|

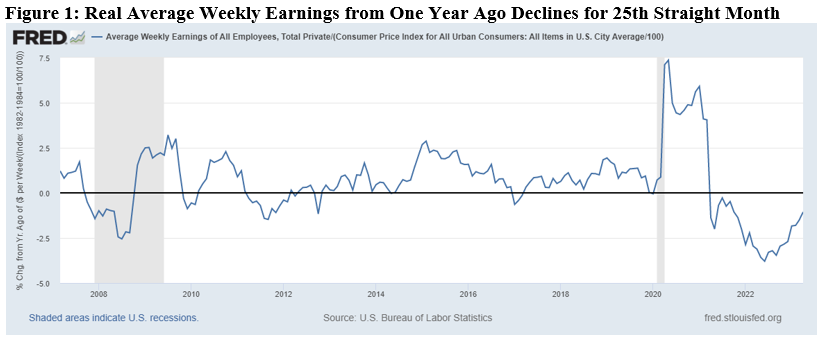

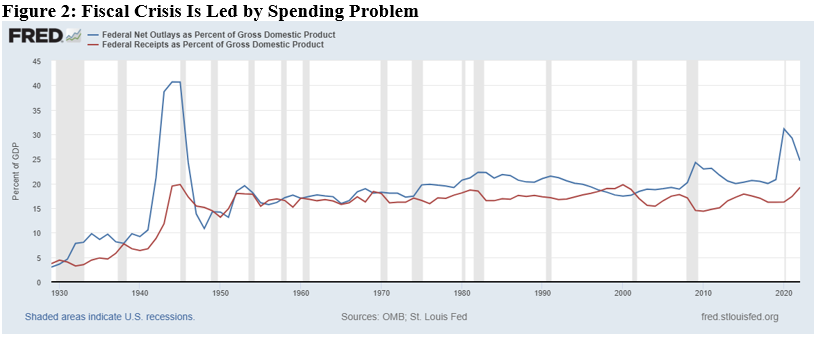

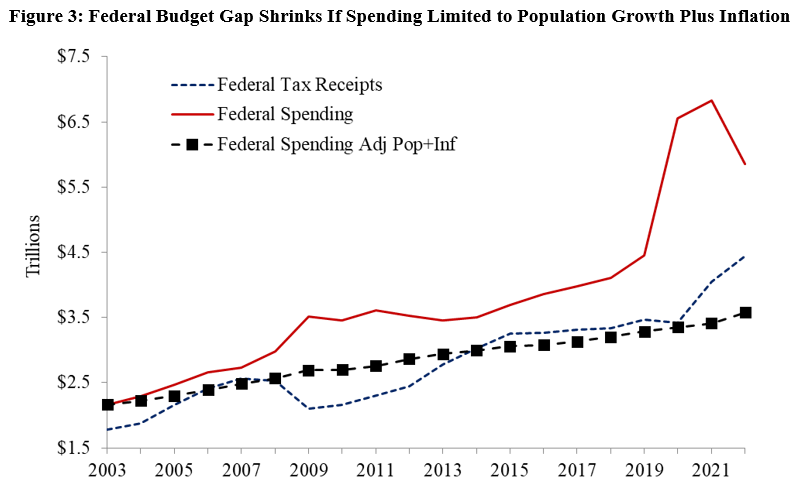

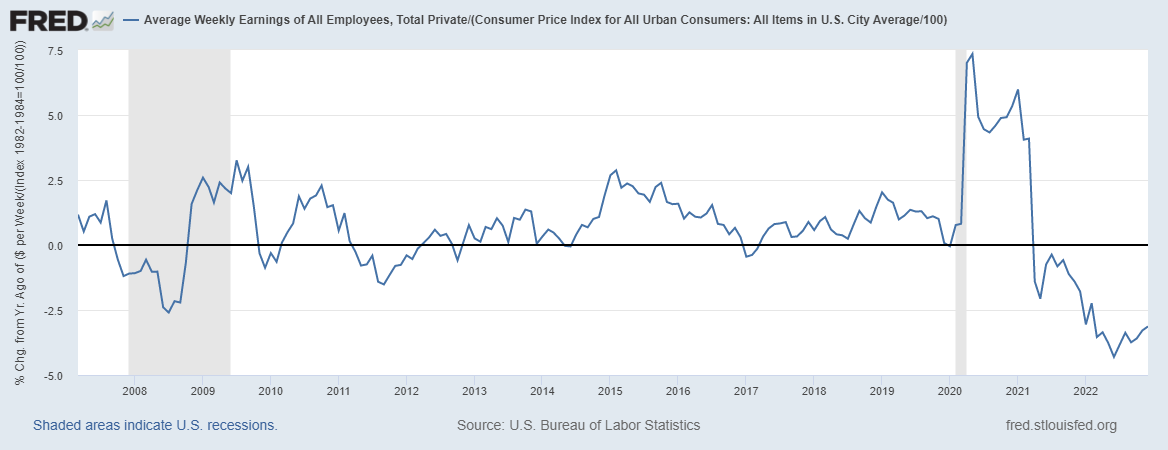

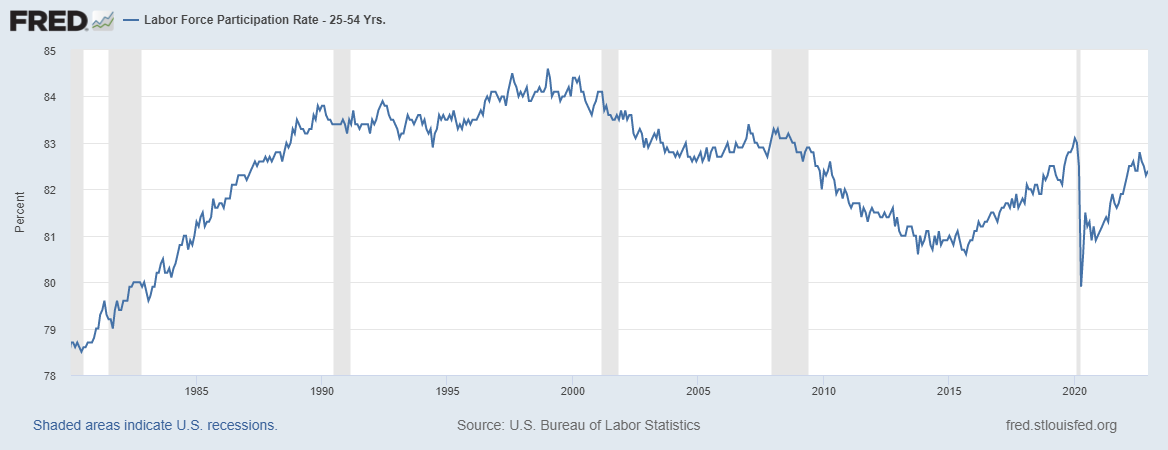

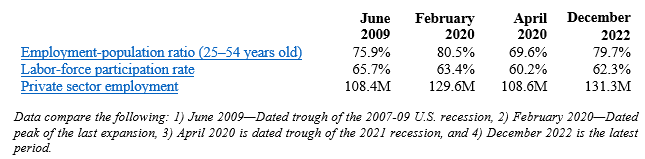

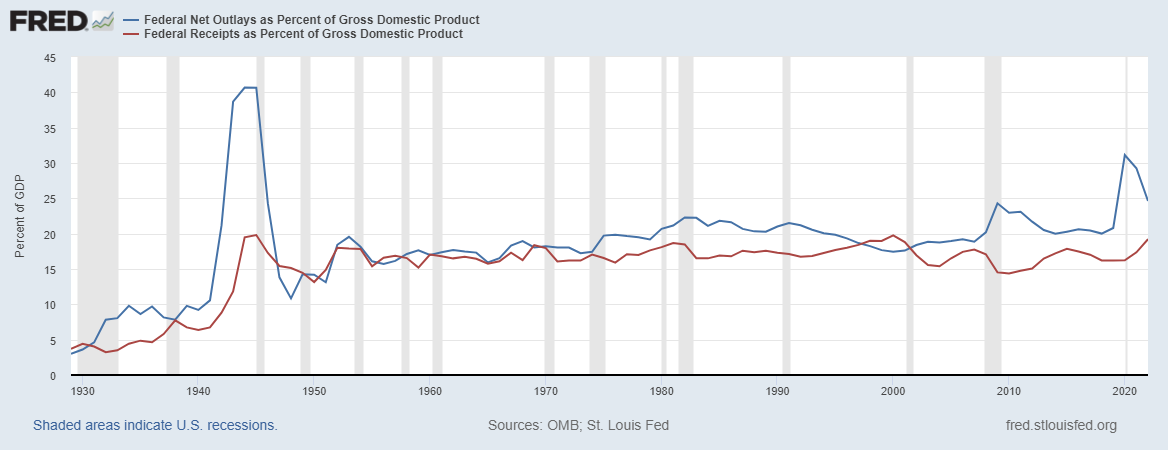

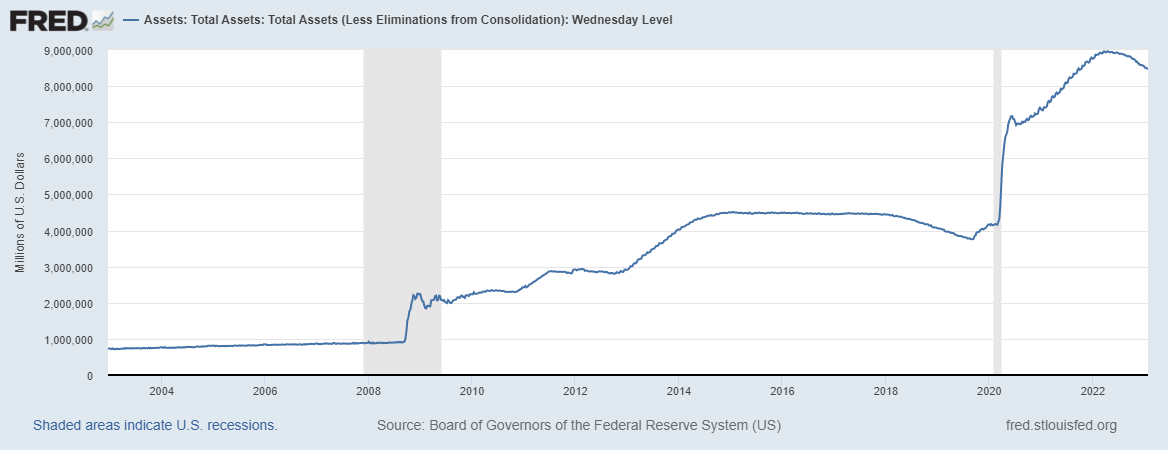

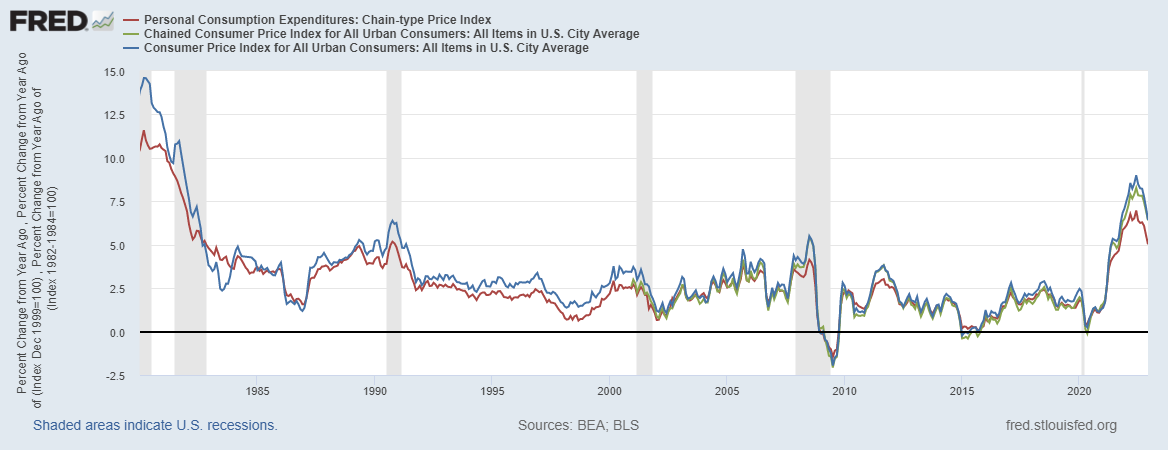

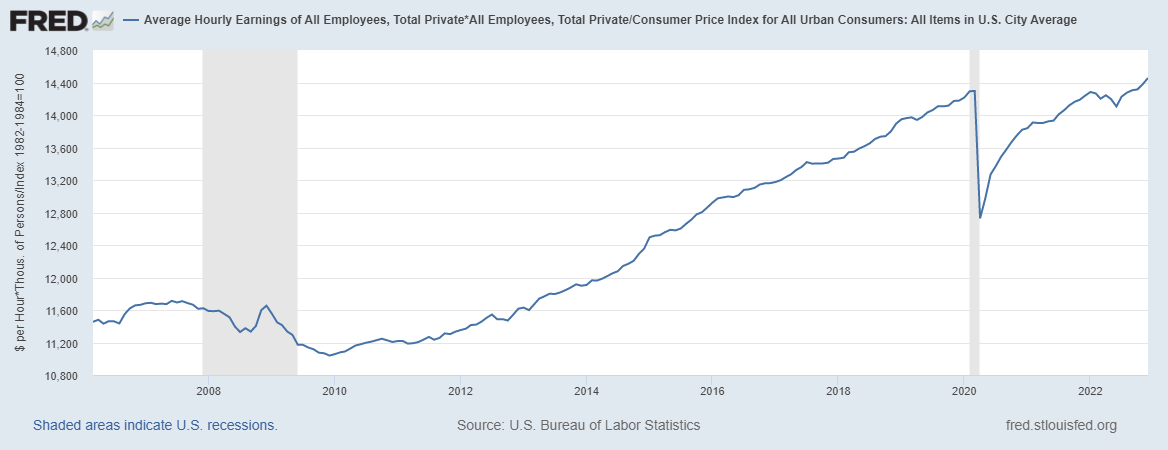

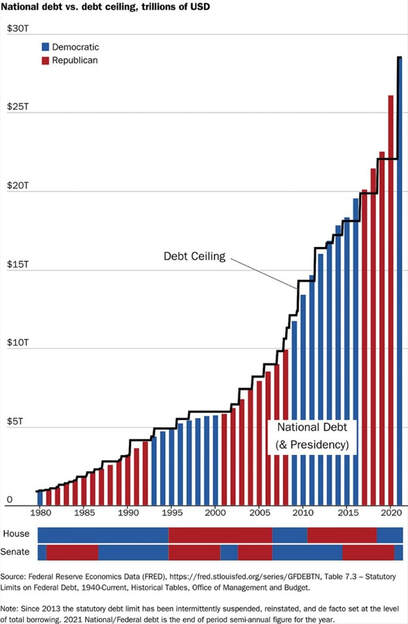

Key Point: The best way to let people prosper is free-market capitalism. Unfortunately, government has created a situation where inflation-adjusted average weekly earnings are down year-over-year for 25 straight months and economic growth is anemic.  Overview: Government failures drove the “shutdown recession” and stagflationary period over the last three years that has plagued Americans, with more banking problems to come. This is fueled by the debt ceiling fight and elevated inflation that has also rocked the U.S. dollar. The answer are pro-growth policies of less spending by Congress, less regulation by the Biden administration, and less money printing by the Fed. Labor Market: The Bureau of Labor Statistic recently released its U.S. jobs report for April 2023, which was another mixed report with some strengths but many weaknesses. The establishment survey is the most reported shows there were +253,000 (+2.6%) net nonfarm jobs added in April to 155.7 million employees, which has increased by +4.0 million over the last year but just +3.3 million since February 2020. However, there were cumulative revisions in the prior two months of 149,000, so on net for that reduced the net increase to just +104,000 jobs indicating a weakening labor market. Over the last month, there were +230,000 jobs (+2.7%) added in the private sector and +23,000 jobs (+2.1%) added in the government sector. Most of the private sector jobs were added in the sectors of private education and health services (+77,000), professional and business services (+43,000), and leisure and hospitality (+31,000), which these three also led over the last 12 months. But wholesale trade lost -2,200 jobs last month while no industry had job losses over the last year. The household survey increased by +139,000 jobs to 161.0 million employed in April. There have been declines in net employment in four of the last 13 months for a total increase of +3 million since April 2022 and +2.3 million since February 2020, which both are 1 million below the jobs reported in the establishment survey. This could be because of reporting issues or the number of jobs each person has in the market. The official U3 unemployment rate ticked down to 3.4% and the broader U6 underutilization rate fell to 6.6%, which both are near or at historic lows. Since February 2020, the prime-age (25-54 years old) employment-population ratio is up by 0.3pp to 80.8%, prime-age labor force participation rate was 0.3-percentage point higher at 83.3%, and the total labor-force participation rate was 0.7-percentage-point lower at 62.6% with millions of people out of the labor force holding the U3 rate artificially low. Given some improvements, challenges remain for Americans as inflation-adjusted average weekly earnings were down (-1.1%) over the last year for the 25th straight month. Economic Growth: The U.S. Bureau of Economic Analysis’ recently released the 1st estimate for economic output for Q1:2023. Table 1 provides data over time for real total gross domestic product (GDP), measured in chained 2012 dollars, and real private GDP, which excludes government consumption expenditures and gross investment. Most of the estimates for Q4:2022 and growth in 2022 have been revised lower, providing more evidence that 2022 was a very weak economy if not a recession.  