|

Thank you for listening to the 47th episode of "This Week's Economy."

Today, I cover the following and more in 10 minutes: 1) National: - The federal fiscal trajectory is unsustainable and must be corrected before more crises happen, as the trust funds for Social Security and Medicare are expected to run dry over the next decade - U.S. household debt rose by $212 billion in Q4 2023 to a new record of $15.7 trillion - Federal Reserve Chairman Jerome Powell recently noted on 60 Minutes that no target federal funds rate cuts until at least May 2024, and Congress must get control of deficit spending - What’s really going on at the border? I wonder if it has anything to do with Trump’s trade war and lockdowns, as apprehensions started increasing in 2020 before Biden took office 2) States: -Texas approved a new constitutional amendment that provides $10 billion for low-interest loans to companies building thermal energy plants, increasing corporate welfare in Texas -Americans for Tax Reform has updated the Sustainable Budget Project website, showing how states can improve budgets and providing economic and fiscal comparisons -The Kansas Policy Institute released the third iteration of the Responsible Kansas Budget, revealing ample opportunity for Kansas to limit government spending and reduce tax rates. 3) My Media Hits & Other: - I had a blast at the Brickell Unconference in Miami with many freedom fighters known as Freedom Conservatives - Check out this week’s LPP episode with Dr. Bryan Caplan on the myth of the rational voter, the case against education, open borders, and more -Don’t miss this upcoming LPP episode on Monday with Dr. Michael Strain on the national debt crisis, Trumpism, and why the American dream isn’t dead Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. Also, subscribe and see show notes for this episode on Substack (www.vanceginn.substack.com) and visit my website for economic insights (www.vanceginn.com).

0 Comments

Podcast: Are Republicans and Democrats Causing America’s Fiscal Crisis? Will the 2024 Election Help?2/5/2024 Episode 82 is with Dr. Bryan Caplan, professor of economics at George Mason University and a New York Times bestselling author.

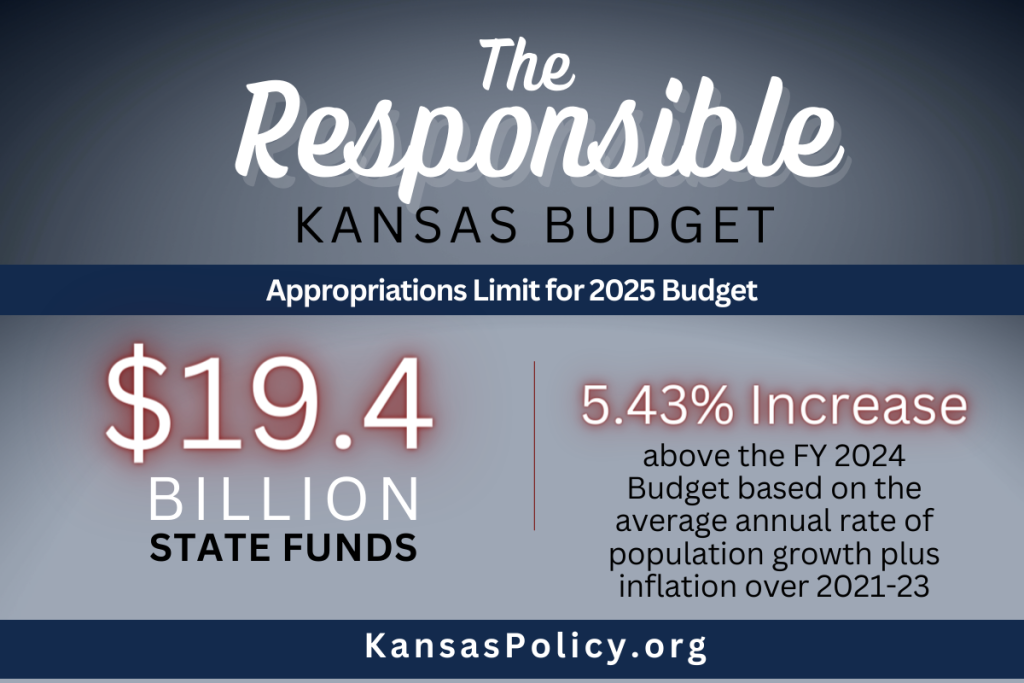

Today, we discuss: 1) Myth of the rational voter and how politics has become a religion, 2) Reasons why the U.S. is heading toward a fiscal crisis because neither party will restrain spending; and 3) Case against education, school choice pros and cons, selfish reasons for having more kids, and open borders. Please like and comment on this video, subscribe to the channel, share it on social media, and provide a rating and review. Thanks! Also, subscribe and see show notes for this episode on Substack (www.vanceginn.substack.com) and visit my website for economic insights (www.vanceginn.com).  Originally published at Kansas Policy Institute. Kansas, like most states, has a spending problem, not a revenue problem. The 2025 Responsible Kansas Budget offers several ways that the state can limit its spending to pave the way for tax reform and economic growth in the future. In June 2023, Kansas ended FY 2023 with collected tax revenues at $10.2 billion – a 4.1% or $402 million increase over the collected tax revenues of FY 2022. According to the Kansas Legislative Research Department, even if Kansas had enacted a flat tax bill during its 2023 legislative session, the state would end FY 2028 with $2.7 billion in its ending balance and $1.8 billion in the Budget Stabilization Fund, totaling $4.5 billion in reserves. At the same time, spending has grown massively over the last decade. According to the FY 2025 Governor’s Budget Report, the approved FY 2024 General Fund budget of $9.918 billion is 13.6% more than the approved 2023 budget. In FY 2020, the State Fund appropriations equaled $12.6 billion, but has ballooned into and after the COVID-19 pandemic to be $19 billion in FY 2023 and a base of $18.4 billion for FY 2024. If Kansas’s annual appropriations had grown at the rate of population growth plus inflation since FY 2005, State Fund appropriations would be $6.4 billion lower in FY 2024 than the actual base appropriations. This equates to a $46.6 billion cumulative difference from FY 2005 to FY 2024. What this number represents is higher taxes on Kansans, slower economic growth, and fewer opportunities for people to flourish. Podcast: Real Average Weekly Earnings Fall AGAIN: Can Americans Keep Up With Costs in 2024?2/2/2024 Thank you for listening to the 46th episode of "This Week's Economy."

Today, I cover the following and more in less than 12 minutes: 1) National: - Average weekly earnings adjusted for CPI or PCE declined in 2022 and 2023 during the Biden administration. - In an X poll, 85% of voters wanted to cut government spending, 10% said to cut taxes, 3% said to raise taxes, and 2% said to raise spending. - Is Oren Cass right to criticize "market fundamentalism”? 2) States: - My research by Texans for Fiscal Responsibility shows how the Legislature’s property tax relief last session was the second largest in state history despite what some have been claiming. - My research on the Responsible Louisiana Budget provides a roadmap to fiscal sustainability in Louisiana. This is needed because employment has declined for 7 straight months, and people keep leaving the state. - My commentary at Complete Colorado calls on Governor Polis to do as he’s promised and reduce tax expenditures so there is more opportunity to cut income taxes, which should include less spending. 3) My Media Hits & Other: - I was quoted in Forbes discussing how Texas could have universal ESAs and save at least $13 billion per year, but too many want to grow the budget. - I was recently accepted to be a 2024 Club for Growth Foundation Fellow. -Don't miss last week's LPP episode with Dr. Bruce Caldwell on Friedrich Hayek, including his upbringing, economics, and much more - Set your alarms for Monday's LPP episode on Monday with Dr. Bryan Caplan on open borders, reasons to have more kids, an end to education, and more. Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. Also, subscribe and see show notes for this episode on Substack (www.vanceginn.substack.com) and visit my website for economic insights (www.vanceginn.com).  Originally published at Pelican Institute.

