Originally published at Econlib.

Amid a heated election year, the teachings of economist Friedrich Hayek provide a guiding beacon, urging us to transcend partisan lines and champion free-market capitalism that benefits everyone. I recently interviewed Dr. Bruce Caldwell of Duke University about his book, Hayek: A Life, 1899-1950, who helped shed light on Hayek’s views on pressing issues today. As we navigate the complex landscape of governance, we should heed Hayek’s call for market-based approaches, especially with trade and immigration, where the clash of political ideologies often obscures the path to rational decision-making. Hayek’s teachings underscore the need for policy approaches prioritizing broader economic health rather than conforming to the whims of political affiliations or interest groups. He did not advocate for simplistic labels like “left and right” but viewed political thought as a triangle, with socialism, conservatism, and liberalism representing the three points. He favored liberalism, in the classical sense. His writings compel us to consider whether policies align with our principles and values. One example is trade protectionism, with tariffs enacted while president and pushed again by Donald Trump. Hayek’s book, The Road to Serfdom, cautioned against the pitfalls of protectionism and advocated for free-market principles that embrace competition in free trade. While protectionist measures like tariffs may appeal to certain political bases, they come at the expense of economic efficiency and growth. They ultimately cost us more for purchases and inhibit our choices as competition is artificially manipulated where it would otherwise organically select the best providers of resources. A Hayekian approach to trade involves understanding that dynamic economies thrive on diversity and exchanging goods and services across borders. Another issue at the forefront of political debates that Hayek’s approach helps shed light on is immigration. He recognized that allowing the free movement of individuals fosters economic dynamism and innovation. Policies that restrict immigration solely for political gain risk stifling economic growth and impeding the exchange of ideas that fuels progress. A Hayekian perspective on immigration advocates for policies that acknowledge the economic benefits of a diverse and dynamic workforce. Instead of succumbing to populist narratives that frame immigration as a threat, Hayek prompts us to view it as an opportunity. An influx of skilled and motivated individuals can contribute to a vibrant economy, filling gaps in the labor market and injecting fresh perspectives that drive entrepreneurship. Too often, misinformation about immigration has led even conservatives to favor more government involvement in tightening borders and deportation. However, as Hayek outlined in his development of “the knowledge problem,” expecting a government of people with limited knowledge of the issue and tradeoffs from policy choices too often results in worse outcomes. The people in government do not and never will have all the answers. Instead, collecting everyone’s ideas in the market leads to having the most available knowledge and, therefore, better outcomes. In short, government failures are worse than any perceived market failures. Taking a cue from Hayek, we should strive for more free trade agreements, especially with our allies, which means an end to all tariffs and other barriers. We should also enact market-based immigration policies that balance national security concerns with the economic advantages of attracting talent from diverse backgrounds. As we prepare to select our nation’s president for the next four years, Hayek’s teachings serve as a guidepost, urging us to prioritize people’s well-being over the allure of party-centric agendas. Embracing a Hayekian perspective requires a willingness to critically evaluate policies based on their economic merit rather than their alignment with partisan ideologies. Only by doing so can we navigate the complex economic landscape and ensure a prosperous and dynamic future for all.

0 Comments

Originally published at AIER.

