|

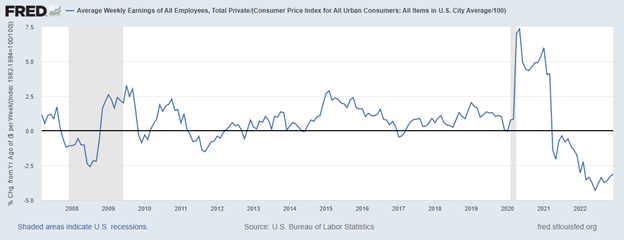

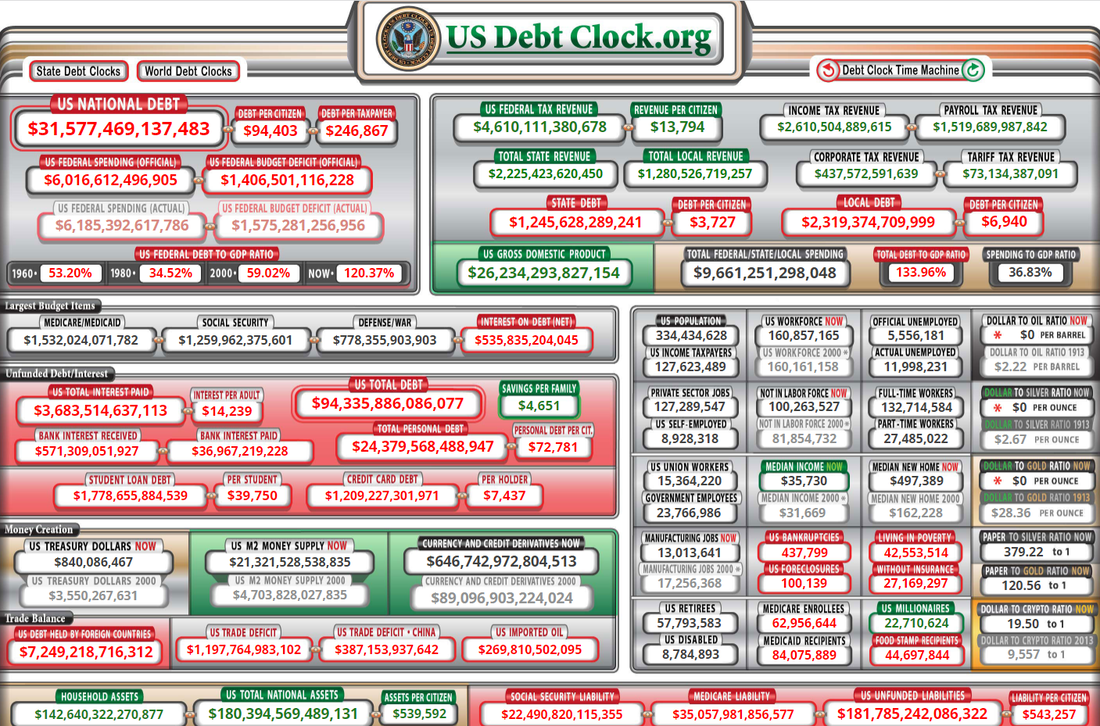

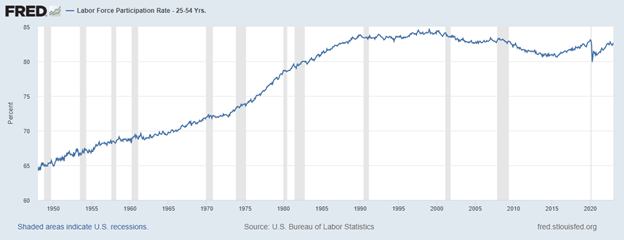

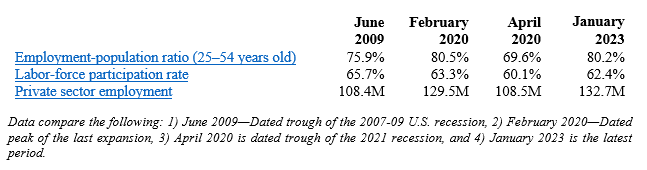

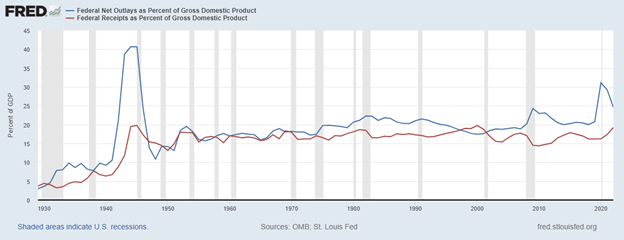

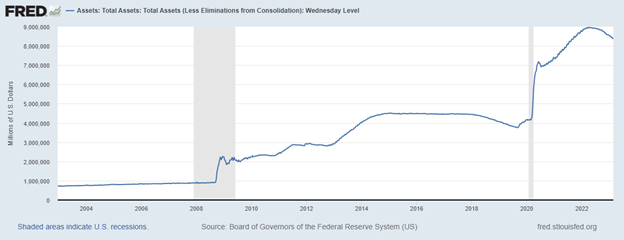

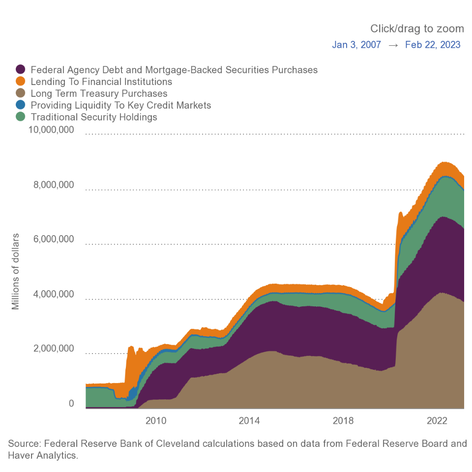

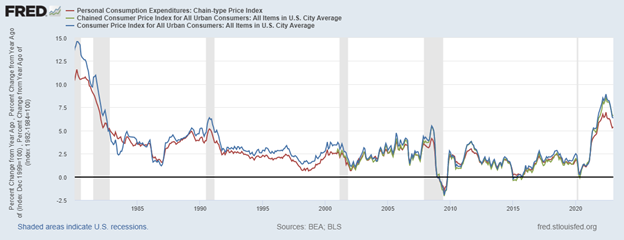

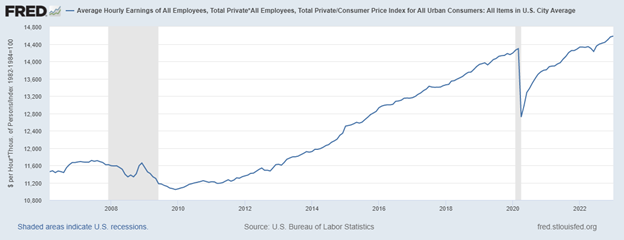

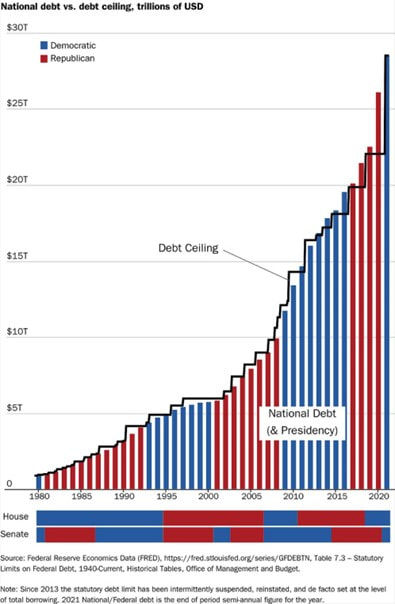

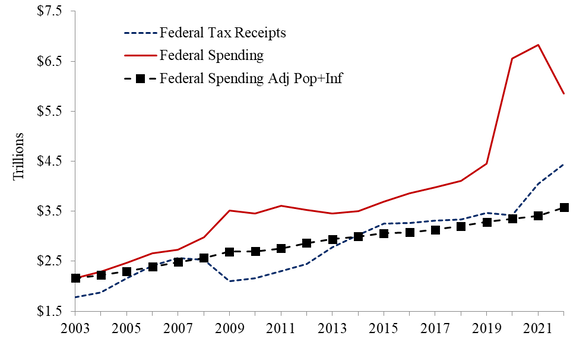

Key Point: The U.S. economy in 2022 had the slowest Q4-over-Q4 growth during a recovery since at least 2009 and average weekly earnings are now down for 22 straight months as inflation keeps roaring. But there’s hope if we just give free-market capitalism a chance to let people prosper.  Overview: Although President Biden recently tried to claim that the state of the union is strong, facts tell a different story. The government failures that drove the “shutdown recession,” high inflation, and weak economic growth over the last three years continue to plague Americans. This includes excessive federal spending leading to massive deficit spending adding up to $7 trillion since January 2020 to reach nearly $31.5 trillion in national debt—about $250,000 owed per taxpayer. This has created a fight between the Biden administration and House Republicans over the debt ceiling, as raising it must come with spending restraint to avoid some of the fiscal insanity that will lead to insolvency if nothing is changed. And more inflation could be on the horizon if the Federal Reserve chooses to monetize more more of the new debt, which past excess has already contributed to 40-year-high inflation rates. These government failures with little relief from pro-growth policies in sight mean that things will get worse before they get better.  Labor Market: The Bureau of Labor Statistic recently released its U.S. jobs report for January 2022. This report came with substantial revisions to seasonal adjustments and population estimates which could bias the data for a while given that the revised estimates include the much of the last three years of data that are highly volatile. And recall the recent report by the Philadelphia Fed finds that if you add up the jobs added in states in Q2:2022 there were just 10,500 net new jobs rather than more than 1 million reported. The establishment survey shows there were +517,000 (+3.3%) net nonfarm jobs added in January to 155.1 million employees, with +443,000 (+3.6%) added in the private sector and +74,000 (+1.4%) jobs added in the government sector. Most of the private sector jobs were added in the sectors of leisure and hospitality (+128,000), private education and health services (+105,000), and professional and business services (+82,000), which these three sectors led over the last 12 months as well; information (-5,000) and utilities (-700) were the only net job declines over the last month and no sector had net job losses over the last year. Average hourly earnings for all employees was up by 10 cents last month to $33.03, or up by +4.4% over the last year. And average weekly earnings in the private sector increased by $13.35 last month to $1,146, or up by +4.7% over the 12 months. The household survey had another large increase of +894,000 jobs added to 160.1 million employed There have been declines in net jobs in four of the last 10 months for a total increase of +1.8 million since March 2022, which is about half of the +3.6 million of the net jobs added per the establishment survey. The official U3 unemployment rate declined slightly to 3.4% which is the lowest since 1969. But challenges remains as inflation-adjusted average weekly earnings were down -1.5% over the last year for the 22nd straight month, weighing on Americans budgets to make ends meet. And since February 2020 before the shutdown recession, the prime age (25-54 years old) employment-population ratio was 0.3-percentage point lower, prime-age labor force participation rate was 0.3-percentage point lower, and the total labor-force participation rate was 0.9-percentage-point lower with millions of people out of the labor force thereby holding the U3 unemployment rate much lower than otherwise.   