Spending, not taxes, is the ultimate burden of government. If you don’t spend money on a program, you don’t need to collect taxes to fund it. And if you don’t spend money on programs, the government can’t regulate things. Remember that government spending is paid for by the people, as the government creates nothing to earn income, so considering what people can afford is crucial. This is why it’s essential for governments at every level to narrow their scope to the essential functions enshrined in constitutions. Otherwise, spending grows too much and results in taxes being too burdensome on people. Governments across the country and the globe are spending too much. And it appears that a sustainable budget revolution is happening! I’ve been working for over a decade to help state, federal, and local governments create and adopt sustainable budgets that fund limited government. This is critical to keeping taxes and regulations lower than otherwise, so families and entrepreneurs have more of their hard-earned money in their pockets. This standard is called a fiscal rule or a tax and expenditure limit (TEL), which goes like this: a government’s budget growth cannot exceed the rate of population growth plus inflation. How does this simple rule work? This approach started in 2013 when I helped develop the Conservative Texas Budget. After years of excessive spending in Texas, we defined the narrative of a tangible cap on appropriations based on the rate of population growth plus inflation. There was no change in the state’s law right away, but this approach worked well for several sessions by helping keep spending within this rate, which represents the average taxpayer’s ability to pay for spending. Importantly, this is a maximum growth limit, as most states need to spend much less than this limit as they are already spending too much, which will help leave more money in people’s pockets. Over the years, this rule has been used to help state and local governments make their budgets more sustainable. One such victory came in 2021 when Texas put Senate Bill 1336 into law. The bill changed the state’s budget limit to not exceed the rate of population growth and inflation when it had been based on personal income growth. This was an extraordinary reform that took nearly a decade to accomplish. It’s not perfect, as it should be in the state’s constitution and should cover all state funds and use population growth plus inflation. But it’s one of, if not the, best in the country. The other spending limit that has long been the gold standard is the Taxpayer’s Bill of Rights (TABOR) in Colorado, which I recently outlined how it needed to be improved as it has been weakened over time. By working with think tanks, grassroots organizations, and lawmakers across the country, I’ve helped create and pass sustainable budgets for the following states: Alaska, Florida, Iowa, Michigan, Mississippi, Montana, South Carolina, and Tennessee. I’ve also worked with other states where a sustainable budget was proposed, such as Kansas and Louisiana, but hasn’t yet passed. Partnering with Americans for Tax Reform, I’ve contributed to creating the Sustainable Budget Project, which monitors state government spending and evaluates the adoption of sustainable budgets across all states. This Project has a slightly different methodology and purpose than the one outlined above, as the focus is on spending at the end of a budget period instead of the one I’ve been using for appropriations at the start of the appropriations process. Together, these approaches can help states define the narrative about the need for spending restraint on the budget process’s front and back end. Given the excessive spending by governments and the incentive to continue doing so, there should be as many safeguards as possible. As Louisiana enters a new year with a new session and new governor this year, lawmakers have an extraordinary opportunity to prioritize sustainable budgeting by adopting what we’re calling a Responsible Louisiana Budget. The Pelican Institute released the first iteration of the RLB last year and the second one this year. This isn’t just about fiscal responsibility; it’s an effort that will help the people of Louisiana prosper. It will do so by helping Louisianans not be overburdened by unnecessary taxes for more money in their pockets. It’s Geaux Time in Louisiana, and that includes sustainable budgeting! Originally published at Pelican Institute. The report to achieve Louisiana’s 2024-2025 Responsible Budget presents solutions to rein in the extraordinary growth of the budget in order to give the state a competitive advantage, much like those used in other states, such as Texas and Florida, limiting the amount of funding appropriated at the beginning of each fiscal year. Over the past decade, state spending has increased an average of 5.9% per year. Using the recommended Responsible Budget growth limit outlined in this report, state spending would have increased by only 2.1% per year, which would allow the excess state revenue to be saved for tax relief for Louisiana families.  Originally published at Texans for Fiscal Responsibility. Episode 81 is with Dr. Bruce Caldwell, research professor of economics at Duke University and author and editor of numerous books, including Hayek: A Life, 1899-1950.

Today, we discuss: 1) Friedrich Hayek’s early life, views, and economic influences; 2) The significance of some of Hayek’s iconic contributions to economics, such as the knowledge problem, spontaneous order, and free trade; and 3) What advice would Hayek have for our current economy, and would he be a conservative today? Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. Also, subscribe and see show notes for this episode on Substack (www.vanceginn.substack.com) and visit my website for economic insights (www.vanceginn.com). Thank you for listening to the 45th episode of "This Week's Economy."