Economic activity has had booms and busts since the government-imposed COVID-related restrictions in response to the pandemic and poor fiscal and monetary policies that severely hurt people’s ability to exchange and work. In 2022, the first two quarters had declines in real total (and private) GDP, providing a reason to date recessions every time since at least 1950. While the second half of 2022 looked better, those two quarters were influenced by net exports and inventories that would have made the economy much weaker. For 2022, real total GDP growth is reported +2.1% year-over-year but measured by Q4-over-Q4 the growth rate was only +0.9%, which was the slowest Q4-over-Q4 growth during a recover on record. Then the anemic growth of just +1.1% in Q1:2023 provides more reason that this is an extended recession or at least stagflation. The Atlanta Fed’s early GDPNow projection on May 8, 2023 for real total GDP growth in Q2:2023 was +2.7% based on the latest data available, but this rate has been lowered in recent quarters. Considering the last expansion from June 2009 to February 2020, there was slower real private GDP growth in the latter part of that period due to higher deficit-spending, contributing to crowding-out of the productive private sector. Congress’ excessive spending since February 2020 led to a massive increase in the national debt by nearly +$7.6 trillion that would have led to higher market interest rates. This is yet another example of how there is always an excessive government spending problem as noted in Figure 2 with federal spending and tax receipts as a share of GDP no matter if there are higher or lower tax rates.  But the Fed monetized much of the new debt to keep interest rates artificially lower thereby creating higher inflation as there has been too much money chasing too few goods and services as production has been overregulated and overtaxed and workers have been given too many handouts. The Fed’s balance sheet exploded from about $4 trillion, when it was already bloated after the Great Recession, to nearly $9 trillion and is down only about 5.2% to $8.5 trillion since the record high in April 2022 after rising nearly $400 billion in March 2023 then down $200 billion since then. The Fed will need to cut its balance sheet (total assets over time) more aggressively if it is to stop manipulating markets (see this for types of assets on its balance sheet) and persistently tame inflation, as we may need deflation which hasn’t happened since 2009 given the rampant inflation over the last two years. The current annual inflation rate of the consumer price index (CPI) has been cooling since a peak of +9.1% in June 2022 but remains elevated at +4.9% in April 2023, which remains the highest since 2008 as do other key measures of inflation. After adjusting total earnings in the private sector for CPI inflation, real total earnings are up by only +2.6% since February 2020 as the shutdown recession took a huge hit on total earnings and then higher inflation hindered increased purchasing power. Just as inflation is always and everywhere a monetary phenomenon, deficits and taxes are always and everywhere a spending problem. David Boaz at Cato Institute notes how this problem is from both Republicans and Democrats. In order to get control of this fiscal crisis which is contributing to a monetary crisis, the U.S. needs a fiscal rule like the Responsible American Budget (RAB) with a maximum spending limit based on the rate of population growth plus inflation. If Congress had followed this approach from 2003 to 2022, the figure below shows tax receipts, spending, and spending adjusted for only population growth plus chained-CPI inflation. Instead of an (updated) $19.0 trillion national debt increase, there could have been only a $500 billion debt increase for a $18.5 trillion swing in a positive direction that would have substantially reduced the cost of this debt to Americans. The Republican Study Committee recently noted the strength of this type of fiscal rule in its FY 2023 “Blueprint to Save America.” And to top this off, the Federal Reserve should follow a monetary rule so that the costly discretion stops creating booms and busts.  Bottom Line: Stagflation will continue with the a deeper recession this year given the “zombie economy” and the unraveling of the banking sector which will hit main street hard. Instead of passing massive spending bills, the path forward should include pro-growth policies that shrink government rather than big-government, progressive policies. It’s time for limited government with sound fiscal and monetary policy that provides more opportunities for people to work and have more paths out of poverty. There is some optimism with the House Republicans debt ceiling bill package, but it’s got an uphill battle to become law with Democrats in the Senate and White House so more must be done.