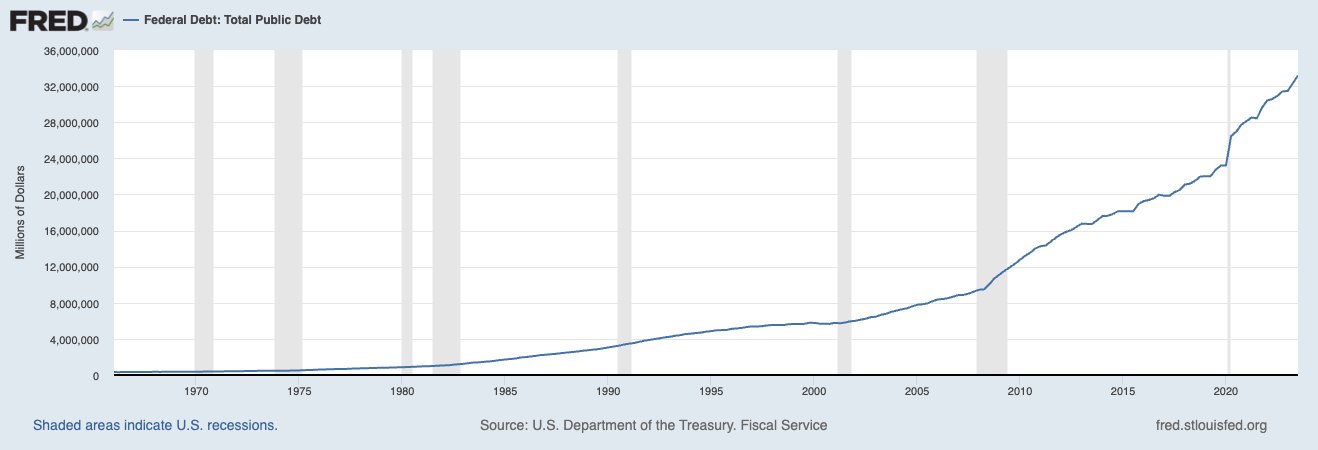

Congress hasn’t done its primary job of passing a balanced budget or even a full-year budget in decades. This must change soon before the fiscal crisis gets worse. But that’s unlikely because few seem to care. Congress recently passed the third continuing resolution for fiscal year 2024 in the amount of $1.7 trillion. This budget legerdemain kicks the federal budget to March, when members will repeat the same omnibus process, one fraught with hijinks and grandstanding. Instead of an actual debate about what we should or should not spend on a department and agency basis, we get calls to “shut down the government” if any number of demands aren’t met. Now, there’s a “bipartisan tax deal” that could add more than $600 billion to the debt over a decade. Democrats don’t seem to care about the debt much, and some who adhere to the ideology of modern monetary theory even think it is helpful for economic growth. But the Republicans also seem to have little, if any, courage to restrain spending, so they just keep cutting taxes and spending us into greater levels of debt. The late, great economist Milton Friedman said, “I am in favor of reducing taxes under any circumstances, for any excuse, with any reason whatsoever because that’s the only way you’re ever going to get effective control over government spending.” But spending is the ultimate burden of government on taxpayers and must be addressed first. The Republican agenda has prioritized border security, rightly or wrongly, over everything else to deal with a humanitarian crisis along the border with Mexico. Former president and top GOP presidential contender Donald Trump has insisted on prioritizing this issue. Events at the border continue to boil with the fight between Texas Governor Greg Abbott and President Biden after a recent Supreme Court decision. The decision has limited reach as it “temporarily allows the Border Patrol agents to continue cutting and moving the razor wire installed by Texas. However, since the ruling came through the emergency docket, the case is now passed back down to the lower court, who will hear the case with oral arguments.” The Republican pursuit of an aggressive border security deal as the number one priority risks further inflating bloated spending as the issue gets subordinated. While some argue that illegal immigration costs far more than border security, compelling studies indicate that immigrants, when provided opportunities, make substantial contributions to society, enriching the economy. The more aggressive approach to border security during Trump’s term contributed to extravagant federal deficit spending. There has also been a high cost to Texans in the state’s budget to address border security issues of more than $5 billion in the current budget and at least $5 billion more since 2016. Addressing illegal immigration issues and averting an impending fiscal crisis requires substantial debate about these issues rather than the current partisan-fueled fire drill over continuing resolution funding. With budget deficits expected to be at least $2 trillion per year over the next decade and net interest payments recently surpassing $1 trillion, every scarce taxpayer dollar must be used wisely, if at all. This could be done with market-based reforms that would foster better fiscal, economic, and border situations. Economist Richard Vedder and others proposed an immigration approach that would create an international market for visas whereby the government issues some of them for refugees, and the rest are auctioned off to people willing and able to purchase them. The government could use this money to pay down deficits, and there would be better accountability for those with visas while providing necessary resources along the border. The biggest national threat continues to be Congress’ profligate spending, which the primary drivers are so-called “entitlements” and must be swiftly reformed with market-based approaches. But right behind it is the Federal Reserve’s bloated balance sheet, which must be addressed. Despite a 14 percent reduction since its peak of about $9 trillion in May 2022, the Fed’s balance sheet remains a staggering 85 percent higher than pre-pandemic levels. Lingering issues of the Fed running losses of $116.4 billion last year, propping up struggling financial institutions with its costly bank term funding program, and the ongoing cost of trying to artificially hold down market interest rates as federal budget deficits soar exacerbate a fiscal-monetary crisis. Manifestations of the underlying economic malaise are evident in falling real wages down 1.3 percent since Biden took office, inflation surpassing set targets, unattainable housing affordability, and families grappling with saving money. These symptoms, rather than isolated issues, indicate the pervasive consequences of unchecked government spending and money printing, casting a long shadow on Americans’ well-being. The latest efforts by Congress to pass the continuing resolution and propose the latest tax deal will make the fiscal situation worse. While the latest idea of a fiscal commission could do what is good in theory, there are already calls to raise taxes, which will be detrimental to the economy and the fiscal picture. The path forward must be fiscal sustainability. This includes a long-term solution of a spending limit. The limit should cover the entire budget and hold any growth to a maximum rate of population growth plus inflation. This growth limit represents the average taxpayer’s ability to pay for spending. Doing so would have resulted in just a $700 billion increase in the debt instead of the actual increase of $20 trillion from 2004 to 2023. The spending limit should be combined with a monetary rule that removes much of the discretion of central bankers. This will support sound money. It can be achieved by moving to a single price stability mandate and preferably a high-powered money growth rate rule of the Fed’s assets. Other rules include the Taylor rule or nominal GDP targeting. While each of these rules has pros and cons, the money growth rate rule advocated for by Milton Friedman is the simplest. It’s simply a rule based on how fast currency plus bank reserves grow. This would be the easiest for the public to understand, to hold officials accountable, and to tie the Fed’s balance sheet directly to inflation. John Taylor proposed what’s been coined the Taylor rule that estimates what the federal funds rate, which is the lending rate between banks, should be based on the natural rate of interest, economic output from its potential, and inflation from target inflation. Scott Sumner most recently popularized nominal GDP targeting, which uses the equation of exchange (MV=Py) to allow the money supply times the velocity of money to equal nominal GDP. There are different variations of it, but the key is that velocity changes over time, so the money supply should change based on money demand to achieve a nominal GDP level or growth rate over time. Rules over discretion, at least until we can rightfully end the Fed, should hold those in Congress and at the Fed in check because their limited knowledge will always result in bad outcomes for people in the marketplace. Such measures are pivotal in preventing further debt accumulation, safeguarding America’s credibility, and preserving the economy’s stability. The choices made today will reverberate into the future, shaping the economic landscape for future generations. This call to action is for policymakers to tread carefully, adopt prudent fiscal and monetary sustainability through a rules-based approach, and prioritize the long-term well-being of the country with market-based reforms over short-term politics. Failure on these issues will prevent us from addressing the humanitarian crisis along the border, China, or other concerns. These efforts will be challenging, but they’re essential for freedom and prosperity.  Originally published at Inside Sources.

The final jobs report for 2023 was recently reported. The headlines look good but don’t tell the full story. This has been a common theme with many economic indicators, from the labor market to economic output. With this being an election year, politicians are trying to milk every apparent “win” or “loss” for voter approval. With all the noise, we need an honest assessment of the economic ups and downs to help guide voters in November. First, the payroll survey shows that were 216,000 net non-farm jobs added in December, which historically is rather robust. However, that’s not even half the story. To examine how many productive private-sector jobs were added in December, we need to make some corrections. This includes subtracting 52,000 unproductive government jobs added in December as they are a burden on private-sector workers. Also, we need to subtract the 71,000 jobs that were revised down for October and November. Doing so leaves just 95,000 productive non-farm jobs added in December, which is historically weak. Couple these findings with even weaker results from the household survey showing 683,000 fewer people were employed compared with November 2023, and this report is even weaker. While the unemployment rate was unchanged from the previous report at 3.7 percent, the labor force dropped by nearly 700,000 last month, meaning fewer people had work or were looking for work. The labor force participation rate dropped to 62.5 percent, the lowest since February 2023. Contributing factors to the declining labor force participation are myriad and complex, not always correlated to the economy. But they are typically connected with expanded roles of government and other factors. For example, the Economic Policy Innovation Center recently released a report highlighting how millions of people have dropped out of the labor force. The author notes “if the employment-to-population ratio were the same today as it was before the COVID-19 pandemic in February 2020, 2.6 million more people would be employed today.” The report finds that the largest share of people leaving have been retirees since the pandemic. The next largest group is 20 to 24 years old, who have been living off the handouts since the pandemic or with their parents. Interestingly, even with skyrocketing daycare costs, those without kids are a large share of those leaving the workforce. This makes some sense as maybe they are young and don’t have kids and have other means to survive, but this also is a conundrum because they’re reducing their long-term earnings potential. But with recent minimum wage hikes by 22 states that no doubt will displace many low-skilled workers and the rise in dependency on government safety nets over the last few years, there’s likely to be more people out of the labor force for longer. Speaking of distortion, average weekly earnings have been improving, but after adjusting for inflation, they are up just 0.4 percent over the last year. While it’s promising to see real wages go up after years when it wasn’t, workers would feel much more relief if inflation were further slowed. But mischief in Congress and the Federal Reserve keeps that from happening. Inflation soared due to the federal government’s deficit spending, mostly monetized by the Federal Reserve. This created a situation of too much money chasing too few goods that resulted in persistent inflation. As purchasing power remains a problem for many Americans, workers become disenchanted with jobs, especially when the monetary benefit of government handouts exceeds wages. Reducing government spending is imperative. Doing so will help the Fed tame inflation, reignite labor force participation, and spur job creation. Celebrating wins is important, especially during the recovery after the Donald Trump lockdowns, but our leaders must not turn a blind eye to underlying problems. As we await jobs reports, we must consider the underlying issues that affect Americans directly rather than just the headlines. What we uncover might shape whether our elected leader champions free-market flourishing or leans toward the big-government ideologies our forefathers warned against.  Originally published at Daily Caller.

