Podcast: Is Texas Becoming Like California? TRUTH On State Spending, Property Taxes & More1/24/2024 This BONUS episode of the Let People Prosper show is with Bradley Swail, host of the Texas Talks podcast.

Today, we discuss: 1) Why "largest property tax relief in Texas history” became the second biggest due to excessive state spending and how the Lone Star State can eliminate the property tax for good; 2) The problem with a mandated minimum wage and reckless spending at the state and federal levels and; 3) Policies Texas leaders and lawmakers should adopt to strengthen the Texas model. Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. Also, subscribe and see show notes for this episode on Substack (www.vanceginn.substack.com) and visit my website for economic insights (www.vanceginn.com).

0 Comments

Originally published at American Institute for Economic Research.

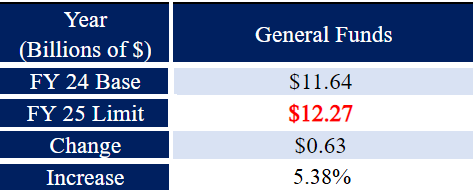

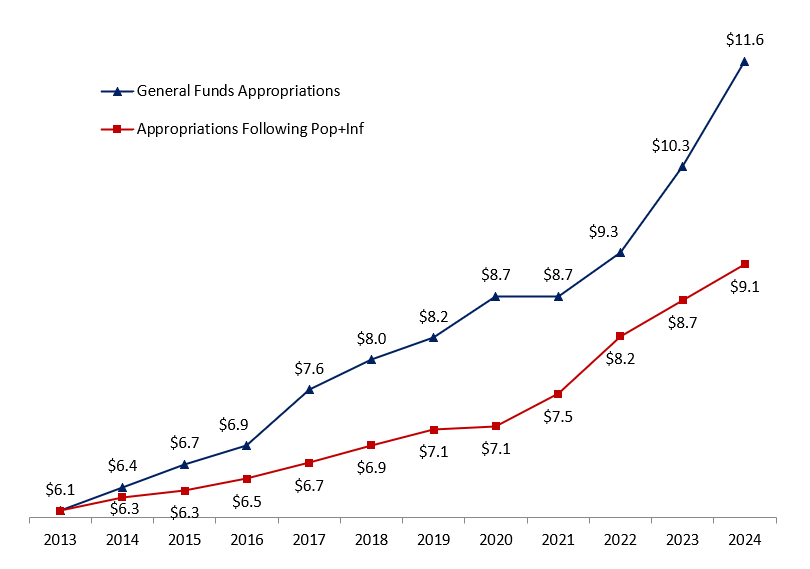

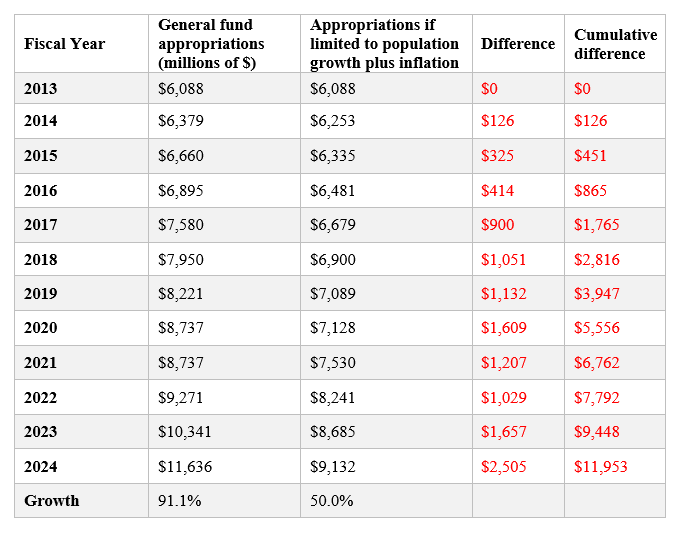

The Economist recently compared Joe Biden’s and Donald Trump’s economic records, concluding Biden wins so far. While the article raises valid points, it excludes key details that make the findings questionable. Ten months from now, there’s a high likelihood Biden and Trump could go head-to-head again for the presidency, especially after the results from the Iowa caucus. But voters should be informed about the effects of their policies on key issues like immigration, inflation, and wages. Starting with a divisive bang, let’s look at each leader’s track record concerning immigration. The Economist correctly noted that apprehensions along the southern border were much lower under Trump. They increased by the most in 12 years during the economic expansion of 2019, decreased early in the COVID-19 pandemic when people could be turned away for public health concerns, and rose again during the lockdowns. While some may see apprehensions rising between Trump and Biden as a loss for Biden, I see it as a loss for both. This metric is somewhat unreliable, given one person can be caught and counted multiple times, and those caught are a subset of total migrants. The truth is immigration is good for the economy, but government failures create unnecessarily complex barriers against legal immigration, contributing to the humanitarian crisis along the Mexico border today. Neither President has pushed for what’s needed (market-based immigration reforms) both lose. Inflation is another hot topic, especially for Biden. The Economist hands the win to Trump, as inflation was far lower during his presidency. But can we give him the credit? Remember, Trump pressured the Federal Reserve to reduce its interest rate target and expand its balance sheet, which was inflationary. His deficit spending skyrocketed during the lockdowns and was mostly monetized by the Federal Reserve, contributing to what was always going to be persistent inflation. Biden made this deficit spending and resulting inflation much worse. Add in the Fed’s many questionable decisions, such as doubling its assets, cutting and maintaining a zero interest rate target for too long, and focusing too much on woke nonsense, and we can see how this was always going to be persistent inflation. But even the Fed’s latest projections indicate it won’t hit its average inflation target of two percent until at least 2026. Likely, it will cut the current federal funds rate target range of 5.25 percent to 5.5 percent three times this year, keep a bloated balance sheet to finance massive budget deficits, and run record losses. If so, this inflation projection is too rosy. Some of Trump’s policies helped stabilize prices, including his tax and regulation reductions. But he still allowed egregious spending. Biden has doubled down on red ink that has contributed to the recent 40-year-high inflation rate. While inflation has been moderating recently under Biden, Trump gets the win. Of course, neither Presidents nor Congress control inflation, as that job is the Fed’s, but its fiscal policies influence it. When it comes to inflation-adjusted wages, The Economist grants a tie. Let’s consider real average weekly earnings that include hourly earnings and hours worked per week, adjusted for the chained consumer price index, which adjusts for the substitution bias and has been used for indexing federal tax brackets since the Tax Cuts and Jobs Act of 2017. Trump’s era witnessed a robust upward trajectory of real earnings, with considerable gains by lower-income earners, thereby reducing income inequality. We must acknowledge a real wage spike in 2020 during Trump’s lockdowns, marked by the loss of 22 million jobs and various challenges. To maintain a fair analysis, I disregard this spike. A year later, real wages demonstrated a decline under Biden. Extending the timeframe to two years later, real wages remain relatively flat to slightly increased. To provide a contextual understanding, when we consider the trend under Trump, excluding the 2020 spike, real wages for all private workers or production and nonsupervisory workers fall below those observed during Biden. It’s worth noting, however, that these wages have been higher since 2019, albeit nearly stagnant for all private workers. Given real earnings, I agree with The Economist that Trump and Biden are tied. While much more can be said for each President’s policies, continuing to add context when making assessments is crucial. I give Trump a nuanced “win” overall because his policies supported more flourishing during his first three years until the terrible mistake of the COVID lockdowns, with its huge, long-term costs. I should note that I made a strong case inside the White House for no shutdowns and less government spending but, alas, my efforts, and those by others, lost to Fauci, Birx, and Trump. Given the improved purchasing power during his presidency, Trump receives better poll ratings than Biden after three years of their presidencies. But this win doesn’t mean that Trump’s record is best regarding these issues, protectionism, and more. Let’s hope free-market capitalism, the best path to let people prosper, is on display this November, no matter who is on the ballot. Originally posted at South Carolina Policy Council. Thanks to a robust state economy, plentiful business opportunities, and a relatively low cost of living, South Carolina remains one of the fastest-growing states in the nation. To maintain this strong position and promote further growth, it is crucial for S.C. legislators to limit state spending and reduce the government’s burden on taxpayers. The S.C. Policy Council created the South Carolina Sustainable Budget (SCSB) to assist in this effort. The SCSB is a maximum limit on annual recurring general funds[1] appropriations based on the rate of state population growth plus inflation. First published in 2022 and again in early 2023, it has served as a data-driven resource to help rein in unsustainable spending and provide more opportunities for tax relief. Unfortunately, the state did not adhere to the SCSB limit of $11.20 billion for its fiscal year (FY) 2024 budget; instead, it appropriated $11.64 billion – a 12.56% increase above the FY23 base of $10.34 billion. To turn the tide of excessive budget growth and provide more room for tax relief, the Policy Council is issuing its third SCSB. Table 1 provides the results outlined in this report for the FY25 SCSB. Table 1. The FY25 South Carolina Sustainable Budget for Appropriations of Recurring General Funds  Based on population and inflation data in 2023, the recommended recurring general funds appropriations limit[2] for South Carolina’s FY25 budget is $12.27 billion. With inflation moderating somewhat since reaching a 40-year high in 2022, primarily because of the errant policies in D.C., the SCSB ceiling is higher than it would be under normal economic circumstances. For example, the average annual rate of population growth plus inflation since 2013 has been 3.78%. Accordingly, the S.C. Legislature should consider freezing spending at the current FY24 budget of $11.64 billion. This would help correct recent overspending in the state’s budget and help put the state on a more sustainable budget path. It would also leave more money available for needed tax relief. At a minimum, recurring general fund appropriations in the FY25 budget must remain below $12.27 billion. Overview A sustainable budget – sometimes called a conservative or responsible budget – is a model for state budgeting that sets a maximum limit on appropriations or spending based on the rate of population growth plus inflation. This metric serves as an indicator of what the average taxpayer can afford to pay for government provisions. It accounts for 1) More people in the state who could potentially pay taxes; 2) Wage growth that’s typically tied to inflation over time to pay taxes; and 3) Economies of scale, as not every new person or wage increase should be associated with new government spending. The SCSB does not make specific recommendations on how general funds should be appropriated in the budget. Instead, it gives legislators the flexibility to appropriate taxpayer dollars to government programs as determined by the General Assembly, while ensuring that spending growth remains in line with what people can afford. Such a voluntary spending limit is key to putting South Carolina in a position for further tax relief. In 2022, Gov. Henry McMaster and lawmakers enacted the first-ever state personal income tax cut, which immediately reduced the top rate from 7% to 6.5% and collapsed the lower bracket to 3%. It also scheduled additional yearly 0.1% cuts to the top rate until it reaches 6%, though general fund revenues must project at least 5% annual growth for the cuts to trigger. The problem with this approach is that it relies on continued revenue growth to deliver incremental tax relief. Following the SCSB would help to accelerate this process, freeing up revenue to buy down the top rate to 6% immediately and fueling other tax cuts. On the other hand, unsustainable spending could build pressure to reverse course and raise taxes, leaving South Carolinians with fewer opportunities to flourish. SC Appropriations vs. Sustainable Budget Figure 1 compares the previous twelve years[3] of South Carolina’s recurring general fund budget appropriations (FY13 to FY24) to those appropriations when limited each year to the rate of population growth plus inflation. Figure 1. South Carolina General Fund Appropriations v. SCSB 12-year GF appropriations: $98.5 billion (+91.1%) 12-year GF appropriations limited to population growth + inflation: $86.5 billion (+50.0%)  Notes. Budget amounts are based on data from South Carolina’s state budget publications, Fed FRED for state population growth and U.S. chained-CPI inflation, and authors’ calculations. Appropriations did not increase from FY20 to FY21 because the state operated on a continuing resolution in FY21.[4] Key takeaways (see Table 2):