Recommendations:

0 Comments

In our system of federalism, competition matters among the states. This reality has been on full display the past few years as people fled big-government states like California and New York to more limited government states like Texas and Florida. But what works best?

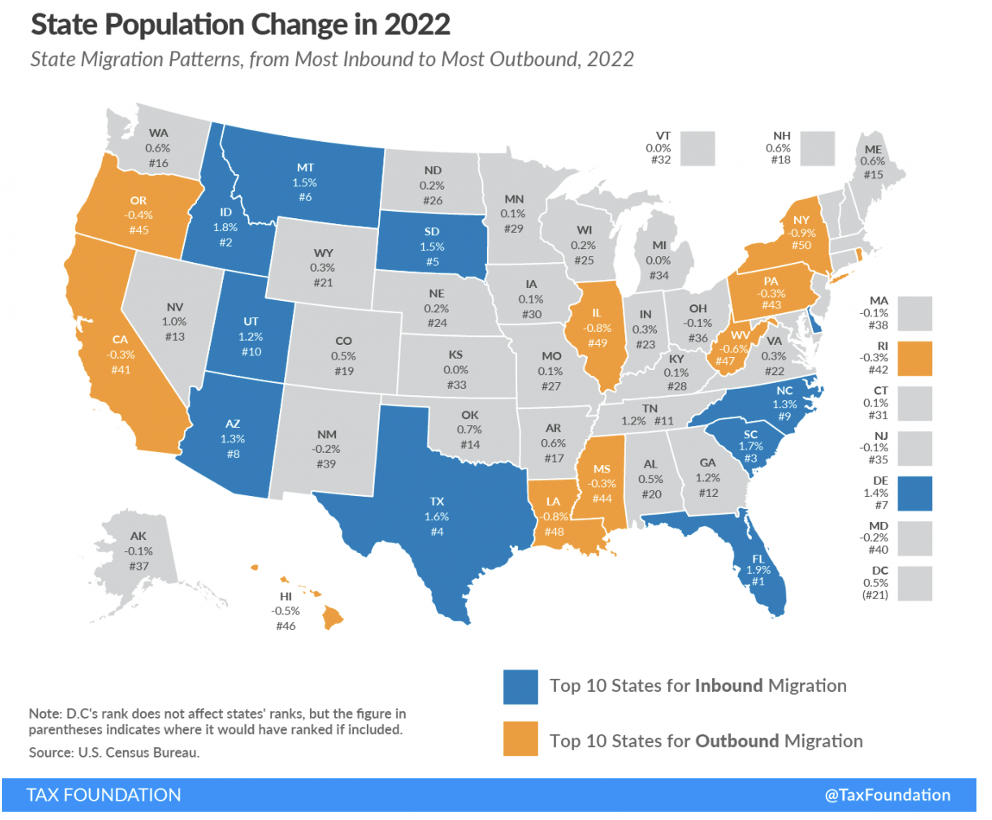

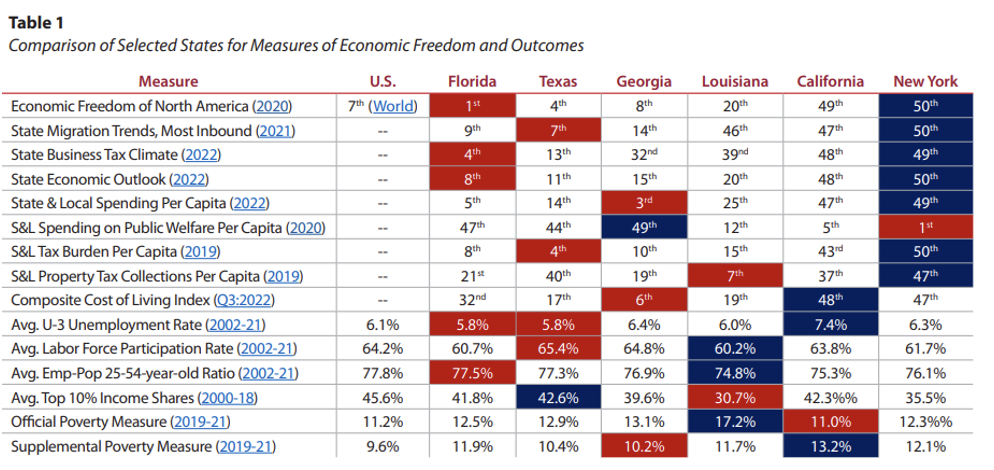

The American Legislative Exchange Council’s (ALEC) “Rich States, Poor States” report is a recent comparison of states. Utah, a politically red state, ranks second best in economic performance and first in economic outlook for 2023. Texas, the largest red state, ranks seventh in performance and 13th in outlook. On the surface, this looks pretty straightforward, but a closer look shows that Texas is a leader but needs much improvement. The report measures performance based on the growth of state gross domestic product, absolute domestic migration, and non-farm payroll from 2011 to 2021. The economic outlook is based on 15 state policy variables, including tax burden, debt and other factors. Utah beats Texas for state GDP and nonfarm payroll growth rates, while Texas wins for absolute domestic migration. This is thanks to people leaving states like California and New York, which rank 45th and 50th, respectively, in outlook, and coming to Texas in search of more economic freedom. Should Utah be a model for Texas? Not necessarily. Note that Utah’s population is about 3.4 million. Texas has more than 30 million people or nearly nine times more people than Utah. Utah is also less diverse, with 77.2% of its population being white, 14.8% Hispanic, and 1.5% black, compared with Texas’ population being 40.3% white, 40.2% Hispanic, and 13.2% Black. Texas also has twice the share of foreign-born residents, with 17.0%, whereas Utah has just 8.5%. Utah has a much lower poverty rate at 8.6% compared with 14.2% in Texas. Clearly, there are significant differences between these two red states. And what works well in Utah likely may not fit well in Texas, given their substantially different demographics and economies. While the ALEC report is insightful, a cursory glance at the two ranks is just that. Considering all the metrics it provides along with state population and diversity, there’s a more holistic picture of which states are thriving. A more reasonable comparison for Texas based on economic and population sizes and diversity is the second largest red state of Florida. Florida has a population of about 22 million, with 52.7% white, 26.8% Hispanic, and 17.0% Black, while 21.0% is foreign-born, and the poverty rate is 13.1%. According to ALEC’s report, Florida ranks first for performance, better than Utah and Texas, and 9th for outlook, better than Texas. Texas and Florida boast business-friendly policy climates, typically spend responsibly, have no state income tax, and are right-to-work states. And the performances of their economies are robust based on multiple indicators. But two of the biggest factors that put Florida above Texas are the same ones that help put Utah above Texas now and for the foreseeable future: lower property tax burden and universal school choice. According to the Tax Foundation, individuals have the 6th highest property tax burden in Texas, 26th in Florida, and 43rd in Utah. Texas’ outrageous property taxes, which are high in large part due to too much local spending, is causing an affordability crisis as home and property values have risen faster than wages for too long. If businesses perceive the cost of doing business as too high due to high property taxes, they may choose to locate elsewhere, which results in less investment, economic growth, and job creation. This is why Texas should spend responsibly and use the at least $33 billion surplus to compress the school district maintenance and operations property taxes that are essentially controlled by the state’s school finance formulas. Combine this with spending restraint at the state and local levels and Texas could put property taxes on a path to elimination within a decade so that Texans can finally fulfill their right to own property while ending a bad wealth tax. Finally, when it comes to school choice, Utah and Florida joined the universal school choice revolution this year, while Texas is still fighting for it. Universal school choice is critical for improved state economies as it’s linked to improved student outcomes and increased teacher pay, both essential to becoming more competitive and producing a population with less criminal activity and higher economic earnings, to name just a few benefits. In short, competition matters! While it’s misleading to declare that Utah or Florida economically outperform Texas overall based on the differences outlined here, they do put pressure on Texas to improve or risk falling behind. Decreased property taxes and universal school choice mean more freedom, which empowers people to prosper. Time is running out this session so the Texas Legislature must act promptly. Originally published at The Center Square.  With weeks left in the Texas Legislature’s 88th regular session, state lawmakers are working to enact the largest tax cut in the history of the nation’s second most populous state. In addition to billions of dollars worth of property tax relief, state legislators are moving to enact a number of innovative reforms before adjourning. Texas should unite to push these measures across the finish line.

Gov. Greg Abbott and leadership in the Texas House and Senate all want to pass a massive property tax relief bill but differ over the best approach. The Senate would like to raise the homestead exemption. The House, however, would rather cut the appraisal cap in half, taking it from 10% to 5%, and put more money toward rate compression than is called for by the Senate plan. Disagreements over these key details threaten to squelch planned relief. Lawmakers should work out a deal before the session ends. “Texas has a historic opportunity to provide much-needed property tax relief with nearly $33 billion in surplus for the current biennium plus extra taxpayer money available in the upcoming biennium, which should be returned to taxpayers,” noted Texas-based economist Vance Ginn, a senior fellow at Americans for Tax Reform. In addition to reducing property tax payments in a state that is home to the nation’s sixth highest average property tax burden, Texas lawmakers are also taking action to reduce regulatory costs. The House passed House Bill 2127 by a 92-55 vote on April 19. HB 2127, introduced by Rep. Dustin Burrows, R-Lubbock, and Sen. Brandon Creighton, R-Conroe, prohibits local governments from regulating products, activities, or industries in a manner that exceeds or conflicts with state law. Proponents of HB 2127, such as the National Federation of Independent Business, which represents small businesses, say it will rectify the patchwork of regulations that currently exist in Texas, which is making it more difficult for a business to operate and create jobs. “There are dozens of reasons why Texas is the best state in the country for business, but its convoluted, unpredictable, and inconsistent patchwork regulatory system is not one of them,” said James Quintero, policy director at the Texas Public Policy Foundation. Quintero says HB 2127 “brings some much-needed common sense to the system, unifying the rules for conducting business in a predictable, reliable, and efficient way to promote compliance.” Lastly, Texas lawmakers have the opportunity to make Texas the first state to ban taxpayer-funded lobbying by enacting Senate Bill 175. SB 175, introduced by Sen. Mayes Middleton, R-Galveston, would bar local governments and other political subdivisions from using taxpayer funds to hire contract lobbyists. Supporters of SB 175 note that contract lobbyists hired with taxpayer dollars frequently work against the interests of taxpayers. In previous sessions, for example, taxpayer-funded lobbyists have worked to kill property tax relief and block reforms that would have government spending grow at a more sustainable clip. This resistance to conservative priorities continues to this day, with taxpayer dollars currently being spent to lobby against Education Savings Accounts. That is why many view SB 175 as a root reform that will beget many other pro-growth reforms. Proponents of SB 175 believe it will help facilitate the future passage of tax relief, ESAs, greater spending restraint, and other pro-taxpayer reforms. As we saw with the criminal justice reform movement that started in Texas and has since swept the nation, enactment of a given reform in Texas makes it easier to pass that same proposal in other states. That’s because lawmakers in many state capitals look to Texas as a model for sound governance. As such, while passage of the aforementioned reforms would benefit Texans, their enactment will also have a positive effect nationally. Hopefully Texas lawmakers can capitalize on these opportunities before them in the remaining weeks of session and send these groundbreaking reforms to the desk of Abbott, who has made clear he wants to sign them. Grover Norquist is president of Americans for Tax Reform. He wrote this for The Dallas Morning News. Originally published at Dallas Morning News.  ATR Senior Fellow Vance Ginn provided remarks at the Tax Day press conference at the House Triangle. Video of Ginn’s remarks can be viewed here. Ginn said: “It is often said that we don’t have a revenue problem, we have a spending problem. And that’s true. But also here on Tax Day, we have a tax problem. What we really need is for free market capitalism, which is the best path to let people prosper, to be able to flourish again. For people to get jobs and higher wages so they could pay for the higher inflation that’s come out of the Biden administration. And it’s just one thing after another. The latest account of this was the Inflation Reduction Act which does no such thing. It continues to raise inflation, raises the debt, and the latest estimates on this show that it will be about four times higher than what the CBO reported just last year. And a lot of this has to do with the tax credits for electric vehicle batteries, which are going to cost nearly $200 billion plus over time. This is another way that they’re infiltrating the overall size of the government through our economy throughout our lives. And fortunately, we have another way that we should go, that’s led by a lot of states that are leading the sustainable state budgets across the nation, that they should look at by spending less, and finding ways to provide tax relief and regulatory reform.“ Originally published Americans for Tax Reform.  Louisiana doesn’t exist in a vacuum, and neither does opportunity. When it comes to the harsh reality of attracting entrepreneurs, creating new jobs and keeping our kids and grandkids home, Louisiana must reckon with the reality that we’re competing against other states in a national — and global — race for a brighter future.