A new study from the International Monetary Fund (IMF) has ruffled assumptions, asserting that “40% of global employment is exposed to AI.” The study also predicts that high-skilled jobs will bear the brunt of this transformation, disproportionately influencing roles that traditionally require higher education and professional experience. Among advanced economies, the IMF estimates that the share of jobs affected by AI could be 60 percent. Half of them could benefit from increased productivity, and the other half hurt by replacement. The IMF concludes that the impending shift should compel countries, particularly those well-prepared for AI integration like the U.S., to implement “robust regulatory frameworks.” They argue this would help cultivate a safe and responsible AI environment with safety nets to help those whose jobs are AI “vulnerable.” But we don’t have to look too far back to realize how attempting to harness AI innovation and its results would be disastrous for people and prosperity. The rise of AI presents a unique chance for society to better adapt to challenges and capitalize on new opportunities. Humanity has always adapted to new technological possibilities, turning most disruptions into positive outcomes. For instance, dedicated professionals called “calculators” once performed complex calculations. With the emergence of pocket-sized calculators in 1971, the computing revolution began, showcasing the transformative potential of technological innovation. Those human calculators, who would today be considered high-skilled, highly vulnerable individuals, went behind the machines and created and perfected better computational technologies. Whether or not they felt threatened by the technology, they adapted nevertheless and made their skills indispensable to the technology. As the electronic calculator removed much busy work, their minds were more available to focus on tasks machines couldn’t perform. The emergence of health-related diagnostic tools like X-rays and MRIs did not render doctors less valuable but widened the breadth of their jobs. Tractors did not displace farmers but made aspects of the role significantly more accessible, allowing for higher output. The examples of technology helping humans by making their jobs easier are endless. High-skilled professionals facing AI exposure should view this revolution as an opportunity to learn and grow. Rather than advocating for regulatory barriers, individuals can proactively enhance their skills, pursue further education, earn certificates, or even explore career transitions. The power of spontaneous order in free markets lies in allowing people to innovate when not restricted by government overreach. The IMF study’s conclusion urging countries to hurriedly embrace AI regulation overlooks the resilience and adaptability inherent in free societies. Attempting to pause AI innovation is impractical in the face of rapid advancements by other nations. Our big tech competitors like China and the UAE will not inhibit progress with red tape, so why would we? We’ve already seen demonstrative instances. Recall that in June 2023, Meta launched what was, at the time, the largest open-source language model ever, Llama 2. For almost two months after that, America was the global AI leader due to this technology, only to be eclipsed by the UAE government with their release of Falcon 180b, which has more than double the parameters of Llama 2. In a matter of weeks, America lost its top spot in AI innovation. Imagine what would happen if we introduced more regulatory barriers, as suggested by the IMF, or required a pause in AI advancement, as suggested by Elon Musk and others last year. It’s not just the U.S. reputation as a world leader at stake but our very security, as we could quickly be overtaken by nations who embrace the power of AI in technology, cybersecurity, and beyond. To maintain leadership in the AI landscape, the U.S. must welcome disruptive changes and cultivate an environment encouraging competitiveness. The future belongs to those who can adapt and innovate, and AI, as a tool created by humans, should be embraced rather than feared.  Originally published at American Institute for Economic Research.

The Economist recently compared Joe Biden’s and Donald Trump’s economic records, concluding Biden wins so far. While the article raises valid points, it excludes key details that make the findings questionable. Ten months from now, there’s a high likelihood Biden and Trump could go head-to-head again for the presidency, especially after the results from the Iowa caucus. But voters should be informed about the effects of their policies on key issues like immigration, inflation, and wages. Starting with a divisive bang, let’s look at each leader’s track record concerning immigration. The Economist correctly noted that apprehensions along the southern border were much lower under Trump. They increased by the most in 12 years during the economic expansion of 2019, decreased early in the COVID-19 pandemic when people could be turned away for public health concerns, and rose again during the lockdowns. While some may see apprehensions rising between Trump and Biden as a loss for Biden, I see it as a loss for both. This metric is somewhat unreliable, given one person can be caught and counted multiple times, and those caught are a subset of total migrants. The truth is immigration is good for the economy, but government failures create unnecessarily complex barriers against legal immigration, contributing to the humanitarian crisis along the Mexico border today. Neither President has pushed for what’s needed (market-based immigration reforms) both lose. Inflation is another hot topic, especially for Biden. The Economist hands the win to Trump, as inflation was far lower during his presidency. But can we give him the credit? Remember, Trump pressured the Federal Reserve to reduce its interest rate target and expand its balance sheet, which was inflationary. His deficit spending skyrocketed during the lockdowns and was mostly monetized by the Federal Reserve, contributing to what was always going to be persistent inflation. Biden made this deficit spending and resulting inflation much worse. Add in the Fed’s many questionable decisions, such as doubling its assets, cutting and maintaining a zero interest rate target for too long, and focusing too much on woke nonsense, and we can see how this was always going to be persistent inflation. But even the Fed’s latest projections indicate it won’t hit its average inflation target of two percent until at least 2026. Likely, it will cut the current federal funds rate target range of 5.25 percent to 5.5 percent three times this year, keep a bloated balance sheet to finance massive budget deficits, and run record losses. If so, this inflation projection is too rosy. Some of Trump’s policies helped stabilize prices, including his tax and regulation reductions. But he still allowed egregious spending. Biden has doubled down on red ink that has contributed to the recent 40-year-high inflation rate. While inflation has been moderating recently under Biden, Trump gets the win. Of course, neither Presidents nor Congress control inflation, as that job is the Fed’s, but its fiscal policies influence it. When it comes to inflation-adjusted wages, The Economist grants a tie. Let’s consider real average weekly earnings that include hourly earnings and hours worked per week, adjusted for the chained consumer price index, which adjusts for the substitution bias and has been used for indexing federal tax brackets since the Tax Cuts and Jobs Act of 2017. Trump’s era witnessed a robust upward trajectory of real earnings, with considerable gains by lower-income earners, thereby reducing income inequality. We must acknowledge a real wage spike in 2020 during Trump’s lockdowns, marked by the loss of 22 million jobs and various challenges. To maintain a fair analysis, I disregard this spike. A year later, real wages demonstrated a decline under Biden. Extending the timeframe to two years later, real wages remain relatively flat to slightly increased. To provide a contextual understanding, when we consider the trend under Trump, excluding the 2020 spike, real wages for all private workers or production and nonsupervisory workers fall below those observed during Biden. It’s worth noting, however, that these wages have been higher since 2019, albeit nearly stagnant for all private workers. Given real earnings, I agree with The Economist that Trump and Biden are tied. While much more can be said for each President’s policies, continuing to add context when making assessments is crucial. I give Trump a nuanced “win” overall because his policies supported more flourishing during his first three years until the terrible mistake of the COVID lockdowns, with its huge, long-term costs. I should note that I made a strong case inside the White House for no shutdowns and less government spending but, alas, my efforts, and those by others, lost to Fauci, Birx, and Trump. Given the improved purchasing power during his presidency, Trump receives better poll ratings than Biden after three years of their presidencies. But this win doesn’t mean that Trump’s record is best regarding these issues, protectionism, and more. Let’s hope free-market capitalism, the best path to let people prosper, is on display this November, no matter who is on the ballot.  On January 1st, 22 states and 38 cities and counties raised their minimum wages, sparking some celebration for 10 million workers who get a pay hike, and many doubts for the rest.