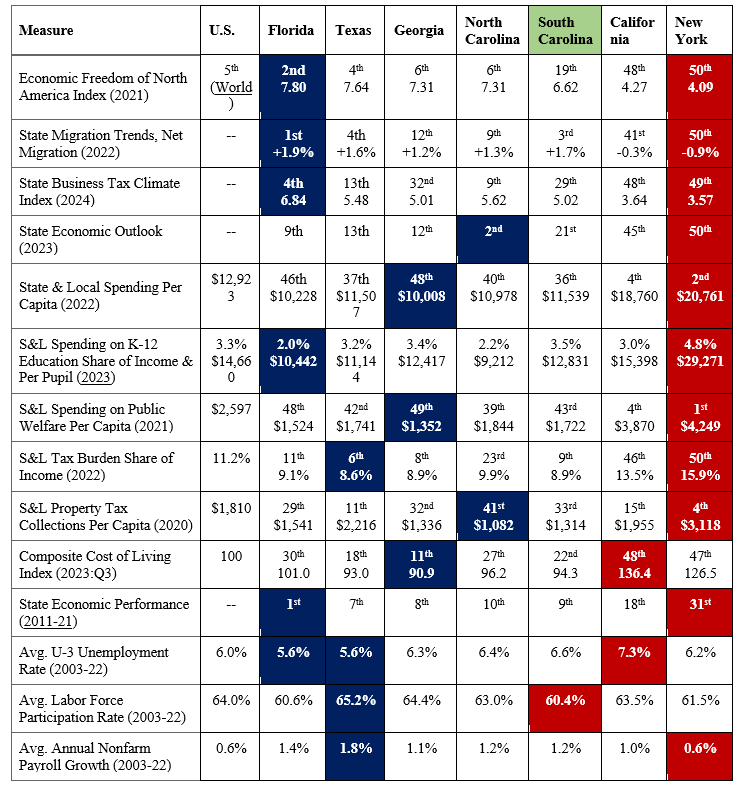

Note. Budget amounts are based on data from South Carolina’s state budget publications, Fed FRED for state population growth and U.S. chained-CPI inflation, and authors’ calculations. These data provide clear evidence that there is room for the state to limit spending growth to reduce taxes substantially. South Carolina has been one of the 25 states in the last three years to cut income taxes, which has helped the state improve compared to its neighbors. However, North Carolina recently passed legislation that could eventually bring their income tax rate to 2.49%, which would be the lowest in the country, excluding the seven states without personal income taxes. On that list are Florida and Tennessee, two major competitors for jobs and investment in the Southeast. South Carolina could improve its position by passing sustainable budgets and using the surplus revenue to cut taxes, especially income taxes. See Table A in the Appendix for more comparisons of South Carolina with other states. Follow the SC Sustainable Budget We strongly encourage legislators to follow the SCSB when drafting South Carolina’s FY25 budget. As a data-driven resource, the SCSB sets a clear spending limit based on what the average taxpayer can afford to pay for government services. Surpassing this limit will fuel excessive government growth and promote unsustainable spending, leaving less revenue that can be used to lower taxes. Recent budget projections show a historic opportunity for tax relief – if legislators are willing to take it. In its November 2023 forecast, the S.C. Board of Economic Advisors (BEA) estimates a recurring budget surplus of $673.1 million for FY25. It also projects the cost of lowering South Carolina’s top personal income tax rate from 6.4% to 6.3% to be roughly $100 million (which is accounted for by BEA prior to their $673.1 million projection). Based on current data, we estimate[1] it would cost an additional $300 million in revenue to cut the top rate immediately to 6% in the new budget. Accordingly, this all-at-once cut could be achieved using less than half of the projected recurring surplus. Passing a sustainable budget would be easier if state agencies followed South Carolina’s legal budget process. Under current law, agencies are supposed to justify every dollar they are requesting when submitting their annual budget plans to the governor – explaining why both new and current programs deserve taxpayers’ money. The law follows a concept known as zero-based budgeting, where all expenses need to be justified annually based on need and performance without regard to previous budgets. Despite this legal mandate, agencies only provide details for new spending requests each year. Fortunately, South Carolina is decently prepared for a rainy day should it occur. Voters in 2022 approved two amendments to increase contributions to the state reserve funds – raising the General Reserve Fund from 5% to 7% (over several years) and the Capital Reserve Fund from 2% to 3% of the previous year’s general fund revenue. By law, the reserve funds act primarily as a shield against year-end budget deficits. While these reserve funds are important to withstand volatility in the budget, lawmakers should focus on limiting or cutting the budget for it to be sustainable over time. Conclusion Following the SCSB will put South Carolina in a better position to reduce taxes, avoid the cost of excessive government growth, and give citizens more opportunities to flourish. Had this been done since 2013, the state could have substantially lowered personal income taxes, if not eliminated them. Fortunately, the upcoming budget provides state leaders with another crucial opportunity to rein in spending and deliver much-needed relief. South Carolina taxpayers are counting on it. Appendix: How Does South Carolina Compare with Other States? Table A shows how South Carolina compares with the largest four states in the country (i.e., California, Texas, Florida, New York) and neighboring states (i.e., Arkansas and Mississippi) based on measures of economic freedom, government largesse, and economic outcomes. Table A. Comparison of States for Measures of Economic Freedom and Outcomes  Notes. Dates in parentheses are for that year or the average of that period. Data shaded in blue indicate “best,” and in red indicate “worst” per category by state.

These rankings show that South Carolina is better than most states in terms of economic freedom, but is substantially less economically free than its neighbors of Georgia and North Carolina. South Carolina does better than others in this comparison in terms of having the lowest supplemental poverty rate and near the best in net migration. South Carolina has the highest state and local government spending per capita among its neighbors and a substantially worse business tax climate than North Carolina. The data show that states with less economic freedom (e.g., New York, California, and South Carolina) tend to perform economically worse. On the other hand, those states with more economic freedom (e.g., Florida, Texas, Georgia, and North Carolina) tend to perform economically better. Given these comparisons, South Carolina has much room for improvement to be more competitive and, more importantly, provide more opportunities for human flourishing.  In 2023, Texas led the U.S. on many fronts: job growth, economic expansion, energy production, and a record surplus of $33 billion. This was when many other states, especially California, were reporting economic challenges and deficits.

Despite Comptroller Glenn Hegar's warning to spend wisely, the 88th Texas Legislature chose out-of-control, record spending. This isn’t a record Texans wanted because it means less available money for property tax relief. Texas can reverse course to lead the U.S. in fiscal responsibility by passing sustainable budgets that result in more surplus to return to taxpayers by reducing school property tax rates until they are zero. In 2023, the Texas Legislature passed the largest spending increase in state history. The fiscal 2024-25 budget increased appropriations by 21.3% to $321 billion, or, excluding federal funds, by 31.7% in state funds to a staggering $219 billion. Even more disturbing is that currently reported amounts may increase further as some legislation passed in the special sessions increases spending. Either way, the budget growth far eclipsed the rate of population growth plus inflation, which increased by 16% over the prior two years. This rate is a good comparison because it represents the average taxpayer’s ability to pay for government spending. This record spending, along with records of over $10 billion in new corporate welfare payments even to multi-billion-dollar companies and more than $13 billion in constitutional amendments that move money outside of the state’s spending limit, sets a challenging path forward. The bloated fiscal 2024-25 budget now looms as the new baseline for lawmakers, expanding government to the chagrin of many Texans. The excessive budget increase overshadowed Gov. Greg Abbott’s historic tax relief compromise signed into law during the Legislature’s second special session. While hailed as the largest property tax cut in Texas history, it fell short. The total for new school property tax relief was $12.7 billion. It falls short of the $14.2 billion appropriated for reducing school property taxes in fiscal 2008-09 due to a Supreme Court of Texas ruling that the school finance system was unconstitutional. But when the amount is adjusted for inflation since then, the $14.2 billion would be about $21 billion. Even when factoring in the state’s contribution of $5.3 billion to maintain reductions in school property taxes in prior sessions, the $18.3 billion in combined relief remains well below the $21 billion needed to be the largest in Texas history. It should be noted that the $14.2 billion for property tax relief for fiscal 2008-09 helped cut school property taxes by just $2 billion in 2007. But then school property taxes increased by $2.3 billion in 2008, surpassing 2006 before the relief by $300 million. Total property taxes decreased by just $450 million in 2007 and then increased by $3.8 billion in 2008. While those with property received some relief in their property tax bill in 2023, especially those with a homestead exemption, the amount will not be nearly as much as some lawmakers claimed. Worse still, these savings won’t likely last as local governments continue to push to pass bonds and increase spending and taxes. The Legislature should focus this interim on doing efficiency audits across the government, much like it started with safety net programs. Finding savings across the government with so much excessive spending recently will help maintain the property tax relief passed last year; spending excesses will not lead to calls for tax increases, and resulting surpluses can put school property taxes on a fast path to zero next session. There will also be an opportunity to put the new, stronger statutory spending limit in the constitution and have this limit cover spending by local governments. There should also be a requirement that at least 90% of resulting surpluses by the state go toward reducing school property tax rates and by local governments to reduce their own property tax rates. Doing so will achieve fiscal sustainability and put all property taxes on a path to elimination. In the meantime, Texans have opportunities in the March primary and November general election to consider many candidates' policy proposals. Do candidates on the ballot support eliminating property taxes, reducing government spending, and increasing prosperity? We need more politicians pushing for these things because they benefit Texas families and entrepreneurs. Let’s not have big-government socialism creep more into Texas but turn back toward free-market capitalism that has contributed to abundance. Originally published at The Center Square. Thank you for tuning into the FINAL Let People Prosper podcast episode 76 of 2023! Today, I have a brief but informative podcast for you, recapping the highlights of the economy and my business, Ginn Economic Consulting, LLC.

As a Christmas gift, I am giving away a complimentary subscription to the paid version of my newsletter and a copy of Lexi Hudson’s fantastic book, “The Soul of Civility: Timeless Principles to Heal Society and Ourselves.” To enter this giveaway, simply fill out the information at the link and rate my podcast on either Apple Podcasts or Spotify. Is there anyone whom you would like for me to interview in 2024? Leave them in the comments. Today, I cover:

This was originally published at National Review.