That’s why Louisiana’s economic environment matters, and why eliminating the state’s income tax is so critical — no matter how difficult it might be — before more employers and families flee our state. Naysayers try to shoot down reforms with scare tactics, as if it’s a zero-sum game in which tax cuts and a strong state can’t coexist. That’s why taking a holistic view of the state’s tax and budget policies is necessary. Eliminating the state’s income tax doesn’t have to mean massive cuts or a big tax swap. The Pelican Institute has proposed a plan to flatten personal income taxes, phase them out using extra taxpayer dollars collected above a stronger spending limit and budget responsibly to meet the needs of the state. When we’re talking about taxes, don’t forget whose money it is. Those are hard-earned dollars that belong to Louisianans, and taxes leave them with less money in their pocket for putting food on the table, gas in their tanks and capital for starting a business. Is it any wonder that so many Louisianans leave for states where they can keep more of their money? When families gather around their kitchen table or businesses look at their balance sheets, take-home pay makes a difference. That’s why Louisiana should phase out income taxes as soon as possible. This is fundamental to ensuring that Louisiana can compete with our neighbors, attract and retain talent and become an economic powerhouse. This is the comeback story we can write together. Originally published at The Advocate. Research: The Inflation Reduction Act's Costly New Tax Credits for Electric Vehicle Batteries4/10/2023  Executive Summary The U.S. Congress passed and President Biden signed into law the so-called “Inflation Reduction Act” (IRA) in August 2022. The IRA includes many provisions which are now estimated to cost $1.2 trillion over a decade per Goldman Sachs’ more recent analysis compared with the Congressional Budget Office’s (CBO) initial estimate of $391 billion. Part of this substantially higher estimated cost is because of the new cost estimates for tax credits for electric vehicle (EV) battery cells and modules manufactured in the U.S. Instead of the initially estimated cost of $30.6 billion by the CBO, new estimates based on more precise projections and growth in the EV market indicate that this could be as high as $196.5 billion (540% higher than initially estimated) per the Mercatus Center and Goldman Sachs. This higher estimate appears more accurate than the original CBO estimate given the large increase in the EV market and the expanding use of these tax credits. Given that the cost of these subsidies passed by Congress and communicated to the public appears to be substantially undervalued, the CBO and other nonpartisan agencies and committees responsible for providing Congress with accurate revenue estimates and sound economic analysis should reexamine their calculations. Originally published at Americans for Tax Reform.  With a debt ceiling fight and bank failures, Congress’ day of reckoning to spend less is now.

Inflation is sky-high, purchasing power is sinking, 60% of Americans live paycheck to paycheck, and credit card debt is soaring to nearly $1 trillion. To make matters worse, between the fourth quarter of 2021 to the fourth quarter of 2022, U.S. real GDP grew by just 0.9%, the slowest growth in a “recovery” since at least 2009 amid the Great Recession. The more the federal budget deficit grows because of excessive government spending, the more the budget is crowded out from funding legislative priorities. In turn, Congress is forced to find ways to pay for interest on the debt, which will soon exceed $1 trillion. It’s not just the budget that’s getting crowded out; productive activity in the private sector fueled by entrepreneurs is stifled due to too much money chasing too few goods and services at the hands of tyranny imposed by big government. The underlying culprits to these economic catastrophes are reckless, weaponized government spending, often funding tyranny against Americans, and the Federal Reserve holding a bloated balance sheet. This excess national debt and money printing contributed to the latest closure of Silicon Valley Bank and will have further consequences. These government failures should be addressed by Congress spending less. This should include reducing federal funds sent to states. Not only do federal funds diminish federalism by making states dependent on the federal government but it also comes with massive red tape. The U.S. system of federalism provides a unique laboratory of competition to see what works across the states. This is best observed and encouraged by letting states be as independent as possible. Considering that federal deficits are expected to increase by an average of $2 trillion annually over the next decade, states would be wise to prepare for fewer federal funds as Congress’ purse strings will tighten. According to Congressman Chip Roy (R-TX) in a recent interview, another major way the government drives up spending is by hiding behind so-called mandatory expenditures such as Medicare and Social Security, and discretionary spending, which is funding tyranny through the weaponization of bureaucrats. “We have to commit to not funding tyranny such as the IRS going after minorities and poor people,” said Congressman Roy. “Why should we fund the FBI labeling Scott Smith, a man who stood up for his daughter being sexually assaulted to her school board, a domestic terrorist? Likewise, military funding should go toward making us a strong defense, not to ensuring that recruits ‘stay woke’ and never say ‘sir’ or ‘ma’am.’” While it’s politically popular for the government to honor its commitments like Social Security and Medicare for current retirees, mandatory spending is excessive and needs reforms to remain solvent over time. Cutting non-defense discretionary spending–including abolishing Departments of Education and Energy–to pre-Covid levels, would mean saving $3 trillion over the next decade. But both Republicans and Democrats have to work at this as they’re equally culpable of driving up spending under many administrations. And these expenditure savings need to be closer to $8 trillion to stabilize the debt to output level per the Committee for a Responsible Federal Budget. In addition to tightening up federal funds sent to states and mandatory expenses, the government should consider adopting a Responsible American Budget, similar to what’s been practiced in Texas, Florida, and Tennessee, that’s helping their economies thrive. This would require adopting some sort of fiscal rule like a spending cap, but as Congressman Roy emphasized, without passing exceptions that would render the rule irrelevant. If such a rule based on the maximum growth rate of population growth plus inflation, which represents what the average taxpayer can afford, had been in place, then we would have accrued $500 billion in new debt rather than $19 trillion over the last 20 years. Returning the federal government to its constitutional role of preserving liberty is key to economic growth. The surest way to suffocate the productive private sector from innovating and Americans from prospering is to let spending increases continue. This is the biggest threat to the American dream today, which younger generations are already counting dead as they’ve seen such poor economic growth in their lifetimes. If the future of the nation and opportunities for upcoming generations is important, the government must earn Americans’ trust by spending less, reforming mandatory programs, cutting federal bureaucracy, and promoting other pro-growth policies. As Congressman Roy shared, “I didn’t inherit a free country to pass down an unfree one. We have to fight.” Originally posted at The Daily Caller. On today's episode of the "Let People Prosper" show, which was recorded on March 6, 2023, I'm honored to be joined by Dr. Arthur Laffer, legendary economist and 2019 recipient of the Presidential Medal of Freedom. We discuss:

Dr. Arthur Laffer’s bio and other info (here):

Iowa’s fiscal foundation remains strong despite national economic uncertainty because of the state’s fiscal conservatism and prudent budgeting.