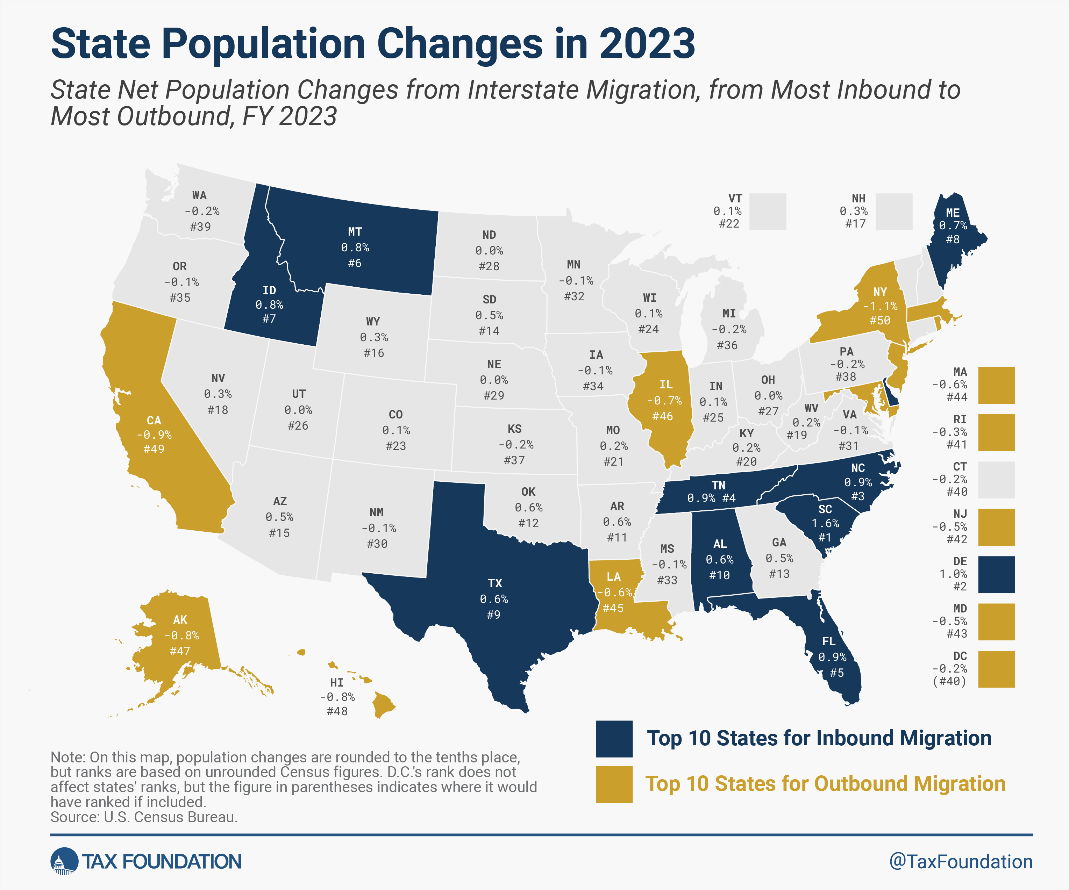

Today, I cover: 1) National: -DeSantis drops out of the race, and New Hampshire primary results put Trump and Haley fairly close, so what happens next? -Real GDP for Q4 2023 was up 3.3%, but the contribution of costly, unproductive government spending makes the real private GDP rate lower. -The stock market has been better under Trump than Biden through three years of their terms, but Trump can’t necessarily take the credit. Will he try? -Grocery prices have moderated but have still outpaced earnings since 2019; what does it mean to you? -Why the tax code shouldn’t serve as social engineering, but why does Congress try? 2) States: -National School Choice Week highlights which states need to provide universal education freedom. Is your state next? -My new paper with Sal Nuzzo of the James Madison Institute notes how Florida can reduce its sales tax burden, but will they do it? -State-level jobs report reveals that job growth is slow across most states, but Texas leads in job creation. How does your state do? 3) My Media Hits & Other: -My recent commentary reveals what’s really going on in the labor market. -My latest bonus LPP episode with Brad Swail of Texas Talks shares my thoughts on the economy, Texas, property taxes, immigration, and more. -Last week’s LPP episode with Matt Mitchell reveals how Estonia is freer than the U.S. -Set your alarms for Monday so you don’t miss my upcoming episode with Dr. Bruce Caldwell on Friedrich Hayek and much more. Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. Also, subscribe and see show notes for this episode on Substack (www.vanceginn.substack.com) and visit my website for economic insights (www.vanceginn.com). Louisiana’s economy needs a comeback. While there are many reasons why, a major reason is that the state has now had a declining population for seven straight years, and employment has declined for six consecutive months. While there are positive indicators on the surface, the reality is much different for many Louisianans. Let’s dive into the data and see what’s going on. The Pelican State has abundant resources, but many failed public policies keep Louisianans from flourishing. Louisiana’s population declines again as people move to other states. The U.S. Census Bureau recently released population data for each state. Louisiana’s population declined in 2023 by 14,274 people to 4.57 million. Making matters worse, this was the seventh consecutive year that Louisiana’s population has declined to a total of 107,000 fewer people residing here since 2016. The new data also provides net domestic migration, telling us how many people enter or exit the Pelican State from other states. Figure 1 shows how Louisiana had the sixth largest outmigration to other states. The net outmigration for 2023 was 29,692 people, representing a 0.6% decline. Figure 1: Louisiana had the Sixth Largest Net Outmigration  Source: Tax Foundation But that’s not the worst part; the state has had net outmigration for at least the last four years, with 110,709 people fleeing Louisiana for another state since 2020. This is a terrible trend for the state as families are broken up, people with higher skills and incomes typically leave, and the economy suffers. Of course, these declines in the population make many of the labor market measures look better than they would have had these people stayed in Louisiana. The U.S. Bureau of Labor Statistics recently released Louisiana’s labor market data for December to help us evaluate how people are doing across the state. Louisiana’s unemployment rate would be 5.5% if the working-age population hadn’t declined since February 2020 instead of the reported 3.7% rate.

Louisiana’s employment level from the household survey shows it has declined in seven straight months for a total decline of 29,450 jobs since May 2023.

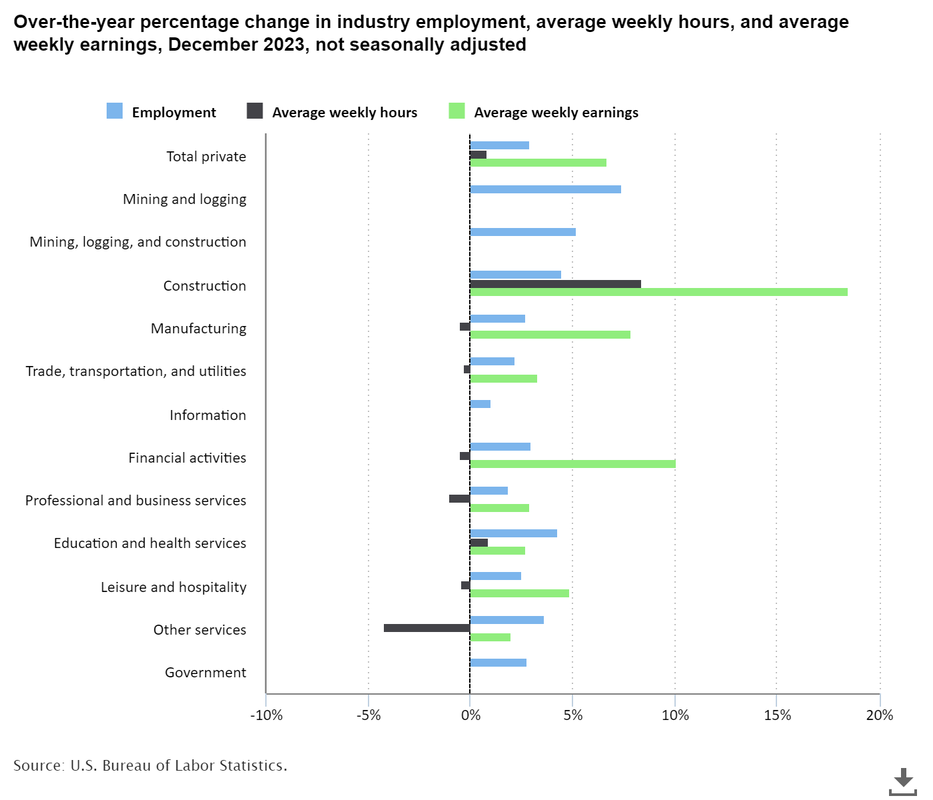

Louisiana workers’ purchasing power continues to decline across most industries.

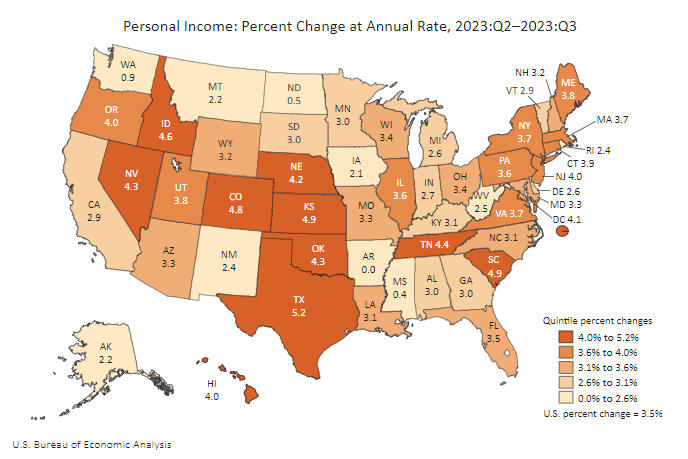

Figure 2. Louisiana’s Labor Market by Industry  Source: U.S. Bureau of Labor Statistics Economic growth has picked up, but personal income lags the U.S. average.

Figure 3: Personal Income Growth by State in Q3:2023  Source: U.S. Bureau of Economic Analysis

Bottom Line: Louisiana’s economy shows some signs of strength when you look at the broader economy. But those gains do not reflect what is going on in the labor market so there is likely going to be less growth in the economy soon with more job losses to come. Given these results, there will not be improvements in the state’s poor business tax climate, net out-migration of Louisianans, or Louisiana having one of the highest poverty rates in the country—unless bold, pro-growth reforms are enacted soon. These bold reforms include:

Originally published at Inside Sources.

