|

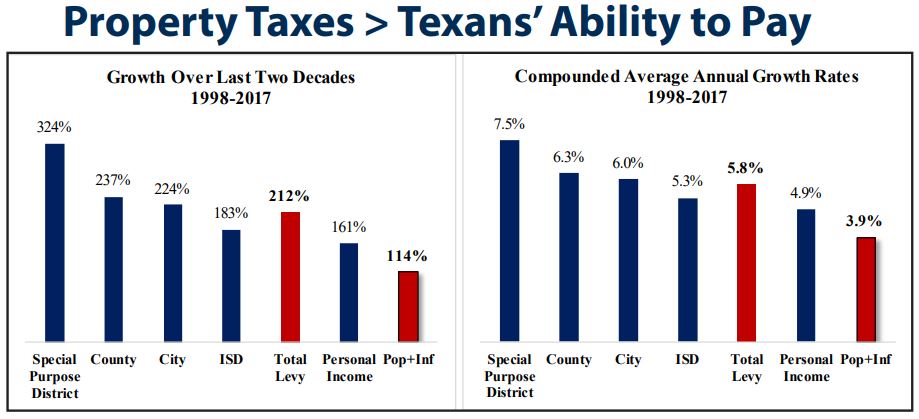

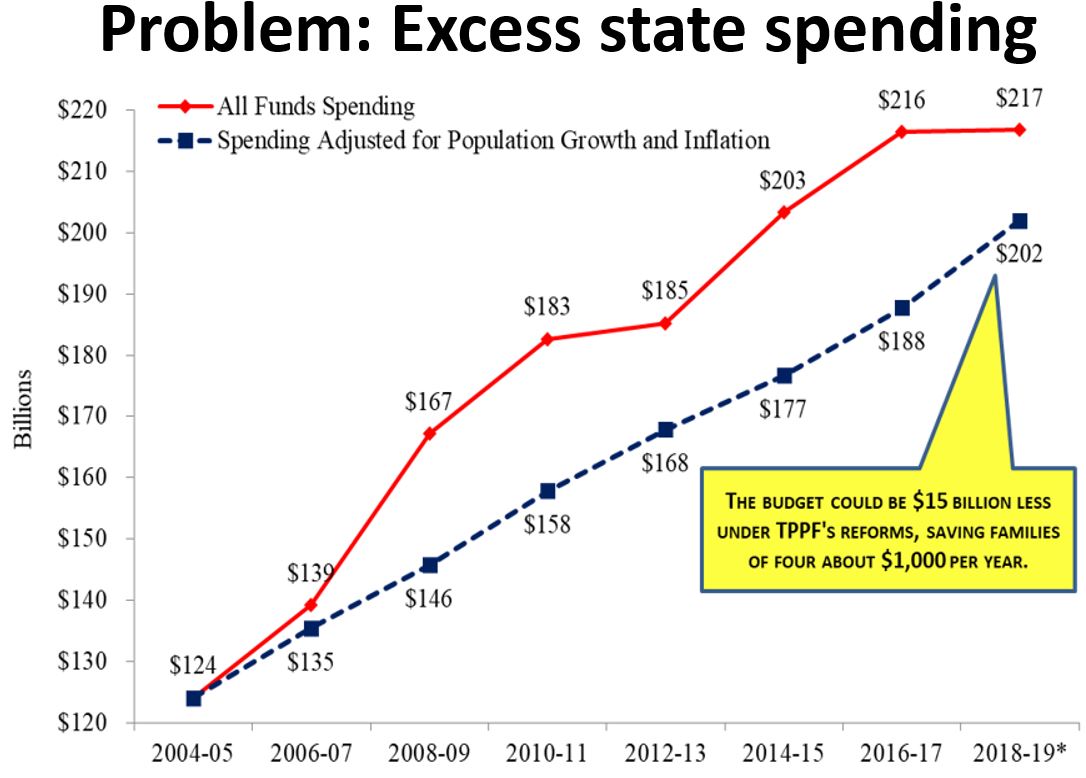

Despite the economic success of the Texas Model of fiscally conservative governance, a skyrocketing local property tax burden remains one of the state’s most pressing policy challenges. Property taxes have been growing faster than Texan’s ability to pay for them, increasing the need to eliminate them.  You get less of whatever you tax. This key economic insight suggests the best type of taxation does the least economic harm, achieved by limiting government spending to only securing liberty. The evidence is clear that Texas should never have a personal income tax. There is nearly a consensus that is true, but there is a growing consensus that Texas should eliminate property taxes that keep Texans renters forever.  Property taxes are an inefficient type of tax. They are based on primarily subjective valuations by appraisal review boards and determined tax rates by local tax entities with little to no feedback from citizens. Given the rising property tax burden and its inefficient collection mechanism, they should be eliminated in exchange for a more efficient, slower-growing sales tax based on objective market transactions that would help appropriately remove taxes on capital (i.e. property)—the driver of the wealth of states.  Property taxes are more regressive than a sales tax. Opponents of a sales tax say it is too regressive, whereby people with lower incomes people pay a larger share of their income to taxes than those with higher incomes. The Texas Comptroller’s recent report confirms that both sales taxes and property taxes are regressive, according to the “suits index” (see following two tables), but suggests property taxes are less regressive. However, this analysis (and others like it) do not account for the fact that sales taxes are paid once at purchase yet property taxes are paid annually, hurting low- and fixed-income Texans the most because the costs compound over time. A property tax also keeps people from getting their first home and kicks many people out of their home and business. Appropriately accounting for these cumulative costs indicates a property tax is more regressive.   