Governor Kim Reynolds has made Iowa a leader in conservative fiscal policy. This approach has already left more money in taxpayers’ pockets, and set the state on course to implement a low, flat income tax by 2026. In its Fiscal Policy Report Card on America’s Governors for 2022, the Cato Institute “grades governors on their fiscal policies from a limited-government perspective.” On this basis, Cato ranked Governor Reynolds as the best in the nation, writing that she “has been a lean budgeter and dedicated tax reformer since entering into office in 2017.” Last year, Governor Reynolds and the Iowa legislature continued to place a priority on prudent budgeting. The $8.2 billion budget for fiscal year 2023 represented a mere 1 percent increase from the prior year. And for FY 2024, Reynolds has proposed an $8.5 billion budget, with the extra funds meant to cover the universal school-choice plan that the legislature recently passed. Iowa’s anticipated $1.6 billion budget surplus for FY 2023 is nearly as much as the $1.9 billion surplus recorded in FY22, with another $2.2 billion surplus expected in FY 2024. The state should have $895.2 million in reserve funds in FY 2023 and $962.5 million in FY 2024 — the statutory maximum for those years. The state’s Taxpayer Relief Fund — the fund into which excess tax revenue is placed so that it can be returned to taxpayers by the legislature — was worth $1.1 billion in FY 2022, and is on track to grow to $2.7 billion in FY 2023 and then to $3.4 billion in FY 2024. In 2022, Iowa also enacted the most comprehensive income-tax-reform package in the nation. Over four years, the nine-bracket income tax will transform into a flat income tax with a 3.9 percent rate. The corporate tax has also already been reduced from 9.8 percent to 8.4 percent, and is set to gradually shrink until it reaches a flat 5.5 percent rate. These measures constitute a sound, pro-growth tax policy that will create incentives to work, save, and invest, and will make Iowa’s economy more competitive on the national stage. Prudent budgeting is essential for ensuring that these income-tax cuts can be responsibly implemented. And on Governor Reynolds’ watch, Iowa’s tax revenues continue to grow, reducing the degree to which the tax cuts must be “paid for” through spending cuts. The most recent numbers, released in February, showed that revenues are at $35.9 million, or 5.7 percent higher than they were at the same time last fiscal year. That said, in addition to proposing a fiscally prudent FY 2024 budget, Governor Reynolds is also proposing to rein in Iowa’s administrative state. It has been 40 years since Iowa made any major reforms to state government, and in that time the size and scope of government have increased. Reynolds is proposing to streamline the executive branch and reverse some of that growth. Currently, Iowa has 37 cabinet agencies. The governor’s proposal calls for a 16-agency cabinet. She argues that government is both too big and too expensive, and streamlining it will result in more efficiency and better services for taxpayers. She estimates that if enacted, this consolidation plan would save taxpayers over $214 million in the next four years. Although Governor Reynolds and the legislature have placed a priority on prudent budgeting, there is more that could be done. Iowa statute currently allows legislators to spend up to 99 percent of projected tax revenues. This rule should be replaced with one that would limit most spending to the rate of population growth plus inflation, which could have saved Iowans as much as $2.9 billion — or $3,700 for the average family of four — in taxes had it been in place since 2013. Meanwhile, Governor Reynolds has already signaled that she does not want to stop at a flat income-tax rate of 3.9 percent. She has said she aims to lower the rate to a flat 2 percent, and to eventually eliminate the tax altogether while continuing to cut state-government spending. Governor Reynolds should be applauded for putting Iowa on the path to a robust economy, and providing a model of sound fiscal policy for the federal government and other states to emulate. Now, she just has to keep at it, because there is more work still to be done. Originally published at National Review Online.  Recent data from the Tax Foundation reveals that Louisiana has the highest average combined state and local sales tax rate of all the states. The bulk of this burden comes from its local taxes, the second highest in the nation.  Pair these findings with Louisiana’s progressive income taxes of a graduated personal income tax rate of up to 4.25% and a corporate income tax rate max of 7.50%, and there’s no wonder why the Pelican State has a net out-migration problem. According to the Tax Foundation’s business tax climate index, the state ranks 12th worst in the country.  Personal income taxes disincentivize work, and sales taxes can lead consumers to shop elsewhere and businesses to relocate. Employers and consumers want to be where they can keep more of what they earn, which helps explain why Florida, a state with no personal income taxes and a combined sales and local tax rate that’s more than 2.5-percentage points lower than Louisiana’s, had the highest net in-migration last year.  Clearly, Louisiana’s tax code needs an overhaul if the growth and flourishing of Louisianans are priorities. But so does the state’s spending. To start, the Pelican State could consider joining the 14 states in the flat-income tax revolution. As more states flatten or remove their personal income taxes, Louisiana’s costly progressive income taxes will become much less appealing. Moving to flat personal and corporate income taxes would be a pro-growth step forward toward the eventual greater goal of eliminating these costly taxes, helping to compete with places like Florida and Texas, both of which don’t have personal income or corporate income taxes. Considering that the ultimate burden of government is how much it spends, reforming the tax code is just one piece of the puzzle. The excessive government spending at the state and local levels, compared with reasonable metrics like the rate of population growth plus inflation which helps measure the average taxpayer’s ability to pay for government spending, burdens Louisianans. Furthermore, Louisiana’s state and local debt is estimated to be about $7,600 per person owed by 2027, plus another nearly $28,000 per person owed in unfunded liabilities over time, so there are clearly massive barriers in the way for Louisianans to flourish. This is an issue because heavy spending leads to heavy burdens on state residents and decreased economic freedom, which Louisiana can’t afford to lose more of, considering how far it falls behind other states.  Not surprisingly, Georgia, Florida, and Texas all boast lower spending than Louisiana, with improved economic freedom and poverty rates. Meanwhile, Louisiana has the highest official poverty rate in the country. The rankings for the Pelican State aren’t quite as bad as the highly progressive states of New York and California, which are hemorrhaging population to other states. Incentives matter, so people are voting with their feet to flee high cost, low freedom states.

Louisiana should start its comeback story by adopting a stronger spending limit, similar to the one recently passed in Texas. Spending caps help governments stay limited, which is imperative for states to thrive as it forces them to narrow their scope. In turn, the private sector has more elbow room to grow and people have greater ability to prosper. This would also help provide more surplus funds to put toward cutting, flattening, and eventually eliminating personal and corporate income taxes. Louisiana has too great of a culture and too much potential for it to be squandered by burdensome spending and taxes. It’s time for serious spending restraint and major tax reforms to provide the best path forward. Originally published at Pelican Institute.  By Victor Skinner | The Center Square contributor | Feb 16, 2023

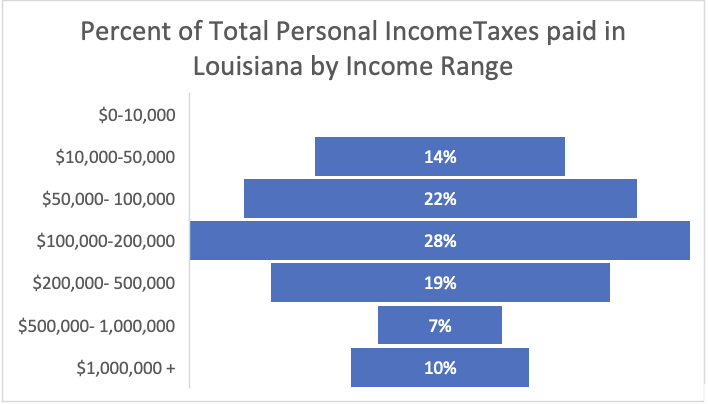

(The Center Square) – Louisiana’s combined state and local sales taxes are the highest in the nation, a reality critics contend is one of several tax and spending issues plaguing the state. The Tax Foundation released a report last week that compares state and local sales taxes across the nation, ranking states based on both the state sales tax and combined state and local rates. The research shows that as of Jan. 1, Louisiana’s state sales tax of 4.45% ranks 38th from the top. But when that figure is added to the average local tax rate of 5.10%, the state’s 9.55% combined rate becomes the highest among 50 states and the District of Columbia. "Sales taxes are just one part of an overall tax structure and should be considered in context," according to the report. "For example, Tennessee has high sales taxes but no income tax, whereas Oregon has no sales tax but high income taxes. While many factors influence business location and investment decisions, sales taxes are something within policymakers’ control that can have immediate impacts." The report comes as Louisiana lawmakers are studying potential changes to the state’s tax structure ahead of the 2023 legislative session. Vance Ginn, chief economist for the Pelican Institute, contends that excessive government spending is one factor driving higher taxes in Louisiana, though he believes personal income taxes are having the biggest impact on the state’s economy. "We have got to find a way to restrain excessive government spending at the state and local level," he said. "The sales tax is high in Louisiana … but really the focus should be on the burdensome income tax." The Pelican Institute is advocating for a flat income tax that eventually phases to zero. "That will allow for more job creation and economic growth," Ginn said. The Tax Foundation ranks Louisiana 25th nationally for income taxes, 32nd in the nation for corporate income tax, and 23rd for property taxes. Those rankings, combined with other measures, puts the state in 39th place overall in the foundation’s 2023 State Business Tax Climate Index. The foundation’s most recent report notes that sales tax rates can have a significant impact on where residents make major purchases and where businesses locate, and it cites examples of states that have increased per capita sales by maintaining rates lower than their neighbors. The analysis shows Louisiana’s 9.55% combined sales tax rate is more than 2% higher than Mississippi’s 7.07% rate, and 1.35% higher than Texas at 8.20%. Arkansas’ combined rate of 9.46% is the third highest nationally, behind Louisiana and Tennessee at 9.55%. California has the highest state sales tax rate at 7.25%, followed by four states tied for the second-highest rate, at 7%: Indiana, Mississippi, Rhode Island, and Tennessee. Five states do not have a state sales tax: Alaska, Delaware, Montana, New Hampshire and Oregon. The lowest rates for states with sales tax include Colorado at 2.9%, followed by Alabama, Georgia, Hawaii, New York and Wyoming, all at 4%. States with the highest average local sales tax rates include Alabama at 5.25%, Louisiana, Colorado at 4.88%, New York at 4.52%, and Oklahoma at 4.48%. Behind Louisiana with the highest combined state and local sales tax is Tennessee, Arkansas, Alabama at 9.25% and Oklahoma at 8.98%. States with the lowest average combined rates are Alaska at 1.76%, Hawaii at 4.44%, Wyoming at 5.36%, Wisconsin at 5.43%, and Maine at 5.5%. Originally published at The Center Square.  Fairness, like beauty, is in the eye of the beholder. This popular sentiment is certainly true in a free market where buyers and sellers determine prices instead of a third party picking winners and losers. Unfortunately, taxes in Louisiana and other states get caught up in this subjective determination when the questions that really matter are what will help more Louisianans stay in the state, and what will bring them well-paying jobs along the way? A recent presentation by Together Baton Rouge before Louisiana’s House Ways & Means Committee made the case that the state’s tax code is unfair. They pointed to research by the left-leaning Institute on Taxation and Economic Policy (ITEP), which considers the distributional effects of tax systems in each of the 50 states. And as you’d expect, ITEP considers those states without a personal income tax as the most regressive because low-income earners tend to pay a larger share of income to taxes than upper-income earners. The fact, however, is that the majority of Louisiana’s individual income tax revenue is paid by middle and higher-income earners, as reported by the Louisiana Department of Revenue in its annual report.  ITEP’s analysis finds that “Louisiana has the 14th most unfair state and local tax system in the country.” And while that’s true in many respects, it’s not necessarily because of rising income inequality as some suggest.

Recent Census data show that people are continuing to leave Louisiana. This is a drain on innovation and job opportunities, so there’s less incentive for businesses to stay. Why would the state resort to trying to smooth the distribution of income, which would inevitably mean raising taxes on entrepreneurs who start businesses and hire workers? Instead, lawmakers’ next steps should be to restrain spending and flatten income taxes until they can be eliminated. This process was started in 2021 by lowering all the personal income tax rates, further stipulating that future increased revenue should “trigger” even lower income tax rates, which could potentially go into effect beginning next year. The state is currently seeing record levels of revenue. In fact, Louisiana is set to have an additional $1.6 billion to use in this fiscal year alone, and there is already an increase of $600 million above current revenue expected for the next fiscal year. But there is a lot of uncertainty surrounding whether the state will hit its revenue targets in future years due to economic downturns and record spending increases. If it does, the state would benefit from the lower tax rates by fueling economic growth. More should be considered in the 2023 legislative session beyond just cutting existing rates. Lawmakers should consider flattening income taxes to just one bracket with a single, low rate for everyone. This is what research has proven effective to incentivize people to work and take risks, much more so than continually taxing their innovative prosperity. Given these factors, a flat income tax would help everyone who pays taxes have skin in the game instead of trying to pick winners and losers. Higher-income earners would still pay much more in taxes with a flat tax rate because their income is higher. Fairness can be a factor, but it shouldn’t be the overarching factor when deciding tax law. The best taxes are those that are broad-based with the lowest flat rate possible, and ultimately without income taxes. This would be fair to workers and the flourishing of Louisianans for many years to come. Originally published at Pelican Institute.  The Pelican State has tremendous opportunity and potential.

