Podcast: What do $34 Trillion Debt, Border Wall, & 22 States Raise Minimum Wages gave in common?1/5/2024 Thank you for listening to the 42nd episode of "This Week's Economy."

Today, I cover: 1) National: -Gross federal debt reaches $34 trillion -Immigration data shows there were more illegal immigrants than American births in August 2023 -Inflation updates and my thoughts on the policies presented by current GOP candidates 2) States: -22 states increased minimum wage, which is a bad idea -Important issues on the Texas Republican primary ballot -Key opportunities for welfare reform in states to lift people out of poverty 3) Other: -My two latest interviews with NTD News discussing interest rates potentially falling and what we can expect from this year's economy -My recent op-ed published at AIER about what America can learn from new Argentine President Javier Milei -My radio interview with Newell Normand on WWL NOLA on changes in tax code in 2024 Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. Also, subscribe and see show notes for this episode on Substack (www.vanceginn.substack.com) and visit my website for economic insights (www.vanceginn.com).

0 Comments

In 2023, Texas led the U.S. on many fronts: job growth, economic expansion, energy production, and a record surplus of $33 billion. This was when many other states, especially California, were reporting economic challenges and deficits.

Despite Comptroller Glenn Hegar's warning to spend wisely, the 88th Texas Legislature chose out-of-control, record spending. This isn’t a record Texans wanted because it means less available money for property tax relief. Texas can reverse course to lead the U.S. in fiscal responsibility by passing sustainable budgets that result in more surplus to return to taxpayers by reducing school property tax rates until they are zero. In 2023, the Texas Legislature passed the largest spending increase in state history. The fiscal 2024-25 budget increased appropriations by 21.3% to $321 billion, or, excluding federal funds, by 31.7% in state funds to a staggering $219 billion. Even more disturbing is that currently reported amounts may increase further as some legislation passed in the special sessions increases spending. Either way, the budget growth far eclipsed the rate of population growth plus inflation, which increased by 16% over the prior two years. This rate is a good comparison because it represents the average taxpayer’s ability to pay for government spending. This record spending, along with records of over $10 billion in new corporate welfare payments even to multi-billion-dollar companies and more than $13 billion in constitutional amendments that move money outside of the state’s spending limit, sets a challenging path forward. The bloated fiscal 2024-25 budget now looms as the new baseline for lawmakers, expanding government to the chagrin of many Texans. The excessive budget increase overshadowed Gov. Greg Abbott’s historic tax relief compromise signed into law during the Legislature’s second special session. While hailed as the largest property tax cut in Texas history, it fell short. The total for new school property tax relief was $12.7 billion. It falls short of the $14.2 billion appropriated for reducing school property taxes in fiscal 2008-09 due to a Supreme Court of Texas ruling that the school finance system was unconstitutional. But when the amount is adjusted for inflation since then, the $14.2 billion would be about $21 billion. Even when factoring in the state’s contribution of $5.3 billion to maintain reductions in school property taxes in prior sessions, the $18.3 billion in combined relief remains well below the $21 billion needed to be the largest in Texas history. It should be noted that the $14.2 billion for property tax relief for fiscal 2008-09 helped cut school property taxes by just $2 billion in 2007. But then school property taxes increased by $2.3 billion in 2008, surpassing 2006 before the relief by $300 million. Total property taxes decreased by just $450 million in 2007 and then increased by $3.8 billion in 2008. While those with property received some relief in their property tax bill in 2023, especially those with a homestead exemption, the amount will not be nearly as much as some lawmakers claimed. Worse still, these savings won’t likely last as local governments continue to push to pass bonds and increase spending and taxes. The Legislature should focus this interim on doing efficiency audits across the government, much like it started with safety net programs. Finding savings across the government with so much excessive spending recently will help maintain the property tax relief passed last year; spending excesses will not lead to calls for tax increases, and resulting surpluses can put school property taxes on a fast path to zero next session. There will also be an opportunity to put the new, stronger statutory spending limit in the constitution and have this limit cover spending by local governments. There should also be a requirement that at least 90% of resulting surpluses by the state go toward reducing school property tax rates and by local governments to reduce their own property tax rates. Doing so will achieve fiscal sustainability and put all property taxes on a path to elimination. In the meantime, Texans have opportunities in the March primary and November general election to consider many candidates' policy proposals. Do candidates on the ballot support eliminating property taxes, reducing government spending, and increasing prosperity? We need more politicians pushing for these things because they benefit Texas families and entrepreneurs. Let’s not have big-government socialism creep more into Texas but turn back toward free-market capitalism that has contributed to abundance. Originally published at The Center Square. Episode 77 is with Dr. Mark Calabria, former chief economist of former Vice President Mike Pence, senior advisor at Cato Institute, and author of “Shelter from the Storm: How a COVID Mortgage Meltdown Was Averted.”

Today, we discuss: 1) His lessons learned from working as Former Vice President Mike Pence's chief economist; 2) How he helped the nation avert a mortgage crisis during COVID and issues with pandemic policies and their ongoing impacts; and 3) Why was the economy in 2019 so successful, and what should be done to improve things in 2024? Check out Mark's book: https://www.cato.org/books/shelter-storm Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. Also, subscribe and see show notes for this episode on Substack (www.vanceginn.substack.com) and visit my website for economic insights (www.vanceginn.com).  Argentina’s new self-described “anarcho-capitalist” President, Javier Milei, is raising eyebrows worldwide with his aggressive attempts to restore the nation’s abysmal economy. On December 20, he signed a decree to remove many government regulations stifling international trade and domestic activity.

