|

Today, I am joined by Dr. Kevin Kosar, senior fellow at the American Enterprise Institute (AEI) and writer of the foreword to the latest edition of Edward Banfield’s book, Government Project.

Kevin explains why government projects don’t work and the following: - Why does the federal government tax and spend so much? - How are some government projects better than others? - What should the future be of work? Please like this video, subscribe to the channel, share it on social media, and rate and review it. I would appreciate it if you would subscribe to my Substack newsletter so you’ll receive my episodes, show notes, and other valuable insights in your inbox twice weekly at vanceginn.substack.com.

0 Comments

Originally published at AIER.

April heralds two markers in Americans’ financial calendar. Neither brings joy. Their anguish reminds us of the dire need for fiscal reform before it’s too late. The first day is Tax Day on April 15, when you must file taxes to the IRS. The other day is Tax Freedom Day on April 16. The latter is the 104th day of the year, which represents when Americans, on average, can stop working to pay taxes and start working to improve their own lives and further their economic goals. We work 30 percent of our days to pay government alone. This stark division of the year into earning to pay for the government versus for oneself casts a revealing light on taxation’s burden. These dismal dates indicate an urgent need to overhaul the fiscal regime of excessive government spending that drives taxes higher. The pain and uncertainty from an ever-changing federal progressive marginal individual income tax system with forced withholding and payment or refund later are destructive. These costs distort our ability to prosper. Central to minimizing these burdens and distortions is for the federal government to spend less, thereby reducing the amount needed from taxes. And the tax system should be simplified by moving to a broad-based, flat-income tax. Eventually, we could eliminate income taxes and fund our significantly reduced spending with a broad-based, flat final sales tax, but politics too often takes precedence over prudence. States without personal income taxes, such as Texas and Florida, often showcase stronger economic performance, underscoring the potential benefits of a consumption-based tax model. The Tax Foundation’s analysis shows that these states enjoy higher growth rates and attract businesses and residents alike, advocating for the efficiency of a less burdensome tax system. Unlike taxes on income, a consumption tax better aligns with economic volatility and taxpayers’ decisions. It introduces a transparent, simpler tax system, starkly contrasting the current convoluted income tax code, thereby supporting more freedom to choose, increased savings, and faster economic growth. But the looming uncertainty inevitably generated by temporary tax measures and seemingly endless, excessive government spending demands attention. For instance, the individual income tax rate reductions, full-expensing, and other provisions of the Tax Cuts and Jobs Act (TCJA) of 2017 expire over the next year, creating a cloud of uncertainty. Moreover, the multi-trillion-dollar deficits from overspending result in further economic destruction because of higher interest rates and less investment. The economic impact was notable, with the Congressional Budget Office reporting a surge in GDP growth following the TCJA’s implementation. But the uncertainty surrounding its future dampens long-term economic prospects and investments. Permanent tax reform, aimed at fostering stability and growth, requires a commitment to fiscal discipline and a reevaluation of government spending priorities. The erratic nature of such spending and tax policies erodes the stability crucial for economic prosperity. Uncertainty, particularly around taxes, inhibits investment and innovation. Predictability is key to strategic planning and growth. For entrepreneurs, uncertainty is a strong disincentive. The fluctuating tax landscape presents a significant barrier to economic expansion. Addressing this uncertainty requires permanent growth-oriented tax policies and controlling government spending. The direction of tax reform must be twofold: advocating for broad-based, flat taxes and championing sustainable government budgets. This dual approach promises to enhance economic liberty and lay a foundation for robust growth, which should also reduce the number of days to Tax Freedom Day so more money is in our pockets. Reflecting on Tax Day and Tax Freedom Day sparks a broader discussion on tax reform. We can envision a society that values freedom, peace, and prosperity by championing pro-growth policies of a simplified, flat tax system and sustainable spending. Dispelling tax uncertainties and controlling government spending pave the way for economic policies that foster rather than hinder human flourishing. The journey toward a more rational tax system is not merely fiscal; it’s a moral imperative. It demands bold, persuasive advocacy for policies that champion economic soundness while embracing the principles of liberty and opportunity. We can inspire a movement toward genuine economic reform on this Tax Day by addressing the challenges posed by the current tax code and advocating for a shift toward a better fiscal regime with more days working for ourselves instead of Uncle Sam.  Thirteen years ago today, I was a graduate student in the doctoral program at Texas Tech University and had just finished judging an undergraduate research poster competition. I was riding the bus back to my apartment when I received a horrible phone call from my mom. She said my dad has passed away in his sleep from SUDEP (Sudden Unexpected Death in Epilepsy: http://www.epilepsy.com/learn/impact/mortality/sudep).