While this is perhaps a well-intentioned policy, intentions don’t indicate a policy’s effectiveness. Many economists argue that this decision will disadvantage the people it aims to help, namely, lower-skilled workers. Minimum wage hikes aim to make it “livable,” an increasingly frequent discussion due to government-created rampant inflation in recent years. I don’t disagree that $7.25 hourly, the federal minimum wage matched by many states, is insufficient for most to afford necessities. But helping lower-skilled workers move up the economic ladder is more complex than governments arbitrarily raising wages. Because I want to see everyone flourish, especially the neediest among us, I’m against a minimum wage and definitely against increasing it more. Elevating the minimum wage this drastically and suddenly will lead to widespread job losses, because employers must balance profitability with labor that costs more but adds no higher output. The spate of layoffs by major corporations in 2023, driven by slowing sales exacerbated by decreased purchasing power, demonstrates this reality. Now, envision a scenario where these higher-paid retained workers burden employers. Rather than a boon, this often translates into more layoffs or price hikes as companies seek to maintain profitability. The optimistic projection by the Economic Policy Institute, suggesting a $6.95 billion windfall for workers from the recent state minimum wage increases, rests on a questionable assumption that every worker will retain his job. In reality, employers may resort to cost-cutting measures to stay profitable, jeopardizing quality and output, and ultimately resulting in layoffs. If an employer must pay someone $16 hourly, the new minimum wage in New York and California, whom will they pay? Would it be a higher-skilled college graduate or a less-skilled worker with only a high school diploma? You can deduce which hire is the safer option. When the cost of obtaining more education or skills is higher than the cost of relying on government unemployment benefits, dependence becomes the more appealing choice over labor-force participation. Another often-overlooked negative impact of minimum wages is decreased negotiating power. When workers with qualifications and experience who merit higher pay are confined to a predetermined minimum wage, their bargaining potential is stifled. These labor market dynamics, however, extend beyond individual choices. The intriguing patterns in state migration rates underscore how higher minimum wages deter people from seeking better opportunities. Look at California and New York, champions of minimum wage increases. Both experienced some of the highest rates of outmigration in 2023. Conversely, with their comparatively lower minimum wages, Texas and Florida witnessed a substantial influx of new residents. People vote with their feet. The allure of better prospects, lower living costs, and increased job opportunities in states with few-or-no minimum wage hikes outweighs the appeal of higher minimum wages in other states. States with lower minimum wages continue to increase in appeal because, contrary to popular belief, only a very small share of hourly paid workers earn minimum wage, and not for long. Professor of Economics at UC San Diego Jeffrey Clemens’ findings reveal that most minimum-wage workers experience consistent wage growth over time. According to his research, over 12 months, about 70 percent of individuals studied initially employed at or near the minimum wage saw an improvement in their earnings, with an average wage increase of $1.39. The data suggest that the narrative surrounding the persistence of “career minimum wage workers” applies to very few people. But even so, those low-wage jobs maintain value. Low-wage positions, typically entry-level or part-time jobs, serve as the initial rung toward better opportunities with higher pay. Unfortunately, governments inadvertently eliminate many of these essential entry-level jobs by advocating for higher minimum wages. This lost first rung has profound consequences, especially for vulnerable groups like young individuals, part-time workers, the unmarried, and those without a high school diploma. Such individuals rely on these low-wage positions for income and to escape the cycle of government dependency and poverty. Employers and workers alike deserve freedom. Burdensome government regulations that hinder free-market flourishing culminate in the mandated minimum wage, which stifles opportunity rather than allowing spontaneous order to create jobs and economic growth. The states that just increased the minimum wage will experience more problems than they’ve already created. People will continue to vote with their feet. Hopefully, leaders at federal, state, and local levels will come to grips with the best paths to help people prosper, however unpopular those paths may be. These paths that improve productivity to demand higher market wages and increase output to supply higher-paid jobs are found in an institutional framework of free-market capitalism. Specifically for the labor market, politicians should provide universal school choice, remove government obstacles like occupational licensing and forced union dues, rein in spending to cut taxes, and reduce regulations. In short, more government isn’t the answer to higher wages because government is the problem. Let’s not double down on government failures. Originally published at AIER.  We must learn from history or be doomed to repeat it. This includes honestly assessing the economy in 2023 so that we have better information for making decisions in 2024.

Starting with a bang on many people’s minds is housing affordability. The year commenced with a surge in the average 30-year fixed mortgage rate from 6.5% in January to nearly 8% in October but has declined recently to about 6.6%. These higher mortgage rates and record-high housing prices contributed to an unaffordable housing market. While existing home sales were up 0.8% in November, they are down 7.3% over the last year, indicating a struggling housing market for families that will unlikely improve much in 2024. Another concern is costly inflation. Rampant hikes in the cost of a typical basket of goods and services have meant less purchasing power for us. This contributes to making housing, food, education, and other expenses for that basket less comfortable or worse for many families. As of November 2023, the core consumption personal expenditures increase was 3.2% year-over-year. This price measure of a basket of goods and services excludes food and energy and is what the Federal Reserve prefers to watch. While core PCE inflation has moderated from close to 6% in 2022, the recent 3.2% inflation rate remains 60% higher than the Fed’s average inflation target of 2%. Although moderating inflation represents some relief for many Americans, the challenge is that average weekly earnings adjusted for core inflation declined in 23 of the last 35 months since January 2021. In total, these real average weekly earnings are down 0.8% since then, indicating why inflation is a top concern. An additional problem is debt. Because earnings haven’t been keeping up with inflation, credit card debt soared to more than $1 trillion as people struggled to make ends meet, which is a bad sign for 2024. And many people have been going through their savings and retirement funds quickly. What about jobs? The White House recently celebrated “total job gains achieved under the Biden administration reached 14.1 million through November 2023.” But this metric becomes less impressive considering that 9.4 million of those jobs were just recovering jobs lost during the pandemic lockdowns. So, there have been 4.7 million new jobs added since January 2021, which is 134,000 per month. While this is positive, it is not record-breaking. The weaker labor market in recent months indicates that 2024 could be tough for many workers. Most people’s pocketbooks did not grow but diminished this year, and the job market similarly lags. But what about the nation’s overall growth? Hasn’t GDP soared? Not exactly. In the third quarter of 2023, the annualized real GDP growth hit 4.9%, which appears robust. But when you dig into the details, it’s more complicated. Government spending, which is a drag on the economy as it must take taxes from the private sector and distort market activities, threw in 0.99 percentage points. And private inventories, influenced by the whims of fluctuating interest rate expectations, chipped in 1.27 percentage points. When you exclude those contributions to consider stable real private GDP, there was just a 2.6% bump up. This slower pace didn’t just pop out of nowhere. It’s been a saga since early 2022, when we hit a two-quarter decline in real gross domestic product, waving a big red flag for a recession. And when you consider the valuable metric of real gross domestic output, which is the average or real gross domestic product and real gross domestic income, the economy has declined in three out of the last seven quarters. While these economic issues suggest stagflation triggered by misguided pandemic lockdowns and subsequent trillions of new money printing of deficit-spending, there may be some relief. The Fed’s slow correction to its bloated assets of $9 trillion at its peak to $7.7 trillion contributed to interest rates soaring since March 2022. But with Congress continuing to deficit spend of about $2 trillion per year and net interest payments soaring to $1 trillion per year, there are massive economic challenges ahead. These deficits will make it more difficult for the Fed to correctly normalize its assets quickly to get them back to at least the pre-pandemic $4 trillion. This is because the budget deficits would contribute to higher interest rates, so the Fed will likely monetize the debt more to help Congress avoid needed spending restraint. While these truths are tough to swallow, many beacons of hope also emerged throughout the year that should be noted. In 2023, a momentous shift unfolded with a transformative surge in educational choice. Twenty states expanded school choice, and a record-breaking 10 states passed some form of universal school choice, making 36% of American students eligible for a private choice program. Some states have been slow to increase educational freedom, but this revolution’s overall impact is historical. Recognizing that children are the cornerstone of our nation’s future and acknowledging that improved education is a pivotal predictor of their success, the catalyst for change is undeniably rooted in more universal school choice. The second bright light is the flat state tax revolution. Many states took bold steps to enhance their economic landscapes. Notably, prominent states like California and New York faced ongoing out-migration as individuals sought refuge from progressive policies, and less heralded states embraced free-market principles, propelling them onto the national stage. More conservative Florida and Texas continued to lead the way in places where people moved in 2023. The third thing to cheer is a responsible movement toward a sustainable state budget revolution. Some states are pushing toward improving their spending limits to one that covers more of the budget, limits budget growth to no more than population growth plus inflation, and has a supermajority vote to bust the limit or raise taxes. The synergy of these reforms demonstrates the power of federalism as states experiment with policies, revealing effective strategies and fostering a healthy laboratory of competition. We need lawmakers at the federal, state, and local governments to recognize what works and implement them. The trajectory in 2024 and beyond hinges on embracing free-market capitalism, which is the best path to let people prosper. This includes less government spending, less money printing, more school choice, and more tax relief. In short, less government. That’s how we get a more prosperous 2024. Happy New Year! Originally published at Econlib.  In 2023, Texas led the U.S. on many fronts: job growth, economic expansion, energy production, and a record surplus of $33 billion. This was when many other states, especially California, were reporting economic challenges and deficits.