Colorado governor Jared Polis (D) and Art Laffer, the economist and Presidential Medal of Freedom honoree, recently critiqued the state’s Taxpayer’s Bill of Rights (TABOR) at this venue. While not meritless, much of their argument is paradoxical, highlighting an overarching issue of fiscal unsustainability that warrants a reality check. TABOR recently had its 30th birthday. Voters approved the constitutional amendment in 1992, establishing the strongest tax and expenditure limit in the country. It’s been the gold standard for a sound spending limit ever since. Under the amendment, annual growth in spending cannot exceed the state’s population growth plus inflation, which is a good measure of the average taxpayer’s ability to pay for spending. When adopted, the limit covered about two-thirds of state spending. It requires voter approval for tax increases and mandates refunds to taxpayers if tax revenue exceeds the limit. In their critique, Polis and Laffer correctly acknowledge that TABOR surpluses indicate that income-tax rates are too high. They’re correct that the state should seek to reduce income-tax rates to prevent overcollection instead of handing out refunds. They’re also correct that a broader tax base is preferable. It enables the tax rates, and therefore the marginal effect of the tax burden, to be reduced as much as possible for all. But Polis and Laffer incorrectly criticize TABOR without realizing its pivotal role in achieving their purported goal to reduce taxes. Without a crucial spending check such as TABOR, the state would tie its budget directly to revenue levels, eliminating any surplus. While Polis has only recently touted reducing state income-tax rates with surpluses, the Independence Institute has long supported a plan called “Path to Zero.” The plan simply limits government spending and uses resulting surpluses to lower tax rates until they’re zero. This is similar to my efforts in Texas, Louisiana, and other states, which start with a sustainable budget approach, as recently explained in a release by Americans for Tax Reform. Unfortunately, courts and politicians have eroded the strength of TABOR over time, primarily because of politicians’ lack of fiscal restraint. The result has been that TABOR now covers less than half of state spending, allowing expenditures of all state funds, which excludes federal funds, to grow faster than population growth plus inflation. Specifically, appropriations of all state funds have increased by 74.2 percent, compared with an increase of just 46.5 percent in population growth plus inflation over the last decade. This has resulted in the state appropriating $4.2 billion more in just fiscal year 2023–24 than if it had been limited to the rates of population growth plus inflation over time, amounting to higher spending and taxes of about $3,300 per family of four. The summed difference each year in all state funds above this metric over the decade amounts to $16.3 billion, or $11,300 per family of four. These amounts don’t necessarily mean that the state needs to start cutting its budget to get back on track, but they do mean that the time to start reining in the budget is now, to reduce these excessive burdens on taxpayers. To that end, Ben Murrey, director of the Independence Institute’s fiscal-policy center, and I have shown the path forward with the Sustainable Colorado Budget (SCB). The SCB is a maximum threshold for the initial appropriations of all state funds and is based on TABOR’s rate of population growth plus inflation. This will help reinforce the original intent of TABOR, by broadening the spending limit to all state funds. The plan would limit nearly two-thirds of state spending each year, as when voters first adopted TABOR. Doing so will result in larger surpluses to reduce income-tax rates yearly until they’re zero. Polis and Laffer are right to want rate reductions, but there are none if there is no surplus. For the upcoming FY 2024–25, the SCB proposes an all-state funds ceiling of $27.70 billion. This uses the prior FY 2023–24 amount of $26.15 billion and increases it by 5.9 percent, calculated using TABOR’s current method and reflecting a 1.0 percent increase in the state’s population and 4.9 percent inflation. As noted above, it would be even better to grow the budget by less or not at all to correct past budgeting excesses. This more robust TABOR approach outlined in the SCB helps to freeze inflation-adjusted spending per capita, allowing the average taxpayer to afford the cost of government. In recent years, the current TABOR limit alone has already produced substantial surpluses that have been refunded to Coloradans. But instead of using this year’s $1.7 billion TABOR surplus to refund overcollected taxpayer dollars, the legislature could have cut the income-tax rate from a flat rate of 4.4 percent, which ranks 14th in the country, to 3.81 percent. Further, had the state over the past decade followed the SCB, which has a larger base budget, lawmakers could have lowered the income-tax rate to 2.96 percent, putting it on a faster path to becoming the lowest flat income-tax rate in the country, below North Carolina’s 2.49 percent. It would also pave the way to zero income taxes by 2042. Polis in his recent article criticizes TABOR for acting as a spending restraint rather than a mechanism to reduce tax rates. Indeed, his track record in the governor’s office demonstrates his distaste for limitations on spending. The state budget has grown 45 percent since he took office less than five years ago; his budget request for the upcoming fiscal year would constitute an astounding 52 percent increase. In a state with a constitutional balanced-budget requirement, it’s paradoxical to support tax cuts without spending restraints. Unfortunately, given his poor track record on spending and his critique of TABOR’s spending restraints — which he and Laffer improperly call a revenue limit — Polis is unlikely to adopt our sustainable budget to produce larger surpluses with which to cut tax rates. On the contrary, this year he supported a measure that would have increased state spending above the current limit, erroneously claiming that it would cut taxes using state surpluses. “A similar tax-rate reduction for property taxes, Proposition HH, failed on the ballot recently in Colorado,” Polis and Laffer write in their recent NRO article. While a clever misdirection, this argument doesn’t hold up. Prop HH didn’t directly offset the TABOR surplus through tax cuts, as an income-tax reduction would. That’s because the measure influenced only local property-tax revenue. Because the State of Colorado generates no tax revenue from property taxes, as those are collected only by local governments, reducing those rates won’t affect the TABOR surplus. Polis and Laffer contend that the state budget indirectly benefits from local property taxes. However, Prop HH would have lessened the state’s share of local funding by only approximately $125 million.  Originally published at Real Clear Policy.

During the fourth Republican presidential candidate debate the four participating candidates were asked to name a past president who would serve as an inspiration for their administration. In his response, Governor Ron DeSantis stated that he would take inspiration from President Calvin Coolidge. Coolidge, stated DeSantis, is “one of the few presidents that got almost everything right.” Further, DeSantis argued that “Silent Cal” understood the federal government’s role and “the country was in great shape” under his administration. To say that the federal budget process is broken is an understatement. The national debt continues to grow driven by out-of-control spending. The budget hawk within the Republican Party is an endangered species. Governor DeSantis is correct that the Republican Party needs to rediscover the principle of limited government. The best way to do this is to take inspiration from the Republican Party’s best known budget hawks and champions of limited government, Presidents Warren G. Harding, and Calvin Coolidge. President Harding assumed office in 1921 when the nation was suffering a severe economic depression. Hampering growth were high-income tax rates and a large national debt after World War I. Congress passed the Budget and Accounting Act of 1921 to reform the budget process, which also created the Bureau of the Budget (BOB) at the U.S. Treasury Department (later changed in 1970 to the Office of Management and Budget). President Harding’s chief economic policy was to rein in spending, reduce tax rates, and pay down debt. Harding, and later Coolidge, understood that any meaningful cuts in taxes and debt could not happen without reducing spending. Harding selected Charles G. Dawes to serve as the first BOB Director. Dawes shared the Harding and Coolidge view of “economy in government.” In fulfilling Harding’s goal of reducing expenditures, Dawes understood the difficulty in cutting government spending as he described the task as similar to “having a toothpick with which to tunnel Pike’s Peak.” To meet the objectives of spending relief, the Harding administration held a series of meetings under the Business Organization of the Government (BOG) to make its objectives known. “The present administration is committed to a period of economy in government…There is not a menace in the world today like that of growing public indebtedness and mounting public expenditures…We want to reverse things,” explained Harding. Not only was Harding successful in this first endeavor to reduce government expenditures, his efforts resulted in “over $1.5 billion less than actual expenditures for the year 1921.” Dawes stated: “One cannot successfully preach economy without practicing it. Of the appropriation of $225,000, we spent only $120,313.54 in the year’s work. We took our own medicine.” Overall, Harding achieved a significant reduction in spending. “Federal spending was cut from $6.3 billion in 1920 to $5 billion in 1921 and $3.2 billion in 1922,” noted Jim Powell, a senior fellow at CATO Institute. Harding viewed a balanced budget as not only good for the economy, but also as a moral virtue. Dawes’s successor was Herbert M. Lord, and just as with the Harding Administration, the BOG meetings were still held on a regular basis. President Coolidge and Director Lord met regularly to ensure their goal of cutting spending was achieved. Coolidge emphasized the need to continue reducing expenditures and tax rates. He regarded “a good budget as among the most noblest monuments of virtue.” Coolidge noted that a purpose of government was “securing greater efficiency in government by the application of the principles of the constructive economy, in order that there may be a reduction of the burden of taxation now borne by the American people. The object sought is not merely a cutting down of public expenditures. That is only the means. Tax reduction is the end.” “Government extravagance is not only contrary to the whole teaching of our Constitution but violates the fundamental conceptions and the very genius of American institutions,” stated Coolidge. When Coolidge assumed office after the death of Harding in August 1923, the federal budget was $3.14 billion and by 1928 when he left, the budget was $2.96 billion. Altogether, spending and taxes were cut in about half during the 1920s, leading to budget surpluses throughout the decade that helped cut the national debt. The decade had started in depression and by 1923, the national economy was booming with low unemployment. Both Harding and Coolidge were committed to reining in spending, reducing tax rates, and paying down the national debt. Both also used the veto as a weapon to ensure that increased spending and other poor public policies were stopped. The results of the Harding-Coolidge economic plan created one of the strongest periods of economic growth in American history. Unemployment remained low, the middle class was expanded, and the economy expanded. From 1920 to 1929 manufacturing output increased over 50 percent and the United States was a global leader in many key industries. In our current era marked by dangerous debt levels and high inflation whoever becomes the Republican presidential nominee should take inspiration from Harding and Coolidge.  Originally published at Independence Institute. In 1992, Colorado voters adopted the Taxpayer’s Bill of Rights (TABOR) to limit the growth in state and local spending. Over the past three decades, however, politicians from both parties and a complicit judicial branch have exempted more and more state spending from the TABOR limit. When voters adopted TABOR, 67% of state spending was subject to the limit. Today, the majority of state spending is not subject to the limit. Consequently, state spending has far outpaced Coloradans’ incomes over the last decade. To uphold the original intent of voters when they adopted TABOR, Independence Institute proposes the Sustainable Colorado Budget (SCB), which limits state spending from state funds (excluding federal funds) at the rate of population growth plus inflation. The state should then use the surplus revenue above the SCB spending limit to reduce the income tax rate for all taxpayers. What can state and federal governments glean from Iowa's example when it comes to responsible budgeting? Find out! If you value responsible government budgeting and fiscal conservatism, I believe you’ll enjoy this podcast episode. Thank you to Iowans for Tax Relief Foundation’s ITR Live podcast for having me on their show to discuss a conservative approach to balancing Iowa’s state budget, my time at the White House, and free trade. Listen on Apple Podcasts or YouTube! Original publication at Iowans for Tax Relief Foundation.  If you’d like to learn more about the responsible state budget revolution sweeping the nation, check out my post, where I dive deeper into the topic, including my extensive work helping reform state budgeting across the country.