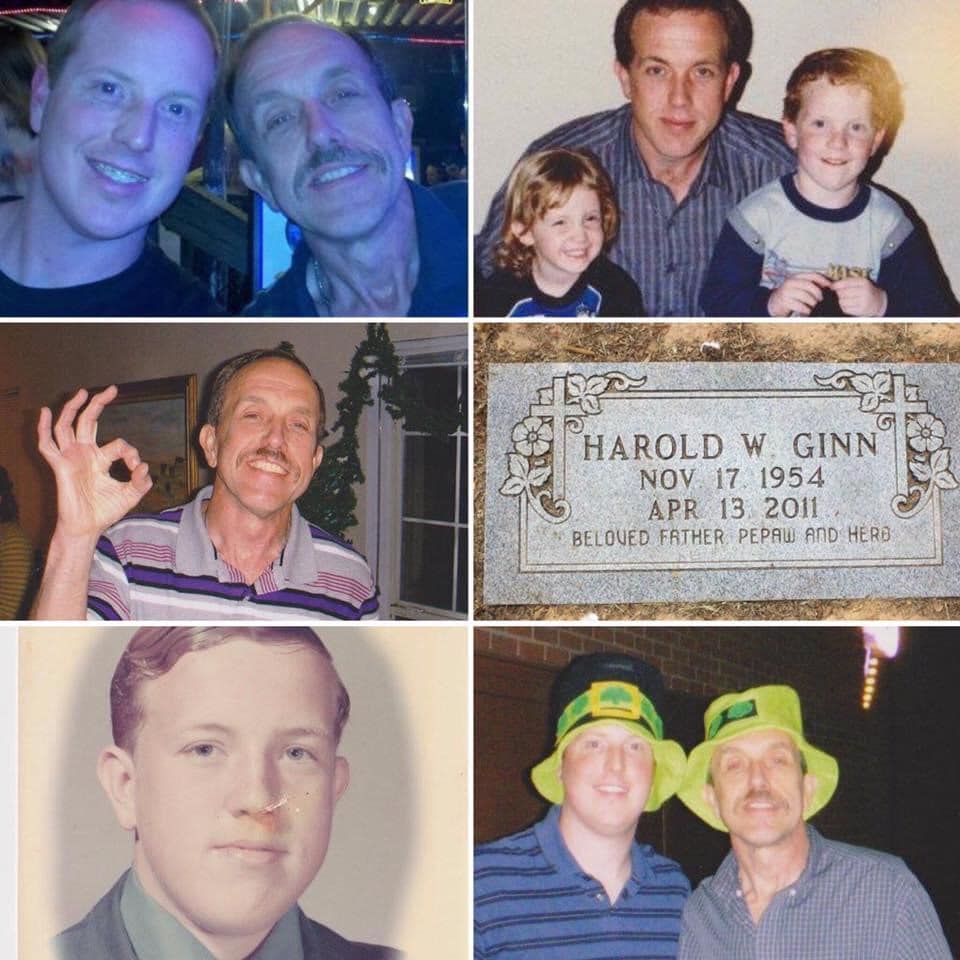

We will come back to that. But first let me tell you about this remarkable person and how he got to this point. One day in 1972, when my dad was 17 and had just left a place in Brookshire, Texas, my dad was in a terrible traffic accident. He was a passenger in a truck that was struck by what we believe was a drunk driver who had seemingly run a red light. The result was that he had a severe head injury. Little did he know it would change his life forever. After weeks in a coma and after the doctors telling his family he may not live, my dad woke up and worked every day to live a "normal" life. Without any memories before the wreck (amnesia) and short-term memory loss thereafter, he battled not knowing anyone in his classes, not knowing he was class president, not knowing he was president of his school's National Honor Society, not knowing he was a football player, and much more. To this day, I still don't know much about him before the wreck. He once shared a story with me of how he was sitting in class after he returned to school and the principal called someone over the loudspeaker. His friend tapped him on the shoulder and told him that he was just called—he periodically didn't know his own name. He was taken to a room for a National Honors Society meeting and told he should sit at the head of the table. He asked why. They said he was the president and would lead the meeting. Of course, he was unable, but the level of respect he had at Royal High School in Brookshire, TX is remarkable. This is one of many similar stories. Let me tell you more. Time passed and he went to school at Sam Houston State University for three years to study drafting before his memory declined so much he started making Bs, Cs, and eventually failing classes, all of which were the first time, I believe, that he earned less than an A. He had to drop out but took what he learned to be a productive draftsman. He would eventually sometimes work two jobs to pay the bills for the family. He later worked at a gas company, Entex, in Houston checking gas meters. He fell in love with my mom while they were living in Brookshire, TX, and they soon married. They were happy and lived life like any other newly married couple would. My dad acted a little strange from time to time, which is why his nickname was "Weird Harold," but not much else seemed wrong. Then in the mid-1980s, something started to change. He started having small petit mal seizures (he would stare into space without being able to speak and would smile big for no reason). No one paid attention the first few times. Eventually, he started having grand mal seizures (features a loss of consciousness and violent muscle contractions; it's the type of seizure most people picture when the person falls to the ground and convulses). He was in and out of hospitals after having grand mal seizures twice per month or even more frequently. After a couple years and wrecking three cars, one while working at Entex (now Reliant Energy), he reluctantly filed for disability in 1987 and never worked or drove again. This crushed him and the numerous drugs he was on and lack of ability to remember things put pressure on his psyche and my parent's marriage—they eventually got divorced, remarried, and divorced again when I was young. He lived off and on with us to help pay bills or with his mom, mainly with my granny during most of my childhood. When he was at home, we would play baseball in the backyard or at Wilson Park and basketball in the front yard for hours. I have so many great memories of those times. He would go over my schoolwork with me while I was in home school. He was a math guru and taught me tricks along the way. He listened to me beating on the drums when I had little clue how to play and later would go to my rock concerts when I was in the band Sindrome. I remember picking him up from his mom's and taking him to the neurologist, Dr. Neumark, at St. Luke's Hospital in Houston's Medical Center for years. I learned much about epilepsy, and how it can affect someone's life from reading books, watching my dad have hundreds of seizures over my lifetime, and talking with him about the struggle he had to deal with his situation. He took roughly 12 pills per day and had a vagal nerve stimulation surgically implanted near his chest that would send electronic impulses to his brain to help him have fewer seizures. It helped reduce the seizures over time from two per month to about one every 3 or 4 months. He would keep track of all his seizures and I remember how proud we were when they were less frequent. Each time he had one he would be exhausted for several days. He was always energetic and in a fairly good mood, so after he had a seizure, it was very unlike him to sit around most the day and not talk much. During my days at Tech, I visited home, South Houston, about twice per year (9-hour drive is too long to visit often). While I was home, I would take dad out as much as possible and play pool, watch Astros games, and have fun. Without the independence to drive and few friends to take him anywhere, he spent most of his time at home and I tried my best to get him out and enjoy the world. He never complained about his situation. He did voice frustration that he couldn't drive or do things others could do, but for the most part, he lived a normal life and could do anything he wanted. Years passed and he moved in with a friend and me in a townhouse in Lubbock on June 1, 2008. It was my second year of graduate school. We would go eat breakfast in the mornings when I didn't have class. We would go for long walks and talk about my research, politics, and the meaning of life. That was how he relaxed; he would go on long walks. There was nothing better for him than being with family or alone with nature. He could get away from the thought of being disabled or feeling trapped in a body that kept him from doing the things he wanted. After I moved in with Emily, dad got an apartment in the same complex about 30 yards away. It was the first time he ever lived on his own and had a sense of independence since that cloudy day in 1972 when his life changed forever. We would barbecue together and he would visit us often. I am so thankful he had the opportunity to know Emily and she will have memories to tell our two sons (oldest has dad's middle name) and daughter. Dad and I had many great memories together in Lubbock. He had some complications with his epilepsy and I stayed in the hospital with him for a week as they did a number of tests to see if they could surgically repair the place on his brain that caused the seizures. They determined it was too risky because it was near the part of your brain that controls your speech and he went on with his life. After two and a half years (in December 2010) living near me in Lubbock, dad moved to Houston to live with my sister, Tiffany, and her family. He was excited about living with them and being around his grandkids, but he was upset about leaving his life in Lubbock. Although I missed him every day, I knew he was happy and everything seemed fine. Then that day came in 2011 when I was on the bus that I received the phone call from my mom. My mom said Tiffany had checked on dad after he seemed to be sleeping unusually late. She found him lying there, not breathing. My first reaction was to my mom telling me he wasn’t breathing was: Why not? What are you doing about it? Is he at the hospital? My mom had few answers other than: "Vance, he passed away." It was the first time that I had someone close to me die. The person that I did not live with much growing up, didn’t know much about his childhood, but had got to know much more during the previous two-plus years had suddenly, without any warning, passed away! I was crushed. I screamed uncontrollably at the front of a packed bus and ran off the bus to my truck as soon as it stopped. I sobbed driving home and frantically paced back and forth around my apartment when I made it home. My dad, one of my best friends, and the person I learned so many lessons from was taken from me. How could I go on? So many things raced through my head and I hoped that I would soon wake up from this nightmare. A truly life-changing event challenged me in ways that I’ve never been challenged. To this day, that moment still gives me chills and makes me teary-eyed. Dad died from what is known as SUDEP (Sudden Unexplained Death in Epilepsy). My sister said that he went to sleep the night before without signs of anything wrong. The best explanation from doctors that we have is that he went to sleep, had a seizure, and his organs shut down. It was not painful and he probably did not know anything was going on. Doctors say that even if he was in the hospital there would be little chance they could have saved him. There is little known about SUDEP and what triggers it, which is why we allowed an autopsy and continue donating to the Epilepsy Foundation today. Somehow, someway, God has a mysterious way of working in our lives. Prayer, family, and friends helped me through the hurt. Days, weeks, months, and years later I find myself weeping over the loss of my dad. To this day, I feel deep sorrow. However, I think about the numerous lessons I learned from my dad during my 29 years around him and treasure the many memories. He loved music. He would sing to classic rock songs and loved Journey, Elton John, and many others. He would snap his fingers when dancing and would clap when listening to music. Music helped him release his worries, along with walking. He also loved playing pool. A man with what some could consider so little left to live for had so much courage to take on the world. No complaining and no handout. He would work every day if he could. Love others unconditionally and never give up is what I take from his life. There are too many who have less and live with many more problems than we do. If my dad can take on the world with his faith in God and his ability to see the sun shining with so many clouds around, it is easy to find hope and find beauty in this world. There is so much for us to be thankful. Thirteen years have passed. Years that I will not be able to tell him the wonderful things that have happened in my life and those in the family. However, I have faith that he knows. I believe he is still watching over us and that we will see him again someday. I believe he is with my kids, me, and the family always. His bright smile is the picture in my head that I see and it fills the hearts of all those who knew him. Years pass in a flash, but my dad's memory will live on. Harold Wayne Ginn was a wonderful father, pepaw, and hero. He will always be our family's hero. There is so much to say. His life is a testimony that I hope will bring joy and a stronger faith for others. I know it does for me. I know he was a Godly, kind, smart, generous, loving, sweet, caring, empathetic, and more man. Thank you, Dad! I love you. In “This Week’s Economy” episode 56, I discuss the following and more in 13 minutes:

- What did the latest jobs and inflation reports tell us about the Fed’s next steps? - How should states advance pro-growth policies? - Why did the Teamsters Union block autonomous vehicles in Kentucky? Please like this video, subscribe, share it on social media, and rate and review it. I would appreciate it if you would become a subscriber to my Substack newsletter so you’ll receive my episodes, show notes, and other valuable insights in your inbox twice per week at vanceginn.substack.com. You can also find this information and more at vanceginn.com. Interview on Fox 5 in DC.

The economy added 303,000 new jobs in March, a number that President Biden touts as a sign his policies are working. What does this mean for inflation, and interest rates? Jim breaks it down with economist and former White House associate OMB director Vance Ginn on The Final 5. Today, I am joined by David Bahnsen, founder, managing partner, and chief investment officer of The Bahnsen Group and author of his latest book, Full-Time Work and the Meaning of Life.

David provides valuable insights on these issues and more on the following: How does full-time work provide meaning in life? What does the Bible say about work and a free and virtuous society? How does the government create barriers to work, and how should we remove them? Please like this video, subscribe to the channel, share it on social media, and rate and review it. I would appreciate it if you would subscribe to my Substack newsletter so you’ll receive my episodes, show notes, and other valuable insights in your inbox twice weekly at https://vanceginn.substack.com/. You can also find this information and more at https://vanceginn.com/ .  Originally published at Freedom Conservatism.