Texas should ultimately have only a single-legged barstool in the form of a broad-based sales tax. Some talk about the need for a three-legged stool of taxation. These legs include a sales tax, property tax, and a personal income tax. Because Texas appropriately doesn’t have the latter, the argument is that there is a need for the other two. But that’s incorrect. Texas needs the most efficient tax system possible to fund limited government. That’s done by expanding the sales tax base as wide as possible to not pick winners and losers to keep the rate as low as possible. There are paths to swapping out city and county property taxes with a higher local sales tax rate if the state doesn’t broaden the base. This is also a good option as it provides a direct funding source for local governments’ maintenance and operations if, and only if, they eliminate the property tax with a revenue neutral swap. Ideally, the sales tax rate would not be allowed to ratchet up further after the swap and the property tax could never come back. The school district maintenance and operations property tax, which comprises about 45 percent of the total property tax burden in Texas, could also be swapped out with a sales tax. A broader sales tax base could allow the rate to fall. Here is an overview of possible rates and sales tax bases to eliminate the school district M&O property tax in Texas with 2017 data, which the ideal option would be to expand the base and not tax property, as property is capital that supports economic prosperity.  Texas should limit spending to limit taxes. While sales tax collections can be more volatile than property tax collections from economic changes, sales taxes better reflects taxpayers’ ability to pay than a property tax that they have little control over. Also, property taxes often don’t reflect the economic climate but rather the whims of appraisal districts and local officials that hurt property holders in the process when their incomes are falling. More importantly though, Texas governments must practice spending restraint so that excessive spending doesn’t drive taxes higher than taxpayers’ ability to pay. High taxes are always and everywhere a spending problem.  This is why there is need to limit spending growth to no more than population growth and inflation, two key measures that reflect the ability to pay from more people and wage growth that’s highly correlated with inflation. By practicing spending restraint, excess taxpayer dollars can be used to lower the sales tax rate after a swap or could even be used to cut the school M&O property tax in the meantime until the elimination of school districts’ maintenance and operations property taxes.

By practicing fiscal restraint and eliminating all taxes in Texas except for a broad-based sales tax, the Texas Model would support even greater prosperity for all Texans.

0 Comments

Leave a Reply. |

Vance Ginn, Ph.D.

|

RSS Feed

RSS Feed

Proudly powered by Weebly