With Argentina’s poverty rate soaring to 40.1 percent in early 2023 and its debt burden owed to the International Monetary Fund (IMF) now $45 billion along with its other mountains of debt, the time is now for a no-nonsense pro-growth approach that gets the government out of the way. Since Milei’s inauguration on December 10, he’s set out bold initiatives. These include reducing government spending by as much as five percent of the nation’s GDP, slashing the number of federal ministries by half to nine, and, most notably, declaring that he will devalue the nation’s currency, the peso, by more than 50 percent. To paint a picture, some estimate that the decision to devalue the peso and other policy changes could bring already rapid inflation of more than 160 percent up to as high as 300 percent. Onlookers have been quick to criticize these actions and their potential effects on the country, but desperate times call for desperate measures. And the US, most of all, should not point fingers. If anything, we could stand to learn a thing or two from Milei’s proactive approach. While Milei’s moves will temporarily exacerbate inflation and further strain the economy, as he’s acknowledged, it also aims to enhance the country’s future. Moving from a government-dominated, top-down economy to one built on free-market capitalism is a significant institutional shift. We already know from the work of economist Douglass North that these economic changes are what support more ways to let people prosper, but that the adjustment period will be challenging. There are currently many hindrances to the free exchange of people in the marketplace, and these inefficiencies take time to correct through a well-functioning price system. But after this “shock therapy” comes a brighter future. There will also likely be a move away from the country’s currency of the peso to the US dollar, which should help stabilize markets, inflation, and economic activity. This would provide a better anchor than the peso does today, even though the anchor of the dollar has its own troubles. It’s hard to conceive how Argentina was one of the world’s wealthiest nations only a century ago. Once surpassing European powers in its economic strength, Argentina’s standing took a nosedive in 1929 when it abandoned the gold standard. The shift began a challenging period as protectionist trade policies, influenced by former Argentina President Juan Peron, eroded its once-thriving trade status. Moreover, excessive regulations further distorted price signals, and the emergence of a military dictatorship during the 70s and 80s brought everything crashing down. But the troubles didn’t stop there. In 2001 and 2002, Argentina experienced a severe economic crisis when the government partially defaulted on its debt, froze bank accounts, and abandoned the dollar. The aftermath was characterized by economic collapse, unemployment, and widespread political and social unrest. Argentina had a rough start to the 21st century, and its challenges have only snowballed since. Rampant inflation, exacerbated by the central bank’s relentless money printing to cover mounting debts, has led to the plummeting credibility of the Argentine peso. So Milei’s strategy will likely worsen things before they can improve. Along with shrinking the government, his objective to balance the budget by the end of 2024 is a historical measure aiming to alleviate debt with spending cuts instead of tax hikes, often the go-to when more money is needed. But as the work of the late economist Alberto Alesina confirms, the best path forward for austerity is to cut government spending, not raise taxes, to avoid a deeper recession and higher debt. Cautious optimism is warranted, as the nation’s leaders have a history of abusing power, and we can’t foresee how Milei will wield his influence over time. One concerning move is his intention to raise taxes on grain, which would be a big blow to many farmers. But even so, things should look up if he sticks to what he initially set out to do and what he has done so far. As the US observes Argentina’s economic trajectory, it must take note of the cautionary tale embedded in Milei’s approach. The focus on reducing government spending and narrowing the scope of government aligns with the prescription needed to combat inflation not just there but here. America’s inflationary challenges, rooted in a bloated Federal Reserve balance sheet helping fund excessive government deficit-spending, require Congress to take decisive action. Inflation will strain household budgets until the reins are pulled on government spending, and the Fed cuts its balance sheet more aggressively. We can’t be too proud to take a tip from Argentina. The perilous outcomes of unchecked government spending can manifest anywhere; strategic policies such as responsible spending limits only become more necessary the longer their implementation is delayed. Argentina’s bold moves, though met with skepticism, could be the beacon the US needs to navigate its own economic storms successfully. But until then, let’s keep cheering what the classical liberal President Milei is doing in Argentina. Originally published at AIER. Today, I cover my predictions for the economy in 2024 in less than 6 minutes, including information on:

Thank you for tuning into the FINAL Let People Prosper podcast episode 76 of 2023! Today, I have a brief but informative podcast for you, recapping the highlights of the economy and my business, Ginn Economic Consulting, LLC.

As a Christmas gift, I am giving away a complimentary subscription to the paid version of my newsletter and a copy of Lexi Hudson’s fantastic book, “The Soul of Civility: Timeless Principles to Heal Society and Ourselves.” To enter this giveaway, simply fill out the information at the link and rate my podcast on either Apple Podcasts or Spotify. Is there anyone whom you would like for me to interview in 2024? Leave them in the comments. Today, I cover:

This was originally published at National Review.

Colorado governor Jared Polis (D) and Art Laffer, the economist and Presidential Medal of Freedom honoree, recently critiqued the state’s Taxpayer’s Bill of Rights (TABOR) at this venue. While not meritless, much of their argument is paradoxical, highlighting an overarching issue of fiscal unsustainability that warrants a reality check. TABOR recently had its 30th birthday. Voters approved the constitutional amendment in 1992, establishing the strongest tax and expenditure limit in the country. It’s been the gold standard for a sound spending limit ever since. Under the amendment, annual growth in spending cannot exceed the state’s population growth plus inflation, which is a good measure of the average taxpayer’s ability to pay for spending. When adopted, the limit covered about two-thirds of state spending. It requires voter approval for tax increases and mandates refunds to taxpayers if tax revenue exceeds the limit. In their critique, Polis and Laffer correctly acknowledge that TABOR surpluses indicate that income-tax rates are too high. They’re correct that the state should seek to reduce income-tax rates to prevent overcollection instead of handing out refunds. They’re also correct that a broader tax base is preferable. It enables the tax rates, and therefore the marginal effect of the tax burden, to be reduced as much as possible for all. But Polis and Laffer incorrectly criticize TABOR without realizing its pivotal role in achieving their purported goal to reduce taxes. Without a crucial spending check such as TABOR, the state would tie its budget directly to revenue levels, eliminating any surplus. While Polis has only recently touted reducing state income-tax rates with surpluses, the Independence Institute has long supported a plan called “Path to Zero.” The plan simply limits government spending and uses resulting surpluses to lower tax rates until they’re zero. This is similar to my efforts in Texas, Louisiana, and other states, which start with a sustainable budget approach, as recently explained in a release by Americans for Tax Reform. Unfortunately, courts and politicians have eroded the strength of TABOR over time, primarily because of politicians’ lack of fiscal restraint. The result has been that TABOR now covers less than half of state spending, allowing expenditures of all state funds, which excludes federal funds, to grow faster than population growth plus inflation. Specifically, appropriations of all state funds have increased by 74.2 percent, compared with an increase of just 46.5 percent in population growth plus inflation over the last decade. This has resulted in the state appropriating $4.2 billion more in just fiscal year 2023–24 than if it had been limited to the rates of population growth plus inflation over time, amounting to higher spending and taxes of about $3,300 per family of four. The summed difference each year in all state funds above this metric over the decade amounts to $16.3 billion, or $11,300 per family of four. These amounts don’t necessarily mean that the state needs to start cutting its budget to get back on track, but they do mean that the time to start reining in the budget is now, to reduce these excessive burdens on taxpayers. To that end, Ben Murrey, director of the Independence Institute’s fiscal-policy center, and I have shown the path forward with the Sustainable Colorado Budget (SCB). The SCB is a maximum threshold for the initial appropriations of all state funds and is based on TABOR’s rate of population growth plus inflation. This will help reinforce the original intent of TABOR, by broadening the spending limit to all state funds. The plan would limit nearly two-thirds of state spending each year, as when voters first adopted TABOR. Doing so will result in larger surpluses to reduce income-tax rates yearly until they’re zero. Polis and Laffer are right to want rate reductions, but there are none if there is no surplus. For the upcoming FY 2024–25, the SCB proposes an all-state funds ceiling of $27.70 billion. This uses the prior FY 2023–24 amount of $26.15 billion and increases it by 5.9 percent, calculated using TABOR’s current method and reflecting a 1.0 percent increase in the state’s population and 4.9 percent inflation. As noted above, it would be even better to grow the budget by less or not at all to correct past budgeting excesses. This more robust TABOR approach outlined in the SCB helps to freeze inflation-adjusted spending per capita, allowing the average taxpayer to afford the cost of government. In recent years, the current TABOR limit alone has already produced substantial surpluses that have been refunded to Coloradans. But instead of using this year’s $1.7 billion TABOR surplus to refund overcollected taxpayer dollars, the legislature could have cut the income-tax rate from a flat rate of 4.4 percent, which ranks 14th in the country, to 3.81 percent. Further, had the state over the past decade followed the SCB, which has a larger base budget, lawmakers could have lowered the income-tax rate to 2.96 percent, putting it on a faster path to becoming the lowest flat income-tax rate in the country, below North Carolina’s 2.49 percent. It would also pave the way to zero income taxes by 2042. Polis in his recent article criticizes TABOR for acting as a spending restraint rather than a mechanism to reduce tax rates. Indeed, his track record in the governor’s office demonstrates his distaste for limitations on spending. The state budget has grown 45 percent since he took office less than five years ago; his budget request for the upcoming fiscal year would constitute an astounding 52 percent increase. In a state with a constitutional balanced-budget requirement, it’s paradoxical to support tax cuts without spending restraints. Unfortunately, given his poor track record on spending and his critique of TABOR’s spending restraints — which he and Laffer improperly call a revenue limit — Polis is unlikely to adopt our sustainable budget to produce larger surpluses with which to cut tax rates. On the contrary, this year he supported a measure that would have increased state spending above the current limit, erroneously claiming that it would cut taxes using state surpluses. “A similar tax-rate reduction for property taxes, Proposition HH, failed on the ballot recently in Colorado,” Polis and Laffer write in their recent NRO article. While a clever misdirection, this argument doesn’t hold up. Prop HH didn’t directly offset the TABOR surplus through tax cuts, as an income-tax reduction would. That’s because the measure influenced only local property-tax revenue. Because the State of Colorado generates no tax revenue from property taxes, as those are collected only by local governments, reducing those rates won’t affect the TABOR surplus. Polis and Laffer contend that the state budget indirectly benefits from local property taxes. However, Prop HH would have lessened the state’s share of local funding by only approximately $125 million. Today, I cover:

