which bills will be heard in committee so you can make your voice heard. In this episode we discuss the state's recommended budgets by the House and Senate and how they compare with the Conservative Texas Budget, bad bill of HB 495 related to criminal history, and a prosperity-enhancing bill of HB 347 related to annexation that builds on passage of SB 6 during the 2017 special session. #LetPeopleProsper How much money does Texas have and what will it do with it? It’s perhaps the most important question the legislature deals with each session – and it all starts with deciding on the state’s priorities. TPPF convenes the important voices who will help answer that question in 2019.

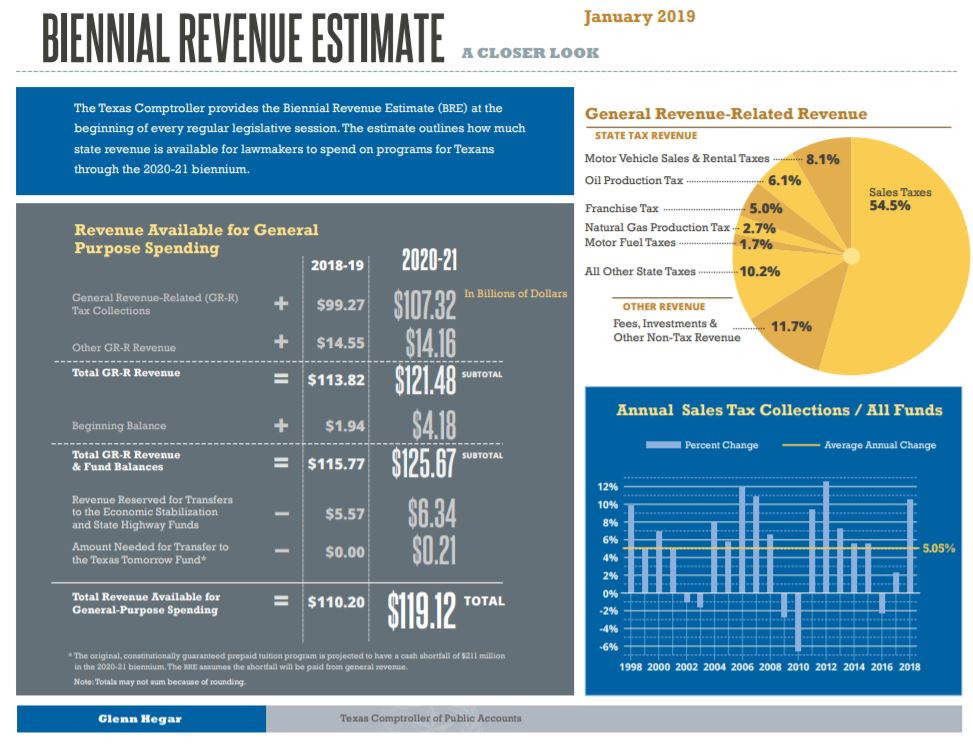

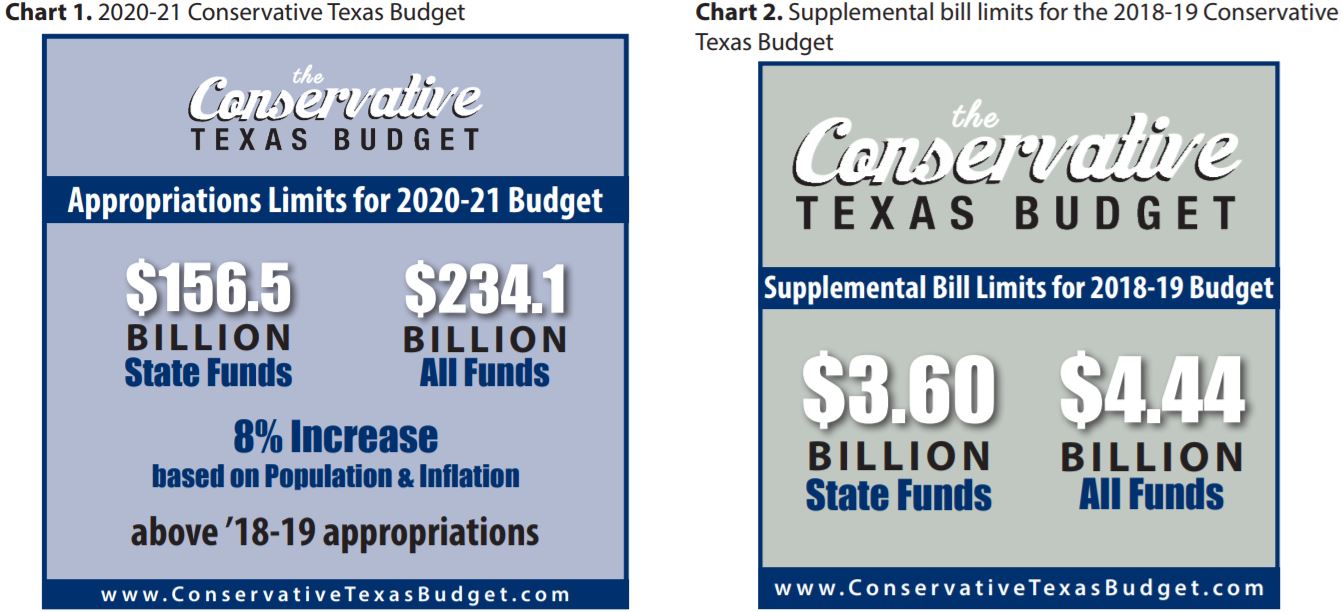

Watch this fantastic discussion with Chairman John Zerwas, Representative Donna Howard, and Chairman John Whitmire as we discuss key issues facing Texas in the upcoming budget. Texas Comptroller's Revenue Estimate Proves Room for Property Tax Relief: Let People Prosper EP 631/7/2019 In this Let People Prosper episode, let's discuss today's release of the Texas Comptroller's Biennial Revenue Estimate report. This report is key because the state's balanced budget amendment means this estimate provides the projected amount of taxpayer money available for the 86th Texas Legislature to appropriate during the upcoming legislative session that starts tomorrow. The revenue estimate indicates that the Legislature can pass a budget that funds legislative priorities while including taxpayers in the budget process by lowering property taxes within the average taxpayer's ability to pay. The report notes that the 2020-21 budget will have available an estimated $265.6 billion in all funds (state funds and federal funds) (6.7% increase), $176.9 billion in state funds (7.3% increase), and $119.1 billion in general revenue-related funds (8.1% increase). Included in these amounts is an available fund balance of $4.2 billion remaining from the 2018-19 budget.  The 86th Legislature has a grand opportunity to pass what could be the third straight Conservative Texas Budget (CTB) while prioritizing taxpayers in the budget process to lower property tax bills and improve education. Specifically, the Conservative Texas Budget Coalition, which includes the Texas Public Policy Foundation and 15 other member organizations, has set conservative spending limits on the 