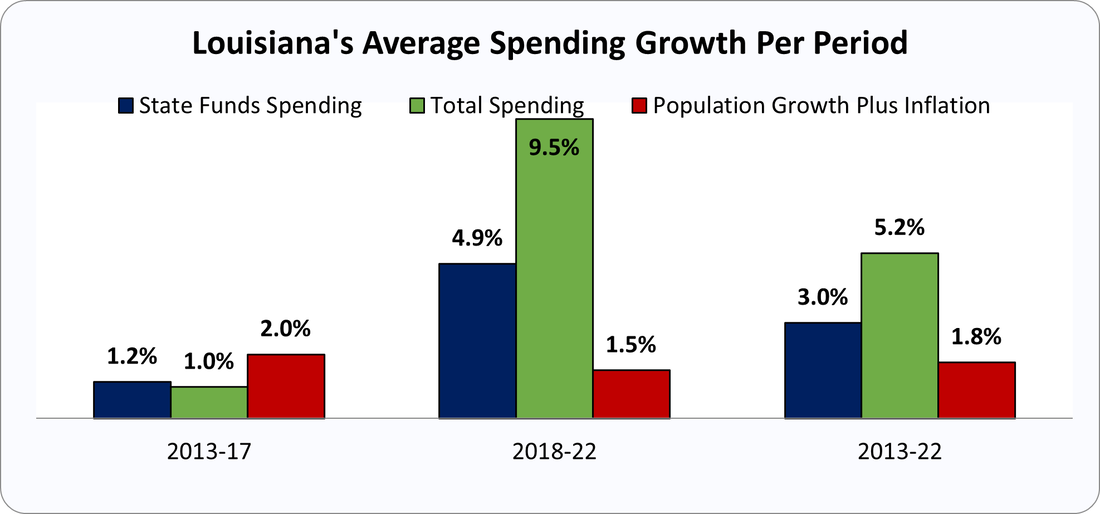

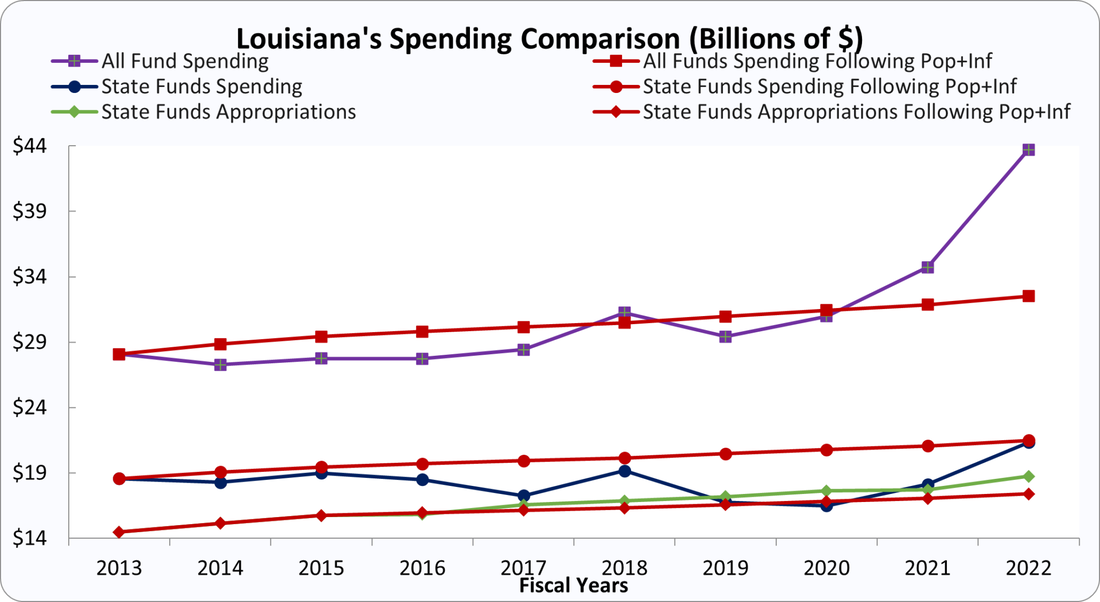

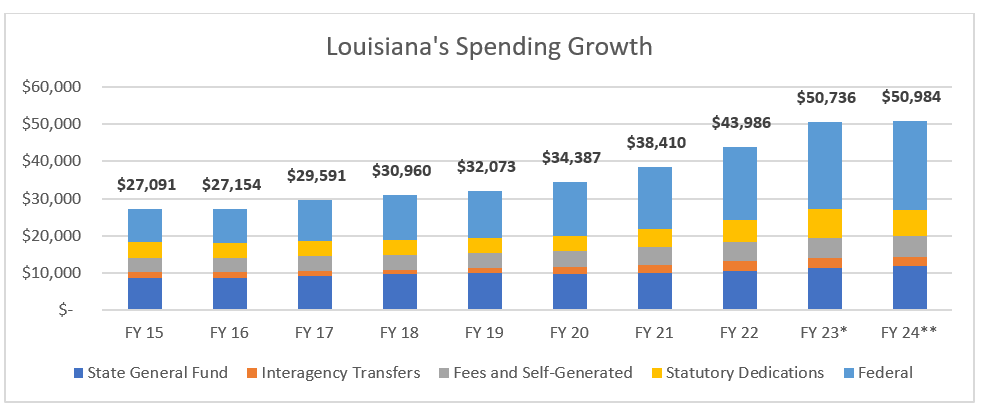

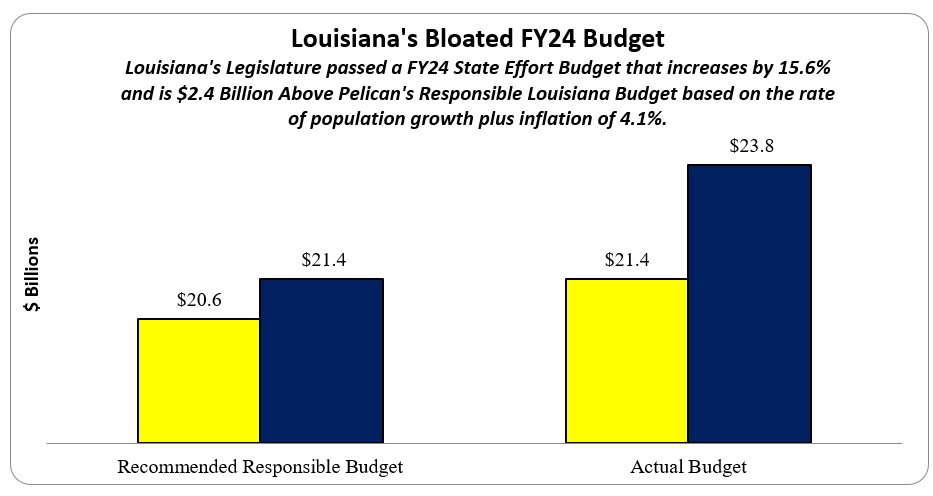

Originally posted at Pelican Institute where I co-wrote it with Jamie Tairov. The Pelican Institute has highlighted the need for better state budgeting and tax reform. This includes the Responsible Louisiana Budget (RLB), which was released earlier this year. The RLB shows that Louisiana’s budget has been growing at unsustainable levels, and that an improved growth factor for the expenditure limit and initial appropriations is needed. Recently, Americans for Tax Reform released a similar comparison for all 50 states, including Louisiana, in its Sustainable Budget Project. This report shows that, on the surface, Louisiana’s spending has not been as unsustainable as the RLB shows. Why is there a different outcome in the two reports?

Outcomes of Each Report The Responsible Budget model is currently being used successfully in other states to rein in spending. This is what Louisiana’s budget would have looked like had the RLB been employed over the last ten years.

Here are the findings from ATR’s Sustainable Budget study over the last decade:

Total spending in FY 22 was 34.4%, or $11.2 billion, higher than the improved expenditure limit. This means that a family of four is paying $8,800 more in taxes to pay for the excess spending, which is not sustainable spending.  Is One Report Better Than the Other?

No. Both reports are accurate and serve different purposes. The RLB uses initial appropriations which helps lawmakers easily compare appropriation amounts from year to year as they are drafting the budget during session. Because it covers spending instead of appropriations, the ATR study is a backwards-looking metric that can be used for making longer-term spending decisions, but it will be limited in its use during a legislative session. Both reports compare the current expenditure limit with a proposed improved expenditure limit. The current limit is the three-year average of personal income growth, which is an extremely volatile measure. The proposed improved limit is the three-year average of population growth plus inflation. The RLB and ATR reports can work together, providing limits on the front and back end to ensure that spending remains responsible throughout the year. Both reports show recent elevated appropriations and spending. There is clearly room for budgeting restraint in Louisiana. These measures have benefits to lawmakers and the public so that they can have the tools necessary to restrain government spending and provide a responsible budget. Doing so will have many payoffs over time, including making the comeback in the Pelican State happen more quickly by eliminating personal income taxes, providing a more dynamic economy, and improving opportunities for people to flourish. Don’t miss episode 72 of the Let People Prosper show with guest Avik Roy, president of the Foundation for Research on Equal Opportunity (FREOPP).

We discuss America’s biggest economic problems and how to solve them. Avik and I discuss the following and more:

Check out the full show notes at my Substack newsletter and subscribe to get my posts directly in your inbox.  The Texas Legislature just found out it has a huge opportunity to correct its profligate spending failures made earlier this year. But instead, they’re gearing up to spend more at the expense of strapped taxpayers. This would be a fatal error for the Lone Star State.

Texas Comptroller Glenn Hegar recently released the Comptroller's Revenue Estimate (CRE). This report acts like a financial checkup to confirm sufficient tax revenue available to cover expenditures based on the state’s balanced budget amendment. The current two-year tax revenue for 2024-25 was updated higher to $194.6 billion available for general spending, an increase of 24.8% from the previous budget. This certified revenue estimate exceeds the $176.3 billion appropriated by the 88th Legislature for general purposes, resulting in a projected surplus of $18.3 billion. This large amount is from a more vibrant economy than previously estimated and could go a long way to putting school property taxes on a path to elimination. Yet the Texas Legislature’s recent out-of-control spending habits indicate taxpayers probably won’t get more property tax relief than the minimal amount passed this year. The state wants to increase spending on a government school system in the current third special session rather than on students to have universal school choice. And spending could go up by more than $13 billion outside of the expenditure limit if voters approve most of the 14 constitutional amendments on the state ballot this year. Add it all up, and it’s no wonder that Texans find living in many places across the state unaffordable. While Texas has witnessed major economic achievements this year, such as noteworthy records for labor force participation and job creation, the 88th Legislature's actions raise serious concerns about the future. This year, the Lone Star State passed its largest spending increase, largest corporate welfare, and just the second-largest property tax cut in state history, which the latter will underwhelm homeowners when they get their bills. This could be a major problem for Republicans who have touted this as the “largest property tax cut in the world” or the “largest property tax cut in Texas history.” While Texans grapple with an affordability crisis, spending the state surplus and voters approving the proposed ballot items, except propositions 3 (prohibit wealth taxes) and 12 (abolish Galveston County treasurer’s office), would add insult to injury. Rather than squandering the surplus, the Texas Legislature should prioritize strengthening the Texas Model by: 1. Spending less at the state and local levels, strengthen the state’s spending limit with the rate of population growth plus inflation covering all state funds, and have that spending limit also cover local government spending similar to Colorado’s Taxpayer’s Bill of Rights. 2. Taxing less by putting local property taxes on a path to elimination using surpluses to reduce school district M&O property tax rates until they are zero. Local governments should leverage their surpluses to reduce their property tax rates until they are zero. 3. Regulating less by removing barriers to work, removing occupational licensing restrictions, reforming safety nets, and passing universal school choice. Strengthening the Texas Model isn't just about fiscal responsibility; it's about securing a thriving future for generations to come. Texas, with its unique spirit and determination, can continue to lead the way, fostering an environment where free-market capitalism thrives and individuals prosper. The surplus, instead of being frittered away on needless pursuits, should be a catalyst for transformation that redefines the Lone Star State's destiny, safeguards liberty, and sows the seeds of enduring prosperity. Originally published at The Center Square.  Texas has been a leader in job creation. But Texas faces major headwinds as this year’s 88th Legislature has looked more like California than what Texans expect. There is a better way.