1) National:

Want more of my insights, check out the paid version of my Substack newsletter.  Originally published at Real Clear Policy.

During the fourth Republican presidential candidate debate the four participating candidates were asked to name a past president who would serve as an inspiration for their administration. In his response, Governor Ron DeSantis stated that he would take inspiration from President Calvin Coolidge. Coolidge, stated DeSantis, is “one of the few presidents that got almost everything right.” Further, DeSantis argued that “Silent Cal” understood the federal government’s role and “the country was in great shape” under his administration. To say that the federal budget process is broken is an understatement. The national debt continues to grow driven by out-of-control spending. The budget hawk within the Republican Party is an endangered species. Governor DeSantis is correct that the Republican Party needs to rediscover the principle of limited government. The best way to do this is to take inspiration from the Republican Party’s best known budget hawks and champions of limited government, Presidents Warren G. Harding, and Calvin Coolidge. President Harding assumed office in 1921 when the nation was suffering a severe economic depression. Hampering growth were high-income tax rates and a large national debt after World War I. Congress passed the Budget and Accounting Act of 1921 to reform the budget process, which also created the Bureau of the Budget (BOB) at the U.S. Treasury Department (later changed in 1970 to the Office of Management and Budget). President Harding’s chief economic policy was to rein in spending, reduce tax rates, and pay down debt. Harding, and later Coolidge, understood that any meaningful cuts in taxes and debt could not happen without reducing spending. Harding selected Charles G. Dawes to serve as the first BOB Director. Dawes shared the Harding and Coolidge view of “economy in government.” In fulfilling Harding’s goal of reducing expenditures, Dawes understood the difficulty in cutting government spending as he described the task as similar to “having a toothpick with which to tunnel Pike’s Peak.” To meet the objectives of spending relief, the Harding administration held a series of meetings under the Business Organization of the Government (BOG) to make its objectives known. “The present administration is committed to a period of economy in government…There is not a menace in the world today like that of growing public indebtedness and mounting public expenditures…We want to reverse things,” explained Harding. Not only was Harding successful in this first endeavor to reduce government expenditures, his efforts resulted in “over $1.5 billion less than actual expenditures for the year 1921.” Dawes stated: “One cannot successfully preach economy without practicing it. Of the appropriation of $225,000, we spent only $120,313.54 in the year’s work. We took our own medicine.” Overall, Harding achieved a significant reduction in spending. “Federal spending was cut from $6.3 billion in 1920 to $5 billion in 1921 and $3.2 billion in 1922,” noted Jim Powell, a senior fellow at CATO Institute. Harding viewed a balanced budget as not only good for the economy, but also as a moral virtue. Dawes’s successor was Herbert M. Lord, and just as with the Harding Administration, the BOG meetings were still held on a regular basis. President Coolidge and Director Lord met regularly to ensure their goal of cutting spending was achieved. Coolidge emphasized the need to continue reducing expenditures and tax rates. He regarded “a good budget as among the most noblest monuments of virtue.” Coolidge noted that a purpose of government was “securing greater efficiency in government by the application of the principles of the constructive economy, in order that there may be a reduction of the burden of taxation now borne by the American people. The object sought is not merely a cutting down of public expenditures. That is only the means. Tax reduction is the end.” “Government extravagance is not only contrary to the whole teaching of our Constitution but violates the fundamental conceptions and the very genius of American institutions,” stated Coolidge. When Coolidge assumed office after the death of Harding in August 1923, the federal budget was $3.14 billion and by 1928 when he left, the budget was $2.96 billion. Altogether, spending and taxes were cut in about half during the 1920s, leading to budget surpluses throughout the decade that helped cut the national debt. The decade had started in depression and by 1923, the national economy was booming with low unemployment. Both Harding and Coolidge were committed to reining in spending, reducing tax rates, and paying down the national debt. Both also used the veto as a weapon to ensure that increased spending and other poor public policies were stopped. The results of the Harding-Coolidge economic plan created one of the strongest periods of economic growth in American history. Unemployment remained low, the middle class was expanded, and the economy expanded. From 1920 to 1929 manufacturing output increased over 50 percent and the United States was a global leader in many key industries. In our current era marked by dangerous debt levels and high inflation whoever becomes the Republican presidential nominee should take inspiration from Harding and Coolidge. Thank you for tuning into the 75th episode of the Let People Prosper Show podcast!