Vance Ginn is the founder and president of Ginn Economic Consulting and host of the “Let People Prosper Show.” A FreeCon signatory and former associate director for economic policy at the U.S. Office of Management and Budget, Ginn currently serves as senior fellow at Americans for Tax Reform, associate research fellow at the American Institute for Economic Research, and chief economist at the Pelican Institute for Public Policy. In a recent AIER commentary, he critiqued President Biden’s proposed federal tax on unrealized capital gains and similar proposals from progressive-led state governments. Such a tax “should be rejected,” Ginn wrote, “as it is fundamentally unjust, likely unconstitutional, and would hinder prosperity and individual freedom.” “A tax on unrealized capital gains means that individuals are penalized for owning appreciating assets, regardless of whether they have realized any actual income from selling them.” He argued that a better way to help disadvantaged Americans would be to reduce their tax burdens and reform regulations to spur more economic innovation and job creation. In a separate piece in Law & Liberty, Ginn recommended the application of two rules to federal policymakers: a cap on annual spending growth and a disciplined approach to monetary policy. “Proper constraints will nudge even the worst politicians to make fiscally responsible choices and reduce net interest costs. Furthermore, America will be better positioned to respond to crises at home and abroad.”  Originally published at Daily Caller.

The National Association of Insurance Commissioners’ (NAIC) recent regulatory proposals have concerned stakeholders across the U.S. insurance landscape. At the heart of the controversy are proposed changes that could fundamentally alter how life insurance companies invest in financial instruments, with far-reaching consequences for the broader economy and, more specifically, the retirement security of millions of Americans. The NAIC, as a non-governmental entity that wields considerable influence over the insurance industry’s regulatory framework, operates in a unique space where its decisions can have national implications. Its recent move to increase capital requirements from 30% to 45% on residual asset-backed securities (ABS) tranches is a poignant example of regulatory action with unintended consequences. The proposal reflects a perceived higher risk assessment by necessitating higher financial reserves against these investments. However, this risk reassessment and the consequent regulatory response have not gone unchallenged. Critics, armed with analyses such as the Oliver Wyman report, contend that the data does not substantiate these changes, highlighting a dissonance between the empirical evidence and regulatory action. The implications of the NAIC’s proposals extend beyond the immediate financial health of life insurance companies to impact broader retirement planning. By disincentivizing investments in ABS and similar financial instruments, these regulatory changes threaten to narrow the investment options available to life insurance companies. Given the critical role that life insurance companies play in providing annuity products and as major institutional investors, the potential for these regulatory changes to affect market dynamics and returns for retirees is a major concern. These decisions should be made from a bottom-up approach in the marketplace, not from a top-down approach by NAIC. Amidst these regulatory developments, the suggested influence of external political forces, including the Biden administration and labor unions, introduces an additional layer of complexity. The assertion that these proposals may be driven by broader political objectives, rather than by an unbiased assessment of market risks and consumer protection needs, underscores the potential for regulatory processes to be co-opted for ideological ends. This prospect is particularly troubling in retirement planning, where American workers’ and retirees’ economic well-being and choices should be paramount. The debate over the NAIC’s proposed regulatory changes highlights the broader challenges of ensuring that this regulatory body operates with a commitment to transparency, accountability and evidence-based policymaking. An institutional framework that supports free-market competition, consumer choice and the economic interests of Americans in this financial space is needed, given the oversized influence of NAIC and the government. As the insurance industry navigates these regulatory waters, the call for a balanced, data-driven approach to regulation — prioritizing American workers’ long-term financial security and the U.S. economy’s health — is urgent. Regulation should be the last resort instead of the first for potential problems, as the marketplace, through a well-functioning price system, is best at regulating things to those who want and provide them most. The NAIC’s regulatory proposals represent a critical juncture for the U.S. insurance industry and the financial system supporting American retirement planning. The potential for these proposals to disincentivize key investment strategies poses a considerable risk to the sustainability of defined-contribution plans. It highlights the need for vigilant oversight of the regulatory process to hold regulators in check. Stakeholders, including policymakers, industry leaders and the public, must engage in substantive dialogue to ensure that future regulatory actions are grounded in solid empirical evidence and aligned with the prosperity of Americans. As this debate unfolds, upholding principles of competition, consumer protection and the integrity of the retirement planning framework in the marketplace remains paramount. At best, the NAIC proposal should be delayed for a year to give more time to examine its effects. But given the evidence so far, the proposal should be trashed.  Originally published at Econlib.

Through the Consumer Financial Protection Bureau (CFPB), the Biden administration has proposed a regulation to cap how much credit card companies can charge us when we’re late on a payment to just $8. This sounds great on the surface, right? Lower fees mean less stress when we’re struggling to make ends meet, as inflation-adjusted average weekly earnings have been down 4.2 percent. But, as with many things that seem too good to be true, there’s a catch. This well-meaning price control could make things the most challenging for those it’s supposed to help. First, why do credit card companies charge late fees? It’s not just about making an extra buck. These fees support more credit available for everyone and encourage us to pay on time, which helps the credit system run smoothly. Now, the CFPB is shaking things up by setting a price ceiling on these fees at $8. While it could save us some money if we slip up and pay late, credit card companies will find ways to compensate for this lost income. And how do they do that? Well, they might start charging more for other things, tightening who they give credit to, or increasing interest rates. That means, in the end, credit could be more expensive and harder to get for all of us. Not just individuals who could feel the squeeze, but small businesses, too. Many small businesses rely on credit to manage their cash flow and growth. If banks start being pickier about who they lend to or raise their fees, these small businesses will find it more costly to get credit. This isn’t just bad news for them; it’s bad news for everyone, as the result will be higher prices for consumers, lower wages, and fewer jobs for workers. Remember that small banks and credit unions are a big deal for the local economy. These institutions often depend on fees to keep things running. If they can charge less for late payments, they might not be able to lend as much. This could hit communities hard, making it tougher for people to get loans for starting a small business, buying a home, or building a project. Economists have long warned about the dangers of well-intentioned but poorly thought-out regulations. By setting a one-size-fits-all rule for late fees, the government would make credit more expensive and less accessible for everyone. The idea is to protect us from unfair fees, but the real-world result would be different if access to credit were limited for those who need it most. History proves that often the biggest challenge is to protect consumers from the consequences of government actions. In trying to shield us from high late fees, the government will set us up for a situation where credit is harder to come by and more expensive. This doesn’t mean we shouldn’t try to protect consumers. Still, we need to think carefully about the consequences of our actions and let markets work, which is the best way to protect consumers as they have sovereignty over their purchases. While capping credit card late fees sounds like a simple fix, the ripple effects would be complex and wide-reaching. It’s crucial to keep credit accessible and affordable, support small businesses, and ensure the financial system remains robust. Let’s look at the implications of this price control regulation before rushing into it. Price controls never work as intended, as history has proven. Instead, we should ensure people in the marketplace determine what’s best for them rather than the Biden administration’s top-down, one-size-fits-none approach. In “This Week’s Economy” episode 55, I discuss the following and more in 11 minutes:

Originally this article with my quotes ran by KTRH News in Houston.