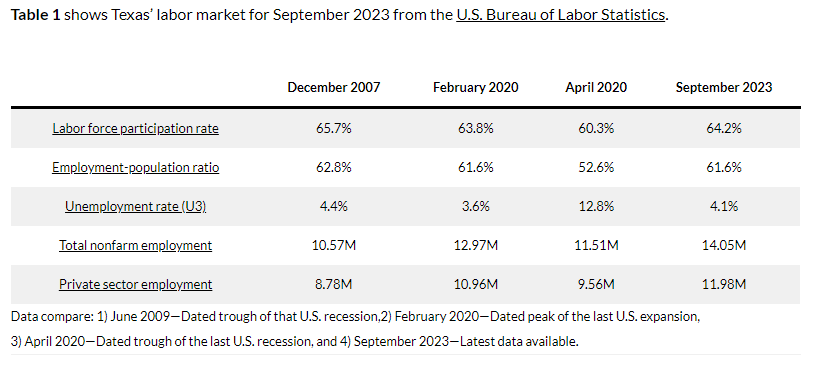

The labor market continues to improve in Texas even as there are some weaknesses.

Originally published at Texans for Fiscal Responsibility. I hope you enjoy the fantastic 67th Let People Prosper Show episode with TX State Rep. Brian Harrison! Please subscribe to my newsletter if you haven’t already, and subscribe to my podcast wherever you get yours. I would appreciate it if you would also rate and review my podcast! Brian (bio) and I discuss:

Please subscribe to my newsletter if you haven’t already, and subscribe to my podcast wherever you get yours. You can find direct links to follow my work at the buttons at the end of this post. I would appreciate it if you would also rate and review my podcast! Ben (bio) and I discuss:

Federal and state layouts are vastly outpacing the combined rate of inflation and population growth.  The U.S. national debt recently passed $33 trillion, more than 120% of gross domestic product. Left-wing politicians assert that Americans are undertaxed, but the data show that the government spends too much.

Americans for Tax Reform launched the Sustainable Budget Project in September to document the rise in government spending over the past decade. The results are clear: Overspending is the problem. Between 2013 and 2022, aggregate annual spending by the 50 state governments, excluding federal funds, increased 51.7%. Total annual federal spending rose 69.4% during the decade, more than three times as fast as the 21.6% increase in the rate of population growth plus inflation. If government grows faster than this rate, then it is growing faster than what the average taxpayer can afford. Had the federal government limited the growth in spending to a maximum of the population growth rate plus inflation during that decade, in 2022 the federal government would have spent $1.6 trillion less than it did, resulting in at least a $200 billion surplus. If the federal government had done this over the past two decades, the national debt would have increased by less than $500 billion instead of $19 trillion. If state governments had limited spending growth to the rate of population growth plus inflation during the last decade, they would have spent $1.39 trillion in 2022, $344 billion less than the $1.74 trillion they actually spent. Had federal and state governments simply grown no faster than the rate of population growth plus inflation, taxpayers could have been spared at least $2 trillion in taxes and debt in 2022 and trillions of dollars more over time. The U.S. hasn’t needed drastic budget cuts, just slower, more sustainable debt growth. Our project defines each state’s overspending problem by providing a dollar-figure spending ceiling and allowing anyone to see how government spending in a state has grown relative to the rate of population growth plus inflation. It will publish and promote an annual benchmark spending level for every state, which lawmakers must not exceed if they want to keep state spending in check. Limiting state spending to the Sustainable Budget Project benchmark isn’t impossible. Lawmakers in more states are beginning to implement the sorts of structural reforms necessary to slow the rate of government spending to a sustainable clip. During the past decade, Colorado and Texas have demonstrated that this can be done. Colorado spent a cumulative $12.8 billion less over the past decade than what could have been available under the benchmark. State lawmakers could have dramatically cut the state’s individual income tax. Instead, there is a push in Colorado to raise taxes and destroy the Taxpayer’s Bill of Rights, the state’s constitutional requirement that all tax increases be subject to voter approval and revenue collected in excess of the state spending cap be refunded to taxpayers. Texas spent $16.4 billion less than the benchmark over the past decade, savings that could have been used to eliminate its gross-receipts-style franchise tax and other bad taxes. Rather than continuing to keep state spending in check, Texas lawmakers instead passed the largest state budget in the state’s history this year. Excessive spending at the federal, state and local levels of government deserves more attention. Tax hikes are easy to identify, but there has been no objective, binary metric to determine whether a state government spends too much. By focusing on the rate of population growth plus inflation, the Sustainable Budget Project provides such a standard. Governors and state legislators need to implement reforms and practice restraint to slow the steep upward trajectory of government spending. That lawmakers in large, politically important states have already demonstrated this ability has shown their counterparts in other states and in Washington that sustainable budgeting is possible. With more modest growth in state government spending, lawmakers can lower taxes and Americans can keep more of what they earn. Mr. Norquist is president of Americans for Tax Reform. Mr. Ginn, a senior fellow at ATR, served as chief economist of the White House’s Office of Management and Budget, 2019-20. Originally published at Wall Street Journal.  This commentary was originally published at The Center Square here.

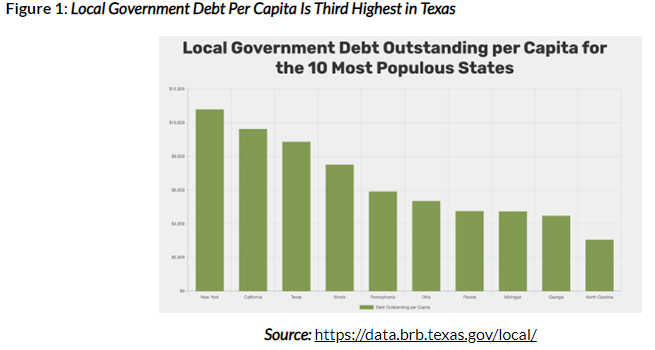

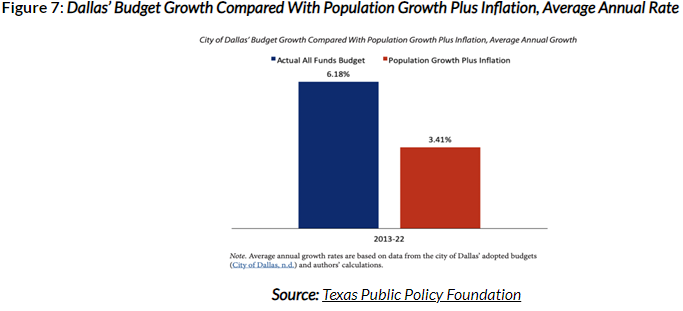

If you live in Texas, then your property taxes are skyrocketing. This has made housing less affordable, especially for the neediest among us. The Texas Legislature passed what some are calling the “largest property tax cut in Texas history,” but it’s the second largest. Regardless, the amount of lower tax bills will likely be underwhelming and leave voters with a bad taste in their mouths come election time next November. There have been some bright spots, but they’re dimming quickly. Dallas was one place that showed promise. Its city council passed the largest budget in city history, going against Mayor Eric Johnson’s (a Democrat who recently stated he will switch to be a Republican) wishes. He aptly voiced what most Texans are thinking in Dallas and beyond about the perils of big budget increases: “In an environment of such economic uncertainty for our residents and businesses, with inflation and interest rates being where they are, I simply could not vote for a budget that is the largest in the history of the city and that is paid for by raising taxes on our residents and businesses.” This increase will completely override the city passing a one-cent tax rate decrease, making people’s property bills 8 percent higher due to rising property values. Dallas is exhibiting on a smaller scale what occurred at the state level a few months ago. Despite the Texas Legislature passing the state’s second-largest property tax cut of $12.7 billion to reduce school district maintenance and operations (M&O) property taxes earlier this year, half of the property tax burden is imposed by other local governments. Because many localities, like in Dallas, are poised to raise property taxes, there are very few places where taxpayers will see a lower property tax bill despite the statewide tax cut. Or, like in Dallas, many local governments pursuing “cuts” will render it irrelevant with excessive spending. Certainly not what should be expected from such a large state tax relief package. And this is likely to hurt Republicans in the next election as they (wrongly) sell this as the “largest property tax cut in Texas history.” Mayor Johnson has it right that reining in spending is crucial to providing tax relief. When spending outpaces a responsible budget, and Dallas’ has for decades, higher taxes and less economic growth have resulted. This is why the biggest governmental burden is always spending, not taxes. Excessive government spending by primarily blue localities in a sea of red helps explain why Texas has some of the most burdensome property taxes nationwide. But Texas is also running up massive debts for even more spending to get around the requirement to pass a balanced budget. The Lone Star state’s total outstanding local government debt is $280 billion, making its local debt per person third most among the top 10 largest states. Regarding local debt, Texas looks much more like New York and California (largest debts per capita) than its southern counterparts, like Florida, where the debt per person is about half of that in Texas. To get spending, and therefore taxes, under control, Texas needs to adopt a responsible budget at the state and local levels. This responsible budget provides a limit that does not exceed what the average taxpayer can afford to fund, restricting the budget to the maximum rate of population growth plus inflation. Ideally, spending should always be below this fiscal rule, but even meeting that cap could save taxpayers billions of dollars. For instance, had Dallas followed this responsible budget model yearly since 2013, the city would have saved $3.4 billion by 2022. This results in substantially higher property taxes in these localities, with similar results in other localities across the state than otherwise. Implementing this budget rule would also result in substantial surpluses because tax revenues generated from sales taxes, fines, and fees typically increase faster than this rule. Through these surpluses, property taxes could be reduced until they are zero. Cities that do this would create so much competition that other cities would be compelled to use their other current revenue sources to reduce their property taxes, leading to the state having much more competitive property taxes overall. With the most competitive rate being zero. That’s one step. The second step to take Texas to the top is to do the same at the state level. The state legislature recently took two steps back and one step forward by passing its largest budget increase in the state’s history in tandem with its hefty property tax cut. But if they stick to the same fiscal rule or, even better, a “Frozen Budget,” they can use surplus funds generated to buy down school district M&O property tax rates each period until they’re eliminated. This process would also take about a decade for the state to fund 100% of the state’s school finance formulas as intended by the Texas Constitution. While Texas boasts many freedoms, including no personal income tax and a business-friendly climate, its burdensome spending and property taxes reduce opportunities for people to flourish. Immediate fiscal restraint at the state and local levels is required for the Lone Star State to continue thriving by seeking to eliminate property taxes. Texans deserve to stop renting from the government and start owning property. Limiting spending is the catalyst to take us there. And localities passing the no-new-revenue rate that would cover all property taxes collected would be a great path eventually eliminating property taxes to better let people prosper.  In 2023, Americans for Tax Reform launched The Sustainable Budget Project, a new venture that monitors state government spending and tracks which states have or have not enacted sustainable budgets.