Today, I’m joined by Dr. Chris Coyne, professor of economics at George Mason University and author of the book, “In Search of Monsters to Destroy: The Folly of American Empire and the Paths to Peace.” Today, we discuss: 1) The economic impact of war and the many consequences of engaging in it; 2) What Friedrich Hayek's principle of "fatal conceit" reveals about America's involvement with war; and 3) The truth about terrorism, what the U.S. got wrong with Afghanistan and Iraq, and Chris' thoughts of how Russia-Ukraine and Israel-Hamas can be at peace.  Originally published at Econlib.

After a year dominated by historically high inflation and soaring home loan rates, 2023 is carving another negative as the annum of antitrust accusations. From lawsuits targeting Amazon and Google to the emergence of concerns over trading card and sandwich shop monopolies, the growing antitrust frenzy poses a threat to what these laws were originally crafted to safeguard: consumers. Actions of antitrust’s biggest modern advocates, like the Federal Trade Commission’s Chair Lina Kahn and U.S. Sen. Elizabeth Warren, reveal their misunderstanding of these competition laws. To maintain their protected freedoms to buy, sell, and trade, consumers and businesses must know the truth enshrined in these laws and not be duped by misrepresentation. Antitrust laws were enacted with a noble purpose—to protect consumers and promote fair competition. These laws were designed to ensure consumer access to various choices across the marketplace and prohibit businesses from engaging in anti-competitive practices. If those parameters seem vague, that’s because they are. That is, without antitrust’s crucial cornerstone, “the consumer welfare standard” established in the 1970s to help narrow the law’s scope. A principle that assesses whether consumers are better or worse off due to a company’s actions, the consumer welfare standard is mathematically defined as “the value consumers get from the product less the price they paid.” The addition of this language shifted antitrust’s emphasis from preserving competitors to competition. But perceived value varies between individuals. Concerns about monopolies can be legitimate when there is concern about diminished value from a product or service because of a company’s actions. Such monopolistic behavior may result in higher prices and lower quality. These tactics are most likely to prevail when outside competition is intentionally stifled by the government through regulations, spending, and corporate welfare. However, having a large or growing market share alone does not violate antitrust laws, as progressives like Warren would lead people to believe. In a healthy competitive market, companies naturally strive to develop and acquire other businesses to expand their offerings and meet consumer demands. Roark Capital’s acquisition of Subway, adding the sandwich chain to its portfolio, and major sports leagues signing contracts with trading card company Fanatics may seem like consolidation of power, but these changes do not inherently harm consumers or competition. In fact, if permitted to expand via purchasing and agreements with other companies or leagues, not just these but all businesses can improve consumer welfare and profitability. To the chagrin of its Italian competitor, the NFL, MLB, and NBA making agreements with the sports trading card company Fanatics was a voluntary decision executed because increased, not diminished, consumer welfare was perceived. While Panini SpA points the antitrust finger at Fanatics, it has three other fingers pointing back at itself, as the company has its own agreements with the NFL and NBA. Rather than viewing the new competition as an opportunity to improve its company and become the first choice, Panini SpA would rather waste time and resources trying to punish its competitor. This is what the FTC will try to do with Subway, the European Union wants to do with Amazon, and the DOJ has tried to do with Google. This knowledge is critical because consumers are being swayed to favor legal action that does not serve their best interest, more than likely because of widespread misinformation. For instance, a recent poll showed that 60% of Americans believe Google is too big and hurts businesses and consumers. However, conflicting data reveal that, overwhelmingly, Google users and employees derive immense value from its service. At the same time, other search engines continue to increase in popularity alongside Google, with Safari recently reaching more than one billion users. So, if the majority of Google users are happy with the service and other search engine options exist, the welfare of its consumers is far from threatened. But that hasn’t stopped the FTC from trying to take them down. So-called “big tech giants” and “trading card monopolies” aren’t the true titans threatening consumer welfare; it’s the rent-seeking politicians, government bureaucrats, and corporate rent-seekers wielding an insatiable appetite for control that are consumers’ actual adversaries. Economic Reality Check: What Do Falling Mortgage Rates & Jobs+Inflation Signal for the 2024 Economy?12/15/2023 Thank you for tuning into the 39th episode of “This Week’s Economy.”

Much information is packed into today’s newsletter, including my new podcast episode revealing the economic news you need to know in less than 14 minutes! Today, I cover: 1) National: -Why the new U.S. jobs report (my latest commentary) is not as strong as some say -Inflation rates have moderated but still remain well above the Fed’s 2% rate target -Federal Reserve paused again with its federal funds rate target in the range of 5.25-5.5%, supporting a boost in the stock market and likely lower mortgage rates 2) States: -Sustainable Colorado Budget was released that I authored with Ben Murrey at Independence Institute, which provides a path forward for the Centennial state to return to its TABOR roots and buy down the income tax -School choice challenges face Texas as many state leaders are against it, and they keep spending too much -California’s deficit reaches crazy highs, proving why spending is the ultimate government burden 3) Other: -Don't miss my latest LPP episode with Jennifer Huddleston discussing problems with regulating technology, including AI -One of my latest op-eds argues why China is not our biggest threat…what is? -Argentina's new president makes significant strides that could set an example for the U.S.  Recent polling data from CNN reveals a grim reality: 84 percent of Americans are concerned about the national economy. Despite President Biden’s efforts to highlight seemingly positive metrics as indicators of the success of his progressive policies, a closer look at the data reveals why most Americans remain dissatisfied.