Despite Comptroller Glenn Hegar's warning to spend wisely, the 88th Texas Legislature chose out-of-control, record spending. This isn’t a record Texans wanted because it means less available money for property tax relief. Texas can reverse course to lead the U.S. in fiscal responsibility by passing sustainable budgets that result in more surplus to return to taxpayers by reducing school property tax rates until they are zero. In 2023, the Texas Legislature passed the largest spending increase in state history. The fiscal 2024-25 budget increased appropriations by 21.3% to $321 billion, or, excluding federal funds, by 31.7% in state funds to a staggering $219 billion. Even more disturbing is that currently reported amounts may increase further as some legislation passed in the special sessions increases spending. Either way, the budget growth far eclipsed the rate of population growth plus inflation, which increased by 16% over the prior two years. This rate is a good comparison because it represents the average taxpayer’s ability to pay for government spending. This record spending, along with records of over $10 billion in new corporate welfare payments even to multi-billion-dollar companies and more than $13 billion in constitutional amendments that move money outside of the state’s spending limit, sets a challenging path forward. The bloated fiscal 2024-25 budget now looms as the new baseline for lawmakers, expanding government to the chagrin of many Texans. The excessive budget increase overshadowed Gov. Greg Abbott’s historic tax relief compromise signed into law during the Legislature’s second special session. While hailed as the largest property tax cut in Texas history, it fell short. The total for new school property tax relief was $12.7 billion. It falls short of the $14.2 billion appropriated for reducing school property taxes in fiscal 2008-09 due to a Supreme Court of Texas ruling that the school finance system was unconstitutional. But when the amount is adjusted for inflation since then, the $14.2 billion would be about $21 billion. Even when factoring in the state’s contribution of $5.3 billion to maintain reductions in school property taxes in prior sessions, the $18.3 billion in combined relief remains well below the $21 billion needed to be the largest in Texas history. It should be noted that the $14.2 billion for property tax relief for fiscal 2008-09 helped cut school property taxes by just $2 billion in 2007. But then school property taxes increased by $2.3 billion in 2008, surpassing 2006 before the relief by $300 million. Total property taxes decreased by just $450 million in 2007 and then increased by $3.8 billion in 2008. While those with property received some relief in their property tax bill in 2023, especially those with a homestead exemption, the amount will not be nearly as much as some lawmakers claimed. Worse still, these savings won’t likely last as local governments continue to push to pass bonds and increase spending and taxes. The Legislature should focus this interim on doing efficiency audits across the government, much like it started with safety net programs. Finding savings across the government with so much excessive spending recently will help maintain the property tax relief passed last year; spending excesses will not lead to calls for tax increases, and resulting surpluses can put school property taxes on a fast path to zero next session. There will also be an opportunity to put the new, stronger statutory spending limit in the constitution and have this limit cover spending by local governments. There should also be a requirement that at least 90% of resulting surpluses by the state go toward reducing school property tax rates and by local governments to reduce their own property tax rates. Doing so will achieve fiscal sustainability and put all property taxes on a path to elimination. In the meantime, Texans have opportunities in the March primary and November general election to consider many candidates' policy proposals. Do candidates on the ballot support eliminating property taxes, reducing government spending, and increasing prosperity? We need more politicians pushing for these things because they benefit Texas families and entrepreneurs. Let’s not have big-government socialism creep more into Texas but turn back toward free-market capitalism that has contributed to abundance. Originally published at The Center Square.  This was originally published at National Review.

Colorado governor Jared Polis (D) and Art Laffer, the economist and Presidential Medal of Freedom honoree, recently critiqued the state’s Taxpayer’s Bill of Rights (TABOR) at this venue. While not meritless, much of their argument is paradoxical, highlighting an overarching issue of fiscal unsustainability that warrants a reality check. TABOR recently had its 30th birthday. Voters approved the constitutional amendment in 1992, establishing the strongest tax and expenditure limit in the country. It’s been the gold standard for a sound spending limit ever since. Under the amendment, annual growth in spending cannot exceed the state’s population growth plus inflation, which is a good measure of the average taxpayer’s ability to pay for spending. When adopted, the limit covered about two-thirds of state spending. It requires voter approval for tax increases and mandates refunds to taxpayers if tax revenue exceeds the limit. In their critique, Polis and Laffer correctly acknowledge that TABOR surpluses indicate that income-tax rates are too high. They’re correct that the state should seek to reduce income-tax rates to prevent overcollection instead of handing out refunds. They’re also correct that a broader tax base is preferable. It enables the tax rates, and therefore the marginal effect of the tax burden, to be reduced as much as possible for all. But Polis and Laffer incorrectly criticize TABOR without realizing its pivotal role in achieving their purported goal to reduce taxes. Without a crucial spending check such as TABOR, the state would tie its budget directly to revenue levels, eliminating any surplus. While Polis has only recently touted reducing state income-tax rates with surpluses, the Independence Institute has long supported a plan called “Path to Zero.” The plan simply limits government spending and uses resulting surpluses to lower tax rates until they’re zero. This is similar to my efforts in Texas, Louisiana, and other states, which start with a sustainable budget approach, as recently explained in a release by Americans for Tax Reform. Unfortunately, courts and politicians have eroded the strength of TABOR over time, primarily because of politicians’ lack of fiscal restraint. The result has been that TABOR now covers less than half of state spending, allowing expenditures of all state funds, which excludes federal funds, to grow faster than population growth plus inflation. Specifically, appropriations of all state funds have increased by 74.2 percent, compared with an increase of just 46.5 percent in population growth plus inflation over the last decade. This has resulted in the state appropriating $4.2 billion more in just fiscal year 2023–24 than if it had been limited to the rates of population growth plus inflation over time, amounting to higher spending and taxes of about $3,300 per family of four. The summed difference each year in all state funds above this metric over the decade amounts to $16.3 billion, or $11,300 per family of four. These amounts don’t necessarily mean that the state needs to start cutting its budget to get back on track, but they do mean that the time to start reining in the budget is now, to reduce these excessive burdens on taxpayers. To that end, Ben Murrey, director of the Independence Institute’s fiscal-policy center, and I have shown the path forward with the Sustainable Colorado Budget (SCB). The SCB is a maximum threshold for the initial appropriations of all state funds and is based on TABOR’s rate of population growth plus inflation. This will help reinforce the original intent of TABOR, by broadening the spending limit to all state funds. The plan would limit nearly two-thirds of state spending each year, as when voters first adopted TABOR. Doing so will result in larger surpluses to reduce income-tax rates yearly until they’re zero. Polis and Laffer are right to want rate reductions, but there are none if there is no surplus. For the upcoming FY 2024–25, the SCB proposes an all-state funds ceiling of $27.70 billion. This uses the prior FY 2023–24 amount of $26.15 billion and increases it by 5.9 percent, calculated using TABOR’s current method and reflecting a 1.0 percent increase in the state’s population and 4.9 percent inflation. As noted above, it would be even better to grow the budget by less or not at all to correct past budgeting excesses. This more robust TABOR approach outlined in the SCB helps to freeze inflation-adjusted spending per capita, allowing the average taxpayer to afford the cost of government. In recent years, the current TABOR limit alone has already produced substantial surpluses that have been refunded to Coloradans. But instead of using this year’s $1.7 billion TABOR surplus to refund overcollected taxpayer dollars, the legislature could have cut the income-tax rate from a flat rate of 4.4 percent, which ranks 14th in the country, to 3.81 percent. Further, had the state over the past decade followed the SCB, which has a larger base budget, lawmakers could have lowered the income-tax rate to 2.96 percent, putting it on a faster path to becoming the lowest flat income-tax rate in the country, below North Carolina’s 2.49 percent. It would also pave the way to zero income taxes by 2042. Polis in his recent article criticizes TABOR for acting as a spending restraint rather than a mechanism to reduce tax rates. Indeed, his track record in the governor’s office demonstrates his distaste for limitations on spending. The state budget has grown 45 percent since he took office less than five years ago; his budget request for the upcoming fiscal year would constitute an astounding 52 percent increase. In a state with a constitutional balanced-budget requirement, it’s paradoxical to support tax cuts without spending restraints. Unfortunately, given his poor track record on spending and his critique of TABOR’s spending restraints — which he and Laffer improperly call a revenue limit — Polis is unlikely to adopt our sustainable budget to produce larger surpluses with which to cut tax rates. On the contrary, this year he supported a measure that would have increased state spending above the current limit, erroneously claiming that it would cut taxes using state surpluses. “A similar tax-rate reduction for property taxes, Proposition HH, failed on the ballot recently in Colorado,” Polis and Laffer write in their recent NRO article. While a clever misdirection, this argument doesn’t hold up. Prop HH didn’t directly offset the TABOR surplus through tax cuts, as an income-tax reduction would. That’s because the measure influenced only local property-tax revenue. Because the State of Colorado generates no tax revenue from property taxes, as those are collected only by local governments, reducing those rates won’t affect the TABOR surplus. Polis and Laffer contend that the state budget indirectly benefits from local property taxes. However, Prop HH would have lessened the state’s share of local funding by only approximately $125 million.  Originally published at Real Clear Policy.