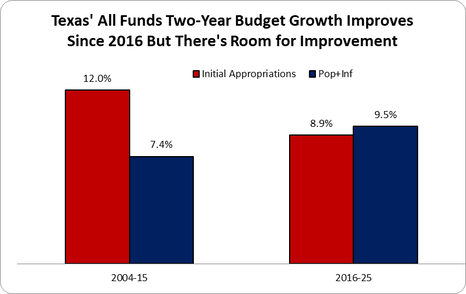

Under the Presidency of Woodrow Wilson in 1913, the Federal Reserve was born. The goal of it was simple, to help avert depressions and inflation, while preventing wealthy Americans from controlling financial markets at lower class expense. For the majority of its lifespan, it has sat mostly unimpactful, until the 1980s. With inflation raging out of control, then-Fed Reserve Chairman Paul Volker gave us tough love, and raised the rates along with restricting the money supply. This led to some hard time initially, especially within the first 6 months, but it eventually helped quell inflationary pressures on the economy, and we transitioned into the economic prosperity of the Ronald Reagan days. But in the last two decades, the Fed has gradually sought to destroy the American dollar, releasing endless money into the economy all while their balance sheet balloons to outrageous levels. It has culminated now in lower-to-middle class Americans struggling to make ends meet and buy basic necessities. Economist Vance Ginn says the many 'band aids' that the Fed has put on the economy, like monetizing debt, have hurt Americans more than ever. "Everyone's cost of living has dramatically increased...and the Fed has directly contributed to that by how much they have manipulated interest rates through their balance sheet, and by increasing the money supply," he says. For the longest time, the Fed kept interest rates has artificially kept he rates low to finance the dramatic government overspending. Then when the pandemic hit in 2020, the Fed created trillions to give away in stimulus checks, and to try and boost the economy, which has now essentially ruined it. As mentioned above, the old chairman Paul Volker's ways were about creating a brighter long-term future, instead of short-term fixes. That, according to Ginn, is what we desperately need again. "We need that style...he used to dramatically cut the money supply, which helped heal the pressures on the economy...so far, current Chairman Jerome Powell has not wanted to do that," he says. "Sometimes you need to have short term pains for long term gains." Current chairman Jerome Powell was a Donald Trump appointee, but the former President has since grown weary of Powell, criticizing him more and more. Trump has made a living on the campaign trail bashing the Biden economy, which he has vowed to fix if he wins office again. But to fix the situation might mean taking a hard look at Powell, and potentially replacing him. "We need someone who understand the economy, and the influence the Fed has on our lives," he says. "We need to make sure there is a sustainable path forward...that will be pivotal for the first part of a Trump Administration in 2025." As for who Trump would tab as a new Chairman is anyone's guess. But the parameters for what is needed are there. "In order to have the Fed come in and make those needed major changes...you have to give someone the leeway to do that, whether Trump like it or not," Ginn says. Trump would very much not like having to cause financial pain for Americans, considering how much he prides himself on winning at all costs. But he may not have a choice. "I think he will be able to sell it to the people though...he can just blame it on Biden," he says. But until then, as with just about every other aspect of our lives, the Biden Administration will continue keeping their thumb down on lower to middle class Americans. Government Spending Is The Problem The late, great economist Milton Friedman said, "The real problem is government spending." This is true as spending comes before taxes or regulations. In fact, if people didn't form a government or politicians didn’t create new programs, then there would be no need for government spending and no need for taxes. And if there was no government spending nor taxes to fund spending then there would be no one to create or enforce regulations. While this might sound like a utopian paradise, which I agree, there are essential limited roles for governments outlined in constitutions and laws. Of course, most governments are doing much more than providing limited roles that preserve life, liberty, and property. This is why I have long been working diligently for more than a decade to get a strong fiscal rule of a spending limit enacted by federal, state, and local governments promptly under my calling to "let people prosper," as effectively limiting government supports more liberty and therefore more opportunities to flourish. Fortunately, there have been multiple state think tanks that have championed this sound budgeting approach through what they've called either the Responsible, Conservative, or Sustainable State Budget. And recently I worked with Americans for Tax Reform to publish the Sustainable Budget Project, which provides spending comparisons and other valuable information for every state. Don't miss the latest updates as of January 2024. This groundbreaking approach was outlined recently in my co-authored op-ed with Grover Norquest of ATR in the Wall Street Journal. When Did This Budget Approach Begin? I started this approach in 2013 with my former colleagues at the Texas Public Policy Foundation with work on the Conservative Texas Budget. The approach is a fiscal rule based on an appropriations limit that covers as much of the budget as possible, ideally the entire budget, with a maximum amount based on the rate of population growth plus inflation and a supermajority (two-thirds) vote to exceed it. A version of this approach was started in Colorado in 1992 with their taxpayer's bill of rights (TABOR), which was championed by key folks like Dr. Barry Poulson and others. (picture below is from a road sign in Texas)  Why Population Growth Plus Inflation? While there are many measures to use for a spending growth limit, the rate of population growth plus inflation provides the best reasonable measure of the average taxpayer's ability to pay for government spending without excessively crowding out their productive activities. It is important to look at this from the taxpayer’s perspective rather than the appropriator’s view given taxpayers fund every dollar that appropriators redistribute from the private sector. Population growth plus inflation is also a stable metric reducing uncertainty for taxpayers (and appropriators) and essentially freezes inflation-adjusted per capita government spending over time. The research in this space is clear that the best fiscal rule is a spending limit using the rate of population growth plus inflation, not gross state product, personal income, or other growth rates. In fact, population growth plus inflation typically grows slower than these other rates so that more money stays in the productive private sector where it belongs. To get technical for a moment, personal income growth and gross state product growth are essentially population growth plus inflation plus productivity growth. There's no reasonable consideration that government is more productive over time, so that term would be zero leaving population growth plus inflation. And if you consider the productivity growth in the private sector, then more money should be in that sector at the margin for the greatest rate of return, leaving just population growth plus inflation. Population growth plus inflation becomes the best measure to use no matter how you look at it. Given the high inflation rate more recently, it is wise to use the average growth rate of population growth plus inflation over a number of years to smooth out the increased volatility (ATR's Sustainable Budget Project uses the average rate over the three years prior to a session year). And this rate of population growth plus inflation should be a ceiling and not a target as governments should be appropriating less than this limit. Ideally, governments should freeze or cut government spending at all levels of government to provide more room for tax relief, less regulation, and more money in taxpayers' pockets. Overview of Conservative Texas Budget Approach Figure 1 shows how the growth in Texas’ biennial budget was cut by one-fourth after the creation of the Conservative Texas Budget in 2014 that first influenced the 2015 Legislature when crafting the 2016-17 budget along with changes in the state’s governor (Gov. Greg Abbott), lieutenant governor (Lt. Gov. Dan Patrick), and some legislators. The 8.9% average growth rate of appropriations since then was below the 9.5% biennial average rate of population growth plus inflation since then, which this was drive substantially higher after the latest 2024-25 budget that is well above this key metric (before this biennial budget the growth rate was 5.2% compared with 9.4% in the rate of population growth plus inflation).  This approach was mostly put into state law in Texas in 2021 with Senate Bill 1336, as the state already has a spending limit in the constitution. The bill improved the limit to cover all general revenue ("consolidated general revenue") or 55% of the total budget rather than just 45% previously, base the growth limit on the rate of population growth times inflation instead of personal income growth, and raise the vote from a simple majority to three-fifths of both chambers to exceed it instead of a simple majority. There are improvements that should be made to this recent statutory spending limit change in Texas, such as adding it to the constitution and improving the growth rate to population growth plus inflation instead of population growth times inflation calculated by (1+pop)*(1+inf). But this limit is now the strongest in the nation as historically the gold standard for a spending limit of the Colorado's Taxpayer Bill of Rights (TABOR) has been watered down over the years by their courts and legislators, as it currently covers just 43% of the budget instead of the original 67%. My Work On The Federal Budget In The White House From June 2019 to May 2020, I took a hiatus from state policy work to serve Americans as the associate director for economic policy ("chief economist") at the White House's Office of Management and Budget. There I learned much about the federal budget, the appropriations process, and the economic assumptions which are used to provide the upcoming 10-year budget projections. In the President's FY 2021 budget, we found $4.6 trillion in fiscal savings and I was able to include the need for a fiscal rule which rarely happens (pic of President Trump's last budget).  Sustainable Budget Work With Other States and ATR When I returned to the Texas Public Policy Foundation in May 2020, as I wanted to get back to a place with some sense of freedom during the COVID-19 pandemic and to be closer to family, I started an effort to work on this sound budgeting approach with other state think tanks. This contributed to me working with many fantastic people who are trying to restrain government spending in their states and the federal levels. Here are the latest data on the federal and state budgets as part of ATR's Sustainable Budget Project. From 2014 to 2023, the following happened:

Result: American taxpayers could have been spared more than $2.5 trillion in taxes and debt just in 2023 if federal and state governments had grown no faster than the rate of population growth plus inflation during the previous decade. And this would be even more if we considered the cumulative savings over the period. My hope is that if we can get enough state think tanks to promote this budgeting approach, get this approach put into constitutions and statutes, and use it to limit local government spending as well, there will be plenty of momentum to provide sustainable, substantial tax relief and eventually impose a fiscal rule of a spending limit on the federal budget. This is an uphill battle but I believe it is necessary to preserve liberty and provide more opportunities to let people prosper.  Sustainable State Budget Revolution Across The Country

Below are the states (in alphabetical order) and state think tanks which I'm helping and information on how this process is going in those states. Here's an overview of this budgeting approach in Louisiana that can be applied elsewhere. I update these periodically, successful versus not successful budgeting attempts being 18-6 so far.

If you're interested in doing this in your state, please reach out to me. P.S. Good write-up on this issue here by Grover Norquist and I at WSJ, Dan Mitchell at International Liberty, and The Economist.  Originally published at Pelican Institute. It’s Geaux Time in Louisiana. The potential changes in Baton Rouge to remove barriers to work and let people keep more of their hard-earned money provide a more optimistic path for the Pelican State. This is much needed given the declining population over time and declines in employment for eight straight months. Let’s consider the latest data to see what’s really going on. The U.S. Bureau of Labor Statistics recently released Louisiana’s labor market data for February. These data provide details to evaluate how people are doing across the state. Louisiana’s unemployment rate increased to 4.2% per the household survey.

Employment has declined by 16,034 since March 2023, with employment declining in eight of the last eleven months.

Louisiana workers’ purchasing power continues to decline across most industries.

Figure 1. Louisiana’s Labor Market by Industry  Economic growth has slowed, and GDP and personal income growth are below the U.S. average.

Bottom Line: Louisiana’s economy is mostly weak with some green shoots for growth. These past results are based on the state’s complicated tax system, high regulations, and excessive government spending that have resulted in a poor business tax climate, net out-migration, and one of the highest poverty rates in the country. But with changes in Baton Rouge this year, there is an opportunity for bold, pro-growth reforms.