The final jobs report for 2023 was recently reported. The headlines look good but don’t tell the full story. This has been a common theme with many economic indicators, from the labor market to economic output. With this being an election year, politicians are trying to milk every apparent “win” or “loss” for voter approval. With all the noise, we need an honest assessment of the economic ups and downs to help guide voters in November. First, the payroll survey shows that were 216,000 net non-farm jobs added in December, which historically is rather robust. However, that’s not even half the story. To examine how many productive private-sector jobs were added in December, we need to make some corrections. This includes subtracting 52,000 unproductive government jobs added in December as they are a burden on private-sector workers. Also, we need to subtract the 71,000 jobs that were revised down for October and November. Doing so leaves just 95,000 productive non-farm jobs added in December, which is historically weak. Couple these findings with even weaker results from the household survey showing 683,000 fewer people were employed compared with November 2023, and this report is even weaker. While the unemployment rate was unchanged from the previous report at 3.7 percent, the labor force dropped by nearly 700,000 last month, meaning fewer people had work or were looking for work. The labor force participation rate dropped to 62.5 percent, the lowest since February 2023. Contributing factors to the declining labor force participation are myriad and complex, not always correlated to the economy. But they are typically connected with expanded roles of government and other factors. For example, the Economic Policy Innovation Center recently released a report highlighting how millions of people have dropped out of the labor force. The author notes “if the employment-to-population ratio were the same today as it was before the COVID-19 pandemic in February 2020, 2.6 million more people would be employed today.” The report finds that the largest share of people leaving have been retirees since the pandemic. The next largest group is 20 to 24 years old, who have been living off the handouts since the pandemic or with their parents. Interestingly, even with skyrocketing daycare costs, those without kids are a large share of those leaving the workforce. This makes some sense as maybe they are young and don’t have kids and have other means to survive, but this also is a conundrum because they’re reducing their long-term earnings potential. But with recent minimum wage hikes by 22 states that no doubt will displace many low-skilled workers and the rise in dependency on government safety nets over the last few years, there’s likely to be more people out of the labor force for longer. Speaking of distortion, average weekly earnings have been improving, but after adjusting for inflation, they are up just 0.4 percent over the last year. While it’s promising to see real wages go up after years when it wasn’t, workers would feel much more relief if inflation were further slowed. But mischief in Congress and the Federal Reserve keeps that from happening. Inflation soared due to the federal government’s deficit spending, mostly monetized by the Federal Reserve. This created a situation of too much money chasing too few goods that resulted in persistent inflation. As purchasing power remains a problem for many Americans, workers become disenchanted with jobs, especially when the monetary benefit of government handouts exceeds wages. Reducing government spending is imperative. Doing so will help the Fed tame inflation, reignite labor force participation, and spur job creation. Celebrating wins is important, especially during the recovery after the Donald Trump lockdowns, but our leaders must not turn a blind eye to underlying problems. As we await jobs reports, we must consider the underlying issues that affect Americans directly rather than just the headlines. What we uncover might shape whether our elected leader champions free-market flourishing or leans toward the big-government ideologies our forefathers warned against.  Originally published at James Madison Institute. Florida is an economic leader because it has produced pro-growth policies of lower government spending, taxes, and regulations for years. This strong institutional framework must continue. A new report, “Reducing the Burden of Sales Taxes in Florida,” authored by The James Madison Institute (JMI) Senior Vice President Sal Nuzzo and JMI Senior Fellow Vance Ginn, Ph.D., outlines recommendations for ways in which Florida lawmakers can reduce the government burden on citizens and businesses. “Florida continues to be the best place to start and grow a business. That requires us to continually examine ways to make it more attractive as states become more and more competitive. One way our policymakers and governor can do this is by addressing the sales tax allowance, which currently places us at a competitive disadvantage when looking at other states, especially within our region. By making this allowance more reflective of how much compliance truly costs, we can ensure that the principles of limited government and economic liberty advance.” — Sal Nuzzo, Senior Vice President, The James Madison Institute “Florida has been a key model for the country with a sound approach to conservative fiscal policy. This includes the commitment to a conservative state budget, no personal income tax, minimal corporate welfare, and sensible regulation. To retain the title of “Free State of Florida” and provide more opportunities that let people prosper, policymakers should continue championing policies that spend, tax, and regulate less so families and entrepreneurs can reach their full potential. Reducing the burden of collecting sales taxes on entrepreneurs by at least doubling the sales tax allowance and streamlining the collection process to reduce compliance costs will help achieve this goal while providing lower prices to families.” — Vance Ginn, Ph.D., Senior Fellow, The James Madison Institute Podcast: Is Texas Becoming Like California? TRUTH On State Spending, Property Taxes & More1/24/2024 This BONUS episode of the Let People Prosper show is with Bradley Swail, host of the Texas Talks podcast.

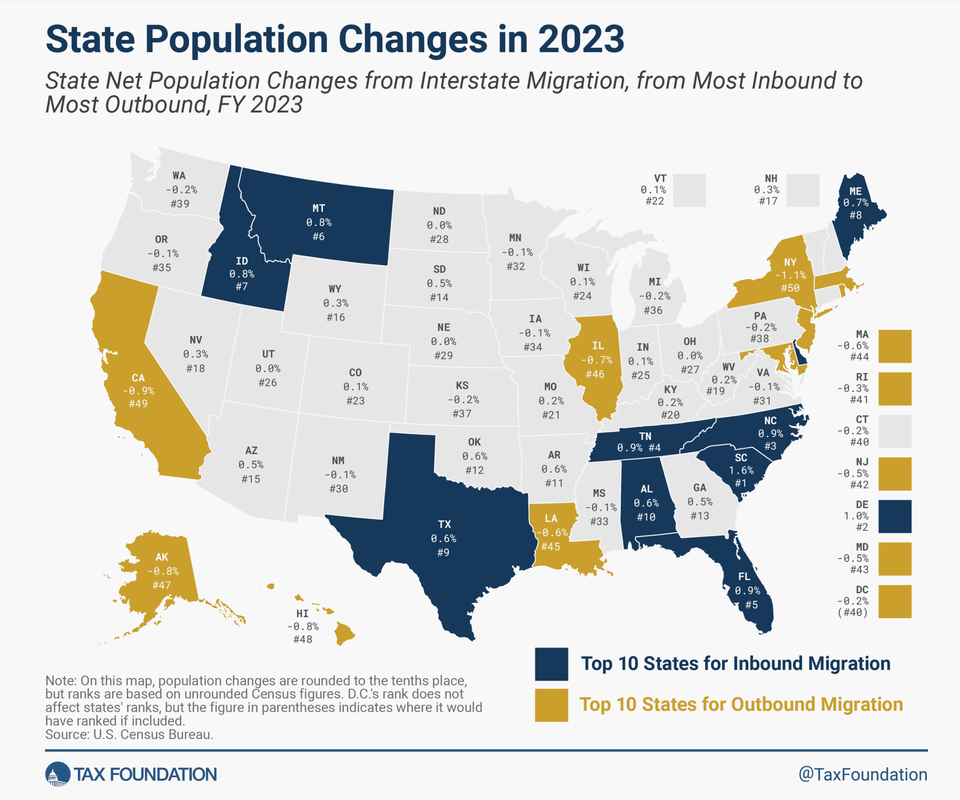

Today, we discuss: 1) Why "largest property tax relief in Texas history” became the second biggest due to excessive state spending and how the Lone Star State can eliminate the property tax for good; 2) The problem with a mandated minimum wage and reckless spending at the state and federal levels and; 3) Policies Texas leaders and lawmakers should adopt to strengthen the Texas model. Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. Also, subscribe and see show notes for this episode on Substack (www.vanceginn.substack.com) and visit my website for economic insights (www.vanceginn.com).  Originally published at Texans for Fiscal Responsibility. While the Texas economy continues to be one of the best in the country, the state must not rest on its laurels. This is because other states are becoming more competitive, and recent efforts by the Texas Legislature have headed Texas in a more progressive, California-style direction. But let’s see what the data tell us about the Lone Star State. 1) Texas had the 9th largest in-migration from other states in 2023.

Figure 1: Texas had the Ninth Best Percent Increase in Net Domestic Migration in 2023  Source: Tax Foundation

2) Texas’ labor market continues to improve but remains well below where it was in 1999.

3) Texas’ employment has been up for 43 of the last 44 months.

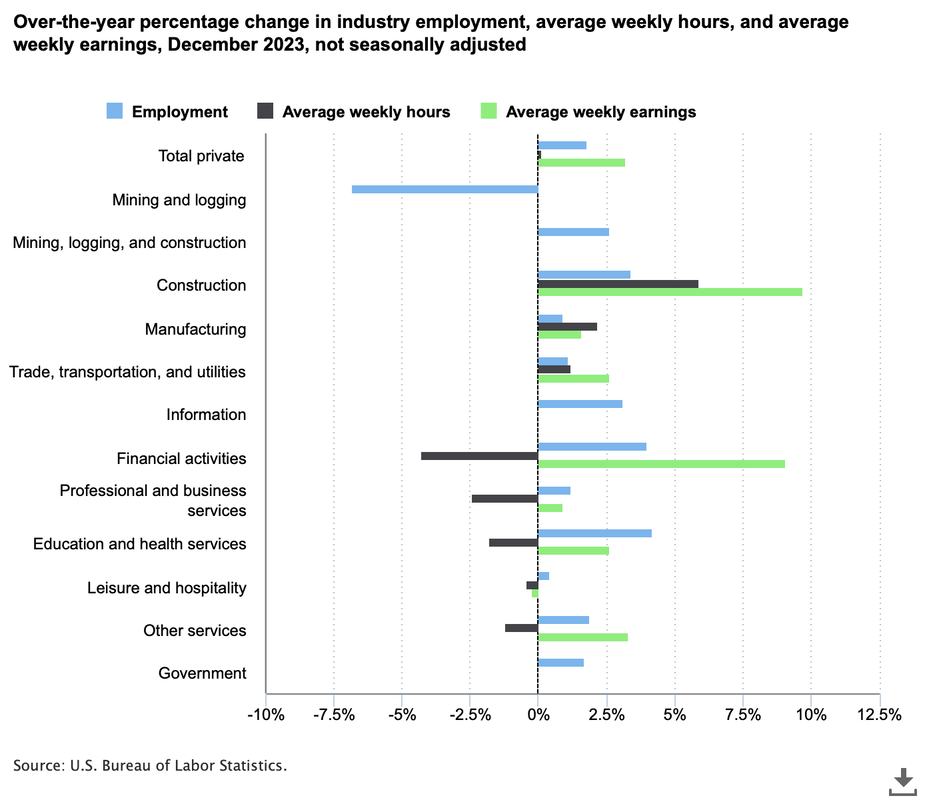

4) Texas’ workers gain jobs in most industries but some have lost purchasing power.