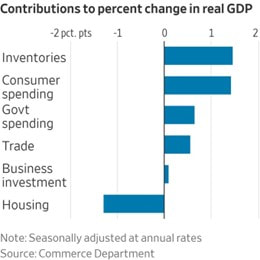

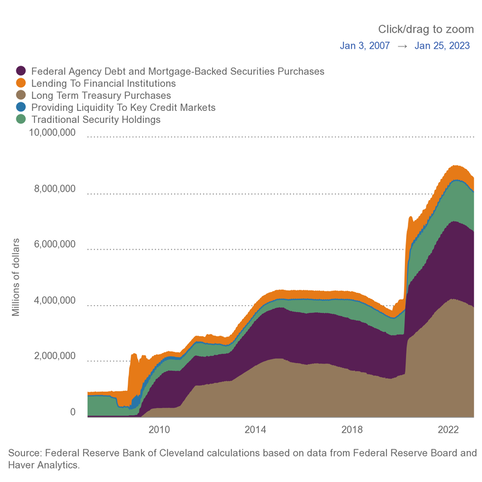

It’s got a diverse culture, renowned festivals, terrific people, and, of course, delicious food. Yet the burdensome and complicated tax code continues to hold it back from becoming what should be an economic powerhouse. The big first step to propel the state forward should be flattening state income taxes, until ultimately eliminating them. It’s no coincidence that Florida and Texas – which have no personal income taxes – had the highest net in-migration among the states last year, while Louisiana was among the bottom 10 states with the largest net out-migration. Taxing people’s income means taxing their success and desire to work. People want to be where they can keep more of their hard-earned paychecks. The exodus of people from Louisiana contributes to what appears to be a low unemployment rate of 3.5%, but it would be much higher without a shrinking labor force. Reforming taxes by first flattening them down to one bracket (Louisiana currently has three:1.85%, 3.5%, and 4.25%), with one rate until eliminating them, helps to put more money back in taxpayers’ pockets. But it also helps decentralize power from the state to the people, where it should be. This is a big deal for Louisiana as it would improve the state’s tax structure that is currently burdening individuals to fund excessive spending, thereby reducing their opportunities to flourish. What’s worse, often, the money taken in income tax isn’t always spent on meeting needs and addressing true priorities. Every year, these dollars get spent on things like splash pads, sports arenas, playgrounds, museums, visitor centers, and special local projects and programs that don’t go through any sort of vetting process. And the state’s potential deficit and unfunded liabilities continue to climb, building a financial burden of more than $22.3 billion for coming generations to pay and weakening economic growth over time. If only Louisiana had amazing results to show for its egregious spending, but it doesn’t. The latest Census report noted that Louisiana has the country’s highest poverty rate at 17.2%, and Measure of America finds that it has the 4th highest rate of 16-24-year-olds who are neither in college nor employed. These aren’t good signs for future prosperity. Making matters worse, half of elementary-aged public school students in Louisiana are unable to read on grade level. The state ranks low in student achievement relative to other states, as measured by the National Assessment of Educational Progress (NAEP), despite spending more per student than many states. And EdWeek’s Quality Counts Report Card gave Louisiana a D+ ranking for K-12 achievement. Something has to give, and it shouldn’t be families and entrepreneurs. Flattening income taxes could not only help revitalize Louisiana’s economy but also help people flourish. The benefits of such reforms can be seen in places like Texas and Florida, where people and businesses keep moving. If Louisiana joins the state flat tax revolution, it would see a substantial influx of businesses and young people coming to take advantage. The role of any state government should be to preserve liberty and limit its influence. Its role is not to rob its citizens via taxes to pay for excessive government spending and increase debt to an insurmountable burden. The best step forward for Louisiana’s growth and to embrace its bright potential is passing responsible budgets, flattening income taxes, and eventually getting rid of them for good. Originally published at The Center Square. Key Point: Americans are suffering under big-government policies as average weekly earnings adjusted for inflation are down for 21 straight months. It's time for pro-growth policies to unleash economic potential to let people prosper.  Overview: The irresponsible “shutdown recession” and subsequent government failures have led to a longer, deeper recession with high inflation that are having persistent consequences for many Americans’ livelihoods. This includes excessive federal spending redistributing scarce private sector resources with deficit spending of more than $7 trillion since January 2020 to reach the new high of $31.4 trillion in national debt—about $95,000 owed per American or $250,000 owed per taxpayer. This new debt has hit its limit and needs to be addressed with spending restraint as the Federal Reserve monetized most of the new debt, leading to a 40-year-high inflation rates. The failed policies of the Biden administration, Congress, and the Fed must be replaced with a liberty-preserving, free-market, pro-growth approach by the new majority by House Republicans so there are more opportunities to let people prosper.  Labor Market: The U.S. Bureau of Labor Statistics recently released the U.S. jobs report for December 2022. The BLS’s establishment report shows there were 223,000 net nonfarm jobs added last month, with 220,000 added in the private sector. Interestingly, while there have appeared to be a relatively robust number of jobs created, a recent report by the Philadelphia Fed find that if you add up the jobs added in states in Q2:2022 there were just 10,500 net new jobs rather than more than 1 million initially estimated. This further indicates that the recession started in (likely) March 2022 (more on this below). That expected revision to the establishment report supports the weak data in the BLS’s household survey, which employment increased by 717,000 jobs last month but had declined in four of the last nine months for a total increase of 916,000 jobs since March 2022. This number of net jobs added since then is much lower than the report 2.9 million payroll jobs in the establishment. The official U3 unemployment rate declined slightly to 3.5%, but challenges remain, including: 3.1% decline in average weekly earnings (inflation-adjusted) over the last year, 0.4-percentage point lower prime-age (25–54 years old) employment-population ratio than in February 2020, 0.6-percentage point below prime-age labor force participation rate, and 1.0-percentage-point lower total labor-force participation rate with millions of people out of the labor force.   These data support my warnings for months of stagflation, recession, and a “zombie economy.” This includes “zombie labor” as many workers are sitting on the sidelines and others are “quiet quitting” while there’s a declining number of unfilled jobs than unemployed people to 4.5 million And that demand for labor is likely inflated from many “zombie firms,” which run on debt and could make up at least 20% of the stock market and will likely lay off workers with rising debt costs. Economic Growth: The U.S. Bureau of Economic Analysis’ released economic output data for Q4:2022. The following provides data for real total gross domestic product (GDP), measured in chained 2012 dollars, and real private GDP, which excludes government consumption expenditures and gross investment.  The shutdown recession in 2020 had GDP contract at historic annualized rates because of individual responses and government-imposed shutdowns related to the COVID-19 pandemic. Economic activity has had booms and busts thereafter because of inappropriately imposed government COVID-related restrictions in response to the pandemic and poor fiscal policies that severely hurt people’s ability to exchange and work. Since 2021, the growth in nominal total GDP, measured in current dollars, was dominated by inflation, which distorts economic activity. The GDP implicit price deflator was +6.1% for Q4-over-Q4 2021, representing half of the +12.2% increase in nominal total GDP. This inflation measure was +9.1% in Q2:2022—the highest since Q1:1981—for a +8.5% increase in nominal total GDP that quarter. This made two consecutive declines in real total (and private) GDP, providing a criterion to date recessions every time since at least 1950. In Q3:2022, nominal total GDP was +7.6% and GDP inflation was +4.4% for the +3.2% increase in real total GDP. But if inflation had been as high as it was in the prior two quarters or had the contribution of net exports of goods and services (driven by natural gas exports to Europe) not been 2.9%, real total GDP would have either declined or been essentially flat for a third straight quarter. In Q4:2022, there was a similar story of weaknesses as nominal total GDP was +6.4% and GDP inflation was +3.5% for the +2.9% increase in real total GDP. But if you consider the +2.9% real total GDP growth was driven by contributions of volatile inventories (+1.5pp), government spending (+0.6pp), and next exports (+0.6pp) which total +2.7pp, the actual growth is quite tepid. For all of 2022, real total GDP growth is reported +2.1% year-over-year but measured by Q4-over-Q4 the growth rate was only +0.96%, which was the slowest Q4-over-Q4 growth for a year since 2009 (last part of Great Recession).  The Atlanta Fed’s early GDPNow projection on January 27, 2023 for real total GDP growth in Q1:2023 was +0.7% based on the latest data available. The table above also shows the last expansion from June 2009 to February 2020. The earlier part of the expansion had slower real total GDP growth but had faster real private GDP growth. A reason for this difference is higher deficit-spending in the latter period, contributing to crowding-out of the productive private sector. Congress’ excessive spending thereafter led to a massive increase in the national debt that would have led to higher market interest rates. This is yet another example of how there is always an excessive government spending problem as noted in the following figure with federal spending and tax receipts as a share of GDP.  But the Fed monetized much of it to keep rates artificially lower thereby creating higher inflation as there has been too much money chasing too few goods and services as production has been overregulated and overtaxed and workers have been given too many handouts. The Fed’s balance sheet exploded from about $4 trillion, when it was already bloated after the Great Recession, to nearly $9 trillion and is down only about 6% since the record high in April 2022. The Fed will need to cut its balance sheet (see first figure below with total assets over time) more aggressively if it is to stop manipulating so many markets (see second figure with types of assets on its balance sheet) and persistently tame inflation.   The resulting inflation measured by the consumer price index (CPI) has cooled some from the peak of 9.1% in June 2022 but remains hot at 6.5% in December 2022 over the last year, which remains at a 40-year high (highest since June 1982) along with other key measures of inflation (see figure below). After adjusting total earnings in the private sector for CPI inflation, real total earnings are up by only 1.1% since February 2020 as the shutdown recession took a huge hit on total earnings and then higher inflation hindered increased purchasing power.   Just as inflation is always and everywhere a monetary phenomenon, high deficits and taxes are always and everywhere a spending problem. The figure below (h/t David Boaz at Cato Institute) shows how this problem is from both Republicans and Democrats.  As the federal debt far exceeds U.S. GDP, and President Biden proposed an irresponsible FY23 budget and Congress never passed one until the ridiculous $1.7 trillion omnibus in December, America needs a fiscal rule like the Responsible American Budget (RAB) with a maximum spending limit based on population growth plus inflation. If Congress had followed this approach from 2002 to 2021, the (updated) $17.7 trillion national debt increase would instead have been a $1.1 trillion decrease (i.e., surplus) for a $18.8 trillion swing to the positive that would have reduced the cost to Americans. The Republican Study Committee recently noted the strength of this type of fiscal rule in its FY 2023 “Blueprint to Save America.” And the Federal Reserve should follow a monetary rule.