Economic Growth: The U.S. Bureau of Economic Analysis’ recently released the 2nd estimate for economic output for Q4:2022. The following table provides data over time for real total gross domestic product (GDP), measured in chained 2012 dollars, and real private GDP, which excludes government consumption expenditures and gross investment. And most of the estimates for Q4:2022 and growth in 2022 were revised lower, providing more evidence that 2022 was a very weak year if not a recession.  The shutdown recession in 2020 had GDP contract at historic annualized rates because of individual responses and government-imposed shutdowns related to the COVID-19 pandemic. Economic activity has had booms and busts thereafter because of inappropriately imposed government COVID-related restrictions in response to the pandemic and poor fiscal policies that severely hurt people’s ability to exchange and work. Since 2021, the growth in nominal total GDP, measured in current dollars, was dominated by inflation, which distorts economic activity. The GDP implicit price deflator was +6.1% for Q4-over-Q4 2021, representing half of the +12.2% increase in nominal total GDP. This inflation measure was +9.1% in Q2:2022—the highest since Q1:1981—for a +8.5% increase in nominal total GDP that quarter. This made two consecutive declines in real total (and private) GDP, providing a criterion to date recessions every time since at least 1950. In Q3:2022, nominal total GDP was +7.6% and GDP inflation was +4.4% for the +3.2% increase in real total GDP. But if inflation had been as high as it was in the prior two quarters or had the contribution of net exports of goods and services (driven by natural gas exports to Europe) not been 2.9%, real total GDP would have either declined or been essentially flat for a third straight quarter. In Q4:2022, there was a similar story of weakness as nominal total GDP was +6.6% and GDP inflation was +3.9% for the +2.7% increase in real total GDP. But if you consider the +2.7% real total GDP growth was driven by contributions of volatile inventories (+1.5pp), government spending (+0.6pp), and next exports (+0.5pp) which total +2.6pp, the actual growth is quite tepid like it was in Q3:2022. For all of 2022, real total GDP growth is reported +2.1% year-over-year but measured by Q4-over-Q4 the growth rate was only +0.9%, which was the slowest Q4-over-Q4 growth for a year since 2009 (last part of Great Recession). The Atlanta Fed’s early GDPNow projection on February 24, 2023 for real total GDP growth in Q1:2023 was +2.7% based on the latest data available. The table above also shows the last expansion from June 2009 to February 2020. A reason for slower real private GDP growth in the latter period is due to higher deficit-spending, contributing to crowding-out of the productive private sector. Congress’ excessive spending thereafter led to a massive increase in the national debt by more than +$7 trillion that would have led to higher market interest rates. This is yet another example of how there is always an excessive government spending problem as noted in the following figure with federal spending and tax receipts as a share of GDP no matter if there are higher or lower tax rates.  