Biden’s claim of adding 14 million jobs since taking office would be impressive if it were true. The reality is that, since he took office in Jan. 2021, 13 million private sector jobs have been added. This appropriately excludes the unproductive addition of one million government jobs that will soon set a record under his watch. But the bigger point negating his rosy scenario is that the vast majority of this touted “job growth” stems from restoring job losses from the pandemic lockdowns. When we accurately tally the new jobs added since the shutdowns began in Feb. 2020, the count stands at 4.5 million private sector jobs added in three years. While this is a positive, it’s an average of 1.5 million jobs yearly, far from qualifying as record-breaking job creation. The latest U.S. jobs report for November provides additional data, reaffirming the mixed nature of the labor market. The payroll report indicates a feeble performance. There was a headline number of 199,000 jobs added. But there were revisions in October of 35,000 fewer jobs added. So, net additions stand at 164,000 jobs. When government jobs are correctly subtracted, the count is just 115,000 new productive private jobs last month. On a more positive note, the household report shows a substantial increase of 532,000 in the labor force, resulting in a 62.8 percent participation rate. Employment experienced robust growth of 747,000, contributing to a decline in the unemployment rate to 3.7 percent. But the broader unemployment rate that includes underemployed and discouraged workers is nearly twice as high at seven percent. However, it’s crucial to note that the average weekly earnings show a 3.7 percent increase over the last year, though this has been overshadowed by the elevated inflation. Fresh data on inflation as measured by the chained consumer price index (chained-CPI), which accounts for the substitution effect of changes in individual prices not accounted for by the headline CPI, reveals signs of moderation. The latest core chained-CPI inflation rate, which excludes food and energy and is watched by the Federal Reserves, for Nov. 2023 was up 3.7 percent year-over-year. Not only is this 85 percent higher than the Fed’s average inflation rate target of two percent, it also nearly matches the increase in earnings, negating any increase in purchasing power. In fact, real average weekly earnings have declined for 24 straight months. No wonder people are concerned about the economy. The ongoing reduction of the Fed’s balance sheet contributes to this inflation moderation, but further cuts to its bloated balance sheet are necessary to stabilize prices across the economy. Their balance sheet currently hovers around $8 trillion, nearly double its pre-pandemic figure, having increased tenfold in fifteen years from $800 billion in 2007. While some blame the national debt crisis on not having enough tax revenue from slower-than-optimal GDP growth, the truth is excessive government spending. Inflation is not your fault, as The Atlantic recently claimed. It’s the fault of excessive government spending by Congress that led to rising national debt which the Fed purchased and printed money. Too much money chasing too few goods is the classic definition of inflation, and it fits this time, too. A better way to solve this would be to slash government spending and taxes like President Calvin Coolidge did a century ago. During the Roaring 20s, the national debt declined, and the economy supported more opportunities for people to flourish. In light of the evidence, the question arises: Is Bidenomics working? The answer, drawn from the data, suggests it is not. To guide the economy back on course, recalibration is imperative. This includes prioritizing fiscal responsibility, pruning the Fed’s ballooning balance sheet, and reining in excessive government spending. Only through such pro-growth measures can we hope to unlock genuine economic recovery and chart a course toward lasting prosperity. Is Being Big Bad? Are Antitrust Accusations of “Big Tech,” “Big Sandwich,” and Others Warranted?12/11/2023 Thank you for tuning into the 74th episode of the Let People Prosper Show podcast.

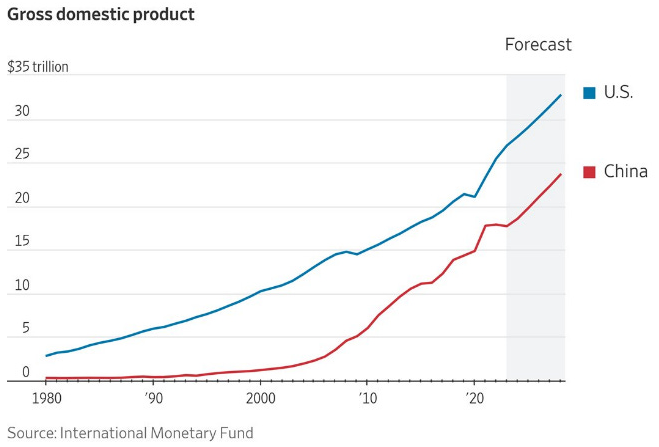

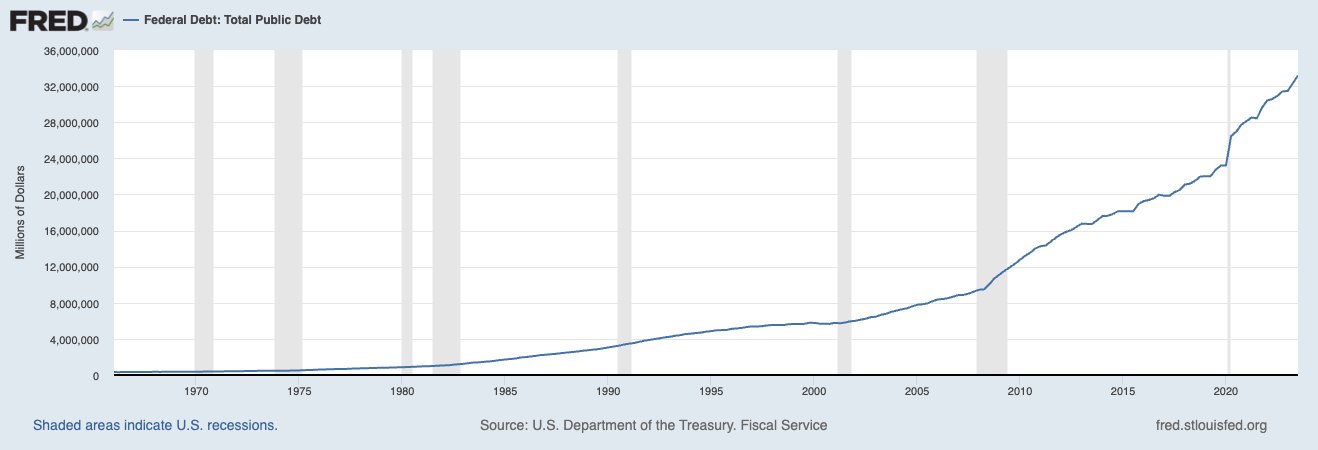

Today, I’m joined by Jennifer Huddleston, a technology policy research fellow at The Cato Institute. Today, we discuss: 1) What is the proper role of government in regulating or adapting to technological advancements; 2) Pros and cons of restricting AI, and why antitrust accusations are on the rise, specifically targeting “big tech,” and; 3) What you should know about government regulation on social media for minors, and how parents can be empowered to facilitate social media use at home.  Originally published at American Institute for Economic Research. Rating agency Moody’s just downgraded China’s credit outlook from stable to negative after doing the same to the US about a month ago. Does this mean that China is on equal footing with us? Worse? Better off? An economic analysis suggests that China is not our biggest threat, nor are we theirs. In fact, the biggest problem we face is completely self-inflicted and found on our home soil. Apprehensions about China’s military actions and trade strategies maintain resonance, especially among middle-aged and older Americans. While caution is warranted, especially concerning their censorship and the treatment of Hong Kong and Taiwan, an economic comparison settles many doubts.  Regarding economic might, the US outshines China with a GDP of $27 trillion compared to China’s $18 trillion. The contrast is stark on a per-capita basis. Americans enjoy an average income of $79,000, six times more than their Chinese counterparts. One alarming similarity stands out though: Both nations have weathered credit downgrades mainly due to escalating budget deficits and national debts. The United States’ national debt is shaping up to be this decade’s hallmark. Now nearly $34 trillion, the deficit spiked in 2020, with trillions of dollars more added since. Net interest payments on the debt climbed by 39 percent and recently surpassed $1 trillion annually.  The repercussions of the national debt crisis are not merely theoretical – they are tangible, affecting the everyday lives of citizens.