These bold reforms include:

The TRUTH about Government’s Role in Social Mobility with John Phelan | Let People Prosper Ep. 904/1/2024 Today, I am joined by John Phelan, economist at the Center of the American Experiment in Minnesota, on the Let People Prosper Show episode 90.

We discuss the following and more:

Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. Subscribe to my Substack newsletter to get my podcast show notes and much more in your inbox: vanceginn.substack.com Visit my website for more economic insights: vanceginn.com  Originally published at Texans for Fiscal Responsibility. Overview

Texas’ employment has been up for 44 of the last 46 months since May 2020.

Figure 1. Texas Labor Market by Industry  Source: U.S. Bureau of Labor Statistics Economic growth has picked up, but personal income lags the U.S. average.

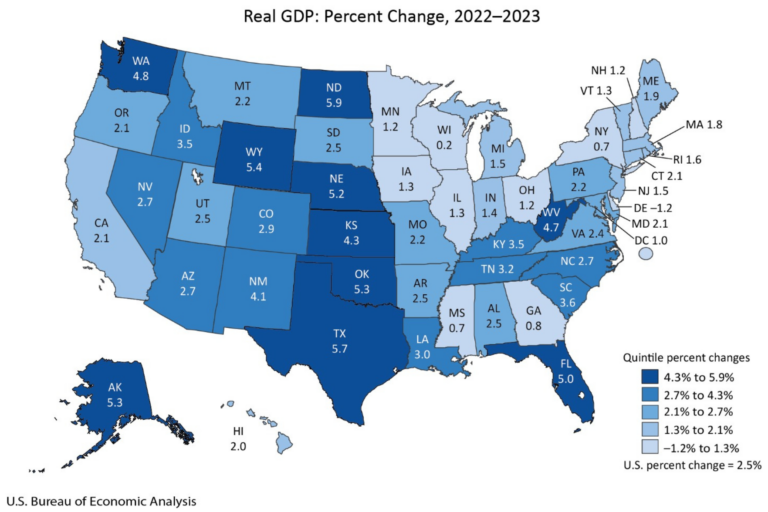

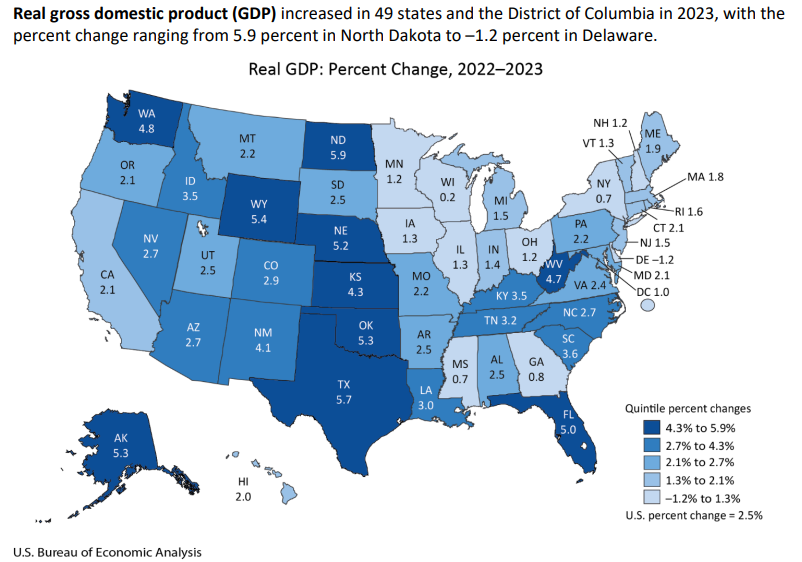

Figure 2: Real Gross Domestic Product by State in 2023  Improve the Texas Model with pro-growth policies that limit government by:

How Government Influences Bridge Repairs and Minors on Social Media | This Week’s Economy Ep. 543/29/2024 In “This Week’s Economy” episode 54, I discuss the following and more:

See show notes on Substack: www.vanceginn.substack.com Visit my website for more economic insights: www.vanceginn.com  Originally published at Texans for Fiscal Responsibility. Highlights

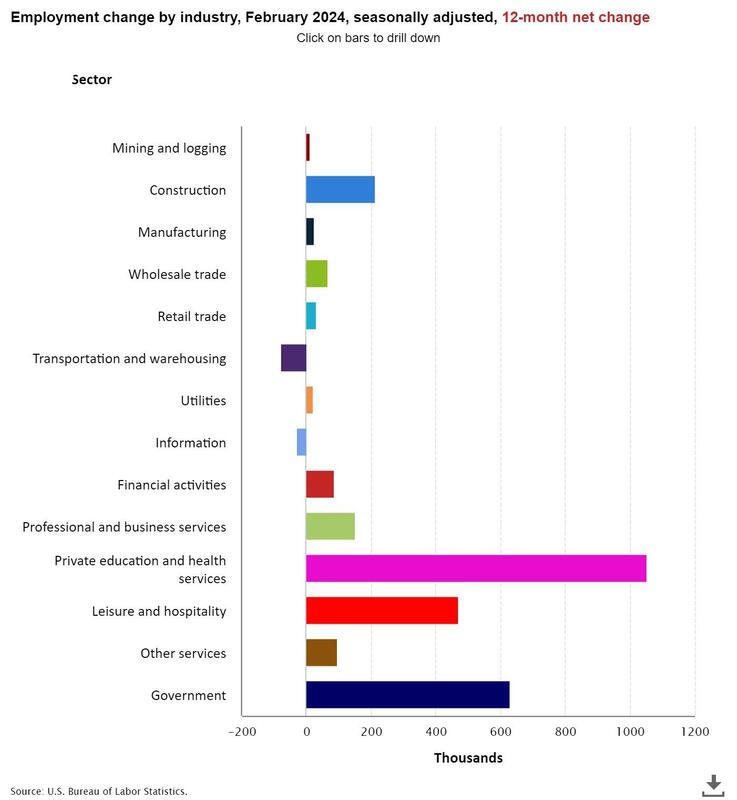

Figure 1: Real Average Weekly Earnings Remain Down 4.2% Since January 2021  Source: Fed FRED Labor Market The Bureau of Labor Statistics recently released its U.S. jobs report for February 2024, which was another mixed report with some strengths but many weaknesses.