But the Fed monetized much of the new debt to keep rates artificially lower thereby creating higher inflation as there has been too much money chasing too few goods and services as production has been overregulated and overtaxed and workers have been given too many handouts. The Fed’s balance sheet exploded from about $4 trillion, when it was already bloated after the Great Recession, to nearly $9 trillion and is down only about 6.5% since the record high in April 2022. The Fed will need to cut its balance sheet (see first figure below with total assets over time) more aggressively if it is to stop manipulating so many markets (see second figure with types of assets on its balance sheet) and persistently tame inflation, which there’s likely a need for deflation for a while given the rampant inflation over the last two years.   The resulting inflation measured by the consumer price index (CPI) has cooled some from the peak of +9.1% in June 2022 but remains hot at +6.4% in January 2023 over the last year, which remains at a 40-year high (highest since July 1982) along with other key measures of inflation (see figure below). After adjusting total earnings in the private sector for CPI inflation, real total earnings are up by only +2.2% since February 2020 as the shutdown recession took a huge hit on total earnings and then higher inflation hindered increased purchasing power.   Just as inflation is always and everywhere a monetary phenomenon, deficits and taxes are always and everywhere a spending problem. The figure below (h/t David Boaz at Cato Institute) shows how this problem is from both Republicans and Democrats.  As the federal debt far exceeds U.S. GDP, and President Biden proposed an irresponsible FY23 budget and Congress never passed one until the ridiculous $1.7 trillion omnibus in December, America needs a fiscal rule like the Responsible American Budget (RAB) with a maximum spending limit based on population growth plus inflation. If Congress had followed this approach from 2003 to 2022, the figure below shows tax receipts, spending, and spending adjusted for only population growth plus chained-CPI inflation. Instead of an (updated) $19.0 trillion national debt increase, there could have been only a $500 billion debt increase for a $18.5 trillion swing in a positive direction that would have substantially reduced the cost of this debt to Americans. Of course, part of this includes the Great Recession and the Shutdown Recession, so these periods would have likely been good reason to exceed the limit, but regardless we would be in a much better fiscal and economic situation with this fiscal rule. The Republican Study Committee recently noted the strength of this type of fiscal rule in its FY 2023 “Blueprint to Save America.” And to top this off, the Federal Reserve should follow a monetary rule so that the costly discretion stops creating booms and busts.  Bottom Line: While there appears to be a strengthening labor market in January, let’s see if this continues as my guess is that these were biased from the data adjustments, and we will see a weaker labor market in the months to come. My expectation is that stagflation will continue along with the a deeper recession this year given the “zombie economy” with “zombie labor” of many workers sitting on the sidelines and others are “quiet quitting” along with the failures of many “zombie firms” that live on debt. Ultimately, Americans are struggling from bad policies out of D.C.. Instead of passing massive spending bills, the path forward should include pro-growth policies. These policies ought to be similar to those that supported historic prosperity from 2017 to 2019 that get government out of the way rather than the progressive policies of more spending, regulating, and taxing. The time is now for limited government with sound fiscal and monetary policy that provides more opportunities for people to work and have more paths out of poverty.