In 2023, the dollar has significantly depreciated. Fitch (and now Moody’s) downgraded our creditworthiness. Home sales hit their slowest pace since 2010. Average 30-year fixed mortgage rates reached their highest point since 2000. And real median household income dipped to its lowest level since 2018, to name just a few of our recent economic woes. These findings shed new light on our competition with China. They should prompt America’s leaders to reevaluate our priorities and consider whether the enemy across the Pacific is as pressing as the ones we face at home. While some argue the government spending that drove the deficits was necessary, especially during the pandemic’s peak, it underscores the broader problem – a lack of fiscal discipline and a predisposition to rely on debt as a quick fix. It is high time the US adopted a spending-limit rule. Without one, we’ve only made things worse and failed to reach budget agreements. A reasonable spending limit of no more than the rate of population growth plus inflation has worked at the state level, and it would work at the federal level. While the US points the finger at China, we have three other fingers pointing back at us. Excessive government spending and a burgeoning national debt are eroding the foundation of our economic stability. Now is not the time to allocate excessive resources to confront external foes, but to address the fundamental issue plaguing us: a government that refuses to rein in spending of taxpayer money. America should also correct the errors in recent years of trade protectionism. There is reason to counter those countries who don’t play by the same rules, like China, but that should be done by joining free trade agreements with allies. This would be a more effective and affordable approach for Americans instead of raising taxes on them through tariffs, appreciating the dollar thereby increasing the trade deficit and contributing to trade wars that often lead to military wars. Let’s refocus our efforts, fortify our economic foundation, and confront the genuine threat within our borders. If not, governments will not be able to do their job of preserving liberty. This is of utmost importance. Does New Data Support that Bidenomics is Working? Former White House Chief Economist Tells All12/8/2023 Thanks you for tuning into the 38th episode of “This Week’s Economy.”

Lots of information is packed into today’s newsletter, including my new podcast episode revealing the economic news you need to know in <13 minutes! Today, I cover: 1) National: Data shows that the economy is Americans' biggest concern and Bidenomics is making it worse, what the latest state and national GDP show, The Atlantic's bizarre claim about inflation, why my tweet about Biden’s job market claims made the community page, and why we should say no to a carbon tariff; 2) States: What a comparison between Florida and California reveal about policy, what I think Texas should do about School Choice and its $20 billion rainy day fund, and how a conservative state budget could take Iowa to the top; and 3) Other: What I learned attending the Meant for More Summit by the American Enterprise Institute and The Alliance for Opportunity about preventing poverty, my recent podcast episode with Dr. Gale Pooley, and a sneak peek of Monday's episode with Jennifer Huddleston.  Originally published at Independence Institute. In 1992, Colorado voters adopted the Taxpayer’s Bill of Rights (TABOR) to limit the growth in state and local spending. Over the past three decades, however, politicians from both parties and a complicit judicial branch have exempted more and more state spending from the TABOR limit. When voters adopted TABOR, 67% of state spending was subject to the limit. Today, the majority of state spending is not subject to the limit. Consequently, state spending has far outpaced Coloradans’ incomes over the last decade. To uphold the original intent of voters when they adopted TABOR, Independence Institute proposes the Sustainable Colorado Budget (SCB), which limits state spending from state funds (excluding federal funds) at the rate of population growth plus inflation. The state should then use the surplus revenue above the SCB spending limit to reduce the income tax rate for all taxpayers.  This commentary was originally published at The Center Square here.

A record number of states have passed universal school choice so far this year, but it seems Texas won’t be among them. Given the lack of universal school choice in multiple bills this year, I’m relieved it hasn’t passed in Texas yet. I’ve long been a researcher and staunch supporter of universal school choice. The way to do this is by making the eligibility and funding for education savings accounts (ESAs) available for all 6.3 million school-age students. ESAs put the power of choosing kids’ schooling in parents’ hands by picking public, private, home, co-op, micro, or other types of schooling. ESAs would be funded through the current school finance system and other general funds or new tax credits as necessary. After the Texas Legislature failed to pass a school choice bill in the regular legislative session earlier this year, Texas Gov. Greg Abbott added school choice to the third and fourth special sessions. The first two special sessions focused on property tax relief and border security. The latest $7.6 billion K-12 education-related bill supported by Gov. Abbott in the fourth special session was killed in the House. The massive education bill died after Rep. John Raney, R-College Station, introduced an amendment to remove Texas’ first ESA program from the bill. The amendment passed with 21 Republicans joining all Democrats, essentially killing the bill as it likely is stuck until the special session ends Dec. 7. Gov. Abbott asserts that he will keep fighting for school choice, with the possibility of calling more special sessions. But trying to pass universal school choice before the next regular session in 2025 would be a mistake. This progress was historic as it was the first time since 2005 that a school choice bill had passed out of the House Public Education Committee and made it to the House floor. The Senate has passed school choice bills out of its chamber many times since then, including several times this year. The latest House bill allocated $7.1 billion for additional public school funding and only $486 million for ESAs. Put another way, that’s more than $14 for public schools for every $1 for school choice, which amounts to providing an ESA of $10,700 to only 45,400 students, or just 0.7% of the 6.3 million school-age kids. Texas is long overdue to join the growing number of states that have passed it. But there’s no path to real school choice for every student in Texas now because of politics, not from a lack of support among Texans. A recent University of Houston survey found that 47% of Texans support school choice “for all parents, regardless of income,” and only 28% oppose it. The support exceeds opposition to it across all demographics, including rural areas. The politics of this is a strange bedfellows of some Republicans and all Democrats spreading fear based on teacher union claims that public schools won’t survive. But doesn’t that fear concede that those schools in a monopoly government school system can’t compete and aren’t serving families well? The best chance to pass true universal school choice, not the minimal and problematic school choice in the House’s and the Senate’s bills, is to vote out representatives who prioritize teacher unions over Texans. Then, come back to the regular session in 2025 and pass a bill that won’t let Texans continue to fall behind. This is how to help students, parents, and teachers–who would see better pay and benefits through school choice. Gov. Abbott is leading the way. He recently endorsed 58 House Republicans who voted against Raney’s amendment and made his first endorsement of a candidate running against an incumbent who voted for the amendment. Some argue that more Texas public school funding is the answer instead of school choice. But as Texas continues to increase funding for public education to record levels, a recent public school ranking shows that Texas public schools rank 13th worst of all 50 states. In another ranking, only 23% of 8th graders performed at or above the National Assessment for Educational Progress (NAEP) proficiency level on its nationally recognized exam. This means that 77% of 8th graders in Texas scored below proficiency on this national exam. Clearly, the monopoly government school system is failing students in Texas. More funds will not fix this monopoly government school system problem; only more parental freedom will. Although history was made this year, these efforts aren’t enough. Universal school choice with ESAs for every parent to choose the type of schooling for their kids must be the outcome for better student outcomes, higher teacher pay, more parental opportunities, and greater taxpayer benefits. Gov. Abbott has been pushing the correct path of universal school choice for more than a year. But given the current makeup of the Legislature, especially in the House, he should give passage of school choice a rest for now. Texans can only hope that the 2024 election will yield a new wave of politicians who reflect what they want: putting kids first. What can state and federal governments glean from Iowa's example when it comes to responsible budgeting? Find out! If you value responsible government budgeting and fiscal conservatism, I believe you’ll enjoy this podcast episode. Thank you to Iowans for Tax Relief Foundation’s ITR Live podcast for having me on their show to discuss a conservative approach to balancing Iowa’s state budget, my time at the White House, and free trade. Listen on Apple Podcasts or YouTube! Original publication at Iowans for Tax Relief Foundation.  If you’d like to learn more about the responsible state budget revolution sweeping the nation, check out my post, where I dive deeper into the topic, including my extensive work helping reform state budgeting across the country.