Figure 2. Texas’ Labor Market by Industry  Source: U.S. Bureau of Labor Statistics 5) Economic growth has picked up, but personal income lags the U.S. average.

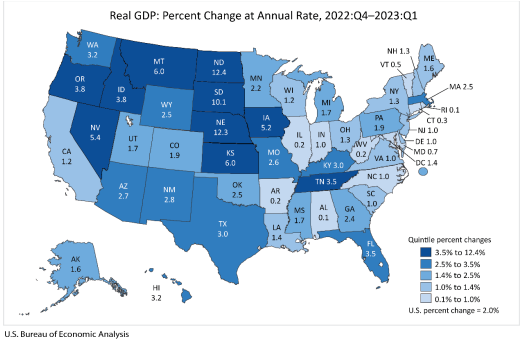

Figure 3: Real Gross Domestic Product by State in Q3:2023  Source: U.S. Bureau of Economic Analysis

Bottom Line:

These Pro-Growth Opportunities Include:

Strengthening the Texas Model will help Texans better resist D.C.’s overreach, be more competitive with other states, and, more importantly, flourish more for generations to come. Let’s start today! Today, I’m joined by Dr. Matthew Mitchell, senior fellow in the Centre for Economic Freedom at the Fraser Institute and author of the new book, “The Road to Freedom: Estonia’s Rise from Soviet Vassal State to One of the Freest Nations on Earth.” Don’t miss this website with terrific interactive information and videos on Estonia and the costs of socialism.

Today, we discuss: 1) Estonia’s inspiring people-led overthrow of socialism and achieving independence; 2) How it became one of the most economically free nations in the world; and 3) What the U.S. can learn from Estonia about taxes, regulations, freedom, and more.  Originally published at Daily Caller.

A new study from the International Monetary Fund (IMF) has ruffled assumptions, asserting that “40% of global employment is exposed to AI.” The study also predicts that high-skilled jobs will bear the brunt of this transformation, disproportionately influencing roles that traditionally require higher education and professional experience. Among advanced economies, the IMF estimates that the share of jobs affected by AI could be 60 percent. Half of them could benefit from increased productivity, and the other half hurt by replacement. The IMF concludes that the impending shift should compel countries, particularly those well-prepared for AI integration like the U.S., to implement “robust regulatory frameworks.” They argue this would help cultivate a safe and responsible AI environment with safety nets to help those whose jobs are AI “vulnerable.” But we don’t have to look too far back to realize how attempting to harness AI innovation and its results would be disastrous for people and prosperity. The rise of AI presents a unique chance for society to better adapt to challenges and capitalize on new opportunities. Humanity has always adapted to new technological possibilities, turning most disruptions into positive outcomes. For instance, dedicated professionals called “calculators” once performed complex calculations. With the emergence of pocket-sized calculators in 1971, the computing revolution began, showcasing the transformative potential of technological innovation. Those human calculators, who would today be considered high-skilled, highly vulnerable individuals, went behind the machines and created and perfected better computational technologies. Whether or not they felt threatened by the technology, they adapted nevertheless and made their skills indispensable to the technology. As the electronic calculator removed much busy work, their minds were more available to focus on tasks machines couldn’t perform. The emergence of health-related diagnostic tools like X-rays and MRIs did not render doctors less valuable but widened the breadth of their jobs. Tractors did not displace farmers but made aspects of the role significantly more accessible, allowing for higher output. The examples of technology helping humans by making their jobs easier are endless. High-skilled professionals facing AI exposure should view this revolution as an opportunity to learn and grow. Rather than advocating for regulatory barriers, individuals can proactively enhance their skills, pursue further education, earn certificates, or even explore career transitions. The power of spontaneous order in free markets lies in allowing people to innovate when not restricted by government overreach. The IMF study’s conclusion urging countries to hurriedly embrace AI regulation overlooks the resilience and adaptability inherent in free societies. Attempting to pause AI innovation is impractical in the face of rapid advancements by other nations. Our big tech competitors like China and the UAE will not inhibit progress with red tape, so why would we? We’ve already seen demonstrative instances. Recall that in June 2023, Meta launched what was, at the time, the largest open-source language model ever, Llama 2. For almost two months after that, America was the global AI leader due to this technology, only to be eclipsed by the UAE government with their release of Falcon 180b, which has more than double the parameters of Llama 2. In a matter of weeks, America lost its top spot in AI innovation. Imagine what would happen if we introduced more regulatory barriers, as suggested by the IMF, or required a pause in AI advancement, as suggested by Elon Musk and others last year. It’s not just the U.S. reputation as a world leader at stake but our very security, as we could quickly be overtaken by nations who embrace the power of AI in technology, cybersecurity, and beyond. To maintain leadership in the AI landscape, the U.S. must welcome disruptive changes and cultivate an environment encouraging competitiveness. The future belongs to those who can adapt and innovate, and AI, as a tool created by humans, should be embraced rather than feared.  Originally published at American Institute for Economic Research.

The Economist recently compared Joe Biden’s and Donald Trump’s economic records, concluding Biden wins so far. While the article raises valid points, it excludes key details that make the findings questionable. Ten months from now, there’s a high likelihood Biden and Trump could go head-to-head again for the presidency, especially after the results from the Iowa caucus. But voters should be informed about the effects of their policies on key issues like immigration, inflation, and wages. Starting with a divisive bang, let’s look at each leader’s track record concerning immigration. The Economist correctly noted that apprehensions along the southern border were much lower under Trump. They increased by the most in 12 years during the economic expansion of 2019, decreased early in the COVID-19 pandemic when people could be turned away for public health concerns, and rose again during the lockdowns. While some may see apprehensions rising between Trump and Biden as a loss for Biden, I see it as a loss for both. This metric is somewhat unreliable, given one person can be caught and counted multiple times, and those caught are a subset of total migrants. The truth is immigration is good for the economy, but government failures create unnecessarily complex barriers against legal immigration, contributing to the humanitarian crisis along the Mexico border today. Neither President has pushed for what’s needed (market-based immigration reforms) both lose. Inflation is another hot topic, especially for Biden. The Economist hands the win to Trump, as inflation was far lower during his presidency. But can we give him the credit? Remember, Trump pressured the Federal Reserve to reduce its interest rate target and expand its balance sheet, which was inflationary. His deficit spending skyrocketed during the lockdowns and was mostly monetized by the Federal Reserve, contributing to what was always going to be persistent inflation. Biden made this deficit spending and resulting inflation much worse. Add in the Fed’s many questionable decisions, such as doubling its assets, cutting and maintaining a zero interest rate target for too long, and focusing too much on woke nonsense, and we can see how this was always going to be persistent inflation. But even the Fed’s latest projections indicate it won’t hit its average inflation target of two percent until at least 2026. Likely, it will cut the current federal funds rate target range of 5.25 percent to 5.5 percent three times this year, keep a bloated balance sheet to finance massive budget deficits, and run record losses. If so, this inflation projection is too rosy. Some of Trump’s policies helped stabilize prices, including his tax and regulation reductions. But he still allowed egregious spending. Biden has doubled down on red ink that has contributed to the recent 40-year-high inflation rate. While inflation has been moderating recently under Biden, Trump gets the win. Of course, neither Presidents nor Congress control inflation, as that job is the Fed’s, but its fiscal policies influence it. When it comes to inflation-adjusted wages, The Economist grants a tie. Let’s consider real average weekly earnings that include hourly earnings and hours worked per week, adjusted for the chained consumer price index, which adjusts for the substitution bias and has been used for indexing federal tax brackets since the Tax Cuts and Jobs Act of 2017. Trump’s era witnessed a robust upward trajectory of real earnings, with considerable gains by lower-income earners, thereby reducing income inequality. We must acknowledge a real wage spike in 2020 during Trump’s lockdowns, marked by the loss of 22 million jobs and various challenges. To maintain a fair analysis, I disregard this spike. A year later, real wages demonstrated a decline under Biden. Extending the timeframe to two years later, real wages remain relatively flat to slightly increased. To provide a contextual understanding, when we consider the trend under Trump, excluding the 2020 spike, real wages for all private workers or production and nonsupervisory workers fall below those observed during Biden. It’s worth noting, however, that these wages have been higher since 2019, albeit nearly stagnant for all private workers. Given real earnings, I agree with The Economist that Trump and Biden are tied. While much more can be said for each President’s policies, continuing to add context when making assessments is crucial. I give Trump a nuanced “win” overall because his policies supported more flourishing during his first three years until the terrible mistake of the COVID lockdowns, with its huge, long-term costs. I should note that I made a strong case inside the White House for no shutdowns and less government spending but, alas, my efforts, and those by others, lost to Fauci, Birx, and Trump. Given the improved purchasing power during his presidency, Trump receives better poll ratings than Biden after three years of their presidencies. But this win doesn’t mean that Trump’s record is best regarding these issues, protectionism, and more. Let’s hope free-market capitalism, the best path to let people prosper, is on display this November, no matter who is on the ballot. Today, I reveal the TRUTH about the Iowa Caucus results, how TX expanding Medicaid for mothers will impact poverty, new data supporting the problem of government safety nets, and lots more.