Recommendations:

0 Comments

Vance Ginn sits down with Newsmakers to discuss the battle against inflation and the rising interest rates the Fed is imposing yet again. He touches on major economic benchmarks and explains what the numbers are really showing. Watch here: https://www.youmaker.com/video/482a32b6-d37b-47bb-b6db-0ed3d975f04f   The latest inflation report reveals that inflation is slowing, but it remains at a 40-year high.

The stock market rose, as softer-than-expected inflation rate gave investors hope the Federal Reserve may not have to raise its target rate quite as fast. A 7.7-percent increase in prices over the last year shouldn’t make people hopeful. Many Americans can’t afford soaring living expenses, however, and the economy will worsen before there’s any relief. Adding to this struggle are inflation-adjusted average weekly earnings, which are down 4 percent over the last year, and have been declining for nearly two years. This deflating of the American Dream is the result of big-government policies, creating too much money chasing too few goods. Just the necessity of food is a struggle. Food prices at work and school are up 95 percent. Eggs are up 43 percent, and chicken, 15 percent. Gasoline to drive to the store is up nearly 18 percent and electricity, 14 percent, so even making meals at home can rock the budget. To cope with less purchasing power, Americans are not only saving less, they’re also accruing credit card debt, to a record high of nearly $1 trillion. Even in states with comparatively low cost of living, like Texas, people with full-time jobs can’t make ends meet for their families and are showing up at food banks for help. Unfortunately, the worst is yet to come. The Fed’s meager strategy for fighting inflation hasn’t included aggressively cutting its $8.6 trillion balance sheet. The balance sheet is only about 3.8 percent less than its record high in April 2022, after more than doubling during the pandemic. This overprinting of money affects many markets, as those dollars aren’t evenly distributed across the economy, resulting in distorted price signals. The Federal reserve adding assets to its balance sheet (by buying Treasury debt, agency debt, and mortgage-backed securities) kept interest rates artificially low. Those markets are starting to correct, as mortgage rates have risen to 20-year highs of around 7 percent. The Fed created the current inflationary situation (too much money), which was fueled by Congress’s deficit spending, and exacerbated by Biden’s overregulation (too few goods and services). Now, the false “boom” is busting. Hardworking families and entrepreneurs bear the brunt. To combat the problem it helped create, the Fed is raising its target federal funds rate, which has grown at the fastest pace since Paul Volcker was Chairman in the early 1980s. Volcker understood that the Fed’s balance sheet mattered most, which seems to be overlooked by the Fed and many economists today. The Fed’s hike of 75 basis points on November 2 brought the top of the target range to 4 percent, which was the fourth consecutive 75-basis-point hike, after rates were held at essentially zero for two years. The Fed signaled that it will slow target rate hikes to likely 50 basis points in December, pushing the top rate to 4.5 percent by the end of 2022. This would be the highest rate in 15 years. The Fed’s attempt to correct elevated inflation comes too late to avert the economic consequences of keeping the target rate too low for too long. As a result, Americans are suffering from persistent inflation, higher interest rates, and a prolonged, deeper economic recession. What should be done? We need pro-growth policies. The executive branch should focus on cutting regulations. Congress should prioritize making the Trump-era tax cuts permanent, cutting the corporate tax rate, and passing spending limits to help balance the budget. The Fed, the source of so much money mischief, should adhere to a monetary rule that will cut its balance sheet as much as possible, hopefully down to nothing. These pro-growth, liberty-oriented policies will unleash the economic potential of the productive private sector and get people back working again at well-paid jobs, while substantially reducing inflation. Big-government policies must end before they send us further down the road to serfdom. Our newly elected officials have a responsibility to prioritize fighting inflation, and restoring the American Dream. Originally posted at AIER.  While a stagnating economy with high inflation is what economists usually call stagflation, the current situation is worse, as the real economy is declining. So there’s much less to go around for everyone—making us poorer in the process.