www.chronicle-tribune.com/opinion/could-social-media-regulation-stifle-our-future/article_1dd66cd8-5e61-5e04-ac82-e9c56b12d166.htmlOriginally published at the Tribune.

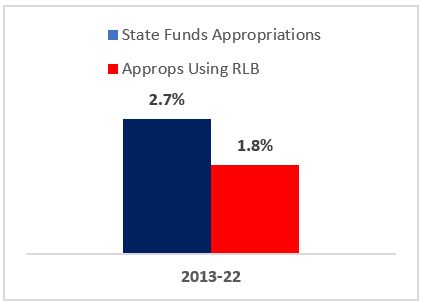

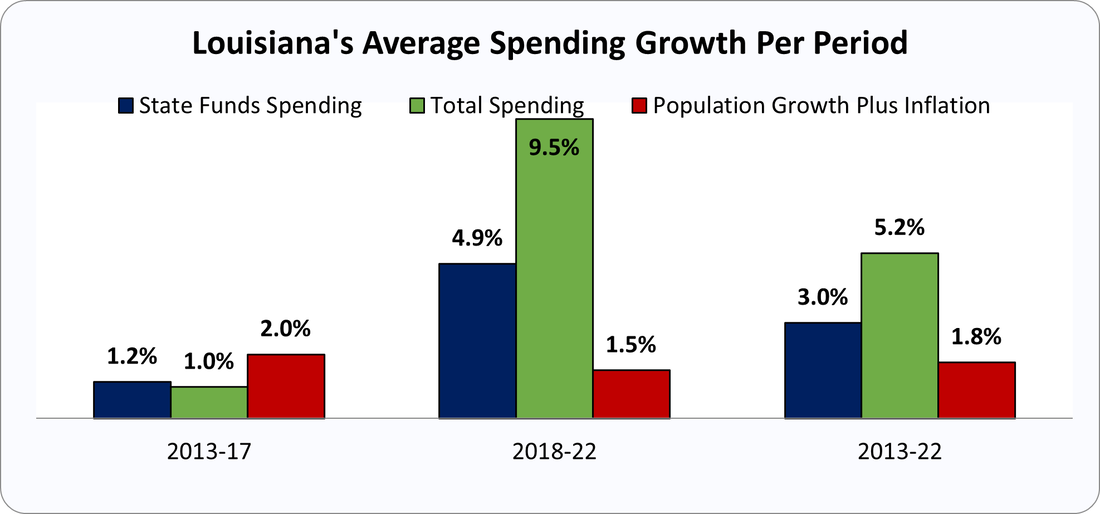

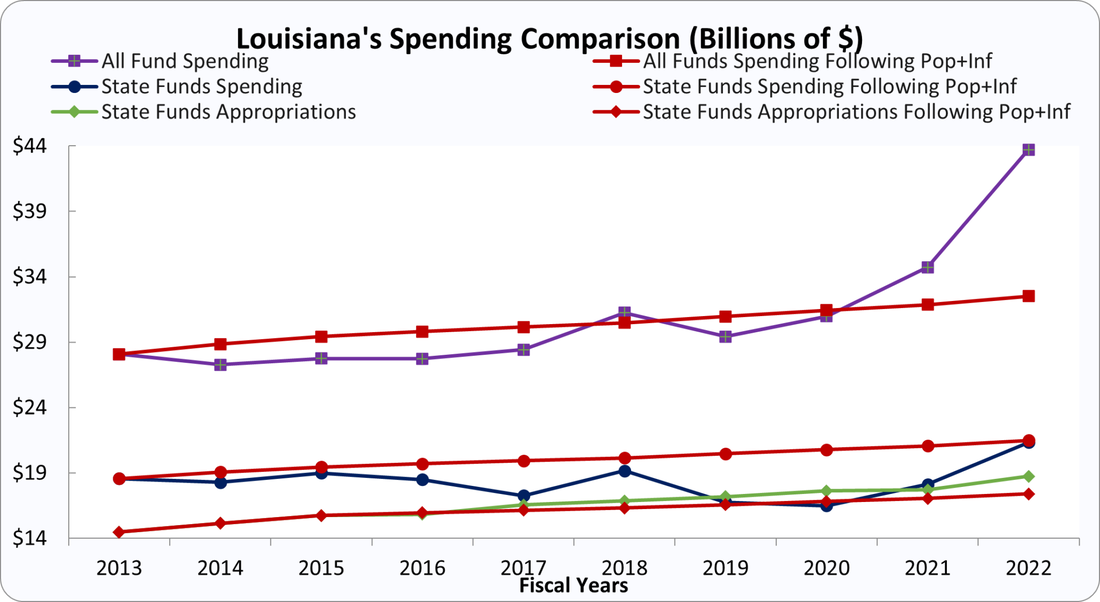

This is the season of controversial big-government actions by Republicans and Democrats. They too often want to direct people’s actions toward how politicians see fit, through policies dealing with industrial support, climate change, and labor markets. One concern is regulating social media. From the Supreme Court’s scrutiny of Texas and Florida’s social media laws to Utah and other states unveiling social media rules for the digital world, parental rights and capitalism are at a pivotal moment. The policy choices we are making now on these issues will impact the brightest spot in the American economy. As economist Thomas Sowell correctly noted, there are no solutions, only trade-offs. This is a reason why it is crucial for Americans to grasp the trade-offs of social media regulation before politicians and bureaucrats take action. Utah’s ”Social Media Regulation Act” serves as a cautionary tale of government overreach with severe trade-offs. While the road to online safety is paved with good intentions, as we all want the best for minors (and everyone), we must evaluate policies by their real-world results. Utah’s law mandates minors under 18 must obtain a guardian’s permission to create social media accounts. If they proceed, the guardian gains full access to the minor’s account, with default curfew settings between 10:30 p.m. and 6:30 a.m. Additionally, minors cannot receive unapproved direct messages, and their accounts are blocked from appearing in search results. While there is mixed evidence suggesting a relationship between excessive social media usage and declining mental health, a recent study from Gallup reveals that parents have an even more prominent role than social media when it comes to well-being: “The strength of the relationship between an adolescent and their parent is much more closely related to their mental health than their social media habits. When teens report having a strong, loving relationship with their parents or caretakers, their level of social media use no longer predicts mental health problems.” Even if the mental health studies are correct, Utah’s law may not help teens most in need. Implementing government regulations always comes with a cost, and in this case, the very thing this policy intends to help could be harmed as a result. Parenting could be taken from parents and given to social media companies and government bureaucrats. Another trade-off looms: Will children growing up with restricted access to social media be disadvantaged compared to their counterparts in states and countries without such restrictions? Social media plays a key role, not just socially, but also professionally. The effect of limited exposure to these platforms remains uncertain. Beyond concerns about parental rights and career challenges, bills like these can seriously disrupt free markets and the prosperity we’ve seen them bring. Instead of restrictions, states and the federal government should focus on education. Indeed, many states are considering such digital literacy laws, following in Florida’s footsteps. On the free speech side of social media regulations, the bills in Texas and Florida aimed to prevent social media companies from selectively influencing digital expression. The Texas law was challenged in court and upheld; the Florida law was challenged and struck down. Now, these laws will be considered by the Supreme Court, and the outcome will have a big impact on the social media ecosystem. Although it’s frustrating for social media companies to potentially influence users by removing, promoting, or de-ranking specific content besides pornography, they are within their rights to do so. Content moderation practices, whether strict or open, bring a great opportunity for competition. For example, platforms like Rumble emerged in response to concerns that the big social media companies were unfairly moderating their content and attracting millions of users. This exemplifies the essence of free enterprise — problems inspire innovation, and competition drives improvement, allowing for diversification. But if social media companies in these states are compelled to adhere to the restrictive regulations, it will deter new startups and stifle growth. The social media landscape is evolving rapidly, and regulations like these demand careful consideration. While the safety of minors online is paramount, for our kids and yours, it’s crucial to strike a balance that preserves parental rights, encourages innovation, protects free speech, and safeguards individual freedoms. As we navigate this digital age, let’s remember that effective solutions should empower parents, consumers, and promote competition, not hinder progress with more government. These are the things that have provided the greatest human flourishing in free-market capitalism.  