I cover the following in less than 13 minutes: 1) National:

Bible Verse of the Week. Please reach out to me if I can be of service to you! Today, we discuss:

1) Why South Carolina was the fastest-growing state in 2023; 2) How SC leads the way in low supplemental poverty and abundant opportunities to prosper; and 3) Why the newly released 2025 SC Sustainable Budget would take South Carolina to the top. Today, we discuss:

1) How U.S. health care evolved away from a free-market system and the importance of restoring consumer control; 2) How to reduce health care costs and improve quality by reducing regulations and subsidies; and 3) The importance of reining in health care costs of Medicare and Medicaid to reduce government spending and balance the federal budget. I cover the following in less than 12 minutes:

1) National:

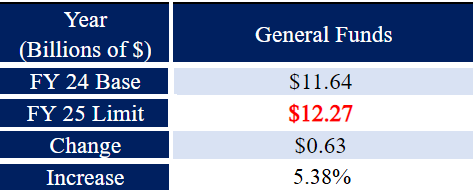

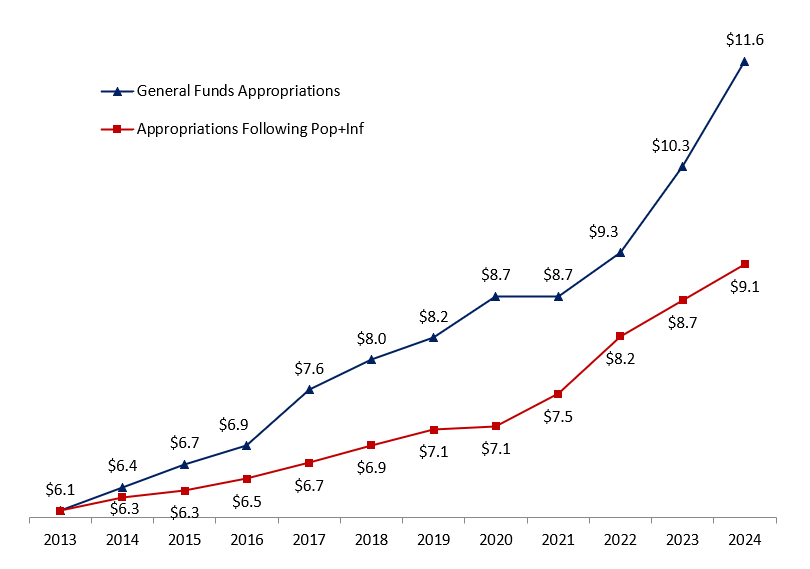

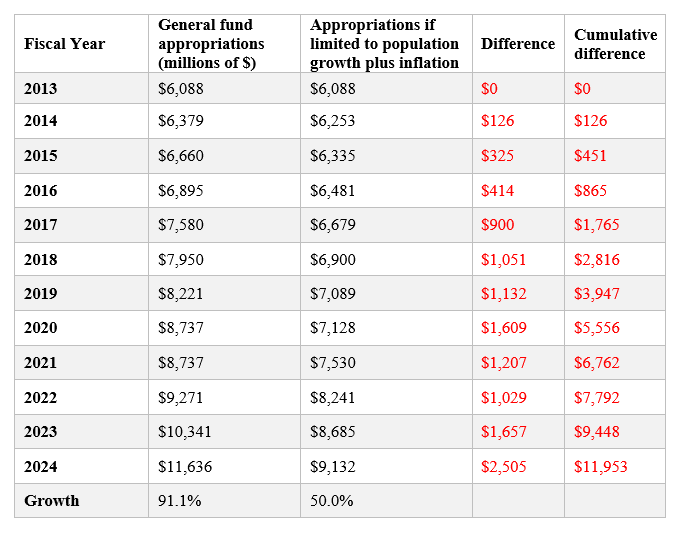

Originally posted at South Carolina Policy Council. Thanks to a robust state economy, plentiful business opportunities, and a relatively low cost of living, South Carolina remains one of the fastest-growing states in the nation. To maintain this strong position and promote further growth, it is crucial for S.C. legislators to limit state spending and reduce the government’s burden on taxpayers. The S.C. Policy Council created the South Carolina Sustainable Budget (SCSB) to assist in this effort. The SCSB is a maximum limit on annual recurring general funds[1] appropriations based on the rate of state population growth plus inflation. First published in 2022 and again in early 2023, it has served as a data-driven resource to help rein in unsustainable spending and provide more opportunities for tax relief. Unfortunately, the state did not adhere to the SCSB limit of $11.20 billion for its fiscal year (FY) 2024 budget; instead, it appropriated $11.64 billion – a 12.56% increase above the FY23 base of $10.34 billion. To turn the tide of excessive budget growth and provide more room for tax relief, the Policy Council is issuing its third SCSB. Table 1 provides the results outlined in this report for the FY25 SCSB. Table 1. The FY25 South Carolina Sustainable Budget for Appropriations of Recurring General Funds  Based on population and inflation data in 2023, the recommended recurring general funds appropriations limit[2] for South Carolina’s FY25 budget is $12.27 billion. With inflation moderating somewhat since reaching a 40-year high in 2022, primarily because of the errant policies in D.C., the SCSB ceiling is higher than it would be under normal economic circumstances. For example, the average annual rate of population growth plus inflation since 2013 has been 3.78%. Accordingly, the S.C. Legislature should consider freezing spending at the current FY24 budget of $11.64 billion. This would help correct recent overspending in the state’s budget and help put the state on a more sustainable budget path. It would also leave more money available for needed tax relief. At a minimum, recurring general fund appropriations in the FY25 budget must remain below $12.27 billion. Overview A sustainable budget – sometimes called a conservative or responsible budget – is a model for state budgeting that sets a maximum limit on appropriations or spending based on the rate of population growth plus inflation. This metric serves as an indicator of what the average taxpayer can afford to pay for government provisions. It accounts for 1) More people in the state who could potentially pay taxes; 2) Wage growth that’s typically tied to inflation over time to pay taxes; and 3) Economies of scale, as not every new person or wage increase should be associated with new government spending. The SCSB does not make specific recommendations on how general funds should be appropriated in the budget. Instead, it gives legislators the flexibility to appropriate taxpayer dollars to government programs as determined by the General Assembly, while ensuring that spending growth remains in line with what people can afford. Such a voluntary spending limit is key to putting South Carolina in a position for further tax relief. In 2022, Gov. Henry McMaster and lawmakers enacted the first-ever state personal income tax cut, which immediately reduced the top rate from 7% to 6.5% and collapsed the lower bracket to 3%. It also scheduled additional yearly 0.1% cuts to the top rate until it reaches 6%, though general fund revenues must project at least 5% annual growth for the cuts to trigger. The problem with this approach is that it relies on continued revenue growth to deliver incremental tax relief. Following the SCSB would help to accelerate this process, freeing up revenue to buy down the top rate to 6% immediately and fueling other tax cuts. On the other hand, unsustainable spending could build pressure to reverse course and raise taxes, leaving South Carolinians with fewer opportunities to flourish. SC Appropriations vs. Sustainable Budget Figure 1 compares the previous twelve years[3] of South Carolina’s recurring general fund budget appropriations (FY13 to FY24) to those appropriations when limited each year to the rate of population growth plus inflation. Figure 1. South Carolina General Fund Appropriations v. SCSB 12-year GF appropriations: $98.5 billion (+91.1%) 12-year GF appropriations limited to population growth + inflation: $86.5 billion (+50.0%)  Notes. Budget amounts are based on data from South Carolina’s state budget publications, Fed FRED for state population growth and U.S. chained-CPI inflation, and authors’ calculations. Appropriations did not increase from FY20 to FY21 because the state operated on a continuing resolution in FY21.[4] Key takeaways (see Table 2):