This inflation-recession could be resolved by Washington reversing course, but President Joe Biden and Democrats in Congress are doing the opposite. Their new bill, called the “Inflation Reduction Act” (IRA), will spend more, raise taxes, increase debt, and contribute to more inflation, resulting in a deeper recession. The IRA includes estimated hikes in taxes with a new 15% corporate minimum tax rate, 87,000 new Internal Revenue Service (IRS) agents to audit more taxpayers, and new closure of “carried interest loophole.” These are each bad policies, but especially during a recession. These add up to an estimated tax hike of about $730 billion compared with current policy over the next 10 years. The main tax hike is the new alternative minimum tax (AMT) of 15% on book income for corporations with net income exceeding $1 billion. This proposal has a rosy revenue projection of $313 billion. But businesses don’t pay taxes; they just submit them. People pay them, through higher costs, lower wages, and fewer jobs. The dynamic effects will result in less tax revenue collected from this hike. According to a recent study by the Tax Foundation, this tax hike alone would contribute to killing 23,000 jobs, a 0.1% cut in wages, and 0.1% less in economic output. If we consider other provisions like the tax hikes on carried interest and reinstatement of the federal Superfund program, the total number of jobs killed is 30,000 with every income group having a reduction in after-tax income. Clearly, this wouldn’t reduce inflation or help the economy recover. But there’s more. While the IRA is aimed at taxing the rich and corporations more, the Congressional Joint Committee on Taxation finds that every income group except those with income between $10,000 to $20,000 per year would face a higher average tax rate. This would mean President Biden’s pledge to not tax anyone earning less than $400,000 per year would be broken, with about half of the burden falling on those earning less than $200,000 per year. And the $80 billion in additional funding for 87,000 new IRS agents to increase tax enforcement and compliance is expected to bring in a phony amount of about $200 billion over a decade. But this will just increase more bureaucracy in an already overly bureaucratic federal government that will make Americans’ lives worse as they put more costs on taxpayers. Specifically, there could be 1.2 million more individual audits per year, and you can bet when the IRS doesn’t increase tax collections from legal tax returns they will come after every tax group, not just those making more than $400,000 per year. On the spending side, the IRA provides tax incentives and subsidies for unreliable wind and solar energy, an expansion of Obamacare subsidies until 2025, and other expenditures to the tune of about $430 billion. Using these rosy assumptions, there is a projected deficit reduction of $300 billion over 10 years. However, more conservative estimates suggest that the IRA will have less deficit reduction and will likely increase the deficit. The Tax Foundation, Penn Wharton Budget Model (PWBM), and Congressional Budget Office (CBO) calculate a $178 billion, $247.8 billion, and $101.5 billion in deficit reduction over the next decade, respectively. But assuming the Obamacare subsidies are extended over the full 10-year period for an apples-to-apples comparison, the PWBM estimates that would bring that deficit reduction down by $158.9 billion to just $88.9 billion over the decade, which is the same amount of the deficit in just June 2022. But recall that these estimates are compared with current policy assumptions over the next decade, which already have massive deficits because of reckless spending, so the IRA will most likely make the deficit worse. Spending will be permanent and is on the front end of the bill, while taxes will likely be temporary and are more on the back end—so the deficit will be higher in the first few years, which will give the Federal Reserve more debt to purchase thereby creating more inflation. And the higher taxes, more debt, and more inflation will stifle economic growth so a deeper recession will result. The IRA does the opposite of what the name implies. This is now too common with Democrats in Congress as they like to keep redefining things that don’t match their narrative. They should instead name this bill the “Inflation Recession Act” because we will get more of both. This far-left agenda must be rejected. Kill the bill. Published at TPPF with Daniel Sanchez-Pinol  Americans are sacrificing their savings to keep up with soaring inflation.