Originally posted at Pelican Institute where I co-wrote it with Jamie Tairov. The Pelican Institute has highlighted the need for better state budgeting and tax reform. This includes the Responsible Louisiana Budget (RLB), which was released earlier this year. The RLB shows that Louisiana’s budget has been growing at unsustainable levels, and that an improved growth factor for the expenditure limit and initial appropriations is needed. Recently, Americans for Tax Reform released a similar comparison for all 50 states, including Louisiana, in its Sustainable Budget Project. This report shows that, on the surface, Louisiana’s spending has not been as unsustainable as the RLB shows. Why is there a different outcome in the two reports?

Outcomes of Each Report The Responsible Budget model is currently being used successfully in other states to rein in spending. This is what Louisiana’s budget would have looked like had the RLB been employed over the last ten years.

Here are the findings from ATR’s Sustainable Budget study over the last decade:

Total spending in FY 22 was 34.4%, or $11.2 billion, higher than the improved expenditure limit. This means that a family of four is paying $8,800 more in taxes to pay for the excess spending, which is not sustainable spending.  Is One Report Better Than the Other?

No. Both reports are accurate and serve different purposes. The RLB uses initial appropriations which helps lawmakers easily compare appropriation amounts from year to year as they are drafting the budget during session. Because it covers spending instead of appropriations, the ATR study is a backwards-looking metric that can be used for making longer-term spending decisions, but it will be limited in its use during a legislative session. Both reports compare the current expenditure limit with a proposed improved expenditure limit. The current limit is the three-year average of personal income growth, which is an extremely volatile measure. The proposed improved limit is the three-year average of population growth plus inflation. The RLB and ATR reports can work together, providing limits on the front and back end to ensure that spending remains responsible throughout the year. Both reports show recent elevated appropriations and spending. There is clearly room for budgeting restraint in Louisiana. These measures have benefits to lawmakers and the public so that they can have the tools necessary to restrain government spending and provide a responsible budget. Doing so will have many payoffs over time, including making the comeback in the Pelican State happen more quickly by eliminating personal income taxes, providing a more dynamic economy, and improving opportunities for people to flourish. Episode 73 is with Dr. Gale Pooley, adjunct scholar at The Cato Institute, senior fellow at The Discovery Institute, and co-author of the new book, "Superabundance."

Gale and I discuss the following and more: 1) The state of abundance in America and how we compare to other countries; 2) How government interference through regulations and subsidies are restricting healthcare, education, and entrepreneurs; and 3) Why AI should be embraced, not feared, and money is not our most valuable economic asset. If you found today's discussion valuable, be sure to check out Gale's book: https://www.cato.org/books/superabundance Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. Also, subscribe and see show notes for this episode on Substack (www.vanceginn.substack.com) and visit my website for economic insights (www.vanceginn.com). Today, I cover the following:

Check out the short from the episode below if you want a quick recap before watching the full episode. Don’t miss episode 72 of the Let People Prosper show with guest Avik Roy, president of the Foundation for Research on Equal Opportunity (FREOPP).

We discuss America’s biggest economic problems and how to solve them. Avik and I discuss the following and more:

Check out the full show notes at my Substack newsletter and subscribe to get my posts directly in your inbox. To show my gratitude this Thanksgiving, I am offering a limited-time special giveaway to one lucky winner!

I hope you all had a wonderful holiday yesterday, and thank you for tuning in to today’s 36th episode of “This Week’s Economy.” This episode includes a special opportunity for one of you to win a complimentary year-long subscription to this newsletter, which is essential in light of my transitioning to a paid format soon. Click the link to enter the giveaway. |

Vance Ginn, Ph.D.

|

RSS Feed

RSS Feed

Proudly powered by Weebly