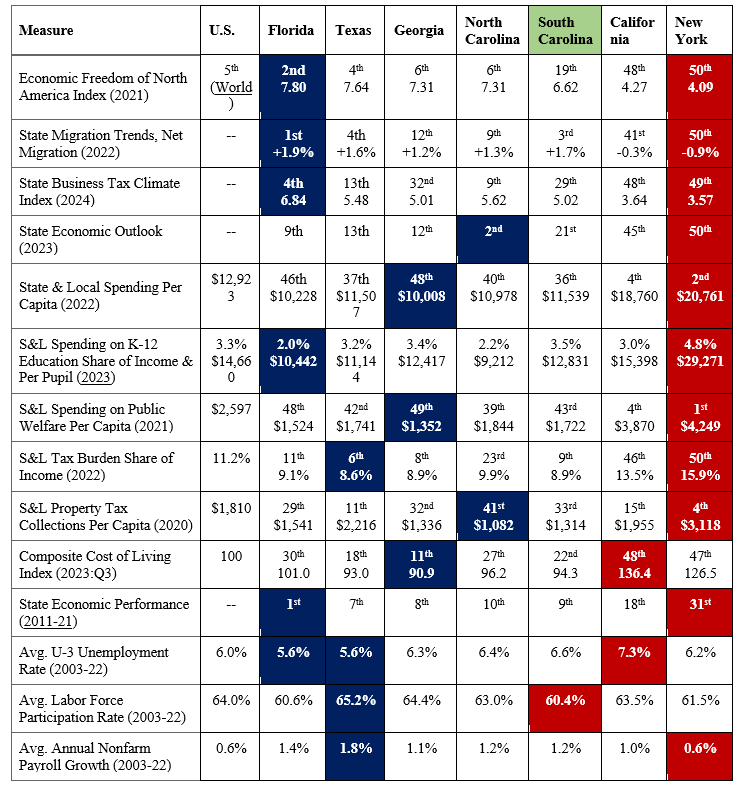

Note. Budget amounts are based on data from South Carolina’s state budget publications, Fed FRED for state population growth and U.S. chained-CPI inflation, and authors’ calculations. These data provide clear evidence that there is room for the state to limit spending growth to reduce taxes substantially. South Carolina has been one of the 25 states in the last three years to cut income taxes, which has helped the state improve compared to its neighbors. However, North Carolina recently passed legislation that could eventually bring their income tax rate to 2.49%, which would be the lowest in the country, excluding the seven states without personal income taxes. On that list are Florida and Tennessee, two major competitors for jobs and investment in the Southeast. South Carolina could improve its position by passing sustainable budgets and using the surplus revenue to cut taxes, especially income taxes. See Table A in the Appendix for more comparisons of South Carolina with other states. Follow the SC Sustainable Budget We strongly encourage legislators to follow the SCSB when drafting South Carolina’s FY25 budget. As a data-driven resource, the SCSB sets a clear spending limit based on what the average taxpayer can afford to pay for government services. Surpassing this limit will fuel excessive government growth and promote unsustainable spending, leaving less revenue that can be used to lower taxes. Recent budget projections show a historic opportunity for tax relief – if legislators are willing to take it. In its November 2023 forecast, the S.C. Board of Economic Advisors (BEA) estimates a recurring budget surplus of $673.1 million for FY25. It also projects the cost of lowering South Carolina’s top personal income tax rate from 6.4% to 6.3% to be roughly $100 million (which is accounted for by BEA prior to their $673.1 million projection). Based on current data, we estimate[1] it would cost an additional $300 million in revenue to cut the top rate immediately to 6% in the new budget. Accordingly, this all-at-once cut could be achieved using less than half of the projected recurring surplus. Passing a sustainable budget would be easier if state agencies followed South Carolina’s legal budget process. Under current law, agencies are supposed to justify every dollar they are requesting when submitting their annual budget plans to the governor – explaining why both new and current programs deserve taxpayers’ money. The law follows a concept known as zero-based budgeting, where all expenses need to be justified annually based on need and performance without regard to previous budgets. Despite this legal mandate, agencies only provide details for new spending requests each year. Fortunately, South Carolina is decently prepared for a rainy day should it occur. Voters in 2022 approved two amendments to increase contributions to the state reserve funds – raising the General Reserve Fund from 5% to 7% (over several years) and the Capital Reserve Fund from 2% to 3% of the previous year’s general fund revenue. By law, the reserve funds act primarily as a shield against year-end budget deficits. While these reserve funds are important to withstand volatility in the budget, lawmakers should focus on limiting or cutting the budget for it to be sustainable over time. Conclusion Following the SCSB will put South Carolina in a better position to reduce taxes, avoid the cost of excessive government growth, and give citizens more opportunities to flourish. Had this been done since 2013, the state could have substantially lowered personal income taxes, if not eliminated them. Fortunately, the upcoming budget provides state leaders with another crucial opportunity to rein in spending and deliver much-needed relief. South Carolina taxpayers are counting on it. Appendix: How Does South Carolina Compare with Other States? Table A shows how South Carolina compares with the largest four states in the country (i.e., California, Texas, Florida, New York) and neighboring states (i.e., Arkansas and Mississippi) based on measures of economic freedom, government largesse, and economic outcomes. Table A. Comparison of States for Measures of Economic Freedom and Outcomes  Notes. Dates in parentheses are for that year or the average of that period. Data shaded in blue indicate “best,” and in red indicate “worst” per category by state.

These rankings show that South Carolina is better than most states in terms of economic freedom, but is substantially less economically free than its neighbors of Georgia and North Carolina. South Carolina does better than others in this comparison in terms of having the lowest supplemental poverty rate and near the best in net migration. South Carolina has the highest state and local government spending per capita among its neighbors and a substantially worse business tax climate than North Carolina. The data show that states with less economic freedom (e.g., New York, California, and South Carolina) tend to perform economically worse. On the other hand, those states with more economic freedom (e.g., Florida, Texas, Georgia, and North Carolina) tend to perform economically better. Given these comparisons, South Carolina has much room for improvement to be more competitive and, more importantly, provide more opportunities for human flourishing.  On January 1st, 22 states and 38 cities and counties raised their minimum wages, sparking some celebration for 10 million workers who get a pay hike, and many doubts for the rest.