Bottom Line: Americans are struggling from bad policies out of D.C., which have resulted in a recession with high inflation. Instead of passing massive spending bills, like passage of the “Inflation Reduction Act” that will result in higher taxes, more inflation, and deeper recession, the path forward should include pro-growth policies. These policies ought to be similar to those that supported historic prosperity from 2017 to 2019 that get government out of the way rather than the progressive policies of more spending, regulating, and taxing. The time is now for limited government with sound fiscal and monetary policy that provides more opportunities for people to work and have more paths out of poverty. Recommendations:

By Victor Skinner | The Center Square contributor | Jan 26, 2023

(The Center Square) — New analysis shows Louisiana’s top corporate income tax rate is the 15th highest in the nation, a reality critics contend is holding the state back. Analysis from the Tax Foundation released Tuesday shows that out of the 44 states that levy a corporate income tax, Louisiana’s top 7.5% rate ranks 15th from the top, the highest in the region. Neighboring Texas does not levy a corporate income tax and instead imposes a gross receipts tax on businesses, while Arkansas’ 5.3% rate ranked 33rd, and Mississippi’s 5% rate ranked 34th. "The rate is too high, 7.5% ranking 15th in the nation means Louisiana is less competitive, especially with its neighbors," Vance Ginn, chief economist at the Pelican Institute, told The Center Square. Ginn noted that the corporate income tax ranking follows a previous report from the Tax Foundation that ranked Louisiana as the 12th lowest state for business tax climate, a measure that takes into account other factors. He contends lawmakers can take action to improve the situation. "What we’ve been looking at is finding ways to flatten the corporate income tax," Ginn said, noting that the state’s current system has three brackets. Reducing the three brackets into one would help in the short term, he said, but the long-term focus should be on "eliminating the income tax and finding ways to limit government spending," he said. "What we’ve been looking at is using surplus funds to buy down the corporate tax," Ginn said. Louisiana "really ultimately needs to be more competitive," he said. "People are moving out. Businesses are moving out." Ginn pointed to recent U.S. Census data that shows 67,508 residents left the Pelican State between April 1, 2020 and July 1, 2022, with most of the loss through domestic migration. The Tax Foundation identified 44 states that levy a corporate income tax, which ranged from North Carolina’s 2.5% rate to 11.5% in New Jersey. Behind the Garden State is Minnesota at 9.8%, Illinois at 9.5%, and Alaska and Pennsylvania, which levy top corporate tax rates of 9.4% and 8.99%, respectively. There are 11 states with top rates at or below 5%. North Carolina is followed by Missouri and Oklahoma at 4%, North Dakota at 4.31%, Colorado at 4.55%, Utah at 4.85%, Arizona and Indiana at 4.9%, and Kentucky, Mississippi, and South Carolina at 5%. Nevada, Ohio, Texas, and Washington use a gross receipts tax instead of corporate income taxes, while Delaware, Oregon, and Tennessee impose both gross receipts taxes and corporate income taxes. "Though often thought of as a major tax type, corporate income taxes accounted for an average of just 7.07% of state tax collections and 4.04% of state general revenue in fiscal year 2021," according to the report. "And while these figures are not high, they represent a substantial increase over prior years. Corporate income taxes accounted for 2.26% of general revenue in FY 2020, which is more in line with historical norms." Originally published at The Center Square.  Texans are struggling with high property taxes, soaring prices, and stagnant income. As a result, most big-budget players favor some property tax relief. For instance, Gov. Greg Abbot declared his intention to use half of the actual surplus fund ($16.3 billion) for this initiative. Likewise, Lt. Gov. Dan Patrick revealed that property tax relief is his first legislative priority.

However, the economic outlook for 2023 is not encouraging. The IMF has announced a slowdown in the global economy, and a third of the world’s economy is expected to be in a recession in 2023. Moreover, the consensus among large financial institutions is that the U.S. will have a recession this year. Consequently, in such a bloomy scenario, caution is warranted on how to use Texas surplus funds prudently. Based on previous data, the Foundation finds that Texas has enough funds to use toward property tax relief, even in the worst-case scenario. Our three key findings are:

Considering that the State’s finances are robust enough to face a recession, the Foundation has proposed a path toward completely eliminating school districts’ maintenance and operations property taxes by using state surplus general revenue-related (GRR) funds to buy them down over time to zero. By following the spending limit of population plus inflation, assigning at least half of the current surplus and 90% of the future surplus thereafter, we should expect the elimination of school district M&O property taxes over the next decade. In case of any revenue shortfall, school districts could cover it with their reserve funds. By gradually replacing property taxes with more efficient sales taxes, more Texans would be able to boost their savings, afford a new home, and preserve their property while improving their ability to afford housing and other necessities. Originally published at TPPF. Payments on COVID disaster loans for small businesses are due, and it couldn't come at a worse time.

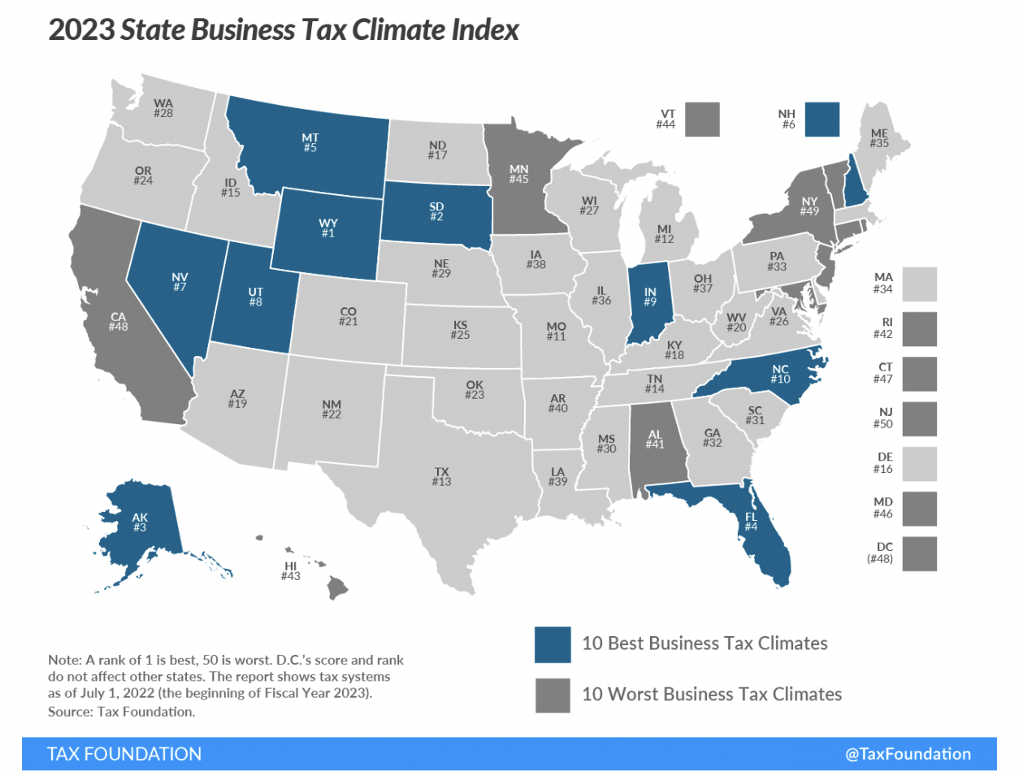

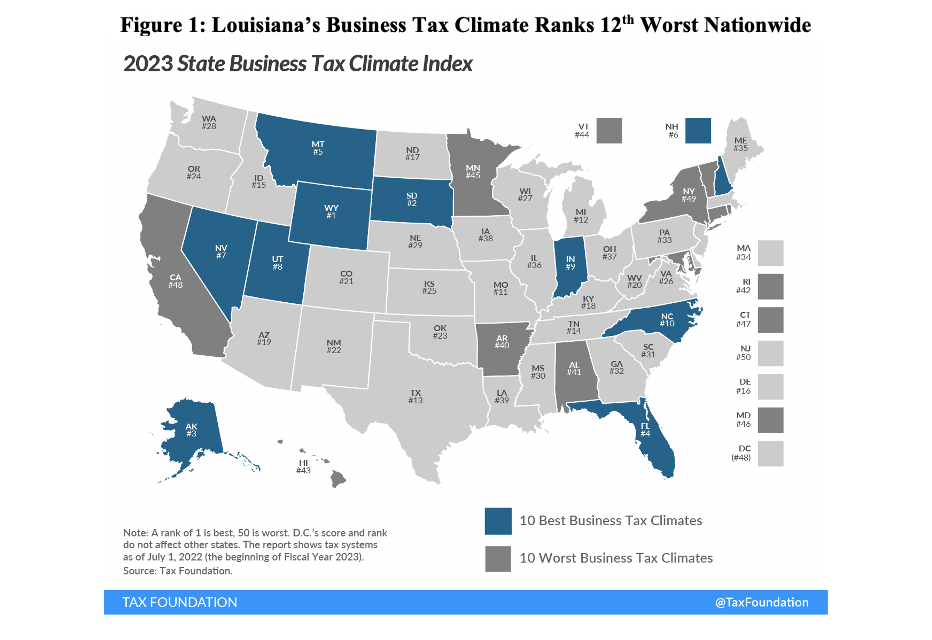

Roughly $390 billion went out to nearly four million small business owners during COVID lockdowns. "Those are starting to come due at the end of 2022 and early 2023, which could add to the financial pressure that a lot of small businesses are facing across the United States," says Vance Ginn, chief economist for the Pelican Institute for Public Policy. Ginn says many small business owners are still struggling to find and/or pay workers, on top of rising costs under Bidenflation. "Small businesses employ about 90 percent of all workers," he says. "This is really where you get the mass number of people working. If they start to pull back, it could lead to a rapid draw down in the number of jobs being created or that are even there now across the economy." At the same time, consumers are starting to pull back spending due to higher interest rates. "As inflation goes up, they don't have as much to spend on other goods and services. So, a lot of these small businesses are taking a hit at the same time they're going to start to pay back a lot of these loans," says Ginn. Originally aired on KTRH News in Houston, Texas. In October, the Tax Foundation released the 2023 State Business Tax Climate Index. The report ranks all fifty states based on the collective burdens of each state’s corporate income tax, individual income tax, sales tax, unemployment insurance, and property tax. The results showed that spending restraint funded with a low rate, broad-based taxes provide the best climate for business activity, which supports more jobs, and we all know that work helps provide people with dignity, purpose, and hope, along with the long-term self-sufficiency that is essential for families to flourish. The Tax Foundation’s report notes what many entrepreneurs in Louisiana already know: the state’s business tax climate needs improving. Figure 1 shows that last year the state ranked as the 12th worst among the 50 states, which is an improvement from the 8th worst ranking in the prior year, but still well below where it needs to be to support more in-migration, economic growth, and well-paying jobs. Last year’s ranking was influenced by the corporate tax rank of 32nd, individual income tax rank of 25th, sales tax rank of 48th, property tax rank of 23rd, and unemployment insurance tax rank of 6th in the nation.  Source: Tax Foundation

Compared with nearby states, Louisiana ranked ahead of Arkansas (40th), behind Mississippi (30th), and remained well-below neighboring Texas which improved from the previous report to 13th best in the nation. Given the upcoming 2023 session in Louisiana, the state legislature has an extraordinary opportunity to learn from the Tax Foundation’s report on how to improve. For Louisiana to provide greater opportunity for entrepreneurs and families to prosper, the business tax climate must improve by limiting spending, reforming and cutting taxes, and reducing regulatory burdens. Doing so will help more Louisianans live the American Dream. Originally published at Pelican Institute.  Is the flat income tax revolution underway across the states enough? No, but it must be advanced.