During the fourth Republican presidential candidate debate the four participating candidates were asked to name a past president who would serve as an inspiration for their administration. In his response, Governor Ron DeSantis stated that he would take inspiration from President Calvin Coolidge. Coolidge, stated DeSantis, is “one of the few presidents that got almost everything right.” Further, DeSantis argued that “Silent Cal” understood the federal government’s role and “the country was in great shape” under his administration. To say that the federal budget process is broken is an understatement. The national debt continues to grow driven by out-of-control spending. The budget hawk within the Republican Party is an endangered species. Governor DeSantis is correct that the Republican Party needs to rediscover the principle of limited government. The best way to do this is to take inspiration from the Republican Party’s best known budget hawks and champions of limited government, Presidents Warren G. Harding, and Calvin Coolidge. President Harding assumed office in 1921 when the nation was suffering a severe economic depression. Hampering growth were high-income tax rates and a large national debt after World War I. Congress passed the Budget and Accounting Act of 1921 to reform the budget process, which also created the Bureau of the Budget (BOB) at the U.S. Treasury Department (later changed in 1970 to the Office of Management and Budget). President Harding’s chief economic policy was to rein in spending, reduce tax rates, and pay down debt. Harding, and later Coolidge, understood that any meaningful cuts in taxes and debt could not happen without reducing spending. Harding selected Charles G. Dawes to serve as the first BOB Director. Dawes shared the Harding and Coolidge view of “economy in government.” In fulfilling Harding’s goal of reducing expenditures, Dawes understood the difficulty in cutting government spending as he described the task as similar to “having a toothpick with which to tunnel Pike’s Peak.” To meet the objectives of spending relief, the Harding administration held a series of meetings under the Business Organization of the Government (BOG) to make its objectives known. “The present administration is committed to a period of economy in government…There is not a menace in the world today like that of growing public indebtedness and mounting public expenditures…We want to reverse things,” explained Harding. Not only was Harding successful in this first endeavor to reduce government expenditures, his efforts resulted in “over $1.5 billion less than actual expenditures for the year 1921.” Dawes stated: “One cannot successfully preach economy without practicing it. Of the appropriation of $225,000, we spent only $120,313.54 in the year’s work. We took our own medicine.” Overall, Harding achieved a significant reduction in spending. “Federal spending was cut from $6.3 billion in 1920 to $5 billion in 1921 and $3.2 billion in 1922,” noted Jim Powell, a senior fellow at CATO Institute. Harding viewed a balanced budget as not only good for the economy, but also as a moral virtue. Dawes’s successor was Herbert M. Lord, and just as with the Harding Administration, the BOG meetings were still held on a regular basis. President Coolidge and Director Lord met regularly to ensure their goal of cutting spending was achieved. Coolidge emphasized the need to continue reducing expenditures and tax rates. He regarded “a good budget as among the most noblest monuments of virtue.” Coolidge noted that a purpose of government was “securing greater efficiency in government by the application of the principles of the constructive economy, in order that there may be a reduction of the burden of taxation now borne by the American people. The object sought is not merely a cutting down of public expenditures. That is only the means. Tax reduction is the end.” “Government extravagance is not only contrary to the whole teaching of our Constitution but violates the fundamental conceptions and the very genius of American institutions,” stated Coolidge. When Coolidge assumed office after the death of Harding in August 1923, the federal budget was $3.14 billion and by 1928 when he left, the budget was $2.96 billion. Altogether, spending and taxes were cut in about half during the 1920s, leading to budget surpluses throughout the decade that helped cut the national debt. The decade had started in depression and by 1923, the national economy was booming with low unemployment. Both Harding and Coolidge were committed to reining in spending, reducing tax rates, and paying down the national debt. Both also used the veto as a weapon to ensure that increased spending and other poor public policies were stopped. The results of the Harding-Coolidge economic plan created one of the strongest periods of economic growth in American history. Unemployment remained low, the middle class was expanded, and the economy expanded. From 1920 to 1929 manufacturing output increased over 50 percent and the United States was a global leader in many key industries. In our current era marked by dangerous debt levels and high inflation whoever becomes the Republican presidential nominee should take inspiration from Harding and Coolidge.  Originally published at Econlib.

After a year dominated by historically high inflation and soaring home loan rates, 2023 is carving another negative as the annum of antitrust accusations. From lawsuits targeting Amazon and Google to the emergence of concerns over trading card and sandwich shop monopolies, the growing antitrust frenzy poses a threat to what these laws were originally crafted to safeguard: consumers. Actions of antitrust’s biggest modern advocates, like the Federal Trade Commission’s Chair Lina Kahn and U.S. Sen. Elizabeth Warren, reveal their misunderstanding of these competition laws. To maintain their protected freedoms to buy, sell, and trade, consumers and businesses must know the truth enshrined in these laws and not be duped by misrepresentation. Antitrust laws were enacted with a noble purpose—to protect consumers and promote fair competition. These laws were designed to ensure consumer access to various choices across the marketplace and prohibit businesses from engaging in anti-competitive practices. If those parameters seem vague, that’s because they are. That is, without antitrust’s crucial cornerstone, “the consumer welfare standard” established in the 1970s to help narrow the law’s scope. A principle that assesses whether consumers are better or worse off due to a company’s actions, the consumer welfare standard is mathematically defined as “the value consumers get from the product less the price they paid.” The addition of this language shifted antitrust’s emphasis from preserving competitors to competition. But perceived value varies between individuals. Concerns about monopolies can be legitimate when there is concern about diminished value from a product or service because of a company’s actions. Such monopolistic behavior may result in higher prices and lower quality. These tactics are most likely to prevail when outside competition is intentionally stifled by the government through regulations, spending, and corporate welfare. However, having a large or growing market share alone does not violate antitrust laws, as progressives like Warren would lead people to believe. In a healthy competitive market, companies naturally strive to develop and acquire other businesses to expand their offerings and meet consumer demands. Roark Capital’s acquisition of Subway, adding the sandwich chain to its portfolio, and major sports leagues signing contracts with trading card company Fanatics may seem like consolidation of power, but these changes do not inherently harm consumers or competition. In fact, if permitted to expand via purchasing and agreements with other companies or leagues, not just these but all businesses can improve consumer welfare and profitability. To the chagrin of its Italian competitor, the NFL, MLB, and NBA making agreements with the sports trading card company Fanatics was a voluntary decision executed because increased, not diminished, consumer welfare was perceived. While Panini SpA points the antitrust finger at Fanatics, it has three other fingers pointing back at itself, as the company has its own agreements with the NFL and NBA. Rather than viewing the new competition as an opportunity to improve its company and become the first choice, Panini SpA would rather waste time and resources trying to punish its competitor. This is what the FTC will try to do with Subway, the European Union wants to do with Amazon, and the DOJ has tried to do with Google. This knowledge is critical because consumers are being swayed to favor legal action that does not serve their best interest, more than likely because of widespread misinformation. For instance, a recent poll showed that 60% of Americans believe Google is too big and hurts businesses and consumers. However, conflicting data reveal that, overwhelmingly, Google users and employees derive immense value from its service. At the same time, other search engines continue to increase in popularity alongside Google, with Safari recently reaching more than one billion users. So, if the majority of Google users are happy with the service and other search engine options exist, the welfare of its consumers is far from threatened. But that hasn’t stopped the FTC from trying to take them down. So-called “big tech giants” and “trading card monopolies” aren’t the true titans threatening consumer welfare; it’s the rent-seeking politicians, government bureaucrats, and corporate rent-seekers wielding an insatiable appetite for control that are consumers’ actual adversaries.  Recent polling data from CNN reveals a grim reality: 84 percent of Americans are concerned about the national economy. Despite President Biden’s efforts to highlight seemingly positive metrics as indicators of the success of his progressive policies, a closer look at the data reveals why most Americans remain dissatisfied.