The Sustainable Budget Project defines a sustainable budget as one that limits the pace of state government spending to lower than the rate of population growth plus inflation, which accounts for the average taxpayer’s ability to pay for government spending.

From 2013 to 2022, the following happened:

There four states that held growth in state funds and all funds below the rate of population growth plus inflation over the last decade, thereby keeping taxes lower than the average taxpayer can afford:

Go to ATR's Sustainable Budget Project to find out the following information:

Originally posted at Americans for Tax Reform. Read the full paper here. Here's the original post by the Pelican Institute. Pelican Institute reform plan would flatten personal and corporate taxes, boost jobs in first year. Baton Rouge — As candidates for Louisiana governor debate the future of the state, a new poll shows Louisiana voters strongly support phasing out the state’s income tax while ushering in fiscal responsibility. Today, the Pelican Institute has released a new tax reform plan that would do just that—transform the state, make it more competitive, pave the way for more and better jobs, and launch Louisiana’s comeback. By a wide margin, 58% of Louisiana voters support phasing out the state income tax (only 20% oppose), and 66% want leaders to prioritize responsible budgeting and limiting the growth of state spending to bring fiscal stability to state government (only 9% oppose). Voters also strongly back education freedom; 62% support giving Louisiana parents the ability to use state funds to select the school of their choice for their child’s education (only 25% oppose). The poll, which was conducted by Cor Strategies in partnership with the Pelican Institute, can be seen here. In Louisiana’s Comeback: A Tax Reform for Our Brighter Future, the Pelican Institute identifies the state’s significant tax problems and proposes a path to set the state in a brighter direction, including flattening the personal and corporate income taxes to 3.5% rates, reducing the number of tax preferences, eliminating the corporate franchise tax and the inventory tax, and reforming the budget to limit the growth of spending, among other changes. “If we are to write Louisiana’s comeback story, we first have to get our fiscal house in order and fix our broken tax code that has, for far too long, landed Louisiana at the bottom of every good list and the top of every bad list,” said Daniel Erspamer, Chief Executive Officer of the Pelican Institute. “Louisiana families are suffering, and too many of our best and brightest are leaving the state to find opportunity elsewhere. It’s time to embrace a bold vision for tax reform proven to bring jobs and opportunity – not to mention our kids and grandkids – back to our state.” Louisiana suffers under a tax system that is brutally punishing for families and businesses. It is painfully progressive, thereby increasing tax rates as more income is earned—and that disincentivizes greater earnings, reduces productivity, and slows economic growth. Meanwhile, tax preferences create exemptions and deductions that make compliance costly, pick winners and losers, and narrow the tax base. That, in turn, requires an even higher tax rate to collect needed revenue for funding limited government. On top of that, Louisiana’s taxes on businesses are particularly burdensome, including a triple taxation on profit, investment, and inventory, that together stifle economic growth. The Pelican Institute’s tax plan solves these problems with a proposal that will kickstart the economy into immediate growth and increase the number of available jobs in the state in the first year. The plan is the latest part of the Pelican Institute’s Comeback Agenda released in March of this year, which lays out a series of policies critical to the state’s future, including tax and budget reform, guaranteeing universal education freedom, enhancing public safety, and reducing regulatory barriers to work. A two-page guide to the reform can be read below and a one-pager below that. Overview

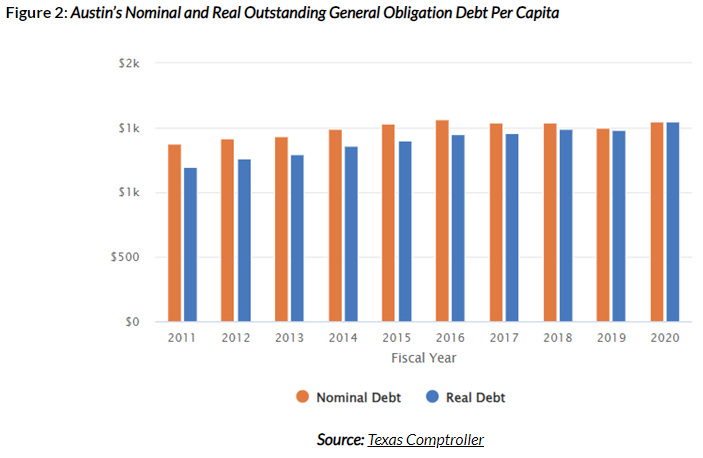

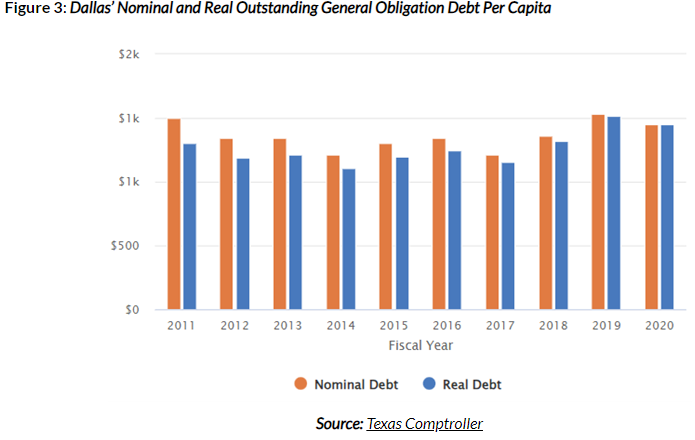

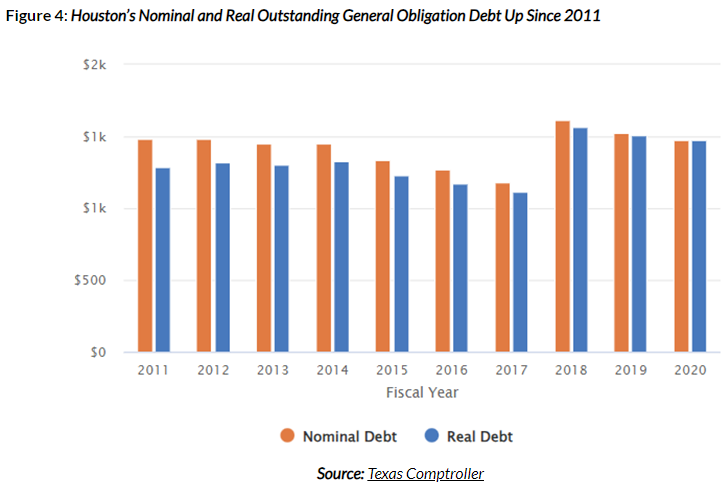

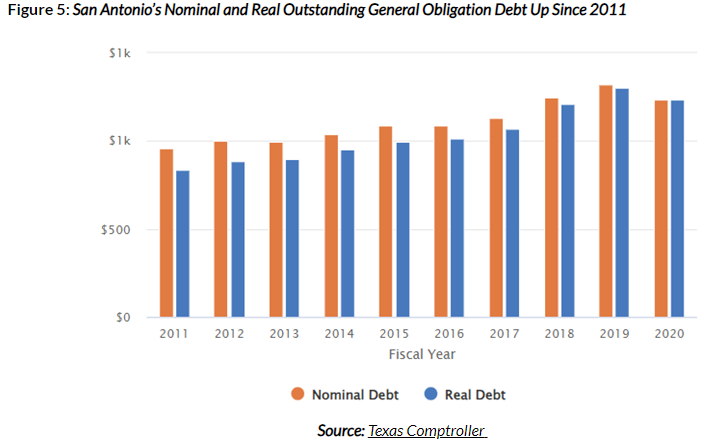

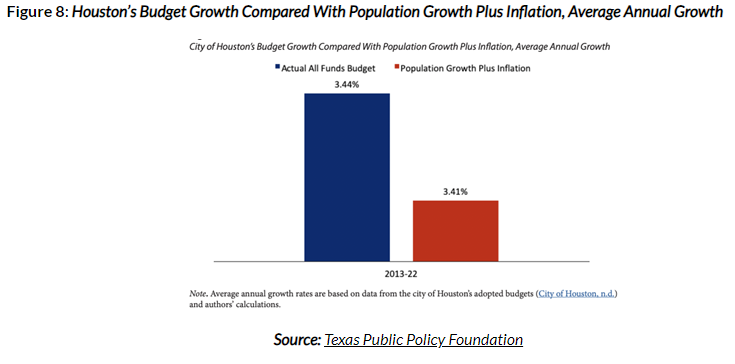

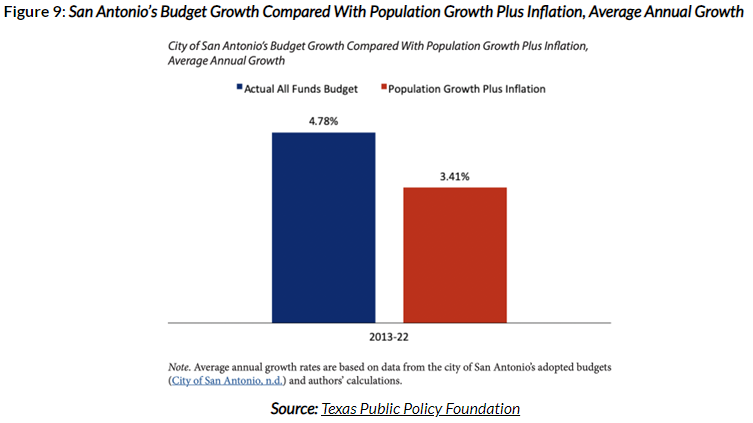

Debt A recent report by the Texas Bond Review Board notes that Texas’ total outstanding local government debt is $280 billion, resulting in debt per capita of $8,869. This puts Texas’ local debt per capita in third place of the largest 10 states, behind only New York ($10,788) and California ($9,621), and nearly twice as high as in Florida ($4,753) (Figure 1).  The following figures show the Texas Comptroller’s data for nominal and real (inflation-adjusted) outstanding general obligation (GO) debt for four of the largest cities in Texas (Austin, Dallas, Houston, and San Antonio). Each of them shows increased GO debt per capita from 2011 to 2020 in nominal and real amounts. But these amounts per capita show some differences.

The unsustainable deficit accumulation across many of Texas’ local governments reflects irresponsible spending. Economist Michael Munger called this “Deficits Are Future Taxes” (DAFT), meaning, increased debt signals a current spending issue and a future taxation problem for the next generations. This is a significant challenge for the state’s future and drives up property taxes higher than otherwise. Spending My analysis in June 2022 found that Texas’ four major cities have exceeded a responsible city budget for years, contributing to higher taxes and debt. This responsible budget sets a maximum threshold based on the average taxpayer’s ability to pay for it, which is best represented by a fiscal rule of a spending limit with the rate of population growth plus inflation. Of course, this growth is a maximum as the budget really should be frozen or even cut for most governments given their spending excesses over time. Truth in Accounting defines the local taxpayer burden as “the approximate dollar amount that would be required of each taxpayer in order to pay off all of a government’s liabilities today. It is calculated by dividing the ‘money needed to pay bills’ by the estimated number of taxpayers in the state or city,” demonstrating the depth of debt.