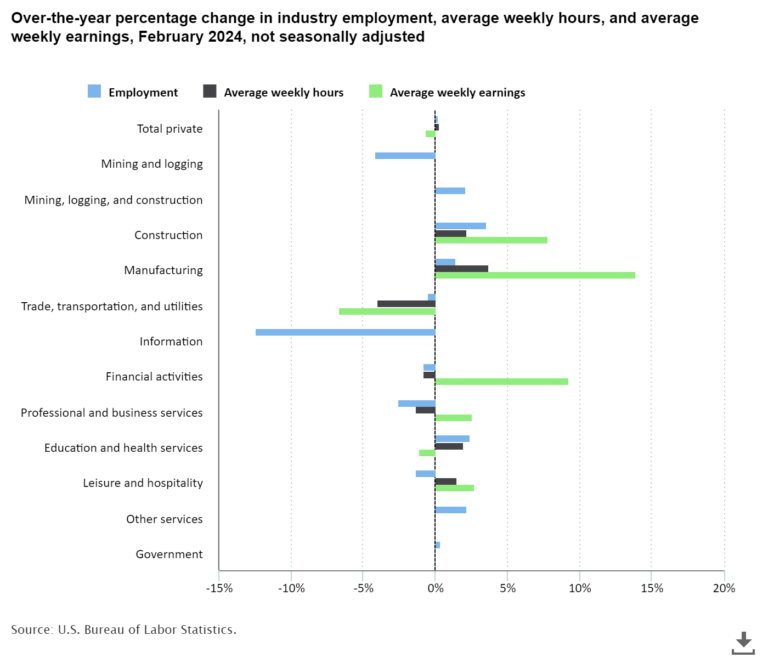

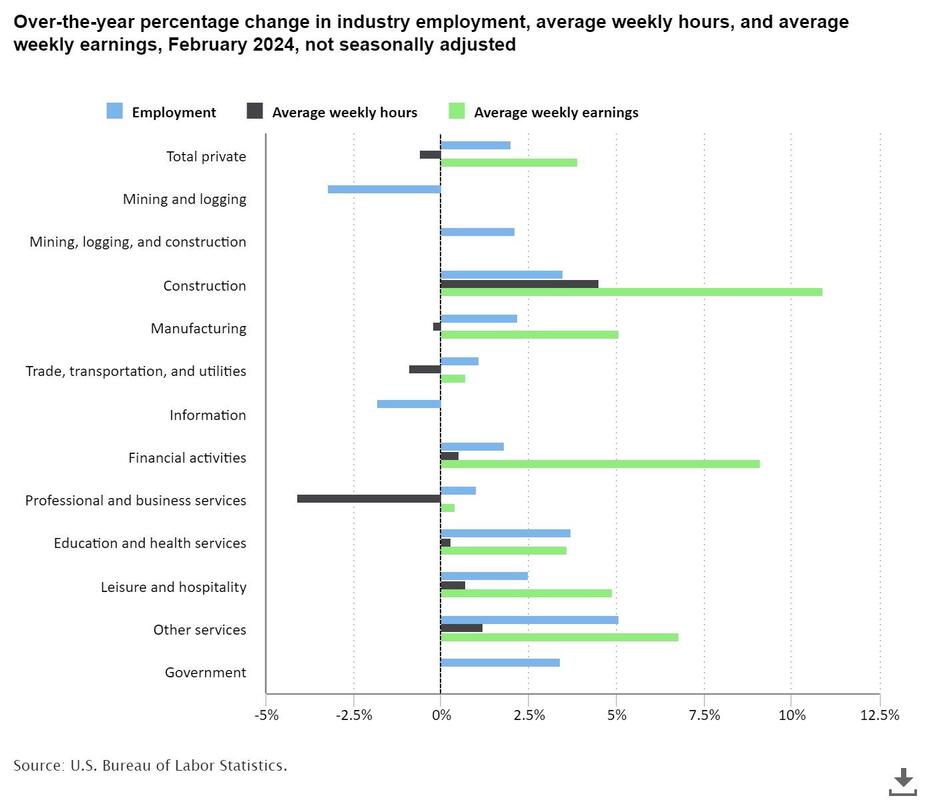

Figure 2. Changes in Employment by Industry Over the Last Year  Source: Fed FRED

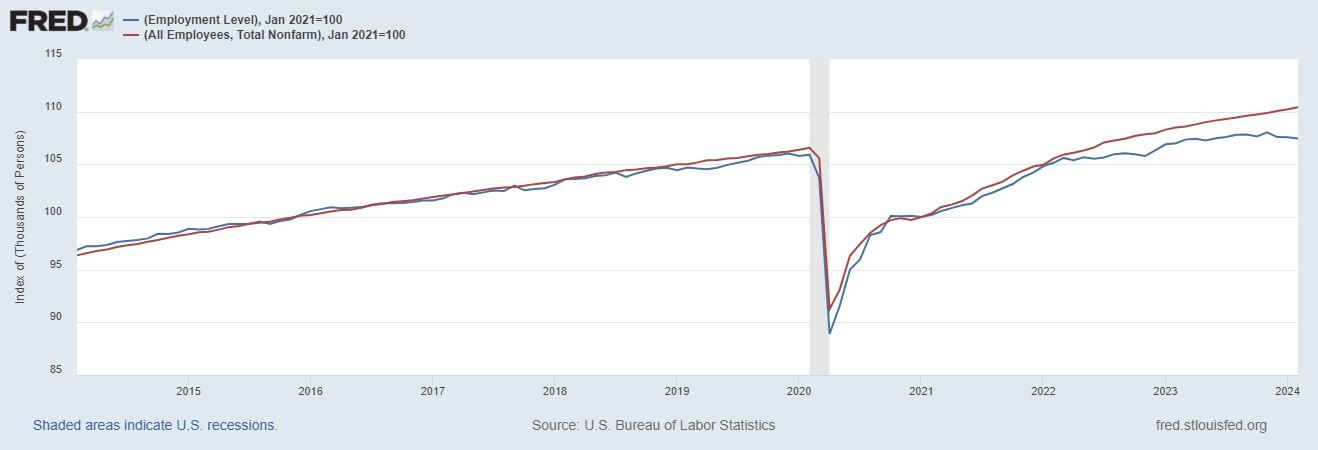

Figure 3. Establishment Nonfarm Jobs Far Outpace Household Employment Level Since March 2022  Source: Fed FRED

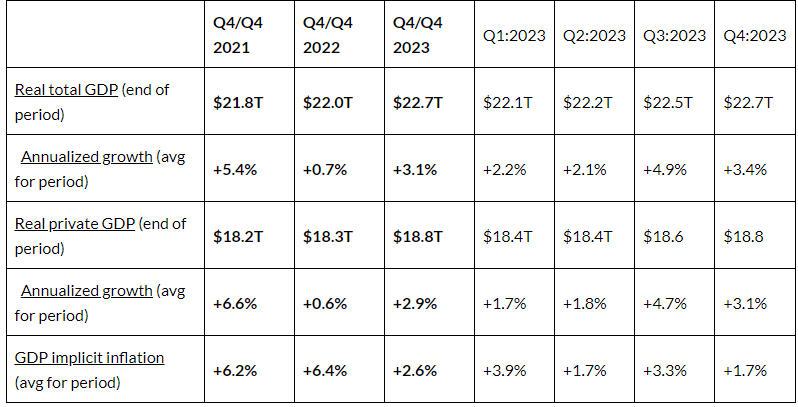

Economic Growth The U.S. Bureau of Economic Analysis recently released the third estimate for economic output in the fourth quarter of 2023.