This extraordinary feat includes four states passing a flat personal income tax in 2022 after only four did over the last century. Now 14 states have or will soon have flat income taxes. But if you consider how the nine states without personal income taxes outperform, on average, the nine states with flat income taxes in economic growth, domestic migration, and nonfarm payroll employment over the last decade, more is necessary. While flattening income taxes is important, eliminating them is best. And this should be tied to spending restraint to avoid the infamous Kansas problem of excess spending while cutting taxes. The five states always with a flat income tax were Massachusetts (1917), Indiana (1965), Michigan (1967), Illinois (1969), and Pennsylvania (1971). The next four states initially with progressive income taxes before improving to a flat income tax were Colorado (1987), Utah (2007), North Carolina (2014), and Kentucky (2019). The four states that passed a flat income tax in 2022 were Idaho (starts in 2023), Mississippi (2023), Georgia (2024), and Iowa (2026). After a recent court decision, Arizona will also have a flat income tax in 2023 at the lowest rate in the nation at 2.5%. This will support greater economic growth as progressive personal income taxes disincentivize people to work and live in those states. This is happening in California, where even its wealthy citizens are fed up with sky-high personal income taxes that will worsen when the top marginal tax rate rises to 14.4% in 2024. According to the American Legislative Exchange Council’s 15th edition of the Rich States, Poor States report that compares the economic performance of the 50 states, the nine states already with a flat income tax rank mostly in the middle of the pack from 2010 to 2020. This includes an average overall ranking for those nine states of 24th based upon three key economic variables with average rankings of 23rd in state gross domestic product (GDP), 29th in absolute domestic migration, and 22nd in nonfarm payroll. The highest overall rankings for these states are Utah (2nd) and Colorado (6th), lowest are Illinois (43rd) and Pennsylvania (45th). States should seek better outcomes that ultimately help people flourish. The nine states without a personal income tax are Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming. These states have average rankings in ALEC’s report of 19th overall, 22nd in GDP, 14th in migration, and 21st in jobs. The highest overall rankings are Florida (3rd) and Washington (5th), with Texas (8th) and Tennessee (10th) also in the top 10, and lowest are Wyoming (41st) and Alaska (49th). Historically, the nine states with the highest personal income tax rates, including California (ranks 19th) and New York (36th), have underperformed in these economic measures and have dire outlooks ranking 48th and 50th, respectively, in ALEC’s report. Progressive, high-income tax structures produce undesirable outcomes, and states should work toward eliminating personal income taxes. Other taxes and policies matter. The Tax Foundation’s latest report on state business tax climates shows how other taxes influence business activity, and thus economic performance. States without a personal income tax or lower tax burdens overall rank the highest in business tax climate with Wyoming (1st), South Dakota (2nd), Alaska (3rd), and Florida (4th) leading the way. And those states with the highest personal income rates perform worst with California (48th), New York (49th), and New Jersey (50th) being last. What many of these states without personal income taxes tend to use to fund their spending are consumption-based taxes. The least burdensome form of taxation tends to be a flat final sales tax with the broadest base and lowest rate possible. Whatever you tax, you get less of it. Taxing consumption results in less consumption but more savings, which can support greater capital accumulation and economic growth while taxing the underground economy, such as drug dealers and undocumented workers. But the ultimate burden of government is not how much it taxes but how much it spends. Jonathan Williams, who is a co-author of the ALEC report, correctly noted, “There are nine states with no income taxes, and they spend substantially less per capita than states with an income tax.” When there’s already heavy headwinds imposed by policymakers in Washington and across many states, it’s time to build on the flat tax revolution by cutting or even freezing state budgets, strengthening state spending limits, and eliminating personal income taxes. Original post at EconLib.  It’s time for Louisiana to join the flat tax revolution. Four states passed a flat personal income tax this year after only four did over the 100 years, bringing the total to 14 states that have or will soon have flat income taxes.

Flattening income taxes provides more opportunities for people to flourish, but eliminating them is best to provide even more prosperity and individual liberty to keep the fruits of your labor. These tax reforms start with spending restraint. Economic data show that the nine states without a personal income tax outperform, on average, the nine states with flat income taxes in economic growth, domestic migration, and non-farm payroll employment over the last decade. Georgia (2024), Idaho (2023), Iowa (2026), and Mississippi (2023) passed flat-income taxes this year. Arizona is set to have a flat income tax in 2023 at 2.5%, which will be the lowest rate in the nation. Through those reforms, these states will have more opportunities to improve the number of well-paid jobs, sectoral growth, and other benefits that advance thriving communities. This contrasts with progressive personal income taxes that disincentivize people from working and living in those states. This is happening in California, where even its wealthy citizens are leaving as personal income taxes soar, and it’s likely to get worse as the top marginal tax rate rises to 14.4% in 2024. Progressive, high-income tax structures produce undesirable outcomes, and states should work toward eliminating personal income taxes. Of course, other taxes and policies matter. Louisiana took a great step in the right direction by dropping our progressive rates and putting in revenue triggers that will lower them further over time. Yet flattening them to one rate would be the best next step. According to the Tax Foundation’s recent report, states without a personal income tax or lower tax burdens overall rank the highest in business tax climate, with Wyoming (1st), South Dakota (2nd), Alaska (3rd), and Florida (4th) leading the way. And those states with the highest personal income rates perform worst, with California (48th), New York (49th), and New Jersey (50th) being last. Louisiana ranks 39th, its best ranking since 2017, after improving three spots from the recent tax reforms. But the state remains near the back of the pack, which could be improved by continuing to cut away at the personal income tax. What would help fund limited government spending with an improved tax system? The increased economic activity from an improved tax system will help increase tax revenue collections, as the state would move more towards a consumption-based tax system. The least burdensome form of taxation tends to be a flat final sales tax with the broadest base and lowest rate possible. Taxing consumption results in less consumption but more savings, which can support greater capital accumulation and economic growth. The ultimate burden of government is how much it spends. Jonathan Williams, who is a co-author of the ALEC report on economic performance by states, recently said, “There are nine states with no income taxes, and they spend substantially less per capita than states with an income tax.” Given major headwinds from D.C., it’s time for Louisiana to join the flat tax revolution by strengthening the state spending limit and flattening its personal income taxes until ultimately eliminating them. Originally published Pelican Institute  Many cities across the nation are facing a fiscal crisis. While pandemic-related problems that were self-induced or otherwise play a part, many of these issues have plagued cities for a long time. A serious cultural shift concerning finances among local governments is critical if people want to flourish in cities.

I recently interviewed Mark Moses who is a municipal government expert and author of the recently published book The Municipal Financial Crisis: A Framework for Understanding and Fixing Government Budgeting. He contends that “many local governments are on track for bankruptcy.” And this downward trajectory can be expected to continue as municipalities fail to restrain their spending and overreach, crowding out opportunities for the private sector to work. We’re seeing this play out in places like New York City, where city-funded expenses have been asked to be cut by 3% and on track to be slashed more in response to their recently reported $10 billion deficit. Moses says that “there’s a lack of economic understanding in lots of municipalities.” This absence of understanding often results in collecting more taxes to fund more “solutions” as a band-aid to the broken system and struggling local finances. As he puts it, “local governments give up trying to balance budget sheets.” But failing to assess and address the tangled economic approach that’s led them to a place where more taxes and regulations seem like the only answer leads to long-term issues and a path that’s difficult to leave. Local governments must limit their scope and focus on core issues. That means letting new initiatives and departments take a back seat while they get spending under control. This is difficult, however, especially after the 2021 American Rescue Plan Act that gave $45.6 billion to municipalities, which temporarily and artificially inflated local finances. More money under lousy management is a weak fix. And now, with rising inflation and energy costs, these municipalities are ill-equipped to thrive in a recession that wasn’t helped by the huge bailout package. A good start to overcoming these challenges would be to get government out of the way in most cases so that the the private sector can solve key issues, which has proven to be the best antidote for most problems throughout history. Overinflating their role instead of sticking to limited governing, such as property rights and a few public goods, is a trap that many cities fall into and that comes at a huge cost. But philanthropic and other private-led solutions tend to be crowded out through higher taxes and regulations when city hall makes promises they can’t fulfill. Moses describes this as municipalities “seeing themselves as an end to themselves,” which is why many local governments resist spending limits or find ways around them. This is an ongoing issue in Texas which is contributing to an affordability crisis. Texas is blessed to have constitutional amendments against state-controlled personal income taxes or property taxes, so all property taxes are local in Texas. While there have been attempts recently by the state to limit their growth, property taxes have increased by 169% in the past 20 years compared with an increase of 104% in the rate of population growth plus inflation. This indicates that property taxes are growing well above the average taxpayer’s ability to pay for them. Some argue that Texas has high property taxes because it has no personal income taxes. But the reality is that it is really from excessive local government spending. For example, Texas has the 6th most burdensome residential property tax according to the Tax Foundation but other states without a personal income tax like Florida and Tennessee rank 26th and 36th, respectively. This is because the latter two states do a better job restraining spending. The best way to get budgets and taxes back on a fiscally conservative track is through a strict spending limit that covers the entire budget and grows no more than the rate of population growth plus inflation. This would help cities, and all local governments, stick to just addressing what’s in their purview. A city’s scope shouldn’t be evaluated from one council meeting to the next but should be assessed in the long term if its local government hopes to see future success and a prosperous economy. The same principles of economic success apply to all government institutions; people flourish where liberty is preserved, and that’s best achieved under limited government whereby politicians’ interventions remain inside their limited scope so that free markets and free people can innovate and thrive. Just as we’re witnessing with this recession, there’s always a trade-off to overspending and unbalanced budgets. The sooner local governments realize that and reel in their spending, which is the ultimate burden of government, the sooner financial crises will be averted. Originally published at EconLib  Louisiana has many of the right characteristics for families to flourish. This includes abundant natural resources and thriving petrochemical, oil and gas, and tourism sectors. In fact, New Orleans was recently ranked as the 9th fastest-growing city for 2022 by the American Growth Project. They note that the worker shortages in New Orleans “could indicate the city has even more room to grow in coming years.”