When local governments want to spend more given their balanced budget requirements, they must raise taxes, and they primarily raise property taxes. Tax Revenue The Texas Comptroller reports that property taxes are the biggest revenue source for local governments. Here are the current total property tax rates for these large cities:

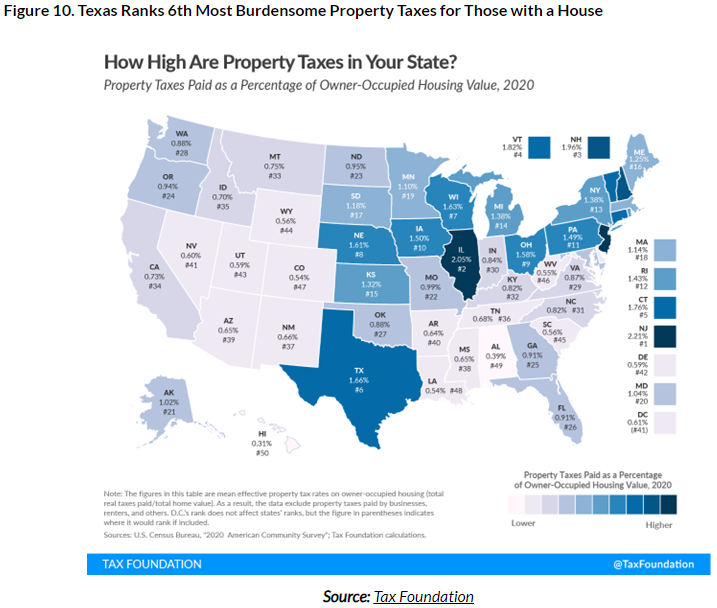

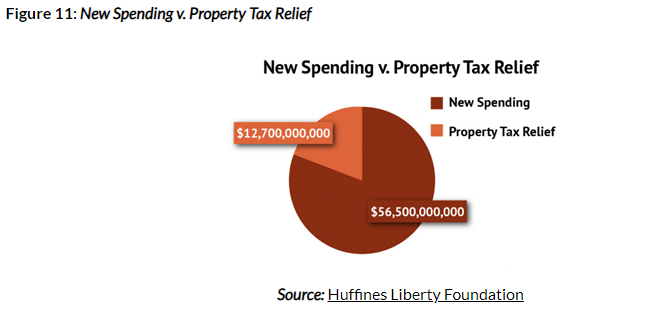

According to the Tax Foundation, Texas currently has the sixth-highest property tax burden on those with a home in the country (Figure 10)  Although the Lone Star State has no income tax, its substantial property tax burden increases because of excessive local government spending increases in recent decades has burdened renters and holders of a home, reducing the state’s affordability. The Tax Foundation’s state business tax climate ranks Texas 38th out of 50 for the burden of property taxes. The Texas Legislature recently passed and Governor Greg Abbott signed Senate Bill 2 with $12.7 billion in property tax relief. This package includes reducing the school district maintenance and operations (M&O) property taxes by 10.7 cents per $100 valuation. It also includes raising the homestead exemption for school district property taxes by $60,000 to $100,000. However, this package should have been much larger, as there were $33 billion in surplus funds available and tens of billions of dollars more available, leaving plenty of taxpayer money to return. The property tax bills provided further complicate the tax system and will not result in as much relief as some are advertising. The best approach was to reduce school district M&O property tax rates with all the relief provided. This should have been at least $21 billion for a reduction of 25 cents per $100 valuation. This would have provided the largest property tax cut in Texas history (Figure 11) instead of the second largest because of the largest spending increase in the state’s history.  Recommendations

For the state to stay competitive and improve the future for Texans, Texas should seek to reform the largest hindrances to its economic flourishing: government spending and property taxes.

Conclusion The ultimate burden of government is not how much it taxes, but how much it spends. This is true at the national, state, and local levels. Texas boasts many metrics of economic freedom, including no personal income taxes, less burdensome regulations, and relatively less government spending. Recent increases in these areas hinder opportunities to prosper. Immediate policy changes to state and local budgeting that will eliminate property taxes, increase transparency for budgets, debts, and taxes, and strengthen their fiscal situation will help Texas better support prosperity for Texans today and for generations to come. Moreover, this will finally give Texans their God-given right to own property instead of renting from the government forever. Stop renting, start owning! Originally published with links to all sources at Texans for Fiscal Responsibility.  Fitch Ratings downgraded the US credit rating from AAA to AA+ because they expect fiscal deterioration over the next few years. While the diagnosis seems delayed, they’re right. Irresponsible bipartisan spending for decades is the culprit. With the national debt approaching $33 trillion, the American economy appears unlikely to recover its AAA status any time soon.

Republicans and Democrats have consistently increased spending more than tax revenues, leading to massive debt and unsustainable deficits. Increased spending under President Biden made a dire situation even worse. For instance, in just five weeks since suspending the debt ceiling, the deficit rose by $1 trillion. Inflation soared once the current administration took office, and still hasn’t leveled off. Real wages are just now catching up with inflation after falling behind for more than two consecutive years. The US dollar’s value has waned. America is not a safe investment, thus the downgrade. Fitch Ratings predicts slower economic growth in the coming years due to high regulations, increased taxes, and demographic changes affecting productivity and population. This slower growth means less tax revenue for the federal government. Also, mandatory spending on Social Security and Medicare, which make up the bulk of federal spending, is projected to grow rapidly, contributing to rising deficits that will soon have just net interest payments exceed spending on national defense. Americans can expect their wallets to be tangibly affected soon. The downgrade will contribute to even higher interest rates than otherwise, which will have a domino effect on various aspects of the economy, including the stock market. Unless severe corrective measures are taken, the situation will likely deteriorate further, impacting people’s prosperity and perpetuating a debt and stagflationary situation. The government should focus on fiscal responsibility and better budget management to avoid a deepening spending crisis, exacerbating Americans’ existing economic burden. First, an approach of zero-based, performance-based budgeting should be implemented throughout the government to identify and eliminate ineffective programs. Second, independent audits by private entities of government spending for programs would provide transparency and guide decision-making regarding which programs to retain, modify, or cut. Third, but likely most important, implementing a fiscal rule that has worked at the state level, such as population growth plus inflation for a maximum budget growth rate, could cap the government’s debt accumulation and support more economic growth. Had such a rule been adopted over the last two decades, the national debt increase would have been significantly lower, by just $500 billion instead of the actual $19 trillion, allowing for better debt management. The US credit downgrade should be a sobering wake-up call that urges Congress and the administration to prioritize fiscal responsibility. As the nation faces economic challenges and increasing debt burdens, it is crucial to adopt prudent measures to put America back on a path to prosperity. Only through concerted efforts to control spending, implement effective budgeting practices, and consider the long-term economic impact of policy decisions can America chart a sustainable and prosperous course for the future. Otherwise, buckle up. It’s going to be a bumpy ride. Originally published at AIER.  Texas Governor Greg Abbott (R) recently signed into law the tax relief compromise by the Legislature’s second special session. This relief is historic with the country’s largest tax cut and the largest net tax cut in Texas history.

But it falls short of what Texans were promised of the largest property tax cut in the state’s history, as it’s instead the state’s second largest property tax cut because of the largest spending increase in Texas history. Rather than providing substantial relief and simplifying the property tax system, the package presents a burdensome approach that could hinder the state's progress. By overspending and adopting a convoluted tax relief strategy, Texas risks falling behind states rather than leading the way in addressing real property tax concerns. The deal provides $12.7 billion in new property tax relief out of the nearly $33 billion surplus as the Legislature increased the upcoming 2024-25 biennial budget by more than 30% in state funds. This is the largest increase in Texas history and well above the the key rate of population growth plus inflation of 16% over the last two years. The major target for property tax relief was reducing school district maintenance and operations (M&O) property taxes. These property taxes are essentially a statewide property tax, which is prohibited by the state’s constitution, as they are partially determined by the state’s school finance system that includes redistribution of property taxes from school districts with high-valued property to districts with lower-valued property. Of the nearly $33 billion in state surplus funds and tens of billions more in new revenue available, the state allocated just $7.1 billion for a modest 10.7-cent reduction per $100 valuation in those property tax rates, called “compression,” which provides long-lasting relief and benefits everyone. The other $5.6 billion is for raising the homestead exemption by $60,000 to $100,000 for the appraised value of primary residences to determine how much is paid for school district property taxes. But this will be short-lived as valuations rise quickly and has failed to provide long-lasting relief the last three times it’s been tried in Texas since 1997 while benefitting only only homeowners. The $12.7 billion over the next two years will hardly alleviate the burden of property taxes on Texans and is a far cry from eliminating them altogether as Gov. Abbot initially set out to do. The package also includes a pilot project of an appraisal cap on non-homestead property at 20% per year for three years. This property doesn’t have a cap on it today so this will benefit some but will mean that local governments will just ratchet up property tax rates to bring in the tax revenue they desire to grow spending. There will also now be three elected officials added to county appraisal boards. Texans are left with this compromise package that unnecessarily complicates the tax system and obstructs efforts to eliminate school M&O property taxes, enabling the government to pick winners and losers. In this case, renters would undoubtedly be among the losers, and they are nearly 40% of households across the state. A more robust approach is necessary soon to achieve significant, long-lasting property tax relief for Texans. The best path being discussed is to buy down school district M&O property tax rates with surplus funds starting with limiting government spending, which was lacking this session after years of an improving budget picture. Ways to improve this overall package would have been by institutionalizing the buy-down plan and imposing spending limits on local governments. The final part of the package is $600 million to raise the exemption of gross receipts to pay franchise taxes from $1 million to $2.47 million, which is important but doesn’t help reduce property taxes and is less effective than cutting the franchise tax rates until they’re zero. This brings the total amount of new tax relief to $13.3 billion. This amount is lower than the $14.2 billion that the Legislature provided to buy down school property taxes in 2008-09, which would be about $21 billion to have the same purchasing power today. And even if you include the state maintaining its property tax rate reduction in 2019 of $5.3 billion in this year’s budget for a total of about $18.6 billion, it would not equal $21 billion. But that 2008-09 relief was done by raising bad taxes of the franchise tax, sales tax on motor vehicles, and cigarette tax which this time no taxes are raised as the taxpayer funds come from surplus money. So, this 2023 tax relief package can be called the “largest net tax cut in Texas history” but not the “largest property tax cut,” and is the largest tax cut in the country. But Texans could have had more relief if the state hadn’t spent so much. Eliminating school property taxes is a crucial next step for Texans to truly own their homes instead of renting from the government forever. And this will be achieved faster when politicians stop spending so much. So while this historic relief is much appreciated, there’s much more to do next session for Texans to stop renting and start owning. Originally published at Real Clear Policy. For at least a decade before the pandemic, Tennessee leaders have practiced conservative budgeting, keeping increases in state spending below population growth plus inflation. This saved Tennessee taxpayers billions of dollars, allowing for further pro-growth tax cuts. As the state is finally spending the last of its federal relief funds, it is more important than ever that Tennessee leaders practice conservative budgeting and fiscal restraint, correct for those excesses, and return to pre-pandemic spending trends. The Conservative Tennessee Budget ensures that the burden on Tennessee families to fund the state government will not increase beyond their ability to pay for it. For the upcoming FY 2025 budget, that maximum threshold would be $59.45 billion. By appropriating below that amount, Tennessee policymakers will continue to give taxpayers the best opportunity to prosper and live their version of the American dream. Finally, Tennessee should make this CTB approach the law of the land by improving the state’s current spending limit with this stronger limit to best let people prosper. Originally published at Beacon Center. Overview