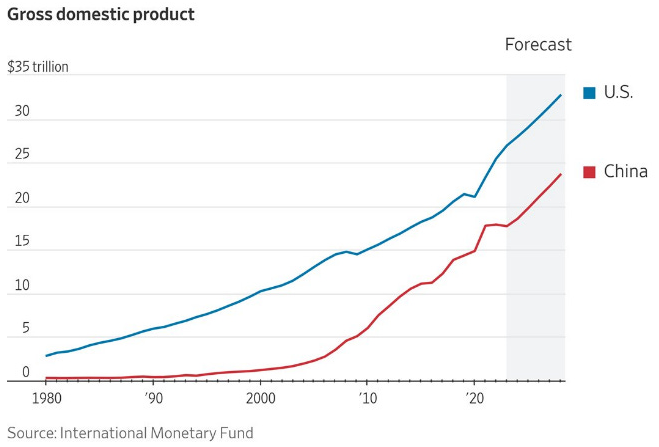

Biden’s claim of adding 14 million jobs since taking office would be impressive if it were true. The reality is that, since he took office in Jan. 2021, 13 million private sector jobs have been added. This appropriately excludes the unproductive addition of one million government jobs that will soon set a record under his watch. But the bigger point negating his rosy scenario is that the vast majority of this touted “job growth” stems from restoring job losses from the pandemic lockdowns. When we accurately tally the new jobs added since the shutdowns began in Feb. 2020, the count stands at 4.5 million private sector jobs added in three years. While this is a positive, it’s an average of 1.5 million jobs yearly, far from qualifying as record-breaking job creation. The latest U.S. jobs report for November provides additional data, reaffirming the mixed nature of the labor market. The payroll report indicates a feeble performance. There was a headline number of 199,000 jobs added. But there were revisions in October of 35,000 fewer jobs added. So, net additions stand at 164,000 jobs. When government jobs are correctly subtracted, the count is just 115,000 new productive private jobs last month. On a more positive note, the household report shows a substantial increase of 532,000 in the labor force, resulting in a 62.8 percent participation rate. Employment experienced robust growth of 747,000, contributing to a decline in the unemployment rate to 3.7 percent. But the broader unemployment rate that includes underemployed and discouraged workers is nearly twice as high at seven percent. However, it’s crucial to note that the average weekly earnings show a 3.7 percent increase over the last year, though this has been overshadowed by the elevated inflation. Fresh data on inflation as measured by the chained consumer price index (chained-CPI), which accounts for the substitution effect of changes in individual prices not accounted for by the headline CPI, reveals signs of moderation. The latest core chained-CPI inflation rate, which excludes food and energy and is watched by the Federal Reserves, for Nov. 2023 was up 3.7 percent year-over-year. Not only is this 85 percent higher than the Fed’s average inflation rate target of two percent, it also nearly matches the increase in earnings, negating any increase in purchasing power. In fact, real average weekly earnings have declined for 24 straight months. No wonder people are concerned about the economy. The ongoing reduction of the Fed’s balance sheet contributes to this inflation moderation, but further cuts to its bloated balance sheet are necessary to stabilize prices across the economy. Their balance sheet currently hovers around $8 trillion, nearly double its pre-pandemic figure, having increased tenfold in fifteen years from $800 billion in 2007. While some blame the national debt crisis on not having enough tax revenue from slower-than-optimal GDP growth, the truth is excessive government spending. Inflation is not your fault, as The Atlantic recently claimed. It’s the fault of excessive government spending by Congress that led to rising national debt which the Fed purchased and printed money. Too much money chasing too few goods is the classic definition of inflation, and it fits this time, too. A better way to solve this would be to slash government spending and taxes like President Calvin Coolidge did a century ago. During the Roaring 20s, the national debt declined, and the economy supported more opportunities for people to flourish. In light of the evidence, the question arises: Is Bidenomics working? The answer, drawn from the data, suggests it is not. To guide the economy back on course, recalibration is imperative. This includes prioritizing fiscal responsibility, pruning the Fed’s ballooning balance sheet, and reining in excessive government spending. Only through such pro-growth measures can we hope to unlock genuine economic recovery and chart a course toward lasting prosperity.  Originally published at American Institute for Economic Research. Rating agency Moody’s just downgraded China’s credit outlook from stable to negative after doing the same to the US about a month ago. Does this mean that China is on equal footing with us? Worse? Better off? An economic analysis suggests that China is not our biggest threat, nor are we theirs. In fact, the biggest problem we face is completely self-inflicted and found on our home soil. Apprehensions about China’s military actions and trade strategies maintain resonance, especially among middle-aged and older Americans. While caution is warranted, especially concerning their censorship and the treatment of Hong Kong and Taiwan, an economic comparison settles many doubts.  Regarding economic might, the US outshines China with a GDP of $27 trillion compared to China’s $18 trillion. The contrast is stark on a per-capita basis. Americans enjoy an average income of $79,000, six times more than their Chinese counterparts. One alarming similarity stands out though: Both nations have weathered credit downgrades mainly due to escalating budget deficits and national debts. The United States’ national debt is shaping up to be this decade’s hallmark. Now nearly $34 trillion, the deficit spiked in 2020, with trillions of dollars more added since. Net interest payments on the debt climbed by 39 percent and recently surpassed $1 trillion annually.  The repercussions of the national debt crisis are not merely theoretical – they are tangible, affecting the everyday lives of citizens.

In 2023, the dollar has significantly depreciated. Fitch (and now Moody’s) downgraded our creditworthiness. Home sales hit their slowest pace since 2010. Average 30-year fixed mortgage rates reached their highest point since 2000. And real median household income dipped to its lowest level since 2018, to name just a few of our recent economic woes. These findings shed new light on our competition with China. They should prompt America’s leaders to reevaluate our priorities and consider whether the enemy across the Pacific is as pressing as the ones we face at home. While some argue the government spending that drove the deficits was necessary, especially during the pandemic’s peak, it underscores the broader problem – a lack of fiscal discipline and a predisposition to rely on debt as a quick fix. It is high time the US adopted a spending-limit rule. Without one, we’ve only made things worse and failed to reach budget agreements. A reasonable spending limit of no more than the rate of population growth plus inflation has worked at the state level, and it would work at the federal level. While the US points the finger at China, we have three other fingers pointing back at us. Excessive government spending and a burgeoning national debt are eroding the foundation of our economic stability. Now is not the time to allocate excessive resources to confront external foes, but to address the fundamental issue plaguing us: a government that refuses to rein in spending of taxpayer money. America should also correct the errors in recent years of trade protectionism. There is reason to counter those countries who don’t play by the same rules, like China, but that should be done by joining free trade agreements with allies. This would be a more effective and affordable approach for Americans instead of raising taxes on them through tariffs, appreciating the dollar thereby increasing the trade deficit and contributing to trade wars that often lead to military wars. Let’s refocus our efforts, fortify our economic foundation, and confront the genuine threat within our borders. If not, governments will not be able to do their job of preserving liberty. This is of utmost importance.  This commentary was originally published at The Center Square here.