2020-21 budget of $234.1 billion in all funds and $156.5 billion in state funds based on an 8 percent increase in population growth plus inflation over the previous two fiscal years above current appropriations. There are also 2018-19 supplemental bill limits of $3.6 billion in state funds and about $4.4 billion in all funds to cover unfunded expenses in the 2018-19 budget. But these amounts could be quickly reached as there's a $1.8 billion amount likely needed to fund a delayed payment to transportation and $2 billion in unfunded Medicaid expenses. Legislators will need to appropriate these dollars wisely so the 2018-19 budget can be the second straight CTB.  But the Conservative Texas Budget is a maximum to just keep in line with the average taxpayer's ability to pay. Given skyrocketing property taxes, the Legislature should add taxpayers in the budget process and limit general revenue-related funds spending so that the rest can be used for property tax relief through the TPPF proposal here. Many have claimed that Texas can't afford TPPF's proposal, but this revenue estimate shows that Texas clearly can and must for the sake of prosperity in the Lone Star State.  If the upcoming 86th Texas Legislature limited spending of general revenue-related funds to just 4% growth, that would provide $4.4 billion in new spending on budget items while allowing the rest of the 4% of those funds under the CTB of $4.1 billion to go to lowering the school maintenance & operations (M&O) property tax.

The school M&O property tax is about 45% of the total property tax burden. The $4.1 billion would amount to an almost 8% biennial cut in that portion of the property tax, leaving more money in the pockets of taxpayers. The school M&O property tax would continue to be lowered each session given taxpayers are part of the budget process and fully eliminated within about a decade. This process could be sped up by lowering the rainy day fund cap and using excess funds, which the rainy day fund amount could grow to more than $15 billion, to provide property tax relief. Although slowing the growth rate of property taxes over time is good step towards reform, taxpayers want lower property tax bills for relief. The TPPF proposal works to lower property tax bills, and the Texas Comptroller's revenue estimate proves that it can and must be done. #LetPeopleProsper |

Vance Ginn, Ph.D.

|

RSS Feed

RSS Feed

Proudly powered by Weebly