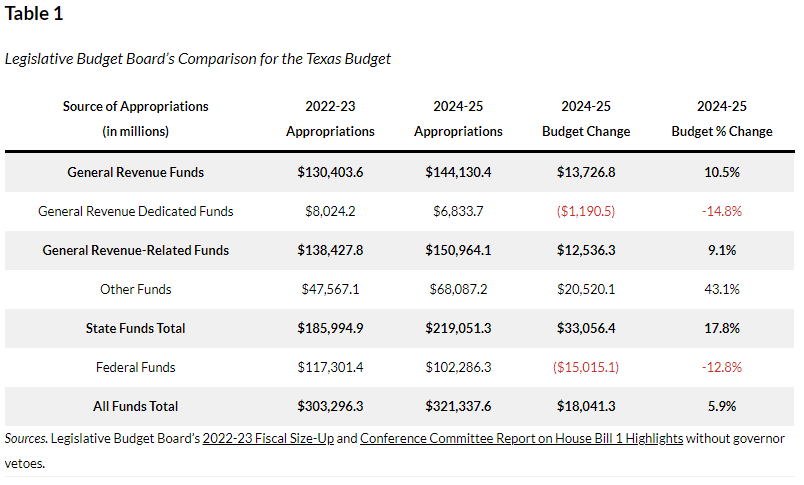

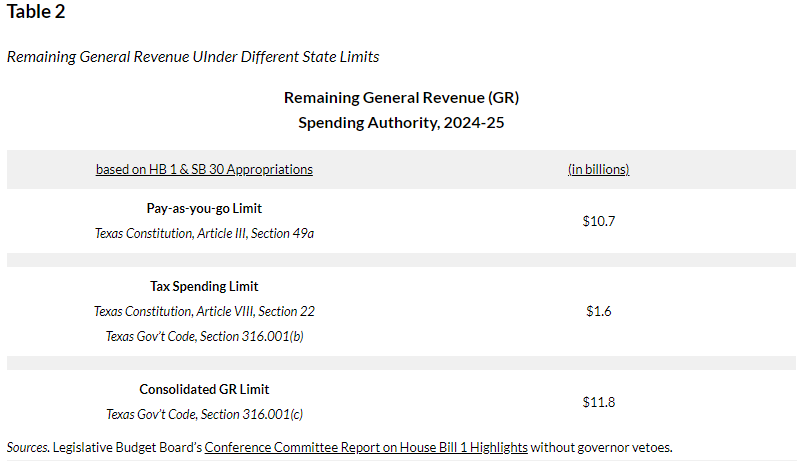

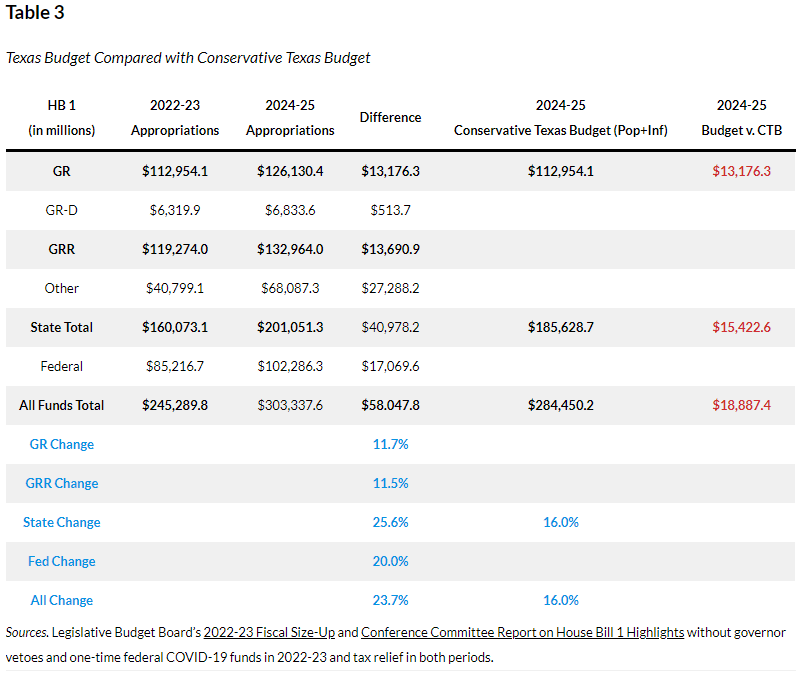

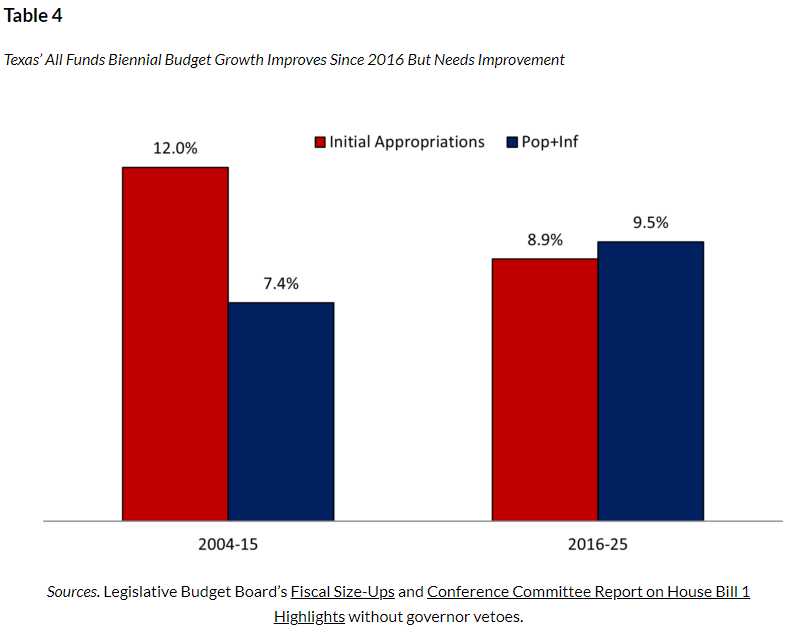

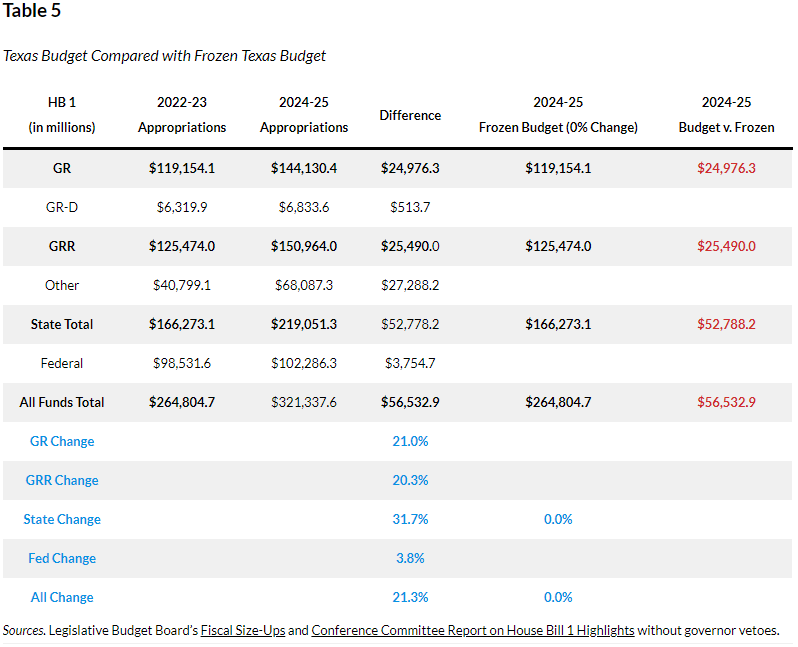

Texas Passes Largest Budget Increase in Texas History Texas Governor Greg Abbott (R) recently signed the Texas budget (HB 1) passed by the 88th Texas Legislature with the largest spending increases, the largest corporate welfare increases, and the largest social safety net increases—without the largest property tax cuts—in Texas history. State officials can claim that the budget increases by less than the rate population growth and inflation using the data in Table 1 by the Legislative Budget Board.  But those calculations use fuzzy math, as they’re based on inflating the 2022-23 base budget of general revenue not dedicated by the Constitution and consolidated general revenue with more spending, then increasing it by the rate of population growth times inflation of 12.33% (determined by the average of population growth times inflation over the last two years and the upcoming two years). Compare this with 2024-25 appropriations, which will be higher later when the supplemental bill passes. These calculations are then spending-to-appropriations, which is like comparing apples with oranges. Even with these calculations, the Legislative Budget Board shows in Table 2 that there is $10.7 billion in tax revenue remaining, $1.6 billion available under the constitutional spending limit using general revenue not dedicated by the Constitution, and $11.8 billion available under the 2021 spending limit with consolidate general revenue using general revenue and dedicated general revenue.  While the data in Table 1 provides an apples-to-apples budget comparison, the charts below are more accurate ways to evaluate the budget growth from an appropriations-to-appropriations approach. Better Comparisons for Budget Growth Understanding that any growth in the budget means an expansion of government, there are two strong arguments for limiting government spending: 1) Table 3 shows data for freezing the budget in inflation-adjusted per capita terms using the rate of population growth plus inflation (i.e., Conservative Texas Budget and responsible budget approach in other states), which was 16% over the last two fiscal years. This approach is appropriate as it grows slower than the economy over time. It also excludes $13.3 billion in COVID-related funding in the first biennium as well as new and old tax relief amounts of $6.2 billion ($100 million in new relief) in the first period and $18 billion (i.e., amounts passed in HB 1 of $5.2 billion for old relief and the latest of $12.7 billion in new relief during the second special session). Excluding these helps to not include one-time federal funding and amounts that don’t grow government.  Using the CTB approach above, Table 4 highlights how the budget has improved since implementation of the CTB started with the 2016-17 budget. This looked much better before the current 2024-25 budget, but the massive growth of the current budget raised the growth of initial appropriations even as the rate of population growth plus inflation rose slightly during the latter five-budget period. If the growth of the budget is not controlled, it will soon surpass the rate of population growth plus inflation like it did during the prior six budget periods.  2) Table 5 shows freezing the budget with zero growth as the budget is already too big (i.e., Frozen Budget), including COVID-related funds in the first period and new and old property tax relief amounts in both periods.  Conclusion