A record number of states have passed universal school choice so far this year, but it seems Texas won’t be among them. Given the lack of universal school choice in multiple bills this year, I’m relieved it hasn’t passed in Texas yet. I’ve long been a researcher and staunch supporter of universal school choice. The way to do this is by making the eligibility and funding for education savings accounts (ESAs) available for all 6.3 million school-age students. ESAs put the power of choosing kids’ schooling in parents’ hands by picking public, private, home, co-op, micro, or other types of schooling. ESAs would be funded through the current school finance system and other general funds or new tax credits as necessary. After the Texas Legislature failed to pass a school choice bill in the regular legislative session earlier this year, Texas Gov. Greg Abbott added school choice to the third and fourth special sessions. The first two special sessions focused on property tax relief and border security. The latest $7.6 billion K-12 education-related bill supported by Gov. Abbott in the fourth special session was killed in the House. The massive education bill died after Rep. John Raney, R-College Station, introduced an amendment to remove Texas’ first ESA program from the bill. The amendment passed with 21 Republicans joining all Democrats, essentially killing the bill as it likely is stuck until the special session ends Dec. 7. Gov. Abbott asserts that he will keep fighting for school choice, with the possibility of calling more special sessions. But trying to pass universal school choice before the next regular session in 2025 would be a mistake. This progress was historic as it was the first time since 2005 that a school choice bill had passed out of the House Public Education Committee and made it to the House floor. The Senate has passed school choice bills out of its chamber many times since then, including several times this year. The latest House bill allocated $7.1 billion for additional public school funding and only $486 million for ESAs. Put another way, that’s more than $14 for public schools for every $1 for school choice, which amounts to providing an ESA of $10,700 to only 45,400 students, or just 0.7% of the 6.3 million school-age kids. Texas is long overdue to join the growing number of states that have passed it. But there’s no path to real school choice for every student in Texas now because of politics, not from a lack of support among Texans. A recent University of Houston survey found that 47% of Texans support school choice “for all parents, regardless of income,” and only 28% oppose it. The support exceeds opposition to it across all demographics, including rural areas. The politics of this is a strange bedfellows of some Republicans and all Democrats spreading fear based on teacher union claims that public schools won’t survive. But doesn’t that fear concede that those schools in a monopoly government school system can’t compete and aren’t serving families well? The best chance to pass true universal school choice, not the minimal and problematic school choice in the House’s and the Senate’s bills, is to vote out representatives who prioritize teacher unions over Texans. Then, come back to the regular session in 2025 and pass a bill that won’t let Texans continue to fall behind. This is how to help students, parents, and teachers–who would see better pay and benefits through school choice. Gov. Abbott is leading the way. He recently endorsed 58 House Republicans who voted against Raney’s amendment and made his first endorsement of a candidate running against an incumbent who voted for the amendment. Some argue that more Texas public school funding is the answer instead of school choice. But as Texas continues to increase funding for public education to record levels, a recent public school ranking shows that Texas public schools rank 13th worst of all 50 states. In another ranking, only 23% of 8th graders performed at or above the National Assessment for Educational Progress (NAEP) proficiency level on its nationally recognized exam. This means that 77% of 8th graders in Texas scored below proficiency on this national exam. Clearly, the monopoly government school system is failing students in Texas. More funds will not fix this monopoly government school system problem; only more parental freedom will. Although history was made this year, these efforts aren’t enough. Universal school choice with ESAs for every parent to choose the type of schooling for their kids must be the outcome for better student outcomes, higher teacher pay, more parental opportunities, and greater taxpayer benefits. Gov. Abbott has been pushing the correct path of universal school choice for more than a year. But given the current makeup of the Legislature, especially in the House, he should give passage of school choice a rest for now. Texans can only hope that the 2024 election will yield a new wave of politicians who reflect what they want: putting kids first. www.chronicle-tribune.com/opinion/could-social-media-regulation-stifle-our-future/article_1dd66cd8-5e61-5e04-ac82-e9c56b12d166.htmlOriginally published at the Tribune.

This is the season of controversial big-government actions by Republicans and Democrats. They too often want to direct people’s actions toward how politicians see fit, through policies dealing with industrial support, climate change, and labor markets. One concern is regulating social media. From the Supreme Court’s scrutiny of Texas and Florida’s social media laws to Utah and other states unveiling social media rules for the digital world, parental rights and capitalism are at a pivotal moment. The policy choices we are making now on these issues will impact the brightest spot in the American economy. As economist Thomas Sowell correctly noted, there are no solutions, only trade-offs. This is a reason why it is crucial for Americans to grasp the trade-offs of social media regulation before politicians and bureaucrats take action. Utah’s ”Social Media Regulation Act” serves as a cautionary tale of government overreach with severe trade-offs. While the road to online safety is paved with good intentions, as we all want the best for minors (and everyone), we must evaluate policies by their real-world results. Utah’s law mandates minors under 18 must obtain a guardian’s permission to create social media accounts. If they proceed, the guardian gains full access to the minor’s account, with default curfew settings between 10:30 p.m. and 6:30 a.m. Additionally, minors cannot receive unapproved direct messages, and their accounts are blocked from appearing in search results. While there is mixed evidence suggesting a relationship between excessive social media usage and declining mental health, a recent study from Gallup reveals that parents have an even more prominent role than social media when it comes to well-being: “The strength of the relationship between an adolescent and their parent is much more closely related to their mental health than their social media habits. When teens report having a strong, loving relationship with their parents or caretakers, their level of social media use no longer predicts mental health problems.” Even if the mental health studies are correct, Utah’s law may not help teens most in need. Implementing government regulations always comes with a cost, and in this case, the very thing this policy intends to help could be harmed as a result. Parenting could be taken from parents and given to social media companies and government bureaucrats. Another trade-off looms: Will children growing up with restricted access to social media be disadvantaged compared to their counterparts in states and countries without such restrictions? Social media plays a key role, not just socially, but also professionally. The effect of limited exposure to these platforms remains uncertain. Beyond concerns about parental rights and career challenges, bills like these can seriously disrupt free markets and the prosperity we’ve seen them bring. Instead of restrictions, states and the federal government should focus on education. Indeed, many states are considering such digital literacy laws, following in Florida’s footsteps. On the free speech side of social media regulations, the bills in Texas and Florida aimed to prevent social media companies from selectively influencing digital expression. The Texas law was challenged in court and upheld; the Florida law was challenged and struck down. Now, these laws will be considered by the Supreme Court, and the outcome will have a big impact on the social media ecosystem. Although it’s frustrating for social media companies to potentially influence users by removing, promoting, or de-ranking specific content besides pornography, they are within their rights to do so. Content moderation practices, whether strict or open, bring a great opportunity for competition. For example, platforms like Rumble emerged in response to concerns that the big social media companies were unfairly moderating their content and attracting millions of users. This exemplifies the essence of free enterprise — problems inspire innovation, and competition drives improvement, allowing for diversification. But if social media companies in these states are compelled to adhere to the restrictive regulations, it will deter new startups and stifle growth. The social media landscape is evolving rapidly, and regulations like these demand careful consideration. While the safety of minors online is paramount, for our kids and yours, it’s crucial to strike a balance that preserves parental rights, encourages innovation, protects free speech, and safeguards individual freedoms. As we navigate this digital age, let’s remember that effective solutions should empower parents, consumers, and promote competition, not hinder progress with more government. These are the things that have provided the greatest human flourishing in free-market capitalism.  Originally published at Econlib.