This burden has contributed to consumer sentiment reaching its lowest level in June since the University of Michigan started the survey in January 1978. And the progressive policies in D.C. could soon make this bad situation worse. The personal saving rate, which is the share of after-tax income not used for consumption, declined again to 5.1% in June. This is after it reached 33.8% in April 2020, which was a record high since January 1959, after the first round of “stimulus” checks sent by Congress during the shutdowns. There were two more rounds of checks sent by Congress, along with enhanced unemployment payments and other handouts that weren’t connected to work, which kept the saving rate historically high as many places were shut down and people made more from handouts than they did while working. Remember, nothing is free. Those handouts and other government spending contributed to more than $6 trillion in additional national debt, which the Federal Reserve then mostly monetized—leading to the generational high in inflation. The higher inflation outpaced saving and income growth since then, as the costly policies came home to roost and cut the saving rate to 5.1%—the lowest since August 2009. What will happen when Americans run out of savings? But there’s little reprieve in sight as inflation looks to keep rising or at least not abating soon from bad policies in D.C. Inflation, which is the loss of purchasing power of your dollar, continues upward to 6.8% in June 2022 as measured by the personal consumption expenditure (PCE) price index—the highest since January 1982. The PCE inflation measure accounts for the substitution effect from high priced goods to lower priced goods. This isn’t reflected in the often-reported measure of the consumer price index (CPI) inflation rate of 9.1%, which is the highest since November 1981. Both measures show Americans’ money isn’t going nearly as far as it did a year ago. In fact, families’ purchasing power is set to be cut in half in just 10 years at the pace of PCE inflation and even faster for CPI inflation. This implies that in order to maintain the same consumption levels, households have to allocate more income to consumption than to savings. And many Americans are turning to increased debt as their savings dry up. Household debt increased to a record high of $16 trillion in the second quarter of 2022. Not surprisingly, credit card debt grew the most by 13%, which is the fastest increase in 20 years. Moreover, household debt to real economic output passed the 80% mark at the end of 2021. It’s up to 82% in the second quarter of 2022, a historically high rate, as debt increased and the real economy declined for two straight quarters. This share will likely get worse in the following quarters as Americans go through their savings and dip further into debt. And interest rates going up means the amount to pay interest on the debt will contribute to higher balances and more pressure to meet their financial obligations. No wonder people don’t feel secure about their economic future. Bad policies by Congress and the Federal Reserve contributed to this destruction and could even make things worse. Congress spent too much, leading to massive deficits, which gave the Fed debt to purchase to inject money into the economy over the last two years. That inflated “boom” had to eventually “bust.” And that’s what is happening now as the redistribution by Congress has slowed some and the Fed is finally raising its target interest rate allowing markets to correct. But Congress should be spending much less and the Fed should be more aggressive in tightening the money supply and raising its interest rate target. The famous Taylor rule suggests a rate of at least 6%, which is substantially higher than the current range between 2.5% to 2.75%. Ultimately, what’s needed now are pro-growth policies of spending, taxing, regulating, and printing cuts instead of what’s coming out of Washington. President Biden and Democrats in Congress aren’t helping the situation with the “Inflation Reduction Act,” as it will lead to more debt and more inflation that will further deplete savings, thereby making a bad situation worse for Americans. Things must change. Published at TPPF with Daniel Sanchez-Pinol  “We’ve had two quarters: 1.5% decline in GDP, that’s actually done the first quarter, and this quarter now is estimated by the Atlanta Fed as being very, very close to zero,” economist Art Laffer told Fox Business. “If it comes in negative, that will be the two quarters in a row—that would be the definition of recession.”