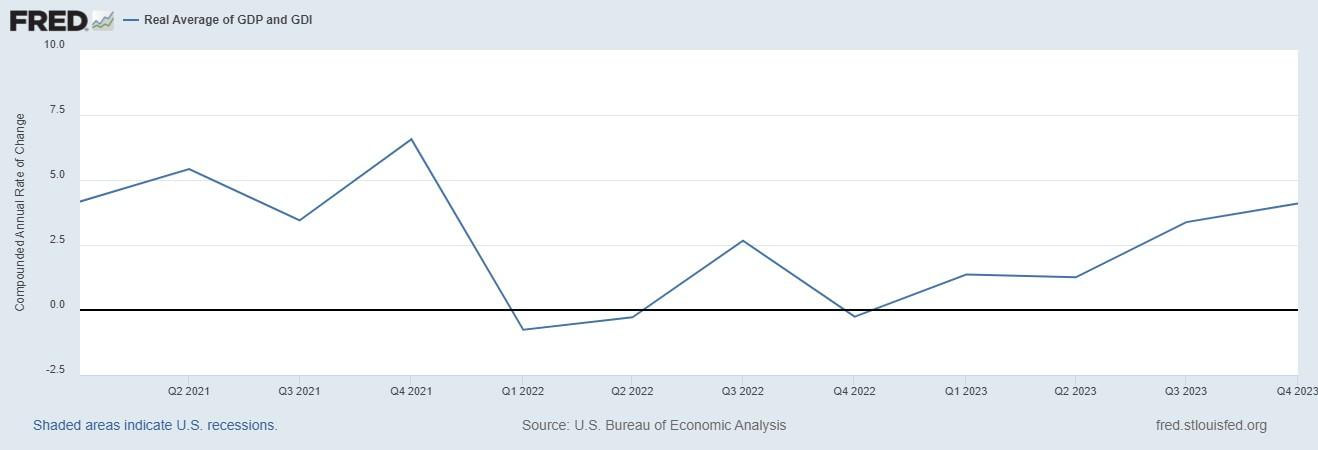

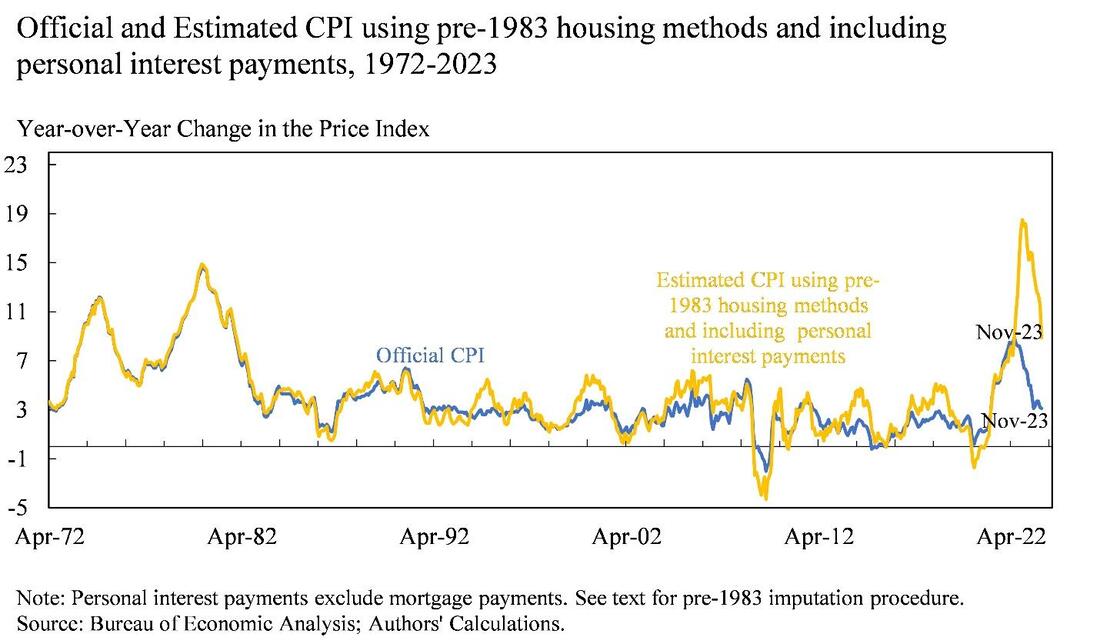

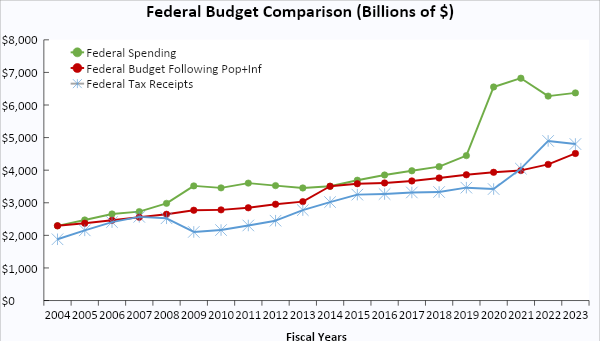

Table 1: Economic Output, Growth, and Inflation  Another key measure of economic activity is the real average of GDP and GDI, which accounts for domestic production and income and is known as real gross domestic output. Real GDO in the third quarter increased by 3.4%, and in the fourth quarter increased by 4.1% to $22.5 trillion. Figure 4 shows how this measure has declined on an annualized basis in three of the last eight quarters, increasing this value by only 2.9% since the fourth quarter of 2021 before the two consecutive quarters of declines in the first and second quarters of 2022. Figure 4. Annualized Real Gross Domestic Output Growth  Meanwhile, the federal budget deficit continues unabated because of overspending and declining tax collections from a weaker economy. The national debt has ballooned to $34.6 trillion, and net interest payments on the debt will soon be a top federal expenditure, rising to above $1 trillion. The Federal Reserve has monetized, or printed, much of the new Treasury debt to keep interest rates artificially lower than where the market would suggest. The Fed will need to cut its balance sheet (total assets over time) more aggressively if it is to stop manipulating markets (see this for types of assets on its balance sheet) and persistently tame inflation. The current annual inflation rate of the consumer price index (CPI) has been moderating since a peak of 9.1% in June 2022 but remains elevated at 3.2% in February 2024. Compared with the Fed’s average inflation rate target of 2%, which really should be 0%, the current CPI inflation rate is too high, as are other key measures of inflation. A recent paper by Larry Summers, who was the 71st Secretary of the Treasury for President Clinton and Director of the National Economic Council for President Obama, and co-authors notes that if the calculation of CPI kept housing calculation methods and personal interest payments in, then the latest peak in inflation would have been 18% instead of 8.1%. Figure 5 shows their chart with these data that also highlights how the method-adjusted inflation would be closer to 10% instead of the reported 3.1%. Figure 5. CPI Inflation Differences When Methods Are Similar Over Time  Just as inflation is always and everywhere a monetary phenomenon, deficits and high taxes are always and everywhere a spending problem. David Boaz at Cato Institute has noted how this problem is caused by both Republicans and Democrats. To control this fiscal and monetary crisis, the U.S. needs a fiscal rule like the Responsible American Budget (RAB) with a maximum spending limit based on the rate of population growth plus inflation. This was recently released as part of Americans for Tax Reform’s Sustainable Budget Project, highlighting this approach’s benefits at the federal, state, and local levels. If Congress had followed this approach from 2004 to 2023, Figure 4 shows tax receipts, spending, and spending adjusted for only population growth plus chained-CPI inflation. Instead of an (updated) $20.2 trillion national debt increase, there could have been only a $700 billion debt increase for a $19.5 trillion swing in a positive direction that would have substantially reduced the cost of this debt to Americans. The Republican Study Committee recently noted the strength of this type of fiscal rule in its FY 2025 “Fiscal Sanity to Save America.” To top this off, the Federal Reserve should follow a monetary rule so that the costly discretion stops creating booms and busts. Figure 6: Federal Budget Gap Shrinks If Spending Limited to Population Growth Plus Inflation  Bottom Line

Bidenomics has been a failure and the policy approach must be redirected to pro-growth policies that shrink government rather than big-government, progressive policies. It’s time for a limited government with sound fiscal and monetary policy that provides more opportunities for people to work and have more paths out of poverty. Recommendations:

In the wake of the Baltimore bridge collapse, a major U.S. port has come to a standstill. The Port of Baltimore is the top U.S. port for vehicle imports and exports, as well as for farm and construction machinery. U.S. Transportation Secretary Pete Buttigieg told MSNBC on Wednesday that while there are many ports on the U.S. East Coast, “there is no substitute for the Port of Baltimore being up and running.”

How will this affect the U.S. economy—and even global supply chains? NTD spoke to Vance Ginn, the president of Ginn Economic Consulting and the former chief economist at the U.S. Office of Management and Budget, to find out more.  Originally published at AIER.

Recently, the Biden administration handed $1.5 billion to the nation’s largest domestic semiconductor manufacturer, GlobalFoundries, the biggest payout from the CHIPS and Science Act of 2022 so far. The argument for this corporate welfare is America is too dependent on chips from China and Taiwan so more should be made domestically. Instead of seeing how America should reduce the cost of doing business for all semiconductor businesses here, some businesses will be picked as winners and others as losers. The cost of this form of socialism gives capitalism a bad rap and should be rejected. This move echoes a broader trend of governments worldwide intervening in their economies through industrial policy. A cocktail of targeted subsidies, tax breaks, and regulatory tinkering, industrial policy aims to sculpt economic outcomes by favoring specific industries or firms, all for the supposed benefit of the national economy. Industrial policy puts business “investment” decisions in the hands of government bureaucrats. What could go wrong? While its champions tout its potential to boost competitiveness and spur innovation, the reality often tells a different story, especially in light of massive deficit spending. In practice, industrial policy tends to fan the flames of higher prices and sow the seeds of economic destruction. Politicians too often meddle with voluntary market dynamics by artificially bolstering favored sectors through subsidies and tax perks, resulting in the misallocation of resources and distorted prices. Moreover, the infusion of government funds to bankroll these initiatives with borrowed money can contribute to the Federal Reserve helping finance the debt, increasing the money supply, and stoking inflation. The nexus between deficit spending and prices looms large over industrial policy. When politicians resort to deficit spending to bankroll industrial ventures, they put upward pressure on interest rates by issuing more debt and competing with scarce private funds. Elevated interest rates disturb private investment, ushering in a likely economic slowdown. Suppose deficit financing leans heavily on monetary expansion, whereby the central bank snaps up government debt. In that case, it fuels inflation by flooding the market with money that chases fewer goods and services. The national debt is above $34 trillion, and the Federal Reserve has already monetized much of the increase in recent years. Racking up even more deficits is insane: repeating the same mistakes and expecting a different result. Excessive spending and money printing have landed us with above-target inflation for over three years running. The repercussions of industrial policy ripple beyond inflation to encompass the broader economic landscape. Excessive government meddling in specific industries crowds out private investment and entrepreneurship. When particular firms enjoy subsidies and preferential treatment, it distorts the competitive landscape and deters innovation. This stifles economic vibrancy and impedes the rise of new industries or technologies crucial for sustained growth. For a cautionary tale of how Biden’s recent move could play out, look no further than Europe. Nations like Sweden, heralded by the West as a utopian example of big government yielding big benefits, spent the last year grappling with economic strife driven by dwindling private consumption and housing construction. Europe’s penchant for industrial policy, marked by subsidies, high taxes, and regulatory hoops, has contributed to its economic stagnation. To sidestep the dilemma of industrial policy missteps, policymakers should stop propping up their favorite sector or industry and instead unleash people to flourish by getting the government out of the way. Politicians should foster an environment conducive to entrepreneurship, innovation, and competition. This entails cutting government spending, reducing taxes, trimming red tape, and championing trade by removing barriers to private sector flourishing. By allowing market forces to determine resource allocation and rewarding entrepreneurship and risk-taking, people here and elsewhere can unleash their full potential and adapt to changing circumstances more effectively than under industrial policy frameworks. Biden’s billion-dollar amount to one company may seem like a lot, but that’s just a drop in the bucket of what’s to come from the CHIPS Act. Instead, these funds should be eliminated, preventing Congress from taking us further down the road to serfdom. Originally published at Texans for Fiscal Responsibility.  Executive Summary

Originally published at Texas Scorecard.