While this is perhaps a well-intentioned policy, intentions don’t indicate a policy’s effectiveness. Many economists argue that this decision will disadvantage the people it aims to help, namely, lower-skilled workers. Minimum wage hikes aim to make it “livable,” an increasingly frequent discussion due to government-created rampant inflation in recent years. I don’t disagree that $7.25 hourly, the federal minimum wage matched by many states, is insufficient for most to afford necessities. But helping lower-skilled workers move up the economic ladder is more complex than governments arbitrarily raising wages. Because I want to see everyone flourish, especially the neediest among us, I’m against a minimum wage and definitely against increasing it more. Elevating the minimum wage this drastically and suddenly will lead to widespread job losses, because employers must balance profitability with labor that costs more but adds no higher output. The spate of layoffs by major corporations in 2023, driven by slowing sales exacerbated by decreased purchasing power, demonstrates this reality. Now, envision a scenario where these higher-paid retained workers burden employers. Rather than a boon, this often translates into more layoffs or price hikes as companies seek to maintain profitability. The optimistic projection by the Economic Policy Institute, suggesting a $6.95 billion windfall for workers from the recent state minimum wage increases, rests on a questionable assumption that every worker will retain his job. In reality, employers may resort to cost-cutting measures to stay profitable, jeopardizing quality and output, and ultimately resulting in layoffs. If an employer must pay someone $16 hourly, the new minimum wage in New York and California, whom will they pay? Would it be a higher-skilled college graduate or a less-skilled worker with only a high school diploma? You can deduce which hire is the safer option. When the cost of obtaining more education or skills is higher than the cost of relying on government unemployment benefits, dependence becomes the more appealing choice over labor-force participation. Another often-overlooked negative impact of minimum wages is decreased negotiating power. When workers with qualifications and experience who merit higher pay are confined to a predetermined minimum wage, their bargaining potential is stifled. These labor market dynamics, however, extend beyond individual choices. The intriguing patterns in state migration rates underscore how higher minimum wages deter people from seeking better opportunities. Look at California and New York, champions of minimum wage increases. Both experienced some of the highest rates of outmigration in 2023. Conversely, with their comparatively lower minimum wages, Texas and Florida witnessed a substantial influx of new residents. People vote with their feet. The allure of better prospects, lower living costs, and increased job opportunities in states with few-or-no minimum wage hikes outweighs the appeal of higher minimum wages in other states. States with lower minimum wages continue to increase in appeal because, contrary to popular belief, only a very small share of hourly paid workers earn minimum wage, and not for long. Professor of Economics at UC San Diego Jeffrey Clemens’ findings reveal that most minimum-wage workers experience consistent wage growth over time. According to his research, over 12 months, about 70 percent of individuals studied initially employed at or near the minimum wage saw an improvement in their earnings, with an average wage increase of $1.39. The data suggest that the narrative surrounding the persistence of “career minimum wage workers” applies to very few people. But even so, those low-wage jobs maintain value. Low-wage positions, typically entry-level or part-time jobs, serve as the initial rung toward better opportunities with higher pay. Unfortunately, governments inadvertently eliminate many of these essential entry-level jobs by advocating for higher minimum wages. This lost first rung has profound consequences, especially for vulnerable groups like young individuals, part-time workers, the unmarried, and those without a high school diploma. Such individuals rely on these low-wage positions for income and to escape the cycle of government dependency and poverty. Employers and workers alike deserve freedom. Burdensome government regulations that hinder free-market flourishing culminate in the mandated minimum wage, which stifles opportunity rather than allowing spontaneous order to create jobs and economic growth. The states that just increased the minimum wage will experience more problems than they’ve already created. People will continue to vote with their feet. Hopefully, leaders at federal, state, and local levels will come to grips with the best paths to help people prosper, however unpopular those paths may be. These paths that improve productivity to demand higher market wages and increase output to supply higher-paid jobs are found in an institutional framework of free-market capitalism. Specifically for the labor market, politicians should provide universal school choice, remove government obstacles like occupational licensing and forced union dues, rein in spending to cut taxes, and reduce regulations. In short, more government isn’t the answer to higher wages because government is the problem. Let’s not double down on government failures. Originally published at AIER. Episode 78 is with Adam Thierer, innovation policy analyst at R Street Institute and author of, “Evasive Entrepreneurs and the Future of Governance: How Innovation Improves Economies and Governments?"

Today, we discuss: 1) What makes nations rich and how America has become the most prosperous nation on earth; 2) The economic importance of failure, freedom, and permissionless innovation; and 3) Why AI and technology must be embraced, and the issues with Biden's AI executive order. Check out Adam's book: https://www.amazon.com/Evasive-Entrepreneurs-Innovation-Economies-Governments/dp/1948647761/ref Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. Also, subscribe and see show notes for this episode on Substack (www.vanceginn.substack.com) and visit my website for economic insights (www.vanceginn.com).  We must learn from history or be doomed to repeat it. This includes honestly assessing the economy in 2023 so that we have better information for making decisions in 2024.

Starting with a bang on many people’s minds is housing affordability. The year commenced with a surge in the average 30-year fixed mortgage rate from 6.5% in January to nearly 8% in October but has declined recently to about 6.6%. These higher mortgage rates and record-high housing prices contributed to an unaffordable housing market. While existing home sales were up 0.8% in November, they are down 7.3% over the last year, indicating a struggling housing market for families that will unlikely improve much in 2024. Another concern is costly inflation. Rampant hikes in the cost of a typical basket of goods and services have meant less purchasing power for us. This contributes to making housing, food, education, and other expenses for that basket less comfortable or worse for many families. As of November 2023, the core consumption personal expenditures increase was 3.2% year-over-year. This price measure of a basket of goods and services excludes food and energy and is what the Federal Reserve prefers to watch. While core PCE inflation has moderated from close to 6% in 2022, the recent 3.2% inflation rate remains 60% higher than the Fed’s average inflation target of 2%. Although moderating inflation represents some relief for many Americans, the challenge is that average weekly earnings adjusted for core inflation declined in 23 of the last 35 months since January 2021. In total, these real average weekly earnings are down 0.8% since then, indicating why inflation is a top concern. An additional problem is debt. Because earnings haven’t been keeping up with inflation, credit card debt soared to more than $1 trillion as people struggled to make ends meet, which is a bad sign for 2024. And many people have been going through their savings and retirement funds quickly. What about jobs? The White House recently celebrated “total job gains achieved under the Biden administration reached 14.1 million through November 2023.” But this metric becomes less impressive considering that 9.4 million of those jobs were just recovering jobs lost during the pandemic lockdowns. So, there have been 4.7 million new jobs added since January 2021, which is 134,000 per month. While this is positive, it is not record-breaking. The weaker labor market in recent months indicates that 2024 could be tough for many workers. Most people’s pocketbooks did not grow but diminished this year, and the job market similarly lags. But what about the nation’s overall growth? Hasn’t GDP soared? Not exactly. In the third quarter of 2023, the annualized real GDP growth hit 4.9%, which appears robust. But when you dig into the details, it’s more complicated. Government spending, which is a drag on the economy as it must take taxes from the private sector and distort market activities, threw in 0.99 percentage points. And private inventories, influenced by the whims of fluctuating interest rate expectations, chipped in 1.27 percentage points. When you exclude those contributions to consider stable real private GDP, there was just a 2.6% bump up. This slower pace didn’t just pop out of nowhere. It’s been a saga since early 2022, when we hit a two-quarter decline in real gross domestic product, waving a big red flag for a recession. And when you consider the valuable metric of real gross domestic output, which is the average or real gross domestic product and real gross domestic income, the economy has declined in three out of the last seven quarters. While these economic issues suggest stagflation triggered by misguided pandemic lockdowns and subsequent trillions of new money printing of deficit-spending, there may be some relief. The Fed’s slow correction to its bloated assets of $9 trillion at its peak to $7.7 trillion contributed to interest rates soaring since March 2022. But with Congress continuing to deficit spend of about $2 trillion per year and net interest payments soaring to $1 trillion per year, there are massive economic challenges ahead. These deficits will make it more difficult for the Fed to correctly normalize its assets quickly to get them back to at least the pre-pandemic $4 trillion. This is because the budget deficits would contribute to higher interest rates, so the Fed will likely monetize the debt more to help Congress avoid needed spending restraint. While these truths are tough to swallow, many beacons of hope also emerged throughout the year that should be noted. In 2023, a momentous shift unfolded with a transformative surge in educational choice. Twenty states expanded school choice, and a record-breaking 10 states passed some form of universal school choice, making 36% of American students eligible for a private choice program. Some states have been slow to increase educational freedom, but this revolution’s overall impact is historical. Recognizing that children are the cornerstone of our nation’s future and acknowledging that improved education is a pivotal predictor of their success, the catalyst for change is undeniably rooted in more universal school choice. The second bright light is the flat state tax revolution. Many states took bold steps to enhance their economic landscapes. Notably, prominent states like California and New York faced ongoing out-migration as individuals sought refuge from progressive policies, and less heralded states embraced free-market principles, propelling them onto the national stage. More conservative Florida and Texas continued to lead the way in places where people moved in 2023. The third thing to cheer is a responsible movement toward a sustainable state budget revolution. Some states are pushing toward improving their spending limits to one that covers more of the budget, limits budget growth to no more than population growth plus inflation, and has a supermajority vote to bust the limit or raise taxes. The synergy of these reforms demonstrates the power of federalism as states experiment with policies, revealing effective strategies and fostering a healthy laboratory of competition. We need lawmakers at the federal, state, and local governments to recognize what works and implement them. The trajectory in 2024 and beyond hinges on embracing free-market capitalism, which is the best path to let people prosper. This includes less government spending, less money printing, more school choice, and more tax relief. In short, less government. That’s how we get a more prosperous 2024. Happy New Year! Originally published at Econlib. |

Vance Ginn, Ph.D.

|

RSS Feed

RSS Feed

{kind=link}

Proudly powered by Weebly