With the economy stagnating and inflation soaring, stagflation is here for the first time since the Great Inflation of the 1970s because of bad policies out of Washington. A recession is inevitable as the government-inflated “boom” busts—and we could already be in one. But pro-growth policies would help ease the pain. The pandemic prompted irresponsible and record-breaking deficit spending by Congress, pumping in massive “stimulus” funds that raised the national debt by $6 trillion to $30 trillion, or about $90,000 owed by every American. And President Biden has also been on a regulatory spree. His administration has finalized 360 rules through June 17 with a cost of about $215 billion, according to the American Action Forum. Compared to the same time since its inauguration, the Trump administration completed 367 rules at an economic cost of $1.2 billion. Those bad policies by Congress and the Biden administration have been a major reason why the economy is stagnating, with negative growth in the first quarter of 2022 and likely little to no growth in the second quarter. And the Fed purchasing that debt and printing too much money to chase too few goods resulted in a 40-year high in inflation. This stagflation affects employers and workers. Firms now can hold less inventory for the same amount they paid previously, which reduces their profitability and causes them to increase prices, cut costs, or reduce output to keep up with inflation. And consumers have less purchasing power. Workers and employers must then reduce their spending and investment, respectively. With workers producing less, productivity declined by at the fastest rate since 1947, contributing to why inflation-adjusted average hourly earnings are down substantially over the last year. Another issue is that safety-net programs were increased without work requirements during and since the pandemic. Those programs included expanding Medicaid, increasing child tax credits, and enhancing unemployment insurance payments. This has created even more dependency on government. And these expansions of government contributed to soaring deficit-spending with a 25% increase in the national debt in just the last two years. These handouts also encouraged people not to work because they would lose more in payments than they would receive from working. There are now 5.5 million more unfilled jobs than unemployed workers. In order to reduce the pain of the inevitable recession, Congress ought to adopt pro-growth policies, similar to those between 2017-2019. These policies included a concerted effort to reduce onerous regulations and to pass the Tax Cuts and Jobs Act. They contributed to the U.S. records of the lowest poverty rate (across most demographics) and the highest inflation-adjusted median household income. But excessive spending was an important factor that was missed then because Congress spent too much. If Congress just reined in spending to no more than population growth plus inflation, as outlined in the Foundation’s Responsible American Budget (RAB), the $20 trillion increase in the national debt over the last 20 years would instead have been a nearly $3 trillion surplus. This would have meant more money in Americans’ pocket and more economic growth from lower interest rates and less debt for the Fed to purchase to create inflation. Which is why the Fed also needs a monetary rule, which would call for it to have a much smaller balance sheet to reduce the quantity of money and a much higher federal funds rate target. Historically, the federal funds rate target must be as high or higher than the rate of inflation. With the latest inflation rate being 8.6% and the federal funds rate target being in a range of only 1.5%-1.75%, the rate target should be much higher. While this would likely result in a quick and deep recession, this is necessary given the government-inflated boom that must now bust. Bad policies have driven this government failure that’s making the situation worse before it gets better. For the sake of Americans, let’s end them now, because more government isn’t the solution. https://www.texaspolicy.com/economic-stagflation-is-here-is-a-recession-next/  Americans have less money than they had last year—though taxes haven’t been raised. So what’s the problem? Inflation, which has increased at a 40-year high annual pace of 7.9%. It acts as a hidden tax because we don’t see it listed on our tax bills, but we sure see less money on our bank accounts.

In fact, inflation-adjusted average hourly earnings for private employees are down 2.8% over the last year. This means a person with $31.58 in earnings per hour is buying 2.8% less of a grocery basket purchased just last February. “For a typical family, the inflation tax means a loss in real income of more than $1,900 per year,” stated Joel Griffin, a research fellow at The Heritage Foundation. The hidden tax of rapid inflation has been avoided for four decades. But that’s understandable because we haven’t seen these sorts of reckless policies out of Washington since the Carter administration. The policies from the Biden administration’s excessive government spending and the Federal Reserve’s money printing must correct course now before things get worse. What’s causing inflation is being debated. One claim is “Putin’s price hikes” stem from the Russian president’s invasion of Ukraine. While this has contributed to oil and gasoline prices spiking recently, these prices—and general inflation—were already rising rapidly. This was because of the Biden administration’s disastrous war on fossil fuels through increased financial and drilling regulations, cancelation of the Keystone XL pipeline, and more. Specifically, the price of West Texas Intermediate crude oil is up about 110% since Biden took office, yet only up 21% since Russia invaded Ukraine. And to think, the U.S. was energy independent in the sense that it was a net exporter of petroleum products in 2019. Another claim is the supply-chain crisis. For example, the global chip shortage has contributed to a large shortage and subsequent increase in the average price of new vehicles—to a record high of $47,000, up 12% over the last year. This contributed to buyers switching to used cars, which has pushed the average price up to nearly $28,000, about 40% higher. These two claims will likely be transitory price increases, though not sufficient to drive down overall inflation to what we’ve experienced for the last year-plus. Inflation is persistent because of rampant government spending and money printing. Larry Kudlow, who served as the director of the National Economic Council for President Trump, stated that inflation “is destroying working folks’ pocketbooks and devaluing the wages they earn, and the root cause of the inflation is way too much government spending, too many social programs without workfare, and vastly too much money creation by the Federal Reserve.” Both political parties share the blame for too much government spending, which has caused the national debt to balloon to $30 trillion. Just over the last two years, the debt has increased by 25% or $6 trillion. While some of that may have been necessary during the (inappropriate) shutdowns in response to the COVID-19 pandemic, much of the nearly $7 trillion passed in spending bills was not, especially the trillions by the Biden administration far after the pandemic had slowed and people were returning to work. Laughably, Speaker of the House Nancy Pelosi recently argued that government spending is helping inflation and President Biden argued that he’s cutting the deficit. Both are false. Government spending doesn’t change inflation because it just redistributes money around in the economy. And the deficit would only be rising from Biden’s big-government policies but he’s taking advantage of an optical illusion: one-time COVID-19 relief funding drying up and tax revenues rising partially from the effects of inflation. Ultimately, the driver of inflation is from discretionary monetary policy by the Federal Reserve as it monetizes much of the $6 trillion in added national debt since early 2020. The Fed did this to keep its federal funds rate target from rising above the range of zero to 0.25% by more than doubling its balance sheet to $9 trillion. More money is fueling the ugly government spending and bubbly asset markets that’s resulting in dire economic consequences. Instead, we need to learn what Presidents Harding and Coolidge realized a century ago. This would mean a return to sound fiscal policy, monetary policy, and the dollar that built on the principles of America’s founding. We need binding fiscal and monetary rules to hold politicians and government officials in check of we hope to tame inflation and return to prosperity. https://www.texaspolicy.com/the-tax-increase-thats-hidden-in-plain-sight/ Overview: The COVID-19 pandemic and forced business closures by state and local governments over the last year left much economic destruction. Many Americans have been recovering as we near herd immunity and states reopen, but fiscal and monetary policies out of D.C. are distorting economic activity and the labor market. For example, the labor market has been improving at a slower pace in recent months, even as there has been at least $6 trillion in passed or proposed bills during the first 100 days of the Biden administration. The federal unemployment “bonuses” and even more in handouts have reduced incentives to work, resulting in a similar number of unemployed as the record high of 9.2 million job openings. Although the economy has withstood these headwinds for now, a pro-growth approach is necessary. Price inflation in May 2021 was up 5% over May of 2020. At this pace, the general level of prices will double in less than 15 years. The last time inflation was running this high was in 2008, when gasoline first breached $4 a gallon. And inflation expectations for the next year have reached a record high.