Texas can pass bold school choice legislation when the next legislative session starts in January 2025. This could finally happen because of the recent election wins in the House primaries, efforts led by Gov. Greg Abbott. The election wins include pro-school choice candidates beating anti-school choice incumbents or filling seats of retiring anti-school choice members. More incumbents, including House Speaker Dade Phelan, were forced to a runoff in May. Moreover, 80 percent of Republicans voted for Proposition 11 on the primary ballot to support school choice, which matters in a dominantly red state. In the evolving educational reform landscape, universal education savings accounts (ESAs) provide the best path to empower parents to decide their children’s education. They are also a practical, fiscally responsible strategy for reimagining the future of education. At least 10 states have passed universal school choice, and more are likely to do so soon. But these states haven’t reached the pinnacle of what a competitive education system should look like. The optimal school choice approach should liberate education from the constraints of the monopoly government school system, draw upon successful market-driven solutions, and offer a simplified education finance system. The Texas Legislature essentially controls the current school finance system with funding from taxpayers through taxes collected by the state, school district, and federal governments. The inefficiency and ineffectiveness of the status quo are stark, including questionable but relevant declining test scores. This highlights a critical need for an approach that better serves students’ and families’ unique needs and aspirations. The state’s school finance system is based on many factors to the school system, but the Texas Education Agency recently reported that the average funding per student was $14,928 in the 2021-22 school year. Total funding was $80.6 billion for 5.5 million students. Of course, this is how much is spent, but the actual cost of the monopoly government school system is hidden and driven higher by politics rather than market outcomes. ESAs provide flexibility in covering many educational services, including various schooling options, tutoring, testing, and other related expenses. This empowers parents to customize their children’s education to suit individual learning styles and interests. This adaptability is vital for fostering environments where children excel academically, socially, and emotionally. Implementing a universal ESA program demands a framework that balances simplicity with accountability, ensuring the focus remains on expanding educational opportunities and improving student outcomes. While many current ESA programs run alongside the government school system, this doesn’t provide the most competitive framework. Running them in tandem, whereby the funding remains the same or even increases for government schools while creating a new system to fund ESAs, is costly and lacks the incentives for optimal outcomes. Instead, we should pursue a simplified education finance approach that maximizes competition, reduces costs, and lowers taxes by funding students, instead of a system. A bold proposal would provide parents with an ESA of $10,000 per child for the school year but paid monthly or the preferred frequency to choose any approved schooling, including government, private, charter, home, co-op, tutoring, or other types of schooling. With about 6.3 million school-age children in Texas, the annual total expenditure would be $63 billion, or $17.6 billion less than what’s being spent today on government schools. Parents could receive an ESA of as much as $12,800 per student to keep the same expenditures as today. However, given the bloated bureaucracy and misguided direction of government schools, the $10,000 amount would help force efficiencies while reducing taxpayers’ costs and incentivizing new education providers. The lower cost of $17.6 billion would provide an opportunity for substantial school property tax relief. Combining ESAs and property tax relief would further accentuate the proposal’s appeal, addressing the lack of school choice and burdensome property taxes. The bold approach eliminates most, if not all, of the current antiquated government school finance system with one that gives parents a way to meet their children’s unique learning needs best. It would help alleviate the hardship for many families that can choose alternatives for financial reasons, pay lower property taxes, or have money remaining to invest in their children’s quality of life and educational pursuits. As states across the nation begin to recognize the transformative potential of this bold universal school choice approach, the momentum is undeniable. This trend underscores a growing consensus on the need for educational systems that prioritize choice, flexibility, and parental empowerment. By breaking free from the monopoly government school finance system and embracing a bold ESA finance approach that empowers parents, we can pave the way for a future where every child can achieve their full potential.  Originally published at The Center Square.

The recent surge of bills attempting to rein in social media outrage in Florida and across America has sparked debate over the role of government in regulating them. Florida Gov. Ron DeSantis vetoed an initial bill banning minors on social media. In his veto message, he said, “Protecting children from harms associated with social media is important, as is supporting parents’ rights and maintaining the ability of adults to engage in anonymous speech.” We should empower parents to determine what's best for their children on social media, or otherwise. This will work better than putting politicians and government bureaucrats in charge, which is what these types of bills do. These bills are likely unconstitutional, as they violate the First Amendment. Furthermore, excessive government regulation of social media stifles innovation and entrepreneurship in the digital space, especially small businesses. By imposing burdensome restrictions on online platforms, we risk hindering the development of new technologies and services that could benefit families. A more pragmatic approach fosters competition in the marketplace, allowing consumers to choose the platforms that best align with their values and preferences. These regulations would hurt many start-up firms as they won’t have the resources to hire as many lawyers to jump through the hoops imposed on them that larger, incumbent companies can afford. They would also need to pay third-party verification systems that cost thousands of dollars, making it more challenging to start a business, as noted in a recent report by Engine. Gov. DeSantis has been a vocal advocate for parental empowerment, emphasizing the importance of transparency and accountability from social media companies. His initial pushback of government overreach of social media should be championed rather than resorting to bans for questionable reasons, as social media isn’t the culprit for bad parenting or bad legislation. In light of ongoing NetChoice cases at the Supreme Court, where the organization has fought against state-level regulations deemed infringing on free speech and commerce, we should uphold free speech in the digital age. By joining parents in advocating for greater transparency and accountability by social media companies where applicable, we can champion the interests of Americans and assert state sovereignty. Rather than relying on government mandates and regulations, we should foster a culture of parental responsibility and provide families with the resources they need to navigate the digital landscape safely. If politicians and bureaucrats take over these responsibilities, it will lead to less incentive for parents to be engaged with their kids and what they’re doing online. This would be a terrible path forward as the government has already made bad situations worse regarding safety-net handouts, a monopoly government school system, and more. Let’s stick with a proven approach that supports parents and social media providers rather than a top-down, likely unconstitutional one. Today, I am joined by Dr. Ed Timmons, the Service Associate Professor of Economics and Director of the Knee Regulatory Research Center at the John Chambers School of Business and Economics at West Virginia University.

Join us on Let People People Show Episode 89 as we discuss the following: - Purpose of government licenses - Costs and benefits of occupational licensing - Ways to get the government out of the way of work Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. Subscribe and see show notes for this episode on Substack - www.vanceginn.substack.com Visit my website for economic insights - www.vanceginn.com Who’s REALLY To Blame for the Housing Affordability Crisis: Investors, Markets, or Governments?3/22/2024 In “This Week’s Economy” Episode 53, I discuss the following and more:

- What’s up with the housing market? - Will Louisiana be next to get universal school choice? - Why can’t we treat people like people instead of pawns? Please like this video, subscribe to the channel, share it on social media, and provide a rating and review. Subscribe and see show notes for this episode on Substack - www.vanceginn.substack.com Visit my website for economic insights - www.vanceginn.com  Last week, the Texas Association of Business, Fort Worth Chamber of Commerce, Longview Chamber of Commerce, U.S. Chamber of Commerce, and American Bankers Association sued to block the Consumer Financial Protection Bureau’s (CFPB) final rule to lower the credit card late fees cap to $8.

This lawsuit challenges the Biden Administration's terrible price control idea that would hurt Texans. Given the entities that sued to block this rule and the effect on Texans, the case should continue in Texas instead of moving it elsewhere as the CFPB would like. Credit card late fees, what some call “junk fees,” are the cost of someone paying their bill late. Nothing is free, so there’s a charge for paying late, as it also influences the expected cash flow of credit card companies. It’s not a price gouging scheme; it’s simply a way to take the risk of giving credit to those in need while keeping cash flow for profitability. This is not only important for businesses, but it also provides an incentive for people to pay their bill online. Without a market-based credit card fee, the cost will be on those who need credit the most as they won’t be able to get it or pay much higher interest rates. The Wall Street Journal Editorial Board wrote: “Even the CFPB acknowledges, the lower penalty may cause more borrowers to pay late, and as a result incur higher ‘interest charges, penalty rates, credit reporting, and the loss of a grace period.” Many Texans depend on credit card access to pay their living expenses. There are more than 3 lines of credit per user in Texas. More than 3 million small businesses also rely on access to credit to grow and expand. Some card issuers most impacted by this rule, including Citi, Chase, and Synchrony, have extensive operations in Texas. JCPenney, based in Plano, offers one of the country's most popular co-branded credit cards through its partnership with Synchrony. The retailer, which employs more than 2,000 Texans, is just a few years removed from bankruptcy and stands to lose big if this misguided rule is allowed to stand. Reports indicate late fees account for 14 to 30 percent of department store credit card revenue. Given the current state of credit card delinquencies at a 10-year high, the CFPB’s rule would exacerbate an already dire situation. This would have far-reaching effects on our community and economy, particularly as consumers and small businesses increasingly rely on credit to navigate lower inflation-adjusted average weekly earnings by 4.2% since January 2021. Most of the plaintiffs in this lawsuit are local organizations that recognize the importance of defending and preserving access to credit. Texas is the rightful venue for this battle. |

Vance Ginn, Ph.D.

|

RSS Feed

RSS Feed

Proudly powered by Weebly