But what did we expect when the government created trillions of dollars and forced people to stay home from work? The Federal Reserve’s balance sheet has exploded by 100% to more than $8 trillion since last year; it was the perfect recipe for inflation with more money supplied than goods and services available to buy. There have been red flags for months, with businesses announcing that they are raising prices. Proctor & Gamble manufactures hundreds of products across dozens of brands from diapers to detergents. General Mills makes various foodstuffs from cereals to soups and pastries to pizzas. Hormel also sells various food products. Whirlpool manufactures appliances. Texas’s own Kimberly-Clark makes tissues and paper towels, among other products. Tempur Sealy sells bedding. Americans use or consume products from these businesses every day, and those companies are all raising their prices, which hurts consumers’ purchasing power. Grocery stores and restaurants across the country have been raising prices as well. But why these sudden price increases? Businesses are facing higher costs. Commodity prices are climbing quickly, as are wages due to labor shortages. The contention that current inflation numbers are skewed because of “base-effects” from the early months of the pandemic is incomplete. The consumer price index (CPI) in May 2020 (the lowest point of pandemic-era prices) was just 1% below the CPI’s then-record high in February 2020, which has been eclipsed since August 2020. So, the base-effects argument does not explain a 5% annual increase. Inflation is a tax, pure and simple, but not an explicit tax. Instead, it robs you of your purchasing power subtly and silently so that most people are none the wiser. It is not accomplished expressly through legislation, but through the sophisticated maneuvers of the Fed, giving inflation an air of mystery. In reality, there is nothing mysterious about inflation. When the Fed creates money faster than the economy grows, then prices will tend to rise. That is why there is also no end in sight to this inflationary wave. The Fed continues to target historically low interest rates by creating money every month at an annual pace of more than $1.4 trillion, far faster than the economy is growing. The result is real wealth being taken from you—taxation without representation. Nevertheless, it is surprisingly easy to stop inflation. Ending inflation only requires the Fed to cease flooding the economy with money. If the Fed slows its money creation, though, then Congress cannot use inflation to finance the nation’s deficits, which seems to be Congress’s favorite way to spend. Conversely, if Congress were to achieve a balanced budget through sound fiscal policy, then the Fed could return to its original mission of price stability, and not worry about backstopping massive federal deficits with newly created money. This could be more quickly be achieved by implementing the Texas Public Policy Foundation’s Responsible American Budget, which sets a total budget limit at no more than the average taxpayer’s ability to pay for it as measured by population growth plus inflation. While this would not completely solve the problem of inflation, a journey of a thousand miles begins with a single step, and this will point the country in the right direction. We must not let the best be the enemy of the good; something must be done sooner rather than later to stop the current runaway spending in Congress. For example: Senators in Congress have recently reached a tentative bipartisan “infrastructure” deal to spend another $579 billion without raising taxes—or more accurately, without explicitly raising taxes. The spending will be financed with bonds purchased by the Fed, which means through the implicit tax of inflation. That $579 billion will still be collected, but not through so obvious a mechanism as the IRS. No, inflation is too subtle, silent, and sophisticated for that. Full article |

Vance Ginn, Ph.D.

|

RSS Feed

RSS Feed

Proudly powered by Weebly